Optimizing Cybersecurity Investments over Time

Abstract

:1. Introduction

2. Literature Review

3. Vulnerability, Investments, and Insurance

- full liability;

- limited liability (with upper limit)

- limited liability with deductibles (both lower and upper limit).

4. The Security Expense Minimization Problem

5. The Periodic Investment Solution

- the vulnerability is close to the maximum vulnerability V

- the maximum vulnerability V is large;

- the investment epochs are not too close to each other.

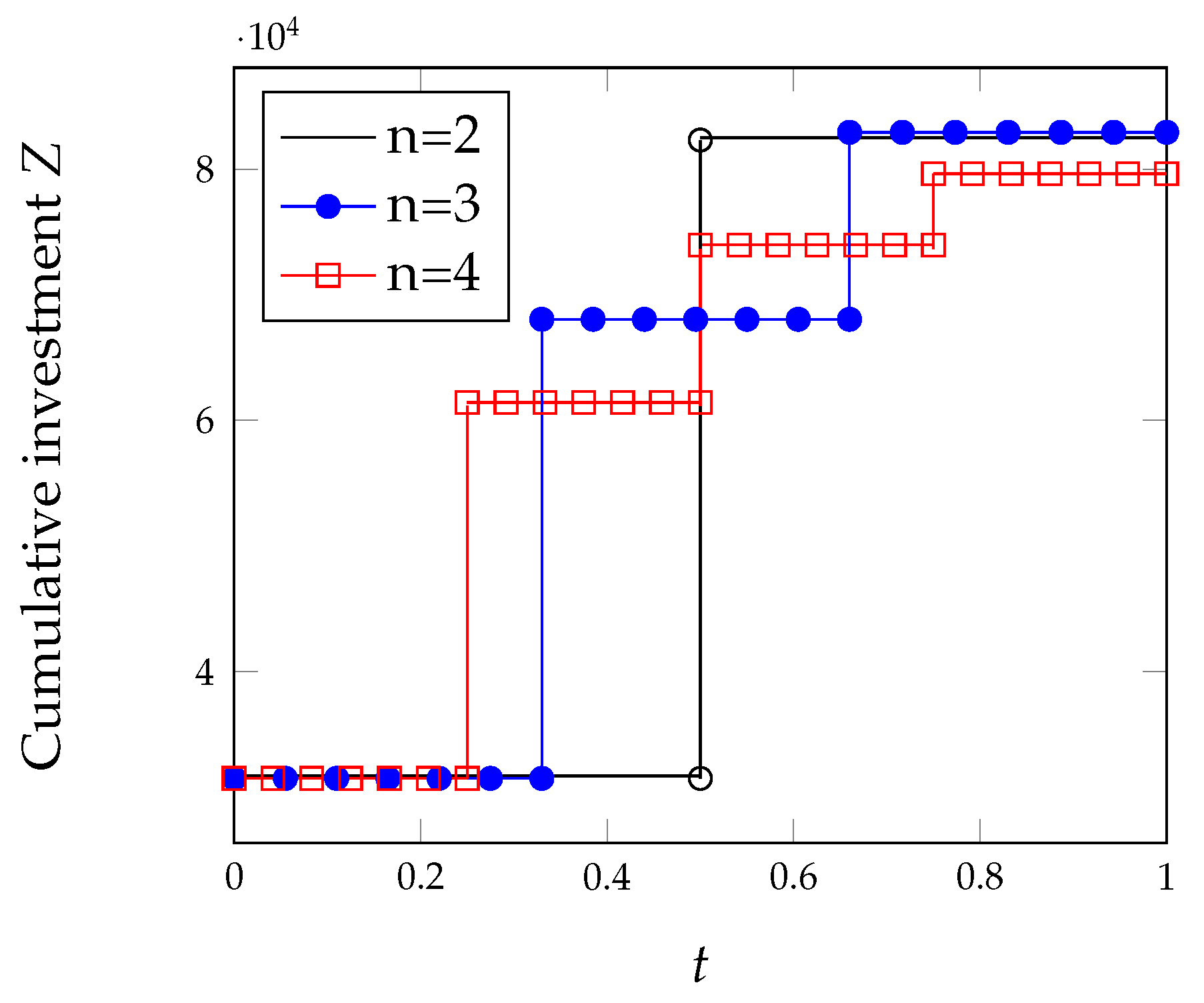

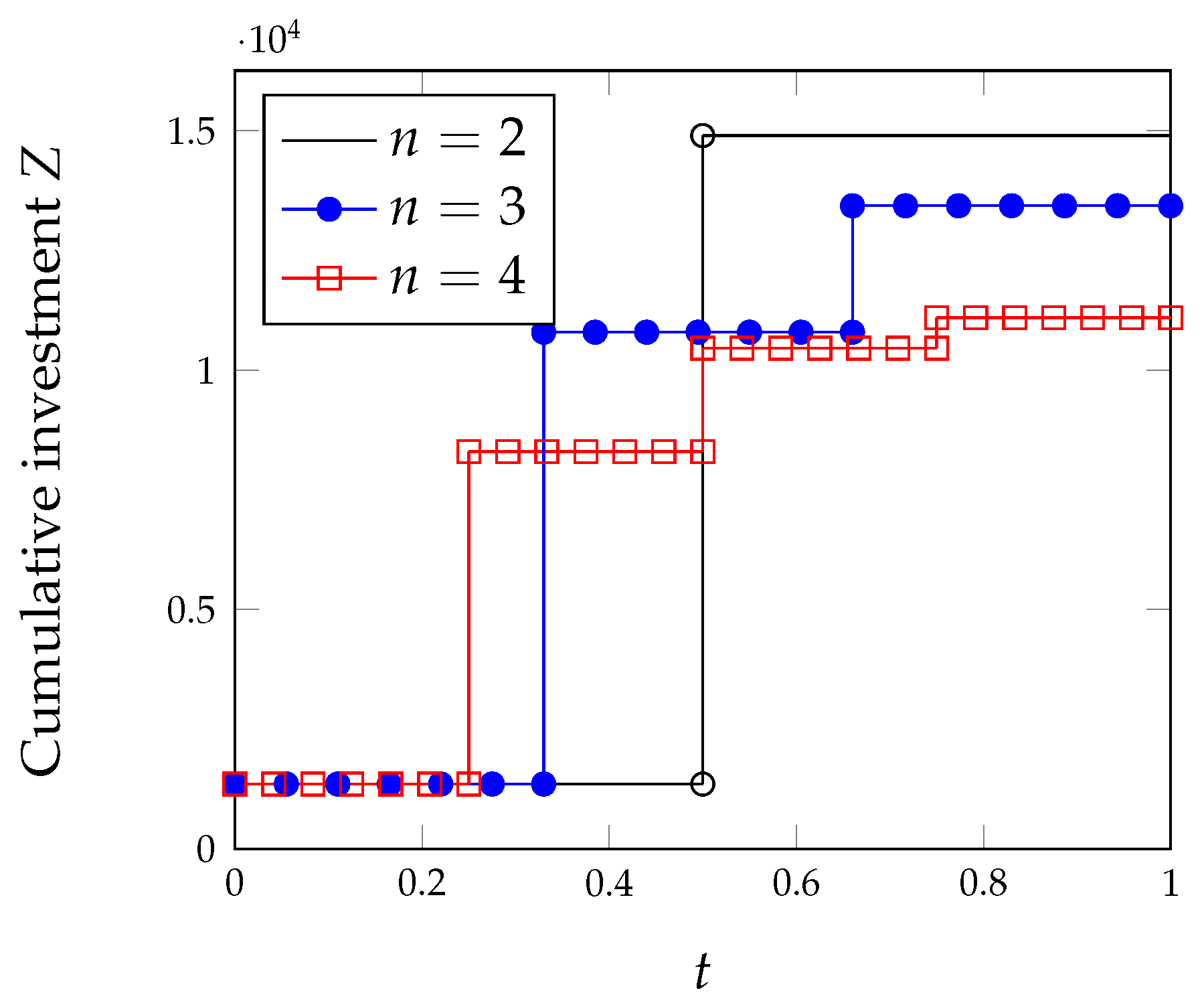

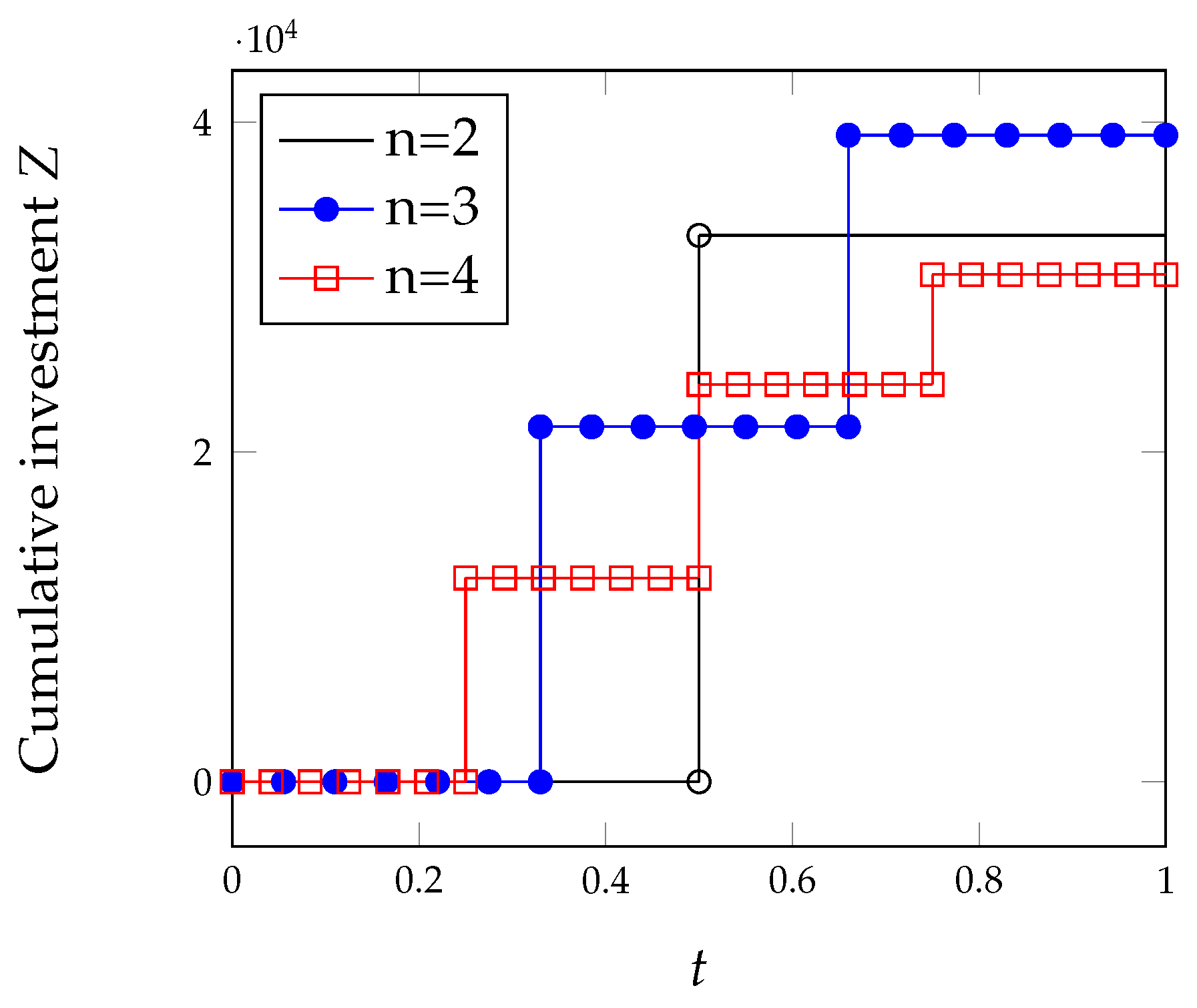

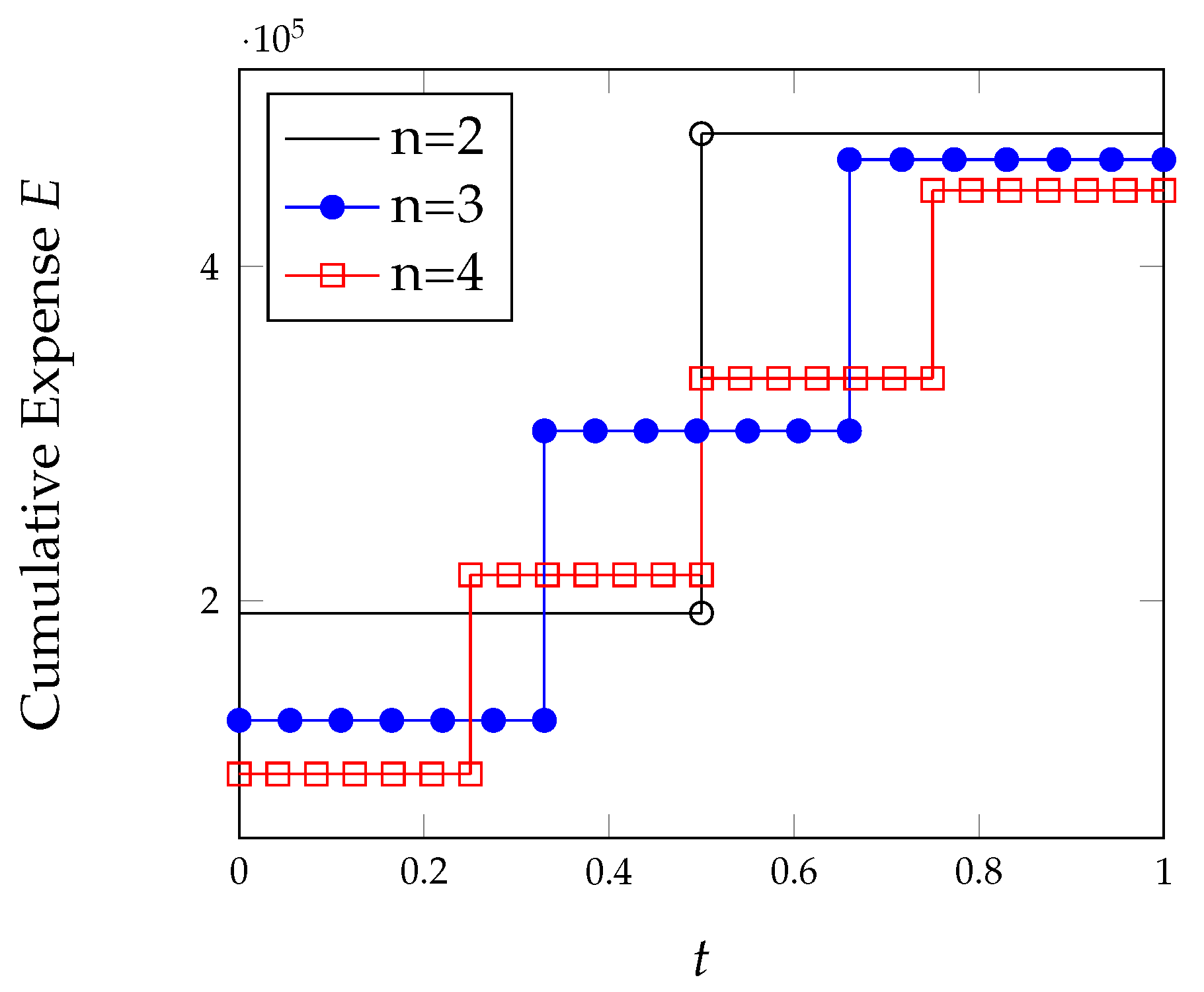

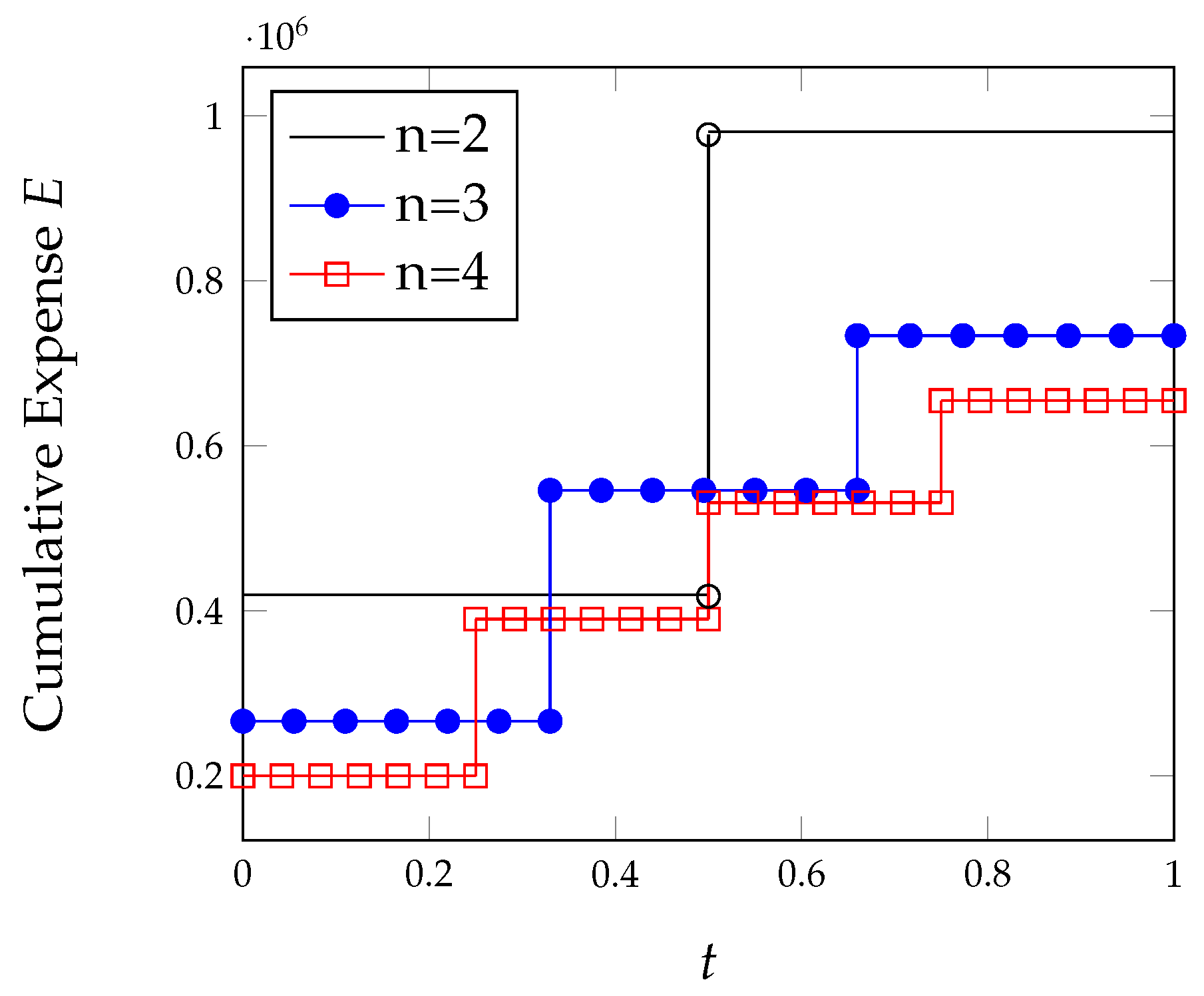

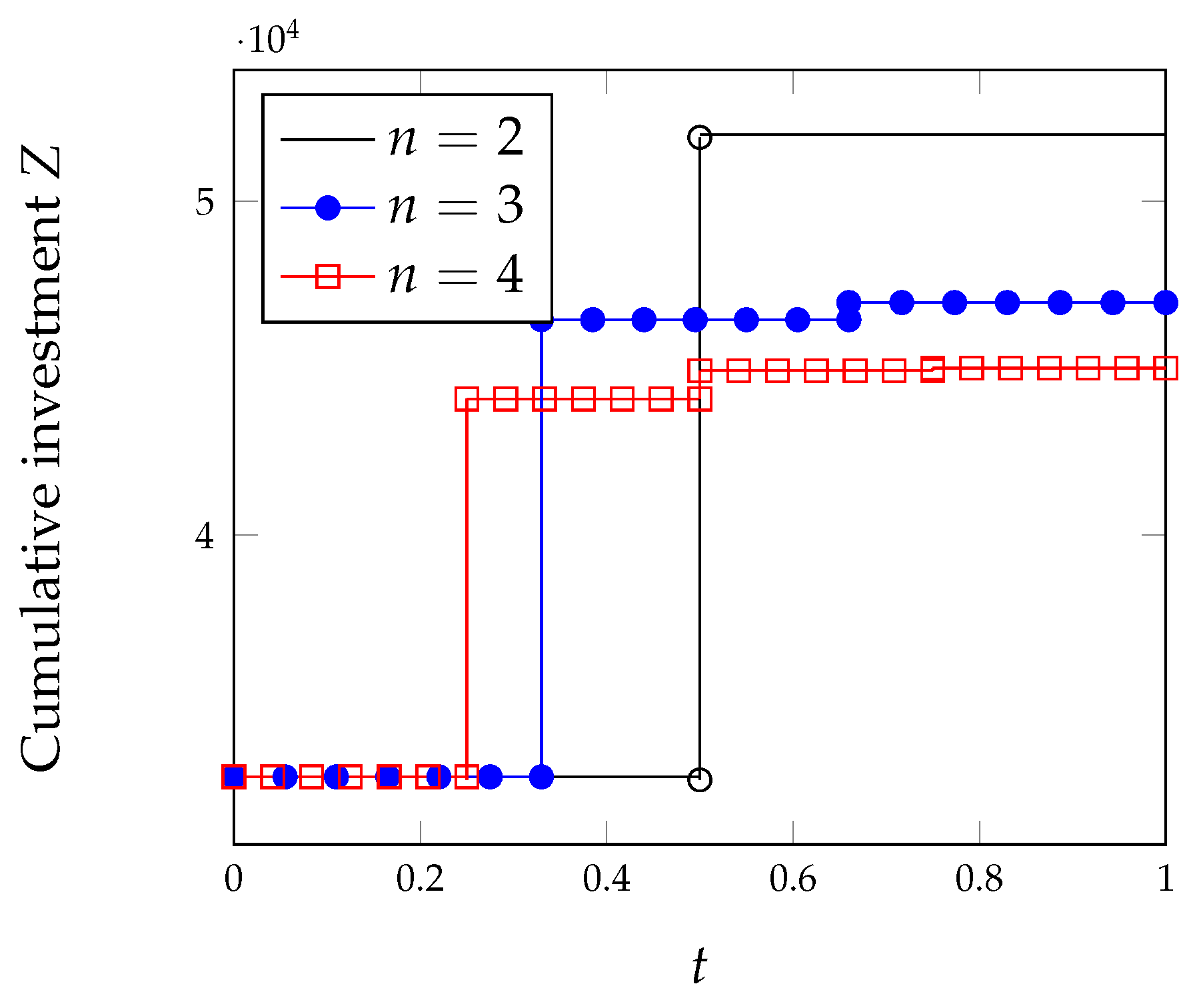

6. Example Application

7. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Maillart, T.; Sornette, D. Heavy-tailed distribution of cyber-risks. Eur. Phys. J. B 2010, 75, 357–364. [Google Scholar] [CrossRef]

- Wheatley, S.; Maillart, T.; Sornette, D. The extreme risk of personal data breaches and the erosion of privacy. Eur. Phys. J. B 2016, 89, 1–12. [Google Scholar] [CrossRef] [Green Version]

- Palsson, K.; Gudmundsson, S.; Shetty, S. Analysis of the impact of cyber events for cyber insurance. Geneva Pap. Risk Insur.-Issues Pract. 2020, 45, 564–579. [Google Scholar] [CrossRef]

- Scala, N.M.; Reilly, A.C.; Goethals, P.L.; Cukier, M. Risk and the Five Hard Problems of Cybersecurity. Risk Anal. 2019, 39, 2119–2126. [Google Scholar] [CrossRef] [PubMed]

- Paté-Cornell, M.E.; Kuypers, M.; Smith, M.; Keller, P. Cyber risk management for critical infrastructure: A risk analysis model and three case studies. Risk Anal. 2018, 38, 226–241. [Google Scholar] [CrossRef]

- Refsdal, A.; Solhaug, B.; Stølen, K. Cyber-risk management. In Cyber-Risk Management; Springer: Berlin/Heidelberg, Germany, 2015; pp. 33–47. [Google Scholar]

- Murphy, D.R.; Murphy, R.H. Teaching cybersecurity: Protecting the business environment. In Proceedings of the 2013 on InfoSecCD’13: Information Security Curriculum Development Conference, Kennesaw, GA, USA, 12 October 2013; pp. 88–93. [Google Scholar]

- Eling, M.; McShane, M.; Nguyen, T. Cyber risk management: History and future research directions. Risk Manag. Insur. Rev. 2021, 24, 93–125. [Google Scholar] [CrossRef]

- Biener, C.; Eling, M.; Wirfs, J.H. Insurability of cyber risk: An empirical analysis. Geneva Pap. Risk Insur.-Issues Pract. 2015, 40, 131–158. [Google Scholar] [CrossRef] [Green Version]

- Franke, U. The cyber insurance market in Sweden. Comput. Secur. 2017, 68, 130–144. [Google Scholar] [CrossRef]

- Xie, X.; Lee, C.; Eling, M. Cyber insurance offering and performance: An analysis of the US cyber insurance market. Geneva Pap. Risk Insur.-Issues Pract. 2020, 45, 690–736. [Google Scholar] [CrossRef]

- Bahşi, H.; Franke, U.; Friberg, E.L. The cyber-insurance market in Norway. Inf. Comput. Secur. 2019, 28, 54–67. [Google Scholar] [CrossRef]

- Strupczewski, G. Current state of the cyber insurance market. In Proceedings of the Economics and Finance Conferences, London, UK, 22–25 May 2018; International Institute of Social and Economic Sciences: London, UK, 2018; p. 6910062. [Google Scholar]

- Carfora, M.F.; Martinelli, F.; Mercaldo, F. Cyber risk management: An actuarial point of view. J. Oper. Risk 2019, 14, 4. [Google Scholar]

- Young, D.; Lopez, J.; Rice, M.; Ramsey, B.; McTasney, R. A framework for incorporating insurance in critical infrastructure cyber risk strategies. Int. J. Crit. Infrastruct. Prot. 2016, 14, 43–57. [Google Scholar] [CrossRef]

- Mazzoccoli, A.; Naldi, M. Robustness of Optimal Investment Decisions in Mixed Insurance/Investment Cyber Risk Management. Risk Anal. 2019, 40, 550–564. [Google Scholar] [CrossRef] [PubMed]

- Miaoui, Y.; Boudriga, N. Enterprise security economics: A self-defense versus cyber-insurance dilemma. Appl. Stoch. Model. Bus. Ind. 2019, 35, 448–478. [Google Scholar] [CrossRef]

- Kröger, W. Critical infrastructures at risk: A need for a new conceptual approach and extended analytical tools. Reliab. Eng. Syst. Saf. 2008, 93, 1781–1787. [Google Scholar] [CrossRef]

- Kure, H.I.; Islam, S. Assets focus risk management framework for critical infrastructure cybersecurity risk management. IET Cyber-Phys. Syst. Theory Appl. 2019, 4, 332–340. [Google Scholar] [CrossRef]

- Gordon, L.A.; Loeb, M.P. The economics of information security investment. ACM Trans. Inf. Syst. Secur. 2002, 5, 438–457. [Google Scholar] [CrossRef]

- Gordon, L.A.; Loeb, M.P.; Zhou, L. Investing in Cybersecurity: Insights from the Gordon-Loeb Model. J. Inf. Secur. 2016, 7, 49. [Google Scholar] [CrossRef] [Green Version]

- Naldi, M.; Flamini, M. Calibration of the Gordon-Loeb Models for the Probability of Security Breaches. In Proceedings of the 2017 UKSim-AMSS 19th International Conference on Computer Modelling & Simulation (UKSim), Cambridge, UK, 5–7 April 2017; IEEE: Piscataway, NJ, USA, 2017; pp. 135–140. [Google Scholar]

- Huang, C.D.; Behara, R.S. Economics of information security investment in the case of concurrent heterogeneous attacks with budget constraints. Int. J. Prod. Econ. 2013, 141, 255–268. [Google Scholar] [CrossRef]

- Naldi, M.; Flamini, M.; D’Acquisto, G. Negligence and sanctions in information security investments in a cloud environment. Electron. Mark. 2018, 28, 39–52. [Google Scholar] [CrossRef]

- Mayadunne, S.; Park, S. An economic model to evaluate information security investment of risk-taking small and medium enterprises. Int. J. Prod. Econ. 2016, 182, 519–530. [Google Scholar] [CrossRef]

- Hua, J.; Bapna, S. The economic impact of cyber terrorism. J. Strateg. Inf. Syst. 2013, 22, 175–186. [Google Scholar] [CrossRef]

- Gao, X.; Zhong, W.; Mei, S. Security investment and information sharing under an alternative security breach probability function. Inf. Syst. Front. 2015, 17, 423–438. [Google Scholar] [CrossRef]

- Gordon, L.A.; Loeb, M.P.; Lucyshyn, W.; Zhou, L. Increasing cybersecurity investments in private sector firms. J. Cybersecur. 2015, 1, 3–17. [Google Scholar] [CrossRef] [Green Version]

- Wu, Y.; Feng, G.; Wang, N.; Liang, H. Game of information security investment: Impact of attack types and network vulnerability. Expert Syst. Appl. 2015, 42, 6132–6146. [Google Scholar] [CrossRef]

- Krutilla, K.; Alexeev, A.; Jardine, E.; Good, D. The Benefits and Costs of Cybersecurity Risk Reduction: A Dynamic Extension of the Gordon and Loeb Model. Risk Anal. 2021, 41, 1795–1808. [Google Scholar] [CrossRef]

- Rosson, J.; Rice, M.; Lopez, J.; Fass, D. Incentivizing Cyber Security Investment in the Power Sector Using An Extended Cyber Insurance Framework. Homel. Secur. Aff. 2019, 15, 2. [Google Scholar]

- Sawik, T. A linear model for optimal cybersecurity investment in Industry 4.0 supply chains. Int. J. Prod. Res. 2022, 60, 1368–1385. [Google Scholar] [CrossRef]

- Mazzoccoli, A.; Naldi, M. Optimal Investment in Cyber-Security under Cyber Insurance for a Multi-Branch Firm. Risks 2021, 9, 24. [Google Scholar] [CrossRef]

- Hausken, K. Returns to information security investment: The effect of alternative information security breach functions on optimal investment and sensitivity to vulnerability. Inf. Syst. Front. 2006, 8, 338–349. [Google Scholar] [CrossRef]

- Wang, S. Optimal Level and Allocation of Cybersecurity Spending: Model and Formula. 2017. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3010029 (accessed on 15 May 2022).

- Wang, S.S. Integrated framework for information security investment and cyber insurance. Pac.-Basin Financ. J. 2019, 57, 101173. [Google Scholar] [CrossRef]

- Feng, S.; Xiong, Z.; Niyato, D.; Wang, P.; Wang, S.S.; Shen, X.S. Joint Pricing and Security Investment in Cloud Security Service Market with User Interdependency. IEEE Trans. Serv. Comput. 2020, 1–11. [Google Scholar] [CrossRef]

- Jerman-Blažič, B. An economic modelling approach to information security risk management. Int. J. Inf. Manag. 2008, 28, 413–422. [Google Scholar]

- Eling, M.; Wirfs, J. What are the actual costs of cyber risk events? Eur. J. Oper. Res. 2019, 272, 1109–1119. [Google Scholar] [CrossRef]

- Arcuri, M.C.; Brogi, M.; Gandolfi, G. How Does Cyber Crime Affect Firms? The Effect of Information Security Breaches on Stock Returns. In Proceedings of the ITASEC, Venice, Italy, 17–20 January 2017; pp. 175–193. [Google Scholar]

- Hovav, A.; D’Arcy, J. The impact of denial-of-service attack announcements on the market value of firms. Risk Manag. Insur. Rev. 2003, 6, 97–121. [Google Scholar] [CrossRef]

- World Economic Forum. Partnering for Cyber Resilience: Towards the Quantification of Cyber Threats; Technical Report; World Economic Forum: Cologny, Switzerland, 2015. [Google Scholar]

- Kamiya, S.; Kang, J.K.; Kim, J.; Milidonis, A.; Stulz, R.M. Risk management, firm reputation, and the impact of successful cyberattacks on target firms. J. Financ. Econ. 2021, 139, 719–749. [Google Scholar] [CrossRef]

- Poufinas, T.; Vordonis, N. Pricing the Cost of Cybercrime—A Financial Protection Approach. iBusiness 2018, 10, 128. [Google Scholar] [CrossRef] [Green Version]

- The Ponemon Institute. 2016 Cost of Data Breach Study: Global Analysis; Technical Report; The Ponemon Institute: Traverse City, MI, USA, 2016. [Google Scholar]

- Zhuo, Y.; Solak, S. Measuring and optimizing cybersecurity investments: A quantitative portfolio approach. In Proceedings of the IIE Annual Conference, Montreal, QC, Canada, 31 May–3 June 2014; p. 1620. [Google Scholar]

- Marotta, A.; Martinelli, F.; Nanni, S.; Orlando, A.; Yautsiukhin, A. Cyber-insurance survey. Comput. Sci. Rev. 2017, 24, 35–61. [Google Scholar] [CrossRef]

- Kesan, J.P.; Majuca, R.P.; Yurcik, W.J. The Economic Case for Cyberinsurance; Technical Report 2; University of Illinois College of Law: Champaign, IL, USA, 2004. [Google Scholar]

- Bolot, J.; Lelarge, M. Cyber insurance as an incentive for Internet security. In Managing Information Risk and the Economics of Security; Springer: Berlin/Heidelberg, Germany, 2009; pp. 269–290. [Google Scholar]

- Yang, Z.; Lui, J.C. Security adoption and influence of cyber-insurance markets in heterogeneous networks. Perform. Eval. 2014, 74, 1–17. [Google Scholar] [CrossRef]

- Pal, R.; Golubchik, L.; Psounis, K.; Hui, P. Will cyber-insurance improve network security? A market analysis. In Proceedings of the INFOCOM, 2014 Proceedings IEEE, Toronto, ON, Canada, 27 April–2 May 2014; IEEE: Piscataway, NJ, USA, 2014; pp. 235–243. [Google Scholar]

- Shetty, N.; Schwartz, G.; Felegyhazi, M.; Walrand, J. Competitive cyber-insurance and internet security. In Economics of Information Security and Privacy; Springer: Berlin/Heidelberg, Germany, 2010; pp. 229–247. [Google Scholar]

- Bandyopadhyay, T.; Mookerjee, V.S.; Rao, R.C. Why IT managers don’t go for cyber-insurance products. Commun. ACM 2009, 52, 68–73. [Google Scholar] [CrossRef] [Green Version]

- Vakilinia, I.; Sengupta, S. A coalitional cyber-insurance framework for a common platform. IEEE Trans. Inf. Forensics Secur. 2018, 14, 1526–1538. [Google Scholar] [CrossRef]

- Mukhopadhyay, A.; Chatterjee, S.; Bagchi, K.K.; Kirs, P.J.; Shukla, G.K. Cyber risk assessment and mitigation (CRAM) framework using logit and probit models for cyber insurance. Inf. Syst. Front. 2019, 21, 997–1018. [Google Scholar] [CrossRef]

- Mazzoccoli, A.; Naldi, M. The Expected Utility Insurance Premium Principle with Fourth-Order Statistics: Does It Make a Difference? Algorithms 2020, 13, 116. [Google Scholar] [CrossRef]

- Khalili, M.M.; Naghizadeh, P.; Liu, M. Designing cyber insurance policies: The role of pre-screening and security interdependence. IEEE Trans. Inf. Forensics Secur. 2018, 13, 2226–2239. [Google Scholar] [CrossRef]

- Mastroeni, L.; Mazzoccoli, A.; Naldi, M. Service Level Agreement Violations in Cloud Storage: Insurance and Compensation Sustainability. Future Internet 2019, 11, 142. [Google Scholar] [CrossRef] [Green Version]

- Herath, H.; Herath, T. Copula-based actuarial model for pricing cyber-insurance policies. Insur. Mark. Co. Anal. Actuar. Comput. 2011, 2, 7–20. [Google Scholar]

- Meland, P.H.; Tondel, I.A.; Solhaug, B. Mitigating risk with cyberinsurance. IEEE Secur. Priv. 2015, 13, 38–43. [Google Scholar] [CrossRef]

- Shetty, S.; McShane, M.; Zhang, L.; Kesan, J.P.; Kamhoua, C.A.; Kwiat, K.; Njilla, L.L. Reducing informational disadvantages to improve cyber risk management. Geneva Pap. Risk Insur.-Issues Pract. 2018, 43, 224–238. [Google Scholar] [CrossRef]

- Aven, T.; Ben-Haim, Y.; Boje Andersen, H.; Cox, T.; Droguett, E.L.; Greenberg, M.; Guikema, S.; Kröger, W.; Renn, O.; Thompson, K.M.; et al. Society for Risk Analysis Glossary; Society for Risk Analysis: Herndon, VA, USA, 2018. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | Value |

|---|---|

| 1.1 | |

| u | |

| ℓ | 5000 |

| 0.05 | |

| q | 0.9 |

| V | |

| r |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mazzoccoli, A.; Naldi, M. Optimizing Cybersecurity Investments over Time. Algorithms 2022, 15, 211. https://doi.org/10.3390/a15060211

Mazzoccoli A, Naldi M. Optimizing Cybersecurity Investments over Time. Algorithms. 2022; 15(6):211. https://doi.org/10.3390/a15060211

Chicago/Turabian StyleMazzoccoli, Alessandro, and Maurizio Naldi. 2022. "Optimizing Cybersecurity Investments over Time" Algorithms 15, no. 6: 211. https://doi.org/10.3390/a15060211

APA StyleMazzoccoli, A., & Naldi, M. (2022). Optimizing Cybersecurity Investments over Time. Algorithms, 15(6), 211. https://doi.org/10.3390/a15060211