Levelized Cost Analysis for Blast Furnace CO2 Capture, Utilization, and Storage Retrofit in China’s Blast Furnace–Basic Oxygen Furnace Steel Plants

Abstract

:1. Introduction

- (1)

- The study has built a CO2 emission database for blast furnaces in China’s BF-BOF process steel plants, established candidate pipeline databases based on existing national highways and land–sea natural gas pipelines in China, and added data for offshore storage sites on top of onshore storage sites.

- (2)

- Based on the above databases, relevant technical parameters, and provincial-level economic indicators for steel plants and the CCUS retrofits of blast furnaces, this study constructs a comprehensive assessment model of source–sink matching-levelized cost in China’s steel industry.

- (3)

- Considering factors such as the future development level of CCUS technology and the carbon market, policy incentives, etc., this study obtains the economic and spatial differences of blast furnace CCUS projects and steel plants after blast furnace CCUS retrofits at the steel plant level.

2. Materials and Methods

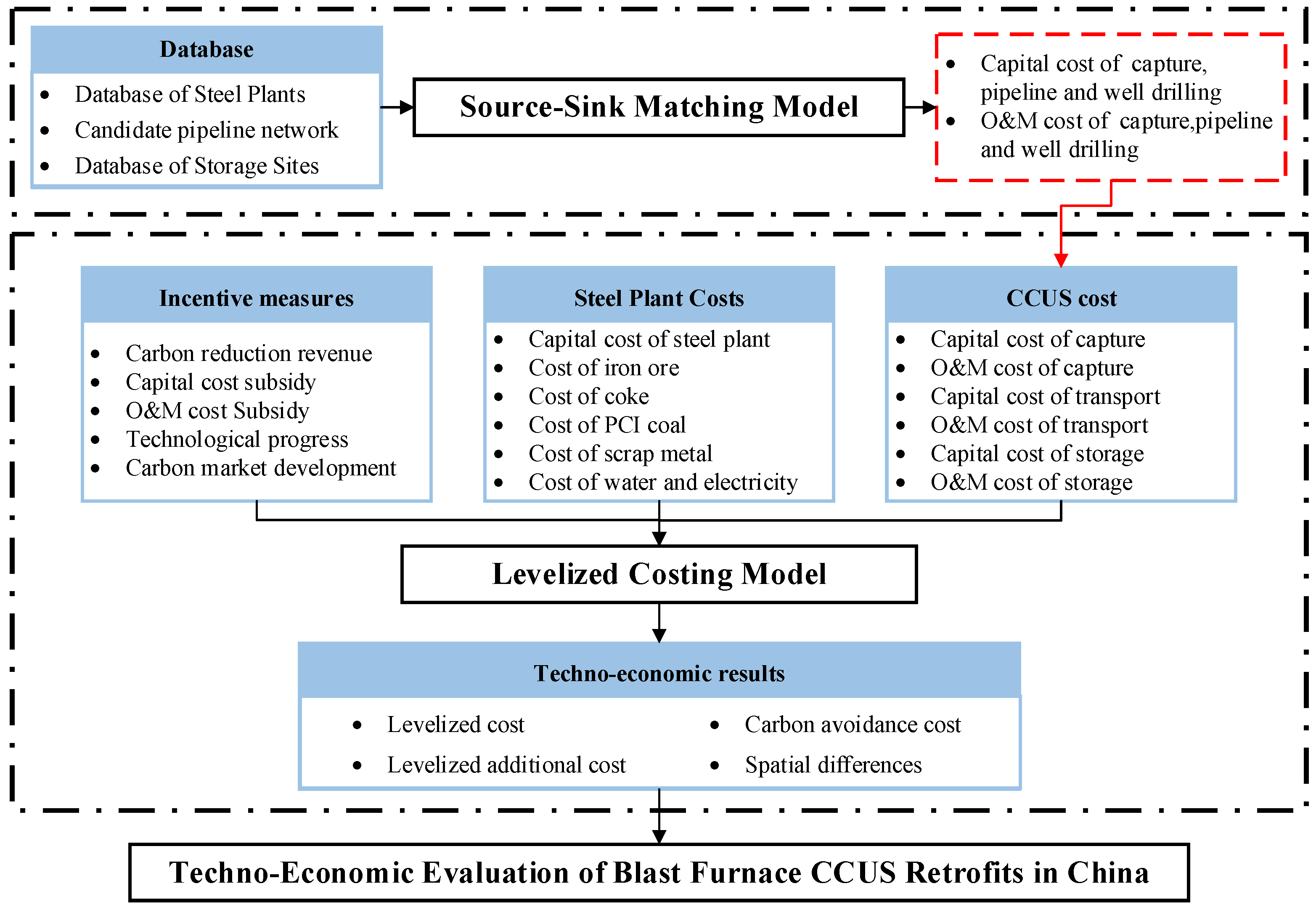

2.1. Research Framework

2.2. Modeling Methods and Techno-Economic Evaluation

2.2.1. Source–Sink Matching Method

2.2.2. Levelized Costing Model

2.2.3. Cost Structure

2.3. Scenario Definition

- (1)

- Business-as-usual scenario (BAU): Only the crude oil revenue and future technological advances are considered, and the year of CCUS deployment is 2025.

- (2)

- Carbon reduction revenue scenario (CRR): Adding carbon reduction revenue to the BAU scenario, i.e., treating CO2 emission reductions as CERs that can be traded in the carbon market and receive revenue.

- (3)

- Subsidy scenarios: Adding a government subsidy to the BAU scenario, i.e., the government subsidizes 100% of the initial investment cost of the CCUS project (S-1) or 50% of the O&M cost of the CCUS project (S-2).

- (4)

- Deferred deployment scenarios: Based on the BAU scenario, the technology cost reductions due to technological advances are considered, i.e., the year of large-scale CCUS deployment is delayed to 2030 (DD-2030), 2035 (DD-2035), 2040 (DD-2040), 2045 (DD-2045), and 2050 (DD-2050). The steel plants retrofitted with CCUS in 2025 will continue to operate until 2060, and the project operation cycle will remain unchanged after the retrofit year is deferred.

- (5)

- Comparison scenario (45Q): Adding the 45Q tax credit to the BAU scenario, the subsidy is referenced to the Inflation Reduction Act of 2022 in the U.S. This scenario serves as a comparison to study the incentive intensity of other incentive measures.

3. Results and Analysis

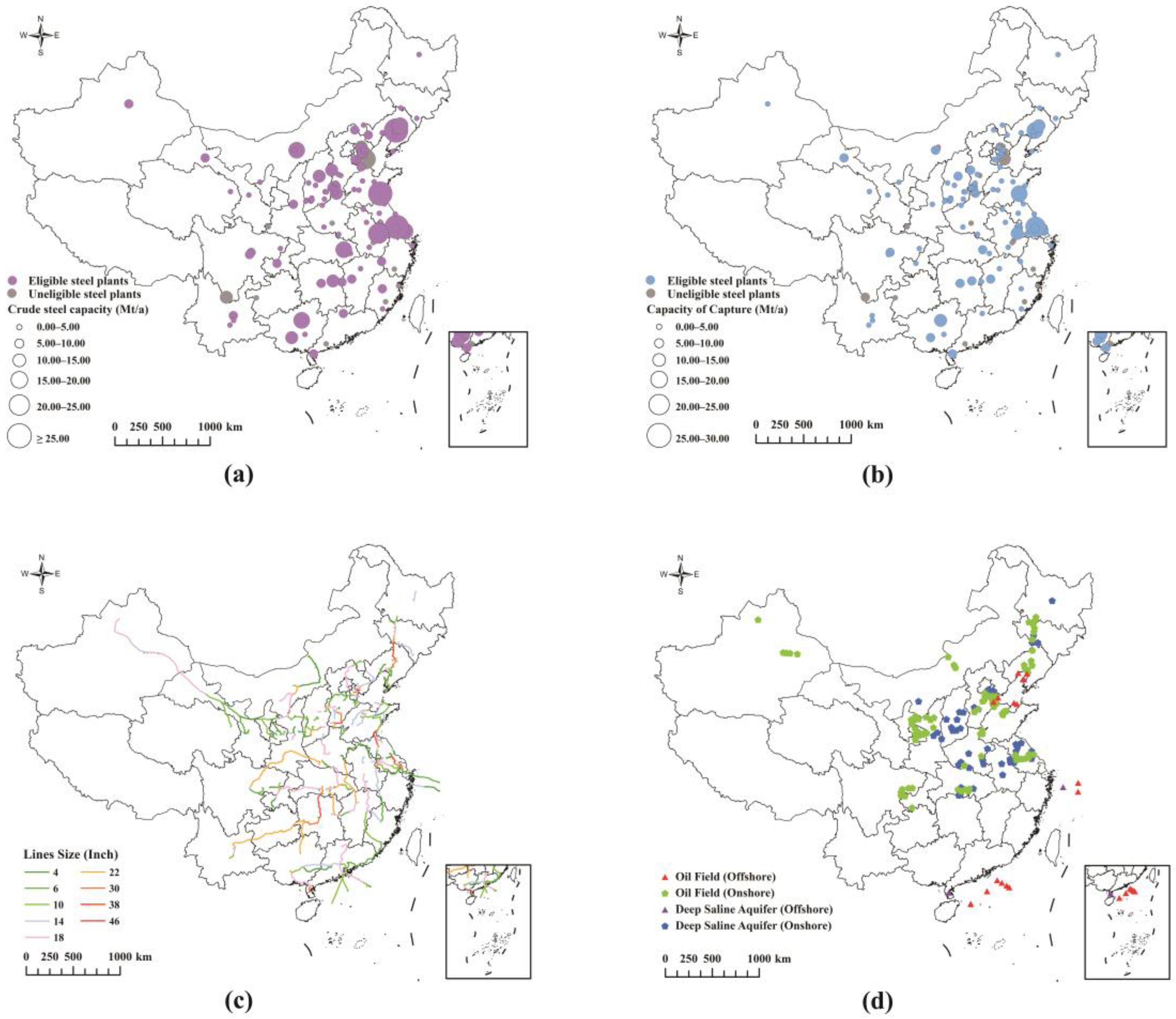

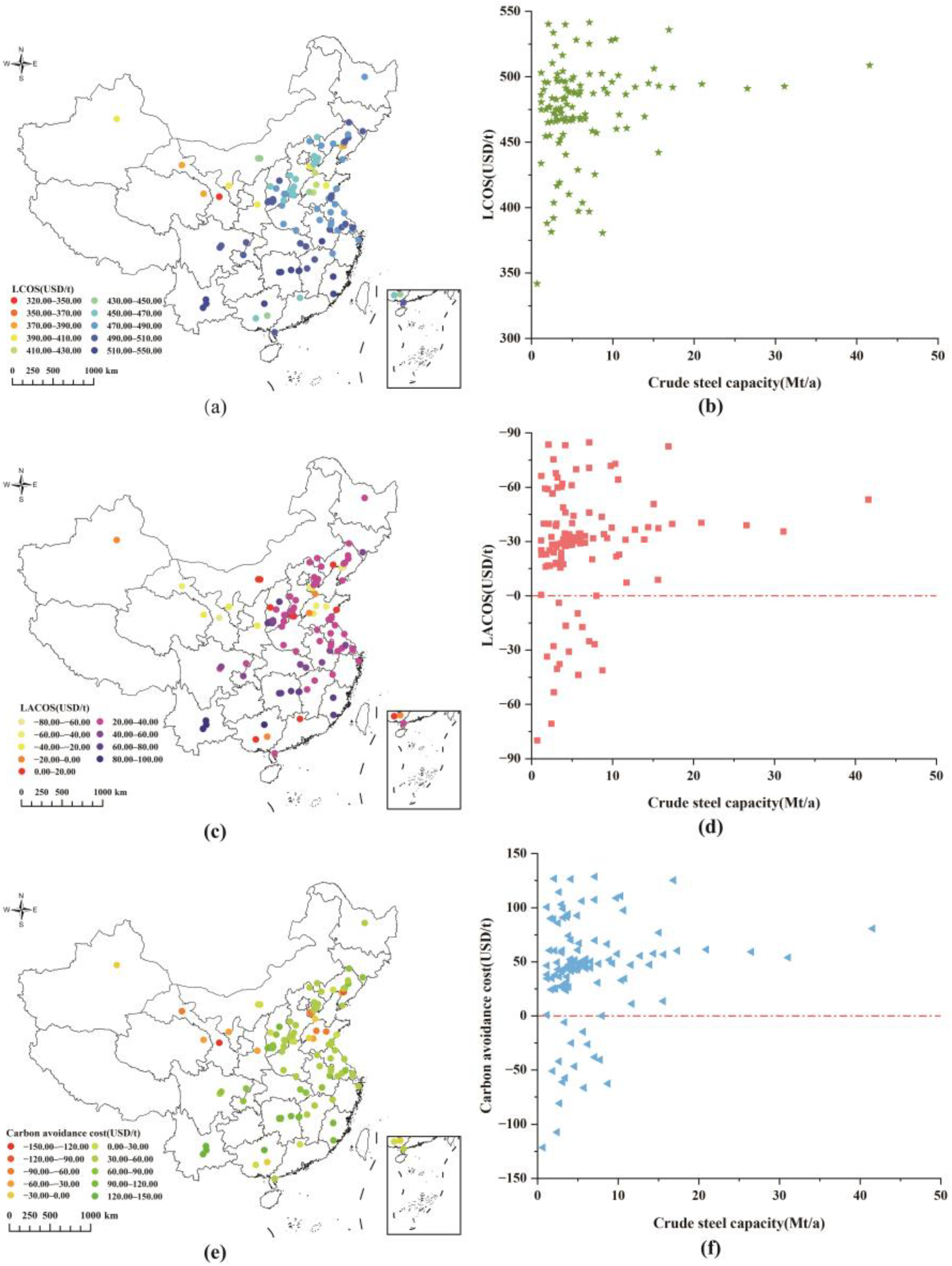

3.1. Emission Source Screening and Source–Sink Matching Results

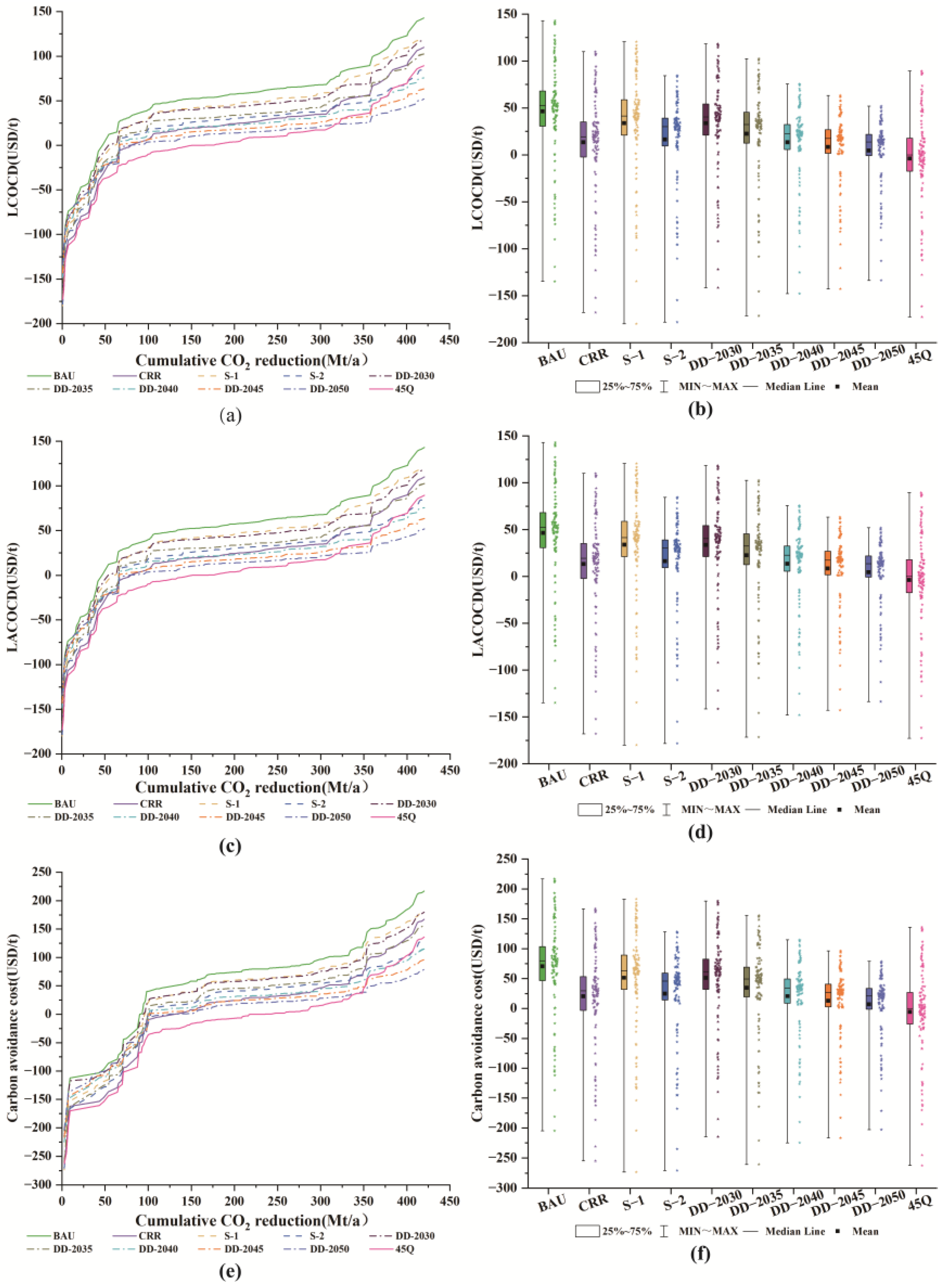

3.2. Economic Analysis of Blast Furnace CCUS Projects

3.3. Economic Analysis of Steel Plant-Coupled CCUS Project

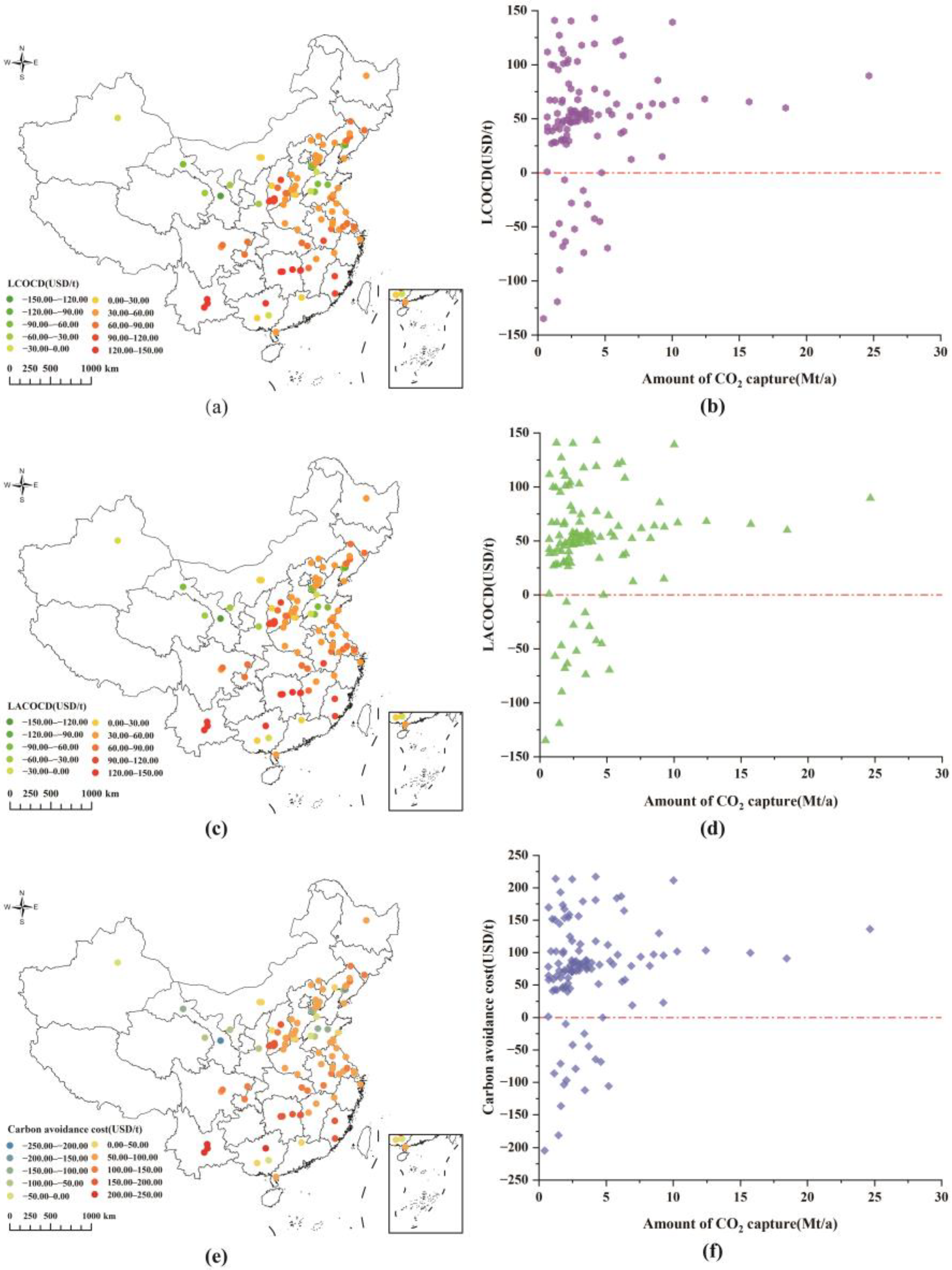

3.4. Spatial Differences in Cost

4. Conclusions

- (1)

- The relatively overlapping geographic locations of emission sources and storage sites offer the possibility of achieving low-cost pipeline construction in China. We obtained a pipeline network layout with minimized cost, but the construction of a 27,348.14 km onshore pipeline and a 1773.96 km offshore pipeline would still entail high pipeline construction costs. This creates a higher demand for more rational planning of pipeline design.

- (2)

- If no extra incentive policy is included (BAU scenario), the blast furnace CCUS retrofit project has a certain negative cost opportunity, which can achieve a 41.84 Mt/a CO2 reduction, accounting for 9.96% of the CO2 abatement potential. The introduction of conditions such as the carbon market, government subsidies, and delayed deployment times have contributed to reducing the application costs of CCUS projects. However, the large-scale deployment of CCUS projects still requires greater subsidies or accelerating technological research and development to reduce costs. Introducing the steel industry into the carbon market and maintaining a stable and positive market development will also promote the low-carbon transition of the steel industry.

- (3)

- The blast furnace CCUS projects have low application costs in North China, Northwest China, and East China’s Shandong Province, and the above regions can prioritize the deployment of blast furnace CCUS projects to provide valuable experience for their large-scale deployment in the steel industry. On the other hand, the higher-cost regions such as Fujian, Hunan, Yunnan, and northern Guangxi need to seek other low-cost, low-carbon technologies or partner with surrounding carbon-utilizing firms to achieve a low-carbon transition.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- IPCC. Global Warming of 1.5 °C; IPCC: Geneva, Switzerland, 2018. [Google Scholar]

- IEA. CO2 Emissions from Fuel Combustion: Overview; IEA: Paris, France, 2021. [Google Scholar]

- Huitu, K.; Helle, H.; Helle, M.; Kekkonen, M.; Saxén, H. Optimization of Steelmaking Using Fastmet Direct Reduced Iron in the Blast Furnace. ISIJ Int. 2013, 53, 2038–2046. [Google Scholar] [CrossRef]

- IEA. Iron and Steel Technology Roadmap; IEA: Paris, France, 2020. [Google Scholar]

- CECAMIECC, CMIPRI. Report on Energy Saving and Low Carbon Development of China’s Steel Industry; China Energy Conservation Association Metallurgical Industry Energy Conservation Committee, China Metallurgical Industry Planning and Research Institute: Beijing, China, 2020. [Google Scholar]

- NBS. Crude Steel Output in 2020; National Bureau of Statistics: Beijing, China, 2022.

- ACEE. 2020 Annual Steel Industry Environmental Assessment Report; ACEE: Beijing, China, 2021. [Google Scholar]

- IEA. China’s Net-Zero Ambitions: The Next FIVE-Year Plan Will be Critical for an Accelerated Energy Transition; International Energy Agency: Paris, France, 2020. [Google Scholar]

- Deng, L.; Adams, T.A. Comparison of steel manufacturing off-gas utilization methods via life cycle analysis. J. Clean. Prod. 2020, 277, 123568. [Google Scholar] [CrossRef]

- Perpiñán, J.; Bailera, M.; Peña, B.; Romeo, L.; Eveloy, V. Technical and Economic Assessment of Iron and Steelmaking Decarbonisation Via Power to Gas and Amine Scrubbing. SSRN Electron. J. 2022, 276, 127616. [Google Scholar]

- Chung, W.; Roh, K.; Lee, J.H. Design and evaluation of CO2 capture plants for the steelmaking industry by means of amine scrubbing and membrane separation. Int. J. Greenh. Gas Control 2018, 74, 259–270. [Google Scholar] [CrossRef]

- Tian, W.; An, H.; Li, X.; Li, H.; Quan, K.; Lu, X.; Bai, H. CO2 accounting model and carbon reduction analysis of iron and steel plants based on intra- and inter-process carbon metabolism. J. Clean. Prod. 2022, 360, 132190. [Google Scholar] [CrossRef]

- Chen, J.; Li, S.; Li, X.; Li, Y. China’s Zero-Carbon Steel Path under the Carbon Neutral Goal; Rocky Mountain Institute: Basalt, CO, USA, 2021. [Google Scholar]

- IEA. Energy Technology Perspectives 2020. In Special Report on Carbon Capture Utilisation and Storage; CCUS in Clean Energy Transitions; International Energy Agency: Paris, France, 2020. [Google Scholar]

- Zhang, X.; Yang, X.; Lu, X.; Chen, J.; Cheng, J.; Diao, Y.; Fan, J.L. China Carbon Dioxide Capture, Utilization and Storage (CCUS) Annual Report (2023); The Administrative Center for China’s Agenda 21, Global CCS Institute, Tsinghua University: Beijing, China, 2023. [Google Scholar]

- Martin-Roberts, E.; Scott, V.; Flude, S.; Johnson, G.; Haszeldine, R.S.; Gilfillan, S. Carbon capture and storage at the end of a lost decade. One Earth 2021, 4, 1569–1584. [Google Scholar] [CrossRef]

- Shen, J.; Zhang, Q.; Xu, L.; Tian, S.; Wang, P. Future CO2 emission trends and radical decarbonization path of iron and steel industry in China. J. Clean. Prod. 2021, 326, 129354. [Google Scholar] [CrossRef]

- Swennenhuis, F.; de Gooyert, V.; de Coninck, H. Towards a CO2-neutral steel industry: Justice aspects of CO2 capture and storage, biomass-and green hydrogen-based emission reductions. Energy Res. Soc. Sci. 2022, 88, 102598. [Google Scholar] [CrossRef]

- Zhang, S.; Yi, B.; Guo, F.; Zhu, P. Exploring selected pathways to low and zero CO2 emissions in China’s iron and steel industry and their impacts on resources and energy. J. Clean. Prod. 2022, 340, 130813. [Google Scholar] [CrossRef]

- Lubecki, M.; Stosiak, M.; Skačkauskas, P.; Karpenko, M.; Deptuła, A.; Urbanowicz, K. Development of Composite Hydraulic Actuators: A Review. Actuators 2022, 11, 365. [Google Scholar] [CrossRef]

- Zhang, Q.; Wei, Z.; Ma, J.; Qiu, Z.; Du, T.J.A.T.E. Optimization of energy use with CO2 emission reducing in an integrated iron and steel plant. Appl. Therm. Eng. 2019, 157, 113635. [Google Scholar] [CrossRef]

- Ho, M.T.; Bustamante, A.; Wiley, D.E. Comparison of CO2 capture economics for iron and steel mills. Int. J. Greenh. Gas Control 2013, 19, 145–159. [Google Scholar] [CrossRef]

- Tsupari, E.; Kärki, J.; Arasto, A.; Pisilä, E. Post-combustion capture of CO2 at an integrated steel mill—Part II: Economic feasibility. Int. J. Greenh. Gas Control 2013, 16, 278–286. [Google Scholar] [CrossRef]

- IEAGHG. Iron and Steel CCS Study (Techno-Economics Integrated Steel Mill); IEAGHG: Cheltenham, UK, 2013. [Google Scholar]

- Cormos, C.-C. Evaluation of reactive absorption and adsorption systems for post-combustion CO2 capture applied to iron and steel industry. Appl. Therm. Eng. 2016, 105, 56–64. [Google Scholar] [CrossRef]

- Biermann, M.; Ali, H.; Sundqvist, M.; Larsson, M.; Normann, F.; Johnsson, F. Excess heat-driven carbon capture at an integrated steel mill—Considerations for capture cost optimization. Int. J. Greenh. Gas Control 2019, 91, 102833. [Google Scholar] [CrossRef]

- Dreillard, M.; Broutin, P.; Briot, P.; Huard, T.; Lettat, A. Application of the DMXTM CO2 Capture Process in Steel Industry. Energy Procedia 2017, 114, 2573–2589. [Google Scholar] [CrossRef]

- Kim, H.; Lee, J.; Lee, S.; Lee, I.-B.; Park, J.-H.; Han, J. Economic process design for separation of CO2 from the off-gas in ironmaking and steelmaking plants. Energy 2015, 88, 756–764. [Google Scholar] [CrossRef]

- Kuramochi, T.; Ramírez, A.; Turkenburg, W.; Faaij, A. Comparative assessment of CO2 capture technologies for carbon-intensive industrial processes. Prog. Energy Combust. Sci. 2012, 38, 87–112. [Google Scholar] [CrossRef]

- Liang, X.; Qianguo, L.; Hasan, M.; Ming, L.; Qiang, L.; Jia, L.; Alisa, W.; Muxin, L.; Francisco, A. Assessing the Economics of CO2 Capture in China’s Iron/Steel Sector: A Case Study. Energy Procedia 2019, 158, 3715–3722. [Google Scholar]

- Wei, N.; Liu, S.; Jiao, Z.; Li, X.-C. A possible contribution of carbon capture, geological utilization, and storage in the Chinese crude steel industry for carbon neutrality. J. Clean. Prod. 2022, 374, 133793. [Google Scholar] [CrossRef]

- Wei, N.; Jiao, Z.S.; Ellett, K.; Ku, A.Y.; Liu, S.N.; Middleton, R.; Li, X.C. Decarbonizing the Coal-Fired Power Sector in China via Carbon Capture, Geological Utilization, and Storage Technology. Environ. Sci. Technol. 2021, 55, 13164–13173. [Google Scholar] [CrossRef]

- Ouyang, X.; Lin, B. Levelized cost of electricity (LCOE) of renewable energies and required subsidies in China. Energy Policy 2014, 70, 64–73. [Google Scholar] [CrossRef]

- IEA. Projected Costs of Generating Electricity 2020; IEA: Paris, France, 2020. [Google Scholar]

- Lazard. Levelized Cost of Energy Analysis 10.0; Lazard: New Orleans, LA, USA, 2016. [Google Scholar]

- Fan, J.-L.; Wei, S.; Yang, L.; Wang, H.; Zhong, P.; Zhang, X. Comparison of the LCOE between coal-fired power plants with CCS and main low-carbon generation technologies: Evidence from China. Energy 2019, 176, 143–155. [Google Scholar] [CrossRef]

- Vazquez, A.; Iglesias, G. Grid parity in tidal stream energy projects: An assessment of financial, technological and economic LCOE input parameters. Technol. Forecast. Soc. Chang. 2016, 104, 89–101. [Google Scholar] [CrossRef]

- Shen, W.; Chen, X.; Qiu, J.; Hayward, J.A.; Sayeef, S.; Osman, P.; Meng, K.; Dong, Z.Y. A comprehensive review of variable renewable energy levelized cost of electricity. Renew. Sustain. Energy Rev. 2020, 133, 110301. [Google Scholar] [CrossRef]

- Aquila, G.; Coelho, E.d.O.P.; Bonatto, B.D.; Pamplona, E.d.O.; Nakamura, W.T. Perspective of uncertainty and risk from the CVaR-LCOE approach: An analysis of the case of PV microgeneration in Minas Gerais, Brazil. Energy 2021, 226, 120327. [Google Scholar] [CrossRef]

- Vartiainen, E.; Masson, G.; Breyer, C.; Moser, D.; Román Medina, E. Impact of weighted average cost of capital, capital expenditure, and other parameters on future utility—scale PV levelised cost of electricity. Prog. Photovolt. Res. Appl. 2019, 28, 439–453. [Google Scholar] [CrossRef]

- Talavera, D.L.; Ferrer-Rodríguez, J.P.; Pérez-Higueras, P.; Terrados, J.; Fernández, E.F. A worldwide assessment of levelised cost of electricity of HCPV systems. Energy Convers. Manag. 2016, 127, 679–692. [Google Scholar] [CrossRef]

- Abdelhady, S.; Borello, D.; Shaban, A. Techno-economic assessment of biomass power plant fed with rice straw: Sensitivity and parametric analysis of the performance and the LCOE. Renew. Energy 2018, 115, 1026–1034. [Google Scholar] [CrossRef]

- Aquila, G.; Nakamura, W.T.; Junior, P.R.; Souza Rocha, L.C.; de Oliveira Pamplona, E. Perspectives under uncertainties and risk in wind farms investments based on Omega-LCOE approach: An analysis in São Paulo state, Brazil. Renew. Sustain. Energy Rev. 2021, 141, 110805. [Google Scholar] [CrossRef]

- Ioannou, A.; Angus, A.; Brennan, F. Stochastic Prediction of Offshore Wind Farm LCOE through an Integrated Cost Model. Energy Procedia 2017, 107, 383–389. [Google Scholar] [CrossRef]

- Lerch, M.; De-Prada-Gil, M.; Molins, C.; Benveniste, G. Sensitivity analysis on the levelized cost of energy for floating offshore wind farms. Sustain. Energy Technol. Assess. 2018, 30, 77–90. [Google Scholar] [CrossRef]

- Dahowski, R.T.; Davidson, C.L.; Li, X.C.; Wei, N. A $70/tCO2 greenhouse gas mitigation backstop for China’s industrial and electric power sectors: Insights from a comprehensive CCS cost curve. Int. J. Greenh. Gas Control 2012, 11, 73–85. [Google Scholar] [CrossRef]

- Fan, J.-L.; Xu, M.; Wei, S.; Shen, S.; Diao, Y.; Zhang, X. Carbon reduction potential of China’s coal-fired power plants based on a CCUS source-sink matching model. Resour. Conserv. Recycl. 2020, 168, 105320. [Google Scholar] [CrossRef]

- Wei, Y.-M.; Kang, J.-N.; Liu, L.-C.; Li, Q.; Wang, P.-T.; Hou, J.-J.; Liang, Q.-M.; Liao, H.; Huang, S.-F.; Yu, B. A proposed global layout of carbon capture and storage in line with a 2 °C climate target. Nat. Clim. Chang. 2021, 11, 112–118. [Google Scholar] [CrossRef]

- Zhang, X.; Li, K.; Wei, N.; Li, Z.; Fan, J.-L. Advances, challenges, and perspectives for CCUS source-sink matching models under carbon neutrality target. Carbon Neutrality 2022, 1, 12. [Google Scholar] [CrossRef]

- Tang, H.; Zhang, S.; Chen, W. Assessing Representative CCUS Layouts for China’s Power Sector toward Carbon Neutrality. In Environmental Science & Technology; American Chemical Society: Washington, DC, USA, 2021; Volume 55, pp. 11225–11235. [Google Scholar]

- Sanchez, D.L.; Johnson, N.; McCoy, S.T.; Turner, P.A.; Mach, K.J. Near-term deployment of carbon capture and sequestration from biorefineries in the United States. Proc. Natl. Acad. Sci. USA 2018, 115, 4875–4880. [Google Scholar] [CrossRef]

- Fan, J.-L.; Fu, J.; Zhang, X.; Li, K.; Zhou, W.; Hubacek, K.; Urpelainen, J.; Shen, S.; Chang, S.; Guo, S.; et al. Co-firing plants with retrofitted carbon capture and storage for power-sector emissions mitigation. Nat. Clim. Chang. 2023, 13, 807–815. [Google Scholar] [CrossRef]

- EUROFER. A Steel Roadmap for a Low Carbon Europe 2050; IEA Global Industry Dialogue and Expert Review Workshop: Paris, France, 2013. [Google Scholar]

- Fischedick, M.; Marzinkowski, J.; Winzer, P.; Weigel, M. Techno-economic evaluation of innovative steel production technologies. J. Clean. Prod. 2014, 84, 563–580. [Google Scholar] [CrossRef]

- Wörtler, M.; Dahlmann, P.; Schuler, F.; Lüngen, H.B.; Voigt, N.; Ghenda, J.; Schmidt, T. Steel’ S Contribution to a Low-carbon Europe 2050—Technical and Economic Analysis of the Sector’s CO2 Abatement Potential; The Boston Consulting Group, Steel Institue VDEh: Boston, MA, USA, 2013. [Google Scholar]

- Gardarsdottir, S.O. Technical and Economic Conditions for Efficient Implementation of CO2 Capture-Process Design and Operational Strategies for Power Generation and Process Industries; Chalmers University of Technology: Gothenburg, Sweden, 2017. [Google Scholar]

- Department of Social Development Science and Technology, MoSaT, ACCA21. Development Roadmap of Carbon Capture, Utilization and Storage Technology in China (2019 Edition); Science Press: Beijing, China, 2019.

- Mac Dowell, N.; Fennell, P.S.; Shah, N.; Maitland, G.C. The role of CO2 capture and utilization in mitigating climate change. Nat. Clim. Chang. 2017, 7, 243–249. [Google Scholar] [CrossRef]

- GCCSI. Global Status of CCS; GCCSI: Melbourne, Australia, 2021. [Google Scholar]

- Wei, N.; Li, X.; Dahowski, R.T.; Davidson, C.L.; Liu, S.; Zha, Y. Economic evaluation on CO2-EOR of onshore oil fields in China. Int. J. Greenh. Gas Control 2015, 37, 170–181. [Google Scholar] [CrossRef]

- Zhou, D.; Zhang, Y.; Haszeldine, S. Engineering Requirements for Offshore CO2 Transportation and Storage: A Summary Based on International Experiences; UK-China (Guangdong) CCUS Centre: Guangzhou, China, 2014. [Google Scholar]

- NEA. 2018 National Electricity Price Regulatory Bulletin; NEA: Washington, DC, USA, 2019. [Google Scholar]

- Mysteel. Absolute Price Index for Iron Ore; Mysteel: Shanghai, China, 2022. [Google Scholar]

- XNLSCL. National Steel Scrap Trading Guide Price. 2022. Available online: http://www.96369.net/map.aspx?type=2 (accessed on 22 October 2023).

- XNLSCL. National Coke Trading Guide Price. 2022. Available online: http://www.96369.net/map.aspx?type=4 (accessed on 22 October 2023).

- MRRN. Limestone Price Graph for 2020. Mineral Rights Resource Network: 2021. Available online: https://www.kq81.com/AspCode/SchqShow.asp?ArticleId=417922 (accessed on 22 October 2023).

- Mysteel. PCI Coal Price Index; Mysteel: Shanghai, China, 2022. [Google Scholar]

- E20. National Water Price; E20 Environment Platform: Beijing, China, 2022. [Google Scholar]

- Tong, Y.; Cai, J.; Zhang, Q.; Gao, C.; Wang, L.; Li, P.; Hu, S.; Liu, C.; He, Z.; Yang, J. Life cycle water use and wastewater discharge of steel production based on material-energy-water flows: A case study in China. J. Clean. Prod. 2019, 241, 118410. [Google Scholar] [CrossRef]

- Chen, Q.; Gu, Y.; Tang, Z.; Wei, W.; Sun, Y. Assessment of low-carbon iron and steel production with CO2 recycling and utilization technologies: A case study in China. Appl. Energy 2018, 220, 192–207. [Google Scholar] [CrossRef]

- He, H.; Guan, H.; Zhu, X.; Lee, H. Assessment on the energy flow and carbon emissions of integrated steelmaking plants. Energy Rep. 2017, 3, 29–36. [Google Scholar] [CrossRef]

- Sun, W.; Wang, Q.; Zheng, Z.; Cai, J. Material–energy–emission nexus in the integrated iron and steel industry. Energy Convers. Manag. 2020, 213, 112828. [Google Scholar] [CrossRef]

- WSA. Steel’s Contribution to a Low Carbon Future and Climate Resilient Societies; WSA: Brussels, Belgium, 2018. [Google Scholar]

- WSA. Energy Use in the Steel Industry; WSA: Brussels, Belgium, 2019. [Google Scholar]

- Zhang, F.; Zhou, Y.; Sun, W.; Hou, S.; Yu, L. CO2 capture from reheating furnace based on the sensible heat of continuous casting slabs. Int. J. Energy Res. 2018, 42, 2273–2283. [Google Scholar] [CrossRef]

- Chisalita, D.-A.; Petrescu, L.; Cobden, P.; van Dijk, H.A.J.; Cormos, A.-M.; Cormos, C.-C. Assessing the environmental impact of an integrated steel mill with post-combustion CO2 capture and storage using the LCA methodology. J. Clean. Prod. 2019, 211, 1015–1025. [Google Scholar] [CrossRef]

- Yang, L.; Xu, M.; Fan, J.; Liang, X.; Zhang, X.; Lv, H.; Wang, D. Financing coal-fired power plant to demonstrate CCS (carbon capture and storage) through an innovative policy incentive in China. Energy Policy 2021, 158, 112562. [Google Scholar] [CrossRef]

- Yang, L.; Xu, M.; Yang, Y.; Fan, J.; Zhang, X. Comparison of subsidy schemes for carbon capture utilization and storage (CCUS) investment based on real option approach: Evidence from China. Appl. Energy 2019, 255, 113828. [Google Scholar] [CrossRef]

- Yao, X.; Zhong, P.; Zhang, X.; Zhu, L. Business model design for the carbon capture utilization and storage (CCUS) project in China. Energy Policy 2018, 121, 519–533. [Google Scholar] [CrossRef]

- Zhang, X.; Huang, X.; Zhang, D.; Geng, Y.; Tian, L.; Chen, W. Research on the Pathway and Policies for China’s Energy and Economy Transformation toward Carbon Neutrality. J. Manag. World 2022, 38, 35–51. [Google Scholar]

- Cai, B.; Li, Q.; Zhang, X. Carbon Dioxide Capture, Use and Storage (CCUS) Annual Report of China (2021)—A Study of CCUS Pathways in China Beijing; Chinese Academy of Environmental Planning, Institute of Rock and Soil Mechanics, Chinese Academy of Sciences, The Administrative Center for China’s Agenda 21: Beijing, China, 2021. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Geographic Region | Province | (CNY/t) | (CNY/t) a | (CNY/t) b | (CNY/t) c | (CNY/t) | (CNY/kkWh) |

|---|---|---|---|---|---|---|---|

| Domestic Price | 113.21 | -- | -- | -- | -- | -- | |

| Imported Price | 106.84 | -- | -- | -- | -- | -- | |

| North China | Tianjin | -- | 323.38 | 263.27 | 144.41 | 0.99 | 53.68 |

| Hebei | -- | 326.49 | 0.66 | 48.94 | |||

| Shanxi | -- | 314.66 | 0.61 | 49.06 | |||

| Inner Mongolia | -- | 316.99 | 0.46 | 41.57 | |||

| Northeast China | Liaoning | -- | 371.76 | 272.66 | 150.31 4 | 0.59 | 56.53 |

| Jilin | -- | 360.63 1 | 0.59 | 55.74 | |||

| Heilongjiang | -- | 351.37 | 0.66 | 56.97 | |||

| East China | Shanghai | -- | 341.77 | 286.03 | 156.31 | 0.40 | 62.57 |

| Jiangsu | -- | 352.07 | 0.29 | 59.78 | |||

| Zhejiang | -- | 340.71 | 0.40 | 63.52 | |||

| Anhui | -- | 344.78 1 | 0.31 | 58.38 | |||

| Fujian | -- | 344.78 1 | 0.35 | 59.38 | |||

| Jiangxi | -- | 357.26 | 0.36 | 63.78 | |||

| Shandong | -- | 344.78 2 | 0.72 | 62.69 | |||

| Central China | Henan | -- | 329.56 2 | 276.18 | 158.59 | 0.69 | 54.33 |

| Hubei | -- | 348.64 | 0.32 | 66.58 | |||

| Hunan | -- | 339.10 1 | 0.38 | 70.02 | |||

| South China | Guangdong | -- | 367.53 | 285.09 3 | 134.38 5 | 0.53 | 67.27 |

| Guangxi | -- | 366.45 1 | 0.24 | 60.94 | |||

| Southwest China | Chongqing | -- | 355.78 | 293.08 | 134.38 5 | 0.50 | 62.94 |

| Sichuan | -- | 363.66 | 0.46 | 67.16 | |||

| Guizhou | -- | 359.72 1 | 0.40 | 50.70 | |||

| Yunnan | -- | 359.72 1 | 0.55 | 62.92 | |||

| Northwest China | Shaanxi | -- | 297.03 | 249.86 | 101.35 | 0.67 | 49.85 |

| Gansu | -- | 322.77 1 | 0.30 | 43.52 | |||

| Qinghai | -- | 322.77 1 | 0.36 | 42.74 | |||

| Ningxia | -- | 322.77 1 | 0.50 | 37.93 | |||

| Xinjiang | -- | 348.51 | 0.47 | 32.81 | |||

| Unit | kg/t Crude Steel | kWh/t Crude Steel | |||||

|---|---|---|---|---|---|---|---|

| Value | 1361.23 | 138.33 | 270.00 | 321.93 | 196.40 | 2.65 | 450.00 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gu, C.; Xie, J.; Li, X.; Gao, X. Levelized Cost Analysis for Blast Furnace CO2 Capture, Utilization, and Storage Retrofit in China’s Blast Furnace–Basic Oxygen Furnace Steel Plants. Energies 2023, 16, 7817. https://doi.org/10.3390/en16237817

Gu C, Xie J, Li X, Gao X. Levelized Cost Analysis for Blast Furnace CO2 Capture, Utilization, and Storage Retrofit in China’s Blast Furnace–Basic Oxygen Furnace Steel Plants. Energies. 2023; 16(23):7817. https://doi.org/10.3390/en16237817

Chicago/Turabian StyleGu, Changwan, Jingjing Xie, Xiaoyu Li, and Xu Gao. 2023. "Levelized Cost Analysis for Blast Furnace CO2 Capture, Utilization, and Storage Retrofit in China’s Blast Furnace–Basic Oxygen Furnace Steel Plants" Energies 16, no. 23: 7817. https://doi.org/10.3390/en16237817