1. Introduction

Power systems are under a period of rapid evolution. The integration of renewable energy sources (RES) is necessary to achieve the Climate Change objectives [

1], but it requires new solutions and more flexible power systems to achieve it at a reasonable cost [

2]. A decentralized and dynamic paradigm is replacing the old centralized and rigid one [

3,

4]. Now, operators use all kinds of flexible resources to preserve balance, ensure the security of supply, and improve the efficiency of the system. New flexibility resources as Demand Side Management (DSM) require operators and policymakers to work together to create the appropriate legal and economic framework [

5] and to establish the terms of flexibility.

Demand Side Management (DSM) refers to planning, implementing, and monitoring the use of electricity to generate changes in the consumers’ demand profile to adapt to different needs [

6,

7]. DSM solutions are a valuable tool to smooth demand peaks [

8], avoid blackouts, reduce investments on the grid [

9] and absorb fluctuations of Renewable Energy Sources (RES) power output [

10]. Nevertheless, these uses were marginal since power systems treated consumers as passive agents without the capacity to modify their loads and relied on the flexibility of fossil generators [

4]. But now, when flexibility needs arise due to RES variability [

2,

11], thanks to the advances in Information and Communication Technologies (ICT), DSM counts as necessary infrastructure to fully participate in the system flexibility throughout Demand Response Products (DRP) [

12,

13].

Demand Response Products (DRP) are not new; many countries have used this kind of program to accommodate them through the years with satisfactory results. The use of Demand Response (DR) was mainly set to avoid extreme and rare events as system blackouts and severe grid conditions to reduce grid decay [

14]. Nowadays, the advances in ICT shows that DR has greater reliability to provide flexible services to the system than conventional generators [

15]. First, DR can have lower costs than other flexible resources and can provide economic profits to the system as a whole and the consumers that provide it [

16,

17,

18]. Second, DR presents an on-site solution to enable efficient integration of Distributed Energy Resources (DERs) that activate new market agents and open new business opportunities [

19,

20,

21]. Third, DR can provide cheap and reliable Ancillary Services (AS) that were exclusively provided by generators, and as well as other consumer-based solutions, can help to reduce market power [

22].

However, regulatory barriers remain an issue for the participation of demand. Regulatory barriers relate to market designs that limit the participation of demand, forcing them to participate in markets designed for generators. For instance, imposing large minimum bidding capacities or long time maintenance requirements that make difficult or even impossible the participation of most consumers [

21]. To overcome the lack of scale, aggregators are gaining increasing attention in many policy interventions [

23,

24]. Aggregation is the activity of grouping several consumers to perform as one entity to respond to the operator in the market. An aggregator is an organization that deals with markets, System Operators (SO), and consumers, acting as the intermediary party to exploit the valuable resources that consumers under a contract can provide [

25].

Therefore, power systems around the world are developing new and more dynamic programs to increase the participation of demand as agents, known as Balance Service Providers (BSP), which act as Demand Response Providers (DRPV) in direct competition with other BSP of other flexibility resources in the Ancillary Services (AS) markets [

26] that are now open to DR.

To our knowledge, no analysis or comparison exists of the different parameters and prices of DRP in AS among different countries. On this basis, this article aims to provide a reference point to policymakers and researchers that work with DRP in the AS markets around the world. The article provides an analysis of the different country programs under a framework of standardized parameters of both AS and DRP. Hence, this work outlines a methodology to compare different DRPs under a common language to analyze the benefits and drawbacks found in them, taking special attention to their main technical parameters and prices. Finally, some policy recommendations for new DRP are presented.

The rest of the paper is organized as follows.

Section 2 presents the methodology used to analyze the different DRP for AS.

Section 3 provides information on the DRPs of different power systems in the different continents. The discussion arises in

Section 4, where a comparison between programs and prices appears. Finally, the main conclusions are stated in

Section 5.

2. Materials and Methods

2.1. Standards to Classify Operation Services

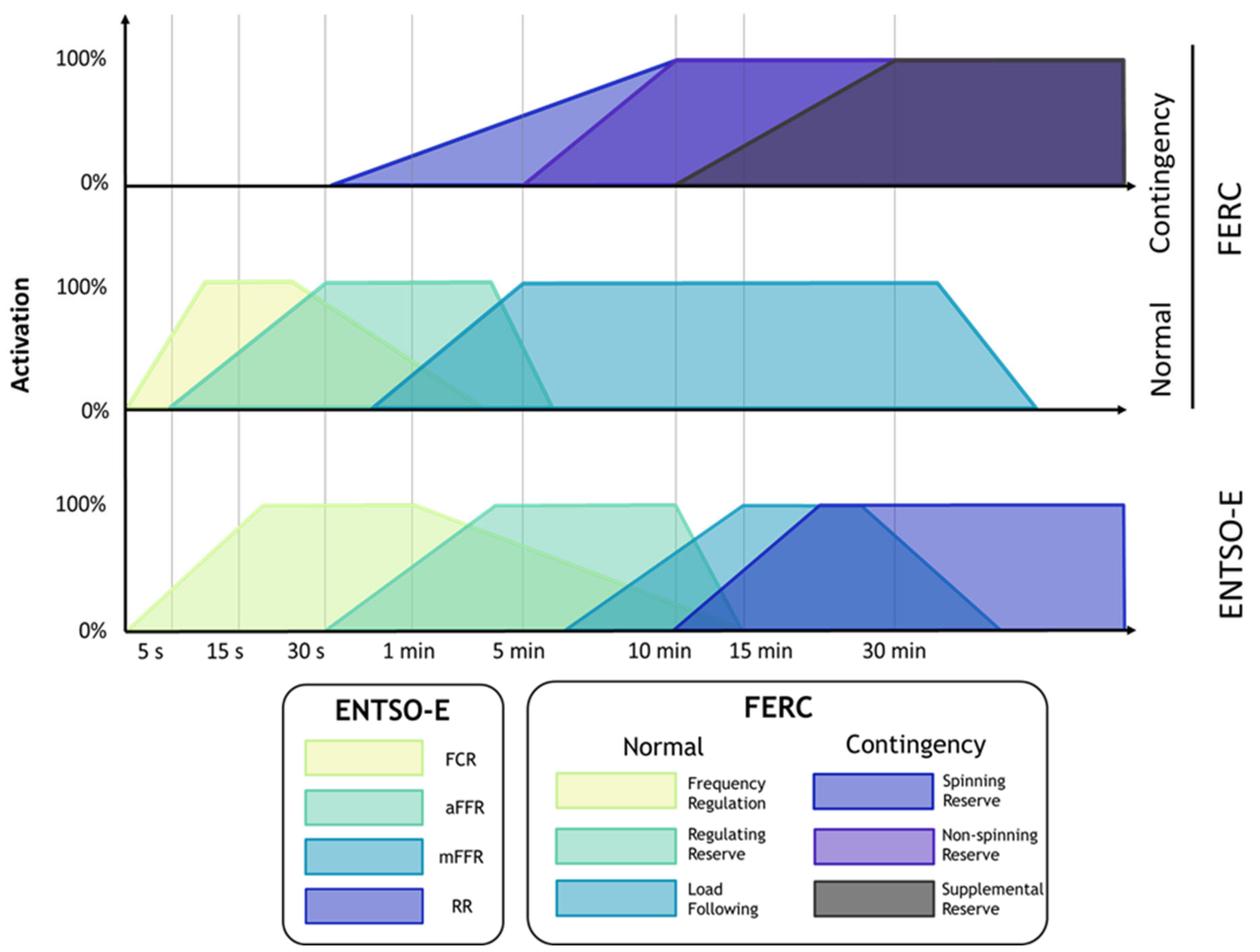

Systems use different nomenclature for AS across the world. In some regions exist degrees of standardization created by Transmission System Operators (TSOs) from neighboring countries and regions. Two of the best-known are the European and the North American standards, developed by the European Network of Transmission System Operators for Electricity (ENTSO-E) and the Federal Energy Regulatory Commission (FERC), respectively.

Figure 1 provides a summary of the described standards.

ENTSO-E

ENTSO-E stands for European Network of Transmission System Operators for Electricity. It is an organization that represents 42 TSOs from 35 European countries. Among many other functions, ENTSO-E coordinates most of the European TSOs and drafts common network codes for the countries. The nomenclature for the European AS is as follows [

27]:

Frequency Containment Reserve (FCR). This service aims to automatically stabilize the frequency after the occurrence of small and unpredictable imbalances. Actions within this type of service must start no later than 30 s from the imbalance, while the response covers up to 15 min. Another common name for this service is Primary Reserve.

Frequency Restoration Reserve (FRR). This service intends to respond to imbalances too long or too large to be solved by FCR. Therefore, its objective is to restore frequency and replace FCR. There are two versions of this service.

- ○

Automatic Frequency Restoration Reserve (aFRR). It works between 30 s and 15 min from the frequency deviation. Also known as Secondary Reserve.

- ○

Manual Frequency Restoration Reserve (mFRR). It responds manually no later than 15 min from the imbalance. Also known as Tertiary Reserve.

Replacement Reserve (RR). This service complements and/or replaces FRR when needed. It is a complementary reserve prepared for additional imbalances, which is manually activated no sooner than 15 min after the frequency deviation takes place.

FERC

FERC stands for Federal Energy Regulatory Commission. It is “an independent agency that regulates the interstate transmission of electricity, natural gas, and oil” in the United States [

28]. Included among its many responsibilities is “to protect the reliability of the high voltage interstate transmission system through mandatory reliability standards”. As part of this responsibility, the FERC has developed a nomenclature that classifies ancillary services over the United States and part of Canada. The services are divided into two groups according to the nature of the frequency disturbance.

Operating Services for Normal Conditions

These services are designed to deal with unpredictable frequency deviations mainly caused by inaccuracy on demand prediction and/or renewables production forecasts. There are three types of service within this group [

29]:

- ○

Frequency Regulation. This service is based on Automatic Generation Control (AGC) and responds immediately to changes in frequency. It must be fully activated 10 s after the frequency disturbance started, and the activation normally lasts from a few seconds to several minutes.

- ○

Regulating Reserve. AGC responds to the System Operator (SO) requests to bring back frequency or interchange programs to target. It must respond between 4 s and 1 min and lasts several minutes.

- ○

Load Following. This service bridges between regulation and intraday energy markets. It is like the Regulating Reserve but with slower starts and longer activity periods. It must respond between 5 and 10 min, while the activation can last from 10 min to a few hours.

Operating Services for Contingency Conditions

These services provide a reserve to face a contingency event (predicted or not) and keep frequency on its normal value. At the same time, they replace other activated reserves so that the system returns to the same level of balance before contingency. There are three types of service:

- ○

Spinning Reserve. It is defined as unloaded generation synchronized to the grid (rotating mass) that can be activated in case there is a frequency deviation caused by a contingency. The definition includes non-synchronized capacity that, by its technical traits, can be connected and activated as quickly as conventional Spinning Reserves. This service activates in less than 10 min from the contingency (normally much faster) and lasts up to 2 h.

- ○

Non-spinning Reserve. This resource has the same target as Spinning Reserve, but it includes offline resources that can connect and be fully active within 10 min and work for up to 2 h.

- ○

Replacement or Supplemental Reserve. This service acts to restore Spinning and Non-Spinning reserves to the status they had before the contingency. The service must be active 30 min after the contingency.

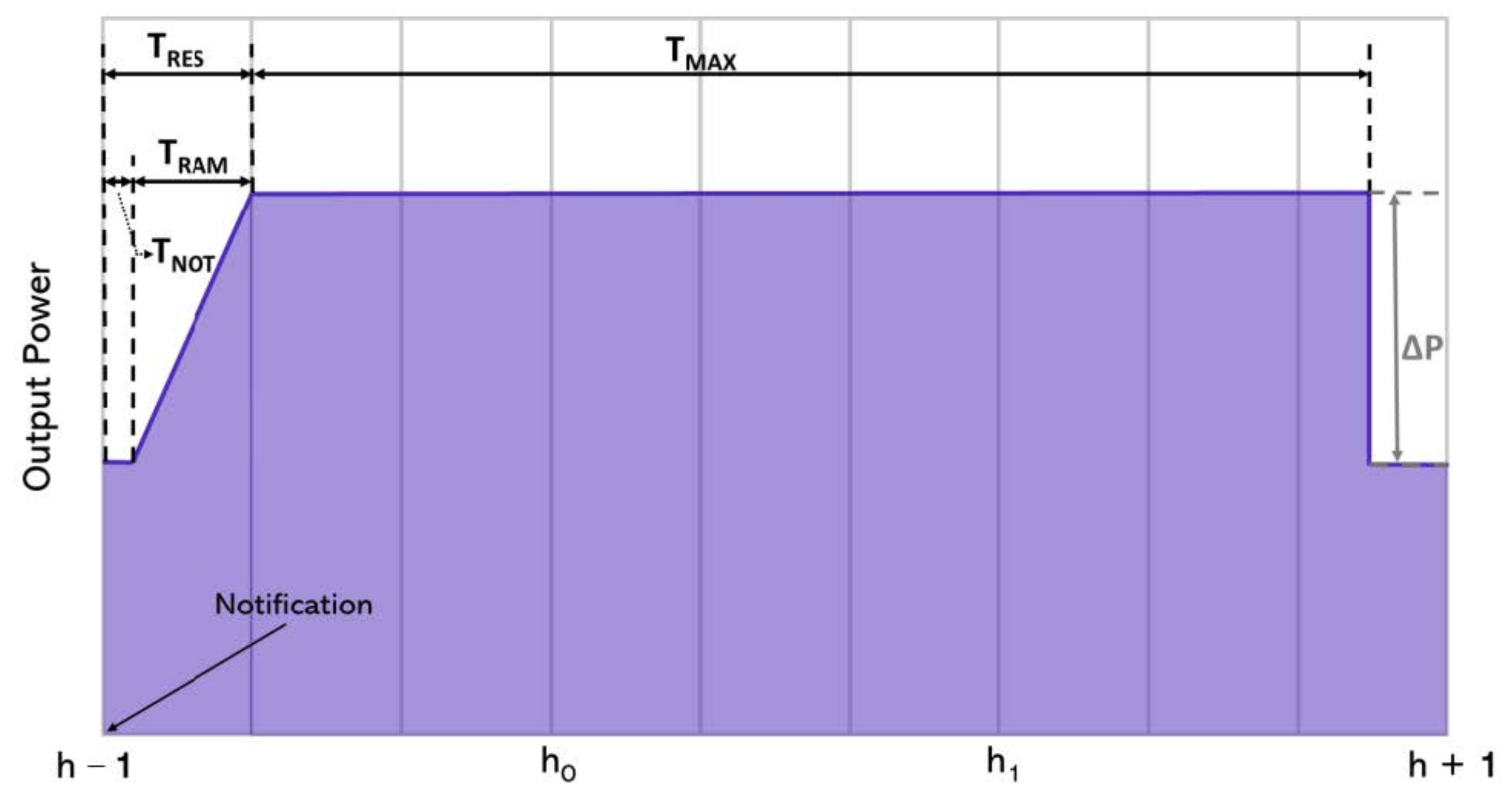

2.2. Ancillary Services Parameters

Table 1 describes the most important parameters that characterize a general AS defined in [

25], which

Figure 2 summarises. These listed parameters consider times, power requested, and characteristics as the type of activation.

2.3. Demand Response parameters

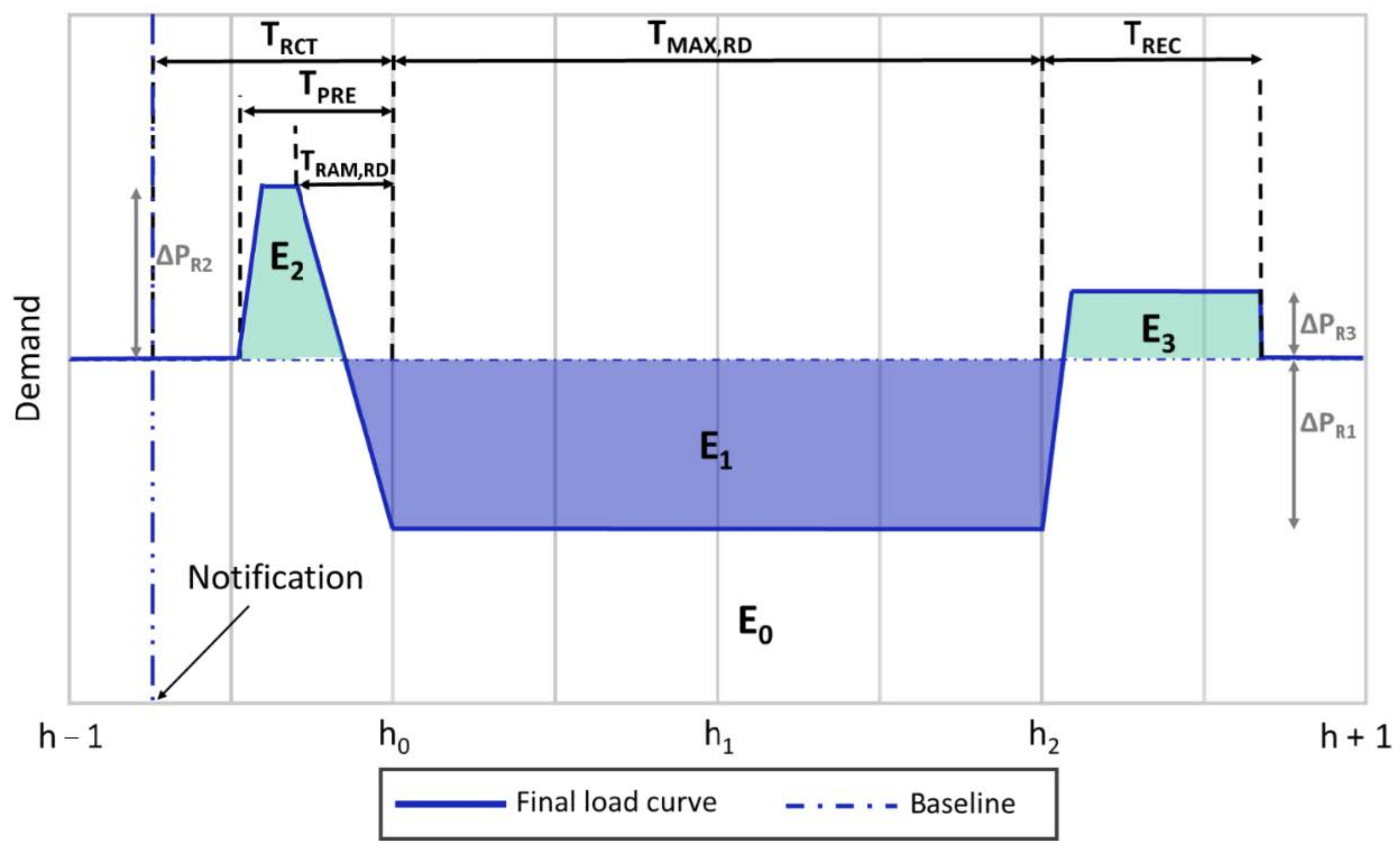

The most significant parameters that characterize a general DR product are described in

Table 2. Technical requirements are also represented in

Figure 3.

2.4. Assessment Methodology

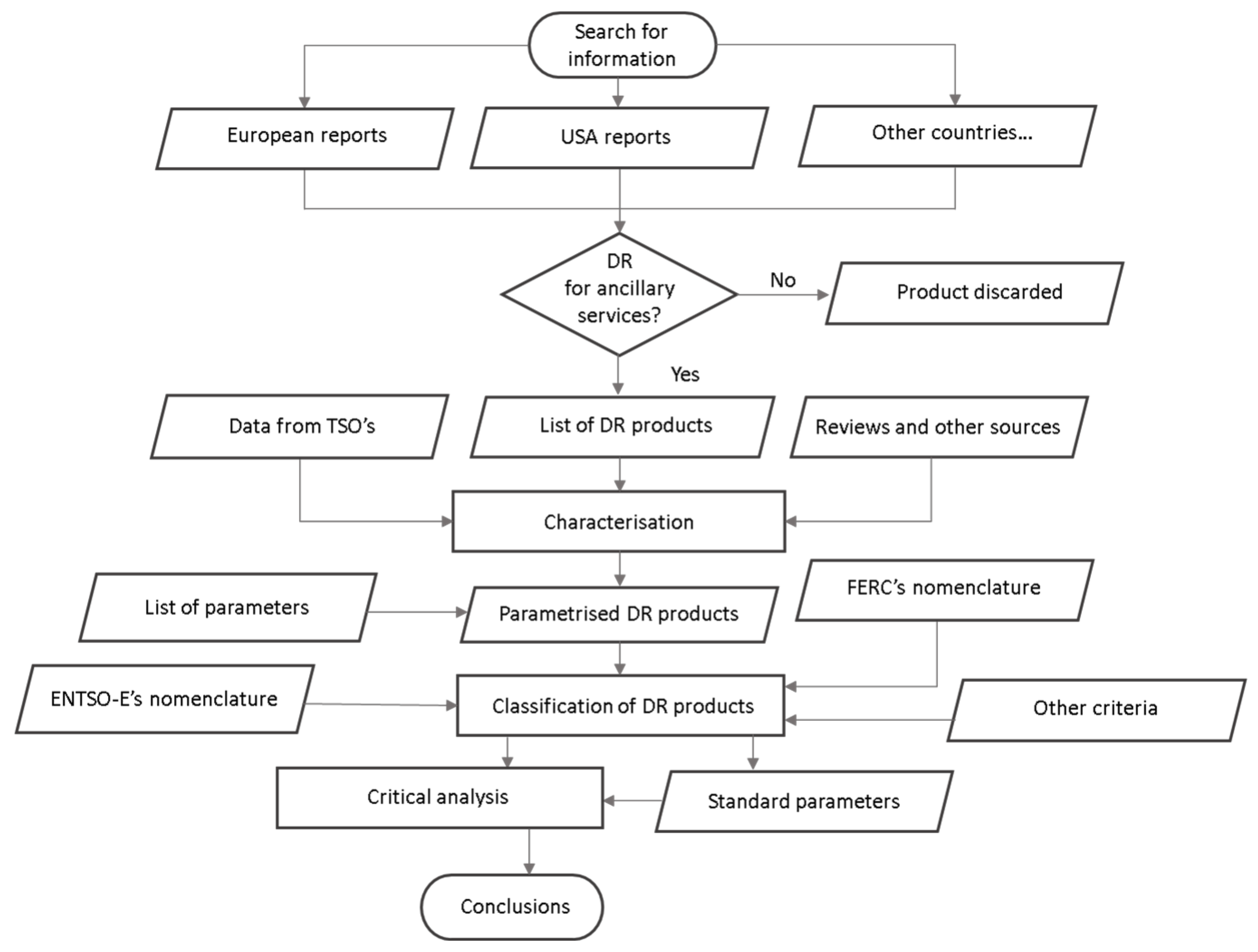

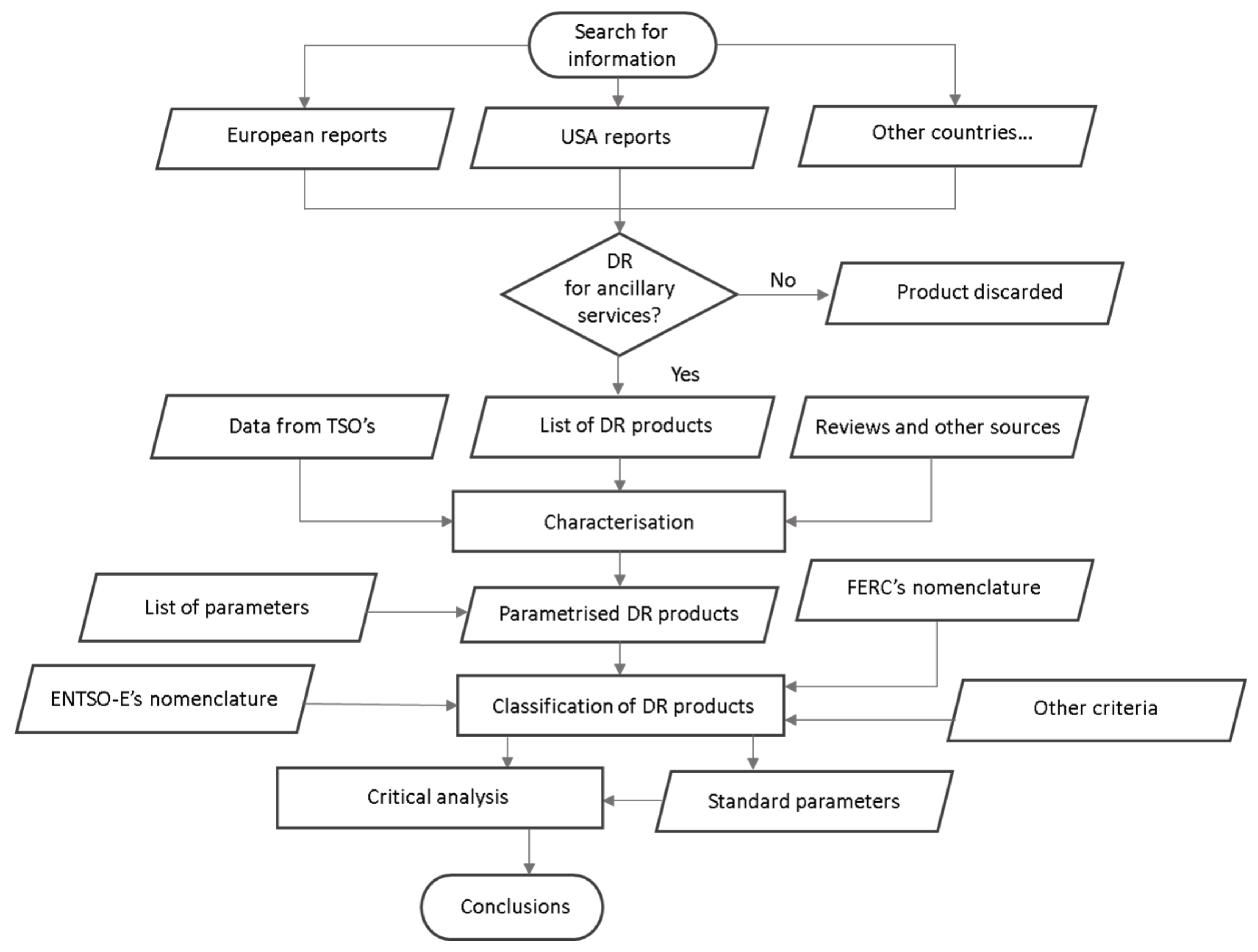

Figure 4 shows the developed methodology to study and compare the different DRP. The first action of the developed methodology consists of the gathering and filtration of general information to construct a list of DRPs. For this first gathering of information, general reports serve as a start. DR works not only as a balancing tool but also in the spot markets [

15]; these programs are out of the scope of this analysis. Here, the methodology discards all the products that do not provide AS.

The information needs a common structure, but products coming from several TSOs have different parameter names when in fact, they represent the same concept due to the lack of standardization [

31]. To homogenize this series of products, the methodology uses the same terms for the same concept, regardless of their original names. A list of DR parameters like the one presented in

Section 2.3 has this purpose. The output of this process is a list of parametrized products.

Once all products are characterized, it is possible to classify them according to the criterion of interest. For instance, depending on the TRCT, the method sets several intervals of time and places each product on its corresponding rank. In our case, the classification follows the ones used by FERC and ENTSO-E. First, we check what kind of services both nomenclatures consider and how they define each of them. After this, we compare our list of parametrized products with these definitions so that it was effortless, for instance, to classify the European products under the American nomenclature and vice versa.

After the classification, the method continues with a review of the success or failure of every product and relate it to their traits and circumstances. The output of this analysis is a series of conclusions regarding what aspects influence the effective participation of DR in the AS and to what extent.

2.5. Consulted Documents

Regarding the search for DR products, there are several reliable sources to start with; depending on the country of interest, the information is normally provided by the TSO or market operator. For a more general view, in the case of the European countries, there is an extensive report prepared by the Smart Energy Demand Coalition [

32] with information about DR programs from 18 different European countries. However, this report came out in 2017, and since DR is rapidly growing in Europe [

15], some of its information is already out of date.

The Regulatory Assistance Project prepared in 2013 a report which presents the history and trends of DR in the United States [

33]. Another source that is interesting and more updated is the Independent System Operator and the Regional Transmission Organization Council’s document referenced in [

34].

The Asia-Pacific region was reviewed by [

35]. In some cases, especially when a country’s electricity system has been recently open to DR, there may not be enough information to correctly characterize its products. Normally, in these countries, data is very short and/or has no English translation. Another problem that can be even harder to tackle is restricted or private information. Some TSOs prepare reports with technical and economic data on DR regularly, but they are only available for market participants. In this case, unless the TSO allows the researchers to access such reports, it will be harder to identify the state of DR in these countries. In this case, the best possible action seems to be to use a secondary source, such as general reports or reviews prepared from these primary sources.

Finally, DR information becomes rapidly out of date due to the quick evolution of electricity markets. In some cases, either because of imperfect market design, unexpected reactions of the stakeholders, or incapacity to encourage demand participation. Consequently, TSOs may want to modify their rules or even withdraw them from the market. Additionally, prices and the share of demand side on AS may widely vary from one year to another. To avoid using outdated information, we searched for the most recent reports and reviews. Furthermore, when it was possible, we contrasted data from international reviews with numbers in reports prepared by each TSO. In some cases, we found recent data on prices and energy volumes, but also old data on market rules and procedures that are three to six years old. In front of these situations, we assume that rules have stayed unchanging during the last years, adding some uncertainty to the analysis.

3. Demand Response around the World: Main Application

3.1. Europe

Many European countries opened most of their AS to DR with the same rules as generation resources to compete to provide capacity. Many TSOs adjusted the technical requirements of these services to match what DRPVs can do. In many other cases, TSOs only developed special programs for Demand Side Resources (DSR) to assure DR participation in front of strong competitors or too demanding technical requirements. At the end of this section,

Table 3,

Table 4,

Table 5 and

Table 6 contain the main parameters that characterize the different programs open to DR in European AS markets.

3.1.1. Belgium

In Belgium, both FCR and mFRR are open to DR. Moreover, there is an Interruptible Service especially designed for load curtailment and a Strategic Reserve, in which DSR represented 10% of total reserves in 2017 [

28]. However, AS exclude residential consumers even if they could provide more than 4700 MW of reserve [

32]. The Belgian mFRR has two different resources. On the one hand, monthly bids on the market of Reserved Volumes, where the service only has an availability payment, and technical requirements vary between Standard R3 and Flex R3 product. The DRPV can choose which kind of product to offer according to their flexibility. Successful bidders in these auctions acquire the responsibility to respond under TSO’s request subject to fines. On the other hand, DRPVs can present bids continuously on the market of Non-Reserved Volumes, up to 15 min before the service activation, to obtain an energy payment [

33]. Regarding the Interruptible Service, as in the case of Reserved Volumes, there are three products with different requirements. In all cases, the maximum response time (T

RES) has the same value, but the maximum duration (T

MAX) is very different from one product to another [

28]. This principle makes it easier to match what DSRs can do with what TSO needs.

3.1.2. Denmark

DR activity in Denmark remains low, even if all electricity markets are open to it. A generator-based design and the scarce need for reserve in this country may be the main reasons for this slow development. Nevertheless, the constant growth of renewable energies will likely increase the necessity of DR to assure the system’s reliability. Denmark divides its power system into two zones. DK1, on the West, is part of the joint continental FCR market, while DK2, on the East, is part of the Nordic synchronous area. Therefore, FCR functions differently according to the corresponding zone [

34]. On the contrary, mFRR rules are the same, regardless of the zone of application. In this service, bids can be upwards or downwards, but a combination of both is not acceptable. The service is remunerated with an energy payment whose minimum (or maximum, for the downwards reserve) price is the electricity price in the spot market.

3.1.3. Finland

All AS accept DR in Finland, although its participation varies among the different services. For instance, the DR share in aFRR was absent in 2018, while in mFRR it reached 400 MW. Close to the aFRR’s case, DR reserves on FCR added only 4 MW [

36]. Some of the most relevant barriers identified are lack of economic benefit, absence of a communication standard, and low motivation for consumers to be involved in load management [

37]. Still, around 1800 MW of loads can be remotely controlled. This represents more than 10% of peak demand in Finland, which in 2014 reached 14,200 MW. FCR is procured through an annual and hourly market, in both cases paid with an availability payment only. In the annual auction, BSPs receive the price for their reserves, which will vary from one day to the next one, and the Finnish TSO acquires all usable capacity at the price determined in the auction. On the other hand, other BSPs can present bids with their reserves daily, and the TSO purchases only the amount needed [

38]. There is a Strategic Reserve used to compensate for higher demand in winter. Technical requirements are like mFRR, and the remuneration is agreed upon in a private contract. In 2018, DR reached 22 MW of capacity in this service [

36].

3.1.4. France

France was one of the first European countries to open its electricity markets to DR. In 2003, industrial consumers were already able to offer their flexibility on the balancing mechanism. In 2011, mFRR opened to DR, and in 2018, it accounted for more than 50% of the Rapid Reserve. Since 2014, industrial consumers larger than 1 MW have got the chance to participate in FCR [

39]. The energy used in the French balancing mechanism, all provided by DR reached 22 GWh in 2018, and the maximum DR reserve activated simultaneously exceeded 1000 MW [

39]. There is also a mechanism in France called “Demand Response Call for Tenders”, designed to promote DR development. It is closed for conventional means of self-generation, and consumers already benefited from the Interruptible Load service. The total capacity provided by this mechanism reached 2900 MW in 2020. In aFRR, BSPs have three products, each of which has its own T

RES requirement. Bids in this service require symmetry and activate at the pro rata of the BSP’s obligation. On the other hand, mFRR and RR have very similar traits, with the biggest difference in T

RES and the price of the payments, being RR cheaper as it is a less demanding service (higher T

RES).

3.1.5. Germany

Germany has a strong industrial sector that has a potential of 6.4 GW DR capacity available for 1 h at least [

40], with DR investments around 10 times smaller than capacity provided by traditional generation, while operation and maintenance costs are dependent on each manufacturing process [

41]. Estimations show that the tertiary sector could provide up to 3.8 GW [

42]. FCR, aFRR, and mFRR services are all open to DR, and there is an Interruptible Service especially designed for DSRs. aFRR bids are weekly presented in a joint market with Austria. The service requires full availability for 12 h a day and a minimum size of the bid of 5 MW (1 MW if only one bid is presented) [

43], but these requisites will be modified soon to fit more DR to AS [

32]. mFRR auctions occur only during weekdays, and availability is required for 4 h instead of 12. It is possible that coming changes would make new aFRR’s design more like current mFRR’s.

3.1.6. Ireland

The rapid growth of wind energy in Ireland has created an increasing need for flexibility, so the Irish TSO works on specific programs to take advantage of DSRs. In 2017, 19 DRPVs were registered to provide a reserve, with a total capacity of 362 MW [

44]. Demand Side Units (DSUs) are DRPVs participating in the capacity market, with a reserve no smaller than 4 MW that can be aggregated from smaller units, not subject to further size limitations. These units are asked to manually modify their load curve with a T

RES of 1 h, and they will be rewarded with an annual capacity payment since they must be available any day, at any time. Powersave is a service designed to reduce load when total demand is close to the available generation capacity. DRPVs with a reserve no smaller than 0.1 MW can participate during working days in exchange for an energy payment [

32].

3.1.7. The Netherlands

Most of the AS in the Netherlands are open to DR. In 2017, the Dutch TSO purchased 1.5 GW of capacity provided by DSRs, with a total activation of 500 GWh. Distribution System Operators and retailers are starting to see demand management as an attractive business [

32]. One particularity of aFRR in the Netherlands is its activation logic. When the TSO detects an ordinary frequency deviation, it activates the reserves by merit order, so that only those BSPs who presented the cheapest bids are activated. However, if the TSO detects an “extraordinary” deviation, it will activate all resources at the pro rata of the BSP’s obligation to achieve the biggest possible power ramp [

45]. This solves the contingency faster, and BSPs get a higher energy payment. There is also a capacity payment determined in an annual auction. The Dutch mFRR services treat upward and downward reserves separately. A single unit can only present one type of reserve, while groups of BSPs can participate in both markets at the same time. Consumers with a contracted power of 60 MW or higher must present their reserves in mFRR. T

RES and the calculation of the price for the energy payment are different for upward and downward reserves. Such prices depend on the spot market price.

3.1.8. Sweden

Sweden is divided into four zones, SE1, SE2, SE3, and SE4. Sometimes certain parameters of AS vary within those zones. Sweden is a country with large water resources, and its capacity reserves come from northern hydroelectric plants. Some thermal plants also activate when there is a congestion problem or during peak load periods. Swedish FCR, aFRR, and mFRR are all open to DR and aggregation, but sometimes technical requirements prevent many DRPVs from participating in them. For instance, the minimum capacity (ΔP

min) is 5 MW in SE4 and 10 MW in the rest of the country, making it difficult for most consumers to meet such requirements and enter the mFRR market. The service has an energy payment only [

32]. There is a Strategic Reserve to be 25% provided by DSRs. The technical requirements of the Strategic Reserve are like mFRR’s, but the service has a capacity and an energy payment.

3.1.9. Switzerland

In 2013, Switzerland became one of the most advanced countries in DR development in Europe. The legislation clearly defines BSP’s roles and mitigates costs and risks. The closure of nuclear power plants and water scarcity may increase the need for flexibility in Switzerland in the coming years [

46]. All AS are open to DR and aggregation, and in 2017 [

47], DR provided 3 MW of reserve in FCR, 10 MW in aFRR, and 49 MW in mFRR [

32]. aFRR in Switzerland has some particularities. Bids take place in a weekly auction and must be symmetric, while the activation occurs at the pro rata of the BSP’s obligation. ΔP

min is 5 MW, and the remuneration is based on a capacity payment dependent on the weekly auction and an energy payment dependent on the spot market price [

48]. Bids for mFRR take place weekly and daily. The weekly auction accepts bids for any hour during the week, while the daily auction has six blocks of 4 h. Products do not have to be symmetric in this service, but they must be larger than 5 MW too. T

RES depends on the direction of the reserve (upwards or downwards) and the type of auction [

48].

3.1.10. United Kingdom

Most of the British ASs are open to DR and aggregation, although its participation remains low in some of them. The British TSO adjusted several market rules and requirements to increase this participation that had as main barriers to the complexity and excess of regulatory changes [

32]. Demand Turn Up is a service designed to decrease generation or increase consumption in times of low demand and high renewable generation. The activation of this service can only be done within a certain schedule, and T

RES and T

MAX do not have fixed values but are based on what each BSP can offer. In 2018, 115 MW of reserve provided this service, with total usage of 1465 MWh. Short-Term Operating Reserve (STOR) used to be the most important program in the UK, but decreasing prices have discouraged many DRPVs from participating in it. This service is like ENTSO-E’s standard Supplemental Reserve. There are three different products within the STOR program, with technical traits and a reward based on capacity and an energy payment. Annual auctions of BSPs determine prices for the next seasons [

49]. The Fast Reserve demands a ΔP

min of 25 MW, where only very large consumers can access it and compete with generators and storage units. Rapid Reserve’s technical requirements make it like aFRR, and the service rewards three concepts: capacity, energy, and nomination. Nomination payment depends on the time provided and not on actual activation nor capacity provided [

50,

51].

3.2. North America

Many North American systems allow DR to access AS markets with similar rules than generation resources to compete to provide capacity. Several TSOs adjusted the technical requirements of these services to match what DRPVs can do. In many other cases, TSOs developed only special programs for DSRs to assure DR participation in front of strong competitors or too demanding technical requirements. At the end of this Section,

Table 7 and

Table 8 contain the main parameters that characterize North American AS for DR.

3.2.1. California Independent System Operator (CAISO)

California Independent System Operators (CAISOs) DRPs participate directly in the region capacity market jointly with the other products [

52,

53], and California DSOs have maintained traditional load disruption and load shifting programs [

54]. California has 1612 MW of DR resources in economic programs that reduce the load based on anticipated offset prices in real-time markets [

55]. The most relevant DRP in the region is a Load Following Service, which is part of the CAISO regulator. As in most of the country’s products, aggregation is allowed. The remuneration is based on a capacity payment where CAISO, in accordance with clients, must agree when they have to offer the service. In turn, and depending on the agreement signed, they are notified in advance in the Day-Ahead Market (13:00), and in Real Time (based on the offer options): 2.5 min, 22.5 min, 52.5 min. The T

REC depends on the parameters of the resources used. Other relevant products of the electricity system have also been developed from different TSOs and DSOs in California. The Pacific Gas and Electric Company (PGE), Southern California Edison Company (SCE), and San Diego Gas and Electric Company (SDGE) have also specific programs used during critical periods of demand, contributing to load shifting.

3.2.2. Electric Reliability Council of Texas (ERCOT)

The Electric Reliability Council of Texas (ERCOT) has several DRP that participate in AS like Non-Spinning Reserve Services, Supplemental Reserve Services (Climate-sensitive, Non-climate-sensitive, and Load Resource), and Regulation Services [

56,

57]. Due to its climatic conditions and particularities, ERCOT has a different range of DRP regarding if they occur on a normal basis or under specific climatic conditions. The Non-Climate-sensitive products can be identified as Non-Spinning Reserve and Supplemental Reserve, which features a ΔP

min of 100 kW and a minimum reduction amount of 100 kW for both T

RAM options, 10 min or 30 min. Remuneration is in the form of security of supply, the T

MAX will last 12 h, and the period in which customers must offer the service will be established based on the service paid time [

58]. The Climate-sensitive products are similar to the previous ones, with the main differences that Climate-sensitive programs are used during the peak loads in summer and winter seasons, have a ΔP

min of 500 kW with a minimum reduction amount of 500 kW and a shorter T

MAX of 3 h. The Non-Spinning Reserve Service “Load Resource” has similar characteristics as the Non-Spinning Reserve/Non-Climate-sensitive service, with the differences that aggregation is not allowed, the T

MAX where the period in which customers must offer the service will be an agreed interval is shorter and the T

RAM is 10 min (Verbal), 30 cycles (Retransmission) [

59]. The Regulation Service does not allow aggregation, the remuneration will be in the form of security of supply, and the period in which customers must offer the service will be an agreed interval [

59].

3.2.3. New England Independent System Operator (NE-ISO)

The New England Independent System Operator (NE-ISO) spent many years designing the first installed capacity market in the country [

60]. With the adoption of the direct capacity market, DR could participate directly in the market, and two capacity programs were established: real-time demand response and real-time emergency generation. Real-time demand response refers to a reduction in energy use at an end-use customer’s facility, while Real-time Emergency Generation refers to a customer-controlled on-site generator, which has environmental permits that limit its operation to “emergency” hours when the system operator calls them to avoid lowering the load. The NE-ISO offers several programs that are active today. Regarding AS managed by the NE-ISO, Regulation Services are the main activity to handle demand flexibility, and they include seasonal and no seasonal products [

61]. The Regulation service products have a common ΔP

min of 100 kW, a minimum reduction amount of 1 kW. The period in which customers must offer the service could be seasonal and in peak hours, in summer between June and August (14:00 to 17:00) and in winter from December to January (18:00 to 19:00) or in summer between June and August and in winter from December to January, on non-holiday days. The notification of the action is defined by market regulators, which inform the members of the program some months or years in advance on when they must provide the service. Therefore, the contract includes a capacity payment on an annual basis [

62,

63].

3.2.4. Midcontinent Independent System Operator (MISO)

The Midcontinent Independent System Operator (MISO) is a TSO responsible for managing 180 GW of installed power to supply around 670 TWh of electricity to 42 million people each year [

64]. MISO distinguishes between two types of DRPV. Type I supplies a fixed reserve by load curtailment only, and it does not have generation resources. Type II supplies a continuous range of reserve through load curtailment or self-generation [

65]. Regarding AS managed by MISO, Regulation, Spinning Reserve, and Supplementary Reserve are all open to DR, with a common ΔP

min of 1 MW. Regulation is only open to DRPV type I and requires a very demanding T

RES (4 s). BSPs must respond automatically to deviations in frequency and provide both upwards and downwards reserve [

66]. Spinning Reserve and Supplementary Reserve are open to DRPV type I and type II. Any DRPV qualified for Regulation is qualified for Spinning Reserve too, and any DRPV qualified for Spinning Reserve is also qualified for Supplementary Reserve [

66]. This is due to the respective technical requirements of each service since Regulation is the most demanding while Supplementary Reserve is the least.

3.2.5. New York Independent System Operator (NYISO)

The New York Independent System Operator (NYISO) manages its Installed Capacity Market to guarantee the adequacy of the resources for its territory of a state with a maximum load of just over 33,000 MW [

67]. The operator of the New York Independent System (NYISO) offers four DR programs that could be identified as Spinning Reserve Service, Regulation Service, and two Supplemental Reserve Services [

68]. The DRPs of Spinning Reserve Service, the first Supplemental Reserve Service, and the Regulation Service have a ΔP

min of 1 MW, a minimum reduction amount of 1 MW. The remuneration is economic (based on the capacity provided) in the three programs, the action lasts the established interval (between NYISO and the agent), and the period in which the clients must offer the service is continuous. Prior notification is made in the Daily Market (11:00) and in real time (75 min, 5 min if Regulation Service). The second Supplemental Reserve Service has a ΔP

min of 100 kW (per zone), a minimum reduction amount of 100 kW (per zone). Remuneration is in the form of security of supply, the action will be during the window of action established by the program, and the period in which customers must offer the service will be seasonal. It is advisable to make a prior notification in the Daily Market, and a prior notice will be made on the day of the action (120 min) [

68]

3.2.6. Pennsylvania-New Jersey-Maryland Interconnection LLC (PJM)

The Pennsylvania-New Jersey-Maryland Interconnection LLC (PJM) manages a total of 13 states with more than 65 million people. It also has an installed generation capacity of 180 GW, and the total energy delivered in 2018 was 807 TWh [

69]. There are mainly three AS open to DR: Day-Ahead Scheduling Reserve, Synchronized Reserves, and Regulation, in which DRSs can provide up to 25%, 33%, and 25% of the total capacity, respectively [

70]. Day-Ahead Scheduling Reserve has the traits of Supplementary Reserve. In all cases, ΔP

min is very accessible (0.1 MW), but DRPVs must send information regarding their consumption every 1 min [

71]. Regarding Synchronized Reserves, DRPVs present bids in a Day-Ahead or in an Intraday market. In 2017, the average DR hourly capacity activated was 110 MW, from which 76% were industrial loads, while the participation of residential loads remained very limited. On the contrary, regulation, which activates as soon as possible, had a remarkable share of residential loads. 79% of DSRs in this service in 2017 came from water heaters, and 9% came from batteries. The average DR hourly capacity provided was 10 MW.

3.2.7. Canada—Independent Electricity System Operator (Ontario)

The Canadian State of Manitoba belongs to MISO’s electricity system, so all its programs and market rules apply in this State too. On the other hand, Alberta Electricity System Operator contracted 150 MW of DR in 2011 with Enel X, and now, a new advance on DR development as reserves is being contracted by Enel X on the basis of 10 to 60 min contracts with particulars through bids on the day ahead [

72]. Apart from Ontario, the rest of the States are still vertically regulated. Independent Electricity System Operator (IESO) launched the first Demand Response auction in 2015. Before that, IESO had secured up 70 MW of DR through a competitive procurement in which bids as small as 1 MW were accepted. The project intended to assess DSRs ability to provide ancillary services. The loads participated in one program [

73]. DRPVs commit to curtailing their loads on a day-ahead or four-hours ahead basis, acting like a Supplemental Reserve. IESO manages an annual DR auction in which DRPVs present bids with the capacity they are willing to provide for a defined period. DR offers are expressed in

$/MW month or year, and successful providers will receive a payment according to the capacity awarded and the resulting clearing price [

74].

3.3. Asia and Oceania

In Asia and Oceania, systems partially allow DR to access AS markets to compete with generation resources. Some TSOs adjusted the technical requirements of these services to match what DRPVs can do. But mostly, TSOs developed special programs only for DSRs, to assure DR participation in front of strong competitors or too demanding technical requirements. At the end of this Section,

Table 9 contains the main parameters that characterize Asia and Oceania AS for DR.

3.3.1. Australia

Australia has a highly branched and poorly meshed electrical network that suffers from imbalances that dramatically increase prices [

75]. One of the measures taken to carry a decentralization of energy production is to invest in flexibility to provide AS, which represents an opportunity to demand [

76]. The service that most concerns DR is the Frequency Control AS-, which Australian Energy Market Operator (AEMO) uses to maintain the adequate frequency of the electrical system. There are two types of frequency control in Australia: Regulatory and Contingency. The regulatory control of the frequency presents two programs whose objective is to correct slight drops and rises that may impair the optimal functioning of the system [

77]. As for contingency programs, two types exist depending on the ramp of action required by the action, and in FERC’s nomenclature, they would be identified as Regulating Reserves and Load Following Services.

3.3.2. New Zealand

New Zealand is another country that has been investing in the implantation of renewable energies and monitoring infrastructures [

78], and betting progressively on demand flexibility. The first projects were based in the residential sector, which is controlled through monitoring-controlled air conditioning, lighting, and certain household appliances during peak loads [

79]. The New Zealand Electricity Authority (NZEA) is the regulatory organization for the country’s electricity market and is, in turn, the promoter of different demand-side flexibility pilot projects. NZEA is currently working on defining AS and DR for the country due to the great number of renewable resources installed, which proves great potential for demand flexibility in New Zealand.

3.3.3. China

The State Electricity Regulatory Commission (SERC), together with the National Energy Commission (NEC), oversees promoting and implementing projects that provide greater demand flexibility, thus improving the potential of the electric system. Various demand management programs have been implemented by the Chinese government, which focus on administrative and technical measures. Pilot demand management programs have been carried out in four major cities in the country (Suzhou, Beijing, Foshan, and Tangshan) [

80]. These programs require an advanced measurement infrastructure (AMI) to measure baseline and consumption in real time and communication devices to inform users of Smart Demand Response (SDR) activities and analyze their reduction commitment [

81]. SDR refers to DR products managed automatically by the country’s large telematic infrastructure, which is adapted to the needs, prices, and system circumstances. The two most important SDR programs are the Interruptible Loads program and the Direct Load Control program. Both receive the same economic incentive in exchange for energy reduction. The mentioned programs can compare to FERC Supplemental Reserve Services standards.

3.3.4. South Korea

Currently, the effective DR program in Korea is not based on a system of offers but on contracts that decide the incentives, the participation interval, the notification time of the event, etc. However, a bid-based DR program was recently conducted but did not have a major impact [

82]. The need for a DSM program is becoming a major problem in Korea and is recognized as a necessary element to solve the demand problem [

83]. The load management programs implemented since 2009 in Korea use the regular KPX (Korean Power Exchange) fund bidding system and a voluntary reduction of the summer load, which KEPCO (Korean Electric Power Corporation) coordinates and carries out during the summer holiday period [

84]. Coordination of the summer vacation period is used to reduce peak summer demand; its objective is the residential client and the industrial client that surpasses a demand of 100 kW (ΔP

min) with an economic incentive. The Load Following Service reduces demand during peak summer afternoon hours are targeted to residential, industrial, and educational customers, who receive an economic incentive that is paid in 30 min rates (T

MAX) depending on the power provided. This system contributes to reducing maximum demand, but it will be more difficult to implement since industry labor regularity is more important than the decrease in the price of electricity in an advanced country. Through these satisfactory experiences, South Korea is willing to continue carrying out DR projects and demand flexibility.

3.3.5. Japan

The catastrophes that occurred in the country caused the nation to feel threatened by the serious lack of electricity supply. These events sparked the national debate regarding nuclear energy and the approach it should take in the future [

85], and one of the measures that were decided to tackle was to encourage the flexibility of the demand for a better insertion of renewable energies. A unique feature of the Japanese approach is the promising role of the business sector, as some of the large Japanese conglomerates such as Toyota, Mitsubishi, Sharp, Toshiba, Fujitsu, Panasonic, NEC Corporation, and Nissan Motors are involved in these projects. Notwithstanding the absence of defined DR programs, due to the massive industry trying to incorporate demand flexibility to their standards, there is great potential for DR in Japan. The main obstacle is found in the massive financing that the deployment of means that the creation of an intelligent network requires; this has been identified as a key barrier for DR [

86].

3.3.6. Singapore

The Singapore Energy Market Authority (EMA) is responsible for demand easing projects and introduced DR programs to improve competition in the Singapore National Electricity Market (NEMS). Consumers can participate directly or through DR retailers or aggregators. The Load Following Service establishes that all customers who can offer a ΔPmin of 0.1 MW for half an hour (TMÁX) can participate. Consumers participating in the program share a third of the savings from lowering electricity prices as incentive payments, up to the limit on wholesale electricity prices. Registered consumers can temporarily provide the required reduction by turning off non-critical equipment, reducing HVAC or pumping system power, or even using backup generators on-site for short periods.

3.4. Africa and Latin America

Africa and Latin America are also regions with a great DR potential, but DR programs have not yet been developed. Nevertheless, countries like South Africa are investigating and proving the viability of demand side management and the regulation of electricity demand from the consumer side [

87].

4. Discussion

As it is proved with the range of DR products from different continents presented in this review, many countries all over the world have developed and keep improving their programs to manage DSRs. DR is one of the elements which are going to characterize electricity markets shortly. A new perspective of decentralized systems, based on Renewable Energy, Distributed Energy Resources, Smart Grids, Virtual Power Plant, and Aggregators, is dominating the debate on how future electricity systems should be, and DR is an essential part of such scenario. The sooner and more efficiently DR is properly implemented in a system’s electricity market, the sooner its society will benefit from it, so it is recommendable for all regions to start working on programs like these shortly.

As it is stated in

Section 2.1, neighboring countries tend to have similar market designs when it comes to general services. Commonly they even create their nomenclature so that communication between such countries becomes easier and collaboration is more profitable. On the other hand, every TSO has its strategies to face particular issues of its country and, consequently, it designs specific DR products to manage them. For instance, Strategic Reserve in Finland is specially designed to face high winter demands, and Demand Turn Up in the UK is used in times of low demand and high renewable generation. These services are uncommon in other countries without such issues.

Regarding ΔPmin in AS programs open to DR, the most repeated value is 1 MW, especially in Europe. Other countries in Asia, America, and Oceania show ΔPmin of 0.1 MW in their programs, a more flexible requirement that facilitates DSRs participation on AS. Normally, aggregators can overcome a technical barrier such as this, but with ΔPmin of 20 or 25 MW (as found in Europe), even aggregators have difficulties meeting the requirements, and only the largest industrial consumers can access those services.

The search for DR products has revealed a pending global issue: the lack of standardization. TSOs from diverse parts of the world use different terms for similar concepts and design AS in a distinct way. Therefore, it often becomes hard to understand a description of a service from another part of the world. Besides, this fact can make it impossible to apply the same strategy to manage loads in two different countries because technical requirements may not be met in both places. Research shows that countries with standardization, such as European countries or the USA, tend to develop appropriate DR programs more quickly. Nevertheless, even if organizations like ENTSO-E and FERC have worked to develop a regional nomenclature accepted by all nearby countries, the standardization must become global to accelerate DR growth all over the world.

Regarding prices for the remuneration of AS provided by DSRs, the prices presented must be considered as an approximation since most of them vary continuously. All energy prices presented refer to upwards activations, that is, a curtailment of load or an increment of generation:

aFRR or Secondary Reserve. In services classified as aFRR, most of the European TSOs offer availability and an energy payment. Prices for the availability concept are around 18 €/MW/h (France), 13 €/MW/h (Finland), 22 €/MW/h (Switzerland) and even 200 €/MW/h (the UK). Prices for the energy concept are around 20–40 €/MWh (Finland), 70 €/MWh over the spot market price (the Netherlands), and 50 €/MWh (Switzerland).

mFRR or Tertiary Reserve. TSOs typically pay successful activations of mFRR and similar services with an energy payment only, although there are some exceptions. Prices found for the availability payment are around 5–6 €/MW/h (Belgium) and 3 €/MW/h (Finland). For the energy payment, average prices are around 47 €/MWh (France) and 41 €/MWh (Sweden). In Denmark and The Netherlands, the minimum price is the correspondent spot market price, and in the latter, there is an upper limit of 200 €/MWh.

RR or Complementary Reserve. As with the mFRR case, most TSOs pay this service with an energy payment only. Typical prices for the availability payment are around 2 €/MW/h (the UK) and 7 €/MW/h (Ireland), and for energy, the payment is around 45 €/MWh (France), 73 €/MWh (the UK), 75 €/MWh (Belgium) and between 380–950 €/MWh (Ireland).

Rewards tend to be more generous when the service is more demanding. That explains why aFRR normally has two payments, and mFRR and RR typically only have a utilization payment. Prices are also higher when technical requirements are tougher. Energy payments are especially common in Europe, while most DR services in other continents tend to apply for a capacity payment only. Security of supply is an interesting way to remunerate DR actions, although it would only apply to countries with weak and tricky networks, being an insufficient reward otherwise.

DR’s success and participation on AS are more common in services with high TRES, such as mFRR and equivalents, but consumers are getting involved in FCR and aFRR gently. In the USA most of the services characterized are equivalent to the spinning reserve, but there are also many products designed to be triggered immediately, probably due to the earlier use of DSRs to provide AS.

DR’s success is dependent on several factors, such as load traits (residential, industrial, and commercial), the share of renewables in a country’s electricity system, or generator competition. A key aspect results from the inclusion of residential consumers in DR programs, which are currently excluded from many markets such as Belgium. This will result from the integration and massification of aggregation services as a key element to untap the residential flexibility as it occurs in most USA systems and South Korea.

To improve the possibility of DR prosperity, all these factors must be analyzed before the design of products, and the conclusions of such analysis must be considered when establishing technical requirements and new market rules. Still, experience proves that some aspects are essential for a prosperous DR progress, such as low ΔPmin, and the acknowledgment of independent aggregators. Moreover, products’ impact on market efficiency and DR development must be tracked to introduce the changes needed.

5. Conclusions

To conclude, DR proves to be a valuable resource to ensure the security of supply while reducing demand peaks, avoid blackouts, reduce investments on the grid, and absorb renewable fluctuations. To do so, programs to allow and enhance the participation of DR in AS have been occurring throughout the globe. Many countries aim to mobilize their demand resources to provide reserves and directly compete with generation in AS markets. DR usage is still scarce, and, in most countries, its deployment is low or inexistent due to inexistent regulation, technical parameters drafted for generators, and lack of experience. Even though most countries follow regional grid standards, where DR programs for AS exist, these do not follow common parameters and lack standardization due to the different parameters involved as a DRPV. In this regard, no analysis or comparison appears in the literature of the different parameters and prices of DRP in AS among different countries.

The contribution of this work is to provide an academic, precise, and concise analysis of the different country programs under a framework of standardized parameters of both AS and DRP. First, the paper has defined the grid standards developed by ENTSO-E and the FERC, the AS associated with them, and their main technical characteristics. Second, we have presented the DRP existing in the different countries and systems around the world that have incorporated DRP in their AS. The programs are presented systematically with their main characteristics such as the minimum response time, the type of payment and activation form, minimum and maximum times, minimum power required to participate, and if aggregation is allowed or not. Third, a review of the average and most common prices and forms of payment and the main policy conclusions around the programs are presented. Our work shows how countries with wider participation have lower minimum power levels and allow aggregation. It is important to note that higher penetrations of renewables, the electrification of demand, and more extreme climate conditions associated with the effects of climate change will impose extra needs on the system, to which DR results in a valuable resource to help to balance it.

{kind=link}

{kind=link}

{kind=link}

{kind=link}