Impact of Carbon Tax Increase on Product Prices in Japan

1

College of Policy Science, Ritsumeikan University, Ibaraki 567-8570, Japan

2

Sustainable Management Promotion Organization (SuMPO), Tokyo 101-0044, Japan

*

Author to whom correspondence should be addressed.

Energies 2021, 14(7), 1986; https://doi.org/10.3390/en14071986

Submission received: 19 March 2021

/

Revised: 1 April 2021

/

Accepted: 1 April 2021

/

Published: 2 April 2021

(This article belongs to the Special Issue Energy Policy for a Sustainable Economic Growth)

Abstract

:The introduction or strengthening of a carbon tax is being considered in many countries as an economic policy instrument to reduce greenhouse gas (GHG) emissions. However, there is no study analyzing the impact of a carbon tax increase in a uniform method for various products, reflecting the energy taxes and exemptions. Therefore, this study analyzes the price changes of products associated with the introduction of a stronger carbon tax, using Japan as an example. A process-based life cycle assessment database was used to enable a detailed product-level analysis. Five scenarios with different taxation amounts and methods were analyzed. The results show that price changes vary greatly by industry sector and product, even within the same industry sector. For example, seasonal vegetables and recycled plastics are less affected by carbon tax increases. Imported products, such as primary aluminum, are not affected by the Japanese carbon tax change, indicating a risk of carbon leakage. If GHGs other than CO2 are also taxed, the price of CH4 and N2O emitting products, such as rice and beef, would rise significantly. The method presented in this paper enables companies to assume price changes in procured products due to carbon taxes and policymakers to analyze the impact of such taxes on products.

1. Introduction

To decarbonize society, economic policy measures, carbon taxes, and fuel taxes have been introduced in many parts of the world [1]. These carbon and fuel taxes have been shown to be effective in reducing CO2 emissions in various countries, such as Canada [2], France [2], Netherland [3,4], Finland [4], and Sweden [2,4,5]. Furthermore, He et al., (2019) [6] indicated that these taxes have reduced CO2 emissions and fossil fuel use in Nordic countries and the G7 countries in the long run. Nadirov et al., (2020) [7] clarified that increasing carbon taxes affects consumer behavior, resulting in a significant shift from petrol to diesel fuel vehicles in 17 countries. Product price changes associated with the introduction of carbon taxes and the associated impacts on households have been studied in various countries, including the United States [8], Japan [9,10,11], France [12], and Thailand [13]. Studies using multi-region input–output tables (MRIOs) clarified that the impact of carbon pricing on households varies according to the income level of a country [14,15]. Therefore, it is important to appropriately recycle carbon tax revenues considering the country’s characteristics [16].

Economic models, such as input–output tables [9,10,13,14] and the computable general equilibrium (CGE) model [17], are used for analyzing the impact of the introduction of a carbon tax policy in advance. For example, Sugino (2021) [10] analyzed the effects of carbon policies that increase the effective carbon rate to the EUR 30 threshold using the Japanese input–output table.

In order to mitigate the impact of carbon taxes on internationally competitive products, for example, a mechanism to rebate the taxes at the time of export has been discussed [1]. For this purpose, it is necessary to clarify the cumulative tax amount for various products in a reasonable method. However, while existing methods can comprehensively analyze the entire economy, it is difficult to conduct a detailed product-level analysis because the granularity of the analysis is limited to statistical classification.

Life cycle assessment (LCA) is a technique for assessing the environmental impact of a product over its life cycle, which is defined in ISO14040:2006 [18]. It is used by companies to develop environmentally conscious products, communicate product environmental performance [19], and by governments to formulate environmental policies [20]. When a company or other organization conducts LCA of its products, the input–output table created from the statistics is used for screening purposes. By assigning the purchase amounts of materials to the relevant sector in the Input–Output table, the cumulative environmental impact of the entire supply chain can be estimated. However, for a detailed product assessment, process-based LCA databases, such as ecoinvent [21] and the inventory database for environmental analysis (IDEA) [22], are commonly used. For example, Japan’s Input–Output table has 400 categories, but IDEA has data in 4700 categories. A process-based LCA database expresses the connections between processes, mostly using physical flows. It is necessary to use a database that reflects the characteristics of materials and energy for product-level assessments.

If the carbon tax is simply proportional to CO2 emissions, the impact of this carbon tax can be calculated by extracting the amount of CO2 emissions from the LCA results and multiplying it by the assumed carbon price. In addition to greenhouse gas (GHG) cases [23,24,25], there are other cases where environmental impacts other than GHG are converted to monetary values [26,27,28,29] using this method.

However, in reality, there are taxes other than carbon taxes. Taxes based on carbon emissions are called explicit carbon taxes, whereas others are called implicit carbon taxes. Implicit carbon taxes include fuel excise taxes and electricity taxes, which have been introduced in many countries and collect much more taxes than carbon taxes [30]. In addition, there are tax exemptions and refunds for specific industries and products (goods and services). However, no product-level analysis has been conducted using a process-based database to reflect the actual state of existing energy taxations and tax exemptions.

Therefore, the purpose of this study is to propose and demonstrate a method to analyze the impact of a stronger carbon tax at the product level. This study focuses on Japan as a case study. In Japan, most energy taxes are fuel taxes. The Special Taxation for Climate Change Mitigation (hereinafter referred to as carbon tax), which is a tax based on the carbon content of fuel, was introduced in 2012, but it only accounts for a small percentage of the tax revenue from energy taxation [30]. However, in October of 2020, Japan’s prime minister declared that Japan will reduce GHG emissions to net zero by 2050, and the introduction of stronger policies for GHG reduction is under consideration. Therefore, each stakeholder needs information about the impact of the carbon tax increase on the products they are involved in.

Section 2 presents the status of energy taxes, including the carbon tax in Japan and the analysis method of this study. The results of the analysis at the industry level and at the product level are presented in Section 3. Section 4 discusses both the results of this analysis and the analysis method. Section 5 summarizes the conclusions.

2. Materials and Methods

2.1. Energy Tax in Japan

In the FY2020 budget, Japan predicted the collection of approximately JPY 4.455 trillion for energy taxation. This accounts for 4.14% of the JPY 107.56 trillion national budget, making it a significant revenue source. An overview of energy taxation is provided in Table 1. Of the energy taxes, gasoline tax (JPY 53.8/L) has the largest tax revenue. The diesel oil delivery tax (JPY 32.1/L) follows this tax. The oil and gas tax (JPY 17.5/kg) is imposed on liquefied petroleum gas (LPG) used by vehicles. These three taxes are used as general revenue sources. The aviation fuel tax is levied at JPY 18.0/L and is used for airport maintenance.

The tax revenue from petroleum and coal taxes is JPY 655 billion. Within the petroleum and coal tax, the carbon tax is proportional to the carbon content of the fuel. The amount of the carbon tax is JPY 289/t-CO2. For example, the petroleum and coal taxes on coal are JPY 1370/t-coal, of which JPY 670 are equivalent to the carbon tax. The electric power development promotion tax (hereafter referred to as electricity tax) accounts for JPY 315 billion in tax revenue. This tax is levied on electricity sold at a rate of JPY 0.375 /kWh. This tax is used as a measure to promote the location of power sources, power utilization, and nuclear safety regulations.

There are industries and products that are subject to additional taxation or exemptions from taxation for a limited period. These are complex and are often extended. For example, the exemption of the petroleum and coal tax on coal for the steel and cement manufacturing industry was a time-limited measure until March 2013, but it was revised to a “temporary” measure with no fixed date of application. Therefore, this study analyzed the present tax status as of January 2021, including temporary measures.

For these energy taxes, tax exemptions and refunds are provided for various uses and industries. Table 2 shows the tax exemptions and refunds considered in this study. For example, naphtha (for manufacturing petrochemical products, such as plastics) is exempted from petroleum and coal taxes. Furthermore, there is no taxation on the energy consumed abroad for imported products. Therefore, no taxation is associated with the energy consumption in processes carried out abroad.

2.2. Database Creation

In this study, LCA [18] was adopted to analyze the price change of products. A process-based LCA database shows materials, energy consumption, and GHG emissions at the product level. Therefore, in this study, a process-based LCA database was used for the analysis. We used IDEA ver. 2.3 [22], the most comprehensive process-based LCA database in Japan. It compiles data on more than 4200 products. Since IDEA ver. 2.3 also has unit price information for more than 2700 products, we analyzed price changes according to the tax policy change.

For each unit process in IDEA ver. 2.3, the tax amount shown in Table 1 was entered as the elementary flow for each energy input of the processes. The tax exemptions and refunds shown in Table 2 were also entered as elementary flows. For example, petroleum and coal taxes on coal for coke production are exempted from taxation. Therefore, the same amount of the elementary flow of taxation and the elementary flow of tax exemption were entered, so that it could be analyzed when the tax exemption was finished.

The tax exemption for the caustic soda industry was applied not only to the caustic soda production process but also to the production process of chlorine, which is a co-product of the caustic soda production. Since the processes with co-products were divided into several processes for representing one output product from one process in IDEA, therefore, this study considered the physical characteristics of these processes in setting the tax exemption/refund.

For energies consumed abroad, an elementary flow indicating tax exclusion was entered; a list of these flows (newly entered into the IDEA database) is shown in Table 3. Since taxation flows were only entered in the energy conversion process, the number of applicable processes was small. In contrast, the number of tax exemption/refund flows and tax exclusion flows was large because there were many applicable processes.

There are other so-called environmental taxes. For example, the automobile tax generated when purchasing a car is reduced according to the fuel economy measured by the official standard. However, although IDEA ver. 2.3 has datasets on automobiles of different sizes and loading rates, there are no datasets for automobiles with different fuel economies. Those differences are not taken into account in the processes of using automobiles. Therefore, taxes and tax reductions on equipment were excluded from this analysis. We also excluded taxes that were uniformly imposed, such as a consumption tax. This is because all products are taxed in the same way, regardless of the environmental performance. After entering the elementary flows of each tax into each process of the LCA database IDEA, the cumulative amount of tax in the entire supply chain was calculated using the LCA software MiLCA ver. 2.2 [32].

2.3. Scenarios

Japan’s carbon tax is relatively low compared to that of other Organisation for Economic Co-operation and Development (OECD) member countries [1]. The Ministry of the Environment of Japan launched a subcommittee on carbon pricing and considered strengthening the carbon tax [31]. However, no concrete plan has been presented for the height of the carbon tax or other energy taxes. Therefore, in addition to the present situation, this study set up five taxation scenarios and analyzed their impact on product prices (Table 4).

Dividing the total amount of energy taxation in 2018 (JPY 4621 billion) by the domestic CO2 emissions from energy sources (1183 million t-CO2) [33], JPY 3906/t-CO2 was calculated. To maintain the same level of tax revenues at the present level, approximately JPY 5000/t-CO2 would be needed, taking into account tax reductions for specific industries and products. The social cost of CO2 was calculated as USD 42/t-CO2 at a discount rate of 3% [34], and JPY 5000/t was close to that value. Therefore, in Scenario 1, we assumed that all present energy taxes were replaced by a carbon tax of JPY 5000/t-CO2.

As mentioned earlier, many industries and products in Japan are exempted from energy taxation. Therefore, Scenario 2 is a case in which industries and products that are subject to a domestic tax exemption/refund are eliminated.

It was suggested that an explicit carbon price of USD 50-100/t-CO2 is needed by 2030 to achieve the goals of the Paris Agreement [35]. Therefore, the case in which the carbon tax is increased from JPY 289/t-CO2 to JPY 5000/t-CO2, while retaining the existing energy taxation, was considered as Scenario 3.

GHGs are emitted from sources other than those currently taxed. For example, in livestock farming, CH4 is emitted during the digestion process of cattle. Dichloromethane, which is used as a cleaning agent for metal products, is a GHG that is released into the atmosphere from various industrial processes. Scenario 4 is a case in which the same carbon tax is imposed on GHGs other than CO2. Each GHG was converted to CO2 equivalents using the 100-year global warming potential (GWP) index [36]. Biomass-derived CO2 was excluded because it was considered carbon-neutral.

The International Energy Agency developed a future scenario called the sustainable development scenario to achieve the 2050 target set by the Paris Agreement [37]. In this scenario, advanced economies, including Japan, need a CO2 price of USD 140 by 2040. It has also been reported that bioenergy for aviation fuel requires a carbon price of USD 150/t-CO2 to be competitive [38]. Similarly, it has been reported that even USD 150/t-CO2 is insufficient for steelmaking by hydrogen reduction to be competitive when the price of electricity is USD 60/MWh or higher [38]. It was also reported that to reduce GHG emissions by 80% by 2050, the price needs to rise to USD 40-150 by 2050 [39]. Therefore, we set Scenario 5 as the case in which the carbon tax is added to the existing energy taxation and the carbon tax is set at JPY 10,000/t.

3. Results

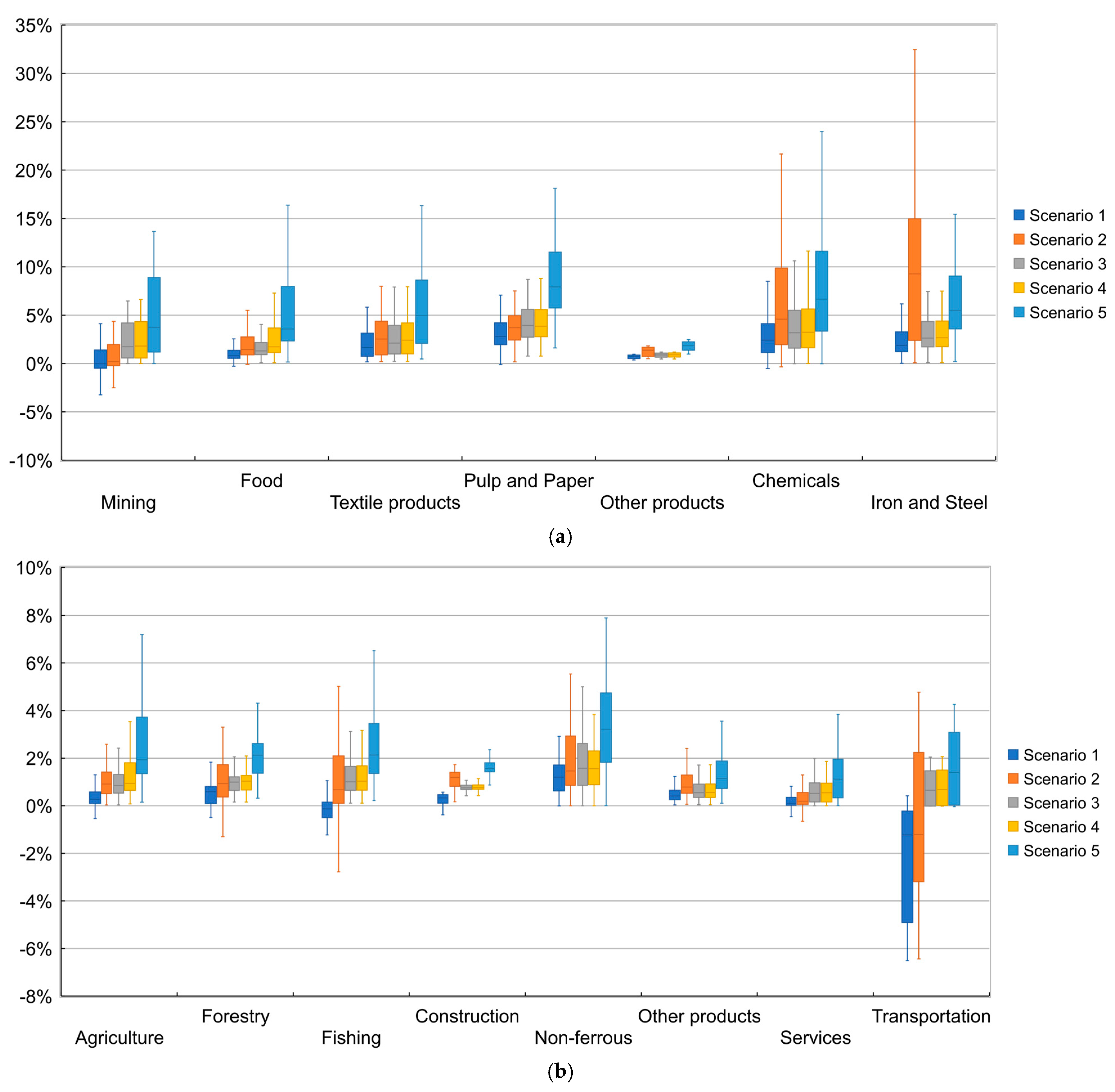

The price changes for each product, by scenario, are shown in Figure 1. This is the result of the unit price of each product included in the IDEA database and is not weighted by the production volume of each product. For this reason, it is different in character from the average when analyzed on an industry sector basis. To calculate price changes, calculation results without unit price data were excluded from Figure 1. In reality, it is not always the case that all increases in product manufacturing costs are directly reflected in prices. However, in this study, all price changes were assumed to be reflected in product prices.

The prices generally increased as compared to the present situation in each scenario. However, some products became cheaper in Scenarios 1 and 2, particularly in the fisheries and transportation sectors. The elimination of the gasoline tax and diesel oil delivery tax in Scenario 1 resulted in lower prices in the transportation (median −1.2%) and fisheries sectors (median −0.1%).

Scenario 2 eliminates tax exemptions and refunds for certain industries, so the price increases were large in the iron and steel (median 9.3%) and chemicals (median 4.6%) sectors, which benefited the most from tax exemptions and refunds. Agriculture, forestry, and fisheries sectors also lost their tax exemptions and refunds, but this was offset to some extent by the effect of lower gasoline and diesel delivery taxes. Although direct comparisons cannot be made due to differences in carbon tax prices and assumptions, these trends were similar to those reported in a previous study [11].

In Scenario 3, the carbon tax is increased from JPY 289/t-CO2 to JPY 5000/t-CO2, while leaving the existing energy taxation in place. The results showed that all sectors showed an increasing trend, but there were relatively large price increases in pulp and paper (median: 3.9%), chemicals (median: 3.2%), iron and steel (median: 2.6%), textiles (median: 2.1%), and mining (median: 1.8%). On the other hand, price increases in agriculture, forestry, fisheries, construction, other products, and the service sector were less pronounced.

In Scenario 4, all GHGs are taxed. Compared to the results of Scenario 3, only the agriculture (median: from 0.8% to 0.9%) and food (median: from 1.3% to 1.7%) sectors showed an upward trend, while the other sectors did not differ significantly in prices. The increase in the value of the food sector is attributed to the agricultural sector. There was also a slight increase in the textile and chemical sectors.

In Scenario 5 the carbon tax is increased to JPY 10,000/t-CO2. Price increases were seen in many sectors, with the largest increases in pulp and paper (median: 7.9%), chemicals (median: 6.7%), iron and steel (median: 5.5%), and textiles (median 5.0%). Mining (median: 3.7%) and food (median: 3.6%) also experienced relatively large increases. There was a wide range of changes in the amount of taxation on products in the same sectors. The following section provides a detailed analysis of products in key industries.

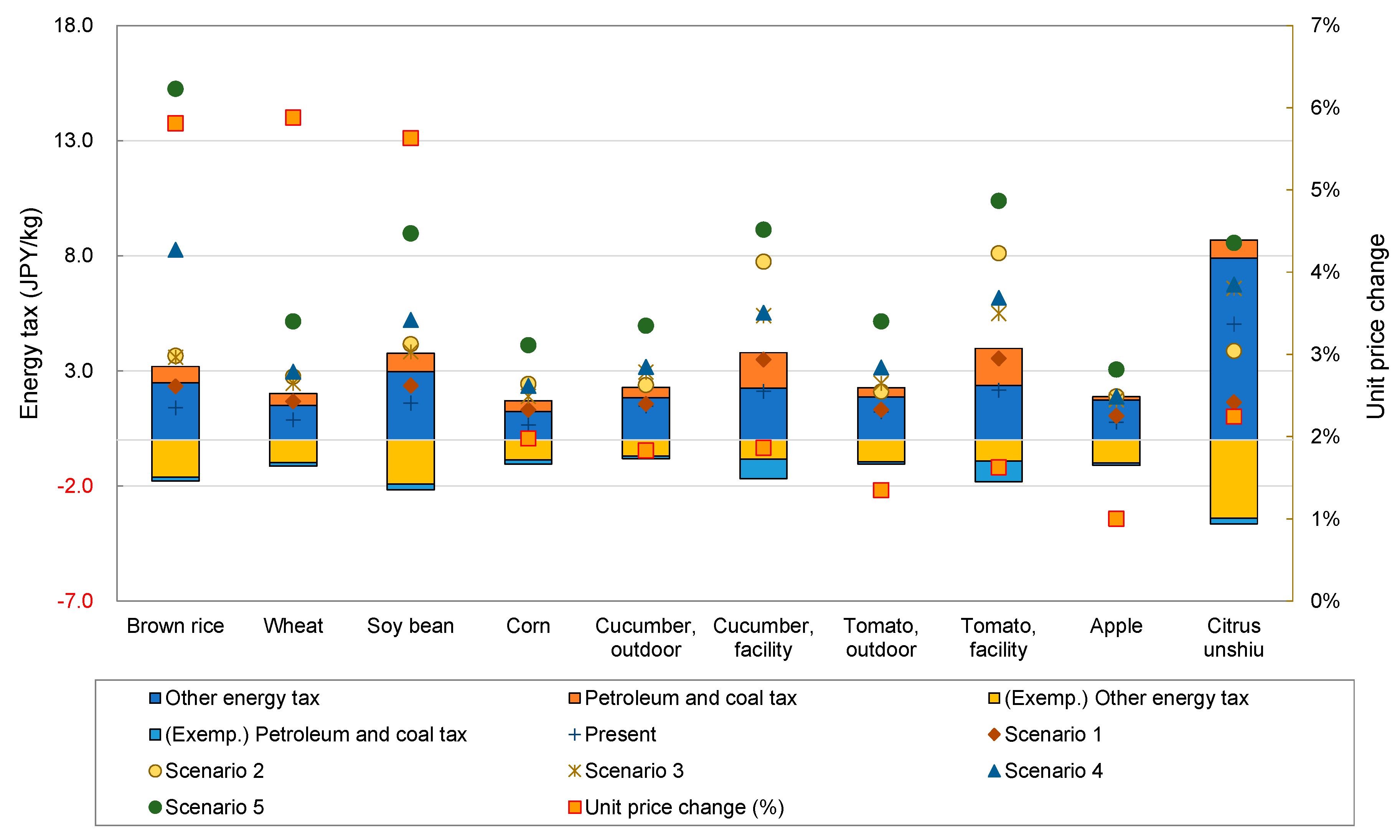

3.1. Agriculture

The results of the analysis of the tax amount per kilogram of product for major grains, vegetables, and fruits are shown in Figure 2. The bar graph in Figure 2 shows a breakdown of the present tax amount. Almost all other energy taxes (mainly gasoline tax and diesel oil delivery tax), both taxable and exempted, accounted for the majority of the tax.

The present tax rate for brown rice is JPY 1.4/kg, but in Scenario 4, where all GHGs are taxed, the tax rate increased significantly to JPY 8.3/kg (a 2.9% increase in the unit price of the product). This is due to the taxation of CH4 generated from rice paddies. Under Scenario 5, which further increased the carbon tax to JPY 10,000/t-CO2, the tax for brown rice was JPY 15.2/kg and increased the product price by 5.8%. In Scenario 5, the product unit prices for wheat and soybeans were 5.9% and 5.6%, respectively.

For vegetables, different results were obtained depending on the cultivation method used. The present tax rate for cucumbers grown outdoors was JPY 1.5/kg, and in Scenario 5, it increased to JPY 5.0/kg. The current tax rate for cucumbers grown in facilities was JPY 2.1/kg, and in Scenario 5, the rate was JPY 9.1/kg. The tax on cucumbers cultivated outdoors increased by JPY 3.5/kg, while the tax on cucumbers cultivated in facilities increased by JPY 7.0/kg. However, due to the higher unit price of facility cultivation, the rate of the price change was approximately 1.8% for both. A similar trend was observed for tomatoes. These vegetables are generally grown outdoors during the summer season and in facilities during other seasons, and fuel is used for heating.

Apples and Citrus unshiu are examples of fruits. For apples, the total amount of energy taxation was relatively low at JPY 3.1/kg in Scenario 5, and the rate of change in the product price was low at 1.0%. Citrus unshiu consumes a large amount of diesel oil; in Scenarios 2 and 3, when the carbon tax was fully implemented, the tax amount was lower than the present amount because the diesel oil delivery tax was eliminated. However, in Scenario 5, the tax was JPY 8.6/kg, and the rate of change in product prices increased by as much as 2.2%.

3.2. Livestock

The amount of energy tax per kilogram of livestock body weight is shown in Figure 3. The current tax rate for beef cattle was JPY 5.1/kg, but it increased to JPY 16.4/kg (1.4% increase in unit price) in Scenario 3, JPY 63.2/kg (7.3%) in Scenario 4, and JPY 122/kg (14.8%) in Scenario 5. In particular, the impact of CH4 from the digestion process and livestock manure treatment contributed significantly to these increases. For eggs, broilers, and pigs, the rate of change in product prices due to the introduction of Scenario 5 was 6.8–7.9%, while for beef cattle, it was 14.8%. The unit price of beef products was higher than that of eggs, broilers, and pigs, and this was a significant price increase.

3.3. Energy

The change in the tax amount per MJ of major energy sources is shown in Figure 4. Note that the electricity values were apparently higher because of the generation efficiency considered. Presently, gasoline, diesel oil, and aviation fuels have high tax rates. In Scenario 2, which eliminated energy taxes and unified them with the carbon tax, the amount of tax for each energy type, except for electricity, was almost the same. In Scenario 5, where the existing taxes were retained and the carbon tax was set at JPY 10,000/t, gasoline continued to have the highest tax due to the high rate of gasoline tax. Except for Scenario 2, coal for coke was the least expensive tax rate because it was exempted from taxes.

The product price of fuel coal increased by 197% in Scenario 5, owing to the low product unit price. Diesel oil, aviation fuel, and gasoline prices rose significantly compared to products in other sectors by 43.8%, 44.5%, and 24.0%, respectively. Electricity saw an 8.4% increase in the product price.

3.4. Plastics

The tax changes in the major plastic materials are shown in Figure 5. In this figure, the results are shown for common plastics such as polyethylene (PE), polystyrene (PS), and polyethylene terephthalate (PET) as well as for engineering plastics, such as polycarbonate (PC) and fluororesin. The results for the major recycled plastics are also presented. Since the market price of recycled plastics is uncertain, the price was calculated to be half that of primary plastics.

Naphtha, the raw material for plastics, was exempted from petroleum and coal taxes. In Scenario 2, which eliminated the tax exemption, PE, PS, and PET had the highest taxes at JPY 24.7/kg, 27.3 JPY/kg, and JPY 28.1/kg, respectively, while PC had the highest tax in Scenario 5 (JPY 69.4/kg) due to its high energy consumption during manufacturing.

Fluororesin contains fluorine in its molecular structure, but due to the high fossil fuel consumption in the production process, the price was JPY 151.7/kg in Scenario 5. Due to the high unit price of the product, the price change was small at 6.1%. In contrast, the price of PC, another engineering plastic, increased by 18.8%.

When comparing PET and recycled PET, the tax amount was smaller for recycled PET in all scenarios. PE is a type of polyolefin, and recycled polyolefin pellets are made from PE. The difference in the tax amount between primary PE and recycled PE increased from JPY 0.6/kg in the present to JPY 5.6/kg in Scenario 5. The same trend was observed for PS, with an increase from JPY 1.2/kg to JPY 8.5/kg.

3.5. Other Materials

The changes in the taxes of the other major materials are shown in Figure 6. The results are shown for crude steel from blast furnaces, which are mainly made from iron ore, and crude steel from electric furnaces, which are mainly made from scrap. At present, the tax amount for both blast furnace steel and electric furnace steel was not more than JPY 1.0/kg because coal used for steel production was exempted from petroleum and coal taxes. In Scenario 2, in which the exemption was eliminated, the amount of tax was increased to JPY 11.4/kg for blast furnace steel and JPY 2.0/kg for electric furnace steel. In Scenario 5, which retained the tax exemption and set the carbon tax rate at JPY 10,000/t-CO2, the tax rates were JPY 2.6/kg for blast furnace steel and JPY 2.4/kg for electric furnace steel, respectively. The rate of increase in product prices was 3.3% for blast furnace steel and 3.0% for electric furnace steel; thus, there was no significant difference.

There are two types of aluminum: primary aluminum, which is produced from bauxite, and secondary aluminum, which is made from scrap. The production of primary aluminum consumes large amounts of electricity. The last primary aluminum production plant in Japan was closed at the end of March 2014, and Japan is now entirely dependent on imports. Therefore, all GHGs from primary aluminum production processes is emitted overseas and were not subject to a carbon tax. The tax amount of primary aluminum was JPY 0.0/kg, but the tax amount of secondary aluminum in Scenario 5 was JPY 10.9/kg, which increased the product price by 4.1%.

Comparing kraft pulp made from wood, the raw material for paper, and recycled paper pulp made from used paper, the tax amount was lower for recycled paper pulp in all scenarios. The increase in the product price was also lower for recycled paper pulp at 5.7% compared to 11.8% for kraft pulp in Scenario 5.

3.6. Transportation

The change in tax per tonne-kilometer (tkm) for major types of freight transports is shown in Figure 7. At present, the highest tax amount was levied on domestic air transport (JPY 11.2/tkm), mainly because of the aviation fuel tax. This was followed by truck transportation (JPY 1.9/tkm), which is mainly subject to the diesel oil delivery tax.

In Scenarios 1 and 2, where the diesel oil delivery tax was eliminated and the shift to a carbon tax was made, the tax amount for truck transportation was decreased, but in the other scenarios, it was increased. For example, in Scenario 5, the increase in the carbon tax was larger than the decrease in the diesel fuel delivery tax, and the tax for truck transportation increased to JPY 3.3/tkm from JPY 1.9/tkm in the present.

A similar trend was observed for the amount of taxes on domestic air transportation. In Scenario 1, aviation fuel on regular domestic routes was exempted from the carbon tax, making it lower. In Scenario 2, where aviation was no longer exempted from the tax, the tax increased to JPY 7.4/tkm, but was still lower than the present price because the aviation fuel tax was eliminated. In Scenario 5, price changes were small for both coastal transportation and air transportation, although they were not zero because of the impact during fuel production. Railway transport increased in price by 3.5% in Scenario 5, owing to higher electricity prices.

3.7. Services

The change in the tax per yen for some service activities is shown in Figure 8. For each service, the tax amount increased as the carbon tax increased. In particular, the tax on bathhouse services increased from JPY 0.01/JPY to JPY 0.07/JPY in Scenario 5. This is equivalent to a 5.9% increase in the price of services. Many bathhouse sites use fossil fuels for their boilers, so they are susceptible to the carbon tax hike. On the other hand, hairdressing and advertising, which are high value-added services, were less affected by the carbon tax hike, and in Scenario 5, the service price increase was only 1.4% and 1.8%, respectively.

4. Discussion

A carbon tax is an economic policy instrument that encourages low-carbon consumption behavior through prices. In the example of cucumbers and tomatoes, the rate of change in product prices was about the same for outdoor cultivation and facility cultivation, but the price increase for facility cultivation was larger. Therefore, by making seasonal vegetables relatively cheaper, it is expected to encourage the consumption and production of seasonal vegetables. In the case of meat consumption, the price increase range for beef was also larger than that for pork and chicken, and this is expected to encourage a change in consumption behavior. Beef has significant environmental impacts, such as water consumption in addition to climate change, and shifting to chicken and plant-based diets can reduce environmental impacts [40].

However, the rate of the price increase for grains tended to be higher than that of vegetables and fruits, by more than 5%. Since grains are a necessity for daily life, the impact on household budgets needs to be carefully analyzed when increasing the carbon tax. Similarly, energy, such as electricity and gasoline, is another necessity for life. Changes in energy prices are generally large, and in Scenario 5, electricity and gasoline prices were calculated to increase by 8.4% and 24.0%, respectively. When prices rise, people will use other products that can be substituted, or they will not purchase them, which will reduce demand. It is known that a decrease in demand due to price hikes or price elasticity is lower for necessities [41]. Since rising food and energy prices cause regressivity, some kind of countermeasure using tax revenues would be necessary.

For plastics, steel, and paper, the carbon tax increase for recycled materials was found to be less than that for primary materials. Although the quality of recycled materials may deteriorate due to impurities, the economic incentive to use recycled materials is considered to be stronger.

Because primary aluminum was imported from overseas, the impact of the carbon tax hike was more apparent in secondary aluminum, and it made more incentive to use primary aluminum on the market. It was pointed out that the introduction of a carbon tax leads to carbon leakage, which will increase production activities overseas that are not subject to taxes. Carbon leakage is an unintended policy consequence of the introduction of carbon taxes. It is recommended that carbon leakage should be considered when strengthening the carbon tax. This is especially true in Japan, where all primary aluminum is imported, but similar caution is needed for other products. The introduction of a border carbon adjustment has been proposed as a countermeasure, but there are issues in its introduction, such as setting an appropriate tax amount and ensuring consistency with international trade rules [42].

4.1. Scenarios

In Scenario 1, all existing energy taxes were shifted to a carbon tax, while maintaining present tax revenues, resulting in the decrease in the price of some products, especially in the transportation sector, where the present tax per carbon was high. In many countries, it is common to heavily tax gasoline and diesel oil for road transport [30], and the same is true if a similar policy is adopted in these countries. Gasoline tax, aviation fuel tax, and electricity tax are all taxes with fixed purposes for spending, but they were eliminated in Scenario 1. Therefore, it is necessary to expand the use of the current carbon tax and allocate it to, for example, public work for airports and measures for nuclear safety regulation. In addition, since a portion of the gasoline tax (JPY 236 billion in 2020 FY budget) is a general fund of local governments, it is necessary to transfer a portion of the carbon tax to local governments.

Scenario 2 analyzed the impact of tax exemptions and refunds. Sugino (2021) [10] does not take tax exemptions/refunds into account and is, therefore, similar to this scenario. This study [10] left out energy tax and used the Input–Output table, so it is not possible to compare the figures due to different assumptions, but the results are the same, in that a large price increase is expected in the steel and plastic sectors. Tax exemptions and refunds are provided mainly to the steel and petrochemical industries, which are exposed to international competition. If these were to be eliminated, prices would rise significantly (iron and steel, median 9.3%; chemicals, median 4.6%). Energy tax is exempted or reduced for specific industries and products in many countries; however, some countries, such as Norway and Sweden, are gradually reducing their exemptions [1]. In Japan, it is recommended to promote the development of low-carbon technologies, such as the steelmaking process by hydrogen reduction and the domestic recycling of plastics.

Scenario 3 assumes the values discussed as the tax amount around 2030 [35]. It was found that even with the tax exemption remaining for specific industries and products, product price increases of several percent still occurred, especially in the materials industry. In addition, it is necessary to pay attention to carbon leakage, which was more pronounced in Scenario 5.

In Scenario 4, a carbon tax was imposed on all GHGs. There is a precedent for the introduction of such a policy. For example, Iceland started taxing F-gas emissions in 2020 [1]. In Japan, businesses are required to report the amount of GHG emissions to the government by the Act on Promotion of Global Warming Countermeasures. However, there are some cases, such as CH4 emissions from rice paddies, where it is difficult to measure the entire amount of such GHGs. The industries that will be mainly affected by introducing this policy are agriculture and the food sector. In particular, rice, the staple food of Japanese people, is expected to increase in price. If this policy is introduced, it is necessary to use a uniform coefficient for the tax calculation or to narrow down the scope of industries because impacts on households are expected to be large [41].

Scenario 5 was calculated with the value discussed as the possibility of taxation in the medium to long term. The range of price increases for each product and service was larger than that in Scenario 4. Although it would be difficult to introduce such a tax rate at present, as the decarbonization of the society progresses, tax revenues are expected to gradually decrease under the present tax rate. Therefore, even if a higher tax is introduced, its impact on the society will be mitigated. However, if a society with net zero GHG emissions is realized, tax revenues in Scenario 5 will also decrease significantly, and other sources of revenue will need to be considered to maintain tax revenues.

4.2. Comparison with GHG Emissions

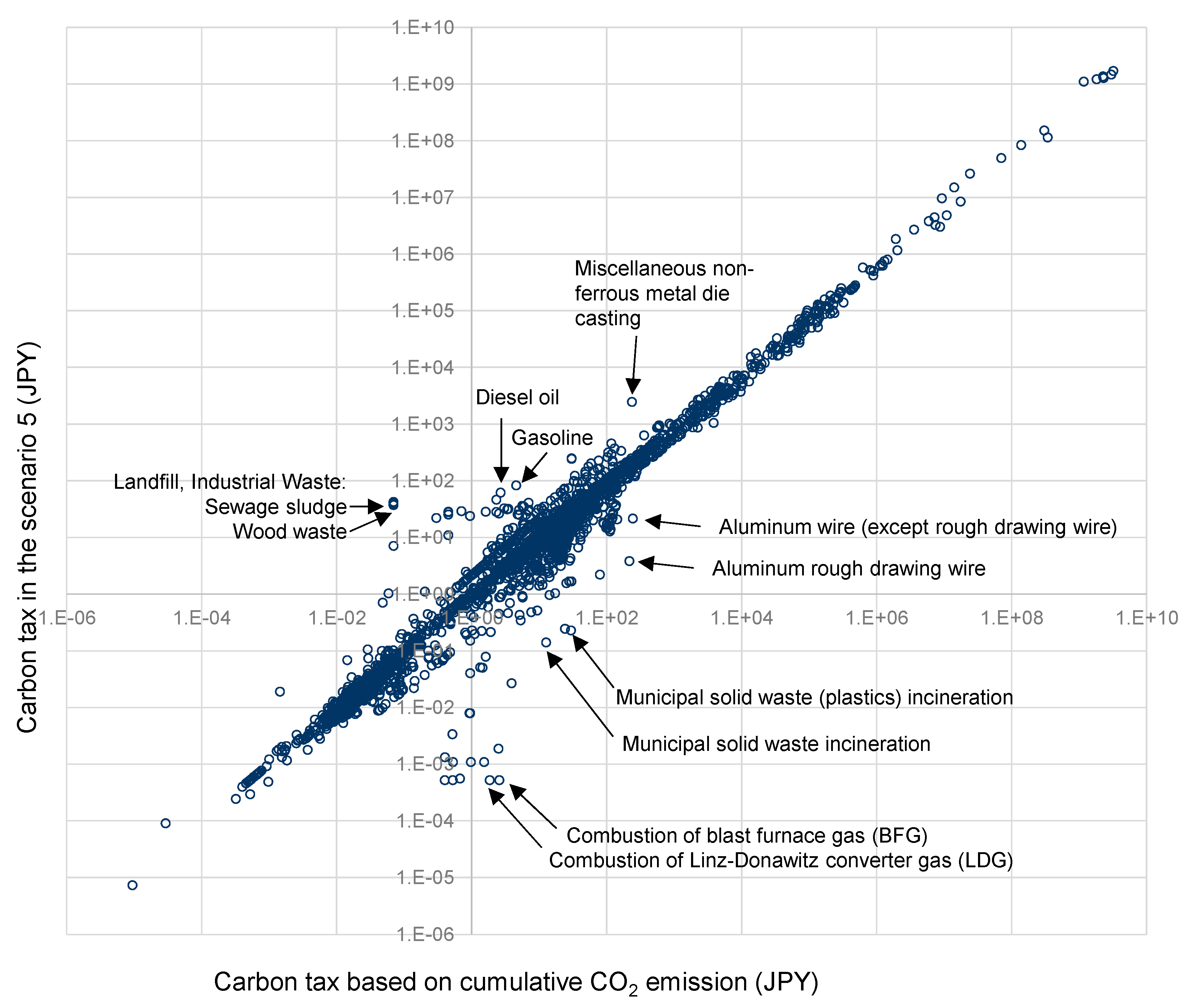

Figure 9 plots the hypothetical tax amount calculated by imposing a carbon tax of JPY 10,000/t-CO2 on the cumulative CO2 emissions of the products included in IDEA ver. 2.3, and the calculation results of the tax amount in Scenario 5. The cumulative CO2 emission is the total amount of CO2 emitted until the product is provided. The results of the calculations for CO2 emissions and Scenario 5 show almost the same trend, with a correlation coefficient of 0.990.

A lower value for Scenario 5 was found for aluminum rough drawing wire. This is because it uses a large amount of primary aluminum, which is excluded from the Japanese carbon tax.

Another process with a low value for Scenario 5 was the incineration of plastic waste. In this process, CO2 from fossil fuels is released into the atmosphere owing to the incineration of waste plastics. Therefore, life-cycle CO2 emissions were recorded. However, no carbon tax was levied when waste plastic was received. The same can be said for the combustion of blast furnace gas (BFG) and the combustion of Linz–Donawitz converter gas (LDG). In IDEA ver. 2.3, the environmental impact of by-product gases is defined as the emissions generated during the combustion of such by-product gases. Therefore, although there were CO2 emissions associated with this energy use, no carbon tax was imposed for CO2 in Scenario 5.

The process of imposing a carbon tax can be changed from fuel production and electricity generation processes to actual CO2 emission processes, such as BFG and LDG combustion processes. However, the present method of taxing fossil fuels at the time of use is also expected to provide incentives for plastic recycling, as shown in Figure 5. Because it is difficult to measure the actual CO2 emissions from these combustion processes, it would be less costly to use the existing taxation system based on the amount of fuel used.

The same is true for pre-combustion fuels. The carbon tax is levied on diesel oil and gasoline even before they are burned, so that the amount of taxation is high compared to the amount of CO2 emissions generated, up to the time of fuel production. However, because most of these fuels will eventually be burned, there will be no problem with taxation at this stage.

On the other hand, the tax on biomass waste treatment, such as sewage sludge and wood waste, was higher than that on CO2 emissions. This is due to the CH4 emitted during the treatment of these wastes. The same applies to wood combustion; the impact of CH4 and N2O generated during wood combustion increased the tax in Scenario 5. Currently, these GHGs are not taxed; however, the cost of waste disposal and biomass energy increased in Scenario 5. In addition, the carbon tax on miscellaneous non-ferrous metal die casting was higher than that on CO2 emissions. This was because SF6 is used as a flame-retardant gas when magnesium is used as the raw material in this process. SF6, which has a high GWP, is released into the atmosphere from this process and contributes to a high tax rate.

4.3. Taxation Analysis Using the Process-Based LCA Database

Using the process-based LCA database, impacts on product prices were analyzed at the product level. While previous studies using the Input–Output table [9,10] had an analytical granularity of approximately 400 categories and the CGE model had 27 categories [11], this study, using the process-based database, was able to achieve approximately 4700 categories. As shown in Figure 1, there was a large range of price changes among products, even within the same industry sector. For example, if economic incentives are given to encourage the purchase of seasonal vegetables, consumers may purchase them to mitigate the impact on household budgets.

The finer granularity of the calculation allows such an analysis to be performed in more detail. Companies evaluate the life cycle environmental impact of their own products using LCA databases when designing products. Using this method, companies can assess the environmental impact, as well as the risk of future cost increases. A mechanism has been proposed to rebate the carbon tax for export products that are exposed to international competition. By using this method to analyze the cumulative tax amount, the amount of rebate can be discussed based on transparent data. There are other process-based LCA databases worldwide, such as ecoinvent. The same type of analysis may be possible in these databases.

While the process-based LCA database has an advantage in product-level assessments, its data on international supply chains are weaker than those of MRIOs, such as EXIOBASE [43] and EORA [44]. Therefore, in this analysis, only processes that could be clearly identified overseas were evaluated as tax exclusions. In reality, this is not simple because some of the products are imported from overseas, but these data are not maintained in IDEA ver. 2.3. Therefore, this study underestimates the percentage of tax exclusions overseas. In addition, product unit prices change daily depending on supply and demand conditions. They also change depending on the type of purchase, such as discounts for large purchases. In this study, we used the price database included in IDEA ver. 2.3 for estimating price changes; however, it is recommended that companies use primary data as much as possible when conducting this analysis.

In this study, we excluded the levy in the feed-in tariff system for electricity because it is not a tax. However, it is possible to include the levy in the analysis by using this method.

5. Conclusions

To reduce GHG emissions in societies, carbon taxes have been gradually introduced around the world. In Japan, in addition to the existing energy tax, the Special Taxation for Climate Change Mitigation, or carbon tax, was launched in 2012, and the rate has gradually been increased. However, the tax amount is still low, and discussions on increasing the tax amount have started. In this study, we analyzed the impact of a carbon tax increase on product prices at the product level using a process-based LCA database. Compared to the analysis of approximately 400 categories using the Input–Output table, the process-based LCA database enabled analyzing at a detailed granularity of approximately 4700 categories. For example, we found that the rate of price increases differs greatly among products, even in the same industrial sector.

In the agricultural sector, the price increase in seasonal vegetables was suppressed. The unit price of beef products increased by 1.4% if the carbon tax was increased to JPY 5000/t-CO2, and by 7.3% if other GHG emissions, such as CH4 and N2O, were also taxed, while pork and poultry price increases were smaller. The introduction of a carbon tax would create economic incentives for consumers to change their diet to a low-carbon one. However, the rate of increase in the unit price of grains, such as rice and wheat, was higher than that of vegetables. The rate of increase in the prices of daily necessities, such as electricity and gasoline, was also high, so the tax is likely to be regressive. Countermeasures using tax revenues will be necessary.

For plastics, steel, and paper, the carbon tax increase for recycled materials is smaller than that for primary materials. Although the quality of recycled materials may not be the same as that of primary materials, the economic incentive to use recycled materials is expected to be stronger. However, there will be no impact of the carbon tax hike on products imported by foreign countries, such as primary aluminum. Because carbon leakage occurs, it is necessary to introduce appropriate measures.

It was found that the CO2 emissions of products in the LCA database differed slightly from the assumed carbon tax in the Scenario 5. By analyzing the differences, the risks of carbon leakage and the missing taxation coverage can be cleared. For example, SF6 emitted from the non-ferrous die casting process is currently not subject to taxation, but if it were to be taxed, the impact would be non-negligible.

The method applied in this study, which uses a process-based LCA database that expresses the connections between detailed industrial processes, mostly using physical flows, enables companies to assume changes in the prices of procured products due to policy changes on energy and carbon tax, and policymakers to analyze the impact on specific products. When designing a mechanism to rebate carbon taxes on exported products, we recommend using this method to discuss the scope of products to be rebated and reasonable rebate amounts. In particular, if the upstream side contains tax-exempt processes/products, the refund will be excessive if this is not taken into consideration. Although this method calculates the general value of each product, the supply chain of the same product may differ depending on the company. In practice, strict operation, such as proof of supply chain, may be required. Since process-based LCA databases exist in other countries, it is recommended to make effective use of these databases. However, since international trade data of process-based LCA databases are weaker than those of MRIOs, further expansion of overseas data is needed.

Author Contributions

Conceptualization, K.N. and K.Y.; methodology, K.N.; software, K.Y.; validation, K.Y.; formal analysis, K.N.; investigation, K.N.; resources, K.Y.; data curation, K.N.; writing—original draft preparation, K.N.; writing—review and editing, K.Y.; visualization, K.N.; project administration, K.N. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Restrictions apply to the availability of data. The LCA database IDEA was obtained from the National Institute of Advanced Industrial Science and Technology (AIST) and Sustainable Management Promotion Organization (SuMPO) and is available (http://www.idea-lca.jp/ accessed on 29 January 2021) with their permission.

Conflicts of Interest

The authors declare no conflict of interest.

References

- World Bank. State and Trends of Carbon Pricing 2020; World Bank: Washington, DC, USA, 2020. [Google Scholar]

- Criqui, P.; Jaccard, M.; Sterner, T. Carbon taxation: A tale of three countries. Sustainnability 2019, 11, 6280. [Google Scholar] [CrossRef] [Green Version]

- Berkhout, P.H.G.; Ferrer-i-Carbonell, A.; Muskens, J.C. The ex post impact of an energy tax on household energy demand. Energy Econ. 2004, 26, 297–317. [Google Scholar] [CrossRef]

- Lin, B.; Li, X. The effect of carbon tax on per capita CO2 emissions. Energy Policy 2011, 39, 5137–5146. [Google Scholar] [CrossRef]

- Andersson, J.J. Carbon Taxes and CO2 Emissions: Sweden as a Case Study. Am. Econ. J. Econ. Policy 2019, 11, 1–30. [Google Scholar] [CrossRef] [Green Version]

- He, P.; Chen, L.; Zou, X.; Li, S.; Shen, H.; Jian, J. Energy taxes, carbon dioxide emissions, energy consumption and economic consequences: A comparative study of Nordic and G7 countries. Sustainnability 2019, 11, 6100. [Google Scholar] [CrossRef] [Green Version]

- Nadirov, O.; Vychytilová, J.; Dehning, B. Carbon taxes and the composition of new passenger car sales in Europe. Energies 2020, 13, 4631. [Google Scholar] [CrossRef]

- Fremstad, A.; Paul, M. The Impact of a Carbon Tax on Inequality. Ecol. Econ. 2019, 163, 88–97. [Google Scholar] [CrossRef]

- Sugino, M.; Arimura, T.H.; Morita, M. The Impact of a Carbon Tax on the Industry and Household—An Input-output Analysis. Environ. Sci. 2012, 25, 126–133. [Google Scholar]

- Sugino, M. The Economic Effects of Equalizing the Effective Carbon Rate of Sectors: An Input-Output Analysis. In Carbon Pricing in Japan; Arimura, T.H., Matsumoto, S., Eds.; Springer: Singapore, 2021; pp. 197–215. ISBN 978-981-15-6964-7. [Google Scholar]

- Takeda, S.; Arimura, T.H. A computable general equilibrium analysis of environmental tax reform in Japan with a forward-looking dynamic model. Sustain. Sci. 2021, 16, 503–521. [Google Scholar] [CrossRef]

- Berry, A. The distributional effects of a carbon tax and its impact on fuel poverty: A microsimulation study in the French context. Energy Policy 2019, 124, 81–94. [Google Scholar] [CrossRef]

- Saelim, S. Carbon tax incidence on household demand: Effects on welfare, income inequality and poverty incidence in Thailand. J. Clean. Prod. 2019, 234, 521–533. [Google Scholar] [CrossRef]

- Dorband, I.I.; Jakob, M.; Kalkuhl, M.; Steckel, J.C. Poverty and distributional effects of carbon pricing in low- and middle-income countries—A global comparative analysis. World Dev. 2019, 115, 246–257. [Google Scholar] [CrossRef]

- Zhong, H.; Feng, K.; Sun, L.; Cheng, L.; Hubacek, K. Household carbon and energy inequality in Latin American and Caribbean countries. J. Environ. Manag. 2020, 273, 110979. [Google Scholar] [CrossRef] [PubMed]

- Klenert, D.; Mattauch, L.; Combet, E.; Edenhofer, O.; Hepburn, C.; Rafaty, R.; Stern, N. Making carbon pricing work for citizens. Nat. Clim. Chang. 2018, 8, 669–677. [Google Scholar] [CrossRef]

- Babatunde, K.A.; Begum, R.A.; Said, F.F. Application of computable general equilibrium (CGE) to climate change mitigation policy: A systematic review. Renew. Sustain. Energy Rev. 2017, 78, 61–71. [Google Scholar] [CrossRef]

- ISO. ISO 14040. Environmental Management—Life Cycle Assessment—Principles and Framework; International Organization for Standardization: Geneva, Switzerland, 2006; Volume 2006. [Google Scholar]

- Stewart, R.; Molin, C.; Fantke, P.; Bjørn, A.; Hauschild, M.Z.; Laurent, A. Life cycle assessment in corporate sustainability reporting: Global, regional, sectoral, and company - level trends. Bus. Strateg. Environ. 2018, 27, 1751–1764. [Google Scholar] [CrossRef]

- Sonnemann, G.; Gemechu, E.D.; Sala, S.; Schau, E.M.; Allacker, K.; Pant, R.; Adibi, N.; Valdivia, S. Life Cycle Thinking and the Use of LCA in Policies Around the World. In Life Cycle Assessment: Theory and Practice; Hauschild, M.Z., Rosenbaum, R.K., Olsen, S.I., Eds.; Springer International Publishing: Cham, Switzerland, 2018; pp. 429–463. ISBN 978-3-319-56475-3. [Google Scholar]

- Wernet, G.; Bauer, C.; Steubing, B.; Reinhard, J.; Moreno Ruiz, E.; Weidema, B. The ecoinvent database version 3 (part I): Overview and methodology. Int. J. Life Cycle Assess. 2016, 21, 1218–1230. [Google Scholar] [CrossRef]

- AIST; SuMPO. LCA Database IDEA Version 2; AIST; SuMPO: Tsukuba/Tokyo, Japan, 2016. [Google Scholar]

- Moberg, E.; Walker Andersson, M.; Säll, S.; Hansson, P.A.; Röös, E. Determining the climate impact of food for use in a climate tax—design of a consistent and transparent model. Int. J. Life Cycle Assess. 2019, 24, 1715–1728. [Google Scholar] [CrossRef] [Green Version]

- Horrillo, A.; Gaspar, P.; Díaz-Caro, C.; Escribano, M. A scenario-based analysis of the effect of carbon pricing on organic livestock farm performance: A case study of Spanish dehesas and rangelands. Sci. Total Environ. 2021, 751, 141675. [Google Scholar] [CrossRef] [PubMed]

- Ibbotson, S.; Kara, S. LCA case study. Part 2: Environmental footprint and carbon tax of cradle-to-gate for composite and stainless steel I-beams. Int. J. Life Cycle Assess. 2014, 19, 272–284. [Google Scholar] [CrossRef]

- Schneider-Marin, P.; Lang, W. Environmental costs of buildings: Monetary valuation of ecological indicators for the building industry. Int. J. Life Cycle Assess. 2020, 25, 1637–1659. [Google Scholar] [CrossRef]

- Timmermans, B.; Achten, W.M.J. From value-added tax to a damage and value-added tax partially based on life cycle assessment: Principles and feasibility. Int. J. Life Cycle Assess. 2018, 23, 2217–2247. [Google Scholar] [CrossRef] [Green Version]

- Finnveden, G.; Eldh, P.; Johansson, J. Weighting in LCA based on ecotaxes: Development of a mid-point method and experiences from case studies. Int. J. Life Cycle Assess. 2006, 11, 81–88. [Google Scholar]

- Hamedani, S.R.; Kuppens, T.; Malina, R.; Bocci, E.; Colantoni, A.; Villarini, M. Life cycle assessment and environmental valuation of biochar production: Two case studies in Belgium. Energies 2019, 12, 2166. [Google Scholar] [CrossRef] [Green Version]

- OECD. Taxing Energy Use 2019: Using Taxes for Climate Action; OECD Publishing: Paris, France, 2019; ISBN 9789264648456. [Google Scholar]

- Ministry of the Environment Japan Subcommittee on the Use of Carbon Pricing. Available online: http://www.env.go.jp/council/06earth/yoshi06-19.html (accessed on 29 January 2021).

- SuMPO. LCA software MiLCA ver.2.2 2019; SuMPO: Tokyo, Japan, 2019. [Google Scholar]

- NIES. National Greenhouse Gas Inventory Report of JAPAN 2020; NIES: Tsukuba/Tokyo, Japan, 2020. [Google Scholar]

- IWGSCGHG. Technical Support Document: Technical Update of the Social Cost of Carbon for Regulatory Impact Analysis under Executive Order 12866; IWGSCGHG: Wahington, DC, USA, 2016. [Google Scholar]

- High-Level Commission on Carbon Prices. Report of the High-Level Commission on Carbon Prices; High-Level Commission on Carbon Prices: Washington, DC, USA, 2017. [Google Scholar]

- Myhre, G.; Shindell, D.; Bréon, F.-M.; Collins, W.; Fuglestvedt, J.; Huang, J.; Koch, D.; Lamarque, J.-F.; Lee, D.; Mendoza, B.; et al. Anthropogenic and Natural Radiative Forcing. In Climate Change 2013: The Physical Science Basis. Contribution of Working Group I to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2013. [Google Scholar]

- IEA. World Energy Outlook 2020; IEA: Paris, France, 2020; ISBN 978-92-64-44923-7. [Google Scholar]

- IEA. Energy Technology Perspectives 2020; IEA: Paris, France, 2020; ISBN 9789264724860. [Google Scholar]

- IMF. Chapter 3: Mitigating Climate Change. In World Economic Outlook, October 2020: A Long and Difficult Ascent; IMF: Washington, DC, USA, 2020; pp. 85–114. ISBN 978-1-51355-815-8. [Google Scholar]

- Poore, J.; Nemecek, T. Reducing food’s environmental impacts through producers and consumers. Science 2018, 360, 987–992. [Google Scholar] [CrossRef] [Green Version]

- National Statistics Center of Japan Family Income and Expenditure Survey. 2020. Available online: http://www.stat.go.jp/data/kakei/index.html (accessed on 31 March 2021).

- Cosbey, A.; Droege, S.; Fischer, C.; Munnings, C. Developing Guidance for Implementing Border Carbon Adjustments: Lessons, Cautions, and Research Needs from the Literature. Rev. Environ. Econ. Policy 2019, 13, 3–22. [Google Scholar] [CrossRef]

- Cabernard, L.; Pfister, S. A highly resolved MRIO database for analyzing environmental footprints and Green Economy Progress. Sci. Total Environ. 2021, 755, 142587. [Google Scholar] [CrossRef]

- Geschke, A.; Wood, R.; Kanemoto, K.; Lenzen, M.; Moran, D. Investigating Alternative Approaches To Harmonise Multi-Regional Input–Output Data. Econ. Syst. Res. 2014, 26, 354–385. [Google Scholar] [CrossRef]

Figure 1.

Percentage change in product prices by taxation scenario. The boxes show the inter quartile range (IQR). The horizontal lines in the boxes are the median. The whiskers indicate maximum or 3rd quartile +1.5 IQR and minimum or 1st quartile −1.5 IQR. (a) Sectors with relatively large price changes, (b) other sectors.

Figure 1.

Percentage change in product prices by taxation scenario. The boxes show the inter quartile range (IQR). The horizontal lines in the boxes are the median. The whiskers indicate maximum or 3rd quartile +1.5 IQR and minimum or 1st quartile −1.5 IQR. (a) Sectors with relatively large price changes, (b) other sectors.

Figure 2.

Changes in product taxes and product prices in agriculture under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 2.

Changes in product taxes and product prices in agriculture under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 3.

Changes in product taxes and product prices in livestock under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 3.

Changes in product taxes and product prices in livestock under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 4.

Changes in product taxes and product prices in energy under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 4.

Changes in product taxes and product prices in energy under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 5.

Changes in product taxes and product prices in chemicals under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 5.

Changes in product taxes and product prices in chemicals under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 6.

Changes in product taxes and product prices in materials under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 6.

Changes in product taxes and product prices in materials under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 7.

Changes in product taxes and product prices in materials under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 7.

Changes in product taxes and product prices in materials under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 8.

Changes in product taxes and product prices in services under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 8.

Changes in product taxes and product prices in services under different taxation scenarios. The bar graphs show the present taxation breakdown. The percentage change in product prices compares the present with Scenario 5.

Figure 9.

Comparison of the carbon tax in Scenario 5 and the calculated carbon tax based on cumulative CO2 emissions when the CO2 price is JPY 10,000. Data are plotted in log-log scale.

Figure 9.

Comparison of the carbon tax in Scenario 5 and the calculated carbon tax based on cumulative CO2 emissions when the CO2 price is JPY 10,000. Data are plotted in log-log scale.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Energy tax in Japan (modified from [31]).

Table 1.

Energy tax in Japan (modified from [31]).

| Name of Tax | Tax Rate 1 | Tax Revenue (2020 FY Budget) | Revenue Spent for |

|---|---|---|---|

| Gasoline tax 2 | JPY 53.8/L | 2440 Bn | General budget |

| Oil and gas tax | JPY 17.5/kg | 12 Bn | General budget |

| Diesel oil delivery tax | JPY 32.1/L | 964 Bn | General budget |

| Aviation fuel tax | JPY 18.0/L | 69 Bn | Public works for airports |

| Petroleum and coal tax | Pet./Oil products: JPY 2.04/L LPG, LNG, etc.: JPY 1.08/kg Coal: JPY 0.70/kg | 655 Bn | Policies for stable fuel supply Policies for modernization of the energy demand/supply structure |

| Carbon tax 3 | Pet./Oil products: JPY 0.76/L LPG, LNG, etc.: JPY 0.78/kg Coal: JPY 0.67/kg | ||

| Electricity tax 4 | JPY 0.375/kWh | 315 Bn | Policy measures for where power plants are located Policies measures for utilization of power source measures for nuclear safety regulation |

1 As of Jan. 2021; 2 local gasoline tax is included; 3 the official name is Special Taxation for Climate Change Mitigation; 4 The official name is electric power development promotion tax.

Table 2.

Tax exemptions and refunds for energy taxes considered in this study.

| Name of Tax | Tax Exemption/Refund |

|---|---|

| Gasoline tax | - |

| Oil and gas tax | - |

| Diesel oil delivery tax | Agriculture, forestry, wood processor, and fishery |

| Aviation fuel tax | - |

| Petroleum and coal tax | Naphtha for manufacturing petrochemical products Coal used in the manufacturing of steel, coke, and cement Coal used for electricity generation in Okinawa Pref. Heavy oil (A type) used in agriculture, forestry, wood processors, and fishery Domestic petroleum asphalt |

| Carbon tax | Diesel oil and heavy oil used for coastal transportation Coal for on-site power generation in the salt manufacturing industry used in the ion exchange membrane process Coal and petroleum products for use in the generation of electricity for the production of caustic soda Diesel oil used for railway business Aviation fuel used for domestic scheduled air transport services |

| Electricity tax | - |

Table 3.

Number of elementary flows on taxation, tax exemption/refund, and overseas tax exclusion input into inventory database for environmental analysis (IDEA) database.

Table 3.

Number of elementary flows on taxation, tax exemption/refund, and overseas tax exclusion input into inventory database for environmental analysis (IDEA) database.

| Name of Tax | Number of Taxation Flows | Number of Tax Exemption/Refund Flows | Number of Overseas Tax Exclusion Flows |

|---|---|---|---|

| Gasoline tax | 1 | - | 3 |

| Oil and gas tax | 1 | - | - |

| Diesel oil delivery tax | 1 | 420 | - |

| Aviation fuel tax | 1 | - | - |

| Petroleum and coal tax | Crude oil: 1 Natural gas: 1 Coal: 2 | Crude oil: 396 Natural gas: 1 Coal: 23 | Crude oil: 253 Natural gas: 67 Coal: 13 |

| Carbon tax | Crude oil: 1 Natural gas: 1 Coal: 2 | Crude oil: 842 Natural gas: 2 Coal: 26 | Crude oil: 253 Natural gas: 67 Coal: 13 |

| Electricity tax | 134 | - | 28 |

Table 4.

Scenarios for estimating the price change of products due to a change in the carbon tax policy.

Table 4.

Scenarios for estimating the price change of products due to a change in the carbon tax policy.

| Name of Tax | Energy Tax (Exc. Carbon Tax) 1 | Carbon Tax | Domestic Tax Exemption/Refund | Taxing Other Greenhouse Gases |

|---|---|---|---|---|

| Present | Yes | Present (JPY 289/t) | Yes | No |

| Scenario 1 | No | JPY 5000/t | Yes | No |

| Scenario 2 | No | JPY 5000/t | No | No |

| Scenario 3 | Yes | JPY 5000/t | Yes | No |

| Scenario 4 | Yes | JPY 5000/t | Yes | Yes |

| Scenario 5 | Yes | JPY 10,000/t | Yes | Yes |

1 If the total amount of energy taxation is converted per t-CO2, it is equivalent to approximately JPY 4000/t-CO2. However, the tax amount differs depending on the energy type. See Table 1 for further details.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Nakano, K.; Yamagishi, K. Impact of Carbon Tax Increase on Product Prices in Japan. Energies 2021, 14, 1986. https://doi.org/10.3390/en14071986

AMA Style

Nakano K, Yamagishi K. Impact of Carbon Tax Increase on Product Prices in Japan. Energies. 2021; 14(7):1986. https://doi.org/10.3390/en14071986

Chicago/Turabian StyleNakano, Katsuyuki, and Ken Yamagishi. 2021. "Impact of Carbon Tax Increase on Product Prices in Japan" Energies 14, no. 7: 1986. https://doi.org/10.3390/en14071986

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.