The Benefit of Collaboration in the North European Electricity System Transition—System and Sector Perspectives

Abstract

:1. Introduction

2. Materials and Methods

2.1. Model Description and Scope

2.2. Transportation Sector

2.3. Industry Sector

2.4. Heat Sector

2.5. Scenarios

3. Results

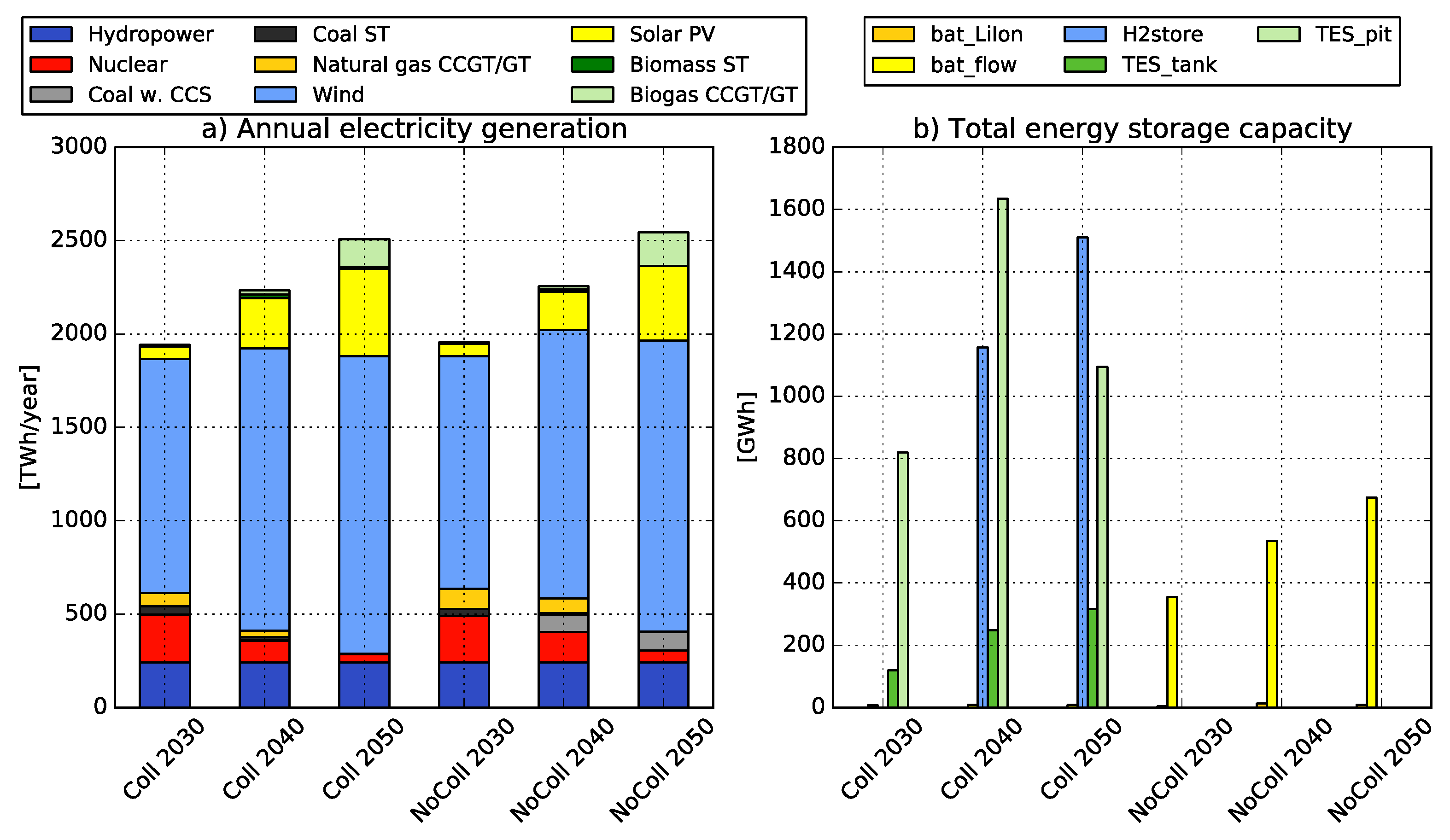

3.1. System Planner Perspective

3.2. Sector Perspective

4. Discussion

4.1. Model Limitations

4.2. Result Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Technology | Investment Cost 2030 [M€/MW] | Investment Cost 2050 [M€/MW] | Variable Costs [€/MWh] | Fixed O&M Costs [k€/MW,yr.] | Life-Time [yr.] | Minimum Load Level [Share of Rated Power] | Start-Time [h] | Start Cost [€/MW] |

|---|---|---|---|---|---|---|---|---|

| Coal ST | 1.56 | 1.56 | 17 | 27 | 40 | 0.35 | 12 | 192 |

| Coal CHP | 1.56 | 1.56 | 21 | 27 | 40 | 0.35 | 12 | 192 |

| Coal CCS | 3.00 | 3.00 | 21 | 91 | 40 | 0.35 | 12 | 192 |

| NG CCGT | 0.78 | 0.78 | 39 | 13 | 30 | 0.2 | 6 | 44 |

| NG GT | 0.39 | 0.39 | 64 | 8 | 30 | 0.5 | 0 | 32 |

| NG CHP | 1.01 | 1.01 | 48 | 17 | 30 | 0.32 | 12 | 102 |

| NG CCS | 1.80 | 1.80 | 53 | 35 | 30 | 0.35 | 12 | 192 |

| Biomass ST | 1.86 | 1.86 | 90 | 50 | 40 | 0.35 | 12 | 192 |

| Biomass CHP | 3.15 | 3.15 | 119 | 58 | 40 | 0.35 | 12 | 192 |

| Waste CHP | 6.63 | 6.63 | 7 | 443 | 40 | 0.35 | 12 | 192 |

| Biogas CCGT | 0.76 | 0.76 | 117 | 13 | 30 | 0.2 | 6 | 47 |

| Biogas GT | 0.38 | 0.38 | 195 | 8 | 30 | 0.5 | 0 | 55 |

| Bio-coal CCS (flex) | 3.46 (3.64) | 3.46 (3.64) | 40 | 107 (113) | 30 | 0.35 (0.15) | 12 (6) | 192 (110) |

| Hydropower | 2.06 | 2.06 | 1.0 | 47 | 500 | 0 | 0 | 0 |

| Nuclear | 5.15 | 5.15 | 16.5 | 154 | 60 | 0.7 | 24 | 670 |

| Solar PV | 0.99 | 0.60 | 1.1 | 10 | 25 | 0 | 0 | 0 |

| Onshore wind | 1.33 | 1.23 | 1.1 | 30 | 25 | 0 | 0 | 0 |

| Offshore wind | 3.29 | 2.21 | 1.1 | 100 | 25 | 0 | 0 | 0 |

| Transmission (OHAC) | 0.6 (per km) | 0.6 (per km) | 0.01 | - | 40 | 0 | 0 | 0 |

| Transmission (HVDC) | 0.756 + 0.63 (per km) | 0.756 + 0.63 (per km) | 0.01 | - | 40 | 0 | 0 | 0 |

| Variation Management Technology | Investment Cost [M€/ MW(h)] | Efficiency [%] | Fixed O&M Costs [k€/MW(h), yr.] | Life-Time [yr.] |

|---|---|---|---|---|

| Battery, Li-ion | 0.15 | 95 | 25 | 15 |

| Battery, Flow | 0.10 | 70 | 13 | 30 |

| Electrolyzer | 0.59 | 75 | 20 | 20 |

| H2 storage | 0.01 | 100 | - | 50 |

| Heat pump | 1.00 | 300 | 8 | 25 |

| Electric boiler | 0.05 | 100 | - | 20 |

| TES tank | 0.03 | 95 | - | 20 |

| TES pit | 0.004 | 80 | - | 20 |

Appendix C

| Iteration Number (j) | ajlow | bj | ajhigh |

|---|---|---|---|

| 1 | 0.5 | 0.5 | 0.1 |

| 2 | 0.6 | 0.6 | 0.1 |

| 3 | 0.7 | 0.7 | 0.2 |

| 4 | 0.8 | 0.8 | 0.2 |

| 5 | 0.8 | 0.9 | 0.3 |

| 6 | 0.8 | 1 | 0.4 |

| 7 | 0.8 | 1 | 0.5 |

| 8 | 0.8 | 1 | 0.6 |

| >8 | 0.8 | 1 | 0.6 |

Appendix D

- Assign NUTS-2 regions to the climate regions deployed in [31]. As the climate regions are not based on a NUTS division the mapping between the regions is not perfect, i.e., borders of a climate region do not align with NUTS-2 region borders. In cases where the NUTS-2 region overlaps two climate regions the NUTS-2 region is assigned to the climate region in which it has the largest area.

- Segment the original building stock and the NUTS-2 data on number of buildings (coming from EU statistics) into archetype categories of single-family dwellings (SFDs) and multi-family dwellings (MFDs). In the original building stock representation this division has already been made. For the Eurostat NUTS-2 building statistics the categories RES1 and RES2 are assigned as SFD and RES_GE3 are assigned as MFDs.

- Create weights, i.e., the number of buildings, for each archetype building in each NUTS-2 region. Start by summing up the total number of SFDs and MFDs, separately, from the Eurostat data in all the NUTS-2 regions belonging to a specific climate region. Then calculate the share of SFDs and MFDs in each of these NUTS-2 in relation to the calculated total number of SFDs and MFDs. This gives the distribution of SFDs and MFDs for the NUTS2-resions within each climate region. The weight of each archetype building in the original building stock description, which is for a whole climate region, is then divided into the NUTS-2 regions based on the share of the category (SFD or MFD) that the archetype building belongs to in the corresponding NUTS-2 region. Thereby, creating weights for each archetype building in each NUTS-2 region.

- The final step is assigning the archetype weights from each NUTS-2 region to each region in Figure A1. As these regions correspond to specific NUTS-2 regions the mapping between these is straight forward. The weights for each archetype for all NUTS-2 regions belonging to a region is summed up, resulting in one weight for each archetype in each region in Figure A1.

References

- Commission, E. A Clean Planet for All—A European Strategic Long-Term Vision for a Prosperous, Modern, Competitive and Climate Neutral Economy; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- United Nations. Paris Agreement; UNFCCC, Ed.; United Nations: San Francisco, CA, USA, 2015. [Google Scholar]

- Lechtenböhmer, S.; Nilsson, L.J.; Åhman, M.; Schneider, C. Decarbonising the energy intensive basic materials industry through electrification—Implications for future EU electricity demand. Energy 2016, 115, 1623–1631. [Google Scholar] [CrossRef] [Green Version]

- Connolly, D. Heat Roadmap Europe: Quantitative comparison between the electricity, heating, and cooling sectors for different European countries. Energy 2017, 139, 580–593. [Google Scholar] [CrossRef]

- International Energy Agency. World Energy Outlook; IEA/OECD: Paris, France, 2018. [Google Scholar]

- Hirth, L. The market value of variable renewables: The effect of solar wind power variability on their relative price. Energy Econ. 2013, 38, 218–236. [Google Scholar] [CrossRef] [Green Version]

- Göransson, L.; Johnsson, F. A comparison of variation management strategies for wind power integration in different electricity system contexts. Wind Energy 2018, 21, 837–854. [Google Scholar] [CrossRef]

- Kiviluoma, J.; Rinne, E.; Helistö, N. Comparison of flexibility options to improve the value of variable power generation. Int. J. Sustain. Energy 2018, 37, 761–781. [Google Scholar] [CrossRef]

- Pilpola, S.; Lund, P.D. Different flexibility options for better system integration of wind power. Energy Strategy Rev. 2019, 26. [Google Scholar] [CrossRef]

- Bernath, C.; Deac, G.; Sensfuß, F. Influence of heat pumps on renewable electricity integration: Germany in a European context. Energy Strategy Rev. 2019, 26. [Google Scholar] [CrossRef]

- Papaefthymiou, G.; Hasche, B.; Nabe, C. Potential of heat pumps for demand side management and wind power integration in the German electricity market. IEEE Trans. Sustain. Energy 2012, 3, 636–642. [Google Scholar] [CrossRef]

- Taljegard, M.; Göransson, L.; Odenberger, M.; Johnsson, F. Impacts of electric vehicles on the electricity generation portfolio—A Scandinavian-German case study. Appl. Energy 2019, 235, 1637–1650. [Google Scholar] [CrossRef]

- Richardson, D.B. Electric vehicles and the electric grid: A review of modeling approaches, Impacts, and renewable energy integration. Renew. Sustain. Energy Rev. 2013, 19, 247–254. [Google Scholar] [CrossRef]

- Foley, A.; Tyther, B.; Calnan, P.; Ó Gallachóir, B. Impacts of Electric Vehicle charging under electricity market operations. Appl. Energ 2013, 101, 93–102. [Google Scholar] [CrossRef]

- Baruah, P.J.; Eyre, N.; Qadrdan, M.; Chaudry, M.; Blainey, S.; Hall, J.W.; Jenkins, N.; Tran, M. Energy system impacts from heat and transport electrification. Proc. Inst. Civ. Eng. Energy 2014, 167, 139–141. [Google Scholar] [CrossRef]

- Lund, P.D.; Skytte, K.; Bolwig, S.; Bolkesjö, T.F.; Bergaentzlé, C.; Gunkel, P.A.; Kirkerud, J.G.; Klitkou, A.; Koduvere, H.; Gravelsins, A.; et al. Pathway analysis of a zero-emission transition in the Nordic-Baltic region. Energies 2019, 12, 3337. [Google Scholar] [CrossRef] [Green Version]

- Brown, T.; Schlachtberger, D.; Kies, A.; Schramm, S.; Greiner, M. Synergies of sector coupling and transmission reinforcement in a cost-optimised, highly renewable European energy system. Energy 2018, 160, 720–739. [Google Scholar] [CrossRef] [Green Version]

- McPherson, M.; Tahseen, S. Deploying storage assets to facilitate variable renewable energy integration: The impacts of grid flexibility, renewable penetration, and market structure. Energy 2018, 145, 856–870. [Google Scholar] [CrossRef]

- Amelin, M.; Englund, C.; Fagerberg, A. Balansering av Vindkraft och Vattenkraft i Norra Sverige; Elforsk: Stockholm, Sweden, 2009. [Google Scholar]

- Müller, C.; Falke, T.; Hoffrichter, A.; Wyrwoll, L.; Schmitt, C.; Trageser, M.; Schnettler, A.; Metzger, M.; Huber, M.; Küppers, M.; et al. Integrated planning and evaluation of multi-modal energy systems for decarbonization of Germany. Energy Procedia 2019, 158, 3482–3487. [Google Scholar] [CrossRef]

- Brown, T.; Schäfer, M.; Greiner, M. Sectoral interactions as carbon dioxide emissions approach zero in a highly-renewable european energy system. Energies 2019, 12, 1032. [Google Scholar] [CrossRef] [Green Version]

- Sørensen, B. Renewable Energy—Physics, Engineering, Environmental Impacts, Economics and Planning; Academic Press: London, UK, 2017. [Google Scholar]

- Göransson, L. A parallel computing approach to account for wind power variation management in electricity system investment models. 2019; Submitted for publication. [Google Scholar]

- Weber, C. Uncertainty in the Electric Power Industry: Methods and Models for Decision Support; Springer: 2005.

- Göransson, L. The Impact of Wind Power Variability on the Least-Cost Dispatch of Units in the Electricty Generation System; Chalmers University of Technology: Gothenburg, Sweden, 2014. [Google Scholar]

- Kjärstad, J.; Johnsson, F. The European power plant infrastructure—Presentation of the Chalmers energy infrastructure database with applications. Energy Policy 2007, 35, 3643–3664. [Google Scholar] [CrossRef]

- Kullingsjö, L.-H.; Karlsson, S. The Swedish Car Movement Data Project; EEVC: Brussels, Belgium, 2012. [Google Scholar]

- Taljegard, M. Electrification of Road Transport-Implications for the Electricity System; Chalmers: Gothenburg, Sweden, 2019. [Google Scholar]

- The Government of the Federal Republic of Germany. Report on the Calculation of Cost-Optimal Levels of Minimum Energy Performance Requirements in Accordance with Article 5(2) and (3) of the EPB Directive (Directive 2010/31/EU of the European Parliament and of the Council of 4 January 2003 on the Energy Performance of Buildings); The Government of the Federal Republic of Germany: Berlin, Germany, 2018.

- Nyholm, E. The Role of Swedish Single-Family Dwellings in the Electricity System—The Importance and Impacts of Solar Photovoltaics, Demand Response, and Energy Storage; Chalmers University of Technology: Gothenburg, Sweden, 2016. [Google Scholar]

- Mata, É.; Kalagasidis, A.S.; Johnsson, F. Building-Stock Aggregation through Archetype Buildings: France, Germany, Spain and the UK. Build. Environ. 2014, 81, 270–282. [Google Scholar] [CrossRef] [Green Version]

- Werner, S. ECOHEATCOOL; Euroheat and Power: Brussels, Belgium, 2005–2006. [Google Scholar]

- IEA. World Energy Outlook 2016; International Energy Agency: Paris, France, 2016.

- Mone, C.; Hand, M.; Bolinger, M.; Rand, J.; Heimiller, D.; Ho, J. 2015 Cost of Wind Energy Review; National Renewable Energy Laboratory: Golden, CO, USA, 2017. [Google Scholar]

- Jordan, G.; Venkataraman, S. Analysis of Cycling Costs in Western Wind and Solar Integration Study; National Renewable Energy Laboratory: Golden, CO, USA, 2012. [Google Scholar]

- Persson, J.; Andgren, K.; Engström, M.; Holm, A.; Pettersson, L.T.; Ringdahl, K.; Sandström, J. Lastföljning i Kärnkraftverk; Elforsk: Stockholm, Sweden, 2012. [Google Scholar]

- Thunman, H.; Larsson, A.; Hedenskog, M. Commissioning of the GoBiGas 20 MW Biomethane Plant. In Proceedings of the International Conference on Thermochemical Conversion Science, Chicago, IL, USA, 2–5 November 2015; Gas Technology Institute: Chicago, IL, USA, 2015. [Google Scholar]

- Johansson, V.; Thorson, L.; Goop, J.; Göransson, L.; Odenberger, M.; Reichenberg, L.; Taljegard, M.; Johnsson, F. Value of wind power—Implications from specific power. Energy 2017, 126, 352–360. [Google Scholar] [CrossRef]

- Lucchesi, R. File Specification for MERRA Products. 2012. [Google Scholar]

- ECMWF. ERA-Interim u- and v-Components of Horizontal Wind, Surface Solar Radiation Downward, Skin Temperature; ECMWF: Reading, UK, 2010. [Google Scholar]

- Nilsson, K.; Unger, T. Bedömning av en Europeisk Vindkraftpotential Med GIS-Analys. PROFU, 2014. [Google Scholar]

- Norwood, Z.; Nyholm, E.; Otanicar, T.; Johnsson, F. A geospatial comparison of distributed solar heat and power in europe and the US. PLoS ONE 2014, 9, 1–31. [Google Scholar] [CrossRef] [PubMed]

- Energistyrelsen. Technology Data for Energy Plants; Energistyrelsen: Copenhagen, Denmark, 2012. [Google Scholar]

- Goransson, L.; Goop, J.; Odenberger, M.; Johnsson, F. Impact of thermal plant cycling on the cost-optimal composition of a regional electricity generation system. Appl. Energy 2017, 197, 230–240. [Google Scholar] [CrossRef]

- Eurostat. Conventional Dwellings by Occupancy Status, Type of Building and NUTS 3 Region (cens_11dwob_r3); Eurostat: Luxembourg, 2011. [Google Scholar]

- Global Modeling and Assimilation Office (GMAO). MERRA-2 Tavg1_2d_rad_Nx: 2d,1-Hourly,Time-Averaged, Single-Level,Assimilation,Radiation Diagnostics V5.12.4; Goddard Earth Sciences Data and Information Services Center (GES DISC): Greenbelt, MD, USA, 2015. [Google Scholar]

- Global Modeling and Assimilation Office (GMAO). MERRA-2 inst1_2d_asm_Nx: 2d,1-Hourly, Instantaneous, Single-Level, Assimilation, Single-Level Diagnostics V5.12.4; Goddard Earth Sciences Data and Information Services Center (GES DISC): Greenbelt, MD, USA, 2015. [Google Scholar]

- European Council. Directive 2010/31/EU of the European Parliament and of the Council of 19 May, 2010 on the Energy Performance of Buildings. Off. J. Eur. Union 2010, 153, 13–35. [Google Scholar]

| Region | 2030 [GWh/year] | 2040 [GWh/year] | 2050 [GWh/year] |

|---|---|---|---|

| SE_N | 650 | 920 | 1300 |

| SE_S | 8400 | 12,000 | 17,000 |

| DE_N | 33,000 | 47,000 | 67,000 |

| DE_S | 55,000 | 78,000 | 110,000 |

| BAL | 4100 | 5900 | 8400 |

| PO_S | 24,000 | 34,000 | 48,000 |

| PO_N | 9400 | 13,000 | 19,000 |

| IE | 4400 | 6200 | 8900 |

| NO | 4000 | 5200 | 6700 |

| FI | 5200 | 7300 | 10,000 |

| UK_S | 43,000 | 61,000 | 87,000 |

| UK_N | 4000 | 5600 | 8000 |

| Region | 2030 [GWhH2/year] | 2040 [GWhH2/year] | 2050 [GWhH2/year] |

|---|---|---|---|

| SE_N | 0 | 12,000 | 12,000 |

| SE_S | 0 | 7600 | 7600 |

| DE_N | 0 | 261,000 | 54,100 |

| DE_S | 0 | 124,400 | 124,400 |

| PO_S | 0 | 0 | 20,000 |

| FI | 0 | 0 | 12,000 |

| UK_S | 0 | 0 | 18,800 |

| Region | 2030 [GWhheat/year] | 2040 [GWhheat/year] | 2050 [GWhheat/year] |

|---|---|---|---|

| DE_N | 6900 | 38,000 | 69,000 |

| DE_S | 17,000 | 93,000 | 170,000 |

| IE | 370 | 2000 | 3700 |

| UK_S | 11,000 | 61,000 | 110,000 |

| UK_N | 1100 | 6300 | 11,000 |

| Sector Coupling Strategy | Collaboration | No Collaboration |

|---|---|---|

| EV charging strategy | Optimized including V2G | Directly after each trip |

| Hydrogen storage | Rock cavern storages available | No hydrogen storage available |

| NG heat replacement | District heating supplied by CHP, EB, or HP | Individual heat pumps |

| Heat storages in DH | Tank, pit storages available | No heat storage available |

| Regions | Cost of H2 Flex (MEUR/year) | Savings from Reduced Electricity Price (MEUR/year) | Return of Investment |

|---|---|---|---|

| SE_N | 64 | 49 | 0.8 |

| SE_S | 44 | 37 | 0.9 |

| DE_N | 640 | 813 | 1.3 |

| DE_S | 1793 | 2350 | 1.3 |

| PO_S | 221 | 288 | 1.3 |

| FI | 120 | 103 | 0.9 |

| UK_S | 458 | 825 | 1.8 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Göransson, L.; Lehtveer, M.; Nyholm, E.; Taljegard, M.; Walter, V. The Benefit of Collaboration in the North European Electricity System Transition—System and Sector Perspectives. Energies 2019, 12, 4648. https://doi.org/10.3390/en12244648

Göransson L, Lehtveer M, Nyholm E, Taljegard M, Walter V. The Benefit of Collaboration in the North European Electricity System Transition—System and Sector Perspectives. Energies. 2019; 12(24):4648. https://doi.org/10.3390/en12244648

Chicago/Turabian StyleGöransson, Lisa, Mariliis Lehtveer, Emil Nyholm, Maria Taljegard, and Viktor Walter. 2019. "The Benefit of Collaboration in the North European Electricity System Transition—System and Sector Perspectives" Energies 12, no. 24: 4648. https://doi.org/10.3390/en12244648