1. Introduction

Studies on the co-movement between crude oil and stock markets have important implications for the formulation of energy policies and portfolio diversification. As one of the most important inputs in industrial production, crude oil significantly influences general price levels as well as economic activity. In the financial economic realm, the risk premium has a significant impact on the asset price of both crude oil and stock prices; for example, credit risk, interest rate, and volatility. As suggested by Hamilton [

1], there has been a growing interest in the effects of oil prices on stock returns and the economy. In this paper, we mainly address the question of which kinds of factors can affect the co-movement between crude oil and stock markets. Understanding these factors will provide the additional information that is needed for portfolio diversification and policy-making. The time-varying correlation has been well documented (Malik and Hammoudeh [

2]; Filis et al. [

3]; Arouri et al. [

4]; Tamakoshi and Hamori [

5,

6]; Basher and Sadorsky [

7]) as a risk management tool in portfolio administration. Moreover, the financialization of the commodity markets is strengthening due to their strong correlation with other financial markets, especially stock markets. There is empirical evidence of a growing correlation between oil and stock markets (Büyüksahin and Robe [

8]; Silvennoinen and Thorp [

9]). Hence, there is good reason to investigate the factors affecting this correlation. Thus, we employed the dynamic conditional correlation–mixed-data sampling (DCC–MIDAS) model proposed by Colacito et al. [

10] to define this long-term correlation. By utilizing the DCC–MIDAS method and panel data analysis, we could uncover the factors that influence the correlation in the long-term.

By adding crude oil to the portfolio as an alternative financial asset, we obtained an additional diversification benefit from its low correlation with the stock-based portfolio. Moreover, the co-movement of cross-assets has significant economic implications for the linkage between crude oil and stock markets, as the price of crude oil is a fundamental economic indicator. In particular, understanding the co-movement between stocks and crude oil markets in the long-term yields information about potential drivers to predict the future economy and hedge portfolio risks.

We provide useful information to investors regarding portfolio allocation or international diversification. This correlation is the key to achieving an optimal portfolio because changes in the correlation imply changes in portfolio weights. Specifically, our results indicate that macroeconomic factors work effectively in determining the correlation between oil and stock markets. Moreover, crude oil can reduce portfolio risk during a financial crisis when the correlation decreases.

Many extensive empirical studies have discussed the relationship between stocks and the stock market extensively. Generally, three types of studies can be categorized: the first type analyzes the causal relationship between stock and crude oil markets. Some studies have shown that stock market returns are significantly influenced by crude oil price movements (Aloui and Jammazi [

11]; Chen [

12]; Ghouri [

13]; Jones and Kaul [

14]; Kilian and Park [

15]; Miller and Ratti [

16]; Sadorsky [

17]; Papapetrou [

18]). These studies provided evidence of a negative effect on stock markets from a positive oil shock, although they employed different samples and consider different countries. On the other hand, other studies indicated that the relationship between the crude oil market and stock market is positive and significant. For example, Chen et al. [

19], El-Sharif et al. [

20], and Narayan and Narayan [

21] provided evidence of a positive impact on the oil and gas sectors’ stock returns in the UK, given an increase in oil prices. In addition, other papers have provided similar evidence in developing countries (Kanjilal and Ghosh [

2]; Li et al., [

22]; Narayan and Narayan [

21]; Zhu et al. [

23]). By contrast, some of the literature has focused on the non-linear relationship between crude oil and the stock market (Narayan and Gupta [

24]; Jiménez-Rodríguez [

25]; Ponka [

26]). Although their findings are mixed, crude oil still exhibits significant power on the stock market.

In contrast to the first type of study, the second type can be classified as investigating the dynamic correlation between stock and crude oil markets. Generally, the multivariate generalized autoregressive conditional heteroskedasticity (MGARCH) model has been applied in the energy finance literature (Arouri et al. [

27,

28]; Arouri et al. [

4]; Basher and Sadorsky [

7]; Conrad et al. [

29]; Filis et al. [

3]; Malik and Hammoudeh [

30]; Malik and Ewing [

31]; Sadorsky [

32,

33]). These studies mainly discussed the spillover effect and volatility transmission between stock and crude oil markets. For example, Filis et al. [

3] provided evidence that the time-varying correlations between stocks and oil prices are similar for both oil-importing and oil-exporting countries. However, there is a bidirectional spillover effect between the US stock and crude oil market and a spillover effect from oil to European stock markets (Arouri et al. [

4]; Arouri et al. [

27]). As shown in the study of Conrad et al. [

29], macroeconomic leading indicators will be helpful predictors of the oil–stock correlation. Basher and Sadorsky [

7] provided an overview of the time-varying correlation between emerging stock and crude oil markets and estimated the hedging ratio. Bampinas and Panagiotidis [

34] also summarized the time-varying cross-market linkage by considering the four major crises and found that oil can be an alternative safe haven asset during crises. Yin [

35] and Nguyen and Walther [

36] also found that the crude oil price responds to the macroeconomic condition sensitively in the framework of GARCH–MIDAS. Kilian [

37] and Kilian [

38] reported that the global real economic activity is an important driver for oil prices.

The third type of study includes other models which are employed to investigate the interdependence between stocks and oil. In most cases, this type of investigation is based on the copula model or wavelet analysis. For example, Aloui et al. [

39] provided evidence of a positive dependence between oil and the stock markets in six Central and Eastern European countries. By employing the wavelet approach, Martín-Barragán et al. [

40] found several correlational breakdowns caused by financial and oil shocks, both at lower and higher frequencies. Aloui and Aïssa [

41] also provided evidence that the dynamics between stocks and oil prices are not constant over time, and the dependence structure of this was significantly affected by the 2007–2009 financial crisis. Cai et al. [

42] analyzed the interdependence between oil and East Asian stock returns using wavelet techniques.

In summary, while numerous studies have explored the interdependence between crude oil and stock markets and volatility spillovers, little is known about the factors determining the long-term correlation between these two variables. The contribution of this study is threefold. First, we elicit detailed information from the volatility in stock and crude oil markets in both the short and long terms. As speculators are more interested in short-term investment, our study provides useful information to speculators and investors regarding hedging or portfolio management. Furthermore, the long-term co-movement between stocks and crude oil may provide an anchor for policymakers to implement economic policy. Secondly, we revealed detailed information about the time-varying correlation between stock and crude oil markets on both short- and long-term scales. Thus, we could detect dynamic structures and changes over various time periods and provide additional information regarding structural breaks in markets and economies. Specifically, instant changes in the market can be detected via short-term scales, while economic structural breaks can be identified by long-term scales. Finally, we comprehensively revealed the factors that can influence the co-movement between stock and crude oil markets. Particularly, by treating macroeconomic and financial factors differently, we could distinguish the influence of each factor, which provided us with a more detailed framework of the determinants of co-movement between stock and crude oil markets.

The rest of this paper is presented as follows.

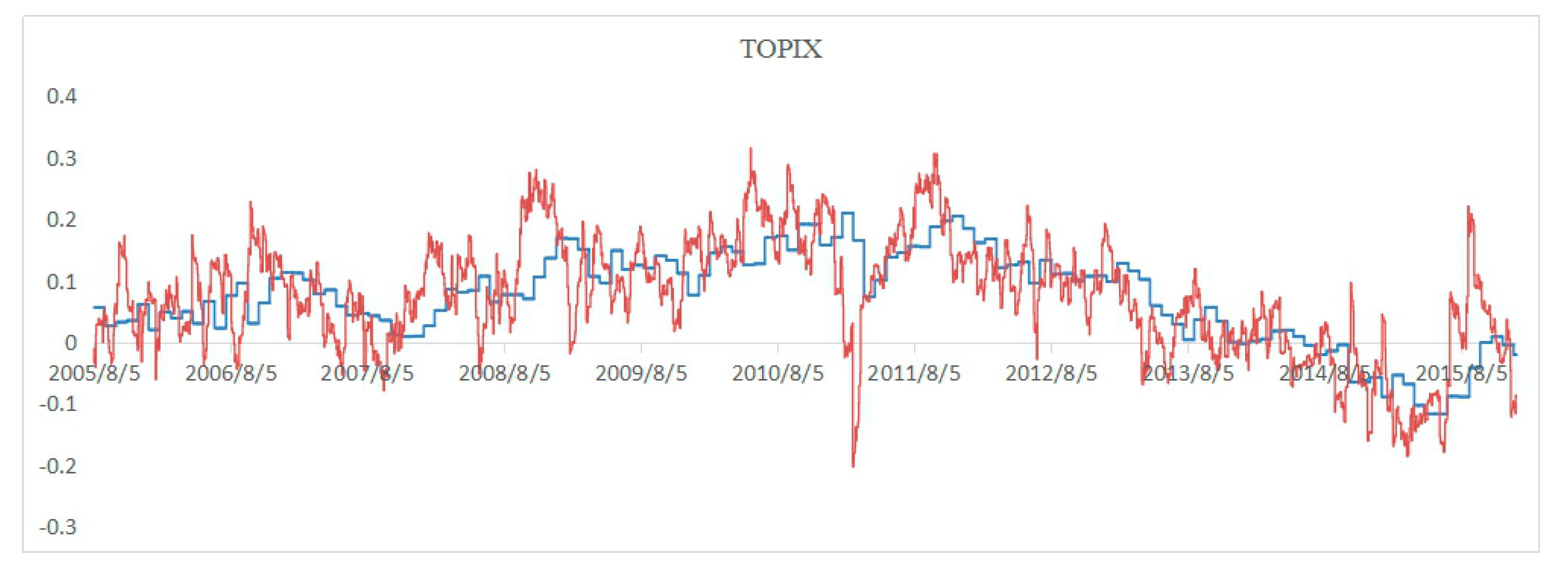

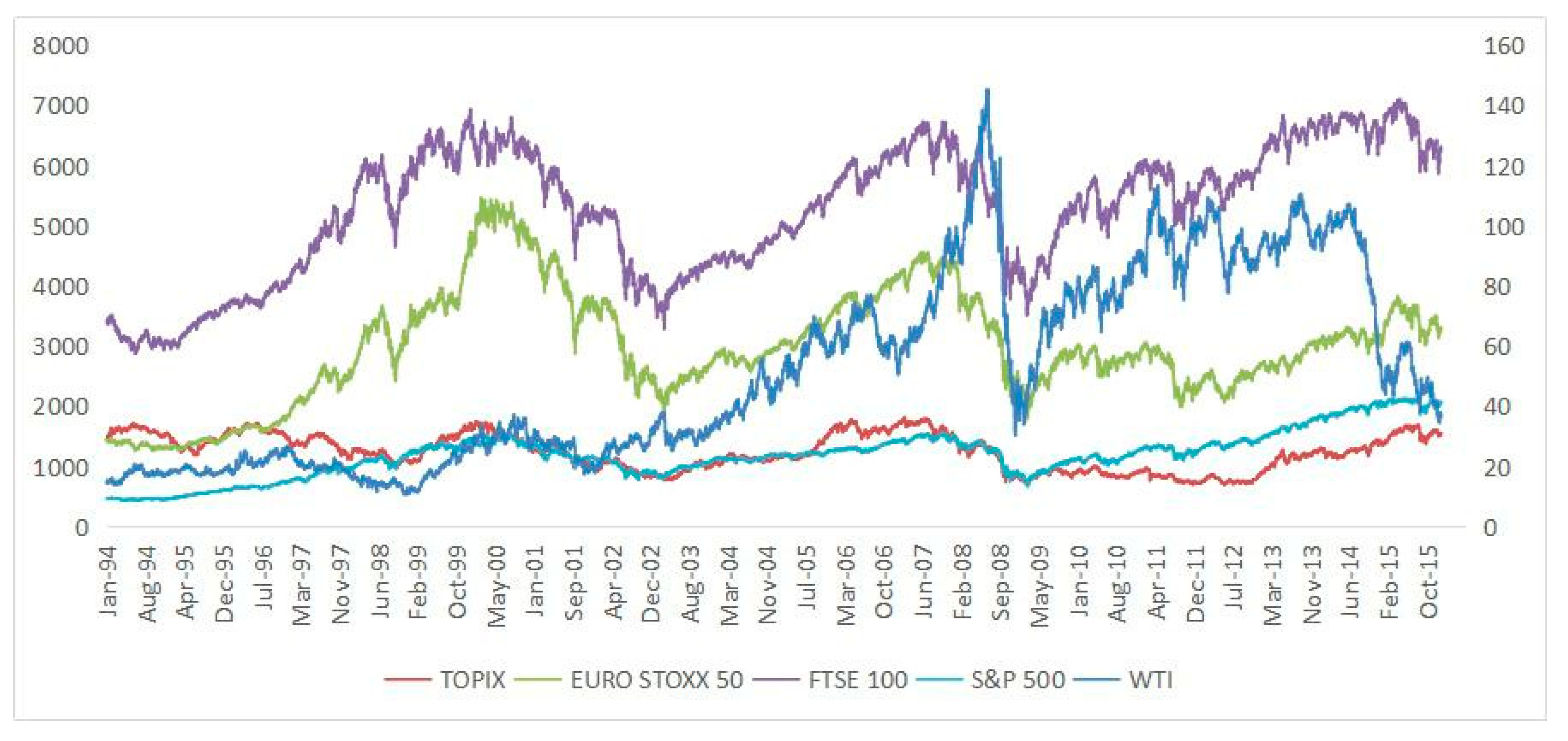

Section 2 analyzes the data based on the GARCH–MIDAS model.

Section 3 identifies the factors that influence the dynamic correlation between the stock and crude oil markets in the long-term.

Section 4 provides concluding remarks.

4. Conclusions

This article investigated the financial and macroeconomic factors that influence the monthly correlation between crude stock and crude oil markets by employing the MIDAS approach and panel data analysis.

In the analysis of the monthly volatility in the stock and crude oil markets, we identified the 2008 global financial crisis as significantly increasing volatility for all markets. By contrast, the 1997 Asian financial crisis had a lower impact on these markets. Furthermore, by employing the DCC–MIDAS model, we investigated the conditional correlation between the stock and crude oil markets in the long term and obtained the following findings. First, the long-term conditional correlations between stock and crude oil markets are positive for all cases, except during 2008 global crisis periods. Second, the Japanese stock market prices show the smallest degree of correlation with oil prices, while the UK stock market prices show the largest degree of correlation. Third, the 2008 global financial crisis had little impact on the long-term correlation between stock and crude oil markets.

We ran panel regressions to further explore the factors that can affect the long-term conditional correlation between the stock and crude oil markets. The results of our panel regression analysis reveal that both economic activity and credit risk have a negative effect on the correlation between stock and crude oil markets in the long-term. However, the long-term correlation between crude oil and stock markets increases with increases in the risk-free rate. Our empirical results imply that a rise in the risk-free rate increases the conditional correlation between crude oil and stock returns in the long-term, while an increase in economic activity or credit risk decreases the conditional correlation in the long-term.

The reasons for these conclusions are twofold. From an economic perspective, a rise in risk-free rate in one country increases the nominal returns on both the stock and crude oil markets. Moreover, relative strength in the economy raises stock market prices, with a relative decrease in the returns on oil prices, since the currency in such an economy appreciates. From a financial perspective, stock prices decline owing to a relatively high risk-free rate environment in one country, whereas the crude oil prices remain independent in such an environment. Moreover, crude oil futures or crude oil-related derivatives may serve as a good hedge asset when the credit risk increases as the stock market slumps.

At least two policy implications can be provided by our research. From an economic perspective, because risk-free rate has a positive impact on the correlation between the stock and crude oil markets, we notice that the inflationary environment works effectively in asset pricing. Therefore, monetary authorities must be prudent when implementing their monetary policies. From a financial perspective, a diversification benefit exists between stocks and crude oil, especially during periods of financial crisis.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}