Decarbonizing the Construction Sector: Strategies and Pathways for Greenhouse Gas Emissions Reduction

Abstract

1. Introduction

2. The Regulative Framework

2.1. Paris Agreement

2.2. European Green Deal

2.3. European Climate Law

2.4. Fit-for-55

- EU emissions trading system (EU ETS);

- Effort sharing regulation;

- Land use and forestry (LULUCF);

- Alternative fuels infrastructure;

- Carbon Border Adjustment Mechanism (CBAM);

- Social climate fund;

- REfuelEU aviation and FuelEU maritime;

- CO2 emissions standards for cars and vans;

- Energy taxation;

- Renewable energy;

- Energy efficiency.

2.5. Renewable Energy Directive

3. Current State of Key European Sectors

3.1. The Energy Sector

3.2. The Environment Sector

3.3. The Construction Sector

3.4. The Real Estate Development Sector

4. Mapping GHG Emissions of Construction Companies

4.1. Structured Four-Step Decarbonization Approach

- Step I: Defining the scope of GHG-based activities;

- Step II: Conducting a GHG inventory for all categories of business functions;

- Step III: Setting targets;

- Step IV: Planning reductions over time.

4.2. Data Sources and Methodology

4.2.1. Data Collection

4.2.2. Emissions Calculation Methodologies

- Scope 1 (direct emissions) [56]: Calculated via fuel consumption data (e.g., diesel, natural gas) using GHG Protocol emission factors.

- Scope 2 (indirect energy emissions): Derived from electricity and heat consumption, adjusted for regional grid emission factors.

- Scope 3 (value chain emissions) [57]: Estimated using input–output analysis for upstream activities (e.g., raw material extraction, cement production) and downstream processes (e.g., waste disposal).

4.2.3. Validation Techniques

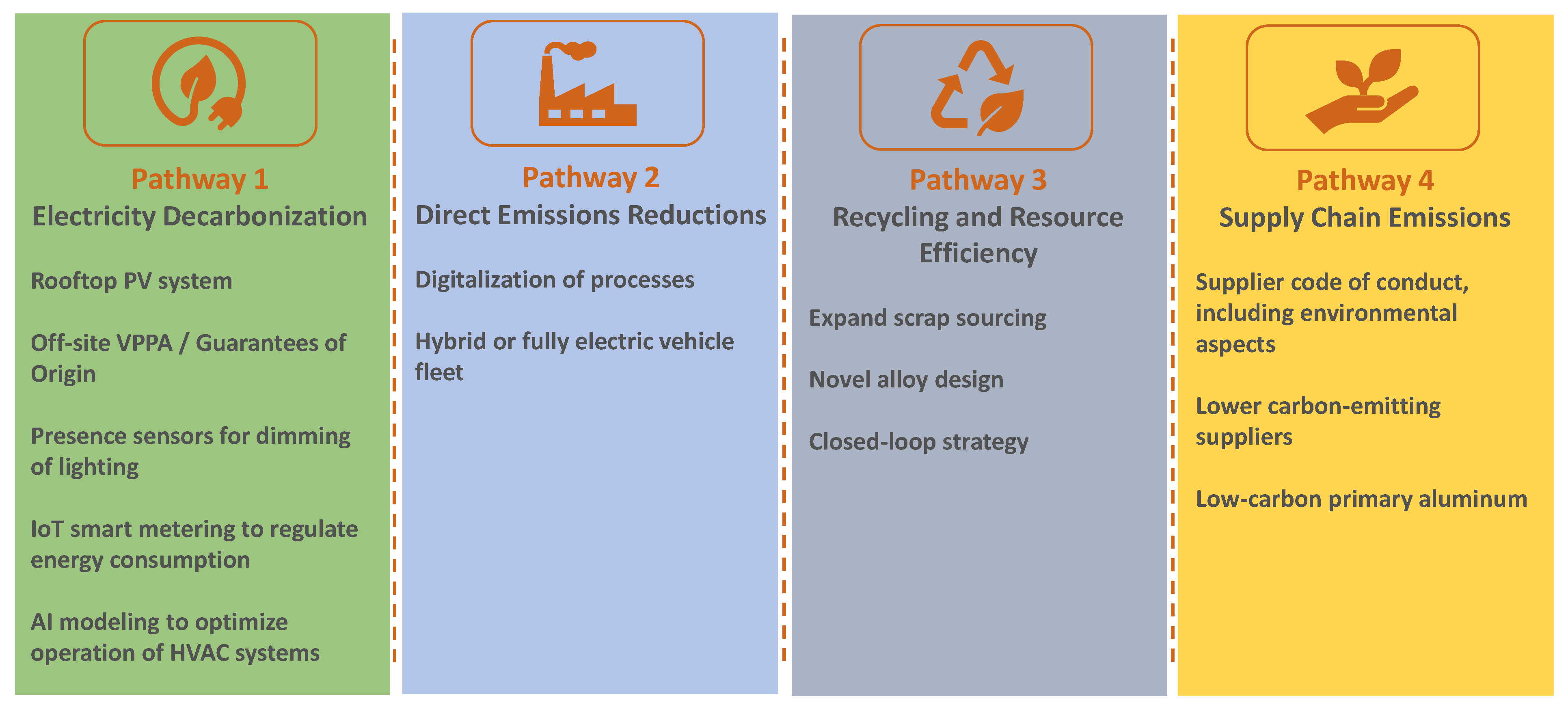

5. GHG Emission Reduction Pathways of Construction Companies

- Pathway 1: Electricity decarbonization.

- Pathway 2: Direct emissions reduction.

- Pathway 3: Recycling and resource efficiency.

- Pathway 4: Supply chain emissions.

5.1. Pathway 1: Electricity Decarbonization

- Reviewing energy consumption documentation;

- Addressing potential recording issues;

- The comprehensive analysis of energy usage by type and purpose;

- Monitoring energy consumption patterns;

- Actionable energy conservation planning and execution;

- Exploring funding avenues;

- Setting and tracking energy performance metrics;

- Facilitating knowledge sharing across subsidiaries.

5.2. Pathway 2: Direct Emissions Reduction

5.3. Pathway 3: Recycling and Resource Efficiency

5.4. Pathway 4: Supply Chain Emissions

6. Empirical Exercise

- Align with the Science Based Targets initiative—the SBTi’s 1.5 °C pathway specifies a 4.2% annual reduction;

- 2030 Target: Reduce emissions by 30% (baseline: 496,200 kg CO2e → 347,340 kg CO2e).

7. Challenges and Mitigation Strategies

8. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Calle Müller, C.; Pradhananga, P.; ElZomor, M. Pathways to decarbonization, circular construction, and sustainability in the built environment. Int. J. Sustain. High. Educ. 2024, 25, 1315–1332. [Google Scholar] [CrossRef]

- Mavi, R.; Morel, J.-C.; Rakhshan, K. Barriers to Implementing the Circular Economy in the Construction Industry: A Critical Review. Sustainability 2021, 13, 12989. [Google Scholar] [CrossRef]

- United Nations Framework Convention on Climate Change. Paris Agreement. 2015. Available online: https://unfccc.int/process-and-meetings/the-paris-agreement/the-paris-agreement (accessed on 27 October 2024).

- European Parliament. The European Green Deal: Striving to Be the First Climate-Neutral Continent. 2021. Available online: https://www.europarl.europa.eu/news/en/headlines/society/20200618STO81513/the-european-green-deal-striving-to-be-the-first-climate-neutral-continent (accessed on 30 October 2024).

- Bouckaert, S.; Fernandez Pales, A.; McGlade, C.; Remme, U.; Wanner, B.; Varro, L.; D’Ambrosio, D.; Spencer, T. Net Zero by 2050: A Roadmap for the Global Energy Sector; International Energy Agency (IEA), IEA Publications: Paris, France, 2021. [Google Scholar]

- Karakosta, C.; Flamos, A.; Forouli, A. Identification of climate policy knowledge needs: A stakeholders consultation approach. Int. J. Clim. Change Strateg. Manag. 2018, 10, 772–795. [Google Scholar] [CrossRef]

- European Commission. Fit for 55: Delivering the EU’s 2030 Climate Target on the Way to Climate Neutrality. 2022. Available online: https://www.eesc.europa.eu/en/our-work/opinions-information-reports/opinions/fit-55-delivering-eus-2030-climate-target-way-climate-neutrality (accessed on 31 October 2024).

- European Commission. Renewable Energy Directive (RED II). 2020. Available online: https://energy.ec.europa.eu/topics/renewable-energy/renewable-energy-directive-targets-and-rules/renewable-energy-directive_en (accessed on 1 November 2024).

- European Commission. RePowerEU Plan. 2022. Available online: https://ec.europa.eu/commission/presscorner/detail/en/ip_22_3131 (accessed on 1 November 2024).

- Charef, R.; Lu, W. Factor dynamics to facilitate circular economy adoption in construction. J. Clean. Prod. 2021, 319, 128639. [Google Scholar] [CrossRef]

- Osobajo, O.A.; Oke, A.; Omotayo, T.; Obi, L.I. A systematic review of circular economy research in the construction industry. Smart Sustain. Built Environ. 2020, 11, 39–64. [Google Scholar] [CrossRef]

- Hossain, U.; Ng, S.T.; Antwi-Afari, P.; Amor, B. Circular economy and the construction industry: Existing trends, challenges and prospective framework for sustainable construction. Renew. Sustain. Energy Rev. 2020, 130, 109948. [Google Scholar] [CrossRef]

- Hertwich, E.G.; Ali, S.; Ciacci, L.; Fishman, T.; Heeren, N.; Masanet, E.; Asghari, F.N.; Olivetti, E.; Pauliuk, S.; Tu, Q.; et al. Material efficiency strategies to reducing greenhouse gas emissions associated with buildings, vehicles, and electronics—A review. Environ. Res. Lett. 2019, 14, 043004. [Google Scholar] [CrossRef]

- Karakosta, C.; Papathanasiou, J. Climate-Driven Sustainable Energy Investments: Key Decision Factors for a Low-Carbon Transition Using a Multi-Criteria Approach. Energies 2024, 17, 5515. [Google Scholar] [CrossRef]

- Agrawal, R.; De Tommasi, L.; Lyons, P.; Zanoni, S.; Papagiannis, G.K.; Karakosta, C.; Papapostolou, A.; Durand, A.; Martinez, L.; Fragidis, G.; et al. Challenges and opportunities for improving energy efficiency in SMEs: Learnings from seven European projects. Energy Effic. 2023, 16, 17. [Google Scholar] [CrossRef]

- Curkovic, S.; Sroufe, R. Using ISO 14001 to promote a sustainable supply chain strategy. Bus. Strategy Environ. 2011, 20, 71–93. [Google Scholar] [CrossRef]

- Iraldo, F.; Testa, F.; Frey, M. Environmental Management System and SMEs: EU Experience, Barriers and Perspectives. Environ. Manag. 2010, 258. [Google Scholar] [CrossRef]

- Karakosta, C.; Askounis, D.; Psarras, J. Visioning the Carbon Market as a Vehicle for Transferring Low Emission Technologies. In Advances in Environmental Research; Daniels, J.A., Ed.; Nova Science Publishers, Inc.: Hauppauge, NY, USA, 2012; Volume 21, Chapter 7; pp. 207–225. ISBN 978-1-61470-007-4. [Google Scholar]

- European Commission. Carbon Border Adjustment Mechanism (CBAM). 2025. Available online: https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en (accessed on 15 November 2024).

- Clora, F.; Yu, W.; Corong, E. Alternative carbon border adjustment mechanisms in the European Union and international responses: Aggregate and within-coalition results. Energy Policy 2023, 174, 113454. [Google Scholar] [CrossRef]

- Karlsson, I.; Rootzén, J.; Johnsson, F.; Erlandsson, M. Achieving net-zero carbon emissions in construction supply chains—A multidimensional analysis of residential building systems. Dev. Built Environ. 2021, 8, 100059. [Google Scholar] [CrossRef]

- Parvin, K.; Hossain, M.J.; Arsad, A.Z.; Ker, P.J.; Hannan, M.A. Building energy technologies towards achieving net-zero pathway: A comprehensive review, challenges and future directions. J. Build. Eng. 2025, 100, 111795. [Google Scholar] [CrossRef]

- Reddy, V.J.; Hariram, N.P.; Ghazali, M.F.; Kumarasamy, S. Pathway to Sustainability: An Overview of Renewable Energy Integration in Building Systems. Sustainability 2024, 16, 638. [Google Scholar] [CrossRef]

- Cucchiella, F.; D’Adamo, I. Issue on supply chain of renewable energy. Energy Convers. Manag. 2013, 76, 774–780. [Google Scholar] [CrossRef]

- Zeng, N.; Liu, Y.; Mao, C.; König, M. Investigating the Relationship between Construction Supply Chain Integration and Sustainable Use of Material: Evidence from China. Sustainability 2018, 10, 3581. [Google Scholar] [CrossRef]

- Hmouda, A.M.O.; Orzes, G.; Sauer, P.C. Sustainable supply chain management in energy production: A literature review. Renew. Sustain. Energy Rev. 2024, 191, 114085. [Google Scholar] [CrossRef]

- Tijanić, L.; Kersan-Škabić, I. Tracking the Green Transition in the European Union Within the Framework of EU Cohesion Policy: Current Results and Future Paths. Economies 2025, 13, 37. [Google Scholar] [CrossRef]

- Ottomano Palmisano, G.; Rocchi, L.; Negri, L.; Piscitelli, L. Evaluating the Progress of the EU Countries Towards Implementation of the European Green Deal: A Multiple Criteria Approach. Land 2025, 14, 141. [Google Scholar] [CrossRef]

- Hartley, K.; van Santen, R.; Kirchherr, J. Policies for transitioning towards a circular economy: Expectations from the European Union (EU). Resour. Conserv. Recycl. 2020, 155, 104634. [Google Scholar] [CrossRef]

- Nowak-Marchewka, K.; Osmólska, E.; Stoma, M. Progress and Challenges of Circular Economy in Selected EU Countries. Sustainability 2025, 17, 320. [Google Scholar] [CrossRef]

- Torgautov, B.; Zhanabayev, A.; Tleuken, A.; Turkyilmaz, A.; Mustafa, M.; Karaca, F. Circular Economy: Challenges and Opportunities in the Construction Sector of Kazakhstan. Buildings 2021, 11, 501. [Google Scholar] [CrossRef]

- Kiani Mavi, R.; Gengatharen, D.; Kiani Mavi, N.; Hughes, R.; Campbell, A.; Yates, R. Sustainability in Construction Projects: A Systematic Literature Review. Sustainability 2021, 13, 1932. [Google Scholar] [CrossRef]

- Alaa, N.; Asser, E. A review of sustainability applications in the construction industry: Perspectives and challenges. Vestn. MGSU 2023, 18, 771–784. [Google Scholar] [CrossRef]

- Nilsson, L.J.; Bauer, F.; Åhman, M.; Andersson, F.N.G.; Bataille, C.; de la Rue du Can, S.; Ericsson, K.; Hansen, T.; Johansson, B.; Lechtenböhmer, S.; et al. An industrial policy framework for transforming energy and emissions intensive industries towards zero emissions. Clim. Policy 2021, 21, 1053–1065. [Google Scholar] [CrossRef]

- Jiang, J.; He, Z.; Ke, C. Construction Contractors’ Carbon Emissions Reduction Intention: A Study Based on Structural Equation Model. Sustainability 2023, 15, 10894. [Google Scholar] [CrossRef]

- Al Khaffaf, I.; Tamimi, A.; Ahmed, V. Pathways to Carbon Neutrality: A Review of Strategies and Technologies Across Sectors. Energies 2024, 17, 6129. [Google Scholar] [CrossRef]

- Zocchi, G.; Hosseini, M.; Triantafyllidis, G. Exploring the Synergy of Advanced Lighting Controls, Building Information Modelling and Internet of Things for Sustainable and Energy-Efficient Buildings: A Systematic Literature Review. Sustainability 2024, 16, 10937. [Google Scholar] [CrossRef]

- Karakosta, C.; Corovessi, A. One-stop Shop Solutions for Residential Building Energy Renovation: Benefits and Challenges. Facta Univ. Ser. Econ. Organ. 2024, 21, 163–174. [Google Scholar] [CrossRef]

- Adams, K.; Osmani, M.; Thorpe, A.; Thornback, J. Circular economy in construction: Current awareness, challenges and enablers. Proc. Inst. Civ. Eng. Waste Resour. Manag. 2017, 170, 15–24. [Google Scholar] [CrossRef]

- Karakosta, C. A Holistic Approach for Addressing the Issue of Effective Technology Transfer in the Frame of Climate Change. Energies 2016, 9, 503. [Google Scholar] [CrossRef]

- European Commission. European Climate Law. 2021. Available online: https://ec.europa.eu/clima/eu-action/european-green-deal/european-climate-law_en (accessed on 20 November 2024).

- European Commission. Proposal for a Revised Renewable Energy Directive. 2021. Available online: https://commission.europa.eu/news/commission-presents-renewable-energy-directive-revision-2021-07-14_en (accessed on 25 November 2024).

- Fan, J.H.; Omura, A.; Roca, E. Geopolitics and rare earth metals. Eur. J. Political Econ. 2023, 78, 102356. [Google Scholar] [CrossRef]

- Nováková, K.; Pražanová, A.; Stroe, D.-I.; Knap, V. Second-Life of Lithium-Ion Batteries from Electric Vehicles: Concept, Aging, Testing, and Applications. Energies 2023, 16, 2345. [Google Scholar] [CrossRef]

- Eurelectric & E.DSO. Decarbonisation Pathways for the European Electricity Sector. 2021. Available online: https://www.eurelectric.org (accessed on 25 November 2024).

- Martins, E. EU Action Plan for Grids: Europe’s Strategy for Upgrading Grid Infrastructure; Synertics GmbH: Munich, Germany, 2024. [Google Scholar]

- Nayanathara Thathsarani Pilapitiya, P.G.C.; Ratnayake, A.S. The world of plastic waste: A review. Clean. Mater. 2024, 11, 100220. [Google Scholar] [CrossRef]

- Tran, T.; Goto, H.; Matsuda, T. The Impact of China’s Tightening Environmental Regulations on International Waste Trade and Logistics. Sustainability 2021, 13, 987. [Google Scholar] [CrossRef]

- United Nations Environment Programme. Global Waste Management Outlook 2024. Available online: https://www.unep.org/resources/global-waste-management-outlook-2024 (accessed on 30 November 2024).

- International Energy Agency. World Energy Outlook 2024; IEA: Paris, France, 2024. [Google Scholar]

- Yilmaz, D.G.; Cesur, F. A Study for the Improvement of the Energy Performance Certificate (EPC) System in Turkey. Sustainability 2023, 15, 14074. [Google Scholar] [CrossRef]

- Wu, H.; Zhou, W.; Chen, K.; Zhang, L.; Zhang, Z.; Li, Y.; Hu, Z. Carbon Emissions Assessment for Building Decoration Based on Life Cycle Assessment: A Case Study of Office Buildings. Sustainability 2023, 15, 14055. [Google Scholar] [CrossRef]

- Saradara, S.M.; Khalfan, M.M.A.; Rauf, A.; Qureshi, R. On The Path towards Sustainable Construction—The Case of the United Arab Emirates: A Review. Sustainability 2023, 15, 14652. [Google Scholar] [CrossRef]

- Gąsior, A.; Grabowski, J.; Ropęga, J.; Walecka, A. Creating a Competitive Advantage for Micro and Small Enterprises Based on Eco-Innovation as a Determinant of the Energy Efficiency of the Economy. Energies 2022, 15, 6965. [Google Scholar] [CrossRef]

- Favour, U.; Emmanuel, A.; Wisdom, E.; Danny, M.; Kehinde, O.; Nwakamma, N.-E. Integrating Renewable Energy Solutions in The Manufacturing Industry: Challenges and Opportunities: A Review. Eng. Sci. Technol. J. 2024, 5, 674–703. [Google Scholar] [CrossRef]

- Greenhouse Gas Protocol. The Greenhouse Gas Protocol. A Corporate Accounting and Reporting Standard, Revised ed.; World Business Council for Sustainable Development: Geneva, Switzerland; World Resources Institute: Washington, DC, USA, 2022; Available online: https://ghgprotocol.org/sites/default/files/standards/ghg-protocol-revised.pdf (accessed on 15 December 2024).

- Greenhouse Gas Protocol. The Corporate Value Chain (Scope 3) Accounting and Reporting. Supplement to the GHG Protocol Corporate Accounting and Reporting Standard; World Resources Institute: Washington, DC, USA; World Business Council for Sustainable Development: Geneva, Switzerland, 2022; Available online: https://ghgprotocol.org/sites/default/files/standards/Corporate-Value-Chain-Accounting-Reporing-Standard_041613_2.pdf (accessed on 15 December 2024).

- European Environment Agency. Total Net Greenhouse Gas Emission Trends and Projections in Europe 2024. Available online: https://www.eea.europa.eu/en/analysis/indicators/total-greenhouse-gas-emission-trends (accessed on 15 December 2024).

- Kansal, R. Introduction to the Virtual Power Purchase Agreement; Rocky Mountain Institute (RMI): New York, NY, USA, 2019. [Google Scholar]

- ISO 14001:2015; Environmental Management Systems—Requirements with guidance for use. ISO: Geneva, Switzerland, 2015.

- ISO 50001:2018; Energy Management Systems—Requirements with guidance for use. ISO: Geneva, Switzerland, 2018.

{kind=link}

{kind=link}

| Definition of Scope of GHG Activities | GHG Inventory | Calculations | |

|---|---|---|---|

| Activity Data | Emission Factors | ||

| Scope 1: Diesel for machinery and company vehicles | Diesel consumption: 20,000 lt/year | Diesel: 2.68 kg CO2e/lt | 53,600 kg CO2e |

| Scope 2: Electricity for offices and workshops | Electricity consumption: 100,000 kWh/year (grid electricity) | EU grid average: 0.276 kg CO2e/kWh | 27,600 kg CO2e |

| Scope 3: Cement, steel, and timber purchased from suppliers | Cement purchased: 500 t/year | Cement: 0.83 kg CO2e/kg | 415,000 kg CO2e |

| Total: | 496,200 kg CO2e | ||

| Pathway 1 Electricity Decarbonization | Pathway 2 Direct Emissions | Pathway 3 Recycling | Pathway 4 |

|---|---|---|---|

| Supply Chain | |||

| Install 50 kW rooftop solar PVs (cost: ~EUR 50,000) | Replace 2 diesel vehicles with EVs (cost: ~EUR 80,000) | Recycle 20% of concrete waste (50 tons/year) | Switch to low-carbon cement (30% less emissions) |

| Annual generation: 50,000 kWh (50% of electricity needs) | Diesel saved: 5000 lt/year | Avoided cement use: 41,500 kg CO2e | Reduction: 124,500 kg CO2e |

| Reduction: 13,800 kg CO2e | Reduction: 13,400 kg CO2e |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Karakosta, C.; Papathanasiou, J. Decarbonizing the Construction Sector: Strategies and Pathways for Greenhouse Gas Emissions Reduction. Energies 2025, 18, 1285. https://doi.org/10.3390/en18051285

Karakosta C, Papathanasiou J. Decarbonizing the Construction Sector: Strategies and Pathways for Greenhouse Gas Emissions Reduction. Energies. 2025; 18(5):1285. https://doi.org/10.3390/en18051285

Chicago/Turabian StyleKarakosta, Charikleia, and Jason Papathanasiou. 2025. "Decarbonizing the Construction Sector: Strategies and Pathways for Greenhouse Gas Emissions Reduction" Energies 18, no. 5: 1285. https://doi.org/10.3390/en18051285

APA StyleKarakosta, C., & Papathanasiou, J. (2025). Decarbonizing the Construction Sector: Strategies and Pathways for Greenhouse Gas Emissions Reduction. Energies, 18(5), 1285. https://doi.org/10.3390/en18051285