3.2. Results from UK Studies

Some data specific to the UK situation have been published. Hesketh et al. [

44] present findings of a fuel cycle study using the ORION code which covers 18 different scenarios although the discussion focuses on the build up to a 75 GWe nuclear fleet with a transition to SFRs after 2040. In terms of uranium demand, the models show that for a UK FR fleet of 40 GWe or above, the reactor fleet only becomes independent of world uranium supplies by 2100. This is due to a shortage of plutonium for the fast reactor cores. The ORION models show that, in terms of fuel supplies, the FR fleet is best preceded by a thermal reactor fleet with reprocessing of SNF and that, as a guideline, a 1 GWe thermal reactor operated for 60 years will generate sufficient plutonium to support 1 GWe of fast reactor operation. The problem for the UK is, therefore, that nuclear energy peaked at around 16 GWe. These issues are not particularly sensitive to increased breeding ratio. For the deployment of FRs from 2040 onwards, reprocessing capacity is needed from 2045, even though the UK has a stockpile of ca. 130 t of separated plutonium already [

45]. Indeed, it is concluded that the fuel supply for the FR fleet will be very dependent on the reliability of the reprocessing plant. The models assumed a six-year cooling period prior to reprocessing which means that the reprocessing plant will need to manage thermal fuel with heat loadings of 3 kW/tHM, whereas FR fuels were calculated to be 13.5 and 7 kW/tHM for two and five years cooling, respectively.

Butler [

17] considered that uranium economics as a driver for more sustainable systems with SNF recycling as future global nuclear scenarios are likely to exceed the known supplies of uranium (6.3 Mt at USD 220/kg). Thermal recycling can increase uranium utilisation by 20% whilst fast reactor systems increase uranium utilisation by factors of 50–60. Butler challenges conclusions from the MIT study which stated: “Our analysis of uranium milling costs versus cumulative production in a world with ten times as many LWRs and each LWR operating for 100 years indicates a probable 50% increase in uranium costs. Such a modest increase in uranium costs would not significantly impact nuclear power economics.” He cites issues with the cost methodology used by MIT and suggests that both cost and energy requirements of the mining and milling operations will affect the OTC viability much earlier at around 40 MtU total consumption with costs becoming prohibitive at 95 MtU. An interesting point is made concerning how increased mining needed to supply the expanded use of once-through nuclear energy could substantially increase carbon emissions from nuclear energy undermining its status as a low-carbon energy source.

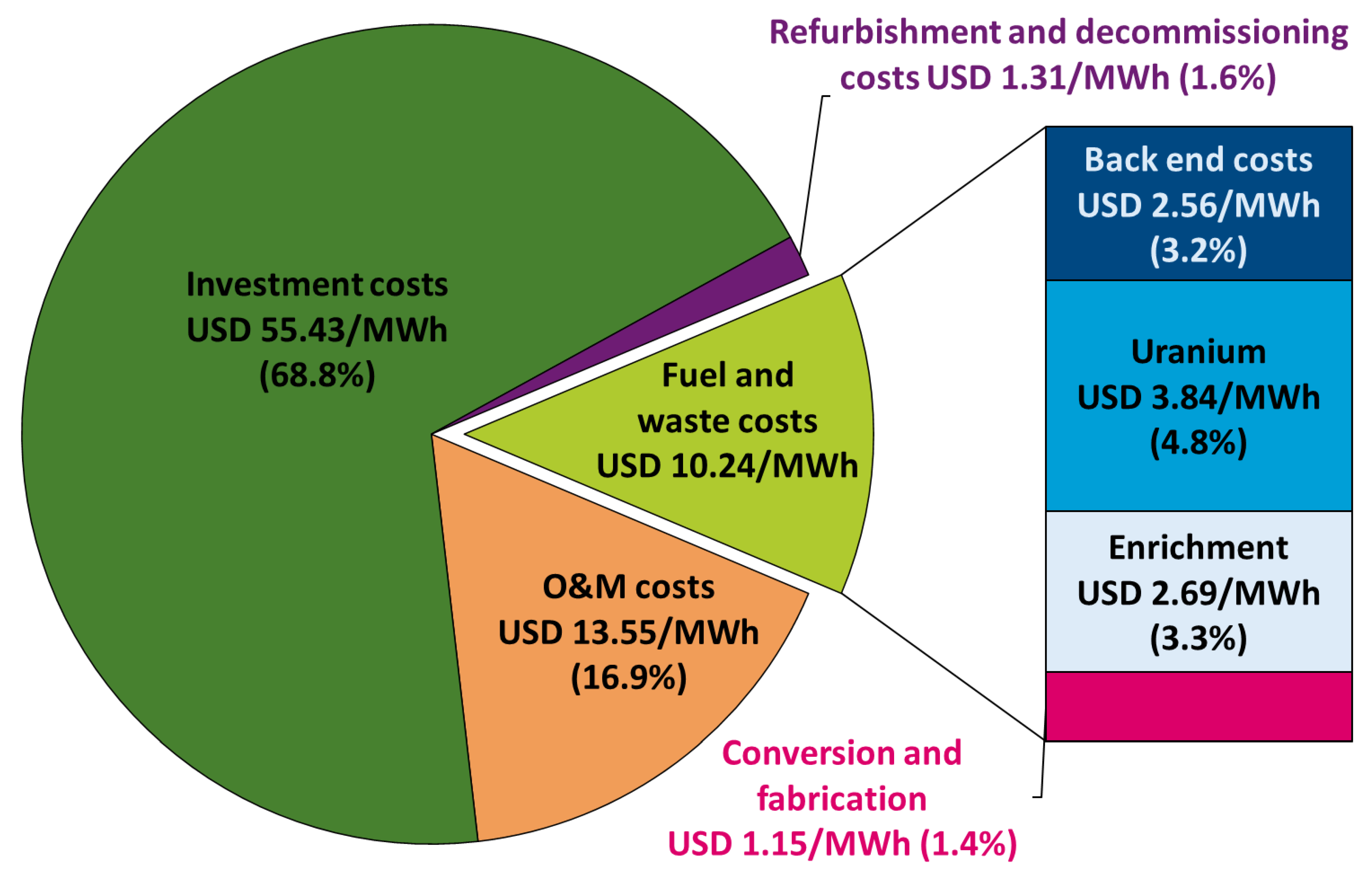

Later work [

46] calculating LCOE for reactors as well as front- and back-end fuel cycle operations exemplifies some of the key findings from economic studies. The reactor dominates the LCOE with only ~3% attributed to back-end fuel cycle costs (

Figure 1). LCOE is most sensitive to capital costs, build times and discount rates assumed. Taking 20% as a significant difference in capital costs of a system and as roughly equivalent to savings in moving from the “first-of-a-kind” (FOAK) to the “nth-of-a-kind” (NOAK), uranium prices or fuel cycle costs have to increase by factors of 3–15 (

Table 3). That is, from the perspective of the LCOE, even the uncertainty in the capital costs of building the reactor swamps any likely fluctuations in the fuel cycle costs. Furthermore, the whole fuel cycle costs have a smaller effect on the LCOE than changing the discount rates by ~1%. Investment/financing costs are a substantial component of the reactor cost; for example a 2% rate for Hinkley Point C new build in the UK would have halved the costs compared to the 9% rate [

36]. However, the authors [

46] caution that when in operation the fuel cycle costs become a significant proportion of running costs and tend to be judged against running costs rather than the overall costs or LCOE.

Dungan [

47] analysed how the changes in disposal footprint [

6] could impact the costs of disposal for five exemplar fuel cycles:

SC1—OTC based on PWRs

SC2—OTC based on high temperature reactors

SC3—TTC based on PWRs

SC4—as SC3 but spent MOX fuel is recycled in SFRs for burning TRU (Pu, Np, Am)

SC5—closed cycle based on SFRs (iso-breeders, conversion ratio of 1)

As with previous studies she showed a substantial reduction in repository footprint with closed fuel cycles and increasing periods of decay storage even up to a factor of 70 for SC5 and 200 years cooling. However, it was found that whilst SC4 and SC5 scenarios might decease the footprint by over 80% the reduction in disposal costs was only 40 to 50% (excluding the fixed costs). Further it was shown that costs of disposal even for the most expensive option (SC1) were not a significant impact on the LCOE and that if even small discount rates were applied then the costs of disposal (50 or more years in the future) were further reduced and the impact of near-term investment costs increased (i.e., the reactor, but this would also apply to any fuel cycle facilities that were built in the near term rather than longer term). Any reductions in disposal costs would likely be offset by costs elsewhere in the fuel cycle (reprocessing and fuel manufacturing). It was concluded that the economics of disposal was not a clear driver for closing the fuel cycle.

3.3. Results from US Studies

Some of the most influential economic studies originate from the United States, including reports from MIT [

48], Harvard [

42], the Boston Consulting Group [

43] and USDOE [

49]. The US has the world’s largest nuclear fleet and an OTC policy, but no operational DGR as yet. The Yucca Mountain repository project has been controversial, with a number of set-backs [

50], and this has stimulated studies of the merits of open versus closed fuel cycles, highly relevant to this review.

The 2003 MIT study on the future of nuclear power [

48] was updated in 2009 [

51]. The authors focused on how new nuclear plants could be economically built at a scale that would contribute towards mitigating climate change and, regarding the fuel cycle, advocated long term storage of SNF to create flexibility. Furthermore, they calculated that there are enough economic uranium reserves to fuel reactors for over 50 years in an OTC and no convincing waste management case for recycle given safety, security and environmental concerns. Regarding economics, their conclusion was that the costs of recycle were “unfavorable compared to a once-through cycle, but, the cost differential is small relative to the total cost of nuclear power generation”. The authors argued against near-term reprocessing in the United States (as proposed by the GNEP (Global Nuclear Energy Programme) initiative at that time [

52]), as it “sent the wrong message” on proliferation, but expressed support for fuel cycle services to be provided by G8 countries to newer users of nuclear power. Instead, nuclear system modelling was recommended to analyse costs, safety, wastes and proliferation characteristics of fuel cycle options. Moderate lab scale research into new separation technologies was proposed in the near term focused on approaches that reduce costs and enhance proliferation resistance and could be deployable in the latter half of the 21st century [

48].

A more detailed analysis of the fuel cycle was subsequently undertaken by MIT in 2011 [

28]. This study also concluded that sufficient uranium resources were available for most of this century and the OTC was the preferred economic option. However, it was recommended that fuel cycle options in the USA should be preserved by pursuing the OTC through (century long) SNF storage and development of the DGR, whilst researching alternative technologies that could meet a range of future nuclear scenarios. Indeed, they specifically stated that the “preservation of options for future fuel cycle choices has been undervalued in the debate about fuel cycle policy”. A related recommendation was that waste management should be integrated into fuel cycle R&D to enable development of optimized solutions. Regarding future fuel cycles the authors warned that:

“The choices of nuclear fuel cycle (open, closed, or partially closed through limited SNF recycle) depend upon (1) the technologies we develop and (2) societal weighting of goals (safety, economics, waste management, and non-proliferation). … Today we do not have sufficient knowledge to make informed choices for the best cycles and associated technologies”.

The long-term nature of closed fuel cycles (transition times of 50–100 years) was highlighted together with a proposal that a conversion ratio near unity is preferable in order to facilitate alternative closed fuel cycle pathways such as use of hard neutron spectrum reactors or start-up of fast reactors with low enriched uranium (LEU); these potentially being more economic or proliferation resistant options. An interesting suggestion is made with regards to the DGR; in that if it is sited before a closed cycle is deployed, co-location of the recycle (reprocessing and fuel fabrication) site with the DGR can be considered to improve both economics and security as well as repository performance through optimization of generated waste forms. The job creation and benefits thus compensating the local community hosting the DGR. In the OTC, fuel cycle costs are estimated to be ~10% of the LCOE with waste management costs about 10% of the fuel cycle costs (1–2% of the LCOE). The capital costs of the reactors thus dominate costs and thus will dictate decisions. Another interesting observation is that whereas ~7 t of LWR SF are needed produce 1 t of LWR MOX fuel, 1 t of spent FR fuel produces ~1 t of new FR fuel. Hence, reprocessing throughput (for the same electricity output) in a fast reactor cycle needs to be only 5–10% of that of an LWR cycle. This suggests scenarios where FR fuel recycle would be economic whilst LWR fuel recycle would not (the authors liken this to mining higher assay ores).

The MIT study used a fuel cycle simulation code CAFCA to model the OTC, TTC and multi-recycling, in both advanced burner (conversion ratio 0 to 1) and fast breeder reactors (conversion ratio of 1.23). LWR fuel burn up was assumed to be 50 GWd/t, five year cooled pre-reprocessing and two years post-reprocessing. The reprocessing plants have an assumed lifetime of 40 years with throughputs of 1000 tHM/y for LWR and 100–500 tHM/y for FR fuel reprocessing (for conversion ratios 0–1.2). The basis of their economic analysis and calculations of LCOE are described in detail in [

53]. For fuel cycles with recycling, they calculate a total LCOE that is then decomposed into separate costs for each reactor cycle by determining a price for recycled elements. The LCOE is based on the decision to recycle and, as the prices for recycled elements (Pu or TRU) are negative (i.e., they are a liability), then it means the reactor burning recycled fuels must be compensated by the first reactor that burned the UOX fuel. Or put another way, this is essentially the cost of “disposal” of the spent fuel from the first reactor and the second reactor is being “paid” for this service. The economic analysis is summarised in

Table 4 where it can be seen that:

The reactor dominates the LCOE, around 80% of the cost of electricity generation in the LWR cycles and over 90% for the fast reactor-based fuel cycle.

The capital and operating costs of the fast reactor are assumed to be 20% higher than the LWR and this cost premium cannot be compensated for by savings in the fuel cycle or increases in uranium prices according to their modelling.

Nevertheless, the total increase in LCOE is calculated to be only around 2–3% for fuel cycles involving recycle of fissile materials.

Whatever fuel cycle is adopted, the back-end fuel cycle costs are a small percentage of the overall LCOE (1.6–4.7%).

However, compared with the OTC, the overall fuel cycle costs have increased by 19 and 33% for the TTC and advanced fuel cycle (AFC) options. This mainly reflects the cost of reprocessing, the cost of MOX fuel disposal (in the TTC) and charges for the recovered TRUs. The premium for the recycling of SNF (the increase in total LCOE) is 21 and 112% for the TTC and AFC when calculated relative to the cost of direct disposal in the OTC (1.3 Mills/kWh).

Additionally, it was shown that the LCOE for the AFC increased with conversion ratio from 85.86 to 86.57 to 86.91 for conversion ratios of 0.5, 1 and 1.2, respectively. It is apparent that, since the LCOE increases only marginally, there are many trade-offs in the fuel cycle economics as the complexity of the fuel cycle increases. With recycle, savings can be made in front-end costs whilst back-end costs rise. Advanced reactors and use of MOX/TRU fuels also add costs.

DeRoo and Parsons [

53] compare their methodology with others such as [

42,

54] who calculated costs based on equilibrium situations (where costs attributed to the recycled TRUs are avoided). Using the example of the AFC with FR fuel recycling it was shown that calculations based on this equilibrium approach would give higher values than the MIT methodology by 4–15% for conversion ratios of 0.5–1.23.

A major (although now dated) analysis of the economics of reprocessing versus direct disposal was carried out by Bunn et al. [

42] in 2003. They draw on a wide range of sources to attribute costs across the full life cycle, including estimates of upper and lower bounds to each reference value. The basis of the component costs, including the costs allocated to reprocessing, MOX fuel fabrication, HLW disposal (including the savings over direct disposal of SNF) and price of uranium, are discussed in detail with reference to a wide base of source materials. They then primarily analyse the economics in terms of the uranium breakeven price, (i.e., the point at which reprocessing would be cheaper than disposal). For their reference uranium price (USD 50/kg),

Table 5 indicates the changes to other costs that would be needed to reach the uranium breakeven price; for instance, it is calculated that reprocessing costs would need to be decreased to 42% of their reference cost or the price of fresh uranium would need to increase to around USD 370/kg.

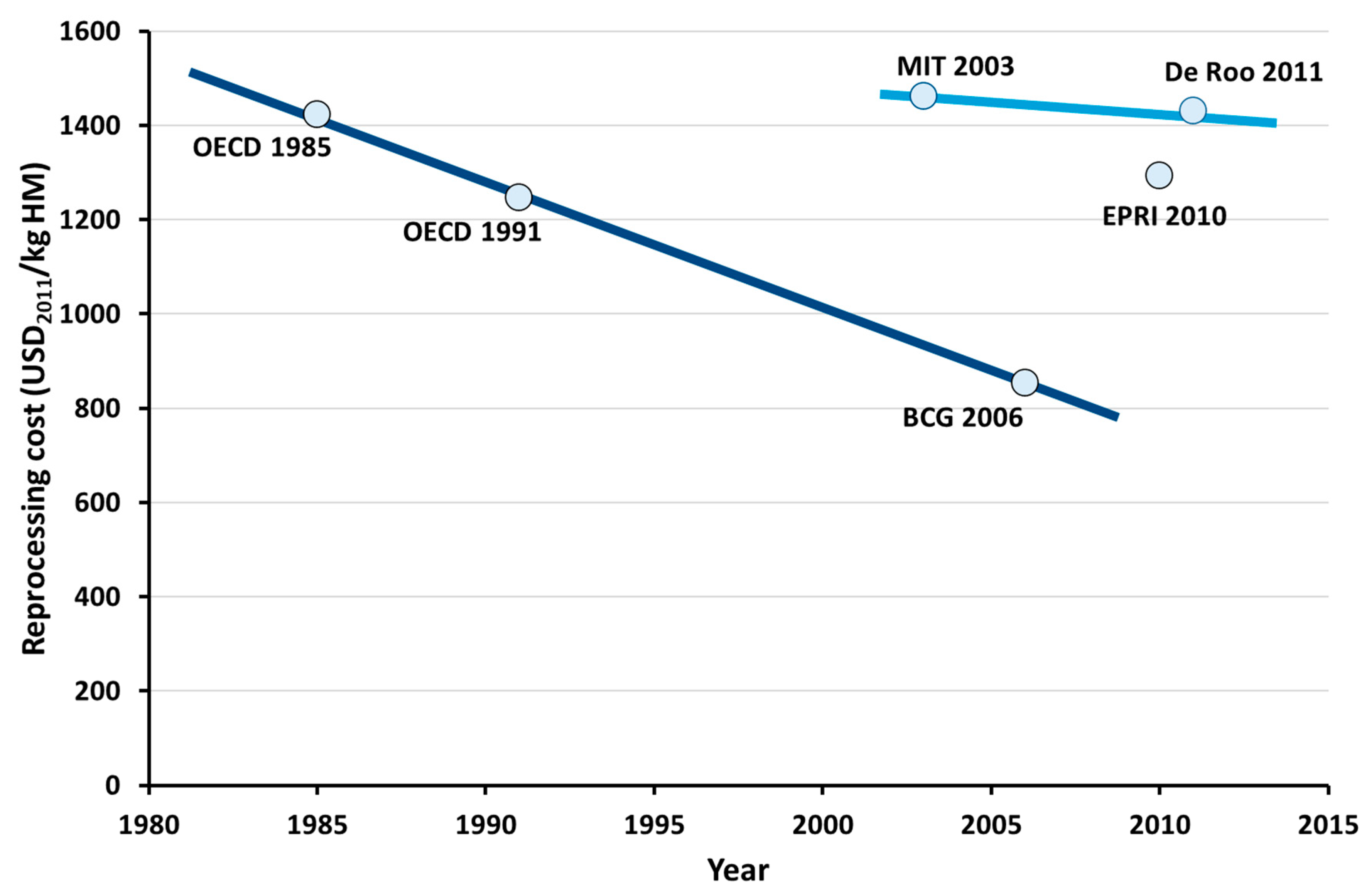

Bunn et al. [

54] also calculate the additional costs of reprocessing to be about 1 Mill/kWh for their reference reprocessing (USD 1000/kgHM) cost up to a uranium price of USD 130/kg. How this additional cost varies with uranium price for reprocessing costs between 50 and 200% of the reference value is illustrated in

Figure 2. They estimate the back-end cost of the OTC is about 1.5 Mills/kWh, so the reference case suggests reprocessing increases the back-end costs by more than 80%. They conclude that given probable global uranium resources, and based on their analysis, that recycling is unlikely to be economically competitive with direct disposal (as indicated by the uranium breakeven price) for more than a century.

The Boston Consulting Group in 2006 arrived at different conclusions based on access to proprietary economic and operational data from reprocessing in France [

43]. They analysed two scenarios for the United States:

A generic greenfield approach with recycling (TTC) and a HLW repository versus an OTC with repository for all SNF.

An implementation approach specific to the US scenario with recycling (TTC) and the Yucca Mountain repository for legacy fuel and HLW (the “portfolio” strategy), versus an OTC with an expanded Yucca Mountain capacity (120 ktHM) and second repository to meet demand over a 50-year period (2020–2070).

The greenfield approach enabled direct comparisons to be made for OTC and TTC in the US and comparisons with other studies. The implementation approach enabled analysis of what were considered at the time to be more realistic deployment scenarios for recycle and disposal in the USA. In the implementation approach with recycling, 125,000 tonnes of legacy and new SNFs are recycled and 50,000 tonnes of legacy SF disposed of in the Yucca Mountain DGR. Furthermore, 15,000 tonnes of MOX fuels are stored at reactor sites for future disposition (no end point). The recycle option assumed an integrated recycling plant incorporating a combined extraction (COEX) reprocessing plant, MOX fuel fabrication, vitrification, hulls waste management and interim storage of spent MOX and vitrified HLW.

The BCG analysis concluded that in the greenfield approach discounted costs of recycling (TTC) are within 10% of OTC costs (USD 520/kg compared with USD 500/kg in 2005). In the implementation approach costs were also very similar up to 2070 (net present costs of USD 48–53 bn for TTC compared to USD 47–50 bn for OTC), and in fact the total undiscounted life cycle cost for the portfolio strategy (TTC) is ~10% lower (USD 113 bn for TTC compared with USD 124–130 bn for OTC; see

Figure 3.). Even when sensitivities to the uranium price and repository cost are analysed, both OTC and TTC strategies exhibit “comparable economics”. One significant difference in the models was the cash-flow predictions with near term peak capital costs to build infrastructure for the portfolio TTC strategy and then a reducing demand compared with a mid-term bulge in the OTC due to operating the first repository whilst constructing the second repository around the mid-century (

Figure 4). Some notable assumptions in their modelling include the assumption that space savings in the repository translate directly to cost savings, a nominal 25-year-decay period before SNF or HLW is emplaced in the repository for both OTC and TTC scenarios and interim storage of spent MOX (~300 t/y). The management of spent MOX fuel, in particular, is a key uncertainty in the proposed portfolio approach. The authors suggest multi-recycling in LWR or burning in fast reactors which may be available later this century and estimate this would increase the recycling costs by 10–15%. Disposal of spent MOX (assuming the nominal 25-year-decay period) is not favoured as it would negate the savings in repository footprint obtained by recycling UOX fuels and add up to 40% to the recycle costs. The other problem with MOX is that there is a “MOX acceptance cost” that is needed to address difficulties that utilities have in using MOX compared with standard fresh UOX fuel. The value of MOX, therefore, is calculated to be ~75% of the value of UOX fuel. De Roo and Parsons [

53] criticise this approach as, in their opinion, it prevents the calculation of the LCOE for the full cycle. Nor does it reflect the market position whereby if there is an option of UOX fuel then an operator with only a UOX license can afford to refuse the use of MOX fuel; hence, any MOX discount would have to be very large to overcome the regulatory and stakeholder challenges of enabling the use of MOX. This would change, of course, if there is a national level strategy based on recycling. Certainly, the assumption of interim storage of spent MOX fuel without a specific costed disposition route leaves a major gap in the fuel cycle strategy.

Since 2003, the US Department of Energy Office of Nuclear Energy has published a regular in-depth review of advanced fuel cycle costs, with the latest edition published in 2017 [

49], although it cautions that the data are best used for relative comparisons of options rather than accurate determinations of fuel cycle costs. Furthermore, that the results of models may vary due to user-defined parameters, such as users’ individual treatment of cost escalations, learning effects, fuel cycle configurations, etc. The impacts of discount rates and accounting for future benefits to present values are discussed and how this leads to delays in adopting technologies; for instance, how this can lead to analyses whereby the cost of dry storage is always less than geological disposal even if packages degrade and require over-packing. The authors highlight that, whilst economics are important, other factors, such as sustainability, proliferation risks and adaptability to future scenarios, also need to be part of the evaluation process. Nonetheless, this work rigorously compiles and evaluates a broad range of cost data across the full future cycle, including assessing sensitivities and providing high and low estimates.

The results of the reprocessing analysis are given in

Table 6 for aqueous reprocessing using the French COEX process, UREX + 1a and UREX + 3a processes and a pyro-electrochemical process. A possible 24% reduction in UREX + 1a costs was noted but not implemented at this time (all reprocessing technologies could possibly be lowered in future). UREX is a modified PUREX process to prevent plutonium extraction, thus achieving waste volume reduction by removing the uranium. Variations of UREX (indicated by the suffixes) include additional separations to recover plutonium, MA and/or HHR, to save space in the DGR but with increased proliferation resistance by avoiding pure separate plutonium compared to the conventional PUREX process. Whilst COEX is a rather conventional PUREX process, adapted to produce a mixed U-Pu product, UREX+ involves sequential separations to recover U, Pu, minor actinides, high heat generating isotopes of caesium and strontium and zircaloy hulls [

55,

56]. Issues related to scaling are discussed in detail and it is considered that plant throughputs in the range of 1000–2000 tHM/y are probably near the minimum of the cost curve even if several lines are needed. FR reprocessing is considered at a lower scale (~300 t/y) where the effects of the relatively larger head end are not significant. For the United States, a plant of 2500 t/y and operating life of 40 years is said to be the most economical deployment. It is noted that the influence of line throughput and solvent extraction contactor type are not explicitly analysed and may have impacts. Interestingly, the head end, chemical separation and U/TRU storage facilities are said to account for nearly 60% of the reprocessing costs with head end (comprising fuel receipt and storage, shearing, dissolution, off gas management, hulls treatment and technetium alloying) being the most expensive facility area.

In the non-aqueous electrochemical processing of SNF [

57], refabrication of fuel is an integral part of the process and must be a remote operation due to high residual activity of the reprocessed products. Cost estimates, therefore, included remote refabrication of fuel, although estimates were made of this activity alone in order to enable better comparisons with aqueous options (

Table 6). Throughputs are generally low (20–300 tHM/y) as, at least in the United States, this technology is considered to be applied to FR fuel (usually metal) recycling either as part of an island site (the Integral Fast Reactor concept [

58]) or servicing a group of FRs. Limitations are also posed by electrochemical processing being a batch process. The report notes that whilst a number of cost studies have been made they are all underpinned by only one practical implementation—the engineering scale facility at the Idaho National Laboratory that processed Experimental Breeder Reactor-II (EBR-II) fuel [

57]. Whilst the report notes scopes for reductions in costs it also warns that costs associated with first of a kind (FOAK) implementation and lack of technology scale-up experience could be significant in this case.

Phathanapirom and Schneider [

41] proposed a decision theory based model to strategise the transition from the OTC to FRs with plutonium and MA recycle given the costs of implementing FRs are unknown. The aim is to use stochastic modelling, in which the “regrets” from pursuing different pathways can be estimated, to develop a hedging strategy and help decision making. Costs are estimated as LCOE and the simulation is essentially for the United States with a 100 GWe fleet in 2015 assuming 1.25% growth per year up to 2100. The strategy is controlled by the availability of TRU; that is the amount of LWR reprocessing capacity and thus timings at which 500 tHM/y and then 3000 tHM/y reprocessing plants are installed. The study concludes that in all scenarios, partial transition to a closed cycle is advised. This involves deploying a pilot scale (500 t/y) reprocessing plant for LWR fuel and adjusting the strategy once build costs of FRs become clearer.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}