3.1. Development Potential of Production and Method of Processing of Wood and Raw Wood

The identification of production areas and methods of raw wood processing proceeds from the information analysed in

Table 2, which demonstrates an increase in the logging volume and the consequent processing cascade at the lower level of inputs in the years before and during the disaster (a strategic referential period for the assessment of the impact of the disaster on the volume and structure of the raw material base).

Table 2 serves as an input for the justification of the argument stated herein that the issue of the use of forest production inputs by the processing industry in the context of sustainability is very important. Looking at the information with an outlook for the next three decades (Figure 3), it is clear from the decennial potential of the stock that the logging volume will decrease compared to the enormously high values during the years of disaster. This poses a significant problem for the woodworking industry and associated sectors due to a significant drop in revenues from economic activity. It is, therefore, justifiable to seek the best and most efficient opportunities for obtaining the highest added value from the given input capacities and thereby preserve the idea of sustainability in its three fundamental pillars: economic, social, and environmental. The trend of the basic inputs from the forest production shows a considerable increase in the logging residues by 24% (it must be borne in mind that it is the best estimate, which means that the percentage may not be exact). Logging residues in forests are mainly used for energy purposes, which is evidenced by the increase in the consumption of biomass for energy generation by 8.2% over the period under review. Apart from its economic benefits (being used in the energy sector), the use of above-ground biomass has some negative effects, too, such as significant losses of high nutritional content (nitrogen, phosphorus, and potassium). To prevent the negative effect of soil degradation, it is reasonable to use biologically worthless agricultural land for energy purposes. One of the potential environmentally friendly methods of forest waste (logging residue) utilisation seems to be the fertilisation with bore dust or wood ashes. In this case, however, the aim is rather to ensure greater height increments of woody plants in forestry, and it cannot be seen as improving the potential of utilisation of material flows into the CZ-NACE 16 sector. It still can bring economic and technological opportunities for utilisation of spare capacities with low investment risk. In circular economy, considerations are also given to so-called spiked fertiliser (with digestate) from waste biomass. Such fertiliser should sort out the problem with soil degradation in both agriculture and forestry. Technological lines for processing of logging waste may also represent an appropriate exit strategy for utilisation of the capacities as well as a competitive edge in the sector. By the recent adoption of the strategic vision (A Clean Planet for All) of the new approach to the climate-neutral economy by 2050 by the EU in 2018, the Member States are bound to decrease their carbon footprints to the level of a carbon-free economy. This objective presupposes a creation of approximately four million jobs and anticipates a significant development of the sector due to implementing the energy-climate objectives of the EU. Considering the implementation of the EU’s objectives and the progressive growth of the utilisation of raw wood for energy purposes, safeguarding the sustainability of the CZ-NACE 16 sector will highly depend on the adaptation of the technological possibilities for creating inputs for the energy industry. Being one of the priority elements of the model presented herein, the energy industry offers prospects for solving the problem with the increasing of the added value of low-quality wood, which the Czech timber market must currently settle, and which is rather difficult with the transformation process taking place in a problematic period. Sawdust processing appears to be an important production area, where the current market with pellets and briquettes (for utilisation in energy generation) faces a lack of production inputs. This situation is caused by the preferred deployment of the current capacities of sawmill businesses in the processing of more valuable construction and joinery lumber, whose price does not significantly decrease despite the crises. It opens opportunities for the construction of technological lines in the form of associated production of woodworking businesses in reaction to the need for increased efficiency of inputs/outputs and decreased costs of sawdust removal. Based on the analysis of secondary sources, the most promising seems to be the utilisation of wood for energy purposes in the form of sawdust processing for the trade with commodities such as pellets and briquettes, where the production input capacities are currently not covering the demand. The progress in production and biomass processing by the energy sector is also evident at the international level. Taking account of the utilisation of wood in the form of biomass for the energy sector, the utilisation rate is considerably lower in the Czech Republic than in more developed countries such as Germany, Finland or Denmark, where the biomass utilisation rate ranges between 7.5% and 13.1% compared to 2.7% in the Czech Republic. In this case, seeking an optimum proportion of the biomass utilisation in the energy sector is worth considering as the desirable proportion differs with the individual countries. This also gives scope for a synergy between the FSC and PEFC certification with plantation growing of fast-growing wood species, which might reduce the negative impacts of generation of impacts for biomass production inputs. The increasing trend of biomass production is illustrated by the statistics of the MAg [

25] on development in fast-growing wood species, whose production has increased 249.93 ha (2008) to 2862.22 ha (2017) over the last 10 years. A similarly major progress can be observed in the paper industry, where the energy production based on own sources (mainly biomass) has risen to almost 100% of the overall energy consumption and the industry in question can qualify as fully self-sustainable in energy production [

26]. The progressive growth rate is also evidenced by the statistics of utilisation of renewable energy sources at the national level as the consumption of solid biomass for energy production (fuelwood, chip wood, pulp leachate, nonagglomerated materials, pellets and briquets, and other biomass) increased by 31.3% (2010—3,216,947 t; 2019—4,683,045 t) between 2010 and 2019.

Another potential prospect at the level of intersector synergy introduced in the model is circular economy and bioeconomy. The selection of these fields is closely linked with the preparation of the strategic framework for the development of circular economy in the Czech Republic (“Circular Czech 2040”), the implementation of the Strategic Framework Czech Republic 2030 in sustainable development and Agenda 2030. Commencing the use of the Czech circular hotspot in 2019, the Czech Republic joined the states actively supporting the change in a transition from linear economic model to circular one. There have also been efforts in bioeconomy to decrease the dependency on fossil fuels and to diversify business lines and increase the number of product categories, which could bring many opportunities for the woodworking industry (e.g., production of innovative materials). Since the biomass supplies from forestry in the EU (for energy purposes) account for nearly 36% while secondary materials (recyclate) for production of products made of wood, pulpwood, and paper account for 47%, this area must be considered as important for future sustainable development of the sector.

Roundwood as a basic input source for further processing is another important area, with an increase in its volume by more than 45% between 2016 and 2019. The fundamental and key assortment for further processing of roundwood is the production of lumber from coniferous plants. Following further processing from assortments to semifinished to finished products, the lumber then enters other sectors, such as the furniture industry and the construction industry (construction elements, panels, and fine arts). Besides roundwood processing into lumber, the assortment also includes pulp and veneers, which also represent a significant part of the industry for which wood is the basic raw material for production. Regarding the mentioned industries, it is the construction sector which seems to be very promising as it has a big potential to increase the added value of the production outputs and, consequently, the economic stability of woodworking businesses in the period of limited sources for the processing industry. The most suitable appear to be environmentally friendly and renewable materials manufactured using specific technologies for constructions of multi-storey buildings and wooden houses, one of them being the high-strength cross-laminated timber technology (“CLT”). In Europe, this renewable environmentally friendly material is much demanded, and its production shows a growing trend. Other alternatives to standard materials (bricks, concrete) are laminated strand lumber (“LSL”), laminated veneer lumber (“LVL”), and ‘konstruktionsvollholz’—solid squared structural timber connected by finger-jointing in length (“KVH”). A problem with material outputs for the construction industry might be the strong dependence on foreign demand and a highly competitive environment since the market with such products quickly established itself and has been expanding ever since. Based on the information provided in the panorama of the manufacturing industry of the Czech Republic 2018, there has also been a quick development trend in the construction of wooden houses. The year-over-year increase in the segment accounted for 36%, which represents an increase in the construction by more than 1060 wooden houses compared to 2017. The argument for increasing the production capacities of CLT, KVH, LSL, and LVL can also be partially justified by the information provided in the reports of StoraEnso from July and August 2019, which mentioned an increase in the then capacities in more countries including the Czech Republic (an increase by 120,000 m

3 in Ždírec) and opening of a new plant with capacity of 100,000 m

3 in Sweden in reaction to the enormous global demand for CLT boards. According to Reportlinker [

27] (2019), a growth in demand for LSL and LVL boards can also be anticipated. The results provided in the report show that the market with laminated materials reached the value of USD 2.33 bilion in 2018. By 2024, the foreseen increase in sales should rise to USD 4.23 bilion. Although the biggest market share is in North America, an increase is also anticipated in Asia, Europe, Latin America, the Middle East, and Africa. The production of KVH structural timber is closely associated with decreasing thermal bridges and thermal protection of outer walls. The material is also suitable for construction of energy-saving and passive houses thanks to the increased stability and tightness of the cladding materials. The assumption of an increase in demands on construction of energy-efficient buildings is linked with the certifications Leadership in Energy and Environmental Design (“LEED”) and Building Research Establishment (“BREEAM”), which rank among the most respected certifications worldwide. At the national level, the SBToolCZ certification is being developed, which should represent an alternative for the Czech conditions.

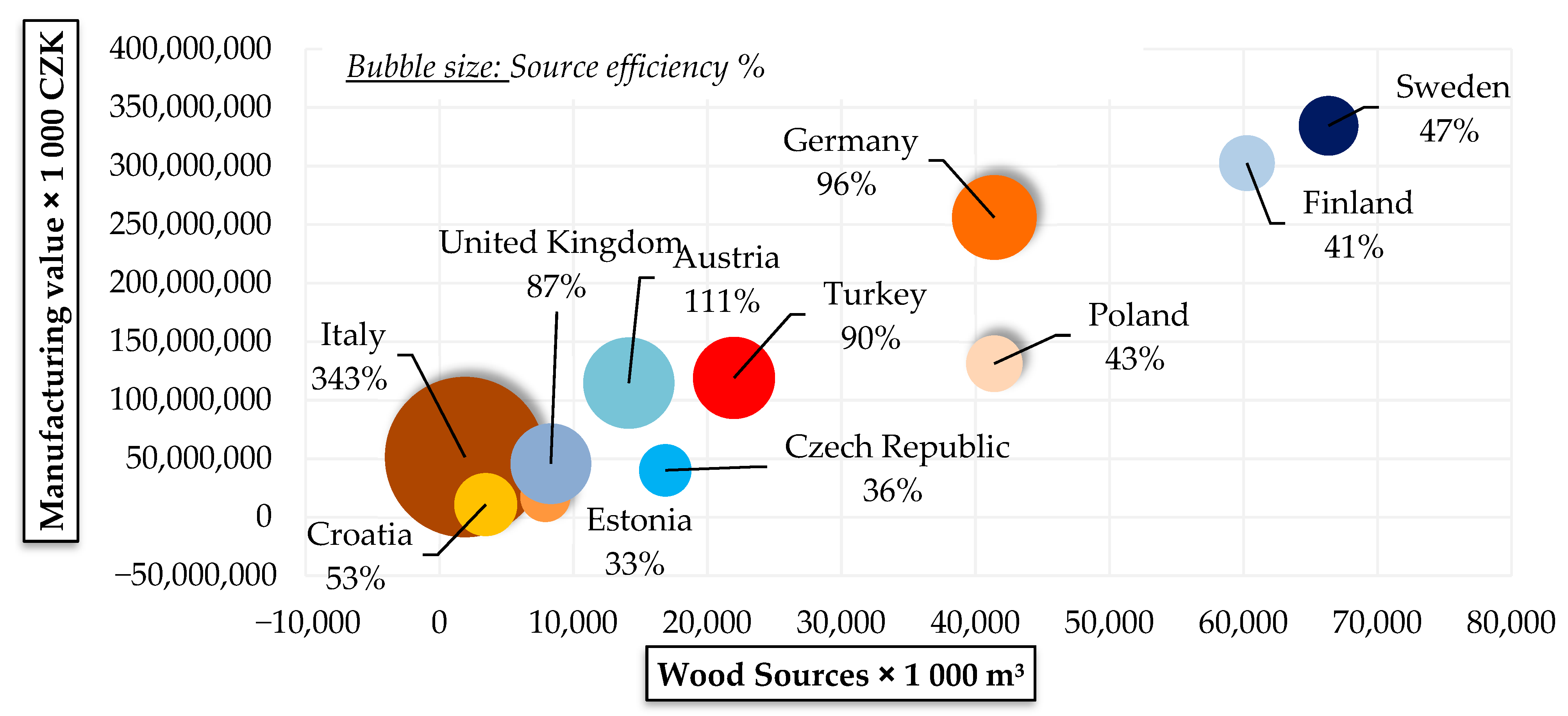

Concerning the increasing of the added value, which represents the linking element between the model’s perspectives, it is necessary to specify the aspects indicating the low level of the added value of production outputs of selected basic assortment in the woodworking industry. It affects the timber trade pricing strategy at both the national and international level, which is therefore vigorously negotiated. It is estimated that the current missing processing capacity exceeds about 17 mil

3. This capacity could be used to transform the salvage felling timber into outputs with higher added value (the estimate builds on the annual logging volume of 2019 and the information obtained from the results of the “Analysis of Impacts of Increased Volume of Timber Processed in the Czech Republic” from 2016 prepared by the Grant Service of Lesy České republiky (hereinafter referred to as the “GS LČR”). Currently, there is a big scope to address the issue of more efficient processing of wood as the Czech Republic ranks among the countries with the lowest efficiency with the efficiency rate at approximately 36% (see

Figure 1) and the capacity utilisation at about 60–64% (see

Table 3).

When assessing the wood-processing capacity potential within the above-mentioned project, the interpreted analysis was carried out as a comparative research project funded by the GS LČR. The report by the LČR limits the potential for further processing to sawmill operations and their assessment of the increase in the volume of processing with respect to their concurrent technological equipment. A report prepared by APICON builds on the maximum achievable operational value and the actual achieved capacity at present. A more detailed specification of the method and presentation of the results are included in the final report of the project [

28].

This problem has several variables which have to be taken into consideration. The increase in the processing capacity can be seen from the perspective of model situations. One of them is the utilisation of the current potential capacity with a lower level of investment and wood processing primarily intended for export. Another alternative calculates with a higher level of investment and construction of new capacities as a long-term strategic goal. However, the investment in the construction of the additional capacity may not have the support in securing long-term future supplies and sales since the current shortage of capacities is mainly caused by unplanned logging and climate change and represents an exceptional condition. Each of the presented scenarios has a specific benefit, ranging from profits and employment to added value and other social and economic characteristics. The third alternative is formatting a national strategy for the creation of capacities depending on the sector needs and thereto adapted conditions for state support. The third alternative includes a continuous process of updating needs as well as increased investment into the sector to ensure more operative changes, which the current disaster, or any future one, might require. An important reaction to the capacity gap is constructing a new sawmill in Štětí in 2019–2020. Regarding the level of investment, the volume of the funds invested accounting for approx. 40% of the sector’s total investments in 2019. Nevertheless, even this investment does not solve the future developments since the problem with insufficient capacity closely relates to long-term investments in the sector, which are irregular and rather low compared to the national level of investments related to the GDP (26.2%-2019) [

29]. The above information may be demonstrated by

Table 4, which shows the average year-over-year growth rate of investments in the sector in the reference period 2016–2019 at the level of 5.68%. The investment growth rate in

Table 4 has to be put into perspective with the above-mentioned investment in the sawmill in Štětí, which has not yet been translated into the whole allocated volume and a part of which will first be reflected in the balance sheet of the Ministry of Industry and Trade (“MIT”) for 2020. A long-term statistic of the year-over-year growth rate between 2010 and 2019 was at the level of 9.85%; however, the major influence of the years 2018 and 2019 has to be noted as there might be a connection with the above-mentioned investment of 2.9 milliards in the sawmill in Štětí.

The negative trend of the investment index mainly results in the stagnation of technological innovations, which influence the efficiency of wood utilisation (material efficiency) and the extent and potential of the associated production.

A potential supporting basis for increasing the investments in the sector at the level of national policy is the subsidies from the Rural Development Programme (“RDP”) and Support and Guarantee Agricultural and Forestry Fund (“SGAFF”), which provide partial financial support. The Ministry of Agriculture allocated funds in the amount of approximately CZK 300 million per year into the RDP and SGAFF. From the analysis of the data from the summary overview of support provided by the RDP to the woodworking sector, the drawing of funds of the woodworking sector amounted to only CZK 180,307,000, i.e., 0.20% share of the total allocation of funds in the RDP, including subsidies for forestry [

31]. The financial resources were mainly focused on technical equipment for woodworking businesses. From this data, it is obvious that the allocation of the drawings in the last 6 years (the summary is provided for years 2014–2020) does not reach the value of the potential annual drawing of the funds.

The proportion of the primary allocation “in thousand CZK” was adopted from the paper “Information about the Current State of Implementation of the Rural Development Programme 2014–2020” as of 31 March 2019 (material from the 9th meeting of the Monitoring Committee of the Rural Development Programme 2014–2020). According to the above document, the primary allocation is considered as CZK 9 milliard. This information demonstrates the very low interest in technological innovations, and it is essential to identify the cause of this disinterest as well as the reason why the growth of the sector is experiencing a downturn.

A major problem, partially linked with the poor technological background of woodworking businesses, is the lack of qualified staff for the transition of the sector to newer technologies as well as the decreasing interannual total number of employees. In the last 10 years, the average number of employees in the sector dropped from 37,016 (2010) to 28,303 (2019). The decrease is connected with several aspects, one of them being the shutdown of many small and medium-scale sawmills in the Czech Republic and downsizing of the manufacturing capacity in several running operations (estimated at approx. 0.5 million m

3 of felling capacity). Another reason is the reaching of the post-productive age by employees and their retirement, which is anticipated with up to 16 thousand employees in 2014–2025 [

32]. Another factor connected with the decrease is the low average wage in the sector at the level of CZK 25,350 (2019), which accounts for approx. 74% of the average salary in the Czech Republic of CZK 34,125 in 2019 and approx. 71% of the last record statistical value of average salary for 2020, which was CZK 35,402 (3Q/2020). A consequence of these facts is a low interest of potential employees in jobs in the sector and a problem with the potential saturation of expanded technological capacities of businesses. A way out of this situation is to increase the attractivity of the posts in the sector by motivating benefits and to put more emphasis on copying the curve of the average wage growth rate in the Czech Republic. In this, unions could play a crucial role in cooperation with the legislation of the state employment policy. The next problem is linked with the number of graduates from technical programmes focused on wood processing and their placeability in the labour market. This issue was addressed at the national level by authors [

33]. The study points out the fact that students’ interest in technical programmes is relatively constant (across all education levels), but the projections for 2000–2027 rank the Secondary sector 2c (timber, paper, and printing industry) among the fastest-decreasing groups as well as to the most decreasing groups in the sector with respect to the number of jobs and employment. Considering the ever-worsening situation with the lack of employees in the sector required for the transition to a higher level of automation and modern production, it is assumed that graduates seek employment in another sector because of more attractive salaries or do not have sufficient qualification for jobs in the wood processing sector.

Technological infrastructure, investment development, and the accompanying factors preventing the growth of the sector have a considerable effect on the added value, which belongs to the primary statistics addressed in this analysis. The added value pursued for the purposes of the data analysis herein was calculated in the following way: trading margin + sales − performance consumptions. The information presented herein points out the significantly low growth rate of the added value in the sector in the last 10 years, which is related to the actual realisation of the production outputs and, above all, their structure, which concentrates on outputs with low added value. The correlation of the data presented in

Table 5 can also be viewed in the context of the obsolete technological infrastructure of the businesses as some technological lines are several decades old (e.g., the technology in Javořice sawmill is 35 years old; the first large technological investment was in 2019). As shown in

Table 5, the growth of the added value was only more evident since 2018 and continued to stagnate in 2019; hence, it cannot be seen as a progressively growing indicator. This information is also illustrated by the average of year-over-year growth rate in 2010–2019, which was at the level of 4.05%. Between 2010 and 2012, the added value growth rate even reached negative values compared to the referential year.

The justification for increasing the added value can also be illustrated by

Figure 2, which shows the added value in correlation with the production outputs of the woodworking industry. This information must be viewed in the context of international demand for outputs with a higher added value.

However, an increase in the added value in the sector must be viewed in a broader context. The ongoing disaster is a factor of the enormous volume of timber, which ends up abroad in the form of basic assortment (roundwood, pulpwood) due to the current capacity and production potential of the woodworking sector and the export orientation of timber trade. This information is substantiated with the proportion of the domestic and foreign sales (the trade balance). As for the foreign trade figures, the export volume has increased 306% (2010–5 364,000 m3; 2019–16 439,000 m3) over the last 10 years, and the share of the exported wood in the overall logging in 2019 accounted for more than 50%. The problem, however, is not the export-oriented timber trade (since the problem with capacities of processors and the follow-up sectors for other outputs is a long-term shortage) but the fact that the realisation of the outputs is oriented towards basic assortment and the domestic market will face a shortage of this raw material in the future. Its potential realisation in the form of more valuable outputs will translate into the sales and investment potential from the capital of businesses on the intersector level. It can also be presumed that the deficit in employment will continue to deepen, and the number of small-scale processing entities will decrease (unless they transform to another production structure and technology in time) due to the lack of inputs for processing. The situation could be solved by a higher extent of utilisation of the current capacities and streamlining and restructuring the production mix in the sector, which could lead to further development and correction of export at the trade balance, or to achieving a realisation of the output with higher added value. Promising areas with significantly growing demand for outputs include the energy industry (pellets, briquettes), the construction industry (construction materials—KVH, LVL, LSL, and CLT), associated production, connections to other areas of the circular economy and bioeconomy, links to the foreseen megatrends in connection with climate challenges and industrial design application (new materials, manufacturing prototypes, etc.) The efficiency of the investment capital thereby increases too, which is reflected in the GNP and taxation and can even lead to a neutral balance of bound CO2 in the country. There is also scope for the state to seek new state incentives to support and develop the sector since it is a two-way flowing effect.

The issue of better realisation of production outputs and higher added value of the DSP has to be addressed without delay, also because it is becoming increasingly problematic to realise salvage felling timber on foreign markets. Unfortunately, these markets are increasingly saturated with domestic timber due to the ongoing bark beetle disaster, and an increase in timber import is unsubstantiated. A temporary solution to this situation is the Chinese market, where the timber export reached the value of 350,000 ton until May 2019 (supposing it concerns spruce timber, the weight of approx. 750 kg = 1 m3, i.e., about 467,000 m3 of timber, which would account for up to 1,000,000 m3 in 2019). The context for these figures can be found in the trade war between the USA and China, where the timber supply from the USA to China dropped by almost 40%; therefore, the current Chinese timber market is willing to accept a higher price and complicated logistics. This trade model, however, bears a high-risk factor in the form of timber cracking due to quick losses of water, mainly in spring and summer. Upon checks, the buyers from China claim it as nonconformities with the agreed requirements of the contract, and the supplier does not get paid. In such a case, a potential transport back to the Czech Republic is irrational for economic reasons. Therefore, export in the form of trade with China can be perceived as an acceptable operational solution to the current lack of export to markets with more favourable conditions of logistics and with lower risks, but this capacity of resources implies a greater margin of uncertainty for the future as for the source base.

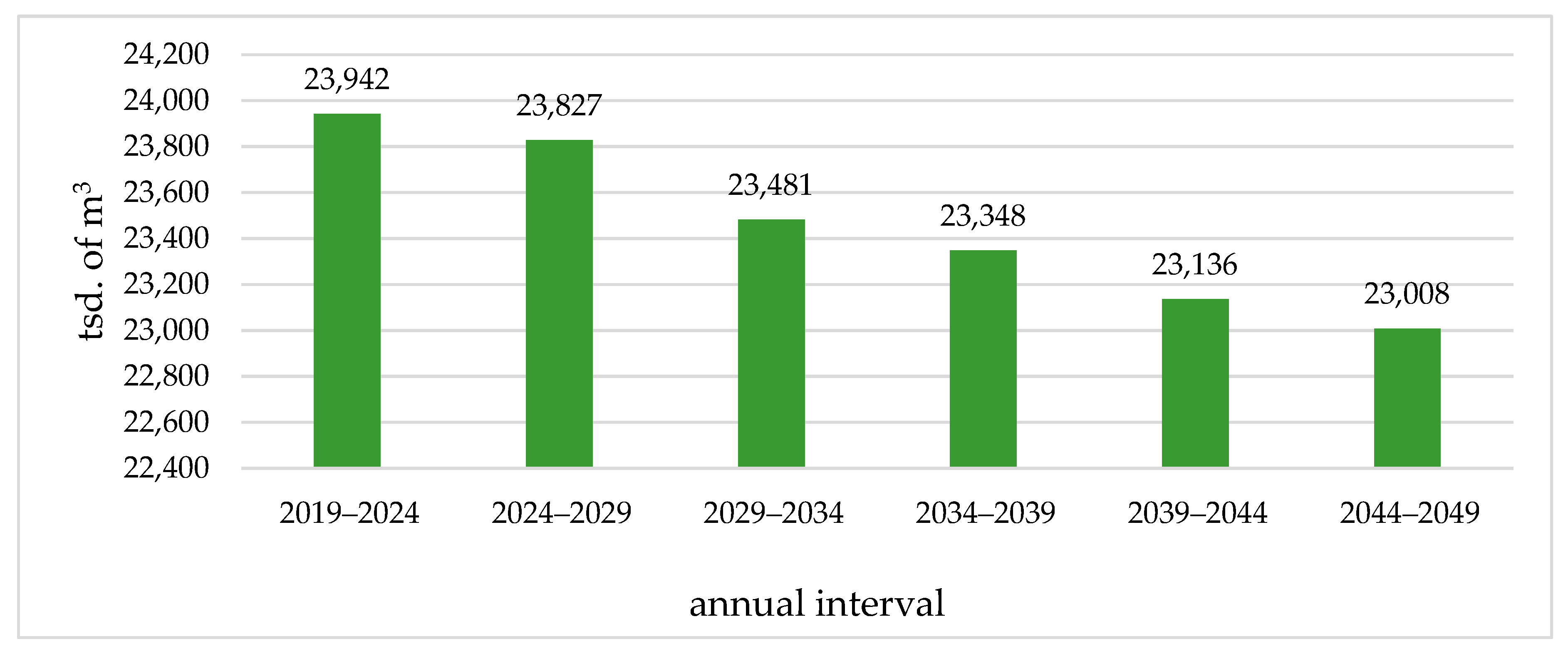

Considering the development of the disaster situation in 2016–2019, further conclusions of the analysis require defining the mentioned potential sources of basic assortment (fuelwood, roundwood, pulpwood) for the next 30 years. The outlook is based on the EFDM method and the data are adopted from the National Forest Inventory NIL2. A more exact specification of the calculation and data processing is provided in internal documents of the FMI, which provides the same data for noncommercial purposes at the national level for free. Based on the information in

Figure 3, it is possible to say that the volumetric capacity of logging decreases in 5-year intervals (the interval was chosen with respect to the validity of the forest management plan and the forecasting period following the disaster) with forest stands of spruce (SM), spruce-pine (SM-BO), and spruce-other (SM-other). This loss will be compensated by an increase in the logging potential in other stand types (oak, beech, spruce-beech, and pine). With spruce, the logging volume loss between 2019 and 2049 represents the sharpest drop by about 20% (2,121,000 m

3/year).

Figure 4 shows the logging potential outlook in 5-year intervals as sum values for all basic assortments (fuelwood, roundwood, pulpwood) and selected stand types. This estimate foresees a decrease in logging of forest types SM, SM-BO, and SM-other in the intervals of 2019–2024 and 2044–2049 at the level of approx. 34,970,000 m

3 (the conversion is based on the interinterval differences in logging with the factor of the 5-year interval).

This information indicates a future risk of SM shortage in all basic assortments for the woodworking industry as well as for the follow-up sectors, which utilise SM raw wood as a production input for further processing. At the same time, it is important to note that the outlook presumes a decrease in the proportion of SM in the overall logging volume from slightly more than 43% (2019–2024) to 35% (2044–2049). Taking account of the available data from 2019, the logging of SM amounted to 90.06% (29,350,347 m

3). These analytical data also confirm the need for alternative scenarios to increase the efficiency for the upcoming changes in the structure of the sector inputs as a condition for its development.

Table 6 presents three potential scenarios (S1, S2, S3) and the initial state (S0) of development in the assortment composition of inputs for the processing industry with various outputs from DSP production and sales, added value, number of employees, and production volume with respect to taxes and levies. Considering the extent and complexity of the project from which the given information follow, the detailed description of the method as well as the summary data for the individual scenarios are provided in the final report on the NAZV projects [

34].

The information provided in

Table 6 allows for several conclusions which indicate the effect of the potential scenarios on the wood processing within the sector with a changed input structure. The S0 scenario represents the current state of the processing industry and hence the original state. It is the situation based on the found facts and data. The S1 scenario employs a version with increased processing capacity (maximisation of production) of basic assortment and reviews the impacts leading to increased employment. The economic efficiency of this model scenario has a major impact namely on the tax load of this structural change and the social levies associated with the higher number of employees. The S2 scenario works with a version of the highest added value per 1 m

3 thanks to the increased capacity of processing volume for products with higher added value (following

Figure 3). This structural change leads to a greater extent of input utilisation (increased efficiency) while maintaining a significant number of employees from the S1 scenario. The S3 scenario has a version with increased production volume and sales from sawmill production and pulpwood, a decrease in production volume of agglomerated boards (a change in the processing structure), and a rather constant number of employees preserved from the original model (S0). This version should also lead to a decrease in the deficit of raw material volume.

The last area, which is often put in contradiction with the three fundamental pillars of sustainability and whose effect on economic results of woodworking (and forest) business is perceived as rather controversial, is timber certification. Two certification systems, PEFC and FSC, are used at the national level in the Czech Republic. The results presented further in this section originate from the two IGA project implemented in 2016–2019. The objective of the presented results is to demonstrate the problems of the certification systems, which could lead to a better interconnection of the preference areas in increasing the efficiency of the sector. To assess the effect of certification on the economic efficiency of businesses, the data primarily linked to economic effects of the use of certification were selected from the survey (a description of the project is provided in the methodology description herein).

Table 7 provides answers to the question “How many years have you been employing the PEFC or FSC certification in your company?” assessed in contingency with the percentage increase (growth) of the individual economic indicators such as sales, profit, added value, and ROE. The input data for

Table 7 were exclusively the questionnaire sheets from businesses which employ certification.

The results provided in

Table 7 suggest that there is a statistical dependency between all the pursued economic indicators and the length of employment of the certification systems in the companies, which follows from the individual statistical probability indicators. They show that the probability of incidental occurrence of such abundance is lower than 1% of the profit, sales, and added value, which is less than the usual criterion for evaluation of hypotheses (5%). The percentage is higher in the case of ROE, but still within the range of a standard statistical deviation. The dependency was tested using three statistical analyses, namely

p-value, Chi-square test, and Cramer’s_V test. It should be mentioned that a purely positive impact of the FSC and PEFC certification of the economic indicators cannot be claimed on the basis of the study as the proportion of positive and negative economic effects with all respondents accounting for 59.8%/40.2%. The statistical significance provided in

Table 7 only accounts for a significant dependency of long-term employment of certification systems on selected economic indicators of an undertaking. Another area under consideration was the survey on consumers’ attitudes to products made of certified wood. The aim was to gain an overview of the level of recognition of certified products allowing for a creation of a concept to raise interest in such products. The results, which are provided in

Table 8, only represent a part of the obtained data, which had already been published by the authors of this article.

The results shown in

Table 8 indicate that 57.8% (233 respondents) of the total of 404 respondents said that they recognised the FSC and PEFC logo, and 34.8% (81 respondents of the total of 233) managed to confirm the previous sensory recognition in the control question. This sample of respondents would stand for slightly more than 20% of the total, which would mean that only every fifth respondent in the Czech Republic associates the FSC and PEFC logo/label in timber products with landscape and nature protection. Another paradox is the fact that many respondents also considered names of companies, public institutions, civic associations, or the World Wide Fund for Nature to be environmental labels. For example, the respondents’ answers included the following: WWF, Ekofol, IKEA, Swedwood, Fair trade, Holz 100, Real Wood, Trepp-art, Tectona, Wild Nature Friendly, FSC MIX, and Lesy ČR. A poor involvement is also perceptible in promotion as only less than 6% of the respondents identified the logo based on advertising in media (Internet, TV, radio). Another almost 6% of the respondents recognised the logo based on advertising materials (advertising spaces, advertising in shops, shopping malls such as OBI, BAUHAUS, and IKEA, and at trade fairs and exhibitions). Slightly more than 10% accounted for advertising at schools within the scope of classes, lectures, or conferences. Indirect advertising in the form of logos on vehicles, buildings, and documents of forestry and woodworking companies accounted for nearly 9%. The last pursued area was a direct promotion of the logo on paper and timber products, and there the products showed the biggest percentage of successful identification, namely almost 27%.

The above results confirm the nonconceptual nature and inconsistency in opinions in the perception of the certification by both professionals and broader public. The current setting does not work well with respect to either marketing or raising interest in the issue of sustainability of the timber trade. With the rising pressure exerted by large companies on supplier and subsupplier chains, the tools that demonstrate the sustainability interests can be said to have a certain level of lobbying influence of such. Since the certified forest area in the Czech Republic accounts for about 65% of the total forest area (2.9 mil. ha), it represents an important timber trade instrument across sectors and its influence needs to be diversified to the desirable level.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}