Abstract

As new sources of energy and advanced technologies are used, there is a continuous evolution in energy supply, demand, and distribution. Advanced nuclear reactors and clean hydrogen have the opportunity to scale together and diversify the hydrogen production market away from fossil fuel-based production. Nevertheless, the technical uncertainties surrounding nuclear hydrogen processes necessitate thorough research and a solid development effort. This paper aims to position pink hydrogen for nuclear hydrogen production at the forefront of sustainable energy-related solutions by offering a comprehensive review of recent advancements in nuclear hydrogen production, covering both research endeavors and industrial applications. It delves into various pink hydrogen generation methodologies, elucidating their respective merits and challenges. Furthermore, this paper analyzes the evolving landscape of pink hydrogen in terms of its levelized cost by comparatively assessing different production pathways. By synthesizing insights from academic research and industrial practices, this paper provides valuable perspectives for stakeholders involved in shaping the future of nuclear hydrogen production.

1. Introduction

Several years have passed since the Paris Agreement [1], and despite tremendous efforts toward an energy transition, the vision of zero-carbon societies seems more distant than ever. During the early stage of the transition, a key focus for research and policy was to demonstrate the technological and economic feasibility of sustainable energy solutions. Today, the situation is different [2]. Transitioning toward a low-carbon economy will require nothing less than a paradigm shift, necessitating large-scale investments [3]. Power systems will be strained to their limits by the combination of electricity produced from distributed and intermittent renewable energy sources and ever-increasing electrical demand. Grid bottlenecks related to grid capacity, intermittency, limited electrical storability, and backup generation capacity will be challenging to address.

Hydrogen’s (H2) unique properties make it a promising alternative fuel that has emerged as a key player in the transition toward a sustainable energy future; the potential benefits of an H2 economy are gradually becoming popular discussion points in the “net-zero” strategies of multiple countries [4,5]. Even though H2 has the highest energy content of any known fuel and is the most abundant element in the universe, it is not readily available in nature and must be produced through a variety of methods [6]. These methods include fossil fuel-based H2 production, biomass-based H2, and H2 from water, requiring heat and electricity. Approximately 70% of power generation plants worldwide are tied to the usage of H2 in open-cycle or combined-cycle gas turbines. Another 10% of power generation utilizes H2 in fuel cells, while 3% of stated projects involve the co-firing of ammonia in coal-fired power plants. Geographically, the majority of these projects reside in the Asia-Pacific area with a share of 39%, followed by Europe and North America with shares of 36% and 25%, respectively [7]. Advocates envision a future in which H2 fuel cells are used not only across the electricity value chain but also in transportation, heat, as well as in the industry sector as feedstock.

Currently, the vast majority of H2 produced is derived from steam reformation of natural gas, making most of the H2 available in today’s market essentially a fossil fuel. According to IEA [7], although low-carbon substitutes such as “Pink Hydrogen” (pink H2) generated from nuclear-powered electrolysis and “green hydrogen” generated from electrolysis powered by renewable energy sources (RESs) remain expensive alternatives, the annual production of low-emission H2 may reach 38 Mt in 2030 if all announced projects are realized; however, 17 Mt come from projects at initial phases of advancement. More specifically, regarding pink H2, the direct emissions from nuclear-based generation are zero. Nonetheless, the nuclear fuel cycle—including uranium mining, conversion, enrichment, and fuel fabrication—results in greenhouse gas (GHG) emissions from 2.4 gCO2-eq/kWh to 6.8 gCO2-eq/kWh. Considering the aforementioned values, the emission intensity of pink H2 generation from nuclear power falls within the range of 0.1 kgCO2-eq/kgH2 to 0.3 kgCO2-eq/kgH2 [7].

With the geopolitical impact of natural gas price volatility intensifying the focus on both low-carbon alternatives and the security of supply, the opportunity for nuclear-powered H2 is greater than ever. A recent analysis from the Nuclear Energy Agency (NEA) of the Organization for Economic Co-operation and Development (OECD) [8] concludes that, given the current volatility in natural gas prices and overarching policy ambitions due to the energy transition, combined with the right initiatives, the prospects of nuclear power contributing to the H2 economy represent a significant opportunity.

It is evident that the global quest for sustainable energy solutions has sparked significant interest in pink H2 production, presenting a promising pathway to clean energy generation. Recent research advancements in nuclear-based H2 production have demonstrated significant potential in addressing the dual challenges of energy sustainability and climate change. On the industrial front, collaborations between nuclear and H2 production sectors are paving the way for pilot projects and commercial-scale implementations, where the potential for pink H2 production extends beyond mere energy generation and progressively becomes a pivotal element in the broader H2 economy. This paper has a two-fold objective: firstly, to provide a comprehensive and updated overview of the recent technological advancements as well as the cost of H2 production. Secondly, it endeavors to assess the readiness of major countries in terms of regulatory frameworks and infrastructure development to foster the growth of a pink H2 economy. Both aspects aim to highlight its economic viability and potential for widespread adoption. To address these two key elements, this work seeks to initially explore the potential of nuclear energy as a reliable and low-carbon source for H2 production by presenting the various underlying principles for nuclear-powered H2 production. Through a comprehensive review of recent advancements in scholarly research as well as the economic viability of pink H2 production, this study aims to shed light on the current landscape, identifying key trends and technological breakthroughs. Toward enriching the current literature of real applications, this work also delves into the discussion for adopting pink H2 production on a global scale, by identifying current national “Hydrogen Roadmaps” and policy frameworks as well as the current and future H2 infrastructure plans at the international level. By synthesizing diverse perspectives and approaches, this research aims to elucidate the current landscape of pink H2 production as well as to provide valuable insights for policymakers, researchers, and industry stakeholders engaged in the development and implementation of nuclear-driven H2 production avenues.

The rest of this work is structured as follows: Section 2 provides an overview of the various H2 generation routes, focusing on pink H2 production and the associated nuclear reactor technologies. Recent advancements in research literature concerning nuclear-based H2 production, along with a comparative assessment of pink H2 production costs, are presented in Section 3. The burgeoning regulatory field of H2 adaptation in the electricity value chain along with opportunities for nuclear-based H2 production is showcased in Section 4. Our concluding remarks are demonstrated in the final section of this study.

2. Pink Hydrogen Production

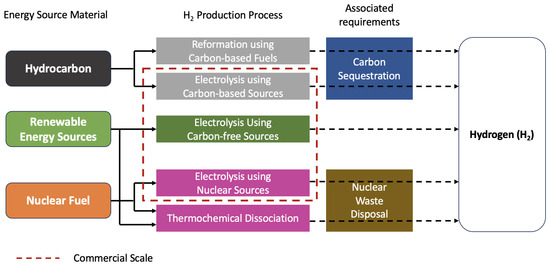

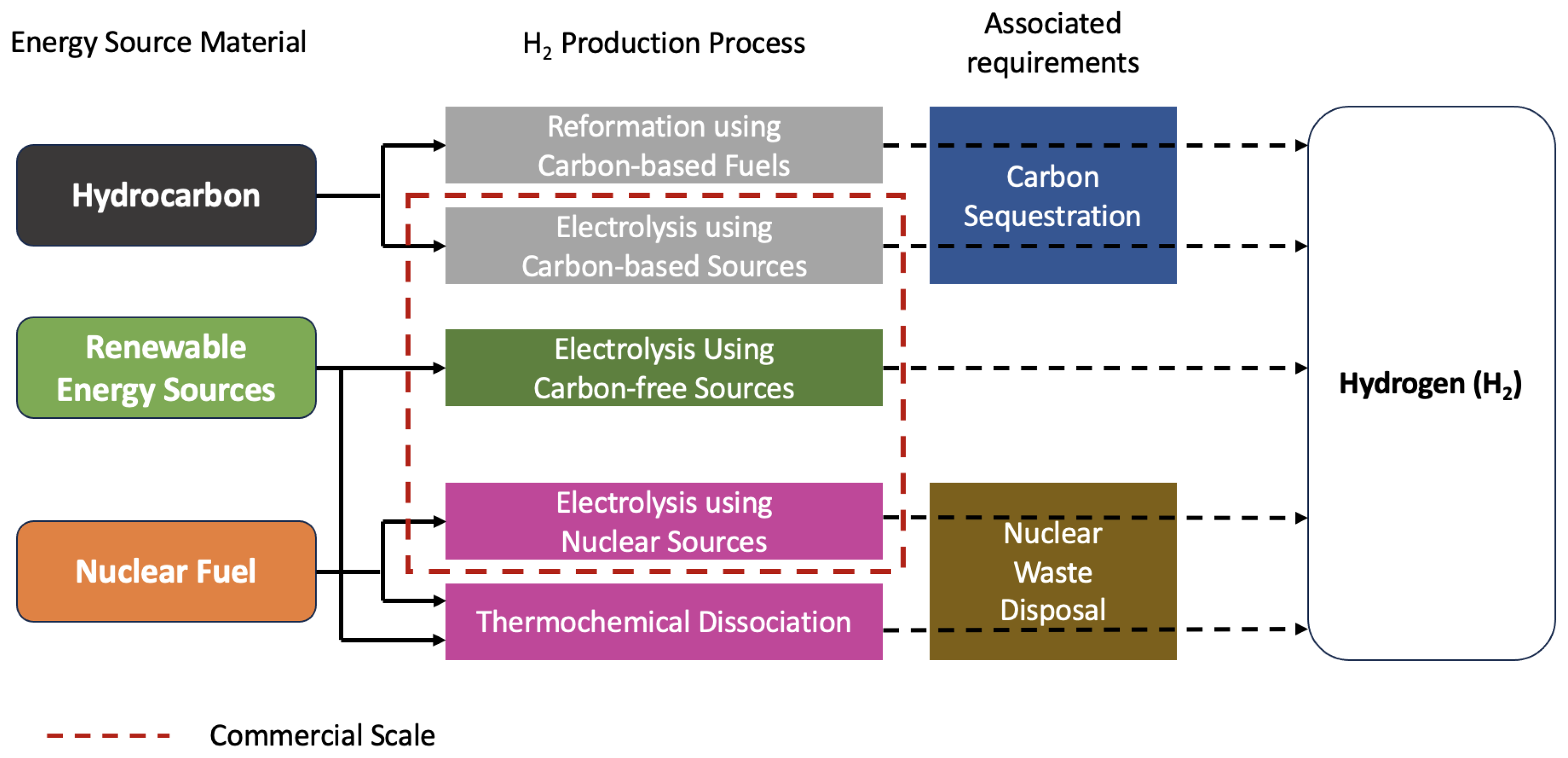

H2 is not available in nature in a similar manner as fossil fuels. However, it may be produced from any primary energy source and utilized as fuel in a fuel cell or for direct combustion in internal combustion engines, with the only byproduct being water. As shown in Figure 1, there are three primary energy sources in the pathway toward H2 production: (a) hydrocarbon fuels, (b) RES, and (c) nuclear fuel.

Figure 1.

H2 production pathway.

The color spectrum is utilized to portray the origin of the produced H2 as well as the volume of carbon dioxide (CO2) emitted during the process. Despite having identical molecular and physical characteristics, different forms of H2 have different carbon footprints. “Gray hydrogen” is deemed as the “traditional” technique and is presently the prevailing form of H2 production. Figure 1 illustrates the production of “gray hydrogen” from natural gas by a steam reforming process, which does not involve absorbing the CO2 emitted during the process. Steam reforming converts natural gas compounds to H2 and CO2, namely synthetic gas, by adding moisture at high pressure (35–40 bar) and temperature (800–900 °C). H2 that is manufactured by natural gas reforming coupled with carbon capture and storage (CCS) is labeled as “blue hydrogen” (Figure 1). H2 production can also be accomplished through thermochemical dissociation (or thermochemical splitting) of water and water electrolysis processes that utilize RES or nuclear fuel as primary energy sources. The thermochemical cycles include sulfur–iodine (S–I), hybrid sulfur (HyS), copper–chlorine (Cu–Cl), and calcium bromide (Ca–Br) as catalysts for the thermochemical splitting of water. These cycles have a significant role in the long-term outlook of large-scale low-carbon H2 production. Nevertheless, these cycles require high temperatures (>500 °C) for operation, which is one of the reasons why thermochemical cycles are still facing obstacles in reaching commercial scale. The simplest and most popular method for producing H2 straight from water is electrolysis, which uses electricity to split water molecules into H2 and oxygen, emitting zero greenhouse gas emissions in the process. Electrolysis generates “green hydrogen” when electricity is supplied by RES as illustrated in Figure 1. Similarly, pink H2 can also be produced via electrolysis when electricity is supplied by nuclear power plants. However, this approach is crippled by low efficiency and poor economics. The solution, toward higher efficiency and economic visibility, comes from leveraging the wasted energy coming from the generated heat. Nuclear energy provides a highly effective source of process heat for a range of industrial applications, such as desalination, synthetic and unconventional oil production, oil refining, biomass-based ethanol production, and H2 generation. Pink H2 production offers significant advantages, including reducing production costs and emissions, making it a sustainable and more cost-effective alternative to conventional methods. It is possible to produce H2 from any kind of nuclear reactor as long as it can supply energy and process heat. But the key factors in figuring out which kind of reactor is better suited for a certain production process are the reactor coolant and its maximum temperature.

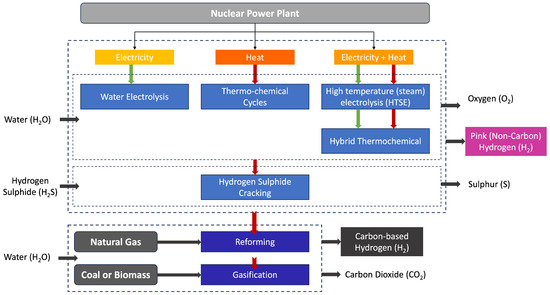

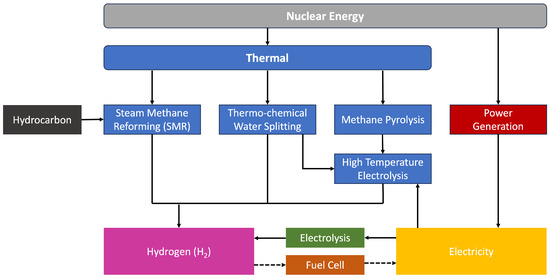

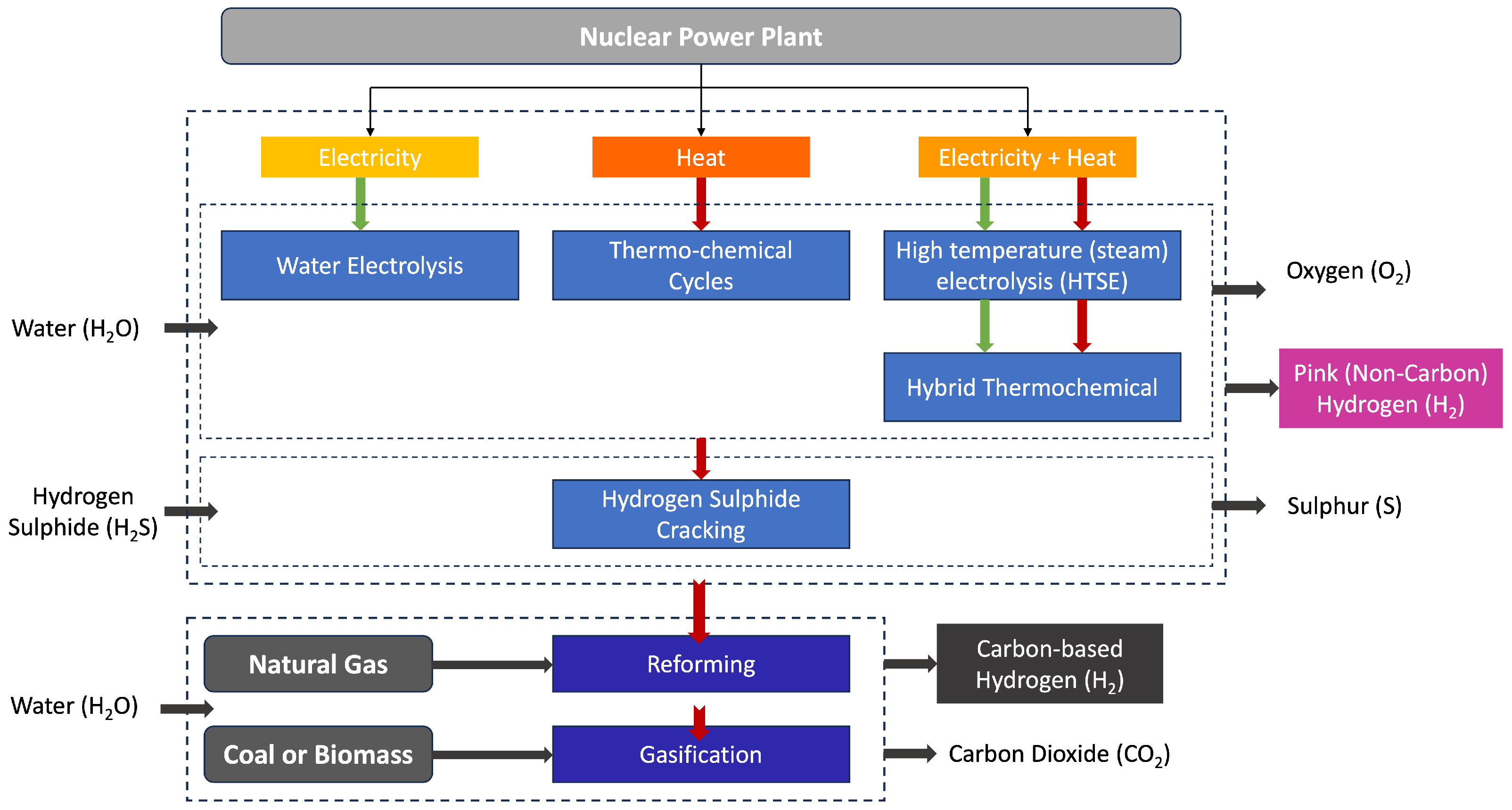

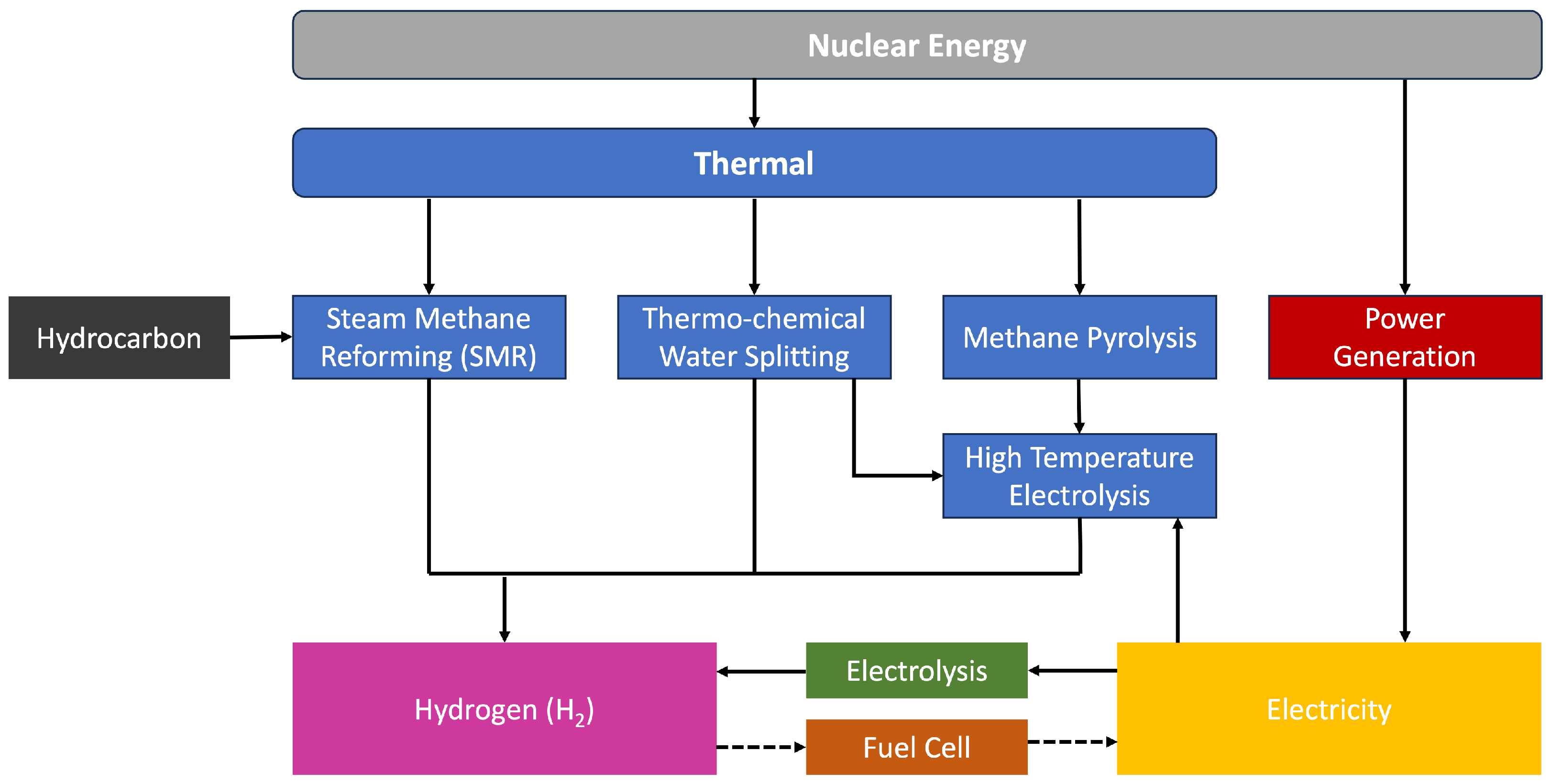

The power scale is another key consideration. While small plants are better suited as single-purpose plants (e.g., for H2 production exclusively), large reactors are better suited for the cogeneration of electricity and H2. Specific reactor types require more particular considerations. For instance, the cost of producing H2 would make it less desirable for a small plant to be utilized exclusively for H2 production. Nevertheless, there are ways to make this process more profitable, like sharing or reducing expenses through cogeneration or the use of a power grid during off-peak periods. Figure 2 illustrates the different routes of pink H2 production combined with carbon-based H2, while Figure 3 captures the thermal processes in a more specific capacity.

Figure 2.

Routes of pink H2 production.

Figure 3.

Thermal-based processes for pink H2 production.

For almost 50 years, the nuclear power industry has been refining and developing reactor technology, and it is currently in the process of constructing the next generation of nuclear power reactors. An overview of the technical characteristics of the various generation nuclear reactors, as presented in [9], is tabulated in Table 1.

Table 1.

Overview of major reactor designs per generation [9].

Reactor generations are typically distinguished from one another. These reactors were originally designed in the 1950s and 1960s, while the final Generation I reactor in the United Kingdom (UK) was shut down in 2015. Nowadays, Generation II reactors comprise the vast majority of the existing global nuclear fleet. They are direct descendants of the prototypes from the 1950s and 1960s and primarily belong to two groups of light water reactors (LWRs): (a) pressurized water reactors (PWRs) and (b) boiling water reactors (BWRs). The advanced reactors are referred to as Generation III (and III+, labeled as “evolutionary designs”); however, the division from Generation II is somewhat arbitrary and primarily focuses on advancements in fuel technology, increased thermal efficiency, upgraded safety systems (including passive nuclear safety), and standardized designs aimed at minimizing maintenance and capital investments. The Generation IV International Forum (GIF) is a global body that oversees the advancement of Generation IV reactors. These reactors are considered to be “revolutionary designs”. While there is no exact definition of a Generation IV reactor, the term refers to nuclear reactor technologies that were being developed around the year 2000. These designs were set up to transform the future of nuclear energy. The six designs include the gas-cooled fast reactor (GFR), the lead-cooled fast reactor (LFR), the molten salt reactor (MSR), the sodium-cooled fast reactor (SFR), the supercritical water-cooled reactor (SCWR), and the very high-temperature reactor (VHTR). China began commercial operations on the high-temperature gas-cooled pebble-bed reactor (HTR–PM) in December 2023, which would make it the world’s first Generation IV nuclear reactor to enter commercial operation [10]. These cutting-edge reactor designs provide advantageous operating properties, which are essential for efficiently producing pink H2. In order to produce pink H2 on a large scale, these reactor designs can handle thermochemical water splitting in addition to low- and high-temperature electrolysis. Several initiatives, feasibility studies, and demonstration projects demonstrate how these cutting-edge reactors might generate clean pink H2 in a variety of ways, while also addressing legacy issues related to large reactor projects from Generation II and Generation III/III+. These challenges include backend spent fuel and decommissioning issues, delays in development, excess budgeted costs, and the inability to cover both initial investments and ongoing expenses.

The nuclear sector has a lengthy track record of secure operation and these operational plants are highly dependable. Nowadays, about 85% of electricity produced worldwide by nuclear power comes from Generation II nuclear reactors and performs with high efficiency, reliability, and commonly with capacity factors exceeding 90% [7]. Small and medium power reactors based on high-temperature gas reactors (HTGRs) are also deemed attractive choices. The HTGR is one of the nuclear power reactors that may be utilized to provide high-temperature steam for H2 production by utilizing the thermal neutron spectrum. HTGR is graphite-moderated, helium-cooled, and has an outlet coolant temperature of about 800 °C.

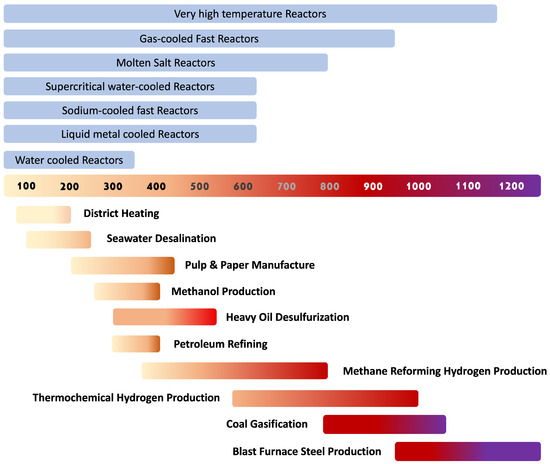

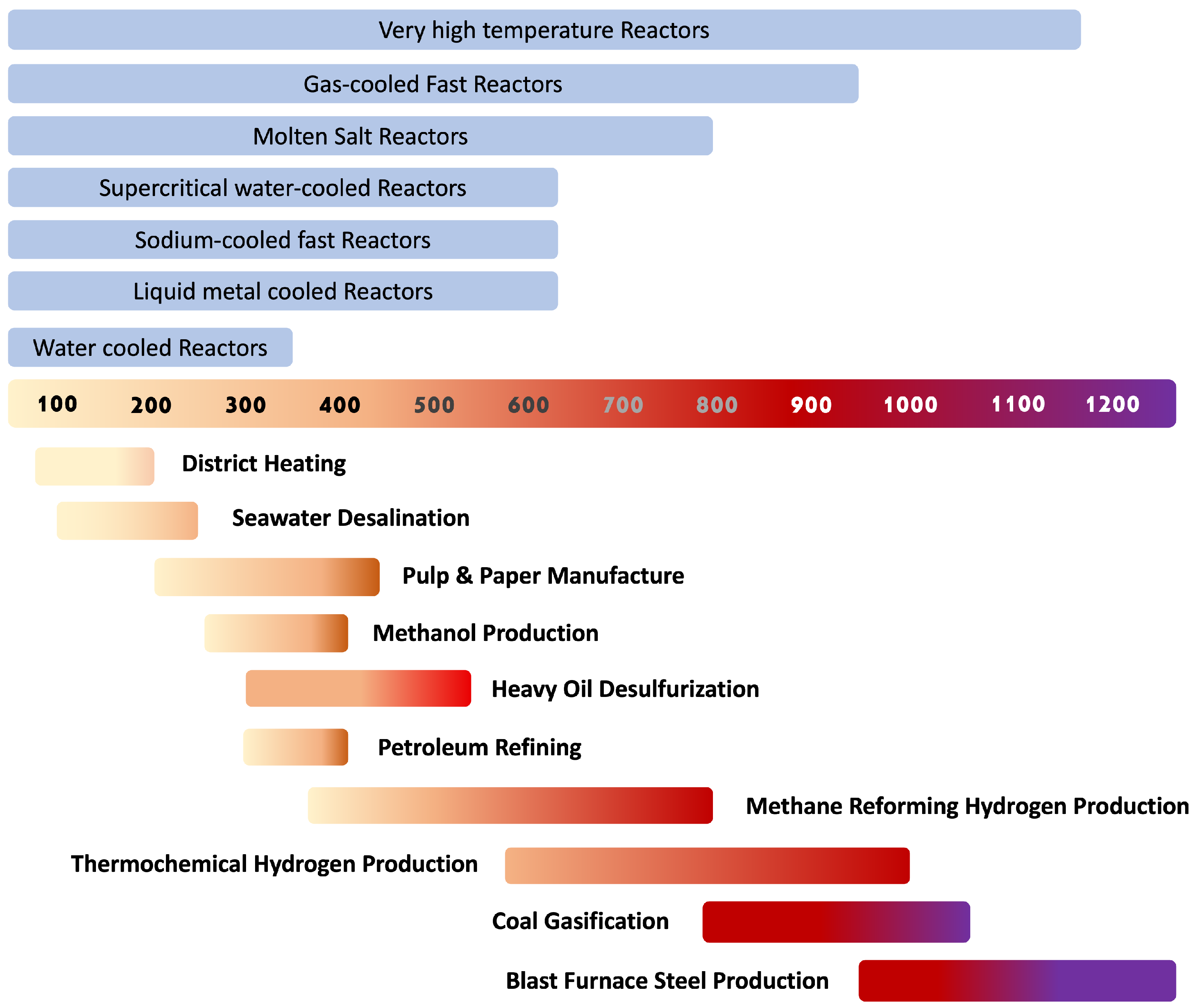

Figure 4 provides an illustration of numerous advanced reactor technologies and their possible applications in various industries, based on their respective operational temperatures.

Figure 4.

Advanced nuclear reactor types and industrial applications.

There is a continuous international effort to create enhanced designs for nuclear power reactors. Future advanced nuclear power plants (NPPs), for instance, Generation IV VHTR or SCWR reactors, could supply both energy and high-temperature process heat, resulting in high net power cycle performance. For example, a VHTR system can deploy high-temperature process heat applications, like coal gasification and thermochemical H2 production, relatively faster compared to previous generations, while maintaining superior efficiency. The helium-cooled core of VHTR is based on the pebble fuel of the pebble bed modular reactor (PBMR) or the prismatic block fuel of the gas turbine modular helium reactor (GT-MHR). Due to the intrinsic safety features of the fuel and reactor, the VHTR system is highly regarded in both safety and dependability as well as economics due to its great efficiency in producing H2. Because of its open fuel cycle, it has an open fuel rating of neutral for sustainability and good for proliferation resistance and physical defense. Although it has the potential to create electricity as well, its main uses are in H2 synthesis and other process-heat applications [11]. Using supercritical water as the working fluid, the SCWR is essentially an LWR with a direct, once-through cycle that operates at greater pressure and temperatures. It could function on a direct cycle, as is generally imagined, much like a BWR, but unlike PWRs, it would only have one phase present because it employs supercritical water as the working fluid. It could also function at pressures and temperatures far higher than those of the PWRs and BWRs in use today. Due to their significant plant simplicity and high thermal efficiency of approximately 45%, as opposed to the current LWRs’ efficiency of roughly 33%, SCWRs are deemed as prospective advanced nuclear systems.

3. Research Advancements in Pink Hydrogen Production

H2 production offers a promising pathway toward decarbonizing the global energy system and addressing the challenges of climate change and energy security. In this scope, several recent studies focused on the future of H2 by presenting challenges and opportunities in the field of production, storage, and applications [6,12,13,14,15] as well as comparative assessments of the technological, economic, and environmental aspects for clean H2 production [16,17,18,19].

The need to shift away from fossil-based H2 generation, due to sustainability targets, has led many researchers to shift to low-carbon H2 technologies that are coupled with RES, namely “green hydrogen”. However, the recent worldwide trends in electricity demand spikes as well as electricity price fluctuations, along with the intermittent and unpredictable nature of RES, are turning the research interest toward more dispatchable sources for producing H2. Nuclear power is currently a significant source of electricity, widely recognized for its established applications. Its ability to operate at high capacity factors is well-suited for producing zero-carbon H2 as an emerging energy carrier that may be employed in various applications. Several studies have been conducted to emphasize the utilization of nuclear energy, considering both the existing reactor fleet and advanced reactors, to generate sustainable H2.

The accelerated advancement of pink H2 production is emphasized in [20], where the authors present a comprehensive, quantitative, and qualitative understanding of the current situation in the field of pink H2 production. This analysis is undertaken via an examination of patterns of publications and collaboration among academic institutions and researchers. However, rather than concentrating on scientometrics, the examination of the keywords and the development of those keywords is the primary focus.

Work conducted in [21] offers valuable perspectives into the prospective application of nuclear energy for H2 production, while also highlighting the efforts of the International Atomic Energy Agency (IAEA) [22] in evaluating the technical and economic aspects of H2 production. Based on the comparative assessment performed by the authors, it is concluded that, despite the possibilities that arise from the advantages that nuclear energy can offer to assist the huge production of H2 utilizing various reactor technologies, there are still bottlenecks as well as challenges that need to be overcome in order to expedite the deployment of nuclear H2. By joining the H2 market, the nuclear industry can expand its role beyond providing clean power and contribute to the sustainable decarbonization of several industries, particularly those that are difficult to decarbonize.

The work conducted in [23] offers a comparative economic analysis of the production of H2 utilizing various nuclear reactors integrated with electrolysis techniques. H2 production based on various technologies is compared using the Hydrogen Economic Evaluation Program (HEEP) software developed by IAEA. The findings demonstrate that the total costs of producing and storing H2 using compressed gas from an advanced pressurized water reactor (APWR) facility are 8.2 US$/kgH2 for an NPP of 360 MWe capacity. However, this cost decreases to 6.06 US$/kgH2 when the NPP capacity is expanded to 1117 MWe. Furthermore, it has been determined that the combination of HTGR technology and HTSE can generate H2 at a cost of 3.51 US$/kgH2, which is slightly cheaper than utilizing grid electricity, which costs 3.55 US$/kgH2.

A similar approach was followed in [24], where the authors presented a cost comparison assessment of selected nuclear-driven hybrid thermochemical cycles by also using IAEA’s HEEP. The results show that the upfront expenses of pure electrochemical technologies make up a little more than 20% of the cost of H2 generation. In thermochemical technologies, on the other hand, the share goes up because multiple units and other parts of the plant are used. The authors emphasize that achieving long-term, ambitious H2 cost targets can be facilitated by hybrid thermochemical technologies, which are an affordable substitute for pure electrochemical technologies. When it is possible to bring such technologies to the market, the costs of H2 production from the HyS and Cu–Cl cycles will be 2.80 US$/kgH2 and 2.86 US$/kgH2, respectively, rendering them more cost-effective than conventional electrolysis.

An economic evaluation of H2 production costs using a combination of HTGR with a steam methane reforming (SMR) plant, which was carried out by using the IAEA HEEP software, is presented in [25]. Two different scenarios are explored, coupling the SMR process for H2 production with 2 HTGRs of 170 MWth each, and 1 HTGR of 600 MWth. The yielded results showcase a competitive value obtained when nuclear heat from HTGR is used. More specifically, H2 production costs equal 2.72 US$/kgH2 for case 1 and 1.72 US$/kgH2 for case 2, as compared to an average value of 2.3 US$/kgH2, which is obtained for the SMR method using natural gas as a primary source.

Another study that utilizes the capabilities of IAEA offerings is showcased in [26]. The authors present an estimation of pink H2 production costs based on LWRs using IAEA’s hydrogen calculator (HydCalc) program [27] based on six existing LWRs. The projection of H2 usage was conducted without considering the carbon tax, as nuclear power does not induce any CO2 emissions. The yielded costs range between 2.6 and 4.85 US$/kgH2 based on the investigated reactor type, while the cost of H2 production for Xcel Energy’s Prairie Island NPP is estimated at 0.69 US$/kgH2 due to the utilization of high-temperature steam electrolysis as a method of H2 production instead of low-temperature electrolysis. The findings underline that the total cost of producing H2 using different reactor technologies is influenced by both the method of production and the expenses associated with the NPP, as well as the rate at which the H2 is generated.

The authors of [28] compare the sustainability of several approaches to producing H2, focusing mostly on nuclear energy methods. The authors suggest the use of the thermo-ecological cost (TEC) index instead of local energy efficiency, where the absolute thermo-ecological cost is expressed in MJ* of non-renewable exergy per 1 MJ of electricity. Additional factors considered in the evaluation include the availability of energy supply, as measured by the capacity factor, the total GHG emissions, and the ratio of resources to production. Furthermore, water electrolysis and the Cu–Cl cycle have been regarded as cogeneration processes, yielding oxygen as a valuable derivative product. The obtained results show that high-temperature electrolysis, which depends on the thermal efficiency of the NPP and the level of fuel enrichment, has the lowest TEC of all the evaluated technologies, ranging from about 25 to 45 MJ*/MJ. TEC in the range of 50–100 MJ*/MJ characterizes H2 generated in the Cu–Cl process driven by nuclear energy, leading to the lowest values. The yield of H2 from traditional water electrolysis is also measured by TEC and ranges from 40 to 85 MJ*/MJ, depending on the H2 generator’s efficiency.

A probabilistic mathematical model for techno-commercial calculations under uncertainty is developed in [29], and it is specifically applied to nuclear H2 generation projects using water electrolyzers coupled to already-existing reactors. A common statistic used to compare potential technology alternatives for near-term implementation is life cycle or levelized manufacturing cost. To do this, a comprehensive discounted cash flow model drawn up for the duration of the project has been utilized. The major findings from this work highlight that there is a difference of almost 0.2 to 1 US$/kgH2 in H2 production costs between these alternative methods, based on current techno-commercial maturity levels. Nuclear H2 is competitive with “green hydrogen”. The cost of nuclear electricity has the highest influence on the cost of H2. NPP capital cost contributes up to 22.1% to the levelized production cost of H2, while variable operating costs account for up to 61.8% of the levelized cost, depending on the NPP capacity. There appears to be a possibility of less than 0.1% of achieving the frequently cited long-term cost goal of 1 to 2 US$/kgH2 with the present scale. The authors conclude that it is theoretically feasible to use electrolyzers to facilitate load-following operations of nuclear reactors and demand response without power restrictions, as long as there is surplus nuclear electricity available from a power plant.

The authors of [30] discuss the production of H2 via the combination of nuclear fusion and biomass conversion. A techno-economic analysis is conducted on the fusion–biomass hybrid system to determine the cost of H2 production and its economic viability compared to other technologies. The techno-economic analysis includes cellulose, hemicellulose, and lignin as biomass components, along with municipal solid waste as an additional feedstock. Stoichiometric calculations are used to determine the conversion of biomass to H2. The gasification facility for H2 production is considered to utilize a bubbling fluidized bed gasifier, which will be supplied with 20.6 MJ/kg of biomass. The findings indicate that the overall syngas capacity amounts to 203 PJ, and 137 PJ of H2 is generated by the use of a ceramic membrane for H2 separation. The levelized cost of hydrogen (LCOH) is determined to be 2.45 US$/kgH2, and the estimated 90% confidence interval for the cost of H2 production is between 1.87 and 3.24 US$/kgH2. The resulting LCOH places the authors’ proposal in an advantageous position compared to traditional approaches. The work concludes that the cost of H2 production can be further reduced with the implementation of carbon pricing by the year 2050 when fusion commercialization is expected.

The work presented in [31] introduces a method for calculating the LCOH generation using discounted cash flow analysis. This method is specifically designed for the economic evaluation of H2 production from NPP-supported energy sources. The proposed methodology fully models the fuel cycle for the NPP as well as the various cost components of the H2 generation plant and NPP. A realistic scenario where the construction costs are sourced via a combination of financing and equity is addressed. Tax payments are also factored into the formula, where every pertinent cost element is represented in the model to match the real-life case. The model simulation and application involve the utilization of both heat as well as electricity as energy inputs for the generation of H2. The findings indicate that reducing the capital cost of the associated NPP is an effective strategy to lower the resulting LCOH.

The authors of [32] discuss the potential development of HTGR for generating electricity using advanced ultra-supercritical (AUSC) Rankine cycles. The study also explores the possibility of producing H2 through electrolysis at temperatures below 750 °C, as well as producing H2 through direct thermochemical cycles on top of AUSC electricity production at temperatures ranging from 950 to 1000 °C. The authors conclude that nuclear thermal energy can be effectively utilized at temperatures below 730 °C by generating electricity through AUSC Rankine cycles. Additionally, a part of this electricity can be used for H2 production through electrolysis, if deemed necessary. On the other hand, if nuclear thermal energy becomes accessible at temperatures around 1000 °C, then there is the possibility of incorporating a thermochemical plant alongside a thermal power plant AUSC Rankine cycle, or even solely utilizing the thermochemical plant.

The utilization of heat from a nuclear cogeneration plant and the application of thermochemical water-splitting technology for H2 synthesis are explored in [33]. The Cu–Cl and S–I cycles are chosen for their ability to operate without relying entirely on external electricity. The authors suggest that the studied HTGR, operating at a maximum outlet temperature of around 750 °C, should be paired with a thermochemical water-splitting Cu–Cl cycle. This is because the Cu–Cl cycle has a high level of heat utilization and the system is less complex, as it does not require additional medium heating. On the other hand, future designs of the HTGR, including the VHTR, have the potential to achieve greater outlet temperatures, reaching up to 1000 °C. As a result, the thermochemical water-splitting S–I cycle is considered a more advantageous method.

The environmental consequences of nuclear-based H2 generation are examined in [34] using a life cycle assessment (LCA) approach based on six indicators. The findings indicate that utilizing nuclear energy for H2 production is a highly favorable choice for mitigating the environmental impact of fossil fuels. From an environmental perspective, high-temperature electrolysis is cleaner than the S–I cycle, with the caveat that it does not involve the use of nitrogen as a carrier gas. Large-scale H2 production can only be achieved by constructing pink H2 production facilities, and the commercialization of H2 production facilities depends on the understanding of H2 leakage and diffusion behavior. The risk of H2 combustion has always been a topic of concern for both the nuclear power industry and researchers.

The authors of [35] concentrate on the quantitative evaluation of the risks of H2 deflagration transitioning to detonation in relation to serious incidents in the large PWR. Both the lumped parameter program and computational fluid dynamics software approaches are examined, taking into account the uncertainty impact of parameters from both temporal and spatial dimensions. The work reveals that there is a notable degree of uncertainty in the estimation of H2 risk when employing the widely used lumped parameter program method. As per the findings, the uncertainty that has been identified can be rectified by merging the outcomes of the gas distribution analysis. This will yield a probability value that is more precise and dependable, thereby serving as a more accurate point of reference for safety analysis and consequently, this will enhance the overall safety of an NPP.

The authors of [36] analyze the effects of several parameters, including wind speed, leakage direction, leakage diameter, leakage height, and leakage angle, on the diffusion of gas leakage from storage tanks. The goal is to understand how the circumstances of the storage tank itself and the external environment contribute to the propagation of leaks. The longest H2 diffusion distance is calculated by combining the above various parameters with severe working conditions. Lastly, the impact of the H2 explosion’s peak overpressure was assessed, and the bare minimum of separation needed to prevent safety hazards was estimated. The findings show that a longer diffusion distance occurs from higher wind speeds, larger leakage diameters, and lower leakage heights when the wind direction is consistent with the leaking direction and the leakage angle is 0 °C. In extremely harsh operating conditions, the flammable H2 cloud’s diffusion distance can extend up to 237 m. The minimum separation distance needed when H2 diffusion erupts is roughly 338 m.

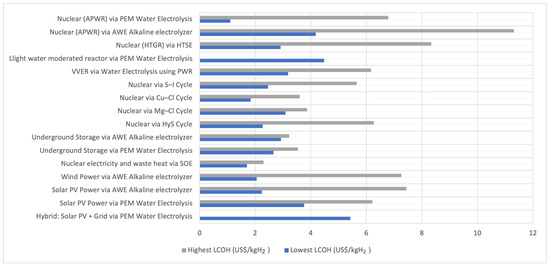

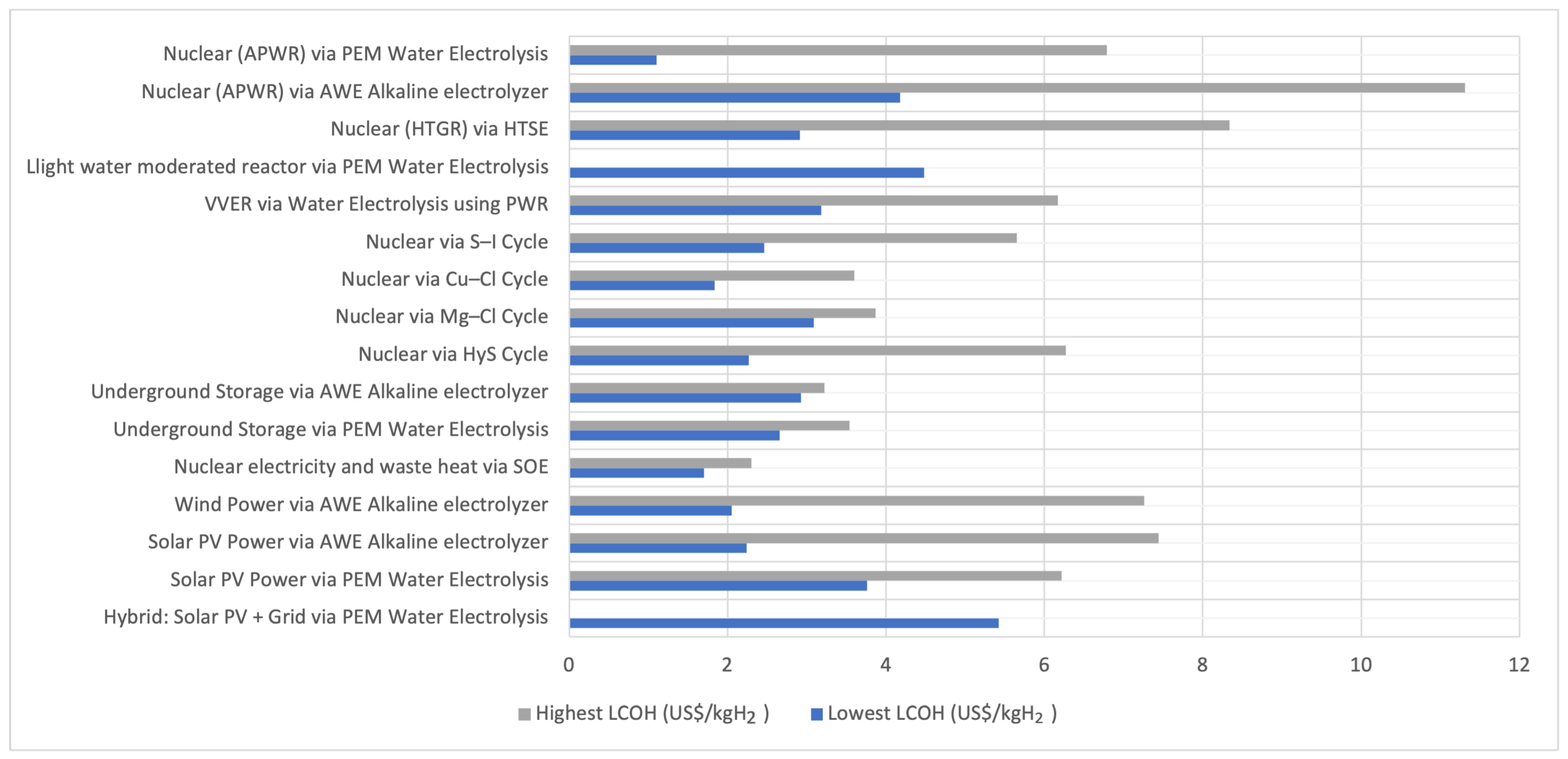

The conducted analysis in the research literature revealed that a critical factor in determining whether nuclear reactors can be successfully deployed for H2 generation is the production cost. In order to realize investment potential and attract financing, an economic evaluation of the various H2 generation and storage systems is necessary. There are costs associated with each color of H2 that must be considered. The process followed, the fuel used (coal, electricity, water, or methane), and other elements like levies (such as carbon taxes) can all affect how much it costs to produce H2. This analysis is based on the LCOH, which accounts for all capital expenditure (CAPEX) and operating expenditure (OPEX) values associated with H2 production. This allows for an equitable comparison among various production methods. This methodology calculates the cost, often in US$ per kilogram of H2 produced, denoted as US$/kgH2. This strategy is analogous to the one used for power generation or energy storage. It is crucial to highlight that the LCOH does not incorporate the expenses associated with H2 storage and transportation, which may be necessary depending on the specific use case. Utilizing the LCOH also allows for comparing the various H2 colors on a comparable basis. To enrich the existing literature, this work provides insights into the latest advancements concerning the LCOH of low-carbon H2, by carrying out a cost-comparative assessment of the most recent research studies. The results are summarized in Table 2. The cost of producing pink H2 ranges between 1.1 and 11.31 US$/kgH2 and mainly depends on the method used. More specifically, it is ascertained that novel approaches that exploit nuclear energy as their primary source, lead to significantly lower LCOH. Indubitably, the accuracy of the results is impacted by the assumptions made by the authors of each work.

Table 2.

LCOH comparative assessment.

The different H2 production costs, identified through the conducted comparative assessment, are clustered based on their energy source as well as the applied technology and graphically illustrated in Figure 5.

Figure 5.

Graphical comparative assessment of LCOH.

4. National Pink Hydrogen Strategies

The urgent need to mitigate climate change and transition toward sustainable energy sources has spurred interest in H2 as a versatile, low-carbon fuel in the global energy landscape. The European Union (EU) has been at the forefront of what has been called the H2 revolution. For the EU, there are two main pressing points: phasing out Europe’s dependency on Russian fossil fuels and addressing the climate crisis while meeting the goals of its own European Green Deal. Initiatives such as the EU strategy on H2 (COM/2020/301) [55], which was adopted in 2020, introduce policy action points in the form of investment support, research, and international cooperation for creating an H2 market and infrastructure, while the REPowerEU plan [56], which was published in 2022, outlines an H2 accelerator to scale up renewable H2 by deploying 17.5 GW by 2025 of electrolyzers to fuel EU industry with homegrown production of 10 Mt of renewable H2 while targeting 10Mt of domestic and imported “green hydrogen” by 2030. In this domain, the REPowerEU plan adjusts state aid rules to support energy infrastructure investments. Moreover, the renewable energy directive (RED III) [57], adopted by the Council on 9 October 2023 after two years of intense negotiations, establishes the EU commitment to ensuring that at least 42% of H2 in the industry is derived from renewable fuels of non-biological origin by 2030. Examining existing H2 policies and initiatives worldwide, this section identifies national H2 roadmaps, mandates, research projects as well as international collaboration frameworks toward the facilitation of the H2 economy. Quantifiable targets for H2 production, distribution, and utilization, aligning with global climate objectives outlined in agreements such as the Paris Agreement [1] are also presented. This section also delineates short-term, medium-term, and long-term national goals by providing an overview of the current and future nuclear projects on a global scale. The analysis is divided into continental levels as follows:

4.1. Europe

On 29 October 2021, Belgium unveiled its federal H2 vision and strategy to position itself as the import hub for H2 produced by RES into Western Europe. The four main pillars of the nation’s vision are to: (i) develop into an import and transit hub for renewable H2 in the continent of Europe; (ii) become a leader in technological advancements; (iii) facilitate a strong local market; and (iv) engage in international cooperation. According to the government’s calculations, importing H2 is more efficient than domestic production. In addition, by 2026, the plan vision for a 150 MW local electrolysis production capacity. The Chilean Ministry of Energy and the ports of Antwerp and Zeebrugge (Belgium) have officially agreed on 4 November 2021 (COP26 in Glasgow), to promote the trading of “green hydrogen” between Western Europe and Chile. The country’s current energy strategy lies in wind and solar power for H2 production. Despite Belgium being a prime prospect for nuclear H2 generation due to its two operational NPPs, the country’s present strategy is to phase them out entirely by 2025. To this end, it is improbable that the nation will produce pink H2 until that policy changes [58,59].

Bulgaria appears to be a major contestant for future pink H2 production as its two nuclear reactors can meet approximately one-third of the country’s electricity demand, while there are plans for the installation of two new reactors [60]. However, no relevant framework or legislation for pink H2 seems to be in place.

In 2020, France restated its H2 plan, defining decarbonized H2 as the energy that employs RES or “carbon-free” electricity. The installation of an electrolyzer with a total capacity of 6.5 GW by 2030—currently deployed at 1 MW and projected at 900 MW—is the plan’s most pertinent goal. Currently, nuclear production makes up more than 70% of the nation’s generation mix. Although the French government’s multinational electric utility corporation—Électricité de France (EDF)—intends to produce H2 at its current fleet, no concrete plans have been disclosed as of yet. The EDF Group and Rosatom, a globally leading nuclear technology company, reached an agreement on 27 April 2021, to collaboratively advance clean H2 projects in both Europe and Russia [61,62].

Developing an H2 society where “green hydrogen” is essential to advancing and completing Germany’s energy transition roadmap is one of the country’s main goals. The goal is to reach an installed capacity of 10 GW of electrolyzers by 2030 along with a pipeline infrastructure that surpasses 1800 km, with a target to substitute a high percentage of natural gas production, while meeting the rising electricity demand in industry and transportation sectors [63]. Despite these efforts, the country’s plan to promptly phase out any NPPs indicates that there are no plans for nuclear-based H2 production.

Through its “National Energy Strategy”, the Netherlands unveiled a roadmap in March 2020 that aims to connect different clusters and scale up established electrolysis capacity to 500 MW by 2025, in tandem with the growth of the demand for H2 and regional infrastructure. The strategy outlines goals for connecting to storage facilities, further developing infrastructure, and expanding up to 3–4 GW of existing electrolysis capacity between 2026 and 2030, provided that a significant increase in renewable electricity is achieved. The country’s current focus is on “green” and “blue hydrogen” [64,65]. Although the Netherlands only has one reactor in operation at the moment, further exploitation of nuclear power, including Advanced Reactors, is being considered. However, the ultimate decision is expected to be influenced by the outcome of the EU taxonomy in terms of nuclear inclusion [66]. No official plans for pink H2 production are currently in place, despite the fact that a nuclear-based electricity supply is in place.

The “Hydrogen Roadmap: A Commitment to Renewable Hydrogen” was endorsed by the Spanish government in October 2020 and will be implemented in three stages: The first phase, which runs from 2020 to 2024, involves installing 300–600 MW of electrolyzer plants. The second phase, which runs from 2025 to 2030, focuses on installing at least 4 GW of electrolyzer plants, establishing renewable-based H2 that constitutes at least 25% of production across the industrial sector as well as commercial H2 projects that will be used for storage by 2030. The Spanish government wants to support an economy centered on the production and use of renewable H2 for the third phase (2030–2050). Although Spain presently has seven fully operational nuclear reactors, the roadmap focuses on H2 produced exclusively from renewables, and for the time being, there are no plans for nuclear-based H2 production [67].

In December 2020, the UK released the “Ten Point Plan for a Green Industrial Revolution” (TTPGIR), which outlined plans to produce 5 GW of low-carbon H2 by 2030. The plan also provisions new funds and policies to put the UK on track to achieve this goal, such as a GB£M240 fund for government co-investment in generation capacity via the Net Zero Hydrogen Fund (NZHF) [68]. In order to achieve the objectives outlined in the TTPGIR—which sets H2-related targets with regard to the areas of production, networks, storage, end-use industries, power, heat, transport, and the market framework—in August 2021, the country released its hydrogen strategy, which employs a twin-track strategy to promote the generation of “blue hydrogen” enabled by carbon capture as well as electrolytic “green” energy, which includes nuclear and renewable sources. The Hydrogen Strategy also specifically mentions nuclear energy as a possible source for thermochemical water splitting, high-temperature electrolysis, and low-temperature electrolysis for the clean generation of H2 [69]. The third point of the TTPGIR depicts the UK’s commitment to expanding current nuclear infrastructure with a variety of from large-scale to small and advanced modular reactors as well as a funding commitment of GB£M525 for the future generation of small and advanced reactors [70]. A feasibility study, commenced by EFD, concludes that nuclear-powered H2 was feasible on technical and safety grounds, while it proposes the “Hydrogen to Heysham” (H2H) project which is a potential expansion of the Heysham 2 NPP that is located in northwest England [71].

4.2. North and South America

With the passage of Law 26.123 in 2006, Argentinean legislation advocating the research, production, and usage of H2 as fuel is already in place. Moreover, the country is planning to construct a new NPP based on the Hualong PWR design that will complement the under-development CAREM project (advanced reactor), as well as the three NPPs that are currently operational. Although there is no direct reference to H2 generation to date, the existing and future nuclear infrastructure provides a solid foundation for pink H2 production [72].

The “Pathway for H2 Economy in Brazil”, issued in 2005 by the national Ministry of Mines and Energy, establishes an H2 roadmap with a regulatory focus to deal with various H2 production paths, storage, and its potential in different sectors. Concerning the current infrastructure, a project exploring pink H2 production has commenced at Angra NPP, while the National Hydrogen Program’s 2023–2025 Triennial Work Plan outlines the nation’s strategy using three different time schedules: by 2025, low-carbon H2 pilot plants will be deployed nationwide; by 2030, Brazil will become a leading producer of low-carbon H2; and by 2035, low-carbon H2 hubs will be consolidated domestically [73]. Brazil aims to exploit H2 through a project at Eletronuclear’s Angra NPP (a mixed-ownership power utility engaged in the construction and operation of NPPs), which targets the H2 formed as a by-product of other processes [74].

Canada’s near-term strategy outlines objectives through 2025 through which the government intends to establish a framework for its H2 economy, which also considers newly-developed infrastructure for H2 supply and distribution. Canada’s near-term strategy sets goals until 2025 through which the country plans to lay the foundation for the national H2 economy. This includes developing new H2 supply and distribution supporting infrastructure. The short target is set at 3 MT/yr. The mid-term strategy concerns a transformative scenario, until 2050, for which Canada sets a target at 4 MT/yr, while the long-term strategy involves the deployment of H2 for higher power demand applications (utility-based) toward H2 storage and energy efficient applications that rely on the usage batteries energy storage systems, setting a target at 20 MT/yr [75]. With regards to nuclear infrastructure, Canada aims to exploit its existing reactors—four NPPs located in New Brunswick—as well as to commercially deploy advanced and small modular reactors. This presents a longer-term possibility for H2 production. Canada also investigates the usage of solid oxide electrolyzer cell (SOEC) electrolyzers to increase thermochemical water splitting as well as H2 production efficiency. Initiatives such as the studies on the economics of pink H2 production conducted at the Bruce Nuclear Generating Station and research on the thermochemical synthesis of H2 by Ontario Tech, a public research university, demonstrate significant domestic interest [76].

In November 2021, the United States (US) Congress passed the “Infrastructure Investment and Jobs Act” that describes “Clean Hydrogen” as the H2 generation associated with the formation of no more than 2 kg of carbon dioxide equivalent per kilogram of H2 at the generation facility, while allocating US$B 8 in four regional clean H2 hubs. The “Hydrogen Shot”, the first initiative under the Department of Energy (DOE’s) Energy Earthshots Initiative, was launched in June 2021 and aims to bring down the cost of clean H2 by 80% to 1 US$/kgH2 within the next ten years. The national target is to produce 10 Mt, 20 MT, and 50 MT of “Clean Hydrogen” by 2030, 2040, and 2050, respectively [77]. Bipartisan support for nuclear energy has resulted in the passage of numerous laws in Congress, such as the Energy Act of 2020 which established an advanced fuels Research and Development (R&D) program, which is crucial to advanced reactor demonstration, and among other things, authorized the Advanced Reactor Demonstration Program [78,79]. In order to conduct a three-year demonstration involving the installation of a Nel Hydrogen 1 MW PEM electrolyzer at one of its Nuclear fourteen BWRs, Exelon (public power utility company) received financing from the DOE’s H2@Scale [80].

4.3. Asia

China is currently regarded as the global leading producer of “gray hydrogen”; hence, H2 is included in the nation’s most recent five-year plan (2021–2025) [81]. Even though, China does not currently have a thorough and clean H2 roadmap, pink H2 production is anticipated to have a vital role in its national H2 strategy in the near future due to the significance of nuclear energy in the country’s energy mix and the rapid expansion of nuclear power. This is predicated on the fact that the Institute of Nuclear and New Energy Technology is pilot-testing initiatives, such as the production of H2 through thermochemical splitting and high-temperature electrolysis [82].

In February 2022, India released the first part of its H2 strategy, which includes incentives to support the government’s efforts to meet its climate commitments and transform the country into a “green hydrogen” hub. By 2030, 5 Mt of “green hydrogen” is expected to be produced, combined with 125 GW of additional renewable capacity while exports are foreseen to reach 10 Mt annually. India has 6.78 GW of nuclear power plants installed, with over 4 GW under development, while it has big aspirations to increase nuclear capacity to 22.48 GW by the end of 2031 [83]. The national H2 strategy plan is still unknown, despite the country’s significant interest in facilitating a local industry for the production of electrolyzers. Even though government reports bring the spotlight to H2 produced by renewables, no reference is made in terms of pink H2 production [84].

The Government of Japan unveiled its third strategic roadmap for H2 and fuel cells in March 2019, through which it views the adoption of H2 within its own country as a feasible method to enhance its energy independence, reduce carbon emissions, improve industrial competitiveness, and establish Japan as a major exporter of fuel cell technology. The “Green Growth Strategy” explicitly incorporates nuclear energy, encompassing the exhibition of small modular reactor technology via global cooperation by 2030, the development of fundamental technology for H2 production through HTGR by 2030, and the continuous advancement of nuclear fusion R&D through international collaborations like the International Thermonuclear Experimental Reactor (ITER) project [85]. The Japan Atomic Energy Agency (JAEA) is now working on showcasing the generation of pink H2 by HTGR thermochemical splitting. Moreover, Japan has recently entered into bilateral treaties with Russia regarding H2 energy [86,87].

The “Energy Strategy 2035” aims for Russia to achieve global leadership in H2 production and export. This shall be accomplished by setting export targets of 0.2 million tonnes by 2024 and 2 million tonnes by 2030 [88]. Russia’s 2024 H2 roadmap prioritizes several key areas, including pilot initiatives for H2 production using nuclear technology, the planning and construction of pilot facilities for carbon-free H2 production, and the creation of a prototype for H2-powered train transport. Its national H2 strategy places significant importance on the creation of pink H2, with Rosatom specifically choosing adiabatic steam methane reforming to investigate the notion of pink H2 production from the MHR-100 (a 200 MWt MHR with prismatic fuel assemblies) [89]. Lately, Russia has entered into bilateral cooperation agreements with the United Arab Emirates (UAE) and Japan on H2 energy. The level of collaboration with either country is unclear, while the framework agreement with the UAE provisions the establishment of a working group that shall focus on matters related to H2 energy development [90].

In January 2019, South Korea unveiled its H2 economy roadmap, laying out a target of providing 15 GW of fuel cell generation capacity by 2040. By 2030, the country’s objective is to have 2.1% of its total electricity production coming from H2 and ammonia. This target is expected to increase to 7.1% by 2036 [91]. A framework for a “Clean Hydrogen Certification Mechanism” was released in 2023 and aims to certify that GHG emissions in the process of producing or importing H2 are below a certain level and support incentives, according to the country’s trade and industry ministry [92]. Currently, the Korean government does not endorse the domestic growth of nuclear power. However, it does offer incentives for the exportation of Korean nuclear energy. Elcogen, a prominent European manufacturer of solid oxide fuel and electrolysis cells, has formed a partnership with Uljin County and the Next Energy Corporation, an impartial and nonpartisan research group. The purpose of this collaboration is to provide Elcogen’s solid oxide electrolyzer technology for a significant nuclear H2 complex in Uljin County, Korea. This deal enables the introduction of pink H2 production into South Korea for the very first time. From 2005 onward, the Korea Atomic Energy Research Institute (KAERI) conducted an assessment of pink H2 generation using three distinct cycles: (i) S–I, (ii) high-temperature electrolysis, and (iii) methane–methanol–iodomethane [93]. Nevertheless, there is a lack of additional information.

On 4 November 2021, at COP26, the UAE’s Ministry of Energy and Infrastructure (MOEI) declared that the “Hydrogen Leadership Roadmap” is considered a crucial element of the UAE’s “Net Zero by 2050 Strategic Initiative”. The vision outlines a plan to produce 1.4 Mt of H2 by 2030, 7.5 Mt by 2040, and 15 Mt by 2050. This will be achieved using a combination of electrolysis driven by renewable and nuclear electricity, as well as the use of natural gas with carbon capture, utilization, and storage (CCUS) technology [94]. The UAE aims to become a prominent player in the low-carbon H2 industry, with seven ongoing projects that specifically target 25% of the market share in major export destinations such as Japan, South Korea, Germany, India, Europe, and East Asia [95]. The Barakah NPP, located in the UAE, currently consists of two operational reactors, one that has finished construction, and one that is still under construction. Additionally, the Emirates Nuclear Energy Corporation (ENEC) and EDF have declared their intention to collaborate on nuclear energy R&D through a memorandum of understanding (MoU) that also encompasses the exploration of pink H2 production [96].

Based on the conducted literature review on the national attempts, the probability of deploying pink H2 production is tabulated in Table 3, taking into consideration both the strategy as well as the infrastructure of each country. The table summarizes the present “National Hydrogen Roadmaps and Strategies” from the aforementioned selected countries and/or regions with nuclear infrastructure as well as plans toward the establishment of a nuclear H2 economy. The first column indicates whether a national hydrogen roadmap is in place and if that roadmap supports nuclear H2 generation. The next two columns are aimed at evaluating the availability of current or future nuclear infrastructure and the probability of facilitating pink H2 production, respectively.

Table 3.

Overview of current national H2 roadmaps and strategies from countries with nuclear infrastructure.

As concluded, Brazil, Canada, Russia, UAE, and the UK all hold a high probability of adopting nuclear H2 economies in the near future, while France is the country with the highest potential of employing nuclear H2 generation first due to the combination of its current nuclear H2 roadmap and the fact that the current nuclear infrastructure meets more than half of the demand of the national energy sector.

5. Conclusions

As the world transitions toward a low-carbon economy, interest in the nuclear production of hydrogen (H2), also color-coded as “pink H2”, is rising globally due to the capacity of nuclear energy to generate power and heat for H2 production in a viable, environmentally friendly, and cost-effective way. This work presents a dual objective: firstly, to provide a thorough analysis of the latest advancements and updated costs related to pink H2 production, and secondly to assess the national readiness level for adopting pink H2 economies. More specifically, this paper offers a comprehensive overview of the developments in pink H2 production, shedding light on its role in advancing the transition toward a sustainable energy future while addressing key considerations in cost-effectiveness and industrial implementation. The cost of H2 production plays a pivotal role in the adoption and viability of pink H2 generation as a sustainable energy solution. Reducing the cost of H2 production through technological innovations, optimized reactor designs, and streamlined manufacturing processes is essential for widespread adoption. Two of the most critical parameters that influence pink H2 production costs are the size of the nuclear power reactor and the production economics, which are directly linked to capital expenditure (CAPEX) and operational expenditure (OPEX), as well as the economic impact of carbon tax. In this domain, the authors delve into the assessment of the levelized cost of hydrogen (LCOH) associated with low-carbon approaches, thus providing insights into the economic viability of pink H2 production.

The evolving regulatory framework on an international level is also explored, focusing on the policy landscape, current relevant infrastructure as well instrumental initiatives and collaborative efforts toward the pink H2 economy.

The synthesis of recent research findings and industrial applications, combined with cost-based assessments and regulatory considerations, provides valuable perspectives for policymakers, energy stakeholders, and researchers involved in advancing pink H2 production. By elucidating the technological progress and economic considerations, this work contributes to informed decision-making toward achieving sustainable and cost-effective H2 production pathways.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- UNFCCC. The Paris Agreement. In Proceedings of the Policies and Measures, COP 21, Paris Climate Change Conference, Paris, France, 30 November–12 December 2015. Available online: https://unfccc.int/documents/184656 (accessed on 17 March 2024).

- Poullikkas, A. Chapter 10: Toward Hydrogen Economy—The Energy Transition of Cyprus. In Sustainable Engineering Technologies and Architectures; AIP Publishing LLC: Melville, NY, USA, 2021. [Google Scholar] [CrossRef]

- Poullikkas, A. Perspectives for the development of energy strategies—Challenges towards a hydrogen economy in Cyprus. Green Energy Sustain. 2021, 1, 0004. [Google Scholar] [CrossRef]

- Nikolaidis, P.; Poullikkas, A. Chapter 19: Power–to–hydrogen concepts for 100% renewable and sustainable energy systems. In Hydrogen Economy, 2nd ed.; Scipioni, A., Manzardo, A., Ren, J., Eds.; Academic Press: New York, NY, USA, 2023; pp. 595–627. [Google Scholar] [CrossRef]

- Poullikkas, A. Long–Term Sustainable Energy Strategy: Cyprus’ Energy Transition to Hydrogen Economy; Easy Conferences Ltd.: Nicosia, Cyprus, 2020. [Google Scholar] [CrossRef]

- Nikolaidis, P.; Poullikkas, A. A comparative overview of hydrogen production processes. Renew. Sustain. Energy Rev. 2017, 67, 597–611. [Google Scholar] [CrossRef]

- IEA. Global Hydrogen Review 2023; International Energy Agency Publications: Paris, France, 2023; Available online: https://iea.blob.core.windows.net/assets/ecdfc3bb-d212-4a4c-9ff7-6ce5b1e19cef/GlobalHydrogenReview2023.pdf (accessed on 10 March 2024).

- OECD. The Role of Nuclear Power in the Hydrogen Economy: Cost and Competitiveness; Nuclear Technology Development and Economics, Organisation for Economic Co–Operation and Development Nuclear Energy Agency Publications: Vienna, Austria, 2022; Available online: https://www.oecd-nea.org/upload/docs/application/pdf/2022-09/7630_the_role_of_nuclear_power_in_the_hydrogen_economy.pdf (accessed on 13 March 2024).

- Poullikkas, A. An overview of future sustainable nuclear power reactors. Int. J. Energy Environ. (IJEE) 2013, 4, 743–776. [Google Scholar]

- WNN. China’s Demonstration HTR–PM Enters Commercial Operation; World Nuclear News Website, World Nuclear Association: London, UK, 2023; Available online: https://www.world-nuclear-news.org/Articles/Chinese-HTR-PM-Demo-begins-commercial-operation (accessed on 18 March 2024).

- NERAC; GIF. A Technology Roadmap for Generation IV Nuclear Energy Systems; U.S. DOE Nuclear Energy Research Advisory Committee and the Generation IV International Forum: Washington, DC, USA, 2002; Available online: https://www.gen-4.org/gif/jcms/c_40481/technology-roadmap (accessed on 11 March 2024).

- Rasul, M.; Hazrat, M.; Sattar, M.; Jahirul, M.; Shearer, M. The future of hydrogen: Challenges on production, storage and applications. Energy Convers. Manag. 2022, 272, 116326. [Google Scholar] [CrossRef]

- Pinsky, R.; Sabharwall, P.; Hartvigsen, J.; O’Brien, J. Comparative review of hydrogen production technologies for nuclear hybrid energy systems. Prog. Nucl. Energy 2020, 123, 103317. [Google Scholar] [CrossRef]

- Kovač, A.; Paranos, M.; Marciuš, D. Hydrogen in energy transition: A review. Int. J. Hydrogen Energy 2021, 46, 10016–10035. [Google Scholar] [CrossRef]

- Arcos, J.; Santos, D. The Hydrogen Color Spectrum: Techno-Economic Analysis of the Available Technologies for Hydrogen Production. Gases 2023, 3, 25–46. [Google Scholar] [CrossRef]

- El-Emam, R.S.; Özcan, H. Comprehensive review on the techno-economics of sustainable large-scale clean hydrogen production. J. Clean. Prod. 2019, 220, 593–609. [Google Scholar] [CrossRef]

- Chakrabarty, P.; Alam, K.; Paul, S.K.; Saha, S.C. Chapter 3—Hydrogen production by electrolysis: A sustainable pathway. In Hydrogen Energy Conversion and Management; Khan, M.M.K., Azad, A.K., Oo, A.M.T., Eds.; Elsevier: Amsterdam, The Netherlands, 2024; pp. 81–102. [Google Scholar] [CrossRef]

- Huang, J.; Balcombe, P.; Feng, Z. Technical and economic analysis of different colours of producing hydrogen in China. Fuel 2023, 337, 127227. [Google Scholar] [CrossRef]

- Wang, B.; Li, Z.; Zhou, J.; Cong, Y.; Li, Z. Technological-economic assessment and optimization of hydrogen-based transportation systems in China: A life cycle perspective. Int. J. Hydrogen Energy 2023, 48, 12155–12167. [Google Scholar] [CrossRef]

- Agyekum, E.B. Evaluating the linkages between hydrogen production and nuclear power plants—A systematic review of two decades of research. Int. J. Hydrogen Energy 2024, 65, 606–625. [Google Scholar] [CrossRef]

- Constantin, A. Nuclear hydrogen projects to support clean energy transition: Updates on international initiatives and IAEA activities. Int. J. Hydrogen Energy 2024, 54, 768–779. [Google Scholar] [CrossRef]

- IAEA. Examining the Techno–Economics of Nuclear Hydrogen Production and Benchmark Analysis of the IAEA HEEP Software; International Atomic Energy Agency Publications: Vienna, Austria, 2018; Available online: https://www.iaea.org/publications/13393/examining-the-technoeconomics-of-nuclear-hydrogen-production-and-benchmark-analysis-of-the-iaea-heep-software (accessed on 23 March 2024).

- Alabbadi, A.A.; Obaid, O.A.; AlZahrani, A.A. A comparative economic study of nuclear hydrogen production, storage, and transportation. Int. J. Hydrogen Energy 2024, 54, 849–863. [Google Scholar] [CrossRef]

- Ozcan, H.; Fazel, H. Cost assessment of selected nuclear driven hybrid thermochemical cycles for hydrogen production. Int. J. Hydrogen Energy 2024, 54, 554–561. [Google Scholar] [CrossRef]

- Dewita, E.; Prassanti, R.; Widana, K.S.; Susilo, Y.S.B. Cost Analysis of Nuclear Hydrogen Production Using IAEA-HEEP4 Software. J. Phys. Conf. Ser. 2021, 2048, 012005. [Google Scholar] [CrossRef]

- Soja, R.J.; Gusau, M.B.; Ismaila, U.; Garba, N.N. Comparative analysis of associated cost of nuclear hydrogen production using IAEA hydrogen cost estimation program. Int. J. Hydrogen Energy 2023, 48, 23373–23386. [Google Scholar] [CrossRef]

- IAEA. HydCalc Hydrogen Production Price Estimator; International Atomic Energy Agency Publications: Vienna, Austria, 2018; Available online: https://www.iaea.org/sites/default/files/18/07/hydcalc-manual.pdf (accessed on 23 March 2024).

- Mendrela, P.; Stanek, W.; Simla, T. Sustainability assessment of hydrogen production based on nuclear energy. Int. J. Hydrogen Energy 2024, 49, 729–744. [Google Scholar] [CrossRef]

- Bhattacharyya, R.; Singh, K.; Bhanja, K.; Grover, R. Assessing techno-economic uncertainties in nuclear power-to-X processes: The case of nuclear hydrogen production via water electrolysis. Int. J. Hydrogen Energy 2023, 48, 14149–14169. [Google Scholar] [CrossRef]

- Nam, H.; Nam, H.; Konishi, S. Techno-economic analysis of hydrogen production from the nuclear fusion-biomass hybrid system. Int. J. Energy Res. 2020, 45, 11992–12012. [Google Scholar] [CrossRef]

- Antony, A.; Maheshwari, N.; Rao, A.R. A generic methodology to evaluate economics of hydrogen production using energy from nuclear power plants. Int. J. Hydrogen Energy 2017, 42, 25813–25823. [Google Scholar] [CrossRef]

- Boretti, A. Hydrogen production by using high-temperature gas-cooled reactors. Int. J. Hydrogen Energy 2023, 48, 7938–7943. [Google Scholar] [CrossRef]

- Hercog, J.; Kupecki, J.; Świątkowski, B.; Kowalik, P.; Boettcher, A.; Malesa, J.; Skrzypek, E.; Skrzypek, M.; Muszyński, D.; Tchorek, G. Advancing production of hydrogen using nuclear cycles—Integration of high temperature gas-cooled reactors with thermochemical water splitting cycles. Int. J. Hydrogen Energy 2024, 52, 1070–1083. [Google Scholar] [CrossRef]

- Ji, M.; Shi, M.; Wang, J. Life cycle assessment of nuclear hydrogen production processes based on high temperature gas-cooled reactor. Int. J. Hydrogen Energy 2023, 48, 22302–22318. [Google Scholar] [CrossRef]

- Sun, J.; Shi, X.; Lin, S.; Wang, H. Research on hydrogen risk prediction in probability safety analysis for severe accidents of nuclear power plants. Nucl. Eng. Des. 2024, 417, 112798. [Google Scholar] [CrossRef]

- Gao, Q.; Wang, L.; Peng, W.; Zhang, P.; Chen, S. Safety analysis of leakage in a nuclear hydrogen production system. Int. J. Hydrogen Energy 2022, 47, 4916–4931. [Google Scholar] [CrossRef]

- El-Emam, R.; Khamis, I. International collaboration in the IAEA nuclear hydrogen production program for benchmarking of HEEP. Int. J. Hydrogen Energy 2016, 42, 3566–3571. [Google Scholar] [CrossRef]

- Sorgulu, F.; Dincer, I. Cost evaluation of two potential nuclear power plants for hydrogen production. Int. J. Hydrogen Energy 2018, 43, 10522–10529. [Google Scholar] [CrossRef]

- El-Emam, R.; Khamis, I. The IAEA HEEP: Description and Benchmarking. In Proceedings of the 7th World Hydrogen Technology Convention, Prague, Czech Republic, 9–12 July 2017. [Google Scholar]

- Lee, T.H.; Lee, K.Y.; Shin, Y.J. Preliminary economic evaluation comparison of hydrogen production using G4ECONS and HEEP code. In Proceedings of the HTR, Weihai, China, 27–31 October 2014. [Google Scholar]

- Ozbilen, A.; Dincer, I.; Rosen, M. Development of a four–step Cu–Cl cycle for hydrogen production: Part II: Multi–objective optimization. Int. J. Hydrogen Energy 2016, 41, 7826–7834. [Google Scholar] [CrossRef]

- Ozcan, H.; Dincer, I. Exergoeconomic optimization of a new four-step magnesium–chlorine cycle. Int. J. Hydrogen Energy 2017, 42, 2435–2445. [Google Scholar] [CrossRef]

- Wang, Z.; Naterer, G.; Gabriel, K.; Gravelsins, R.; Daggupati, V. Comparison of sulfur–iodine and copper–chlorine thermochemical hydrogen production cycles. Int. J. Hydrogen Energy 2010, 35, 4820–4830. [Google Scholar] [CrossRef]

- El-Emam, R.S.; Ozcan, H.; Zamfirescu, C. Updates on promising thermochemical cycles for clean hydrogen production using nuclear energy. J. Clean. Prod. 2020, 262, 121424. [Google Scholar] [CrossRef]

- Wang, Q.; Liu, C.; Luo, R.; Li, D.; Macián-Juan, R. Thermodynamic analysis and optimization of the combined supercritical carbon dioxide Brayton cycle and organic Rankine cycle—Based nuclear hydrogen production system. Int. J. Energy Res. 2022, 46, 832–859. [Google Scholar] [CrossRef]

- Nguyen, T.; Abdin, Z.; Holm, T.; Mérida, W. Grid-connected hydrogen production via large-scale water electrolysis. Energy Convers. Manag. 2019, 200, 112108. [Google Scholar] [CrossRef]

- McDonald, A.; Kambitsch, C. Decarbonising Hydrogen in a Net Zero Economy; Aurora Energy Research: Oxford, UK, 2021; Available online: https://auroraer.com/insight/decarbonising-hydrogen-in-a-net-zero-economy/ (accessed on 3 February 2024).

- Veron, E. Preliminary Economic Assessment of GW Scale Nuclear Enabled Hydrogen Production; National Nuclear Laboratory Publications: Cumbria, UK, 2022; Available online: https://www.nnl.co.uk/wp-content/uploads/2022/03/Preliminary-Economic-Assessment-of-Nuclear-Enabled-Hydrogen-Production-Final-Approved.pdf (accessed on 25 March 2024).

- Nadaleti, W.; Gomes de Souza, E.; Souza, S. The potential of hydrogen production from high and low-temperature electrolysis methods using solar and nuclear energy sources: The transition to a hydrogen economy in Brazil. Int. J. Hydrogen Energy 2022, 47, 34727–34738. [Google Scholar] [CrossRef]

- Cany, C.; Mansilla, C.; da Costa, P.; Mathonnière, G. Adapting the French nuclear fleet to integrate variable renewable energies via the production of hydrogen: Towards massive production of low carbon hydrogen. Int. J. Hydrogen Energy 2017, 42, 13339–13356. [Google Scholar] [CrossRef]

- Grimm, A.; de Jong, W.A.; Kramer, G.J. Renewable hydrogen production: A techno-economic comparison of photoelectrochemical cells and photovoltaic-electrolysis. Int. J. Hydrogen Energy 2020, 45, 22545–22555. [Google Scholar] [CrossRef]

- Touili, S.; Merrouni, A.A.; Azouzoute, A.; hassouani, Y.E.; illah Amrani, A. A technical and economical assessment of hydrogen production potential from solar energy in Morocco. Int. J. Hydrogen Energy 2018, 43, 22777–22796. [Google Scholar] [CrossRef]

- Matute, G.; Yusta, J.; Beyza, J.; Monteiro, C. Optimal dispatch model for PV-electrolysis plants in self-consumption regime to produce green hydrogen: A Spanish case study. Int. J. Hydrogen Energy 2022, 47, 25202–25213. [Google Scholar] [CrossRef]

- Rezaei, M.; Khozani, N.; Jafari, N. Wind energy utilization for hydrogen production in an underdeveloped country: An economic investigation. Renew. Energy 2019, 147, 1044–1057. [Google Scholar] [CrossRef]

- European Commission. A Hydrogen Strategy for a Climate–Neutral Europe; Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions: Brussels, Belgium, 2020; Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52020DC0301 (accessed on 26 March 2024).

- European Commission. REPowerEU Plan; Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions: Brussels, Belgium, 2022; Available online: https://commission.europa.eu/publications/key-documents-repowereu_en (accessed on 26 March 2024).

- European Commission. Directive (EU) 2023/2413 of the European Parliament and of the Council of 18 October 2023 Amending Directive (EU) 2018/2001, Regulation (EU) 2018/1999 and Directive 98/70/EC as Regards the Promotion of Energy from Renewable Sources, and Repealing Council Directive (EU) 2015/652; European Parliament and Council: Brussels, Belgium, 2023; Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32023L2413&qid=1699364355105 (accessed on 11 March 2024).

- Belgian Federal Government. Vision and Strategy: Hydrogen. Update October 2022. 2022. Available online: https://economie.fgov.be/sites/default/files/Files/Energy/View-strategy-hydrogen.pdf (accessed on 26 March 2024).

- PWC Belgium. Energy Transition: The Regulatory Pulse of Belgium’s Hydrogen Strategy; PWC Belgium Website: Brussels, Belgium, 2023; Available online: https://news.pwc.be/energy-transition-the-regulatory-pulse-of-belgiums-hydrogen-strategy/ (accessed on 26 March 2024).

- Republic of Bulgaria. Integrated Energy and Climate Plan of the Republic of Bulgaria 2021–2030; Ministry of Energy, Ministry of the Environment and Water: Sofia, Republic of Bulgaria, 2019; Available online: https://faolex.fao.org/docs/pdf/bul212381.pdf (accessed on 12 March 2024).

- Bouacida, I. France’s Hydrogen Strategy: Focusing on Domestic Hydrogen Production to Decarbonise Industry and Mobility; Discussion Paper; Research Institute for Sustainability: Brandenburg, Germany, 2023. [Google Scholar] [CrossRef]

- Rte. The Transition to Low–Carbon Hydrogen in France: Opportunities and Challenges for the Power System by 2030–2035. Le Reseau de Transport d’Electricite. 2020. Available online: https://assets.rte-france.com/prod/public/2021-03/Hydrogen%20report_0.pdf (accessed on 17 March 2024).

- BMWK. National Hydrogen Strategy Update: NHS 2023; Federal Ministry for Economic Affairs and Climate Action: Berlin, Germany, 2023; Available online: https://www.bmwk.de/Redaktion/EN/Publikationen/Energie/national-hydrogen-strategy-update.pdf?__blob=publicationFile&v=2 (accessed on 21 March 2024).

- Detz, R.; Lenzmann, F.; Sijm, J.; Weeda, M. Future Role of Hydrogen in the Netherlands: A Meta–Analysis Based on a Review of Recent Scenario Studies; TNO report; Institute for Sustainable Process Technology, Energy Systems Transition Centre: Freiburg, Germany, 2019; Available online: https://www.newenergycoalition.org/custom/uploads/2020/05/Detz-et-al.-2019-TNO-2019-P11210-Future-Role-of-Hydrogen-in-the-Netherlands_final2-002.pdf (accessed on 21 March 2024).

- Government of the Netherlands. Government Strategy on Hydrogen; Ministry of Economic Affairs and Climate Policy: The Hague, The Netherlands, 2020. Available online: https://www.government.nl/documents/publications/2020/04/06/government-strategy-on-hydrogen (accessed on 21 March 2024).

- NWP. Hydrogen Roadmap for the Netherlands; Dutch National Hydrogen Programme, Ministry of Economic Affairs and Climate Policy: The Hague, The Netherlands, 2022; Available online: https://nationaalwaterstofprogramma.nl/documenten/handlerdownloadfiles.ashx?idnv=2379389 (accessed on 21 March 2024).

- Spanish Government. Hydrogen Roadmap: A Commitment to Renewable Hydrogen; Ministerio para la Transición Ecológica y el Reto Demográfico (MITECO): Madrid, Spain, 2020; Available online: https://www.miteco.gob.es/en/ministerio/planes-estrategias/hidrogeno.html (accessed on 23 March 2024).

- HM Government. The Ten Point Plan for a Green Industrial Revolution: Building Back Better, Supporting Green Jobs, and Accelerating Our Path to Net Zero. United Kingdom. 2020. Available online: https://assets.publishing.service.gov.uk/media/5fb5513de90e0720978b1a6f/10_POINT_PLAN_BOOKLET.pdf (accessed on 24 March 2024).

- DNV. UK Energy Transition Outlook 2024; Det Norske Veritas: Hovik, Norway, 2024; Available online: https://www.dnv.com/energy-transition-outlook/uk/index (accessed on 27 March 2024).

- HM Government. Hydrogen Strategy Delivery Update: Hydrogen Strategy Update to the Market; Department for Energy Security and Net Zero: London, UK, 2023. Available online: https://assets.publishing.service.gov.uk/media/65841578ed3c3400133bfcf7/hydrogen-strategy-update-to-market-december-2023.pdf (accessed on 24 March 2024).

- EDF. H2H—Hydrogen to Heysham Feasibility Report; EDF Energy R&D UK Centre: London, UK, 2019. Available online: https://assets.publishing.service.gov.uk/media/5e4ab9beed915d4ff62d1d55/Phase_1_-_EDF_-_Hydrogen_to_Heysham.pdf (accessed on 24 March 2024).

- Argentina Presidency. National Strategy for the Development of Hydrogen Economy; Secretariat for Strategic Affairs: London, UK, 2023; Available online: https://emarr.cancilleria.gob.ar/userfiles/strategie_nationale_de_developpement_de_leconomie_de_lhydrogene_0.pdf (accessed on 24 March 2024).

- Brazilian Republic. Programa Nacional de Hidrogênio—PNH2; Ministry of Mines and Energy: Lisbon, Portugal, 2021. Available online: https://www.gov.br/mme/pt-br/assuntos/noticias/mme-apresenta-ao-cnpe-proposta-de-diretrizes-para-o-programa-nacional-do-hidrogenio-pnh2/HidrognioRelatriodiretrizes.pdf (accessed on 28 March 2024).

- Chantre, C.; Andrade Eliziário, S.; Pradelle, F.; Católico, A.C.; Branquinho Das Dores, A.M.; Torres Serra, E.; Campello Tucunduva, R.; Botelho Pimenta Cantarino, V.; Leal Braga, S. Hydrogen economy development in Brazil: An analysis of stakeholders’ perception. Sustain. Prod. Consum. 2022, 34, 26–41. [Google Scholar] [CrossRef]

- Government of Canada. Hydrogen Strategy for Canada: Seizing the Opportunities for Hydrogen: A Call to Action; Ministry of Natural Resources: Ottawa, QC, Canada, 2020; Available online: https://natural-resources.canada.ca/sites/nrcan/files/environment/hydrogen/NRCan_Hydrogen-Strategy-Canada-na-en-v3.pdf (accessed on 27 March 2024).

- Government of Ontario. Ontario’s Low–Carbon Hydrogen Strategy—A Path Forward; Ministry of Energy, Canada: Toronto, ON, Canada, 2022; Available online: https://www.ontario.ca/files/2022-04/energy-ontarios-low-carbon-hydrogen-strategy-en-2022-04-11.pdf (accessed on 13 March 2024).

- U.S. Government. U.S. National Clean Hydrogen Strategy and Roadmap; U.S. Department for Energy: Washington, DC, USA, 2023. Available online: https://www.hydrogen.energy.gov/docs/hydrogenprogramlibraries/pdfs/us-national-clean-hydrogen-strategy-roadmap.pdf (accessed on 16 March 2024).

- U.S. Government. Pathways to Commercial Liftoff: Clean Hydrogen; U.S. Department for Energy: Washington, DC, USA, 2023. Available online: https://liftoff.energy.gov/wp-content/uploads/2023/05/20230320-Liftoff-Clean-H2-vPUB-0329-update.pdf (accessed on 16 March 2024).

- Connelly, E.; Elgowainy, A.; Ruth, M. Current Hydrogen Market Size: Domestic and Global; Hydrogen and Fuel Cells Program, U.S. Department of Energy: Washington, DC, USA, 2019. Available online: https://www.hydrogen.energy.gov/docs/hydrogenprogramlibraries/pdfs/19002-hydrogen-market-domestic-global.pdf?Status=Master (accessed on 16 March 2024).

- Holt, M. Advanced Nuclear Reactors: Technology Overview and Current Issues. In CRS Report prepared for Members and Committees of Congress, Congressional Research Service; Library of Congress: Washington, DC, USA, 2023. Available online: https://crsreports.congress.gov/product/pdf/R/R45706#:~:text=The%20Energy%20Act%20of%202020%20authorized%20the%20Advanced%20Reactor%20Demonstration,for%20possible%20future%20demonstration%20plants (accessed on 16 March 2024).