Abstract

Distributed Energy Resources (DERs) are spreading under the pressure of climate change mitigation plans and the framework, recognized as the most suitable to exploit DER diffusion, is the Energy Community (EC). Understanding the role of energy companies, especially Aggregators, in this context, is still an open topic, as it is not clear how they can support members in the aggregation process and how they create value through their business. The aim of the study is therefore to revise whatever is currently present in the research agenda and consequently a systematic literature review has been carried out. The contribution of this work consists of illustrating the main features of Aggregators, pointing out how they implement their strategies in the energy markets, with which services they capture value, who their partners and customers are, what the financial aspects are of their activities with respect to the size of the aggregated clusters, and, in conclusion, which are the main business model structures currently deployed. Then, considerations are made concerning EC context, identifying the areas where an Aggregator could usefully support communities’ establishment and management, solving well-known hindrances, and what gaps future research should fill.

1. Introduction

The energy sector is currently facing a substantial transformation. Geopolitical turmoil led to upward pressure on commodity prices [1], causing a temporary shift to more polluting energy sources due to the high cost of gas. This is exacerbating already worrying climate change-related threats, diverting attention and economic resources to climate mitigation initiatives that are fading.

Otherwise, the present context is raising awareness among Europeans on two significant themes: the necessity to free themselves from unstable suppliers and the need to cope as soon as possible with global warming’s severe externalities. This is leading to a strengthening of the normative framework, although its developing path has deep roots. The first move to combat climate change was made back in 1972 when the United Nations organized the Conference on the Human Environment, which aimed to put at the same table industrialized and developing countries, focusing the debate on human activities’ ecological impact on ecosystems and natural resource deprivation. Major results of the Stockholm conference were the creation of the United Nations Environment Program (UNEP) and the promulgation of the Stockholm Declaration and Action Plan for the Human Environment, a resolution that includes principles for sustainable management of the environment. Other milestones were unquestionably the COP 3 conference, held in Kyoto in 1997, and the COP 21 conference (Paris, 2015). The former is extremely relevant for its signature Kyoto Protocol, the first international treaty to acknowledge the urgency of reducing greenhouse gas emissions, while the latter was the first agreement to be legally binding and added the goal of keeping the annual increase in temperature below the 1.5 °C threshold (United Nations Conference on the Human Environment, Stockholm 1972|United Nations: https://www.un.org/en/conferences/environment/stockholm1972, accessed on 4 March 2023).

The European Union has set its strategy in parallel, identifying specific community objectives, such as Agenda 2020, which was released by the European Commission in 2008 and enacted into legislation in 2009. It is the first strategic document defining a set of laws passed to ensure the EU meets its climate and energy targets (https://climate.ec.europa.eu/eu-action/climate-strategies-targets/2020-climate-energy-package, accessed on 24 March 2023). The package sets three key targets: a 20% cut in greenhouse gas emissions (from 1990 levels), 20% of EU energy from renewable energy sources (RES), and 20% improvement in energy efficiency. Returning to the present, according to the European Commission Green Deal (2019), targets to be reached on carbon footprints include a 55% reduction in polluting emissions by 2030 and climate neutrality by 2050 (European Commission, Brussels, 11.12.2019 com (2019) 640 final communication from the Commission to the European Parliament, the European Council, the Council, the European economic and social Committee and the Committee of the Regions the European Green Deal: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52019DC0640, accessed on 25 March 2023). Reducing emissions to such an extent as to make them completely absorbable would boost the shift to RES, as increasing penetration of renewables is recognized as one of the key drivers in the energy transition, and an unavoidable step to reach the aforementioned goals. These explain the number of policy tools that have been designed over the years, especially on solar photovoltaic (PV) technology, such as feed-in tariffs, fiscal incentives, subsidies, and certificate trading [2].

It is also thanks to these advances that eolian energy and photovoltaic (PV) capacities are still globally growing; the latter will probably soon become a primary source of energy [3].

The electric power sector definitely has a central role in mitigating the impact of climate change, but electrification and decarbonization of industrial processes and the transportation sector will provide a substantial contribution as well [4]. However, this implies the growth of electric energy demand, which could start a vicious cycle if this energy is not produced cleanly and sustainably. To solve both issues introduced so far, the aim is to shift from a centralized fossil production system to a polycentric renewable one, and the direction undertaken by the energy sector is to advance the diffusion of distributed energy resources (DERs) [5].

One of the instruments conceived to make the most of renewables is the Energy Community (EC), a collective association of citizens that allows for an increase in the efficiency of energy use through self-consumption and helps the integration of DERs within the network, which is still difficult. On the technical side, this merger is only possible thanks to the IC Technologies of Smart Grids, considered an enabling framework [6], and to the efforts of a system operator known as an Aggregator. The Aggregator is a demand service provider that combines multiple short-duration consumer loads for sale or auction in organized energy markets (Directive 2012/27/EU of the European Parliament and of the Council on energy efficiency, amending Directives 2009/125/EC and 2010/30/EU and repealing Directives 2004/8/EC and 2006/32/EC: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex%3A32012L0027, accessed on 29 March 2023) and serves as a broker for transactions between energy suppliers and consumers [7], also managing aggregated energy clusters or communities.

The main goal of this study is therefore to identify the state of the art on the Aggregator’s role in renewable energy production systems, especially in the Energy Community context, outlining how it creates value along the chain and in which way it could be useful in supporting energy transition.

2. Motivation and Research Purpose

As the big picture of the energy sector talks about huge and fast transformations forced by the negative impacts of climate phenomena, as previously mentioned, the key instrument to get closer to a rapid transition is the diffusion and integration of decentralized renewable energies. Our paper focuses on one of the new key players in the future of energy markets. Considered a means to locally produce green energy, DERs are low/medium-voltage technologies, mainly wind- and solar-based, that are operated within the electric distribution system [8]. Wind power and PV have a strongly intermittent nature, which means that they are not continuously available due to factors that cannot be controlled (connected with site and weather) such as wind speed, air density, solar radiation, and cloud cover. This variable feature makes these sources of electricity non-dispatchable, meaning that they generate electrical energy but cannot be sufficiently flexible in production to meet fluctuating electricity needs.

Since storage is not mature enough in all its technologies [9], balancing demand and supply in the system is more challenging with relevant risks of the grid’s reliability, congestion rents, and power outages. DERs have their strong point precisely in avoiding transmission costs and mitigating overloaded transmission lines, controlling price fluctuations, strengthening energy security, and jointly raising the grid’s stability [10]. Therefore, the relevance of the Aggregator has a technical motivation.

The aim of recent policies is to use local flexible energy production for these purposes, but as already mentioned, there are technical reasons for entrusting the Aggregator to manage groups of low-flexibility providers. In the rest of the paragraph, we will delve deeper into the process that led to the identification of the Aggregator as a key role for the integration of renewable energy sources.

The DER components consist of Distributed Generation (DG) and Distributed Storage (DS) [11]. A key aspect of DG plants is modularity, which returns two advantages:

- the possibility of constructing the facility in stages, gaining a positive stream from the part of the plant that is already complete and working;

- helping cluster managers in operations, thanks to the deployment of modules that can work or stay idle depending on energy demand.

On the storage technologies side, the main purposes include balancing the changing load impacts of renewable energies. Through these devices, it is possible to access extra services such as frequency and voltage stability, maintain a stable energy supply, improve power quality (voltage), and save a lot of money for power grid enlargement [12].

Increasing the efficiency thanks to a more controllable power supply implies obtaining both lower pricing of electricity and ecological benefits such as emissions reduction. There are several methods for storing energy, but generally, the main solutions are based on mechanical, electrical, chemical, electrochemical, and thermal technologies [13]. In any case, ES is important in energy systems especially for demand-side management, “bridging the gap present between the power demanded and supplied” [14].

Inherent to the classification presented above, in [15], authors also add Demand Response (DR) and point out several features:

- Basic principles inherited from demand-side management are peak shaving, valley filling, load shifting, or reduction.

- To involve consumers in DR programs is crucial to offer a fair tariff as leverage to induce them to modify their consumption patterns. Since the required reduction is a voluntary choice, price signals and incentives must be designed correctly.

- Real-time pricing is the development direction for tariff setting, to inform the consumer daily (or hourly) of their consumption options.

Summing up, DERs provide consumers with a broad package of benefits [16]:

- Electricity price reduction;

- Upgrade in reliability of the service and the possibility to participate in competitive electric power markets;

- Increased penetration of renewable energy sources such as solar and wind into the DER, boosting the deployment of self-sustained power supply technologies;

- Application of solar and wind resources, minimizing fossil fuel consumption and reducing the overall emissions intensity of the greenhouse gases;

- Enhancement in the local economic development.

Also known as energy clusters, these decentralized production systems are spreading due to important private investments (homeowners) [17].

The core idea is to raise financial capital by mobilizing the private financial resources of consumers, who undertake proactive behavior on the production side and by managing the consumption and storage of their energy. This outline enhances the impact of renewables thanks to users’ money but also defines a new figure of consumer and producer: the prosumer. In the existing political and legal frameworks, directives 2018/2001/EU (RED II) and 2019/944/EU (IEMD) marked a milestone in the recognition of the centrality of prosumers in the energy transition.

Defined in [18] as an “electric customer who generates electricity and sells excess back to the Utility”, the prosumer retrieves both energies from the grid and self-produced energy from rooftop solar panels or other generating devices, while injecting into the grid only the power that exceeds its need [19]. A prosumager instead is also equipped with a storage device, which allows him to maximize efficiency since the self-consumption is extended in non-productive hours and vice versa; what is produced and not instantly consumed can be stocked [20].

The prosumer concept makes a lot of sense if collaboration among them is established, which means creating a virtual place where the demand and supply of surplus energy can be matched. This is possible only if each prosumer is provided with metering technologies and participates in the local market, where energy is exchanged through a digital platform. What is discussed here is peer-to-peer trading (P2P), namely a decentralized structure where all peers (prosumers and consumers) cooperate with the energy generated through small-scale Distributed Energy Resources that they have available [21]. In the literature, this kind of local market can be shaped in different ways, depending on the nature of peers’ interaction. If they directly negotiate the energy with each other, a full P2P market model is in place; alternatively, the community-based market is set, where a community manager supervises all the transactions [22]. In both cases and eventually in a hybrid configuration too, P2P energy trading encourages multidirectional trading, in contrast with conventional energy trading, which is mainly unidirectional. This tendency is construed in the new regulatory scheme mentioned before, which empowers the creation of a prosumer-centered electricity market in substitution of the conventional hierarchical and top-down approach [23]. On this side, the most important concept that emerged from European directives is the Energy Community (EC). EC is defined as a legal entity “open, voluntary, autonomous, controlled by shareholders or members located in the proximity of the renewable energy projects owned and developed by that legal entity”. Here consumers and prosumers are gathered in a unique cooperative infrastructure whose main aim is to allow members to share their energy, maximizing self-consumption and withdrawing as little energy as possible from the grid, striving for community autarky. What EC represents is a paradigm change, a switch from isolated consumers to active prosumers that participate in energy production, from a collaborative perspective. First of all, this would lead to an increase in efficiency and penetration of clean technologies, but also fight energy poverty and increase social inclusion through a new community spirit [24]. Moreover, EC is considered the most rapid way for citizens to take part in the energy supply chain. Despite social and ecological implications, saving in the bill remains the main driver to the community establishment, even if remarkable results have been achieved in projects such as H2020 GRETA, where associations, committees, and groups of active citizens, working for years on community engagement, have triggered energy community aggregation through civic activism initiatives.

If energy clusters are the underlying technical framework, EC is the governance scheme, and on that side, a lot of work must be done to make communities a standard model in the energy market. Relationships with partner companies and especially related business models (BMs) are under evaluation. The rationale behind these BMs is to “broaden the capital participation” of consumers or “permit the co-investments of different actors” [25], such as Energy Companies, Energy Services Companies, and Aggregators. Achieving transition targets implies designing a lean and fast process to group consumers and prosumers in a solid and manageable structure. The community has as a main requirement to ensure open access and exit and to be the result of a “bottom-up” aggregation, and this feature is perhaps the biggest inhibitor to the rapid diffusion of EC, even if several other barriers are in place. Lack of trust and motivation of consumers in community models, absence of technical know-how on microgrid operation, legal and bureaucratic barriers, difficult access to finance, and weak incentives are the major issues to deal with [26]. It is quite clear that these challenges are not adequate for standard user skills, and a suitable partner is required both for technical and financial aspects. Considering this framework, it is now evident that, among various types of energy companies, the right choice could be an Aggregator in accordance with the expertise gained operating local facilities, infrastructures, and services connected to DER production. The Aggregator has, in fact, the role of gathering electricity demand, the energy produced, and load flexibility from the prosumer’s devices, engaging different electricity markets in which electricity and ancillary services are traded [27]. The literature on Aggregators is not so extensive, but the most acknowledged setup for this entity is the local flexible market operator, which supervises the cluster’s activities and internal transactions, as described in [28]. In this layout, the Aggregator interacts with the Distribution System Operator (DSO) for voltage and power control and with the Balance Responsible Party (BRP) for portfolio optimization, and remunerates collaborating prosumers. Inside the EC field, it is still not at all obvious what could be the function of theAggregator, due to lack of clarity in regulations, implying that the business model cannot be shaped with certainty. Hence, the main goal of this study is to identify whatever has been investigated concerning the Aggregator’s place in the renewable energy supply chain. Figuring out the main services that an Aggregator can offer and which would be pros and cons to enter the EC business area is crucial to understanding if it could be a worthwhile partner for Energy Communities. For this purpose, a systematic literature review has been conducted.

3. Materials and Methods

In this section, we present the method followed by the structured review and utilized materials.

3.1. Method

The systematic literature review has been designed following the method of Preferred Reporting Items for Systematic Reviews and Meta-Analysis (PRISMA), proposed inter alia by Brown (2007) [29] and Ceglia et al. (2022) [30] in the article The State of the Art of Smart Energy Communities: A Systematic Review of Strengths and Limits. The method consists of the following four phases:

- Identification;

- Screening;

- Eligibility;

- Inclusion.

The reference database Web of Science was chosen, as it is the most business-oriented and has the highest level of scientific contributions.

3.2. Identification: Keywords

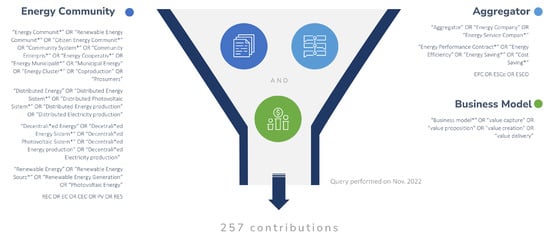

With regards to keyword definition, these are focused on the three main topics that make up the research theme (Figure 1): the business model of an Aggregator in the Energy Community context. Selection criteria are exhibited below.

Figure 1.

Identification phase: keywords and query output.

- Energy Community: Keywords related to Renewable Energy production and Energy Community concepts have been considered jointly with keywords inherent in distributed/decentralized energy production. This choice is motivated by preliminary review activities that revealed the relevance of topics not directly involved in EC.

- Aggregator: In addition to Aggregator, keywords such as Energy Company and Energy Service Company have been selected. Furthermore, key terms concerning Performance Contracting and Efficiency concepts are included to check the presence of this subtopic in the literature.

- Business Model: In addition to BM, the other keywords chosen pertain to the notion of «value», that is added from the company’s activity: creation, proposition, delivery, capture.

3.3. Screening, Eligibility, and Inclusion

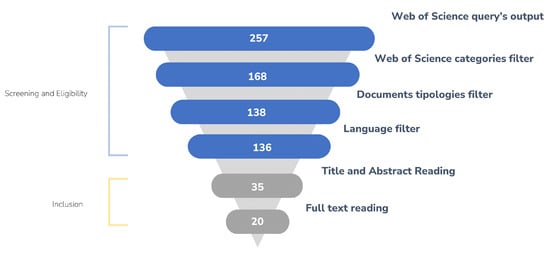

Screening and Eligibility phases are performed; once identified, the 257 contributions obtained as research results were assessed according to the following requirements:

- Belonging to Web of Science meaningful categories, which, according to the research topic, are energy fuels, environmental studies, environmental sciences, green sustainable technologies, management, business, economics;

- Belonging to document’s typologies, Article, Review Article, or Early Access, in order to maintain the scientific level of contributions;

- Language: English.

Finally, the Inclusion part is organized in two sections:

- Selection in accordance with research topic relevance: reading title, abstract, and introduction;

- Selection in accordance with contribution coherence: reading full text.

The outcome of this procedure was removing a consistent number of articles. After the application of categories, documents, and language filters, the remaining contributions totaled 136. Through reading the title, abstract, and introduction, the selection was further refined. This filtering activity eliminated papers on biology, chemistry, and electric engineering that entered the findings due to the double meaning of acronyms like EPC and REC or expressions like “value creation”, which also has business-related meanings. Finally, the obtained 35 articles were shrunk to a final sample of 20 via reading of the full text. The main sorting criterion was the coherence with other papers, based on the presence of a strong focus on Aggregator BM, not always the core topic of these contributions. Screening, Eligibility, and Inclusion phases are reported in Figure 2.

Figure 2.

Filtering process: contributions’ selection steps.

4. Research Findings

This section is dedicated to the presentation of the results, showing interesting aspects and statistics of selected contributions.

Meta-Analysis

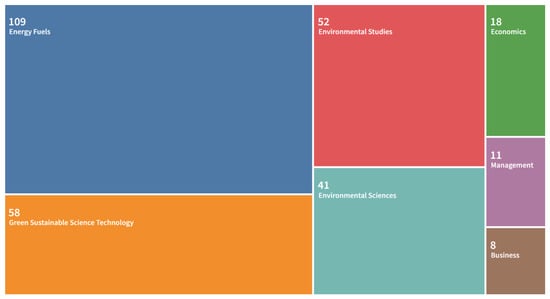

From the meta-analysis, it emerged (Figure 3) that research areas more involved in the study of the presented topics are Energy Fuels, Environmental Studies, and Sciences, Green Sustainable Technologies, and categories related to social sciences (Economics, Management, and Business). That shows the interdisciplinary nature of the research theme. Due to the overlapping of WoS categories, the total number of contributions in the following table does not match the 136 articles found through filtering activity.

Figure 3.

Web of Sciences selected categories.

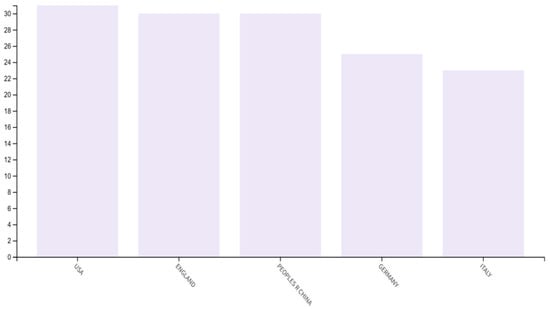

Coming to the geographical origin of contributions (Figure 4), the more consistent production of knowledge is attributed to the US and China, where DER and EC are relevant topics, due to several factors: increasing energy demand, huge remote areas where the grid connection is difficult and expensive, and a growing awareness of climate change issues. Nevertheless, in the top five can be found England, Germany, and Italy. This is quite an important acknowledgment for European research that demonstrates the strong focus on EC. That ranking reflects a real-world scenario, where the UK exhibits an already mature market environment related to EC, while Germany has the European record amount of 1751 active communities [31] and Italy is currently at the initial stages, with an allocated budget of 2.2 billion from PNRR public investment program.

Figure 4.

Articles’ geographical origin.

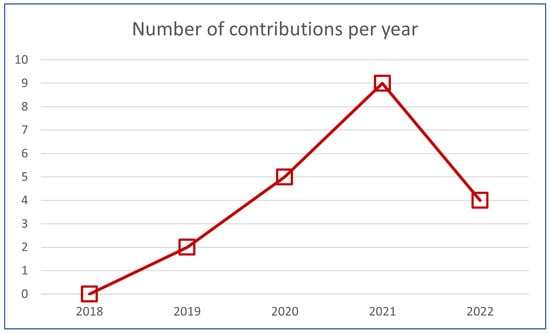

From the perspective of the publication year (Figure 5), excluding 2016, in the top five list appear contributions from 2019 onwards. This substantial increase in publications reflects the enactment of the RED II directive (Dec. 2018), which boosted the focus on self-consumption and energy communities.

Figure 5.

Articles’ publication year.

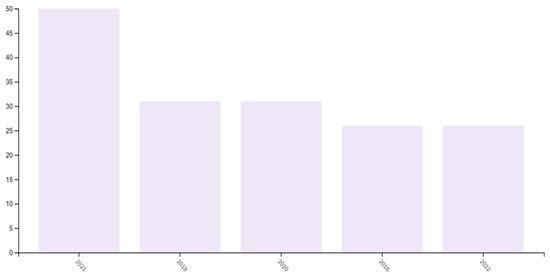

It can be helpful to perform the same analysis taking into consideration the final selection of articles. If the publication year window is almost the same as the first selection (Figure 6), the geography of contributions is quite heterogeneous.

Figure 6.

Reviewed articles: number per publication year.

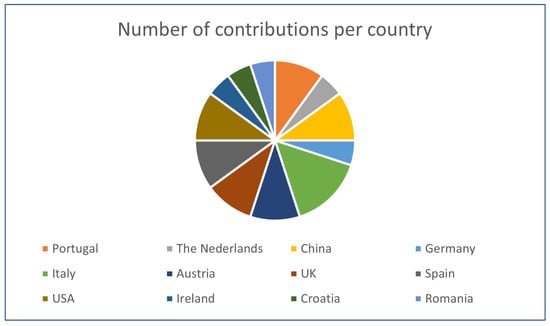

Indeed, it can be noted that 20 contributions are carried out by 12 countries (Figure 7). Nevertheless, it is quite evident the predominance of EU research.

Figure 7.

Reviewed articles: number per country.

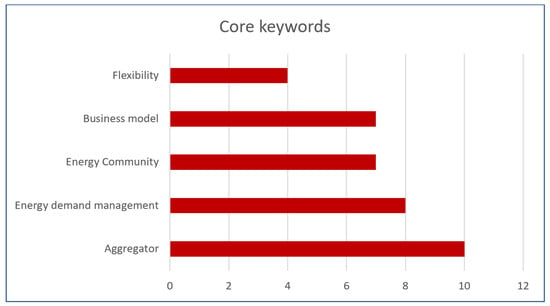

Finally, on the keyword side, the most cited ones are strictly connected with the research query (Figure 8). The top five, in fact, include “Aggregator”, “Business model”, and “Energy Community”. Terms referring to distributed renewable energies are missing since they are scattered in different synonyms and acronyms, such as “distributed energy”, “local energy”, “DERs”, etc. In any case, a remarkable placement in the list occurs for keywords related to Energy Demand (Demand Response and Demand Side Management) and Flexibility exploitation. This is an essential insight for deep literature analysis given that flexibility services will be presented frequently as one of the main activities in the Aggregator’s business.

Figure 8.

Reviewed articles: core keywords.

The final subset of contributions has been arranged in a synoptic panel to summarize the content, reporting aims, findings, and adopted method. The table is set out in Appendix A.

5. Discussion of Results

The overall framework that emerges from this overview of the literature is the absolute centrality of the Aggregator figure in the future energy system. An aggregator can be defined as a single entity engaging the electricity market, the role of which is to gather flexibility from the prosumer’s devices to sell it to the DSO or the BRP, maximizing its profit by “supplying that flexibility to reduce grid congestions, deferring the need for network reinforcements, limit any penalties due to balance supply” [32], arbitraging on energy price.

This importance is derived from its role in the energy transition, as it is recognized as an exploiter of DERs. To be an aggregator of resources is a feature that the Utilities of the future will be required to have [33]. This figure can be classified on the basis of structure and offered services. In the following section, a brief taxonomy based on reviewed literature is presented.

5.1. Taxonomy

The main categorization of the Aggregator relies on its technical activities. In [34], the Aggregator is primarily the technical operator of a Virtual Power Plant (VPP), which is defined as an “information and communications technology system with the functionalities of enhancing renewable power generation, aggregating DERs and valuing them on market” [35]. So, in this role, it performs a twofold activity on VPP:

- Commercial side: trading on wholesale markets, balancing of the internal portfolio;

- Technical side: management of the system locally in collaboration with DSO and offering ancillary and balancing services to TSO.

On the other hand, a similar distinction is offered by [36], where the Aggregator is performing basically two main functions:

- Trading energy and flexibility on behalf of aggregated consumers;

- Controlling the local market, defining contracts, managing platforms, and providing ITC services.

Another interesting categorization reported in both [37,38] is built on the types of provided flexibility:

- Demand aggregators: manage demand-side programs.

- Load aggregators: collect load flexibility, which relies on flexible, semi-flexible, and non-flexible loads.

- Production aggregators: operate small-size renewable generation units, gathering them into a VPP.

Another categorization is built on optimized resources:

- Aggregators as resource consumers: The activity is focused only on handling load elasticity, participating in DR, and monetizing obtained flexibility.

- Aggregators as resources producers: Energy is generated by small power plants, mainly renewable like solar and wind resource-based systems, or traditional ones (hydro and combined heat power).

- Aggregators as consumers and producers: Aggregators perform activities of both previous categories and use energy storage devices to increase efficiency. These facilities can be static, like batteries, or dynamic, like electric vehicles (EVs).

5.2. Partners, Relations, and Value Creation

To be a successful part of a value chain, a company has to add value through its process. This occurs with an exploration of heterogeneous resource endowments, which can be the source of advantage if “competing firms are unable to imitate these resource use” [39]. In [40], value creation for an Aggregator is separated into fundamental (or intrinsic) value and opportunistic value. The former represents the core value creation given by the Aggregator and consists of economies of scale (fixed cost offsetting) and scope (relations outline simplification due to service bundling). The latter is a transitory value that emerges from taking advantage of regulatory imperfections, information asymmetries, or favorable market designs. Hence, the authors indicate several main sources of value in Aggregators’ activity:

- Closing information gaps between Systems Operators and customers, and those that are not aware of system conditions (peak hours, prices, available control technologies);

- Managing uncertainty owing to forecasting competencies and hedging from risks on electricity markets thanks to financial products, available only to large market agents;

- Increasing agent’s engagement, which is hindered by system complexities;

- Supporting energy management automation and technological innovation (IoT equipment diffusion).

With regards to Aggregators’ key counterparts, these are mainly their technical partners. First would be technology suppliers, maintenance teams, installers, and the generic local skilled workforce. Disposing of this human capital is a strategic strength of the Aggregator and a crucial support for its activities. Next is the power System Operators, the Distribution System Operator and Transmission System Operator. The former gains an advantage in network management due to the local supervision provided by the Aggregator. Services provided, like peak smoothing, allow for avoiding onerous investments on power production and grid reinforcement [41]. The latter instead is facilitated in coordinating DERs into balance procedures, as once pooled together, they are more visible [34]. End-users or customers, who can be seen much more as a resource rather than a partner, are the last relation considered. They benefit from the Aggregator’s activity as they can receive an extra financial stream thanks to the access to the energy market that would otherwise be denied due to insufficient capacity to meet market requirements. Moreover, in [42], authors demonstrate that the Aggregator’s action, through DR programs, can bring permanent energy savings. Hence, in addition to flexibility remuneration, customers have another economic driver connected to a definitive reduction in consumption from the baseline load. Finally, another value proposition to private customers is to enjoy smart grid services and gain access to a green electricity community [43]. In conclusion, the Aggregator is a value adder since it triggers a market structure simplification and delivers substantial enhancements to its partner. However, another important result regards CO2 emissions. In [41], it is demonstrated that, independently from the adopted control strategy, the Aggregator performs a carbon dioxide emission reduction. In [38], the same result is achieved, and this influences the reputation of the Aggregator in the eyes of customers. Clients in fact express a positive attitude towards collaboration with the company to reach lower emissions, coherent with the current sensibility on climate issues.

5.3. Key Activities and Provided Services

Summing up, the main activities of an Aggregator are the following: trading surplus on the wholesale markets, optimizing energy consumption to increase self-consumption, and pooling customers’ flexibility by trading it on ancillary services markets. Flexibility can be obtained through dispatchable power plants, energy storage exploitation, or demand-side management [44]. This practice is the result of synergies between Energy Efficiency (EE) measures and Demand Response (DR) programs [45].

The first refers to permanent changes in consumption resulting from technical efficiency improvements. The second is only a temporary change in consumption, which remains the same in amount but is shifted from peak hours to off-peak hours. In [37], the authors describe the main steps of the DR implementation process, which starts with the enrollment of customers, which are qualified on the basis of DR eligibility parameters. Forecasting capability is also a required skill for Aggregators, who must predict load, price, and generation. The same themes are faced in [38], where the main goal of the research is to define the optimal acceptance level of DR from consumers’ perspective. In [46], the focus is instead on the remuneration tariff offered by the Aggregator to customers. However, writers connect the fairness of fees to acceptance level, suggesting adding a new phase called classification to typical phases of DR implementation, such as scheduling, aggregation, and remuneration. At this stage, through classification algorithms, clients are grouped on the basis of load characteristics and DR acceptance levels. This operation is made dynamically in real time and delivers homogeneous resources clusters that can be allocated a proper remuneration.

In addition to DR, the Aggregator offers another important service: energy storage systems management. These can be static devices like lithium-ion batteries typically deployed in PV plants or dynamics such as electric vehicles. In this regard, in [47], an energy cluster application is presented, where vehicles are not only part of a diffused storage scheme but are energy vectors rebalancing the grid. It is proved that this electricity reallocation technique substantially increases self-consumption without further investments. Storage management is a value-adding activity for many reasons. First, as claimed by [43], sophisticated algorithms can prevent batteries from early aging. Second, the Aggregator can make the best use of customers’ devices, which otherwise would be idle most of the day [48], permitting clients to have a greater return on their investment. Aggregators also have to offer Design, Operation, and Maintenance expertise to run aggregated customers’ devices. In the first phase, it is necessary to plan a suitable intervention on the customer’s status. In [43], the authors shape the framework in which the Aggregator approaches its customer with a defined energy project, composed of an optimized DER bundle shaped on the user’s load profile and geographic location (relevant for solar radiation).

On the O&M side, in addition to mechanical care, the capability of managing data, performing real-time forecast analysis, and handling ICT infrastructures is a relevant hard skill [38]. These platforms are essential for metering, peer-to-peer trading [36], and, independent of control strategies, performing the following daily Aggregator operations [41]:

- Day ahead: weather parameter forecast, flexibility availability calculation, communication, and bid optimization.

- Real time: flexibility activation, prosumer consumption setup, and execution.

Furthermore, customers’ data security is a relevant concern, with the increasing risk of cyber-attacks [37].

5.4. Market Participation and Strategies

It is evidence that keeping profitability in the Aggregator’s BM is crucial to activating different financial streams [36]. One way to do so is participating in different energy markets. In the European framework, the structure is sequential, which means that each player is responsible for what is offered [49].

This outline consists of three main markets:

- Day-ahead spot market (DAM);

- Intra-day market;

- Balancing market: consists of frequency containment reserve (FCR), automatic frequency containment reserve (aFCR), and manual frequency containment reserve (mFCR).

In [50], authors suggest participation in all of these markets, with the proper risk management preparedness. Nevertheless, it is more remunerative to optimize the strategy on DAM. To profit in this market, different strategies are adopted. Arbitrage on energy procurement is the main way to increase revenues in the DAM, purchasing and selling electricity at the proper time [43]. Flexibility trading is instead conducted on the intra-day market. Finally, in balancing markets, power reserves are provided to help TSO in system imbalances, together with frequency regulations and congestion management [44]. One of the most relevant streams remains to balance the internal portfolio [38]. Developing these strategies is required for the Aggregator to exhibit strong skills in asset coordination and flexibility management. This is possible thanks to optimization algorithms, typically of mixed-integer linear (MILP) optimization [34,50,51], the development of which is a crucial success factor of the aggregator’s activity.

5.5. EPS and Financial Support

A short stream of the reviewed literature explores the energy performance and supply contracting schemes in the energy sector. The most relevant topic concerning this research area is the financial sustainability to consumers that comes from this kind of agreement. As said previously, upfront capital is a relevant hurdle to DER diffusion, and mobilizing private capital turns out to be particularly hard. A first model is proposed in [52]. Here customers offer their rooftops to a Utility, which invests in renewable energy production technologies. A smart meter is installed to compute the amount of energy produced. Owners are awarded a reimbursement through bill discount or with a fixed monthly payment. This solution gives a double advantage; it increases the penetration of renewables developing distributed generation clusters, overcoming the upfront capital barrier, but it especially raises awareness among end-users on self-consumption, taking a first step in the prosumerism direction. In [53], the authors propose instead financial support to customers based on an energy supply contract (ESC) in a neighborhood EC. Here the contractor oversees the finance, design, construction, and operation of the system on the customer’s property, recovering these costs through energy sales. The study’s results demonstrate, using different business cases, that ESC works not only on heat supply but also on electricity provision. Moreover, it represents a sustainable way to reduce financial risks related to uncertainty of energy-saving mechanisms, fostering energy system modernization and lowering households’ energy costs.

5.6. Business Models

In [54], four types of BM for energy sharing are proposed. Aiming for the full exploitation of DERs, these are inspired by other BMs of famous companies operating in other sectors of sharing or the digital economy (BlaBlacar, Airbnb, eBay), basically grounded on value addition gained from

- resource sharing (storage units) among prosumers;

- connection of unrelated consumers and prosumers;

- sharing idle productive assets to increase efficiency through a virtual platform;

- participation in demand-side management schemes.

An Aggregator could actually perform each of these tasks, merging them in a unique business package. However, from the reviewed literature, researchers propose several different business models that can be summed up in three main categories.

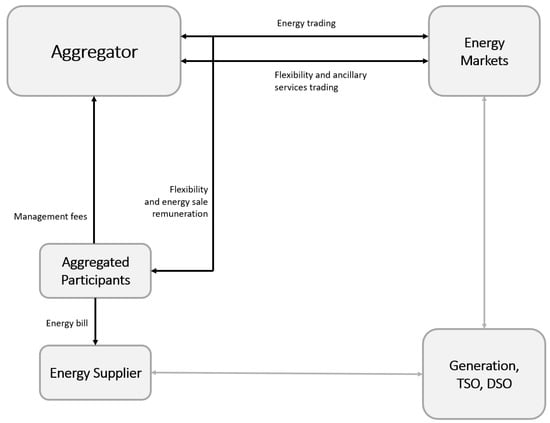

5.6.1. Standard Aggregator Business Model

This reflects the most referenced [36,48,51] BM for an Aggregator (Figure 9), which performs its usual basic functions of

Figure 9.

Standard Aggregator business model.

- trading energy and flexibilities implementing DR programs;

- managing platforms, ITC infrastructure, and defining exchange contracts.

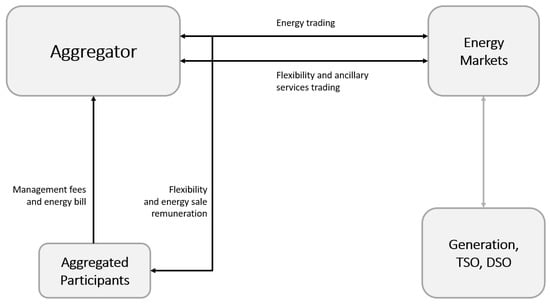

5.6.2. DER operator Business Model

This second kind of BM (Figure 10) is different from the first one simply for energy supply. Here the Aggregator is also the owner of DER power plants that manage providing locally produced green energy to aggregated users [37,38,55]. This is what mainly embodies the future setup of a public Utility, reshaping its role in the energy supply chain in a more and more decentralized manner.

Figure 10.

DER operator business model.

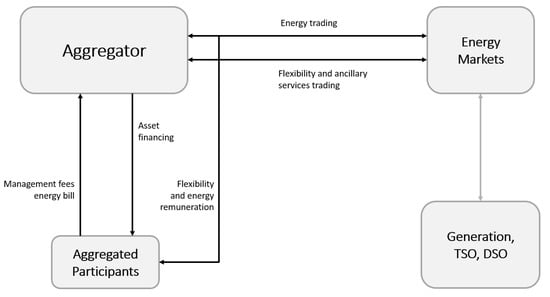

5.6.3. Central Planner Business Model

Finally, the last model (Figure 11) is the most centralist. Here the Aggregator is the cluster planner, offering all default services, including energy supply, but is also responsible for purchasing, construction, and installation of customers’ assets. The research for system optimality brings the operator to select the investment strategy for each aggregated participant, deciding where and how many resources to allocate [43,56,57].

Figure 11.

Central planner business model.

In this last setup especially, due to the high number of tasks assigned to the Aggregator, there is the risk that an Agency Problem may occur. As addressed in [51], it is crucial that contracts among aggregated customers (or EC) and support companies guarantee goal alignment. There are in fact substantial asymmetries between these two entities. The Aggregator, with respect to the client, is strong in technical competence, financial and marketing power, and information advantage. The panel below shows, for each contribution, services offered by the Aggregator in its BM.

5.6.4. Sizing and Profitability of Business Models

The measure of an energy cluster is linked to the number of participants. Because of this information, from the Aggregator perspective, investment in technologies and assets is dimensioned. Sizing is the most relevant information for business model sustainability. Talking of optimal aggregation level or optimal community size is the same; participants must exceed a minimum threshold that allows the Aggregator to create adequate economies of scale, spreading upfront costs. Even in DR programs, to ensure a sufficient diversification of load profiles, a critical size is required. Merely as an example, authors state in [58] that a group of 3000 end-users is not sufficient to keep the BM lucrative.

5.7. In the Energy Community Context

The energy community’s literature is quite recent. Business models for EC are just sketched out. However, in this early-stage context, the figure of the Aggregator is presented as a key partner of the community. Due to expertise in DER management, the Aggregator is identified as the most suitable supporter of EC in infrastructures and services management [34]. In [58], researchers offer a review of a communities BM, in which the Aggregator is a coordinator of the community, responsible for facilitating members’ relationships and pooling process. This is obviously in addition to these technical duties of the EC manager, such as metering of shared energy, administration of the local energy market, data collection and analysis, ICT platform operation, and interaction with System Operators. In the same article, researchers do not fail to underline all the hardships of EC establishment and diffusion:

- technological issues related to DER exploitation;

- socio-economic inertia: low awareness of users’ role in energy

- supply chain, the propensity to remain a passive consumer (not becoming prosumers), unpreparedness on electricity markets functioning, the inadequacy of incentives, the high initial cost of assets;

- environmental considerations: awareness of climate strike and proximity of emissions reduction goals and uncertainty about the impact of battery recycling;

- unclear institutional framework: lack of suitable legislation on roles and support schemes, vagueness on proper contractual tools.

Barriers that the Aggregator can help to overcome are certainly technical ones. Furthermore, on market guidance and environmental themes, companies can raise customers’ consciousness thanks to marketing competencies through information initiatives. If the legal setting is the only truly exogenous factor, the upfront capital is still a point of discussion. Could the Aggregator sponsor the EC establishment, financing assets, and enabling the purchase of technologies on the account of community members? This is an open question, but from the literature it emerges that the most eligible option is embodied by the third business model presented in the previous chapter. For the authors of [57], EC can develop by means of a strong partnership with an Energy Company (Utility, Aggregator), the value proposition of which consists precisely of upfront cost removal. The company involved fully finances the community, keeping control and ownership of assets and bearing all related risks. As a recovery for these costs, the investing company triggers consistent remuneration streams derived from all energy services offered.

6. Conclusions

Energy Communities diffusion is one of the most important developing frameworks to achieve energy transition by exploiting DER diffusion and, for this reason, it is a burning issue among researchers and practitioners. Understanding the role of energy companies, especially Aggregators, and the value creation process of their business was the aim of the study, and consequently a systematic literature review was carried out. The contribution of this work consists of illustrating the main features of Aggregators, pointing out how they operate in energy markets, with which services they capture value, and who their partners and customers are. Then, considerations are made concerning EC context, identifying the areas where an Aggregator could usefully support communities’ establishment and management, solving well-known hindrances. Finally, regarding the big picture, through the review of selected articles the following overall remarks are raised.

Firstly, in the energy system, the Aggregator is recognized as a value-adding entity. Several studies reveal that the Aggregator has a positive impact on aggregated customers, in terms of environmental, social, and economic indicators [34,41,42,51,59]. This is an important acknowledgment, as it delineates a component that can be put at the center of the system and that may offer all required capabilities to successfully connect end-users and System Operators. Alongside the acknowledgment, this evidence shall encourage policies oriented towards fostering the implementation phase for both energy communities and Aggregators’ business models, as often there is a lack of operative guidelines to realize projects, and this is particularly true for the energy community environment.

Secondly, upfront capital is recognized as one of the most relevant problems in aggregation [43,51,53,57,58]. Among the aforementioned aggregation difficulties, the steeper slope to climb is the financial one. To solve this issue, a few articles propose business outlines where the Aggregator is sustaining financial customers in their path to becoming prosumers, managing the community with higher or lower levels of control. A way to express this support, recovering from incurred costs, is through ESC contracting. Different studies have assessed that this kind of agreement keeps business models profitable, empowering DER diffusion and aggregation [6,41,43,48]. Although an extensive and detailed analysis of the financial feasibility of these business models is still missing in the literature, we think that further research shall focus on this aspect, in order to also understand how to design proper incentives and supporting measures to foster the development of aggregations. Finally, strictly connected with this topic is the level of aggregation. Sizing is indeed a key point in business model sustainability [47,50,51,53,56,58]. For both demand response programs and productive asset investment viability, having a minimum number of participants is crucial, but also on this issue, the literature presents a huge knowledge gap. A much deeper investigation is therefore required on the sizing of local communities. The results will be helpful to support the development of programs for citizen engagement in the Energy Transition.

Author Contributions

M.B.: original draft, revision, supervision; G.M.: conceptualization, investigation, original draft, revision. All authors have read and agreed to the published version of the manuscript.

Funding

Levi Cases Centre for Energy Economics and Technology of the University of Padua, under the project “The future of energy: institutions, regulation and enabling factors”.

Conflicts of Interest

The authors have no conflict of interest to declare.

Appendix A

Table A1.

Synoptic table of reviewed contributions.

Table A1.

Synoptic table of reviewed contributions.

| Synoptic Table | ||||

|---|---|---|---|---|

| Authors | Title | Aims | Findings | Methods |

| Reis, IFG; Goncalves, I; Lopes, MAR; Antunes, CH | Business models for energy communities: A review of key issues and trends | Review business models for Energy Community, focusing on value proposition of this new framework. | Several trends emerged: majority of BM are focused on self-consumption and trading surplus, and integration of demand flexibility programs or electric vehicles is still scarce; cooperatives are the most diffused initiative; customer-side investment is the mostly used financing solution. | Review |

| Okur, O; Heijnen, P; Lukszo, Z | Aggregator’s business models in residential and service sectors: A review of operational and financial aspects | Provide insights on financial and operational aspects of Aggregator’s business models | Different strategies are discussed: exploit flexibility trading (in intra-day and day-ahead markets), provide power reserve and congestion management, balance the internal asset portfolio. Lack of investigation emerges on financial relations between Aggregator and electricity markets, Aggregators and consumers, business model feasibility. No investigation on business models involving battery energy storage systems. | Review |

| Iazzolino, G; Sorrentino, N; Menniti, D; Pinnarelli, A; De Carolis, M; Mendicino, L | Energy communities and key features emerged from business models review | Identify key elements of Energy Community business models, testing through simulation the economic feasibility of the proposed framework in both Aggregator’s and end users’ perspectives. | Size of EC results a key element in the BM sustainability. Financial reasoning is required for big communities, as smaller ones develop following non-economic drivers (social and environmental). Initial investment is still a tough obstacle to overcome. | Simulation Analysis |

| Lu, XX; Li, KP; Xu, HC; Wang, F; Zhou, ZY; Zhang, YG | Fundamentals and business model for resource aggregator of demand response in electricity markets | Describe fundamentals features and business mechanisms of resource Aggregators in the electricity market. | Main features of Aggregators’ business model are the following: enrollment and qualification of customers, information prediction, trading. In the energy system perspective, Aggregator creates value in assisting the system operator to better match the requirements of different markets, such as the long-term planning requirements of the capacity market and managing bi-directional information’s flow. | Review |

| Schwabeneder, D; Corinaldesi, C; Lettner, G; Auer, H | Business cases of aggregated flexibilities in multiple electricity markets in a European market design | Investigate the economic benefits of a business model for aggregation of residential flexibility, based on multiple markets participation. | The possibility to access balancing and intraday markets can significantly improve economic benefits compared to single-market optimization. Battery storages contribute most to these benefits. Business models on multiple markets are complex in terms of business model design and optimization, but they are economically advantageous for both aggregators and customers. | Case Study |

| Specht, JM; Madlener, R | Energy Supplier 2.0: A conceptual business model for energy suppliers aggregating flexible distributed assets and policy issues raised | Shape a conceptual business model of an “Energy Supplier 2.0”, as an evolution from the traditional model of electricity provider to the aggregator of flexibility capacities at the household level. | A new customer-driven business model for future energy suppliers, in which they would act both as an energy supply contractor (through third-party ownership) and an aggregator of energy assets for its customers, using the assets’ flexibility to generate additional revenue streams by solving issues for the other market participants. Households would be massively supported by the process of becoming prosumers without having to take any risks or having to engage a lot themselves or suffering from a decrease in comfort in their daily life. | Theory |

| Fioriti, D; Frangioni, A; Poli, D | Optimal sizing of energy communities with fair revenue sharing and exit clauses: Value, role and business model of aggregators and users | Discuss a business model for Aggregator in the Energy Community context, solving its optimization problem by taking into account all the most relevant pitfalls such as benefit sharing and fair services payment. | Through enabling energy sharing, increasing self-consumption, and renewable technologies penetration, Aggregator promotes social, technical, and environmental benefits for the community, allowing a cost reduction and suggesting the positivity of its role in the EC context. So, it shall operate directly with the community, under a fair remuneration scheme, that is proposed. Results show that 16–24% of generated savings can be the right share for Aggregator. | Case Study |

| Chen, Y; Zhao, CH | Review of energy sharing: Business models, mechanisms, and prospects | Review of concepts, structures, applications, models, and designs in the emerging energy-sharing economy. | Four categories of the business model are identified to optimize DERs sharing: company-owned resources sharing (storage), a company acting as an intermediate to connect consumers and service providers, sharing of idle consumer assets to increase efficiency through a virtual platform operated by the company, demand response program to minimize the global social cost of the system. | Review |

| Monsberger, C; Fina, B; Auer, H | Profitability of Energy Supply Contracting and Energy Sharing Concepts in a Neighborhood Energy Community: Business Cases for Austria | Evaluate the profitability of energy contractors BM in different business cases for energy cost savings services | The profitability of contractors is ensured in each business case. The financing activity of contractors, through energy supply contracting for electricity, is the key to overcoming relevant upfront investment costs and unlocking high energy-saving potential technologies. It is proved also that energy supply contracting benefits both the contractor and then residents. | Case Study |

| Rodrigues, B; Anjos, MF; Provost, V | Market integration of behind-the-meter residential energy storage | Proposes an innovative business model to harness the potential of aggregating behind-the-meter residential storage in which the aggregator compensates participants for using their storage system on an on-demand basis | Case study results confirm that the proposed business model has strong economic potential for prosumers and Aggregators. Profits seem sufficient to mitigate the important equipment costs incurred by the Aggregator or Utility when aggregating residential Energy Storage Systems (smart controllers). The correct compensation of participants is the main driver of a successful implementation. | Case Study |

| Eras-Almeida, AA; Egido-Aguilera, MA; Blechinger, P; Berendes, S; Caamano, E; Garcia-Alcalde, E | Decarbonizing the Galapagos Islands: Techno-Economic Perspectives for the Hybrid Renewable Mini-Grid Baltra-Santa Cruz | Perform several techno-economic assessments, focusing on different electricity demand scenarios, to identify the most reliable alternatives for the progressive decarbonization of this local energy system. The comprehensive business model is proposed to achieve a resilient energy supply, based on a combination of auctions and energy community models. | Results show that photovoltaic generation is the most techno-economically viable technology for Galapagos because of solar resources and investment prices. Its implementation, coupled with a battery storage system, makes the LCOE more affordable. Moreover, due to the low availability of land, a distributed generation is posited as the most attractive alternative. A widespread installation of this technology is supported by an auction-based business model, and so the capacity required by the residential and commercial sectors for distributed generation is provided. Then equipped citizens create cooperatives according to the energy community framework. The aggregator here joins only as an O&M operator. | Case Study |

| Silva, C; Faria, P; Vale, Z | Demand Response and Distributed Generation Remuneration Approach Considering Planning and Operation Stages | Find new business models to provide a practical solution that includes the concepts of demand response and distributed generation in the energy markets, managing uncertainties associated with the aggregation of small resources. The main goal of the study is to define a method to allow fair remuneration on a real-time basis. | After testing four different remuneration methods, a business model for Aggregator (VPP - virtual power player) is proposed with four main phases: optimal scheduling, aggregation, remuneration, and classification. This added new (w.r.t. the literature) classification phase, has the main purpose of assisting the Aggregator in creating groups of remuneration in a real-time framework, considering also results from optimal scheduling of the system. | Case Study |

| Barbose, G; Satchwell, AJ | Benefits and costs of a utility-ownership business model for residential rooftop solar photovoltaics | Study the financial benefits and costs of a business model based on allowing utilities to own and operate rooftop solar systems, in return for fixed monthly payments or bill credits. | Over a 20-year period, the program increases shareholder earnings by 2–5% relative to a no-solar scenario, compared to a 2% earnings loss when an equivalent amount of rooftop solar is instead owned by non-utility parties: the conclusion is that the program could therefore be attractive from the perspective of utility investors. | Simulation Analysis |

| Barbero, M; Casals, LC; Corchero, C | Comparison between economic and environmental drivers for demand side Aggregator | Find the best strategy to adopt in demand-side flexibility for Demand Aggregators, in the case of residential and tertiary buildings. This study compares two Demand Aggregators strategies and analyses the effect of CO2 prices on the Demand Aggregator business model. | Results show that Demand Response activities reduce both the costs and the building CO2 emissions independently from the strategy adopted, and so this is one key driver for the Aggregator’s activity. | Case Study |

| Henriquez-Auba, R; Hidalgo-Gonzalez, P; Pauli, P; Kalathil, D; Callaway, DS; Poolla, K | Sharing economy and optimal investment decisions for distributed solar generation | Evaluate three different models to address the distributed solar photovoltaic (PV) investment problem: the status quo of net-metering, a sharing economy model, and a cooperative PV decision problem faced by an aggregator participating in wholesale electric markets. | Proposed business models, such as the sharing economy model or cooperative participation (aggregator managed), offer a plausible pathway to maintain and even accelerate PV investment. Discussing attractiveness for prosumers, no PV investment occurs if remuneration is equal to wholesale prices. | Case Study |

| Bahloul, M; Breathnach, L; Cotter, J; Daoud, M; Saif, A; Khadem, S | Role of Aggregator in Coordinating Residential Virtual Power Plant in StoreNet: A Pilot Project Case Study | Assessment of business models of a DERs Aggregator with different control strategies for Virtual Power Plants (VPP) management. The role of the Aggregator turns out to be relevant in allowing the participation of consumers in the VPP community, which exhibits significative cost reduction. | Five control approaches for VPP are analyzed: as a result, the capacity of batteries is the main driver of business model economic feasibility. Additional revenue streams thanks to ancillary and reserve markets participation are a valuable option for the Aggregator only if a sophisticated optimization algorithm is designed. | Case Study |

| Barone, G; Buonomano, A; Forzano, C; Giuzio, GF; Palombo, A | Increasing self-consumption of renewable energy through the Building to Vehicle to Building approach applied to multiple users connected in a virtual micro-grid | Asses a novel energy management approach, namely Building to Vehicle to Building, in which electric vehicles act as vector devices for renewable energy exchanges among buildings within an energy cluster. The proposed energy management scheme represents an example of novel aggregator energy and business model. | Simulation results, linked to the case study and the simulated climate, suggest that this BM provide effective benefits to the whole systems in terms of reduction of electricity consumptions from the power grid, increase of the self-consumption of renewable energy, and reduction of operating costs achieved without the implementation of additional technologies. | Case Study |

| Braunholtz-Speight, T; McLachlan, C; Mander, S; Hannon, M; Hardy, J; Cairns, I; Sharmina, M; Manderson, E | The long-term future for community energy in Great Britain: A co-created vision of a thriving sector and steps towards realizing it | Using the concept of business models, interrogate how community energy could be structured in the future, diversifying from its current focus on renewable electricity generation and energy efficiency, into new areas of the energy system: demand-side flexibility, mobility, and heat. | Three main key findings are delivered. Confederation of community energy groups may be a way to resolve the tension between achieving economies of scale and preserving local groups’ roots in their communities. Technological change is one enabler of new business models. Community energy has a positive impact on social and environmental sides, defining an equitable and accountable system, based on strong and stable human relationships where “no one is left behind”. | Interview |

| Maric, LL; Keko, H; Delimar, M | The Role of Local Aggregators in Delivering Energy Savings to Household Consumers | Evaluate new BM based on Aggregator, in which it serves as a permanent energy savings provider, through asset optimization, and not only as a medium to market participation. | It is proved that the focus on exploiting the individual flexibility of consumers brings to the extraction of a load reduction of 10% per asset. These little individual amounts, if aggregated, can deliver a consistent cash business opportunity for the local Aggregator. | Case Study |

| Tantau, A; Puskas-Tompos, A; Fratila, L; Stanciu, C | Acceptance of Demand Response and Aggregators as a Solution to Optimize the Relation between Energy Producers and Consumers to Increase the Amount of Renewable Energy in the Grid | Analyze the importance of demand response and the role of Aggregator for the new development of the electricity market, researching the optimal acceptance level on the energy consumer side. | Outcome of the research: DR programs attract consumers and new business models can be shaped around Aggregator’s figure, as consumers show good attitude to it. An important driver for DR diffusion is the awareness of contributing to reduction of CO2 emissions and global warming. | Survey |

References

- Mbah, R.E.; Wasum, D. Russian-Ukraine 2022 War: A Review of the Economic Impact of Russian-Ukraine Crisis on the USA, UK, Canada, and Europe. Adv. Soc. Sci. Res. J. 2022, 9, 144–153. [Google Scholar] [CrossRef]

- Boomsma, T.K.; Meade, N.; Fleten, S.E. Renewable energy investments under different support schemes: A real options approach. Eur. J. Oper. Res. 2012, 220, 225–237. [Google Scholar] [CrossRef]

- Hahnel, U.J.; Herberz, M.; Pena-Bello, A.; Parra, D.; Brosch, T. Becoming prosumer: Revealing trading preferences and decision-making strategies in peer-to-peer energy communities. Energy Policy 2020, 137, 111098. [Google Scholar] [CrossRef]

- De Sisternes, F.J.; Jenkins, J.D.; Botterud, A. The value of energy storage in decarbonizing the electricity sector. Appl. Energy 2016, 175, 368–379. [Google Scholar] [CrossRef]

- Agostini, M.; Bertolini, M.; Coppo, M.; Fontini, F. The participation of small-scale variable distributed renewable energy sources to the balancing services market. Energy Econ. 2021, 97, 105208. [Google Scholar] [CrossRef]

- Wu, Y.; Wu, Y.; Cimen, H.; Vasquez, J.C.; Guerrero, J.M. Towards collective energy Community: Potential roles of microgrid and blockchain to go beyond P2P energy trading. Appl. Energy 2022, 314, 119003. [Google Scholar] [CrossRef]

- Talari, S.; Khajeh, H.; Shafie-khah, M.; Hayes, B.; Laaksonen, H.; Catalão, J.P.S. Chapter 5-The role of various market participants in blockchain business model. In Blockchain-Based Smart Grids; Shafie-khah, M., Ed.; Academic Press: Cambridge, MA, USA, 2020; pp. 75–102. [Google Scholar] [CrossRef]

- Gharehpetian, G.B.; Mousavi Agah, S.M.; Gharehpetian, G.B. Distributed Generation Systems: Design, Operation and Grid Integration; Butterworth-Heinemann, An Imprint of Elsevier: Oxford, UK; Cambridge, MA, USA, 2017. [Google Scholar]

- Nguyen, T.T.; Martin, V.; Malmquist, A.; Silva, C.A. A review on technology maturity of small scale energy storage technologies. Renew. Energy Environ. Sustain. 2017, 2, 36. [Google Scholar] [CrossRef]

- Mahish, P.; Mishra, M.R.; Mishra, S. Distributed generating system integration: Operation and control. In Microgrid Cyberphysical Systems; Elsevier: Amsterdam, The Netherlands, 2022; pp. 29–66. [Google Scholar] [CrossRef]

- Akorede, M.F.; Hizam, H.; Pouresmaeil, E. Distributed energy resources and benefits to the environment. Renew. Sustain. Energy Rev. 2010, 14, 724–734. [Google Scholar] [CrossRef]

- Kumi, E.N. Chapter 1-Energy storage technologies. In Pumped Hydro Energy Storage for Hybrid Systems; Kabo-Bah, A.T., Diawuo, F.A., Antwi, E.O., Eds.; Academic Press: Cambridge, MA, USA, 2023; pp. 1–21. [Google Scholar] [CrossRef]

- Hussain, F.; Rahman, M.Z.; Sivasengaran, A.N.; Hasanuzzaman, M. Chapter 6-Energy storage technologies. In Energy for Sustainable Development; Hasanuzzaman, M., Rahim, N.A., Eds.; Academic Press: Cambridge, MA, USA, 2020; pp. 125–165. [Google Scholar] [CrossRef]

- Kalaiselvam, S.; Parameshwaran, R. Chapter 2-Energy Storage. In Thermal Energy Storage Technologies for Sustainability; Kalaiselvam, S., Parameshwaran, R., Eds.; Academic Press: Boston, MA, USA, 2014; pp. 21–56. [Google Scholar] [CrossRef]

- Chicco, G.; Di Somma, M.; Graditi, G. Overview of distributed energy resources in the context of local integrated energy systems. In Distributed Energy Resources in Local Integrated Energy Systems; Elsevier: Amsterdam, The Netherlands, 2021; pp. 1–29. [Google Scholar] [CrossRef]

- Kumar, P.; Pal, N.; Kumar, M. Hybrid operational deployment of renewable energy—A distribution generation approach. In Design, Analysis, and Applications of Renewable Energy Systems; Elsevier: Amsterdam, The Netherlands, 2021; pp. 627–643. [Google Scholar] [CrossRef]

- Tricarico, L. Is community earning enough? Reflections on engagement processes and drivers in two Italian energy communities. Energy Res. Soc. Sci. 2021, 72, 101899. [Google Scholar] [CrossRef]

- Blansfield, J.C.; Jones, K.B. Industry Response to Revenue Erosion from Solar PVs. In Distributed Generation and Its Implications for the Utility Industry; Elsevier: Amsterdam, The Netherlands, 2014; pp. 287–301. [Google Scholar] [CrossRef]

- Stagnaro, C.; Benedettini, S. Smart meters: The gate to behind-the-meter? In Behind and Beyond the Meter; Elsevier: Amsterdam, The Netherlands, 2020; pp. 251–265. [Google Scholar] [CrossRef]

- Brown, M.; Woodhouse, S.; Sioshansi, F. Chapter 1-Digitalization of Energy. In Consumer, Prosumer, Prosumager; Sioshansi, F., Ed.; Academic Press: Cambridge, MA, USA, 2019; pp. 3–25. [Google Scholar] [CrossRef]

- Zhang, C.; Wu, J.; Zhou, Y.; Cheng, M.; Long, C. Peer-to-Peer energy trading in a Microgrid. Appl. Energy 2018, 220, 1–12. [Google Scholar] [CrossRef]

- Sousa, T.; Soares, T.; Pinson, P.; Moret, F.; Baroche, T.; Sorin, E. Peer-to-peer and community-based markets: A comprehensive review. Renew. Sustain. Energy Rev. 2019, 104, 367–378. [Google Scholar] [CrossRef]

- Tushar, W.; Yuen, C.; Saha, T.K.; Morstyn, T.; Chapman, A.C.; Alam, M.J.E.; Hanif, S.; Poor, H.V. Peer-to-peer energy systems for connected communities: A review of recent advances and emerging challenges. Appl. Energy 2021, 282, 116131. [Google Scholar] [CrossRef]

- Casalicchio, V.; Manzolini, G.; Prina, M.G.; Moser, D. Optimal Allocation Method for a Fair Distribution of the Benefits in an Energy Community. Solar RRL 2022, 6, 2100473. [Google Scholar] [CrossRef]

- Lowitzsch, J.; Hoicka, C.; Van Tulder, F. Renewable energy communities under the 2019 European Clean Energy Package—Governance model for the energy clusters of the future? Renew. Sustain. Energy Rev. 2020, 122, 109489. [Google Scholar] [CrossRef]

- Lazdins, R.; Mutule, A.; Zalostiba, D. PV Energy Communities—Challenges and Barriers from a Consumer Perspective: A Literature Review. Energies 2021, 14, 4873. [Google Scholar] [CrossRef]

- Pakere, I.; Gravelsins, A.; Bohvalovs, G.; Rozentale, L.; Blumberga, D. Will Aggregator Reduce Renewable Power Surpluses? A System Dynamics Approach for the Latvia Case Study. Energies 2021, 14, 7900. [Google Scholar] [CrossRef]

- Olivella-Rosell, P.; Lloret-Gallego, P.; Munné-Collado, Í.; Villafafila-Robles, R.; Sumper, A.; Ottessen, S.; Rajasekharan, J.; Bremdal, B. Local Flexibility Market Design for Aggregators Providing Multiple Flexibility Services at Distribution Network Level. Energies 2018, 11, 822. [Google Scholar] [CrossRef]

- Brown, C. Economic Theories of the Entrepreneur: A Systematic Review of the Literature. Master’s Thesis, Cranfield University, School of Management, Bedford, UK, 2007. [Google Scholar]

- Ceglia, F.; Marrasso, E.; Pallotta, G.; Roselli, C.; Sasso, M. The State of the Art of Smart Energy Communities: A Systematic Review of Strengths and Limits. Energies 2022, 15, 3462. [Google Scholar] [CrossRef]

- Caramizaru, A.; Uihlein, A. Energy communities: An Overview of Energy and Social Innovation; Publications Office of the European Union: Luxembourg, 2020; Volume 30083. [Google Scholar]

- Merino, J.; Gómez, I.; Fraile-Ardanuy, J.; Santos, M.; Cortés, A.; Jimeno, J.; Madina, C. Fostering DER integration in the electricity markets. In Distributed Energy Resources in Local Integrated Energy Systems; Elsevier: Amsterdam, The Netherlands, 2021; pp. 175–205. [Google Scholar] [CrossRef]

- MIT Energy Initiative. Utility of the Future; MIT Energy Initiative: Cambridge, MA, USA, 2016. [Google Scholar]

- Bahloul, M.; Breathnach, L.; Cotter, J.; Daoud, M.; Saif, A.; Khadem, S. Role of Aggregator in Coordinating Residential Virtual Power Plant in “StoreNet”: A Pilot Project Case Study. IEEE Trans. Sustain. Energy 2022, 13, 2148–2158. [Google Scholar] [CrossRef]

- Sierla, S.; Pourakbari-Kasmaei, M.; Vyatkin, V. A taxonomy of machine learning applications for virtual power plants and home/building energy management systems. Autom. Constr. 2022, 136, 104174. [Google Scholar] [CrossRef]

- Braunholtz-Speight, T.; McLachlan, C.; Mander, S.; Hannon, M.; Hardy, J.; Cairns, I.; Sharmina, M.; Manderson, E. The long term future for community energy in Great Britain: A co-created vision of a thriving sector and steps towards realising it. Energy Res. Soc. Sci. 2021, 78, 102044. [Google Scholar] [CrossRef]

- Lu, X.; Li, K.; Xu, H.; Wang, F.; Zhou, Z.; Zhang, Y. Fundamentals and business model for resource aggregator of demand response in electricity markets. Energy 2020, 204, 117885. [Google Scholar] [CrossRef]

- Tantau, A.; Puskás-Tompos, A.; Fratila, L.; Stanciu, C. Acceptance of Demand Response and Aggregators as a Solution to Optimize the Relation between Energy Producers and Consumers in order to Increase the Amount of Renewable Energy in the Grid. Energies 2021, 14, 3441. [Google Scholar] [CrossRef]

- Bowman, C.; Ambrosini, V. Value Creation Versus Value Capture: Towards a Coherent Definition of Value in Strategy. Br. J. Manag. 2000, 11, 1–15. [Google Scholar] [CrossRef]

- Burger, S.; Chaves-Ávila, J.P.; Batlle, C.; Pérez-Arriaga, I.J. A review of the value of aggregators in electricity systems. Renew. Sustain. Energy Rev. 2017, 77, 395–405. [Google Scholar] [CrossRef]

- Barbero, M.; Casals, L.C.; Corchero, C. Comparison between economic and environmental drivers for demand side aggregator. Util. Policy 2020, 65, 101077. [Google Scholar] [CrossRef]

- Luttenberger Marić, L.; Keko, H.; Delimar, M. The Role of Local Aggregator in Delivering Energy Savings to Household Consumers. Energies 2022, 15, 2793. [Google Scholar] [CrossRef]

- Specht, J.M.; Madlener, R. Energy Supplier 2.0: A conceptual business model for energy suppliers aggregating flexible distributed assets and policy issues raised. Energy Policy 2019, 135, 110911. [Google Scholar] [CrossRef]

- Okur, Ö.; Heijnen, P.; Lukszo, Z. Aggregator’s business models in residential and service sectors: A review of operational and financial aspects. Renew. Sustain. Energy Rev. 2021, 139, 110702. [Google Scholar] [CrossRef]

- Wohlfarth, K.; Worrell, E.; Eichhammer, W. Energy efficiency and demand response–two sides of the same coin? Energy Policy 2020, 137, 111070. [Google Scholar] [CrossRef]

- Silva, C.; Faria, P.; Vale, Z. Demand Response and Distributed Generation Remuneration Approach Considering Planning and Operation Stages. Energies 2019, 12, 2721. [Google Scholar] [CrossRef]

- Barone, G.; Buonomano, A.; Forzano, C.; Giuzio, G.F.; Palombo, A. Increasing self-consumption of renewable energy through the Building to Vehicle to Building approach applied to multiple users connected in a virtual micro-grid. Renew. Energy 2020, 159, 1165–1176. [Google Scholar] [CrossRef]

- Rodrigues, B.; Anjos, M.F.; Provost, V. Market integration of behind-the-meter residential energy storage. J. Energy Storage 2021, 44, 103268. [Google Scholar] [CrossRef]

- Cretì, A.; Fontini, F. Economics of Electricity: Markets, Competition and Rules; Cambridge University Press: Cambridge, UK, 2019. [Google Scholar]

- Schwabeneder, D.; Corinaldesi, C.; Lettner, G.; Auer, H. Business cases of aggregated flexibilities in multiple electricity markets in a European market design. Energy Convers. Manag. 2021, 230, 113783. [Google Scholar] [CrossRef]

- Fioriti, D.; Frangioni, A.; Poli, D. Optimal sizing of energy communities with fair revenue sharing and exit clauses: Value, role and business model of aggregators and users. Appl. Energy 2021, 299, 117328. [Google Scholar] [CrossRef]

- Barbose, G.; Satchwell, A.J. Benefits and costs of a utility-ownership business model for residential rooftop solar photovoltaics. Nat. Energy 2020, 5, 750–758. [Google Scholar] [CrossRef]

- Monsberger, C.; Fina, B.; Auer, H. Profitability of Energy Supply Contracting and Energy Sharing Concepts in a Neighborhood Energy Community: Business Cases for Austria. Energies 2021, 14, 921. [Google Scholar] [CrossRef]

- Chen, Y.; Zhao, C. Review of energy sharing: Business models, mechanisms, and prospects. IET Renew. Power Gener. 2022, 16, 2468–2480. [Google Scholar] [CrossRef]

- Eras-Almeida, A.; Egido-Aguilera, M.; Blechinger, P.; Berendes, S.; Caamaño, E.; García-Alcalde, E. Decarbonizing the Galapagos Islands: Techno-Economic Perspectives for the Hybrid Renewable Mini-Grid Baltra–Santa Cruz. Sustainability 2020, 12, 2282. [Google Scholar] [CrossRef]

- Henriquez-Auba, R.; Hidalgo-Gonzalez, P.; Pauli, P.; Kalathil, D.; Callaway, D.S.; Poolla, K. Sharing economy and optimal investment decisions for distributed solar generation. Appl. Energy 2021, 294, 117029. [Google Scholar] [CrossRef]

- Reis, I.F.; Gonçalves, I.; Lopes, M.A.; Antunes, C.H. Business models for energy communities: A review of key issues and trends. Renew. Sustain. Energy Rev. 2021, 144, 111013. [Google Scholar] [CrossRef]

- Iazzolino, G.; Sorrentino, N.; Menniti, D.; Pinnarelli, A.; De Carolis, M.; Mendicino, L. Energy communities and key features emerged from business models review. Energy Policy 2022, 165, 112929. [Google Scholar] [CrossRef]

- Padghan, P.R.; Arul Daniel, S.; Pitchaimuthu, R. Grid-tied energy cooperative trading framework between Prosumer to Prosumer based on Ethereum smart contracts. Sustain. Energy Grids Netw. 2022, 32, 100860. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).