1. Introduction

In recent decades, promotion policies have been developed and implemented in the field of renewable energies. In the case of wind power, these have been based on price-setting, the requirements of production quotas, the prioritized marketing system, and any possible tax allowances [

1], among other factors. Most countries share similar wind power objectives: reduction of fossil fuel consumption and of the sector’s environmental impact, an increase in the importance of renewable energies, and progress in methods to deal with a new type of development. However, the way they deal with these issues varies depending on a range of factors, e.g., social [

2], cultural, historical factors. [

3]. There are some studies which focus all their attention on these aspects of wind energy, or which offer data relevant to the consequences of developing the sector [

4], but they do not highlight the impact of how the sector is financed. The literature indicates that a single model of development has not been established worldwide, and that when models in Europe and further afield are compared [

5], neither a uniform approach nor any replicated elements can be identified [

6].

It is, however, worth highlighting the case of Denmark. At the height of the 1973 crisis, Denmark designed a more sustainable and less fossil fuel dependent model, adapted to the existing demand and using technological advances [

7]. All the agencies involved in the sector helped develop an integrated model, in which the owners of the wind farmland (i.e., members of the local community) were offered the chance to be shareholders in the farms, in addition to subsidies for production from 1979 to 1989, feed-in tariffs up to 1999 [

8], and reliance on local property protection to avoid any kind of speculation [

9]. It was copied by Holland, where the principal legislative achievement was the recognition of wind farm installation as an industrial use of land, thereby favoring a fairer remuneration for the landowners [

10]. In Germany, use was made of the feed-in tariff system, as well as enabling access to soft loans for technological firms in wind turbine production and the exhausting of land available for new wind farms [

11].

An ad hoc model of development and promotion for wind power would include the participation of all the variables and agents involved (in particular, all the landowners of the land) as well as potential shareholders and financial backers [

12]). In Spain, there is no such model. Instead, the business projects make small lease payments to local landowners. However, these payments are small in proportion to the high level of profits which the wind-promoting companies make (in Galicia, a wind farm is built on smallholdings belonging to several owners. The payments to be received vary according to the direct affectation, being more remunerated the land on which the aerogenerators are installed and not receiving any remuneration, the adjacent land on which the fences of the park perimeter are located. Therefore, the payments to be received are varied and reduced compared to the operating profits of wind activity. Furthermore, in Galicia and Spain, landowners cannot participate as shareholders in wind farms (as is the case in Denmark), thus reducing their income possibilities) [

13]. In contrast, if wind turbines were locally-owned, this would contribute to the economic development of the region [

14]. Wind power installations may attract people to work, visit or live in that community, with a subsequent impact on the local economy [

15]. Social acceptance also depends in part on the transparency of the administrative process, the extent to which the local inhabitants benefit, and, the valuation of the woodland where the farm is located. Such was the case in the Galicia region of Spain, where the evolution of the wind sector was characterized by a notably positive involvement by public administration. This meant that they did not choose an integrated set of rules which would have allowed all the agents involved to participate and represent their interests, as was done in other countries like Denmark, Holland or Germany [

16,

17].

Ownership of wind farms, determined by the final shareholders of the wind-promoter firms and the methods of financing (project finance) [

18,

19,

20], has been evolving from the financial project to the involvement of investment funds [

21]. Energy initiatives are capital intensive and have traditionally received direct foreign investment [

22] through bank loans and credits. In Spain, the sector never contemplated the participation of small investors, whether titleholder of the land to be used or not. This contrasted with Denmark and Japan, where small investors did participate. We therefore pay special attention to “Project Finance” [

19,

20]: the template for the promotion of wind farms in Galicia during the period 1995–2017.

The literature on investments in the wind sector has been primarily aimed at analyzing capital financing models. However, the study of the ownership structure of this capital does not receive the same attention, despite the fact that it is considered to have a significant impact at local level. For this reason, we consider that it would be necessary to deepen the knowledge of which companies or business or financial groups are present in this business. Our work allows us to advance in this knowledge, showing the links that these projects have with international business or financial groups and the degree of participation of local investors.

The main objective is to analyze the ownership of the capital that financed the installed wind farms in Galicia, based on “installed wind capacity” and which could even lead to comprehending (in a more in depth analysis and with other study variables) the interaction of these financial power networks with political parties, governments and other institutions. The aim was to detect relationships among the different matrix companies so as to understand the presence of certain international business groups, which bring together economic, financial and energy interests (among others), and that were found in the end to be the owners of wind farms in Galicia. Therefore, due to their involvement in these farms, they were the reported beneficiaries. Within Spain, Galicia was the autonomous community which registered the biggest advance in terms of power.

The novelty of this research lies in the knowledge of the real ownership structure of wind farms through the application of Domhoff’s power structure analysis to the wind business network of a region, allowing an approach to the ownership and decision making relationships that underlie the nominal ownership of the wind farm

This period was chosen because it was in 1995 that this sector became operational in Galicia. Its evolution, based on installed wind power, will be analyzed by using official final data updated to 2017. The results of this study indicate that the approach taken to wind farm development favored ownership of the relevant business concerns by a small number of foreign companies, but did not consider the involvement of small local investors.

This paper is organized as follows:

Section 2 presents the literature review and

Section 3 presents the methodology and characteristics of the case study;

Section 4 analyses the development of wind energy in Galicia and the wind power assigned to each business concern;

Section 5 discusses the results obtained from the network of firms that own the installed wind power, and, finally,

Section 6 shows the main conclusions and implications for policy-makers.

2. Literature Review

There is an extensive bibliography on factors related to the installation of wind farms: socioeconomic, environmental, energy, cultural, territorial, political, technical and technological. The importance of each factor may vary in different regions and contexts (the citizens of a country may not share the acceptance and proactive attitude of their government towards wind energy development in their territory) [

23,

24,

25,

26]. For this study, the shareholder knowledge of wind farms is the most important. The literature review does not provide conclusive results regarding the characteristics of wind farm investment, or of the sector’s relationship with the owners of the financing capital. However, it refers to the participation of public administrations and local investors as shareholders in wind farms, and the financing from the banking sector. Several authors relate the participation of governments and/or local companies in the ownership of a wind farm with the existence of more favorable impacts on the local environment, highlighting the level of social acceptance. Thus, Devine-Wright et al. [

27] indicate that the implementation of wind farms causes impacts in at least three dimensions (markets, socio-political and community). Krug and Ohlhorst [

23] suggest that environmental factors play a significant role as acceptance factors, but economic factors, distributional injustice and poor public involvement and participation are even more important [

24]. The level of local ownership of wind farms, and the generation of benefits and income in the local area are analyzed by Wang and Wang [

25] which also highlights the importance of the transparency of the administrative process by the involvement by public administration with an integrated regulatory framework.

The manner in which local or national government participates in the ownership of wind farms can also have a positive effect on public acceptance [

28,

29,

30,

31,

32] or opposition [

33]. There can be a lack of social acceptance if government agencies do not involve communities in wind power development with the regulatory framework that authorizes wind farms. Devine-Wright [

28] argues that community attitudes may be favorably affected by ownership models characterized by some form of public participation in wind farms. Boon and Dieperink [

29] define an integrated model to explain the development of local renewable energy organizations in The Netherlands (Figure 2, page 310) showing the effect of regulatory framework and the division of ownership and the direct involvement of locals, among other elements. This is what not happened in the Galician region [

34] due to the characteristics of the planning model (privileged projects) applied by the Galician government, a non-integral model where all the agents involved were not represented. The authors describe the complex wind development model applied in Galicia, forming part of the regional energy policy carried out, in which the participation of the local community has not been considered. The regulatory framework is related to the sources of income associated with wind power generation (taxes and revenues, and municipal ownership), too [

35]. Copena et al. [

35] and Liebe et al. [

36], indicate that economic benefits are strongly linked to the local acceptance of wind farm projects, in particular, the positive relationship between local ownership of wind farms and local acceptance.

The degree of “local ownership” is also emphasized by Liebe et al. [

36], who affirm that a farm is accepted much more when there is local participation in the ownership of the wind farm rather than exclusive ownership by a foreign investor. The authors investigated people’s attitudes towards wind power in Germany and Poland, using key variables such as type of ownership, degree of local participation in the planning process, distribution of turbines across regions, and the motivation for developing wind power. Leiren et al. [

26] (to highlight the information in Table 2 on page 6) identified the key factors in acceptance-related patterns of wind energy development, emphasizing the degree of local ownership of the wind farms of the impacts on economy: local community stakeholders enjoy “higher levels of trust than commercial developers, which are not usually embedded locally” (page 18) and help to generate local added value and “contribute to a more democratic energy system and social economic development”(page 18). Regueiro and Doldán [

37] explain that the participation of all the agents involved and landowners or small investors as shareholders are some of the key factors in policy developing wind energy in Europe. If local investors participated in the ownership of a wind farm, it would bring the local community closer to the benefits derived from the wind energy production [

38]. It would also result in a more equitable distribution of benefits and a greater influence on the development of the windfarm [

39]. Other important factors include the number and geographical location of the wind turbines (due to their negative externalities). Linnerud et al. [

33] stress that a change in ownership has a significant negative effect on their attitudes toward the project.

An issue of particular importance is how local citizens perceive their relationship with shareholder groups, since this will affect the social acceptance of wind energy (ibid). In this regard, the distribution of costs and benefits among all the agents involved is presented as a critical factor, since the smaller the group of beneficiaries (investors) and the broader the group that has to bear the negative impacts of a wind farm, the lower the social acceptance [

23]. These authors also report that in local renewable energy projects, community acceptance is greater if investors contribute to the creation of local benefits, and even more if there is community (co-) ownership and citizen energy companies. In Spain, the financing of wind farm construction has, mainly, followed the model of “Project Finance”, with bank loans or credits for the promoting companies [

40]. The applicable law did not permit the participation of small investors, (be they the landowners of the land or not) in contrast to the system used in Denmark, Japan and Germany, amongst other countries. Renewable projects have also been funded, at least in part, by international financial institutions. For example, during the period 2005–2011, The European Investment Bank gave 1.4 billion Euros to offshore wind power in the United Kingdom, 883 million to Germany, 750 million to Belgium and 240 million to Denmark [

41].

Finance from the banking sector has been one of the driving forces behind advances in the Spanish energy sector [

42]. The influence and power of the big energy companies enables them to centralize capital while controlling a large part of industrial investment and links with other sectors (construction companies and banks) (ibid) [

43,

44]. The leading role that the banks have taken in industrial and commercial expansion has been examined in several studies, for instance, in an analysis of the business network in America [

45]. This analysis found that the presiding power was obtained by the participation of financial institutions in other corporations. This was because, firstly, it was perfectly in line with the companies established procedures [

46] or secondly, it was obtained to enable a credit cash flow [

47]. This same behavior was also studied in relation to the United Kingdom, the United States and Japan during the 1970s [

48]. What was found was that the most important companies were not controlled by just one shareholder, but rather by a system of interpersonal and inter-corporation participation. One other point that stood out in this system was the link between elite businesses and the political class, a connection which influences the structure of the legal framework applied, and can also determine investment and distribution of capital in an economy [

49,

50,

51].

When it is known where the capital for any investment comes from, it will be possible to identify pyramid structures that are used to concentrate power in the hands of a few [

52,

53], enabling them to organize activities on the basis of favors and personal connections [

54]. Moreover, the small number of business owners and a non-integrated legal system (which does not represent the interests of all the participating agents) are factors which increase the importance of personal/corporative networks, where the leaders are the dominant shareholders [

55,

56]. What underlies this situation is the idea of financial capital being the symbolic relationship between “money capital” and “industrial capital”, a relationship which explains this new power structure [

44].

Although it is not the focus of this study, it is necessary to mention here the Spanish accounting regulations, which, in relation to interconnected companies are based on the General Plan of Accountancy. This encompasses the provisions of the European Parliament Directive of 2013/34/UE, and that of the Council of 26th June 2013 [

57], which relate to the current financial state of the firms, consolidated financial states and reports on other types of firms. The aim of these regulations is to enable cross-border investment and improve methods of comparing different financial systems. They also include reports on issues such as public confidence in the accuracy and coherence of information. For example, a distinction is made between matrix companies (which control one or several companies), subsidiaries (which are controlled by the matrix company), groups (the matrix company and all of its subsidiaries), linked companies (two or more inter-connected companies within a group), and associated companies (in which one firm influences the running of another).

3. Research Design and Case Study

The empirical study of capital ownership structure is based on Domhoff’s membership network analysis, [

58,

59,

60,

61,

62] identifying membership in networks which begins with a search for connections among the organizations that are thought to constitute the dominant group. After that, it is necessary to study other types of links such as kinship ties or flows of information between organizations (one of the most important of these types of links is about the size and direction of money flows in the network). The approach provided by this methodology is entirely feasible for the objectives sought, by allowing an understanding of the relationship between the investments made at the regional level with the power networks that own that capital, which act globally and which could even lead to comprehending (in a more in depth analysis and with other study variables) the interaction of these financial power networks with political parties, governments and other institutions. However, this methodology has limitations, based on its instrumentalism by not extending knowledge of the structural relations within the capitalist society and with State interaction, or not being useful for studying the distribution of wealth and income.

The publicly data was facilitated by the Government of Galicia [

63].

In order to understand the information, it is necessary to distinguish between a company owner and a concern that is a dominant owner. For our purposes, we denominate company owner as the firm responsible for running a particular wind farm (the industrial operation), whereas a dominant owner is an enterprise or an individual shareholder that holds shares in that farm.

To evaluate the ownership of wind projects and the relationships among the dominant owners, an analytical approach was used, based on five consecutive and interdependent phases (

Table 1):

Phase 1: Summary of all wind farms installed in Galicia during the period analyzed, based on data from the Official Bulletin of Galicia and the Register of wind farms. Together with this is an analysis of the regulations, aimed at determining the possible legal, economic and financial factors which the farms must consider.

Phase 2: Restructuring of the information on the list of wind farms installed in Galicia (1995–2010), creating a new list, in which the number and name of assigned wind farms and their total wind power are given for each promoting company (wind farm owner).

In order to compile this approximation, the starting point is the relationships among authorized wind farms in Galicia from 1995 to 2017, as published by INEGA. The analysis indicates the following variables: name of the wind farm, promoting firm, date of authorization, power declared to the relevant authority (in kW), and the municipality where the farm is located.

Phase 3: Hand-collected data on ownership structure for the companies analyzed for the period under scrutiny, from the SABI (Sistema de Análisis de Balances Ibéricos) Database [

64] and from the Spanish Securities Exchange Commission (Comisión Nacional de la Competencia (CNMV)) [

65]. These sources also facilitated identification of the principal concerns that were shareholders, using the list of wind farm promoters in Galicia (grouped according to assigned power). In addition, it also shows any overlaps among them or if some companies were involved in more than one venture. The corporative and financial information contained in this database comes from the balance sheets submitted by companies in the Commercial Registries. This database is a web tool that offers both general and company information relevant to more than 2.5 million Spanish and 800,000 Portuguese businesses. It is particularly useful because it is one of the few sources which contains economic and financial information relevant to the developer companies that promote the given wind farms. It is the most comprehensive source of corporate, economic, financial and employment information on companies.

Phase 4: The fact that some promoter companies appear two or more times indicates that there are links between the members of the promoter firms. This pattern of concurrent ownership suggests that there are corporate links among the promoting firms. Our analysis is represented here in a matrix (

Table 2).

The information in the matrix and

Table 1 allows us to create the first network of linked companies, showing to which business groups they belong. As Domhoff [

63] indicated, it can be seen that there are investors who act as “the center”, in that they participate in several promoter companies (SH2), while other investors only have one investment (SH20).

Using these findings, it is possible to observe the presence of certain business groups and shareholders (grouped according to total power in their wind farms), who are, definitively, the owners of the wind farms located in Galicia. We should, therefore, attribute any profits or losses to them.

Phase 5: Once the principal shareholders have been identified, the same process can be used for them in order to reveal the dominant owners and ultimate shareholders who are the real beneficiaries of Galician wind (be they sole traders, companies, investment funds or insurance companies). This knowledge facilitates the creation of the network of shareholders who own installed wind power in Galicia.

The analysis of business links was studied in-depth through the composition of their social capital. The aim was to detect relationships among the different matrix companies so as to understand the presence of certain international business groups, which bring together economic, financial and energy interests (among others), and that were found in the end to be the owners of wind farms in Galicia. Therefore, due to their involvement in these farms, they were the reported beneficiaries. Based on these considerations and the data obtained, a network of wind farm-owners in Galicia was established, and this is the source of a graphical representation of the relationships among the matrix companies that participate in the wind business.

The connections arose from a business group investing in other companies, subsidiaries or not, but, in any case, having the existence of the initial investment of this business group in common.

Case Study: The Region of Galicia

Worldwide wind power has developed considerably, enabling growth in the contribution that renewable sources make to meeting energy needs.

The latest data published by the International Renewable Energy Agency (IRENA) [

66] and the World Wind Energy Association (WWEA) [

67] for the year 2018 confirms the strength of the wind sector in these times of crisis (4780 MW in 1995; 180,852 MW in 2010 and 563,659 MW in 2018), and demonstrates a clear advance in this source of energy in many parts of the world, particularly Asia (40% of installed capacity), Europe (32%) and North America (20%). China was the world leader in accumulated wind power installed (32.8% of the world total), followed by the United States (16.7%), Germany (10.5%), India (6.3%), Spain (4.2%) and the U.K. (3.9%) (

Figure 1). This panorama can partly be explained by growth in recent years, especially in the countries which lead production.

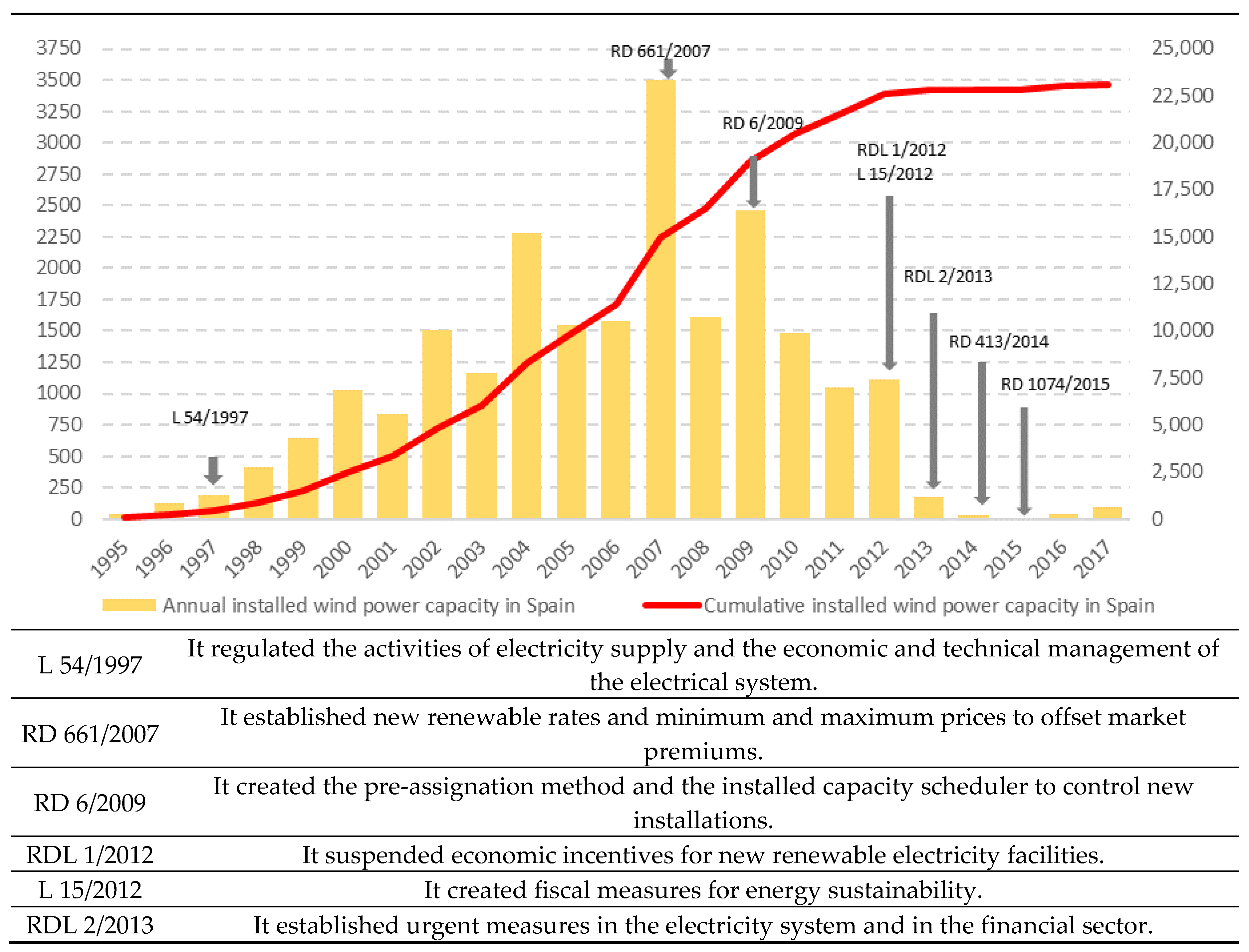

The advance of wind power in Spain was accompanied by a proliferation of regulations. These regulations enabled progress in the 2000s, but they did not prevent the slowing-down of development from 2011 onwards, which was caused by the shock measures adopted to confront the systemic crisis: support for renewable energies was paralyzed by the end of subsidies, the failure to promote wind power, and the difficulty for financial institutions to support this type of initiative (in particular due to the regulations approved in 2012 and 2013).

In Spain, there is a broad regulatory framework for the energy sector, with state and regional regulations that do not always coincide.

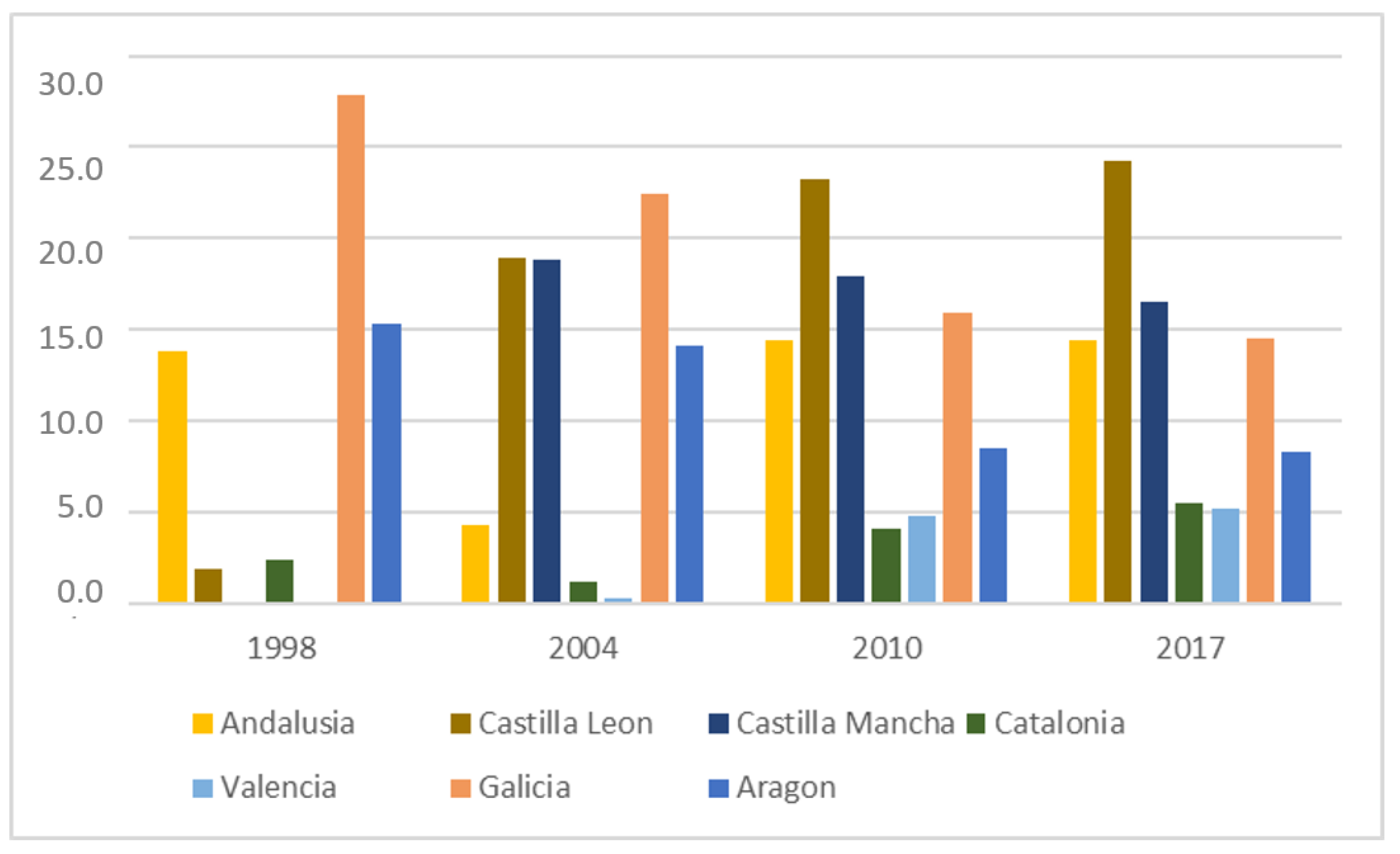

Figure 2 shows the main regulations affecting the wind energy sector in Spain. Until 2009, there was a notable advance in wind power, although a comprehensive wind power promotion model was not implemented. The diversity of regulations, the availability of wind resources and the technology employed in each region (Rodriguez, Regueiro and Doldán, 2020) [

68], lead to a different evolution by region for the same period of time (

Figure 3).

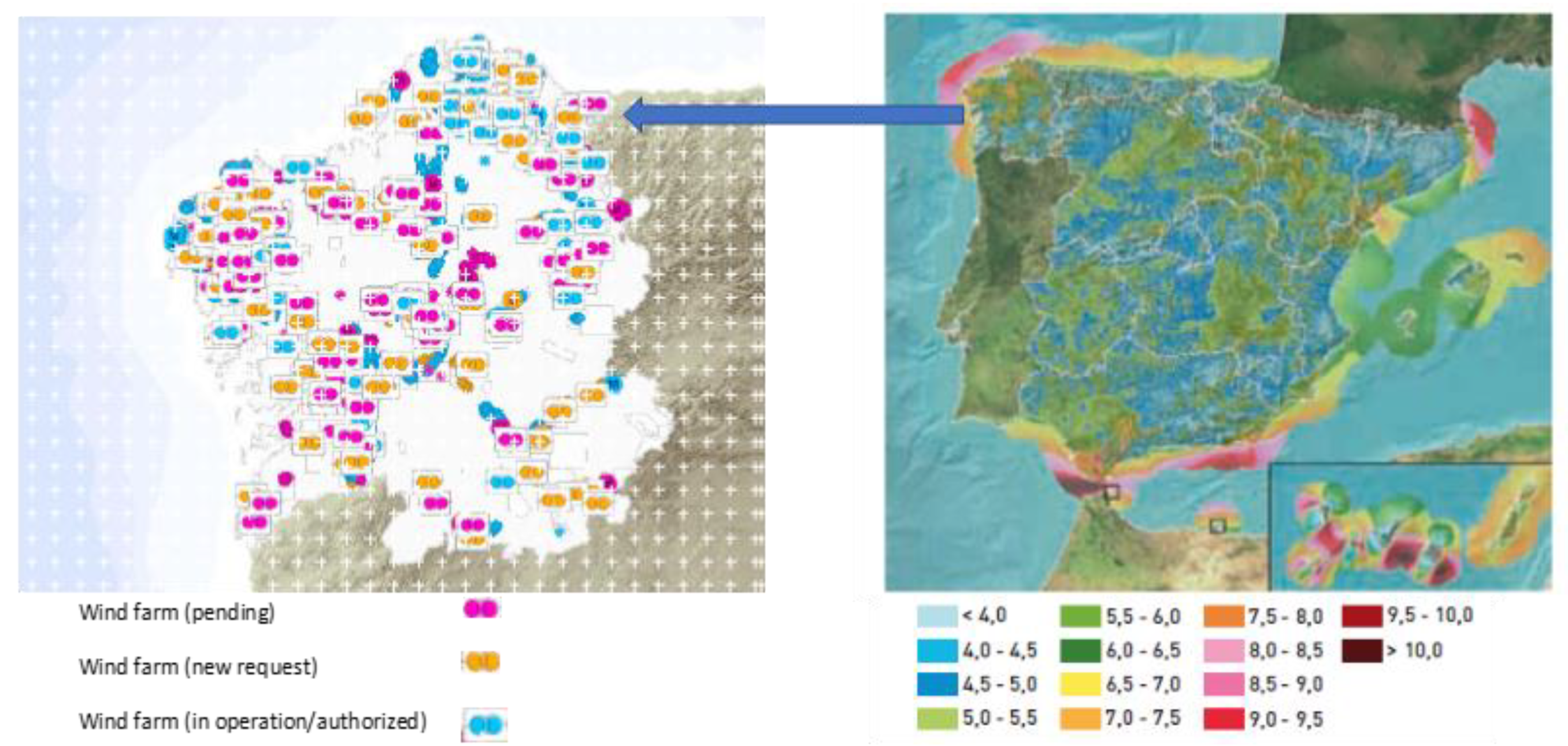

The complexity of the energy system, and also of the electricity mix (covered by much legislation but lacking integrated wind policy), with regions that had very good wind records for commercial exploitation (

Figure 4) led to an unequal growth of wind promotion in Spain, which was organized on a regional basis (

Figure 3).

4. Galician Wind Development (1995–2017): Principal Results of the Analysis

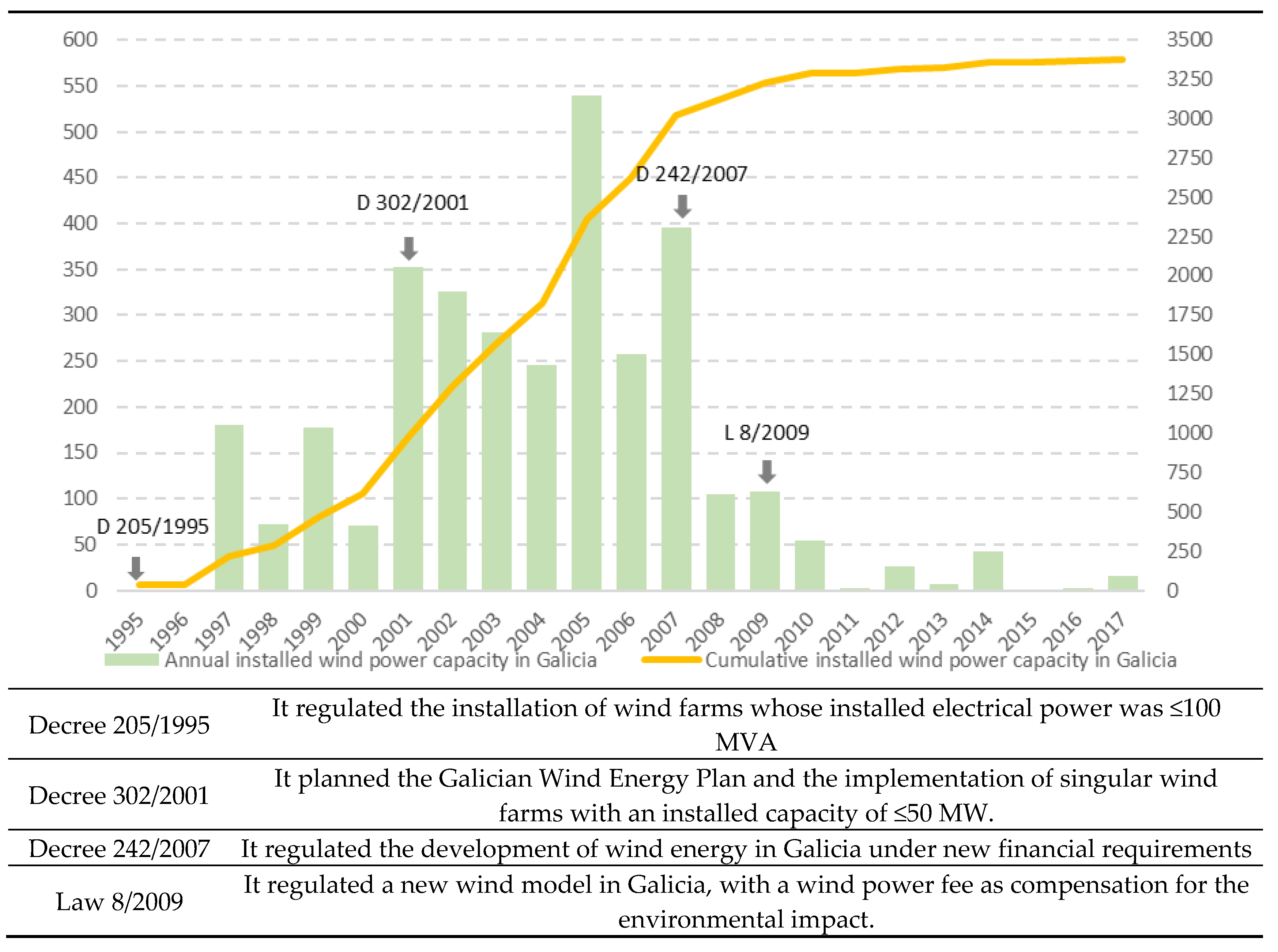

In Galicia, three decrees and a law were passed during the period of this study (

Figure 5), with notable differences regarding the hub of activity among wind promoters. Decrees 205/1005 and 302/2001 established demonstrating the feasibility of the industrial technology plan and development forecasts; expected investments and implementation time; the technological and financial capacity of the developer; the industrial, socio-economic, technological and environmental contributions and effects of the plan and developments linked to affected land and municipalities [

63,

68].

Decree 242/2007 and Law 8/2009 [

63,

68] indicated that applicants must prove legal, technical and economic capacity to carry out the project, so that technical capacity would be accredited by one of the following requirements (having carried out the activity of electricity production during, at least the last three years, or having a partner who participates in the share capital with a percentage equal to or greater than 25 per 100 and who can prove his experience during the last three years in the activity of electricity production, or have signed a technical assistance contract for a period of three years with a company that proves they have experience in the activity of electric power production). Economic capacity would be demonstrated if the developer submitted documentation proving the ownership of funds involving at least 20% of the investment required for the realization of the project or projects, establishing that the projects submitted by companies demonstrating greater technical and financial capacity for the material setting up of the wind farm [

63,

68].

An analysis of official figures from the Galician government has confirmed that 153 wind farms were installed in Galicia during the period 1997–2017.

This represents a total of 3,321,245 kW of installed power, as shown below in

Table 3:

The sample used in this study is made up of 134 wind farms operating in Galicia, and the companies who own them. Neither small scale wind farms (municipal or belonging to firms) or experimental wind farms, were taken into consideration. In the case of smaller scale wind farms, this is because they have limited installed power (less than 50 kw) and belong to either a company or a council.

The identification of the main shareholders of the companies promoting the 134 wind farms made it possible to draw up a classification, considering two variables: the type of company (energy groups and/or investment funds, or regional energy companies, from other sectors and mixed companies) and the wind power that belonged to them. This analysis of wind farm owners was carried out using SABI, and it shows that there are corporate links between the companies, resulting in ownership being concentrated in a smaller number of shareholders than would superficially appear (

Table 4):

This analysis of wind farm owners was carried out using SABI, and it shows that there are corporate links between the companies, resulting in ownership being concentrated in a smaller number of shareholders than would superficially appear. The information facilitated by the CNMV [

69], which was up to date as at the end of 2017, demonstrated previously unclear links between enterprises, or, in any case, links that could not be determined from the information given by SABI [

68]. This was the case for economic and financial reports of the wind farm owning companies which were indicated in the list mentioned earlier (

Table 5):

The analysis of the information gathered in

Table 5 establishes that from 1995 to 2017, ownership of authorized wind farms in Galicia was in the hands of multinational business groups. The capital is predominantly Spanish and foreign, although there is a minority of Galician capital from local companies.

5. Discussion: From Small Local Businesses to the Predominance of Foreign Investment Funds

The initial classification of companies owning wind farms in Galicia (

Table 4) shows that that there are two types of owner depending on the installed wind capacity: firstly, energy groups and/or investment funds, who occupy the main positions in the ranking; and secondly, regional energy companies, from other sectors and mixed companies which includes energy companies dedicated to other activities, or to a mixture of energy and other types of ventures.

It should be noted that in the regional energy group the companies Norvento, Adelanta and Fergo Galicia Vento occupy the top positions in this category, surpassing in value Eon and Canepa Energy Luxemburg, which are in the final positions of the first group. The analysis displays the following characteristics:

A. Energy groups and/or investment funds.

This type of company owns 88% of installed wind power in Galicia. The composition of this group is heterogeneous.

The companies Acciona, Iberdrola, Enel, Endesa, Edp and Naturgy, stand out in this list. Naturgy, Endesa and Iberdrola also operate in other markets, and it is important to realize that two companies, Endesa (connected to EnelSpa) and Iberdrola, represent nearly 70% of the Spanish electricity market. This situation seems to hide a policy of intense involvement in wind resources in Galicia, like the situation in the hydroelectric sector, as described by Beiras [

74]. It is also possible to think of a vertical integration that could also entail implementing a series of measures such as asymmetric information, creating obstacles for companies trying to enter the market, due to its economic, financial and interest capacity. In light of these facts, it could be surmised that the companies cooperate in organizing the industry, although this is difficult to prove. On the same basis, we can establish the origin of this cooperation in Endesa during its process of constitution.

E.on and Enerfin (which are part of the matrix company Elecnor), who have relevant experience in Spain as well as an international presence.

FCC (Fomento de Construcciones y Contratas) a multinational construction company (domiciled in Spain), which has diversified its activities and has a noticeable presence in the renewables sector.

Canepa Green Energy Luxembourg and Hopefield Investments, both of which are investment funds linked to the ownership of a wind farm.

B. Regional energy companies, from other sectors and mixed companies.

This group own 12% of installed wind power in Galicia, and like the first group, its composition is heterogeneous:

Energy companies such as Norvento, Adelanta and Engasa, who have mainly developed their business at a regional level.

Companies connected to business groups that are principally involved in other activities. Examples of such companies are: Jealsa (canned fish), Gestamp (automotive services), Fergo Galicia (excavation and construction), Epifanio Campo-Rodonita.

Mixed companies, financed by public and private capital, examples being: Sotavento, Somozas Council-Cobra, Hidroeléctrica del Arnoya.

Smaller scale electricity production companies, or regional investment firms, for instance: Okechobee Energías, Vento Continuo Galego, Sergio Farina and Patricia Gómez.

This ownership structure of the wind business in Galicia could be considered a sample of the strategic role of the energy sector in Spain, given that, control an important part of the whole economic system, and because the energy groups are large units of decision and economic power, running the process of centralizing capital [

43,

74]. Thus, Acciona and FCC are business groups with diversified activities, including construction and service companies, among other sectors. This means that the energy/construction link does not appear strange in this panorama, but rather a consequence of the system itself, which allows the combination of diverse activities, in the same business group, intensive in capital, energy consumption and complementary activities. It would represent the power of the big energy companies. In the case of the regional companies, this situation is practically testimonial, with the examples of Fergo Galicia Vento and Epifanio Campo.

This result contrasts with what Brown et al. [

14] indicated, so that if the owners are not locally-owned companies, this would not contribute to the economic development of the region, and the impact on the local economy would be more reduced [

15]. Furthermore, this situation could be favored by the lack of a regulatory framework supporting the participation of other types of shareholders (individual shareholders, cooperatives), which did exist in other European countries [

16,

17,

34,

35].

The results also show the dominance of project finance as a method of financing wind farms, in which the presence of financial institutions and investment funds was common practice [

18,

20,

21], due to the intensive use of capital in the energy sector. In Galicia, the financial sector has also been a determining factor in the advancement of the removable energy sector, as has happened in Spain [

42].

The matrix of the results identifies the dominant owners of Galician wind development and their origin (

Table 5):

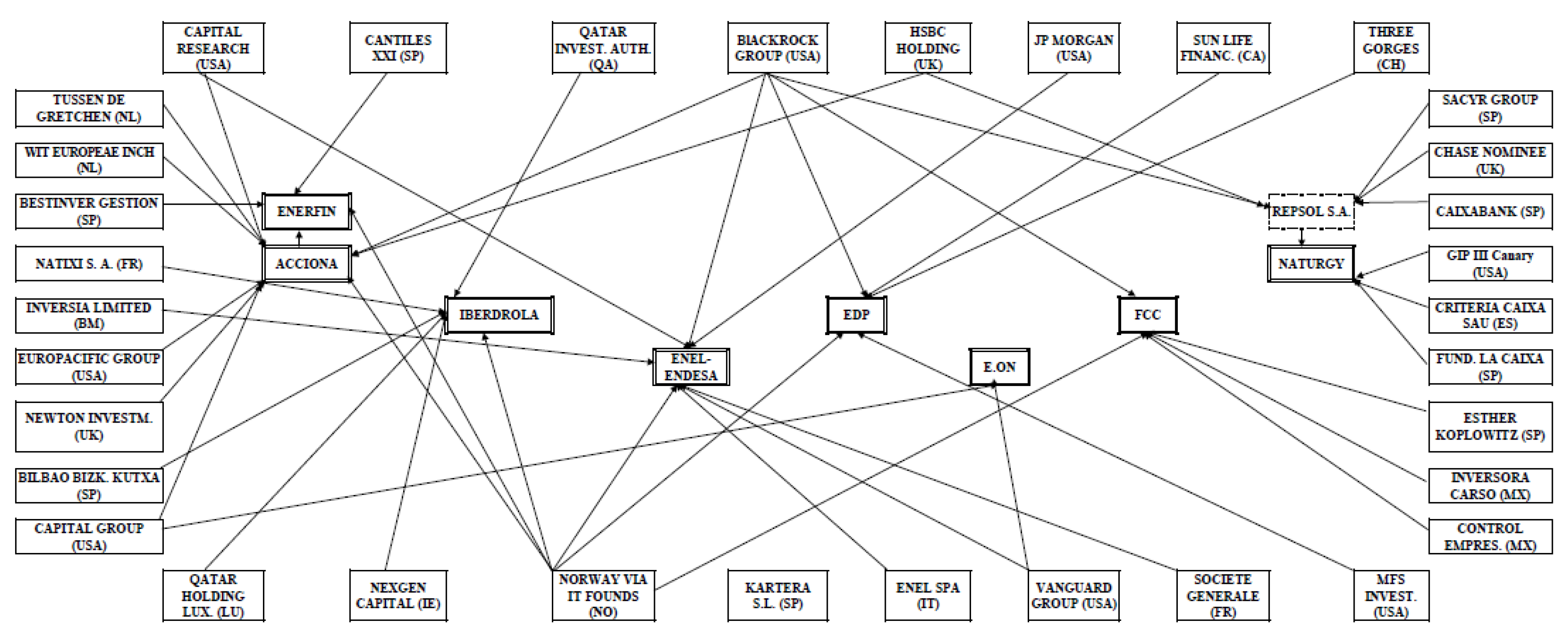

Acciona is a wind farm-owning concern and a dominant owner, among other reasons because other firms such as Enerfin participate., and this connection, and the possible status of Acciona as an interest group, can be seen. However, Witgroup owns 27% of Acciona.

Naturgy has the energy group Repsol S.A. for one of their principal shareholders. In turn, Repsol’s principal shareholders are: CaixaBank (Spain), Sacyr Group (Spain), Chase Nominee (UK) and Blackrock Group (USA). Both Naturgy and Repsol are considered interest groups.

Hopefield Investments and Canepa Green Energy are isolated models of ownership, according to Domholf (2012). They each finance only one company and are therefore not included in the definitive matrix or in the network.

In Norway, Vanguard Group and Blackrock Group act as “ownership reference centres” and they are principal dominant owners, given that they are shareholders in many companies.

It can be seen that energy groups (for example, Iberdrola, Enel Endesa and EDP) are linked, since they have principal shareholders in common (Blackrock Group) or Acciona and Enel Spa (Capital Research). The major financial and investment groups are the owners of the energy groups, and the three entities go forward in the same direction. The Acciona group is linked to, and participates with, foreign energy groups, and this also determines the business policy that is followed. The same is true of Iberdrola, EDP and Gas Natural (

Figure 6). Thus, this network of dominant owners obtained through the Domhoff’s membership network analysis, [

58,

59], allows to have an approach to know where the capital for any investment comes from, and a preliminary identification of the power structure that runs it [

52,

53]. It would be characterized by the small number of business owners and a non-integrated legal system, which has not allowed the participation of other types of shareholders, favoring the interests of corporative networks [

44,

55,

56]. Our results are compatible with the findings of Leiren et al. [

26] because the analysis of the available information clearly shows a model in which the promoting companies are extremely active in wind power. The result is that ownership of authorized wind farms in Galicia is, mainly, in the hands of multinational business groups, who are involved in energy, banking and diverse investments. The greater part of the benefits do not stay in Galicia, because this activity normally generates financial benefits, which can ultimately be attributed to the business groups who are the real investors in the wind farms. As behind these business groups lie the interests of the big investment or international investment groups, these discoveries lead to a fuller understanding of the leadership situation. Furthermore, because if local communities have a certain degree of ownership, the levels of trust and the local added value will be higher and will create benefits at the local level [

36]. It is clear that in Galicia, the period 1995 to 2017 can be characterized as a time of intense activity related to the resource “wind” fostered by the characteristics of the regulatory framework and the planning model decided by the Galician Government activity carried out by investment groups, businesses, and/or transnational energy companies, stating that “the coalitions or special interest groups that are relatively privileged in terms of social, human and/or financial capital are more capable of influencing and shaping the results of the planning process than the less organized local groups” (Simón et al. [

34] p. 10). These operations conditioned the expansion policy of the sector’s small firms, which are mainly funded by Galician capital. It was, furthermore, carried out in a permissive institutional framework and an incomplete model of support for the sector, which did not represent the interests of all those involved, but rather prioritized business interests before those of the region [

75]. The maps of Spanish electric power and of wind energy companies in Galicia are connected, as indicated by Liebe et al. [

36]. Above all, it is essential to highlight the fact that 55% of installed wind power in Galicia is in the hands of four large energy groups (Acciona, Ibedrola, Enel-Endesa and Naturgy), which also have business links outside Spain. It is, therefore, these companies who funnel the benefits of wind power operations in Galicia. A less local involvement in wind farm ownership, a lesser degree of “local ownership” could mean less social acceptance, being also related to the level of information opacity on the part of the operating companies and energy groups [

37].

6. Conclusions and Policy Implications

This study appears to be the first time that an analytical approach has been taken to examine the impact of the economic development of wind farms in Spanish regions, and the results have clear implications for policy makers. In response to the planned objective, it helps to make up for the lack of information on the characterization of wind farm investors, by going beyond the analysis of nominal ownership and establishing, through the methodology used, the relationship that exists with the large Spanish and international business and financial groups. In this way, the network of interests that links local resources and capital with international capital is revealed.

The dominant owner structure obtained leads to the conclusion that the real owners are the heterogeneous group formed by the energy groups and/or investment funds, because they own 88% of installed wind power in Galicia, and the energy companies, involved in other activities or a mixture of ventures, own 12% of installed wind power in Galicia, and like the first group, its composition is heterogeneous, too.

We can therefore say that wind power in Galicia is in the hands of international investment funds (Tussen de Grechten B.V. and Wit Europeae Inch from the Netherlands; Capital Research, Blackrock Group, Capital Group Co., Europacific Group and others from the USA; Qatar Investment Authority and Qatar Holding from Luxembourg; Norway via it founds and Three Gorges from China; and many others. Serían los receptors de los beneficios generados por esta actividad. They would be the recipients of the profits generated by this activity.

It could be concluded that the ownership of wind energy farms can represent a strong influencing factor over communities and policy makers. The majority presence of foreign investors, who lead processes of capital concentration, has been favored by a regulatory framework that has not allowed the participation of other types of agents as investors/shareholders (land owners, farmers, individuals).

The results obtained allow a better understanding of the existing relations between the agents involved in wind development, indicating ways which could facilitate a greater acceptance of wind projects by local agents, as warned by various authors mentioned in the literature review. The public administrations involved could act politically to encourage this relationship. In this sense, and considering the experiences developed in other countries, it would be interesting to revise the regulations to facilitate the participation of all the agents involved. Another regulatory possibility is to promote the visibility of the social benefits of the development of the wind sector, with formulas which allow at least part of the business profits to be reinvested in the communities close to the locations where the wind farms are installed, especially if there is no direct participation by local agents. Furthermore, in light of the results obtained, it would be worthwhile for both the Spanish and regional governments to reflect on the way in which wind energy is promoted, which leads to the concentration of ownership of the exploitation of a natural resource in the hands of a small group of real owners, a large part of whom are foreigners, but leaves out most of the local agents where this resource is located.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}