Truffle Market Evolution: An Application of the Delphi Method

,

,  ,

,

Abstract

:1. Introduction

2. Materials and Methods

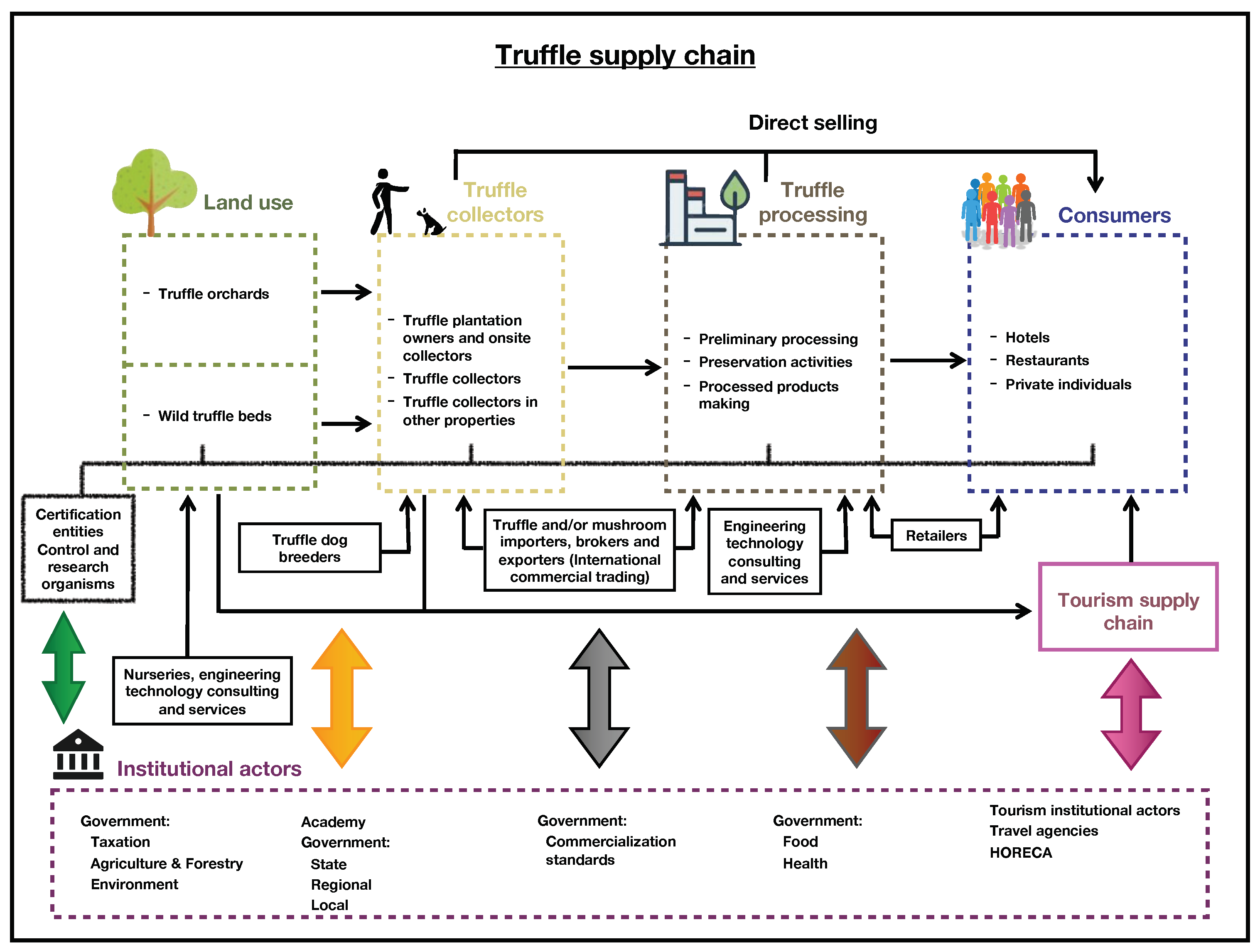

3. Results

3.1. Description of the Supply Chain

3.2. SWOT Analysis of the Truffle Sector

3.3. Challenges of the Truffle Sector

3.4. Actions to Develop the Truffle Sector and Guarantee Its Resilience

4. Discussion

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Boa, E. Wild Edible Fungi: A Global Overview of Their Use and Importance to People; Non-Wood Forest Products, No. 17; Food and Agriculture Organization of the United Nations: Rome, Italy, 2004; ISBN 92-5-105157-7. [Google Scholar]

- Peintner, U.; Schwarz, S.; Mešić, A.; Moreau, P.-A.; Moreno, G.; Saviuc, P. Mycophilic or Mycophobic? Legislation and Guidelines on Wild Mushroom Commerce Reveal Different Consumption Behaviour in European Countries. PLoS ONE 2013, 8, e63926. [Google Scholar]

- Guerin-Laguette, A. Successes and challenges in the sustainable cultivation of edible mycorrhizal fungi—Furthering the dream. Mycoscience 2021, 62, 10–28. [Google Scholar] [CrossRef]

- Brundret, M.; Bougher, N.; Dell, B.; Grove, T.; Malajczuk, N. Working with Mycorrhizas in Forestry and Agriculture; ACIAR Monograph 32; ACIAR: Canberra, Australia, 1996; ISBN 1863201815. [Google Scholar]

- Bonito, G.M.; Gryganskyi, A.P.; Trappe, J.M.; Vilgalys, R. A global meta-analysis of Tuber ITS rDNA sequences: Species diversity, host associations and long-distance dispersal. Mol. Ecol. 2010, 19, 4994–5008. [Google Scholar]

- Reyna, S.; Garcia-Barreda, S. Black truffle cultivation: A global reality. For. Syst. 2014, 23, 317–328. [Google Scholar] [CrossRef]

- Benucci, G.M.N.; Gógán Csorbai, A.; Baciarelli-Falini, L.; Marozzi, G.; Suriano, E.; Sitta, N.; Donnini, D. Taxonomy, Biology and Ecology of Tuber macrosporum Vittad. and Tuber mesentericum Vittad. In True Truffle (Tuber spp.) in the World: Soil Ecology, Systematics and Biochemistry; Zambonelli, A., Iotti, M., Murat, C., Eds.; Springer International: Cham, Switzerland, 2016; pp. 69–86. ISBN 978-3-319-31434-1. [Google Scholar]

- Bach, C.; Beacco, P.; Cammaletti, P.; Babel-Chen, Z.; Levesque, E.; Todesco, F.; Cotton, C.; Robin, B.; Murat, C. First production of Italian white truffle (Tuber magnatum Pico) ascocarps in an orchard outside its natural range distribution in France. Mycorrhiza 2021, 31, 383–388. [Google Scholar] [CrossRef]

- Liu, B.; Fischer, C.; Bonet, J.A.; Olivera, A.; Inchusta, A.; Colinas, C. Pattern of Tuber melanosporum extramatrical mycelium expansion over a 20-year chronosequence in Quercus ilex-truffle orchards. Mycorrhiza 2014, 24 (Suppl. S1), S47–S54. [Google Scholar] [CrossRef]

- Merényi, Z.; Varga, T.; Bratek, Z. Tuber brumale: A Controversial Tuber Species. In True Truffle (Tuber spp.) in the World: Soil Ecology, Systematics and Biochemistry; Zambonelli, A., Iotti, M., Murat, C., Eds.; Springer International: Cham, Switzerland, 2016; pp. 49–68. ISBN 978-3-319-31434-1. [Google Scholar]

- Zambonelli, A.; Iotti, M.; Hall, I. Current status of truffle cultivation: Recent results and future perspectives. Micol. Ital. 2015, 44, 31–40. [Google Scholar]

- Šiškovič, N.; Strojnik, L.; Grebenc, T.; Vidrih, R.; Ogrinc, N. Differentiation between species and regional origin of fresh and freeze-dried truffles according to their volatile profiles. Food Control 2021, 123, 107698. [Google Scholar] [CrossRef]

- Riccioni, C.; Rubini, A.; Belfiori, B.; Gregori, G.; Paolocci, F. Tuber magnatum: The special one. What makes it so different from the other Tuber spp.? In True Truffle (Tuber spp.) in the World: Soil Ecology, Systematics and Biochemistry; Zambonelli, A., Iotti, M., Murat, C., Eds.; Springer International: Cham, Switzerland, 2016; pp. 87–103. ISBN 978-3-319-31434-1. [Google Scholar]

- Oliach, D.; Morte, A.; Sánchez, S.; Navarro-Ródenas, A.; Marco, P.; Gutiérrez, A.; Martín-Santafé, M.; Fischer, C.; Albisu, L.M.; García-Barreda, S.; et al. Las trufas y las turmas. In Los Productos Forestales No Madereros en España: Del Monte a la Industria; Sánchez-González, M., Calama, R., Bonet, J.A., Eds.; INIA, Ministerio de Ciencia e Innovación; Gobierno de España: Madrid, Spain, 2020; pp. 283–324. ISBN 978-84-7498-585-6. [Google Scholar]

- Molinier, V.; Peter, M.; Stobbe, U.; Egli, S. The Burgundy truffle (Tuber aestivum syn. uncinatum): A truffle species with a wide habitat range over Europe. In True Truffle (Tuber spp.) in the World: Soil Ecology, Systematics and Biochemistry; Zambonelli, A., Iotti, M., Murat, C., Eds.; Springer International: Cham, Switzerland, 2016; pp. 33–47. ISBN 978-3-319-31434-1. [Google Scholar]

- Lancellotti, E.; Iotti, M.; Zambonelli, A.; Franceschini, A. The Puberulum Group Sensu Lato (Whitish Truffles). In True Truffle (Tuber spp.) in the World: Soil Ecology, Systematics and Biochemistry; Zambonelli, A., Iotti, M., Murat, C., Eds.; Springer International: Cham, Switzerland, 2016; pp. 105–124. [Google Scholar]

- De Roman, M.; Boa, E. Collection, marketing and cultivation of edible fungi in Spain. Micol. Apl. Int. 2004, 16, 25–33. [Google Scholar]

- Büntgen, U.; Latorre, J.; Egli, S.; Martínez-Peña, F. Socio-economic, scientific, and political benefits of mycotourism. Ecosphere 2017, 8, e01870. [Google Scholar] [CrossRef]

- Murat, C. Forty years of inoculating seedlings with truffle fungi: Past and future perspectives. Mycorrhiza 2014, 25, 77–81. [Google Scholar] [CrossRef]

- Le Tacon, F.; Marçais, B.; Courvoisier, M.; Murat, C.; Montpied, P.; Becker, M. Climatic variations explain annual fluctuations in French Périgord black truffle wholesale markets but do not explain the decrease in black truffle production over the last 48 years. Mycorrhiza 2014, 24, S115–S125. [Google Scholar] [CrossRef] [PubMed]

- Büntgen, U.; Egli, S.; Camarero, J.J.; Fischer, E.M.; Stobbe, U.; Kauserud, H.; Tegel, W.; Sproll, L.; Stenseth, N.C. Drought-induced decline in Mediterranean truffle harvest. Nat. Clim. Chang. 2012, 2, 827–829. [Google Scholar] [CrossRef]

- Thomas, P.; Büntgen, U. A risk assessment of Europe’s black truffle sector under predicted climate change. Sci. Total Environ. 2019, 655, 27–34. [Google Scholar] [CrossRef] [PubMed]

- Federación Española de Asociaciones de Truficultores (FETT); Sarrión, Spain. Personal communication, 2021.

- Čejka, T.; Trnka, M.; Krusic, P.J.; Stobbe, U.; Oliach, D.; Václavík, T.; Tegel, W.; Büntgen, U. Predicted climate change will increase the truffle cultivation potential in central Europe. Sci. Rep. 2020, 10, 21281. [Google Scholar] [CrossRef] [PubMed]

- Ramírez, R.; (Agritufas SpA, Talca, Chile). Personal communication, 2021.

- Čejka, T.; Isaac, E.; Oliach, D.; Martínez-Peña, F.; Egli, S.; Thomas, P.; Trnka, M.; Büntgen, U. Risk and reward of the emerging truffle sector under predicted global climate change. Environ. Res. Lett. 2021. submitted for publication. [Google Scholar]

- Oliach, D.; Colinas, C.; Castaño, C.; Fischer, C.R.; Bolaño, F.; Bonet, J.A.; Oliva, J. The influence of forest surroundings on the soil fungal community of black truffle (Tuber melanosporum) plantations. For. Ecol. Manag. 2020, 469, 118199. [Google Scholar] [CrossRef]

- Masiero, M.; Pettenella, D.; Secco, L. From failure to value: Economic valuation for a selected set of products and services from Mediterranean forests. For. Syst. 2016, 25, e051. [Google Scholar] [CrossRef] [Green Version]

- Lovrić, M.; Da Re, R.; Vidale, E.; Prokofieva, I.; Wong, J.; Pettenella, D.; Verkerk, P.J.; Mavsar, R. Non-wood forest products in Europe—A quantitative overview. For. Policy Econ. 2020, 116, 102175. [Google Scholar] [CrossRef]

- Lovrić, M.; Da Re, R.; Vidale, E.; Pettenella, D.; Mavsar, R. Social network analysis as a tool for the analysis of international trade of wood and non-wood forest products. For. Policy Econ. 2018, 86, 45–66. [Google Scholar] [CrossRef]

- Samils, N.; Olivera, A.; Danell, E.; Alexander, S.J.; Fischer, C.; Colinas, C. The Socioeconomic Impact of Truffle Cultivation in Rural Spain. Econ. Bot. 2008, 62, 331–340. [Google Scholar] [CrossRef]

- Büntgen, U.; Egli, S. Breaking new ground at the interface of dendroecology and mycology. Trends Plant Sci. 2014, 19, 613–614. [Google Scholar] [CrossRef]

- Rowe, G.; Wright, G. Expert opinions in forecasting: The role of the Delphi technique. In Principles of Forecasting: A Handbook for Researchers and Practitioners; Armstrong, J.S., Ed.; Kluwer Academic Publishers: Boston, MA, USA, 2001; pp. 125–144. [Google Scholar]

- Green, K.C.; Armstrong, J.C.; Graefe, A. Methods to Elicit Forecasts from Groups: Delphi and Prediction Markets Compared. Int. J. Appl. Forecast. 2007, 8, 17–20. [Google Scholar]

- Truffle Prices. Available online: http://www.observatoriforestal.cat/preus-de-la-tofona/ (accessed on 7 June 2021).

- Bonet, J.A.; Oliach, D.; Fischer, C.; Olivera, A.; de Aragon, J.M.; Colinas, C. Cultivation Methods of the Black Truffle, the Most Profitable Mediterranean Non-Wood Forest Product; A State of the Art Review. In Proceedings of the Modelling, Valuing and Managing Mediterranean Forest Ecosystems for Non-Timber Goods and Services, Palencia, Spain, 26–27 October 2007; Palahí, M., Birot, Y., Bravo, F., Gorriz, E., Eds.; European Forest Institute Proceedings No. 57. European Forest Institute: Joensuu, Finland, 2009; pp. 57–71. [Google Scholar]

- Bonet, J.A.; Colinas, C. Cultivo de Tuber melanosporum Vitt. Condiciones y rentabilidad. Forestalia 2001, 5, 38–45. [Google Scholar]

- Fischer, C.; Oliach, D.; Bonet, J.A.; Colinas, C. Best Practices for Cultivation of Truffles; Forest Sciences Centre of Catalonia (CTFC): Solsona, Spain; Yaşama Dair Vakıf: Antalaya, Turkey, 2017; ISBN 978-84-697-8163-0. [Google Scholar]

- Andrés-Alpuente, A.; Sánchez, S.; Martín, M.; Aguirre, A.J.; Barriuso, J.J. Comparative analysis of different methods for evaluating quality of Quercus ilex seedlings inoculated with Tuber melanosporum. Mycorrhiza 2014, 24 (Suppl. S1), S29–S37. [Google Scholar] [CrossRef] [PubMed]

- Murat, C.; Bonneau, L.; De la Varga, H.; Olivier, J.-M.; Sandrine, F.; Tacon, F. Trapping truffle production in holes: A promising technique for improving production and unravelling truffle life cycle. Ital. J. Mycol. 2016, 45, 47–53. [Google Scholar]

- Garcia-Barreda, S.; Marco, P.; Martín-Santafé, M.; Tejedor-Calvo, E.; Sánchez, S. Edaphic and temporal patterns of Tuber melanosporum fruitbody traits and effect of localised peat-based amendment. Sci. Rep. 2020, 10, 4422. [Google Scholar] [CrossRef]

- Olivera, A.; Bonet, J.A.; Palacio, L.; Liu, B.; Colinas, C. Weed control modifies Tuber melanosporum mycelial expansion in young oak plantations. Ann. For. Sci. 2014, 71, 495–504. [Google Scholar] [CrossRef]

- Piñuela, Y.; Alday, J.G.; Oliach, D.; Castaño, C.; Bolaño, F.; Colinas, C.; Bonet, J.A. White mulch and irrigation increase black truffle soil mycelium when competing with summer truffle in young truffle orchards. Mycorrhiza 2021, 31, 371–382. [Google Scholar] [CrossRef]

- Şen, İ.; Piñuela, Y.; Alday, J.G.; Oliach, D.; Bolaño, F.; Martínez de Aragón, J.; Colinas, C.; Bonet, J.A. Mulch removal time did not have significant effects on Tuber melanosporum mycelium biomass. For. Syst. 2021, 30, eSC02. [Google Scholar] [CrossRef]

- Martín-Santafé, M.; Pérez-Fortea, V.; Zuriaga, P.; Barriuso-Vargas, J. Phytosanitary problems detected in black truffle cultivation. A review. For. Syst. 2014, 23, 307. [Google Scholar] [CrossRef]

- Latorre, J.; De-Magistris, T.; de Frutos, P.; García, B.; Martinez-Peña, F. Demand for mycotourism products in rural forest areas. A choice model approach. Tour. Recreat. Res. 2021. [Google Scholar] [CrossRef]

- Campo, E.; Guillén, S.; Marco, P.; Antolín, A.; Sánchez, C.; Oria, R.; Blanco, D. Aroma composition of commercial truffle flavoured oils: Does it really smell like truffle? In Proceedings of the Acta Horticulturae, Cartagena, Murcia, 21–24 June 2016; International Society for Horticultural Science (ISHS): Leuven, Belgium, 2018; pp. 1133–1140. [Google Scholar]

{kind=link}

| Statement | Yes, I Agree | Not, I Disagree | I Don’t Know |

|---|---|---|---|

| Supply chain will not change a lot in the future, the only thing that could change is the impact of some stakeholders and their weights | 14 | 2 | 1 |

| Truffle producers will become more powerful actors, developing more and more their own marketing network, selling directly on the retail market, or selling online | 14 | 3 | 0 |

| It is expected to have global competition, and thus truffles will lose their uniqueness | 11 | 6 | 0 |

| The increasing offer worldwide, will bring (generally) a price drop. In this context, local producers will seek to distinguish themselves through environmental quality of their production or to develop territorial designations | 13 | 4 | 0 |

| There will be a decrease in wild production whilst more plantations in Southern Mediterranean Europe will be established, but without affecting the supply chain | 10 | 6 | 1 |

| Some intermediaries will disappear, due to the better organization of the owners and hunters | 12 | 4 | 1 |

| More online buying and selling of fresh and processed products. More local consumption and increase in truffles supply worldwide and year-round | 16 | 0 | 1 |

| It is expected to have an important increase of both demand and offer (more slowly) in areas of Greece | 12 | 0 | 2 |

| It is expected to have a more complex supply chain, with more truffle species that have been somewhat sidelined until now in the market | 11 | 5 | 1 |

| Statement | Mark (SD) (0–10) 1 | SWOT Category |

|---|---|---|

| The truffle is characterized by a very passionate dimension also providing additional incomes | 9.1 (0.8) | Strengths |

| Truffles are very unique products, appreciated for their organoleptic quality and highly appreciated in gastronomy | 9.0 (1.2) | Strengths |

| Increasing awareness of the truffle possibilities in the culinary world | 8.8 (0.6) | Strengths |

| There are strong business companies in the Mediterranean that are leading the sector | 8.4 (1.2) | Strengths |

| The cultivation of black truffles is compatible with environmental conservation as it is easily adaptable to organic farming requisites | 8.2 (1.5) | Strengths |

| Truffle growers have to contribute to the agricultural social security as soon as they start the activity whereas the truffle production will only take place after 7 years or so | 8.9 (2.0) | Weaknesses |

| Consumers are not informed enough about truffles and truffle products and their use in gastronomy | 8.6 (2.0) | Weaknesses |

| In spite of associationism, the productive sector is atomized and non-professional. There is an increase of local initiatives, but a lack of cooperation for the development of greater scope projects | 8.4 (1.4) | Weaknesses |

| Imprecise management techniques (i.e., irrigation management, weed control, fertilization, pruning) for truffle cultivation | 8.2 (0.7) | Weaknesses |

| The return-on-investment period is long for black truffle plantations (in comparison with other agricultural products) | 7.9 (2.0) | Weaknesses |

| Big potential for truffle-associated touristic and gastronomic activities | 8.9 (1.0) | Opportunities |

| Mediterranean countries still have high potential for truffle cultivation | 8.4 (1.1) | Opportunities |

| Integration of the truffle with other products with high rural values that will be attractive for luxury tourism (“terroir” concept) in several regions | 8.4 (1.2) | Opportunities |

| Markets are still demanding more truffles, both fresh and processed | 8.3 (1.1) | Opportunities |

| Increasing market trend of high quality, organic and proximity products (three of the main features of the truffles) | 8.0 (1.2) | Opportunities |

| Present pandemic and future global events might create economic crises in tourism sector | 9.3 (0.9) | Threats |

| Use of phytosanitary products in truffle cultivation is altering the image of an organic product | 8.9 (1.9) | Threats |

| Large disturbance such as mega-fires could affect the truffle yields | 8.2 (1.9) | Threats |

| Increase of wild boar populations threats mostly wild truffle populations (in spite of their ecological role of spreading spores) | 8.1 (1.7) | Threats |

| The chemical additives used as “truffle flavoring” in second tier restaurants decreases truffles’ prestige | 7.7 (3.0) | Threats |

| Challenge | Type of Challenge | Mark (SD) (0–10) 1 |

|---|---|---|

| Common procedure for the certification of truffle-inoculated seedlings (not only for T. melanosporum) | Production/harvesting | 8.9 (0.9) |

| The improvement of the mechanization of truffle farms | Production/harvesting | 7.9 (2.0) |

| Promote the CMO (Common market organizations) for truffles in Europe | Transformation | 8.6 (1.6) |

| Common Quality standards | Transformation | 7.9 (1.6) |

| Promote the traceability of truffle products | Transformation | 7.7 (2.9) |

| Promote the phasing out of artificial “truffle” flavors | Transformation | 7.4 (2.3) |

| Increase of the communicative efforts focusing on countries which do not have a tradition in truffle consumption | Commercialization | 8.9 (0.8) |

| Truffle tourism | Commercialization | 8.6 (1.5) |

| Traceability, labels, regional and cooperative brands | Commercialization | 7.7 (1.9) |

| Education, training, and awareness | Other challenges | 7.9 (1.7) |

| Minimize the fraud in truffle markets | Other challenges | 7.4 (1.7) |

| Consolidation of the actor organizations, particularly the producers by adequate means, before an inter-professional integration | Other challenges | 7.3 (0.9) |

| Prioritized Actions to Be Taken | Mark (SD) (0–10) 1 |

|---|---|

| Strengthen the link between truffles, tourism, and gastronomy | 9.1 (0.9) |

| Evaluate the role of truffles as important mycorrhizal symbionts in reforestation after large forest fires | 9.1 (1.2) |

| Increase the effort at European level for the recognition of truffle production, helping to develop truffle culture, and marketing | 8.9 (1.2) |

| Homogenize the international EU trade and taxation policies | 8.9 (1.6) |

| Develop a common protocol for the certification of the mycorrhized seedlings | 8.7 (1.0) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Oliach, D.; Vidale, E.; Brenko, A.; Marois, O.; Andrighetto, N.; Stara, K.; Martínez de Aragón, J.; Colinas, C.; Bonet, J.A. Truffle Market Evolution: An Application of the Delphi Method. Forests 2021, 12, 1174. https://doi.org/10.3390/f12091174

Oliach D, Vidale E, Brenko A, Marois O, Andrighetto N, Stara K, Martínez de Aragón J, Colinas C, Bonet JA. Truffle Market Evolution: An Application of the Delphi Method. Forests. 2021; 12(9):1174. https://doi.org/10.3390/f12091174

Chicago/Turabian StyleOliach, Daniel, Enrico Vidale, Anton Brenko, Olivia Marois, Nicola Andrighetto, Kalliopi Stara, Juan Martínez de Aragón, Carlos Colinas, and José Antonio Bonet. 2021. "Truffle Market Evolution: An Application of the Delphi Method" Forests 12, no. 9: 1174. https://doi.org/10.3390/f12091174

APA StyleOliach, D., Vidale, E., Brenko, A., Marois, O., Andrighetto, N., Stara, K., Martínez de Aragón, J., Colinas, C., & Bonet, J. A. (2021). Truffle Market Evolution: An Application of the Delphi Method. Forests, 12(9), 1174. https://doi.org/10.3390/f12091174