Business Model Canvas and Energy Enterprises

Institute of Public Affairs, Jagiellonian University, 30-348 Kraków, Poland

*

Author to whom correspondence should be addressed.

Energies 2021, 14(21), 7198; https://doi.org/10.3390/en14217198

Submission received: 4 October 2021

/

Revised: 26 October 2021

/

Accepted: 27 October 2021

/

Published: 2 November 2021

(This article belongs to the Special Issue Impact of Sustainable Financial and Economic Development on Greenhouse Gas Emission)

Abstract

:So far, little is known about the Business Model Canvas development in the energy sector. In this paper, we fill this knowledge gap and modify the Business Model Canvas. Based on the cause–effect analysis combined with the literature searching method, we suggest that Osterwalder’s Canvas for energy enterprise should be modified because the available Canvas adaptations cannot fully capture the energy enterprise’s business model or realise its business operations combined with the public interest. We propose a new original Canvas adaptation by adding two crucial blocks representing the mission, energy accountability, and impact on stakeholders in the Business Model Canvas. The findings make two main contributions. First, they contribute to developing entrepreneurship theory. We formulate an original definition of a business model, first showing the limitations of current definitions. We verify Chesbrough’s functions of business models. Second, compared to earlier business model frameworks, the new model clearly points out that accountability in firms’ everyday businesses is at the core of business development. Moreover, this article formulates future research avenues in the energy sector and provides a helpful planning tool for practitioners.

1. Introduction

No doubt, one of the critical industries in today’s economy is the energy industry, which enables energy production, consumption, and economic growth [1,2,3]. Although there are many studies of business model usage by different firms, e.g., [4,5,6,7], little is known about how the Business Model Canvas can be used by energy firms [8]. Therefore, against the background of mounting research on the Business Model Canvas, this paper presents the findings of an analysis of the existing Business Model Canvas and its adoption to energy sector requirements.

Energy firms operate under specific legal requirements that are different from the requirements of traditional businesses focusing on profit and expanding business advantage. The analysis of the Energy Law and energy firms’ tasks led to the following research question, which may eliminate the identified research gap: Does the current Business Model Canvas consider the specificity of energy companies?

The following hypothesis is proposed: the business operations of energy firms are affected by the necessity of ensuring State energy security, and thus a modification of Osterwalder’s Business Model Canvas is required.

This article explains why the traditional Business Model Canvas cannot be perceived as an energy firms’ universal method.

The structure of this article is as follows: firstly, the paper proceeds to discuss the Business Model Canvas assumptions used contemporarily by enterprises; next, we provide evidence that the current Canvas is not universal and modify it; finally, we formulate a conclusion and point out avenues of further research.

2. The Literature Review

The Business Model Concept

Many research works dealing with business models exist in the literature. Business models became an issue of particular interest in the last 10 years of the 20th century [9,10,11,12,13,14,15,16,17,18,19,20]. Scholars seek the theoretical foundation of business models in the transaction cost economics and capital budgeting literature. Examples include Schumpeter’s theory of innovation, Porter’s value chain framework, and the resource-based view of the firm [4,9,10,19]. Authors underline the business model linkages to managerial cognition [16]. Based on the literature review [4,5,6,7,12,13,14,15], it is possible to show the three major classes of the definition of business models that fit the energy sector:

- Economic: The models focus on profit generation through revenue streams and cost structures.

- Operational: The models focus on the configurations of different business activities.

- Strategic: The models determine the position of a firm in its environment.

As an example, Apple has shown the business model’s importance in business success. One may agree with Zott and Amit ([18], p. 216) that a firm’s business model can be perceived as “a system of interdependent activities that transcends the focal firm and spans its boundaries”. Teece underlines that a business model shows management’s assumptions about customers’ needs and expectations and how a company can meet these needs best and receive expected profit [17]. One may generalise following Baden-Fuller and Morgan that the business model reflects how a firm creates and profitably distributes value, or that a business model visualises the organisational and financial structures of a business [19,20].

Osterwalder and others conclude that a business model is a concept showing a set of items, terms, and relationships to express a specific firm’s business logic. They stated that business models are about how a firm works, creates value, and communicates with customers [4,21]. We underline the necessity of understanding the business environment much more broadly and not limiting it to the customers. Following the Hatch concept of the business environment [22], one may generalise that a model is not limited to clients. It also includes suppliers, co-operators, and competitors, as well as other stakeholders. Therefore, based on the conceptual analysis, we formulated the following definition of a business model: it presents how a business works, what kind of business value is provided, and how this is accountable and presented to the firm’s stakeholders.

Regardless of the classification of business models, they have some primary purposes. Chesbrough and Rosenbloom understand a business model as a tool that allows one to capture a solution that can be commercialised [23]. Zott, Amit, and Massa perceive a business model as connecting innovative technology and customers [7]. We think that the business model reduces uncertainty through the visualisation of business assumptions and their potential effects. This is accomplished through the following functions of the business model: information, prevention, standardisation, and education.

The model includes data helping in the preparation of investors’ decisions. The preventive function manifests itself in identifying threats to achieving goals and tasks and preparing measures to mitigate business risks. The standardisation function is combined with the educational one and consists of developing mechanisms that facilitate decision-making and the implementation of tasks. Chesbrough point outs the following functions: the business model shows the firm’s value and explains why customers value the firm’s products and services; it identifies the strengths and weaknesses of a firm and its competitors; it determines the firm’s value chain structure required to create and distribute its products and defines assets needed to realise its goals and tasks; and it determines the revenue stream mechanism for the firm and the cost of the firm’s operation [24].

We think that the business model also enables risk management, especially risk mitigation, to accomplish all scheduled tasks without any obstacles. Business models have elements that enable one to understand what the firm will do and how planned tasks will be financed [4,7,21]. Thus, one may generalise that the business model covers all financial and non-financial aspects, including those related to the enterprise’s network architecture and environment.

The business model serves practice [20] and offers decision-makers a coherent way to visualise their options in fast-moving and unpredictable environments [25]. The business model should be reasonably straightforward, logical, measurable, comprehensive, and operationally meaningful [4]. Then, such a model can be helpful for future users. We think that the comprehensive model fits firms’ endogenic and exogenic features, which are the subject of modelling.

3. Materials and Methods

Considering that the literature can be a source of research inspiration, as noted by Nordqvist and Gardner [26] and Short and Payne [27], this paper’s insights have emerged iteratively based on the systematic literature review [28,29]. To resolve the research question and prove the hypothesis, we used non-standardised and non-structured interviews [30] with the literature study [31,32]. We used the methodology of a systematic literature review. It helped to identify a research gap in the literature, which justified the undertaking of research and the formulation of the research hypothesis. The universal Web of Science database was used to select the literature. Then, we selected the literature using keywords. Next, we performed a bibliometric analysis and a content analysis. This allowed for the analysis of the theoretical and practical achievements presented in the studies listed in this paper’s references.

Our research aimed to determine whether the Business Model Canvas in its current form entirely considers the specificity of energy companies. Therefore, we took into account two ways of resolving the research question and proving our hypothesis. At the beginning of our research, we considered how to prove our hypothesis that the business operations of energy firms are affected by the necessity of ensuring State energy security, and that it requires modification of Osterwalder’s Business Model Canvas. There were two ways we could accomplish this: first, we could verify our model based on actual energy firm activities; second, we could focus on the legal environment of energy firms compared to the legal requirements of other firms. We chose the second way. We analysed all essential laws and regulations that influenced business in one European Union Member State—Poland—to determine whether investments in the energy sector are strictly regulated or whether economic freedom exists, like in other industries. We assumed that a positive answer to such a question would create a starting point for further analysis of whether the current Business Model Canvas considers energy companies’ specificity.

In addition to the literature study, interviews with 28 representatives of energy firms were carried out. They represented energy companies and belonged to middle management coming from Polish private and public firms. The non-structured and non-standardised interviews were conducted between February 2018 and December 2020. This long-term period was justified because the data was collected during MBA studies (the 28 representatives from the energy firms participated in MBA studies). We did not consider the company’s size, as we decided that it did not affect the logic of business modelling using the Business Model Canvas. Table 1 shows the respondents who participated in the study. We used the interviews to determine whether interviewees were familiar with the Business Model Canvas and how they perceived the usefulness of the current Osterwalder’s Business Model Canvas in energy firms’ operations. This helped us to resolve the research question and verify our hypothesis.

4. Results and Discussion

4.1. The Legal Environment of Energy Firms: Case of Poland

Legal frames have a significant impact on business models in the energy sector. As with any other European Union Member State, the energy policy of Poland must comply with Directive 2005/89/EC of the European Parliament and the Council [33]. This Directive states that the European Union Member States must have transmission system operators to maintain an adequate level of operational network safety, which is to be understood as the uninterrupted operation of the energy transmission network [34].

The Act of 10 April 1997, the Energy Law, defines the principles of creating the State’s energy policy and determines the activities of energy enterprises. The Act aims to create energy security following the country’s sustainable development conditions, counteracting the harmful effects of natural monopolies by considering environmental protection requirements, obligations arising from international agreements, and balancing the interests of energy companies and their consumers [35]. These objectives are equivalent, and therefore, they must be equally assessed when interpreting this right, both at the administrative and judicial stages. The concept of sustainable development does not differ from that adopted by the United Nations. It means, in accordance with the provisions of Article 3 of the Environmental Protection Law, that socio-economic development must be made while maintaining the natural balance, to guarantee the possibility of satisfying the basic societal needs of both the modern generation and future generations [36,37].

According to Article 4 of the Energy Law, each energy company engaged in the transmission or distribution of fuels or energy, the storage of energy or gaseous fuels (including liquefied natural gas), the liquefaction of natural gas, or the regasification of liquefied natural gas is obliged to maintain the ability of devices, installations, and networks to supply these fuels or energy continuously and reliably while maintaining the applicable quality requirements. An energy company engaged in the transmission or distribution of gaseous fuels or energy is obliged to provide all customers and companies dealing in the sale of these products, based on equal treatment, with the provision of transmission or distribution services, on the terms and to the extent specified in the Energy Law; the provision of transmission or distribution services for these fuels or energy takes place based on a contract for the provision of these services [35].

The discussed Act defines energy security as a situation in the economy that allows consumers’ current and future demand for fuels and energy to be covered if technically and economically justified while maintaining environmental protection requirements [35].

Ensuring the country’s energy security is a task carried out by public administration bodies and energy companies that have been granted certain powers. Energy companies perform public tasks. This generalization resulting from the analysis of legal provisions alone allows for the conclusion that energy companies also have goals other than those resulting from running a business and common to other companies, for example, to generate profit, comply with the law, and develop. The Law of Entrepreneurs [38] defines the principles of starting, performing, and terminating economic activity in the territory of Poland, including the rights and obligations of entrepreneurs and the tasks of public authorities in this respect. It states that taking up, carrying out, and terminating a business is free for everyone equally. Economic activity is carried out on one’s behalf and continuously. Economic freedom is treated as a public subjective law of a negative nature, which corresponds to the general obligation of the State to not infringe upon the freedom of operation of economic entities in the sphere of their economic activity. It belongs to the category of negative liberal rights, the essence of which is the possession of a claim to the State by the entitled person [38].

The Energy Law states that the adverse effects of natural monopolies should be counteracted. Analysis of the provision of Article 1 of the Act, as mentioned earlier, allows for a generalization that the Act is not concerned with preventing the creation of natural monopolies but with counteracting their harmful effects. The Energy Law obliges energy companies to cooperate with competitors or even take unfavourable actions for such an energy company [35]. For example, a company with economic nodal power transmission lines cannot effectively release itself from the obligation to make them available to an entity wishing to compete with it on a previously monopolized market, indicating that it will lose part of the market and some profit. One will not find such regulation in other industries—for example, the clothing or the car industry. We prove again that the law provisions determining the legal environment for energy companies differ from other companies’ legal provisions.

Finally, we provide an additional argument. Based on Article 6 of the Energy Law, the Minister of Energy regulates audits conducted by energy companies [39]. The regulation specifies in a detailed manner how energy enterprises, which transmit or distribute fuels or energy, conduct audits of the legality of fuel or energy consumption by clients of energy firms; audits of measurement and billing systems; and audits of compliance of the clients’ activities with concluded contracts and correctness of settlements with energy companies. These are powers that companies operating in other industries, except for public transport, do not have. However, even public transport firms cannot influence the daily business operations of their clients as deeply as energy firms [35,40,41]. This means that the Business Model Canvas cannot be considered universal. The current model fits firms operating in the open market without public tasks such as energy security. Since energy companies have rights under the Energy Law, they must be accountable for their business activities, which is noticeable, and use the rights granted by law. In addition, the implementation of public tasks indicates the need to consider the public mission in planning their activities, including goals resulting from the provision of Article 1 of the Energy Law.

4.2. Results of Interviews

The study confirmed that almost all the interviewed participants (25 out of 28 people) were familiar with the Business Model Canvas assumptions. Three people from private firms did not know this model in business. They declared that they prefer SWOT analysis and Porter’s 5 Forces because they have become used to these analyses of the perspectives of their companies. All 28 people knew about the importance of models in business operations. Twenty-five people stated during the interviews that the Business Model Canvas is a method to show intended actions in one canvas. One of them said that “nine-building parts of the model that are shown on a one-page canvas template is the strength of this approach”. However, out of 25 people, 20 said they do not know where to include data specific to their public energy company in the current Business Model Canvas.

One of them said, “the energy firm has a mission which is not reflected in Business Model Canvas”. Another said that public energy firms must show the tasks listed in the Energy Law. Others also pointed out the necessity of energy firms following the Energy Law. One interviewee added, “I do not know where to show the accountability process in Business Model Canvas”. All the 28 interviewed people said that public energy firms are obliged to deliver energy constantly, and they have some impact on other firms and individuals because of their public status. The public energy firms are supported by the State and they have to be accountable for realising public tasks. During the interview, one individual pointed out that “there is no need to change Business Model Canvas but to think how to consider energy firm’s features in well-known model”. All 28 people said that public energy firms have different features than private ones. Energy firms operate in an energy market regulated by the State. They should generate profit but are also supposed to fulfil their public tasks. Private firms may focus only on making a profit.

4.3. Business Model Canvas: Towards a Modified Model

There are two primary assumptions in selecting the Business Model Canvas for energy enterprise: the Business Model Canvas and energy enterprise characteristics. Before one begins preparing the Business Model Canvas, there is a need to define energy enterprise, especially, when public energy firms belong to the State and realise government policy. One may define an energy firm as an organisation that serves a public task through market-based strategies. Based on this definition, it is clear that there is a difference between an energy firm and a business enterprise. An energy firm’s fundamental principles are mission-related impact, not only profit oriented, mainly when public energy firms belong to the State and realise government policy. Thus, energy enterprises may generate profits, but it is not the sole target of the enterprise. One may perceive the similarities between energy firms and social enterprises because these firms create profits, but these profits are a means to achieve sustainability in providing a public benefit [42]. In addition, profits are the result of activities covered by a specific government policy. Examples include regulated electricity prices, numerous complex permits for the production and transmission of electricity, or the extraction of fossil fuels. Finally, the effects of energy companies’ activities are “accumulated” in products or services. For example, purchasing energy is included in agricultural production, agricultural processing, and any other production and service. Thus, customers of energy companies are, directly or indirectly, all State citizens and inhabitants.

By purchasing energy products, customers partially participate in government policy an social change. Therefore, it is not a purely market purchase like a car (which someone can buy or not). In addition, energy companies with State capital may pay dividends to the State. Considering these characteristics, one should consider the Mission of energy enterprises (MEE) in the Business Model Canvas. In addition, some of these enterprises may be obliged to non-financial reporting and green-deal issues. However, energy enterprises must realise the social Mission and not solve social problems. From such a perspective, one may understand that Osterwalder’s Canvas, mainly designed for a commercial business organisation [42,43,44,45,46,47,48,49,50,51,52,53], does not fit an energy enterprise fuelled by monetary and non-monetary values and costs. Therefore, there is a need to eliminate potential ambiguity and confusion through re-modelling the traditional Osterwalder’s Canvas.

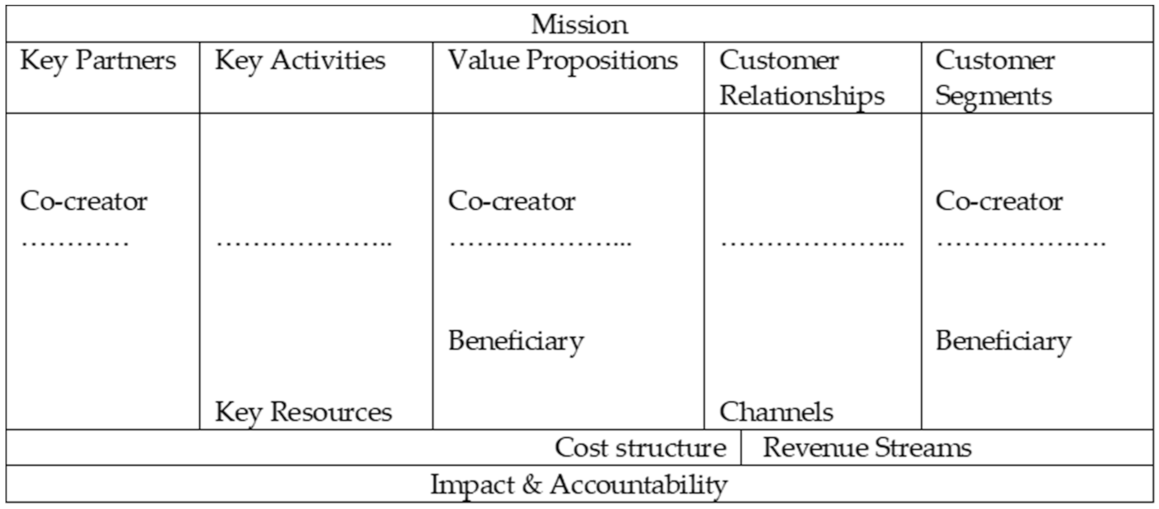

Based on the analysis, one may modify the traditional Business Model Canvas in the following way. First, following previous research on the Business Model Canvas [54], we added the Mission block, which clearly states the purpose of the energy firm and is linked with its vision. Next, the Impact block was added to show the benefits for the energy firm customers and the measures of the success and progress of the energy enterprise. Finally, the typical business model is designed to ensure agility and creates processes to fulfil customer needs in the best way. However, traditional commercial business models allow for opportunistic behaviours even if such models are customer-focused and profit-driven. Meanwhile, the energy enterprises performing tasks are limited by legal frameworks, such as Energy Law. Therefore, the Canvas should consider one more value, which is energy Accountability.

The concept of accountability has become a buzzword in recent decades and is presented in many scientific studies, e.g., [55,56,57,58,59,60,61,62,63]. However, not so long ago, there was a research gap in the field of energy accountability. We understand the term “energy accountability as an obligation or willingness to accept responsibility or to account for one’s actions in the field of planning, producing, obtaining and sustainably using energy” ([63], p. 1). For energy enterprise, energy accountability and its Mission are explicit and central for such a firm. Considering specific tasks of energy firms, including providing energy security for the State and its citizens, the additional blocks of Mission, Impact, and Accountability in the Business Model Canvas of energy enterprises need to be added. This is a difference in comparison to the traditional Osterwalder’s Canvas, which has no such blocks. Energy enterprise thrives to achieve social goals determined in government policy, and it requires the involvement of many stakeholders. Some of them, such as the parliament and the government, determine the rules for energy firms, including price policies and energy security requirements. Therefore, there is a need to modify the concept of Osterwalder and Pigneur [28] and Graves [55] and separate the co-creators of energy policy from its beneficiaries [56]. See the adaptation of the Business Model Canvas for energy enterprise in Figure 1.

This study is in line with the research of Ching, Fauvel [44], Komisar, Lineback [52], and Qastharin [56], which showed limitations of the current Business Model Canvas. As in the case of social enterprises [56], the proposed changes also cause a different sequence of the traditional Osterwalder’s Canvas building blocks. Instead of starting from Customer Segments, we propose starting from Mission, continuing as suggested by Osterwalder to Customer Segments, and ending with Impact and Accountability right after Cost Structure. This is because the energy firm is mission-focused and impact-driven.

5. Conclusions

Up until now, there was little known about the Business Model Canvas development in the energy sector. In this paper, this knowledge gap was filled out, and we proposed the modified Business Model Canvas. We proved our hypothesis that the business operations of energy firms are affected by the necessity of ensuring State energy security, and that it requires modification of Osterwalder’s Business Model Canvas. Energy firms cannot operate the same way as business firms, only focusing on profit, business advantage, and eliminating competing firms. Legal frames have a significant impact on the energy sector, and thus they must be included in the Business Model Canvas. Each energy company engaged in the transmission or distribution of fuels or energy, the storage of energy or gaseous fuels (including liquefied natural gas), the liquefaction of natural gas, or the regasification of liquefied natural gas, is obliged to maintain the ability of devices, installations and networks to supply these fuels or energy continuously and reliably while maintaining the applicable quality requirements. An energy company engaged in the transmission or distribution of gaseous fuels or energy is obliged to provide all customers and companies dealing in the sale of these products, based on equal treatment, with the provision of transmission or distribution services for gaseous fuels or energy.

The analysis of the legal environment of energy companies and the analysis of the current Business Model Canvas proposed by Osterwalder created the basis for seeking an answer to the research question of whether the current Business Model Canvas considers the specificity of energy companies. First, we showed a need to modify the business model definition and argued that it presents how a business works, what kind of business value is provided, and how this is accountable and presented to the stakeholders. We understood the goal of the business model as a tool of reducing uncertainty through the visualisation of business assumptions and their potential effects. Therefore, we verified and modified Chesbrough’s functions of business models. Next, based on the research, it was found that Osterwalder’s Business Model Canvas cannot wholly fit the business model of an energy enterprise. We proved that an energy firm is an organisation that realises public tasks through market-based strategies. Therefore, such a firm needs a different Business Model Canvas than that of a firm focused mainly on profit. We showed that there is a need to add additional building blocks to the Business Model Canvas to understand how an energy firm operates, creates values, and is accountable for its operations. These blocks are Mission, Impact, and Accountability. In the Mission block, the purpose of the energy firm, its reason for existence, is stated. The Impact and Accountability blocks describe the benefits for the energy firm customers and the measurements as the indicators of the success and progress of the energy firm in energy policy. The additional blocks also change their sequence and start from Mission.

One may argue that what we describe as specific characteristics of energy firms can apply to other utility companies such as public transportation, water, or telecom companies required to abide by the security of supply regulations. Moreover, some public firms are obliged to provide public services even at a loss, which is recompensated by grants. However, energy firms are most crucial for others because of energy supply and energy security. Therefore, we focused our study on this kind of firm.

Pointing out the necessity to consider Mission, Accountability, and Impact on others in the Business Model Canvas, we followed arguments of Joyce and Paquin [50] that sustainability issues, which cover accountability, should be included in the Business Model Canvas. Besides, we followed Edvardsson, Gustafsson, Kristensson, Witell, and Tronvoll [64,65], pointing out that business operates in the social environment and public structures. Compared to earlier business model frameworks, this model’s fundamental contribution is the consideration of the firm’s accountability issues. Daily business operations of energy firms responsible for energy security must be accountable. The modified Business Model Canvas is a tool that enables the company to introduce, develop, and measure its created values effectively.

This study developed a helpful tool for companies interested in enhancing their business with the Business Model Canvas. The modified business model framework considers both the providers’ and the customers’ interests along with the public interest. Moreover, our study expands the research on models and forms avenues for future research.

The following avenues for further studies emerge from our findings. Firstly, we think that practitioners’ readiness to understand and use theoretical generalisations in their daily work requires practical solutions. To ensure that the efforts to improve business planning do not remain only as an academic discussion, we focused on developing tools for implementation theory into practice. However, we notice that our study is based on qualitative empirical research. We think that a quantitative study in future research can ensure that the formulated conclusions obtain statistical reliability, comparing outcomes of firms using the modified and unmodified Business Model Canvas in their business operations. Secondly, more research is needed on the Business Model Canvas usage in the public sector and other hybrid organisations, which operate with less profit-dominant business models. Future research may also focus on how the Business Model Canvas includes risk management related to the Internet of Things and Big Data [66] or recycling issues [67]. Such research would help to get the Business Model Canvas approach into a public organisation’s operations sooner.

Author Contributions

Conceptualization, Z.D. and Ł.S.; research, Z.D. and Ł.S.; content writing and final editing, Z.D. and Ł.S. All authors have read and agreed to the published version of the manuscript.

Funding

Funder: Jagiellonian University. Funding program no: FS.1.2.2021. Open access license of the publication was funded by the Priority Research Area Society of the Future under the program “Excellence Initiative—Research University” at the Jagiellonian University in Kraków.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The author declares no conflict of interest.

References

- Al-Mulali, U. GDP growth—Energy consumption relationship: Revisited. Int. J. Energy Sect. Manag. 2014, 8, 356–379. [Google Scholar] [CrossRef]

- Simionescu, M.; Bilan, Y.; Krajňáková, E.; Streimikiene, D.; Gȩdek, S. Renewable energy in the electricity sector and GDP per capita in the European Union. Energies 2019, 12, 2520. [Google Scholar] [CrossRef] [Green Version]

- Hannesson, R. Energy and GDP growth. Int. J. Energy Sect. Manag. 2009, 3, 157–170. [Google Scholar] [CrossRef]

- Osterwalder, A.; Pigneur, Y.; Tucci, C.L. Clarifying business models: Origins, present, and future of the concept. Commun. Assoc. Inf. Syst. 2005, 16, 1–25. [Google Scholar] [CrossRef] [Green Version]

- Amit, R.; Zott, C. Value creation in e-business. Strateg. Manag. J. 2011, 22, 493–520. [Google Scholar] [CrossRef]

- Morris, M.; Schindehutte, M.; Allen, J. The entrepreneur′s business model: Toward a unified perspective. J. Bus. Res. 2005, 58, 726–735. [Google Scholar] [CrossRef]

- Zott, C.; Amit, R.; Massa, L. The business model: Recent developments and future research. J. Manag. 2011, 37, 1019–1042. [Google Scholar]

- Gabriel, C.A.; Kirkwood, J. Business models for model businesses: Lessons from renewable energy entrepreneurs in developing countries. Energy Policy 2016, 95, 336–349. [Google Scholar] [CrossRef]

- Antle, R.; Eppen, G.D. Capital rationing and organizational slack in capital budgeting. Manag. Sci. 1985, 31, 163–174. [Google Scholar] [CrossRef]

- Harris, M.; Raviv, A. The capital budgeting process, incentives and information. J. Financ. 1996, 51, 1139–1174. [Google Scholar] [CrossRef]

- Zott, C.; Amit, R. The fit between product market strategy and business model: Implications for firm performance. Strateg. Manag. J. 2008, 29, 1–26. [Google Scholar] [CrossRef] [Green Version]

- Betz, F. Strategic business models. Eng. Manag. J. 2002, 14, 21–27. [Google Scholar] [CrossRef]

- Hedman, J.; Kalling, T. The business model concept: Theoretical underpinnings and empirical illustrations. Eur. J. Inf. Syst. 2003, 12, 49–59. [Google Scholar] [CrossRef]

- Shafer, S.M.; Smith, H.J.; Linder, J.C. The power of business models. Bus. Horiz. 2005, 48, 199–207. [Google Scholar] [CrossRef]

- Tikkanen, H.; Lamberg, J.A.; Parvinen, P.; Kallunki, J.P. Managerial cognition, action and the business model of the firm. Manag. Decis. 2005, 43, 789–809. [Google Scholar] [CrossRef]

- Johnson, M.W.; Christensen, C.M.; Kagermann, H. Reinventing your business model. Harv. Bus. Rev. 2008, 86, 50–59. [Google Scholar]

- Teece, D.J. Business models, business strategy and innovation. Long Range Plan. 2010, 43, 172–194. [Google Scholar] [CrossRef]

- Zott, C.; Amit, R. Business model design: An activity system perspective. Long Range Plan. 2010, 43, 216–226. [Google Scholar] [CrossRef]

- Magretta, J. Why business models matter. Harv. Bus. Rev. 2002, 80, 86–92. [Google Scholar]

- Baden-Fuller, C.; Morgan, M.S. Business models as models. Long Range Plan. 2010, 43, 156–171. [Google Scholar] [CrossRef]

- Osterwalder, A.; Pigneur, Y. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers; John Wiley and Sons: Hoboken, NJ, USA, 2010. [Google Scholar]

- Hatch, M.J. Organization Theory. Modern, Symbolic, and Postmodern Perspectives, 4th ed.; Oxford University Press: Oxford, UK, 2018. [Google Scholar]

- Chesbrough, H.; Rosenbloom, R.S. The role of the business model in capturing value from innovation: Evidence from Xerox Corporation′s technology spin-off companies. Ind. Corp. Change 2002, 11, 529–555. [Google Scholar] [CrossRef] [Green Version]

- Chesbrough, H. Business model innovation: It’s not just about technology anymore. Strateg. Leadersh. 2007, 35, 12–17. [Google Scholar] [CrossRef] [Green Version]

- McGrath, R.G. Business models: A discovery driven approach. Long Range Plan. 2010, 43, 247–261. [Google Scholar] [CrossRef]

- Nordqvist, M.; Gartner, W.B. Literature, fiction, and the family business. Fam. Bus. Rev. 2020, 33, 122–129. [Google Scholar] [CrossRef]

- Short, J.C.; Payne, G.T. In their own words: A call for increased use of organizational narratives in family business research. Fam. Bus. Rev. 2020, 33, 342–350. [Google Scholar] [CrossRef]

- Lukka, K. Exploring the possibilities for causal explanation in interpretive research. Account. Organ. Soc. 2014, 39, 559–566. [Google Scholar] [CrossRef]

- Lukka, K.; Modell, S. Validation in interpretive management accounting research. Account. Organ. Soc. 2010, 35, 462–477. [Google Scholar] [CrossRef]

- Popay, J.; Roberts, H.; Sowden, A.; Petticrew, M.; Arai, L.; Rodgers, M.; Britten, N.; Roen, K.; Duffy, S. Guidance on the Conduct of Narrative Synthesis in Systematic Reviews. A Product from the ESRC Methods Programme. Version 1; Lancaster University: Lancaster, UK, 2006. [Google Scholar]

- Hart, C. Doing a Literature Search: A Comprehensive Guide for the Social Sciences; Sage: Thousand Oaks, CA, USA, 2001. [Google Scholar]

- Van Aken, J.; Andriessen, D. Handboek Ontwerpgericht Wetenschappelijk Onderzoek: Wetenschap Met Effect; Boom Lemma Uitgevers: Amsterdam, The Netherlands, 2011. [Google Scholar]

- Directive 2005/89/EC of the European Parliament and of the Council of 18 January 2006, on measures to ensure the safety of electricity supply and infrastructure investments. J. EU L. 2006, 33, 22.

- Dobrowolski, Z. Energy and local safety: How the administration limits energy security. Energies 2021, 14, 4841. [Google Scholar] [CrossRef]

- Ustawa z Dnia 10 Kwietnia 1997 r. Prawo Energetyczne (Dz. U. z 2021 r., poz. 716 ze zm.). Available online: https://isap.sejm.gov.pl/isap.nsf/download.xsp/WDU20210001093/O/D20211093.pdf (accessed on 11 August 2021).

- Act of April 27, 2001, Environmental Protection Law (Journal of Laws of 2020, Item 1219). Available online: https://isap.sejm.gov.pl/isap.nsf/DocDetails.xsp?id=WDU20200001219 (accessed on 11 August 2021).

- Dobrowolski, Z.; Sułkowski, Ł. Implementing a Sustainable Model for Anti-Money Laundering in the United Nations Development Goals. Sustainability 2020, 12, 244. [Google Scholar] [CrossRef] [Green Version]

- Pietrzak, A. Prawo Przedsiębiorców. Komentarz; Wolters Kluwer Polska: Warsaw, Poland, 2019. [Google Scholar]

- Rozporządzenie Ministra Energii z Dnia 15 Grudnia 2016 r. w Sprawie Przeprowadzania Kontroli PRZEZ przedsiębiorstwa Energetyczne (Dz. U., poz. 2166). Available online: https://isap.sejm.gov.pl/isap.nsf/DocDetails.xsp?id=WDU20160002166 (accessed on 11 August 2021).

- Ustawa z Dnia 20 Grudnia 1996 r. o Gospodarce Komunalnej (Dz. U. z 2021 r., poz. 679). Available online: https://isap.sejm.gov.pl/isap.nsf/DocDetails.xsp?id=WDU20210000679 (accessed on 12 August 2021).

- Ustawa z Dnia 16 Grudnia 2010 r. o PUBLICZNYM transporcie Zbiorowym (Dz. U. z 2021 r., poz. 1371). Available online: https://isap.sejm.gov.pl/isap.nsf/DocDetails.xsp?id=WDU20210001371 (accessed on 12 August 2021).

- Weill, P.; Malone, T.W.; D’Urso, V.T.; Herman, G.; Woerner, S. Do Some Business Models Perform Better than Others? A Study of the 1000 Largest US Firms; Sloan School of Management Massachusetts Institute of Technology: Cambridge, MA, USA, 2006; Available online: https://mpra.ub.uni-muenchen.de/4752/1/MPRA_paper_4752.pdf (accessed on 21 May 2021).

- Ojasalo, J.; Ojasalo, K. Service logic business model canvas. J. Res. Mark. Entrep. 2018, 20, 70–98. [Google Scholar] [CrossRef]

- Joyce, A.; Paquin, R.L. The triple layered business model canvas: A tool to design more sustainable business models. J. Clean. Prod. 2016, 135, 1474–1486. [Google Scholar] [CrossRef]

- Ching, H.Y.; Fauvel, C. Criticisms, variations and experiences with business model canvas. Eur. J. Agric. For. Res. 2013, 1, 26–37. [Google Scholar]

- Business Model Canvas. Available online: https://www.businessmodelsinc.com/about-bmi/tools/business-model-canvas (accessed on 12 August 2021).

- Vargo, S.L.; Lusch, R.F. Service-dominant logic: Continuing the evolution. J. Acad. Mark. Sci. 2008, 36, 1–10. [Google Scholar] [CrossRef]

- Schlager, T.; Maas, P. Reframing customer value from the dominant logics perspective. Int. J. Mark. 2012, 51, 101–113. [Google Scholar] [CrossRef] [Green Version]

- Grönroos, C.; Voima, P. Critical service logic: Making sense of value creations and co-creation. J. Acad. Mark. Sci. 2013, 41, 133–150. [Google Scholar] [CrossRef]

- Heinonen, K.; Strandvik, T.; Mickelsson, K.J.; Edvardsson, B.; Sundström, E.; Andersson, P. A customer dominant logic of service. J. Serv. Manag. 2010, 21, 531–548. [Google Scholar] [CrossRef]

- Critically Assessing the Strengths and Limitations of the Business Model Canvas. Available online: https://essay.utwente.nl/64749/1/Coes_MA_MB.pdf (accessed on 12 August 2021).

- Brandenburger, A.M.; Stuart, H.W. Value-based Business Strategy. J. Econ. Manag. Strategy 1996, 5, 5–24. [Google Scholar] [CrossRef]

- Komisar, R.; Lineback, K. The Monk and the Riddle: The Art of Creating a Life While Making a Living; Harvard Business School Press: Boston, MA, USA, 2001. [Google Scholar]

- The Meaning of Social Entrepreneurship. Available online: http://www.caseatduke.org/documents/dees_sedef.pdf (accessed on 14 May 2021).

- Using Business Model Canvas for Non-Profits. Available online: http://weblog.tetradian.com/2011/07/16/bmcanvasfor-nonprofits (accessed on 29 April 2021).

- Business Model Canvas for Social Enterprise. The 7th Indonesia International Conference on Innovation, Entrepreneurship, and Small Business. 2015. Available online: https://www.researchgate.net/profile/Annisa-Qastharin/publication/323393037_Business_Model_Canvas_for_Social_Enterprise/links/5aa8e20d0f7e9b0ea308294a/Business-Model-Canvas-for-Social-Enterprise.pdf (accessed on 21 June 2021).

- Ospina, S.; Diaz, W.; O′Sullivan, J.F. Negotiating accountability: Managerial lessons from identity-based nonprofit organizations. Nonprofit Volunt. Sect. Q 2002, 31, 5–31. [Google Scholar] [CrossRef]

- Smith, A. Emerging in between: The multi-level governance of renewable energy in the English regions. Energy Policy 2007, 35, 6266–6280. [Google Scholar] [CrossRef]

- Ackerman, J. Co-governance for accountability: Beyond “exit” and “voice”. World Dev. 2004, 32, 447–463. [Google Scholar] [CrossRef]

- Leithwood, K.; Earl, L. Educational accountability effects: An international perspective. Peabody J. Educ. 2009, 75, 1–18. [Google Scholar] [CrossRef]

- Melville, E.; Christieb, I.; Burningham, K.; Way, C.; Hampshire, P. The electric commons: A qualitative study of community accountability. Energy Policy 2017, 106, 12–21. [Google Scholar] [CrossRef] [Green Version]

- Whittle, R.; Ellis, R.; Marshal, I.; Alcock, P.; Hutchison, D.; Mauthe, A. From responsibility to accountability: Working creatively with distributed agency in office energy metering and management. Energy Res. Soc. Sci. 2015, 10, 240–249. [Google Scholar] [CrossRef]

- Sułkowski, Ł.; Dobrowolski, Z. The role of supreme audit institutions in energy accountability in EU countries. Energy Policy 2021, 156, 112413. [Google Scholar] [CrossRef]

- Edvardsson, B.; Gustafsson, A.; Kristensson, P.; Witell, L. Customer integration in service innovation. In The Handbook of Innovation and Services; Gallouj, F., Djellal, F., Eds.; Edward Elgar: Cheltenham, UK, 2010; pp. 301–317. [Google Scholar]

- Edvardsson, B.; Tronvoll, B. A new conceptualization of service innovation grounded in s-d logic and service systems. Int. J. Qual. Serv. Sci. 2013, 5, 19–31. [Google Scholar] [CrossRef] [Green Version]

- Dobrowolski, Z. Internet of things and other e-solutions in supply chain management may generate threats in the energy sector—The quest for preventive measures. Energies 2021, 14, 5358. [Google Scholar] [CrossRef]

- Dobrowolski, Z.; Sułkowski, Ł.; Danielak, W. Management of waste batteries and accumulators: Quest of European Union goals. Energies 2021, 14, 6273. [Google Scholar] [CrossRef]

Figure 1.

Business Model Canvas for energy enterprise (Source: The authors’ own elaboration based on Qastharin [56]).

Figure 1.

Business Model Canvas for energy enterprise (Source: The authors’ own elaboration based on Qastharin [56]).

{kind=link}

Table 1.

Respondents from energy firms who participated in the study.

| The Type of Energy Firm (Private or Public Production of Energy or Energy Utilities) | Number of Respondents Representing Particular Energy Firm |

|---|---|

| Private, production | 3 |

| Public, production | 25 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Dobrowolski, Z.; Sułkowski, Ł. Business Model Canvas and Energy Enterprises. Energies 2021, 14, 7198. https://doi.org/10.3390/en14217198

AMA Style

Dobrowolski Z, Sułkowski Ł. Business Model Canvas and Energy Enterprises. Energies. 2021; 14(21):7198. https://doi.org/10.3390/en14217198

Chicago/Turabian StyleDobrowolski, Zbysław, and Łukasz Sułkowski. 2021. "Business Model Canvas and Energy Enterprises" Energies 14, no. 21: 7198. https://doi.org/10.3390/en14217198

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.