1. Introduction

Alongside most Nordic countries, Finland has set ambitious climate goals. Most recently, the government introduced legislation to ban the use of coal for energy production by 2029 [

1]. These goals are also further fortified by the decisions of individual cities as the latest strategy of Helsinki, for example, includes the goal of achieving carbon neutrality by 2035 [

2]. However, achieving these goals is not a simple task. The Helsinki Metropolitan area has been struggling, especially with potential sources of heat production. In all Finnish cities, District Heating (DH) with large Combined Heat and Power (CHP) plants, combined with heat-only boilers (HOB’s) for peak-load use, is the prevailing technology. Finland is one of the Western countries where DH is used the most. Currently, DH has 46% market share of all heating in Finland and in large cities DH with CHP is the dominating technology with a share of 80% or more [

3]. Finnish CHP technology uses fuels with an exceptional overall efficiency. For example, a coal-fired CHP plant typically has an electrical efficiency of about 30% and heat efficiency of about 60%, yielding a total efficiency of 90%. However, DH still relies heavily on fossil fuels and peat, which is a domestic fuel with a CO

2 emission coefficient slightly more than that of coal. In the Helsinki region, CHP plants use either coal or natural gas as fuel. In Helsinki coal-fired power plants, also minor fractions of biomass have been recently introduced.

The cities in the area, Helsinki, Espoo and Vantaa, are most likely trying to fill the hole left by the eventual decommissioning of fossil fuel fired plants with biomass, but recent motions put forward in multiple city councils have called for an evaluation of the potential of small modular reactors (SMR) as a source of district heating [

4,

5]. This study, based on the M.Sc thesis of Värri [

6], attempts to look into the assumptions under which SMRs would be a valid choice for energy production in the chosen market beyond the year 2030. The results are not meant to be taken as final due to the high amount of uncertainty surrounding most of the data, including the hypothetical combined market case used, but to be considered as a preliminary overlook of SMR’s economic potential and possible role in the DH system.

SMRs have been brought up in DH discussions mainly for their ability to provide CO

2 free energy at a scale smaller than traditional nuclear power plants (NPP), but the new plant designs can also provide increased safety through passive systems, possibilities for reduced costs and higher quality fabrication through factory based manufacturing and other possible advantages [

7]. While these advantages are significant, there are still a number of issues to be solved before large scale deployment can be considered including licensing considerations and emergency planning zone sizes [

8]. These are considered solvable issues in this study, as the focus is on the techno-economical assessment.

Finland is a viable location for early SMR deployment, considering that the country has historically been positive towards nuclear and is currently finishing a new NPP in Olkiluoto and is in the early stages of a new build at Hanhikivi [

9,

10]. The country also has a long history with DH networks and the share of DH of the total heating is presumed to stay at 75–85% of the overall heat demand in the Metropolitan area, as indicated for instance by the Nordic Energy Technology Perspectives 2016 (NETP16) [

11]. The large physical infrastructures of DH networks also generally result in local monopolies in Finland, where both the distribution and production is owned and controlled by the same company [

12]. This brings forth some additional considerations regarding the addition of a nuclear SMR into an existing network, as the investor would most likely need to be an existing operator in the region.

It is important to note that Finland does not exist in isolation and larger trends in energy affect the future of heat production in the country as well. When considering the potential deployment of SMRs for DH in Finland, the most significant trends are: transformation towards more distributed electricity supply with enhanced transmission capacity both inside the Nordics and towards Europe, and a steep increase in wind generation and electrification of heating. All three are also intertwined with each other. Wind power investment cost is forecast to drop significantly and in combination with the target shares of renewables, there are many estimates that wind generation will increase manifold by 2030 to cover 30% of the overall Nordic electricity generation [

11,

13,

14]. A share this large of intermittent generation from wind could not be integrated directly into the current electricity system, but would require the system to be fitted with greater amounts of flexible supply- and demand-side resources [

15,

16]. The large share of hydro power in the Nordics provides a backdrop for this growth but the system will also require balancing through demand response, storage and wider electricity trade. The electrification of heating could potentially provide opportunities for both demand response and storage through heat pump utilization and heat storages. The NETP16 forecasts that electricity based heating will start growing significantly between 2025 and 2030 and could, based on the reports assumptions and different scenarios, cover between 30% to 50% of the DH demand in 2050 with most of the remainder being covered by biomass and waste. In the backdrop, the transmission capacity between Nordic countries is expected to grow by 11.2 GW and by around 14 GW between Nordics and Europe [

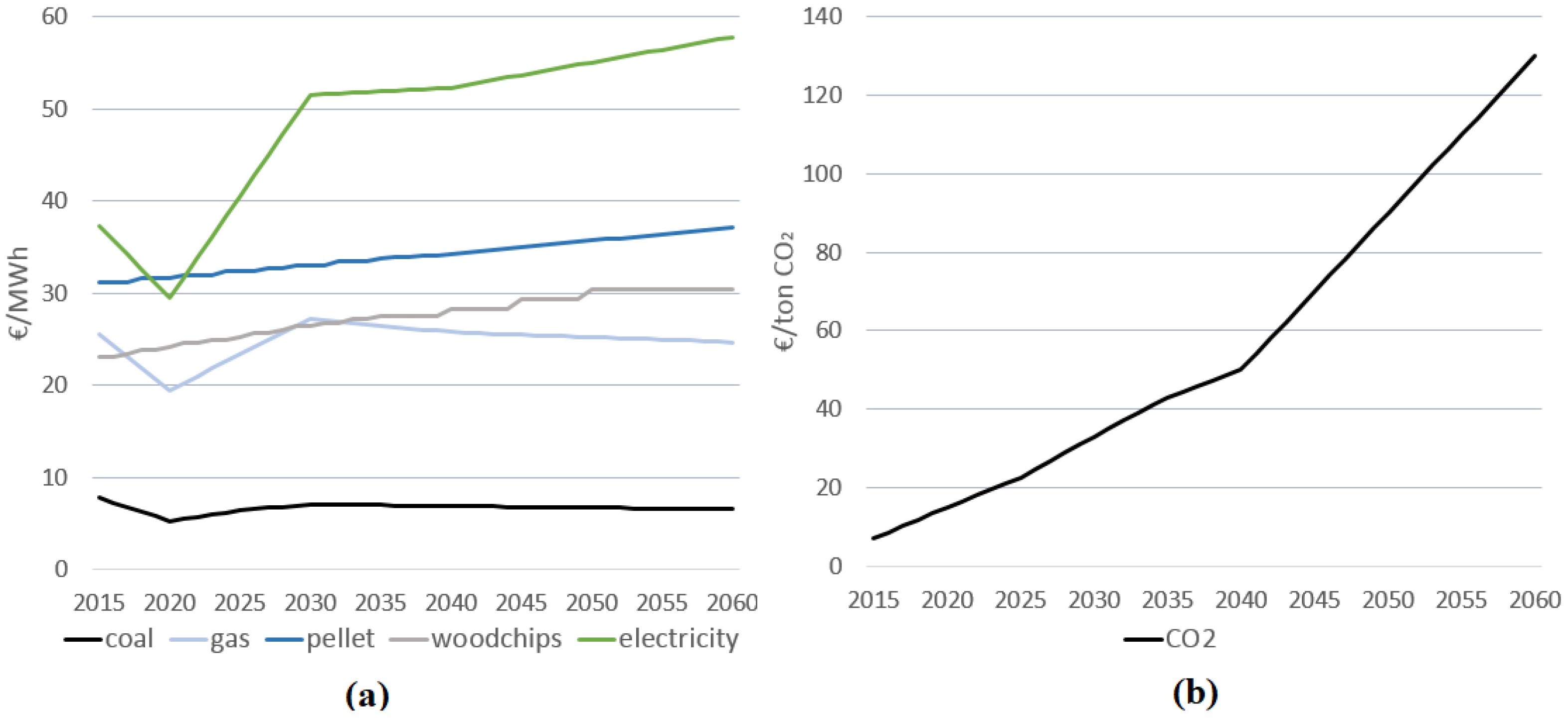

11]. The electricity prices and temporal variations used in this analysis are based on Reference [

11].

Biomass and combustion of Municipal Solid Waste (MSW) are widely proposed options for the decarbonisation of heating systems and DH in Europe. Utilisation of MSW as fuel in DH has expanded in many European city regions (see, e.g., Reference [

17]). This has led to significant increases in both MSW imports in the Baltic sea region and raised questions regarding the sustainability of these transports and the diversion of resources away from recycling [

18]. The sustainable amount of biomass use in relation to the requirements of the latest IPCC report [

19], in turn, is currently a hot topic of expert and policy-making debate in Finland, as increased use of biomass is planned for new pulp and paper production plants and both for transportation biofuel and power plant use. There is thus a concrete threat that the forest carbon sink may decrease significantly from the current level [

3].

In Europe, heating still relies heavily on fossil fuels [

20]. The most common fuels in individual heating in the European Union (EU) are natural gas and light fuel oil and buildings are a huge CO

2 emissions source in the EU with 634 MtonCO

2-eq. in 2015 [

20,

21]. District heating is very common in many countries of Northern and Eastern Europe, and the prevailing fuels are coal and natural gas. In light of the recent IPCC report on 1.5 °C warming [

19], there is an urgent need to transform global energy systems into carbon neutrality. Thus, the analysis performed in this study has relevant and timely indications for all city regions where heating is predominantly based on fossil fuels.

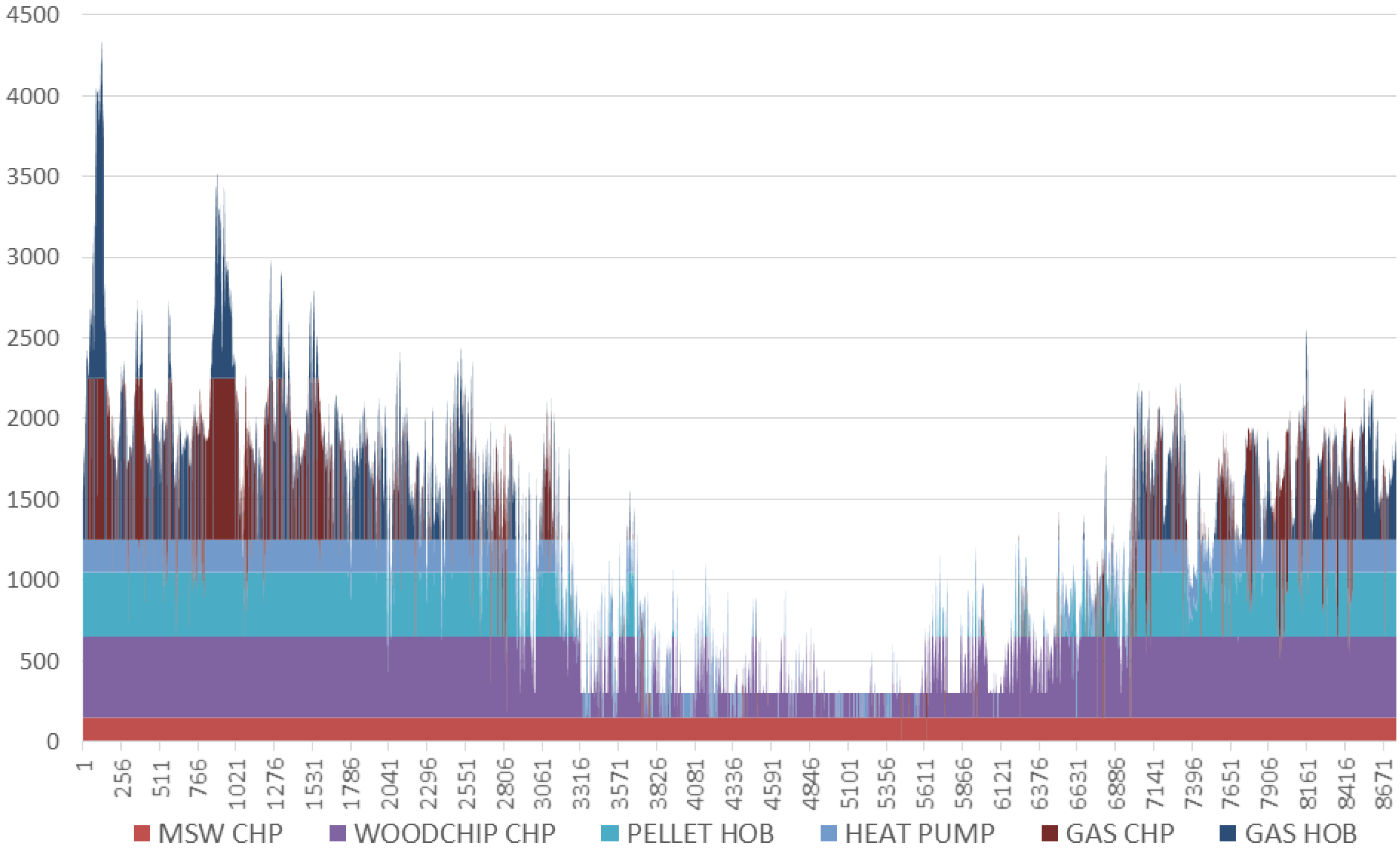

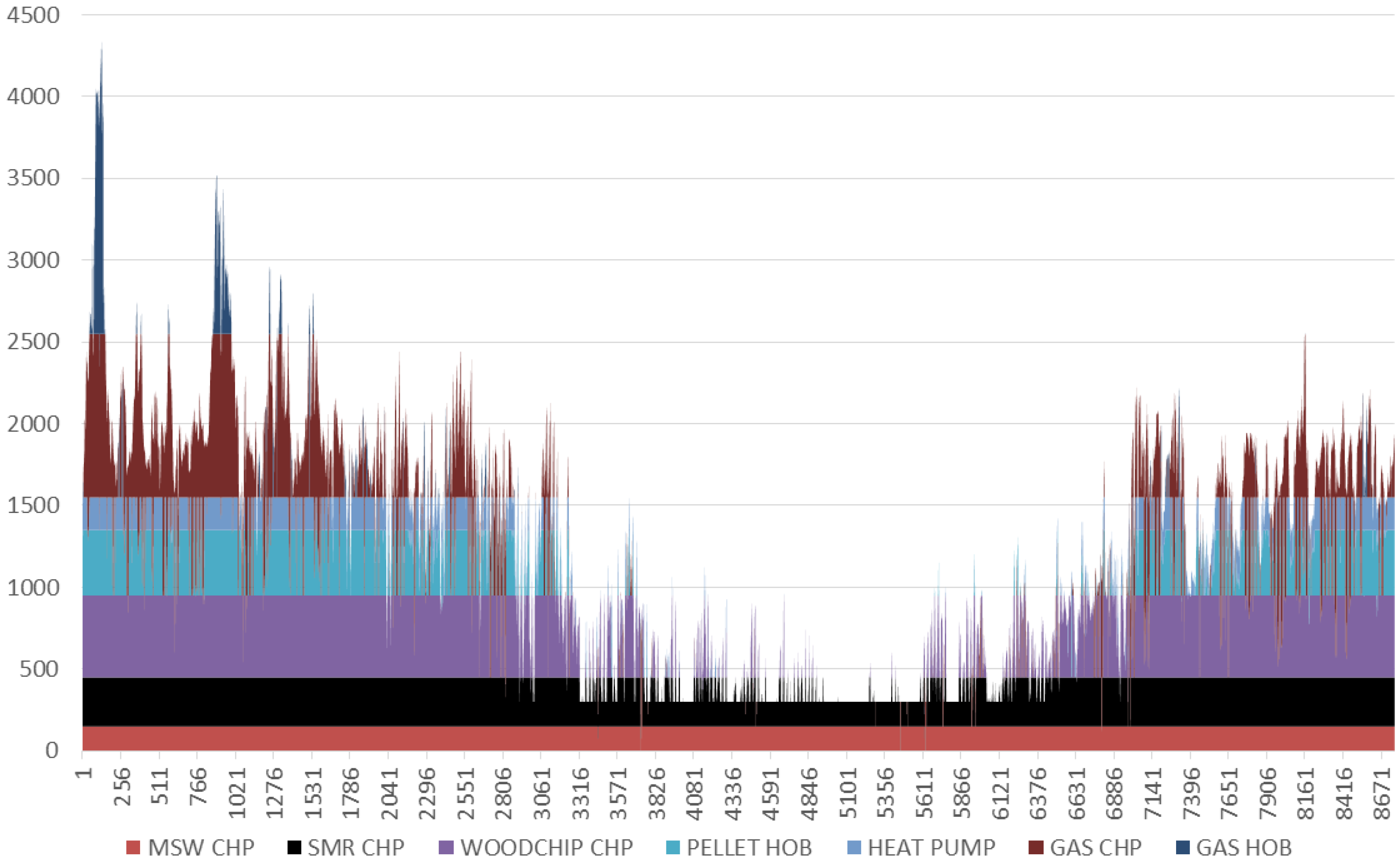

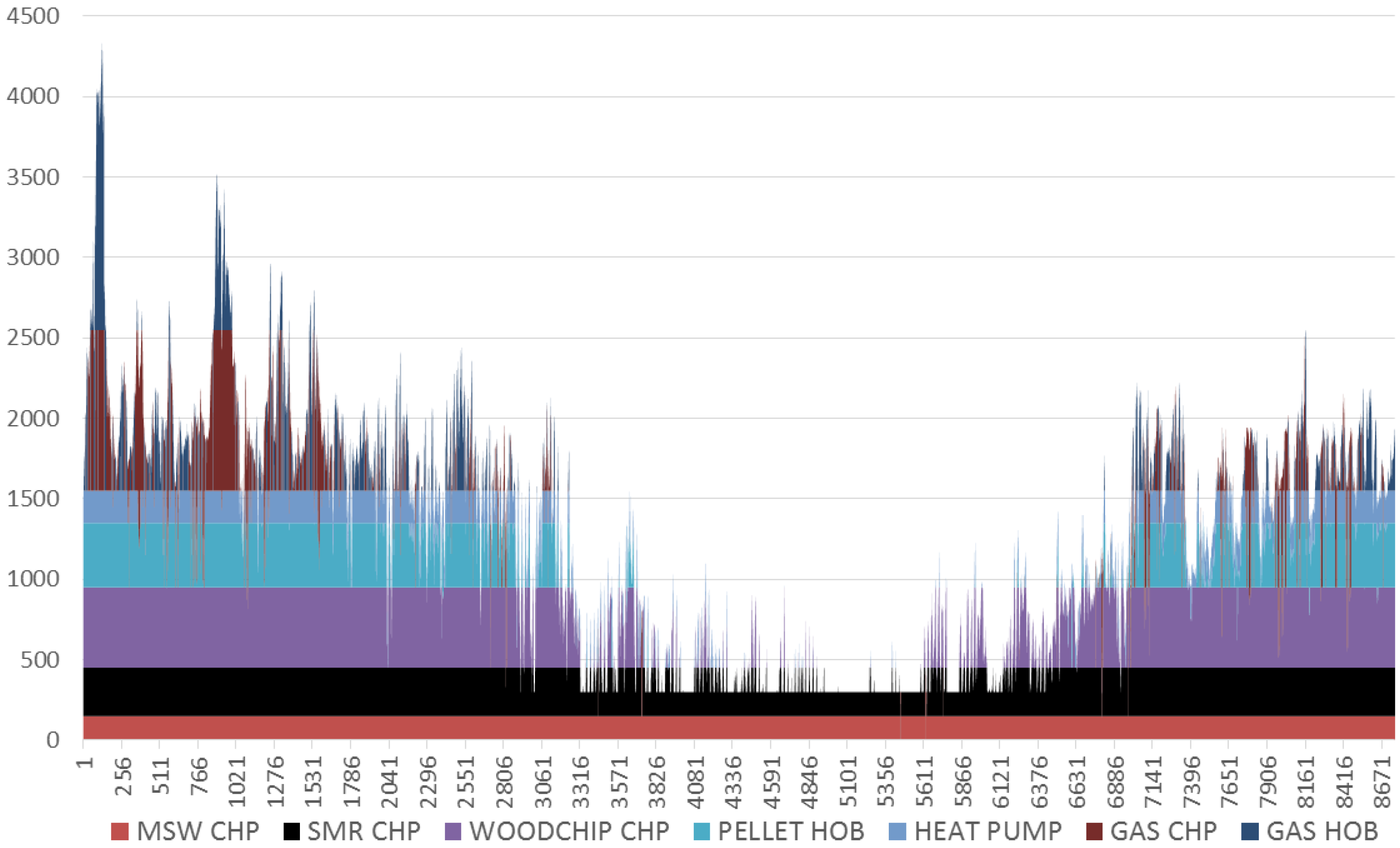

5. Discussion

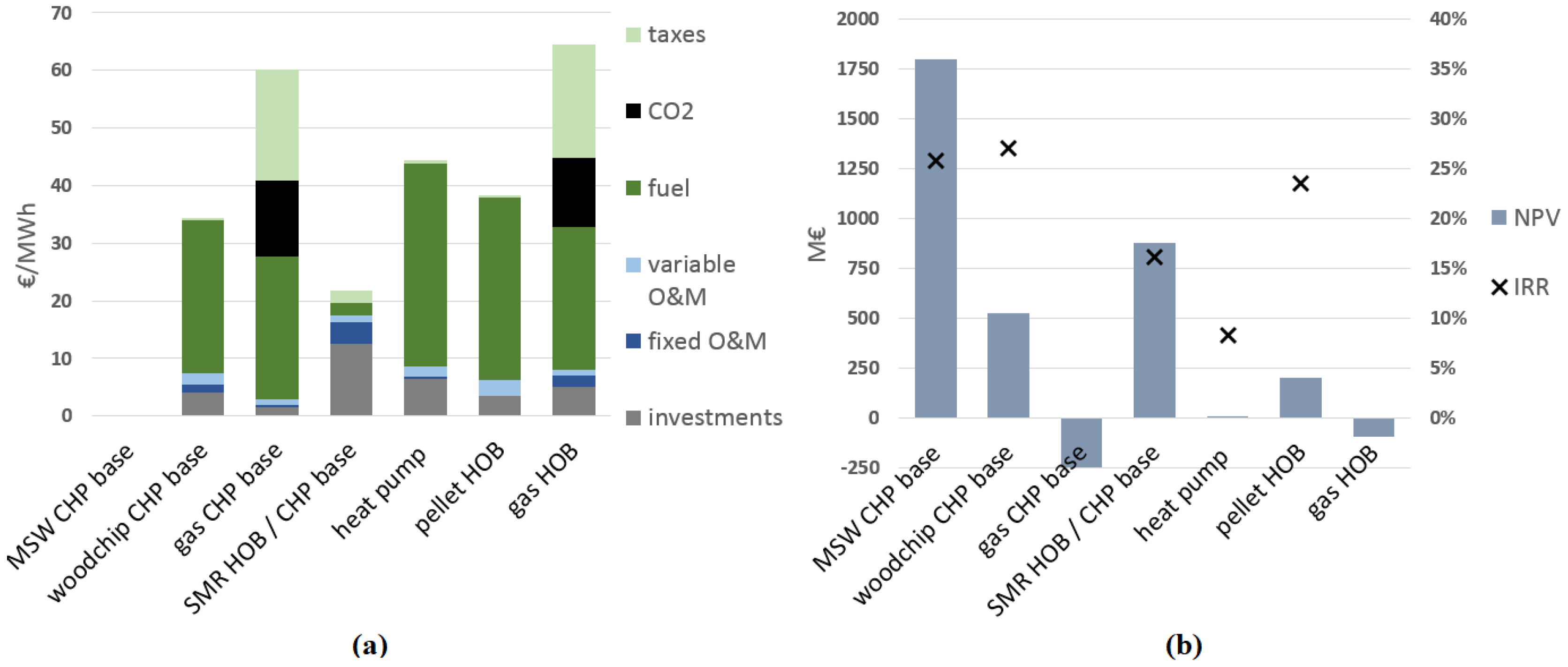

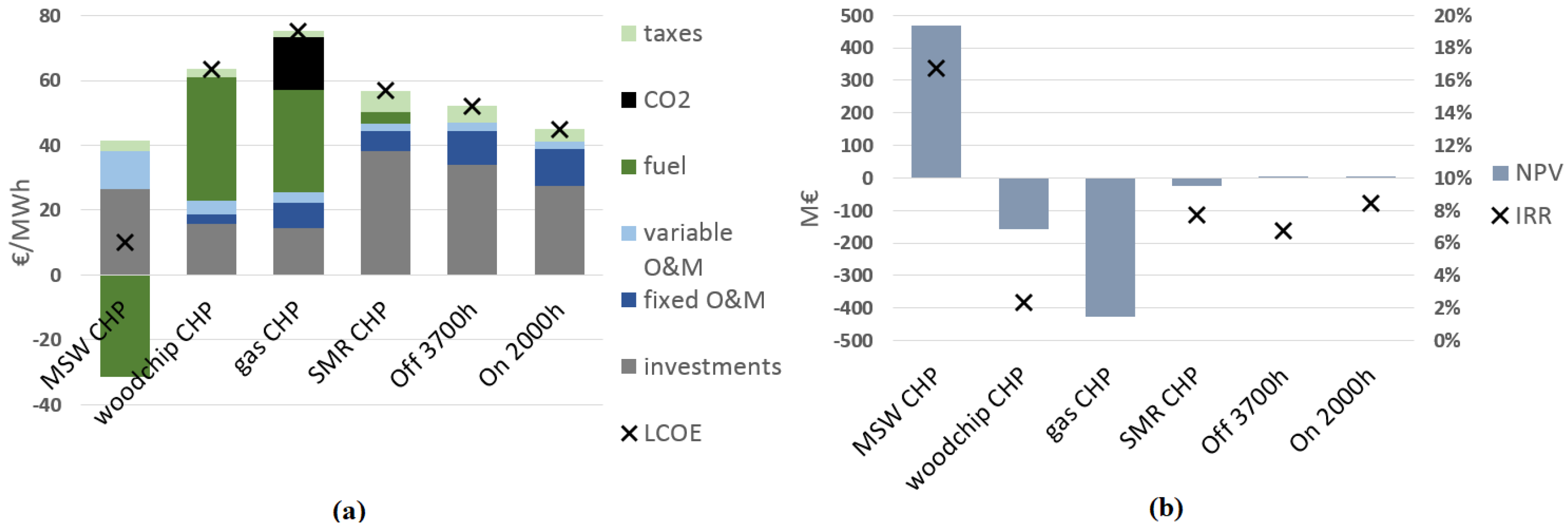

As the scenario analysis contains a fair amount of uncertainty, the most important takeaways from it are rather general ideas. The SMR HOB and CHP both have potential as baseload plants. This is especially true when considering which plants they primarily run against. While biomass and especially waste might seem like attractive options, both should be looked at through the lens of fuel supply and its sustainability. If considering the fuel sourcing for both and additionally the siting for biomass, both must be considered quite limited in their capacity for expansion. In this case, the question starts to move away from “What is the cheapest way to produce heat sustainably?” towards “What options for sustainable heat production are there left?”.

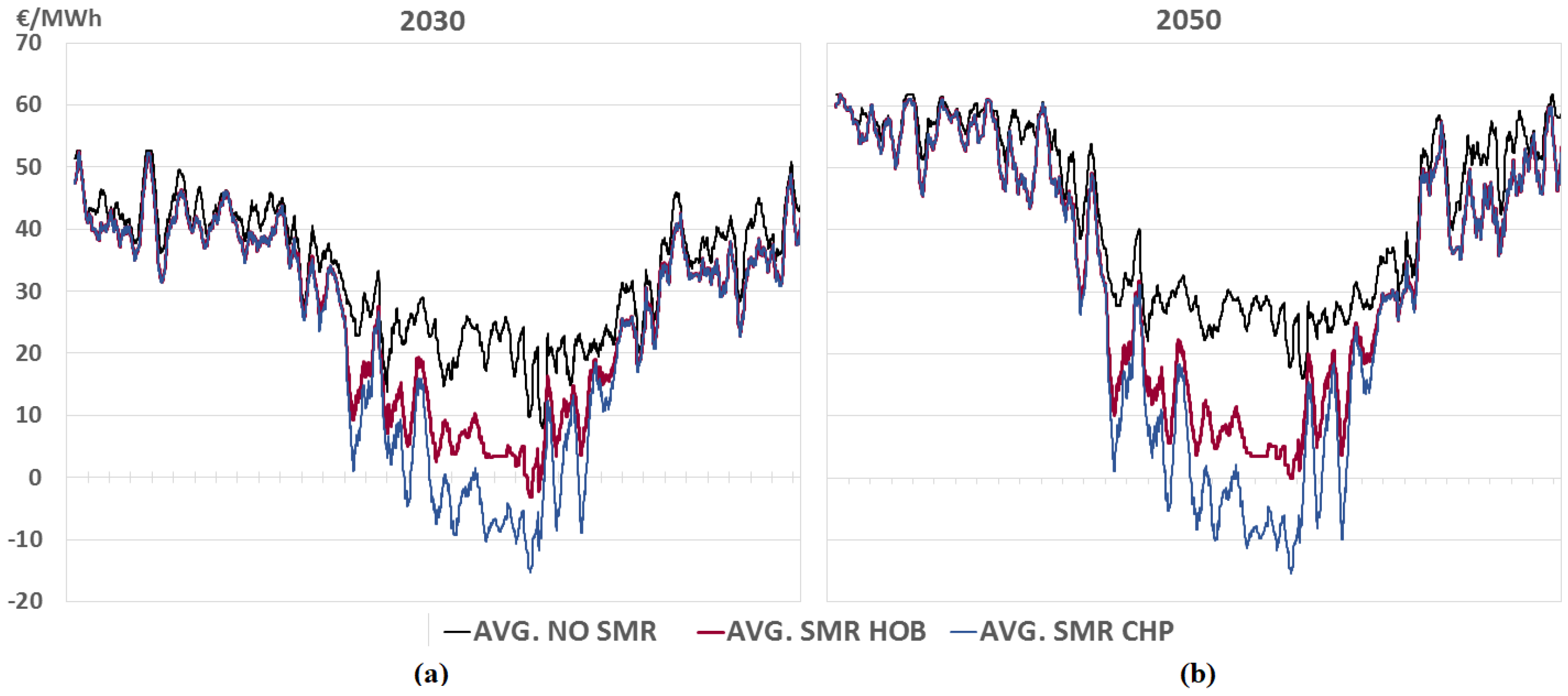

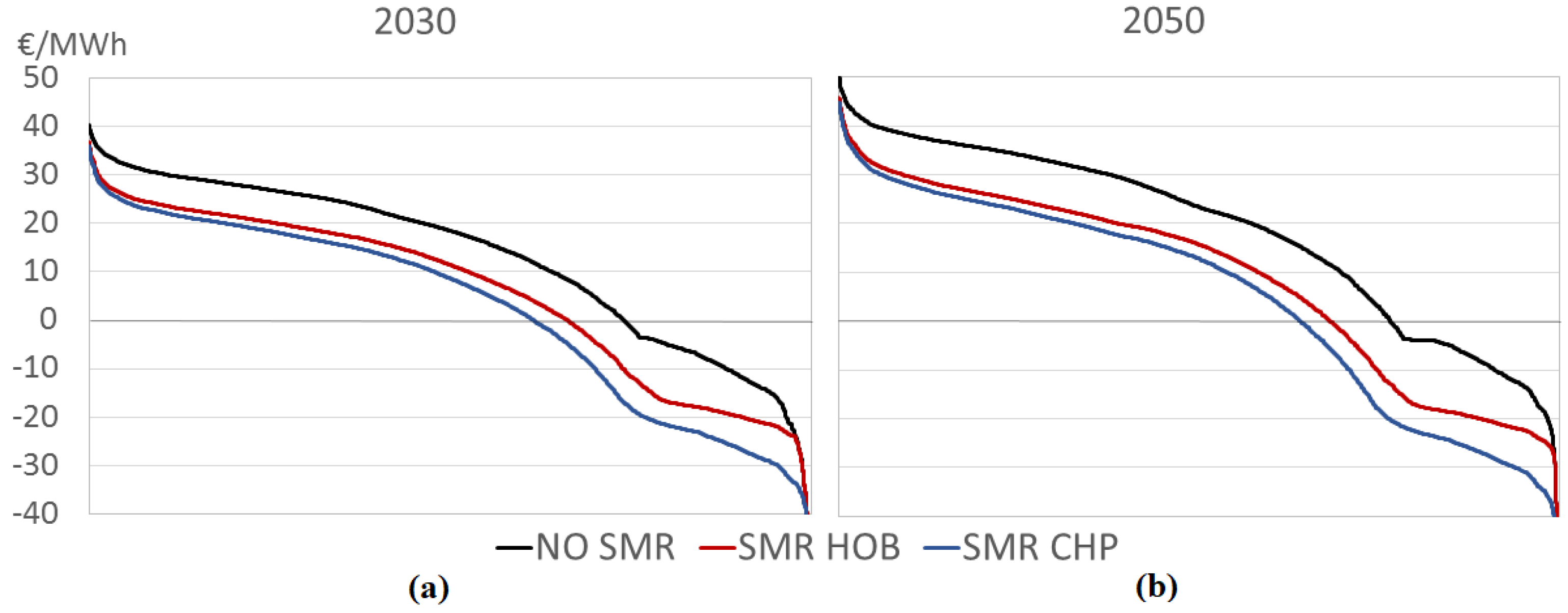

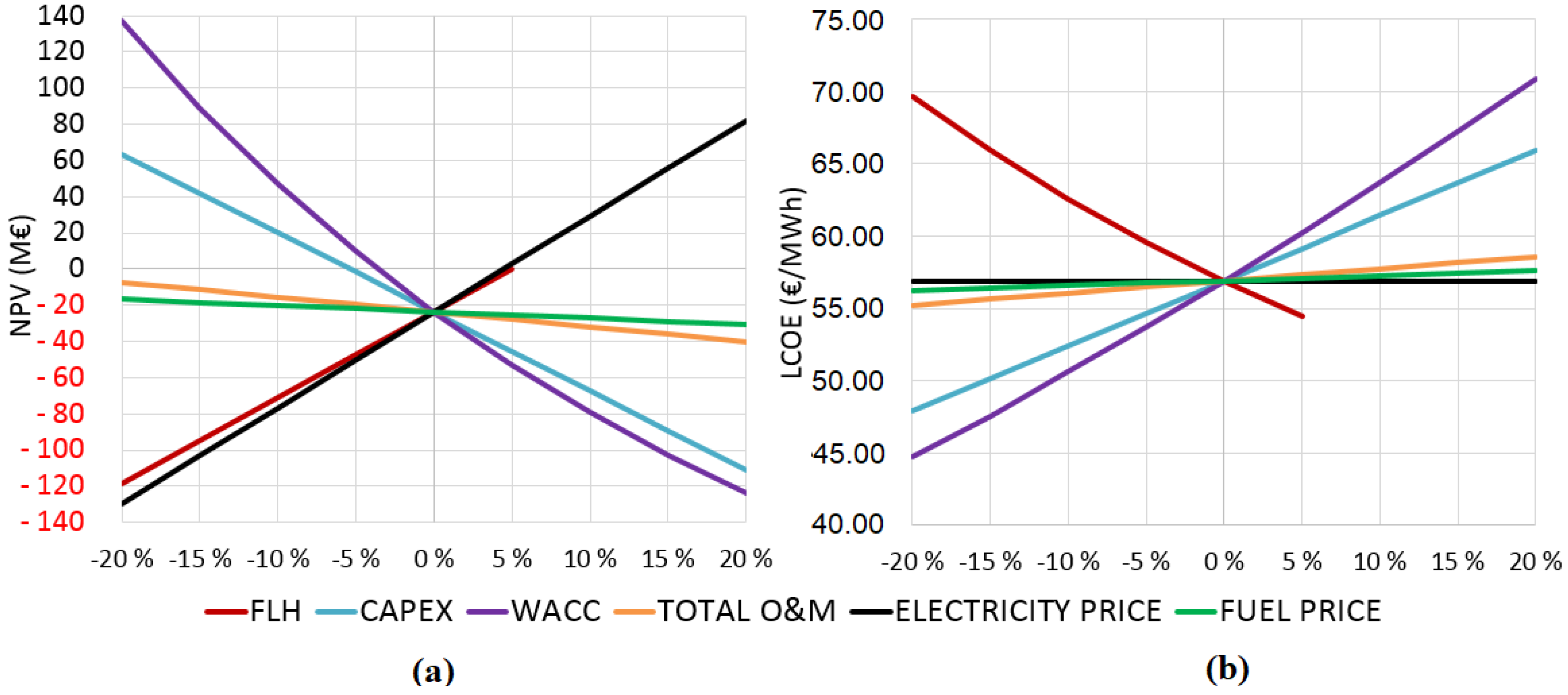

In this discussion, based on the scenario runs, the SMR option is rather strong. Compared to, for example, the pellet HOBs and heat pumps that the companies Helen and Fortum have invested in the greater Helsinki region, heat produced by SMR HOB is cheaper based on its LCOH and its NPV and IRR values seem comparatively strong. Similarly to the currently existing situation, the trend of investments towards HOBs instead of CHP plants also seems to continue. While the investments would overall be profitable, the additional investments compared to just building a HOB do not necessarily justify themselves. This is especially true if wind power’s learning rate stays at its presumed level and its LCOE continues to drop. The continued build-up of wind power might still also result in a resurgence of CHP, if there is enough monetary value given to the ability to support the power system when it suffers from the negative effects of high amounts of intermittent generation. The SMR CHP is already very close to profitability at the WACC of 8% and if it could realize additional profits through load following and heat storage, it would most likely be a more viable option. Still as noted in the sensitivity analysis, the FLH amount is critical to the profitability of the SMR CHP and if the increased amount of wind power drives other production out of the market, the CHP investment starts to look undesirable.

Even if the sustainability of expanding the use of biomass might be questionable, the option should be assessed. The main comparisons are between SMR and pellet HOBs and SMR and woodchip CHP plants. Between the HOBs, the pellet option has some significant advantages. While the SMR LCOH is lower, the pellet HOB has significantly lower initial investment costs and a higher IRR. The same point of lower initial investment also applies to the woodchip CHP. It should also not be ignored that the SMR is built with a lifetime of 60 years in mind. While this has some advantages in the form of overall longevity, it also leaves the plants profitability more vulnerable to changes unforeseeable at the point of the investment decision. In comparison, the woodchip CHP has a lifespan of 30 years, while a pellet HOB would need to be replaced after 20 years. Also, while still vulnerable to changes over time, any life and depreciation time of over 7 years for an SMR HOB in the investment model does still produce a positive NPV. This brings the credibility of the values used to question, but functions as a starting point to note that the plant does not require its full lifetime to become profitable.

While gas production was mostly driven out in this scenario by taxation and CO2 pricing, there are still cases where this might not necessarily be certain. The CO2 and gas prices can change beyond assumptions used here, while the plants are still cheap and extremely maneuverable. If one of SMR CHPs’ selling points is its load following capacity, it could also face competition in this field from peaking gas plants. Gas HOBs might also still continue to see investments to fulfil the peak load demand as they are among the lowest cost plants with regard to investment cost. The secondary option for this would be electrical boilers, which could fulfil similar ramping role.

Similar to the electrical boilers, heat pump profitability is also dependent on the relation between the heat and electricity pricing. While most likely profitable, the expansion of the capacity is also limited by the amount of heat sources available close to the network. It should also be noted that district cooling is also an opportunity for heat pumps that was ignored here and would most likely increase their profitability.

Between the SMR HOB and CHP plant, the HOB seems like the more stable investment. If built, the plant would most likely provide stable baseload at a low cost over its lifetime, if the network it is connected to has a high enough base heat demand. A city the size of Helsinki, even without the full metropolitan area, would most likely be able to support a module or two. The CHP plant is a more complicated matter. While the electricity price is presumed to rise here, estimating in detail the level and volatility of the electricity price series with the presumed high levels of wind power is outside of the scope of this work.

The uncertainty of the base data still permeates most of the results presented here. The sensitivity analysis performed provides an initial view of what kind of effect various developments to the plant data could have. While the NPV and IRR values for the HOB presented here might seem somewhat unrealistic, the profitability and the affordability of the production seem to be fairly stable even under changes to some primary values. For the additional investment towards a CHP plant, the situation is almost reversed as the already unprofitable plants NPV does decrease in a noteworthy manner with even minor changes. For both plants, the financing of the plant will be critical and 2030 as a starting point might seem early as the plants will need to prove themselves to be both financially and technically competitive for the cost of capital to drop down to suitable levels.

6. Conclusions

It might still be too early to definitively answer the main question of this work: Under which assumptions would SMRs be financially appealing for DH production? Nevertheless, the initial results gained here do seem promising for any DH network with a large enough base heat demand that cannot be directly supplied alone by MSW incineration plants and where stringent CO2 emission reduction targets are pursued. The SMR technology itself seems suitable for district heating. The small scale means that a single module can fit into a fairly small DH network. At the same time, the modular nature of SMRs also means that the plants can be built for a variety of production configurations. At the moment, producing only heat seems like the better choice from the return on investment point of view, but this will rely heavily on the future development of both the electricity and heating markets. The recent increase in power rating of 20% for the NuScale SMR without an increase in the capital costs means that even though the numbers used here contain a fair amount of uncertainty, the acceptable margin of error has grown significantly when considering the credibility and accuracy of the results. If the financing costs can be kept down and generating the full baseload by MSW and/or biomass is not possible or sustainable, SMRs could be a recommendable future option for sustainable heat production.

It would also be important to have this foresight in the development of national legislation: currently, Finnish nuclear licensing legislation is aimed at individual large nuclear generation units, whereas the introduction of small modular reactors into commercial use might need a change of legislation to allow the licensing of common reactor designs instead of heavy and time-consuming full licensing procedure of each individual unit. This development would also most likely require heavier international co-operation between authorities to utilize common guidelines for licensing to truly achieve unified reactor-fleets that can utilize the economies of scale on a wider scale.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}