1. Introduction

In order to mitigate carbon leakage in international trade and improve the competitiveness of products within the EU, the EU proposed for the first time the EU Carbon Border Adjustment Mechanism (CBAM) in December 2019 in the European Green Deal. This mechanism would tax imports of specific carbon-intensive products based on the product’s carbon emissions and the EU carbon market price, which could eliminate the cost difference in carbon emission reduction between firms within the EU and foreign firms [

1]. On 16 May 2023, the EU CBAM Act was officially published in the Official Journal of the European Union, indicating that the EU CBAM had completed all legislative procedures; it entered into force on 17 May. According to the content of the act, the EU will formally impose tariffs on 1 January 2026, after a three-year transition period. Although the EU CBAM is still in transition, it will change the global trade division to a certain extent in the future, especially for countries with a high proportion of carbon-intensive exports and close trade with the EU [

2].

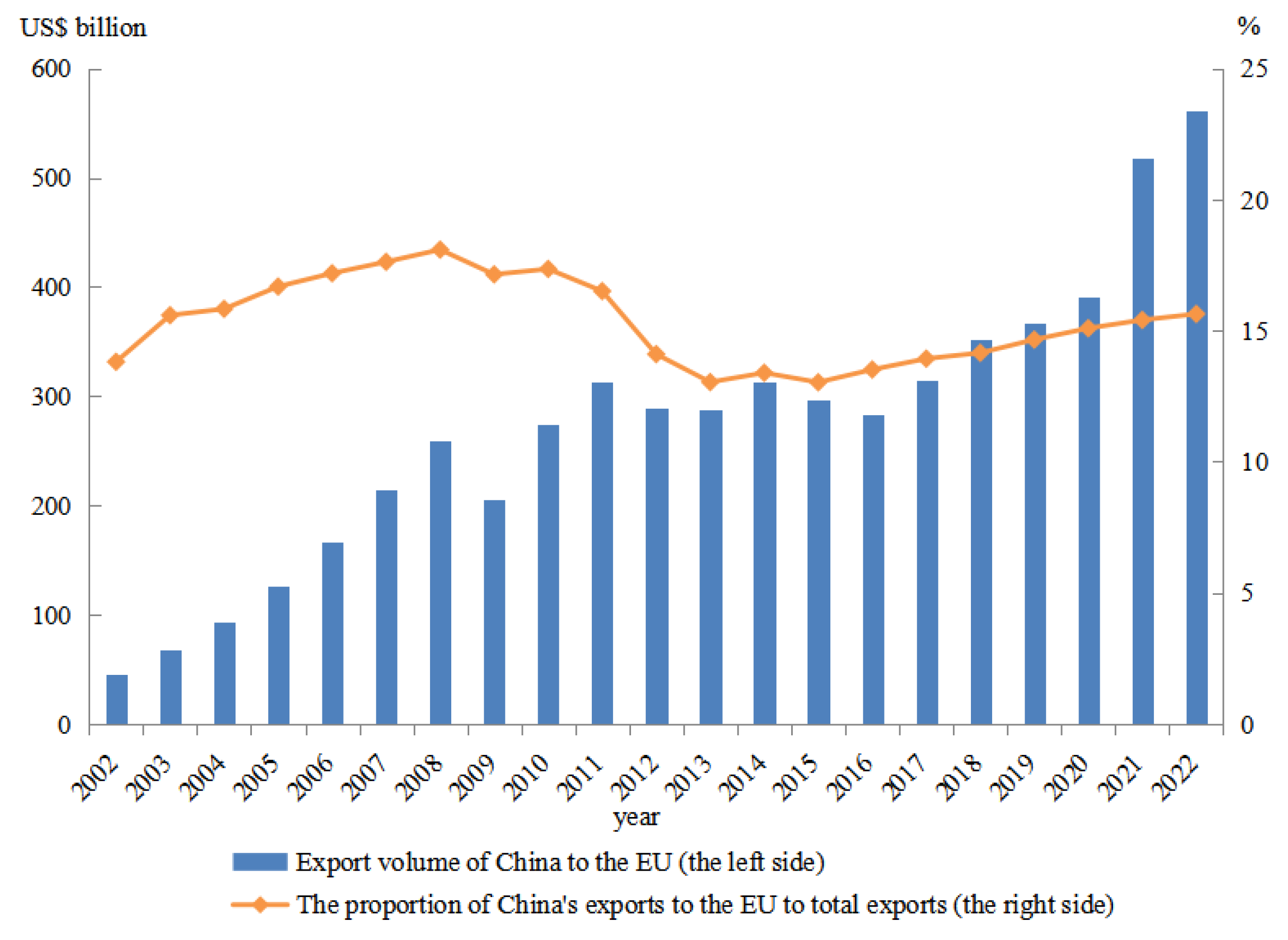

China, which is both the EU’s major trading partner and the largest source of carbon emissions embodied in EU import trade, will undoubtedly be affected by the EU CBAM. China’s exports to the EU have been growing over the past 20 years, from USD 44.97 billion to USD 56.197 billion (see

Figure 1 for details). During the period 2002–2022, China’s exports to the EU accounted for about 15% of China’s total exports. Statistics show that, in 2022, the share of China’s exports of high-carbon leakage products (that is, products included in the EU’s carbon leakage list) to the EU was 31.14%. In addition, some steel and aluminum are exported from China to other countries as intermediate products, which are processed and re-exported to the EU [

1]. Given the large volume of trade between China and the EU and the carbon-intensive characteristics of China’s exports [

3,

4], the EU’s carbon tariffs will inevitably have a negative impact on China’s export of carbon-intensive products and their related sectors. Therefore, before the tariffs are formally imposed, it is of great significance for the Chinese government to formulate targeted measures to mitigate the impact of the CBAM on China’s foreign trade by assessing the possible impact of the EU CBAM on China’s exports to the EU.

Since the CBAM was proposed, its rationality has caused a lot of controversy [

5,

6,

7], and a growing number of studies have begun to focus on the impact of the CBAM. A widely discussed issue is that, by imposing additional prices on imports, developed countries might increase the competitiveness of domestic products at the expense of imports and transfer part of the costs of emission reductions to trading partners [

8]. This makes the CBAM suspected to be a green trade protectionist tool [

9], and considered to violate the principle of common but differentiated responsibilities (CBDR) in the United Nations Framework Convention on Climate Change [

10,

11]. This argument is often put forward in developing countries [

12], because they are export-oriented and production technologies are usually carbon-intensive [

13].

Relevant research on the impact of the CBAM focuses on discussing the impact of the CBAM implementation on the economy and trade. Research on specific countries shows that the implementation of carbon-based Border-Tax Adjustments (BTAs) in the United States negatively affects China’s exports and reduces domestic income [

14]. Although Gros [

15] found that the imposition of carbon tariffs could increase global welfare, more results from global dimensions suggest that the economic and trade losses caused by the CBAM will be greater than the benefits. Burniaux et al. [

16] used a global general equilibrium model to show that, although the economic effects of BTAs vary due to the way they are implemented, their welfare effects are generally negative at the world level. Using a GTAP-E model, Septiyas and Widodo [

17] also confirmed that if China imposes tariffs on coal imports to the United States, there would be a global trade offset and a trade depression.

As one of the EU’s core policy tools to address climate change, the EU CBAM has become a hot topic in academia recently. Carbon tariffs on imports from EU trading partners might bring tangible results in avoiding carbon leakage, as well as a significant impact on trade [

8,

18,

19]. By simulating changes in the overall exports of EU member states and non-EU member states to the EU, Zhong and Pei [

11] found that after the implementation of the EU CBAM, output in the EU would increase by 0.38%, while output in the rest of the world would decrease by 0.1%. Due to the degree of exposure of countries exporting CBAM products to the EU varying substantially, at least 2% of exports and 1% of production in many developing countries would be affected by the EU CBAM [

20]. In relative terms, Russia, Ukraine and China would suffer large welfare losses [

21]. A study of China’s agricultural trade by Yang et al. [

22] found that the EU’s carbon tariffs would result in a reduction of about 0.06% in the production of most of China’s taxed agricultural commodities, while only petroleum, fruit and vegetables, and dairy products would not be affected. Lin and Zhao [

1] used steel rebar and aluminum futures data from the Shanghai Futures Exchange (SHFE) and examined the impact of the EU CBAM on China’s steel rebar and aluminum futures contracts. They found that both steel rebar and aluminum futures in China would be negatively affected by the CBAM, and aluminum is more sensitive due to its high export intensity and carbon emissions.

Although the above studies make some contributions to analyzing the impact of the EU CBAM on China, it still needs further exploration. First, early studies mainly investigated the global or country-specific impacts of similar carbon tariff mechanisms, such as the BTAs implemented by the United States. While most of the recent research has begun to focus on the impacts of the EU CBAM, little of this literature pays attention to China, which will be the main relevant country for impacts of the EU CBAM as it is an important trading partner for EU carbon-intensive product imports. Second, the EU CBAM currently applies to six sectors, cement, electricity, fertilizers, steel, aluminum and hydrogen, but there is still potential to expand the coverage of sectors in the future. For this reason, it is necessary to further consider the impact of the EU CBAM under different sector coverage scenarios.

To solve these problems, this paper analyzes the impact of the EU CBAM on China’s exports to the EU based on the GTAP-E model. First of all, this paper uses the recursive dynamic method to update the GTAP-E database to 2026, and sets up simulation scenarios according to different sector coverage and carbon emission calculations. Then, the impact of the EU CBAM on China’s exports to the EU under different scenarios is simulated from four perspectives: export price, trade structure, trade value and terms of trade.

This paper expands existing studies in the following aspects. First, this paper innovatively quantifies the impact of the EU CBAM on China’s exports to the EU. Previous studies richly discuss the EU CBAM or other similar mechanisms through the equilibrium model, but ignore the possible impact on trade between China and the EU. The results of this paper can not only provide empirical evidence for the Chinese government to better respond to the impacts of the EU CBAM, but also provide an effective reference for other developing countries trading with the EU. Second, simulating the impact of different sector coverage and carbon emission calculations could provide a more comprehensive analysis for assessing the impact of the EU CBAM. This is crucial to reduce uncertainty in the simulation results.

The rest of the paper is organized as follows.

Section 2 describes the legislative process and content of the EU CBAM.

Section 3 details the model, data and scenario settings for simulating the impact of the EU CBAM on China’s exports to the EU. Simulation results under different scenarios are presented in

Section 4.

Section 5 summarizes the conclusions and presents policy implications.

2. The Legislative Processes and Contents of the EU CBAM

Carbon leakage occurs when carbon-intensive firms try to reduce their carbon costs by moving production to countries with less stringent environmental regulations, because carbon emissions of these countries offset the mitigation effect of strict environmental regulations [

23,

24,

25]. The EU CBAM is recognized as a policy measure to address carbon leakage, and the EU CBAM could ensure that the EU’s carbon-intensive firms are competitive against foreign firms [

26,

27].

Specifically, the EU CBAM was first proposed in December 2019 in the European Green Deal. In this deal, the EU Commission proposed to achieve climate goals by expanding the coverage of the carbon market, accelerating the rate of free quota degradation and introducing the CBAM. In March 2020, the EU Commission published an assessment report on the initial impacts of the EU CBAM, which identifies the elements that need to be taken into account in the design of the EU CBAM as well as the framework for impact assessment. The EU Commission also publicly solicited comments in the following months. The EU CBAM was included in the 2021 legislative proposal in September 2020 and passed a vote in the European Parliament in March 2021. The EU Commission formally submitted the EU CBAM proposal in July 2021, which meant that this proposal would enter the legislative process. On 25 April 2023, the EU Council voted to approve the EU CBAM proposal, which entered into force 20 days later. The EU CBAM Act thus successfully completed all the legislative processes and became part of EU law. The main events in the EU CBAM legislative process are shown in

Table 1.

According to the act, the content of the EU CBAM can be summarized as follows. The EU CBAM initially covers products in six sectors: steel, aluminum, cement, fertilizers, electricity and hydrogen. The specific scope of the levy is the direct emissions of these products as well as embodied emissions other than steel and aluminum (where direct emissions refer to carbon emissions during production that are directly controlled by the producer, and embodied emissions also include carbon emissions from electricity consumption, heating and cooling). The transition period for the EU CBAM is from 1 October 2023 to 31 December 2025, during which time firms need only to fulfill the reporting obligations; that is, they need to submit data on the quantity of direct carbon emissions and embodied carbon emissions of imported products every year without paying fees. On 1 January 2026, the EU CBAM will be formally implemented and will be fully implemented by 2034. After that, firms will not only have to report the annual carbon emission data of imported products, but will also have to pay the corresponding carbon emission fees in the form of purchasing CBAM vouchers. The fees to be paid depend on the product’s carbon emissions after deducting free quotas, the carbon price of the exporter and the price of the EU CBAM voucher. It is worth noting that the price of the EU CBAM voucher is calculated by the EU Commission based on the average closing price of carbon quotas in the EU Emissions Trading System (EU-ETS). Thus, the EU CBAM is also seen as a supplement to the EU-ETS [

1]. With the expansion of coverage, the EU CBAM would capture more than 50% of the carbon emissions of the EU-ETS.

5. Conclusions and Policy Implications

Since the latest provisions of the EU CBAM were officially released only in May 2023, the existing literature has not yet provided a targeted assessment of the implemented new act. Therefore, it is of great significance for this paper to use the recursive GTAP-E model to simulate the impact of the EU CBAM on China’s exports to the EU in terms of the four aspects of export price, trade structure, trade value and terms of trade, by setting up various simulation scenarios based on the content of the act. The main simulation results are as follows:

(1) When the EU imposes carbon tariffs on China, the export prices of the taxed sectors in China decreases. At the same time, it will also have certain spillover effects on other sectors, so that all sectors other than crude oil and natural gas extraction have the same change trend. The export price of each sector changes more greatly when the carbon emission calculation is changed from direct carbon emissions to embodied carbon emissions. With the expansion of the scope of taxation, agriculture, forestry, animal husbandry and fishery replaced non-metallic mineral products as the most affected sector. (2) The simulation results in China’s export volume to the EU show that most of the taxed sectors show an export transfer effect and export inhibition effect. For other sectors that are not taxed, the growth rate of export volume to the EU is higher than that of other countries (regions). (3) In terms of trade value, the effect of the EU CBAM on some sectors of China would not only inhibit China’s total export value, but would also significantly reduce the EU’s total exports, and the latter’s decrease is even greater. With the expansion of the scope of taxation and the change in the carbon emission calculation method, the change in the export value of China and the EU increases in multiples. Compared with the expansion of the scope of taxation, the change in the carbon emission calculation method has a greater impact on China’s exports. (4) The implementation of the EU CBAM improves the terms of trade of the EU and worsens the terms of trade of China. If the EU taxes China, not only do China’s terms of trade deteriorate, but also the terms of trade of the United States and South Africa deteriorate slightly, and the trade balance is negative. There is also significant heterogeneity in the changes in China’s trade balance across sectors.

In summary, the implementation of the EU CBAM will negatively affect China’s exports to the EU. The findings of this paper provide a new empirical evidence and policy implication for Chinese policymakers and firms on how to take measures to deal with these shocks, and also provide a reference for other developing countries to better respond to the EU CBAM. First, China should strengthen negotiations with the EU on issues such as the measurement of carbon emissions and the determination of the carbon price, in order to secure favorable conditions for the export of China’s carbon-intensive products to the EU. At the same time, China should strengthen cooperation with developing countries in climate change, and improve its discourse power by agreements such as RCEP and the Belt and Road. Second, China should promote the construction of a unified national carbon market as soon as possible. By establishing reasonable carbon pricing and expanding the carbon emission trading sector, the carbon cost of carbon-intensive sectors would be increased, thereby narrowing the price gap between China and the international carbon emission trading market. In order to avoid double taxation, China could take the initiative to levy a differentiated carbon tax domestically, thus allowing the proceeds to be better used to promote the operation of the national economy. Third, the implementation of the EU CBAM has increased the pressure on China’s exports, especially carbon-intensive products, as China is the largest source of embodied carbon emissions from EU imports. To this end, policymakers should consider expanding other areas in the international market to reduce dependence on the EU market, and achieving a diversified international trade strategy, which could help mitigate export losses caused by the EU CBAM and increase the resilience of China’s trade. Finally, firms should establish a carbon emission accounting system for production while improving green R&D technologies. By tracing the carbon footprints of the products, we could gradually achieve carbon reduction targets and minimize the risk of tariffs on exports.

Although this paper reveals the impact of the EU CBAM on China’s exports to the EU, there are still some limitations. Since the latest data on the GTAP-E 10 database are from 2014, this paper obtained the forecast data for 2026 by the recursive dynamic method. The impact of COVID-19 and trade conflicts may lead to deviations between these data and reality. Therefore, in the future, more accurate simulation results could be provided if the latest data are available.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}