1. Introduction

In recent years, many for-profit firms have been engaged in improving the social and environmental consequences of their activities by implementing a set of CSR initiatives and philanthropic initiatives in particular [

1,

2]. Corporate foundations designed to act as an intermediate channel for corporate giving come into being as part of these efforts. Firms can support external charitable causes through intermediary corporate foundations or donating directly to public charities [

3]. Specifically, as the intermediary organization, corporate foundations promote public welfare and charity by transferring funds from their founder firms to external charitable causes [

4]. Their services cover a wide range of social fields including education, health, poverty relief, public security, culture, environment, and animal protection. In China, corporate foundations are growing explosively in number, size, and importance in recent years [

5]. According to statistics provided by the China Foundation Center, by December 2016, the total number of corporate foundations reached 768 and their total net assets was about ¥19 billion, which accounts for nearly one-seventh of China’s charitable foundations. However, although corporate foundations have been playing a much more important role in corporate philanthropy, they are still a novelty in China where they were almost non-existent until the Regulations on the Administration of Foundations (RAF) was issued in June 2004 [

6].

There has been a series of scandals and misconduct in corporate foundations in China recently and, thus, they have come under attack from critics who suggest that some corporate foundations do not embody the natural expression of corporate philanthropy but become substantial tools of their founder firms to pursue self-interest [

7]. For example, the Shanghai Jianguo foundation secretly transfers tens of millions of donated funds back to its founder firm in the form of interest-free loans numerous times over a period of five years. As a type of non-profit organization born from for-profit firms, corporate foundations can be regarded as vessels of the founder firms for three reasons. First, corporate foundations derive most of their income from the founder firms [

8]. Second, corporate foundations mainly depend on the founder firms for nonfinancial resource (staff support, management, and knowledge) [

9]. Third, corporate foundations always have their founder firms’ executives as members of their boards of directors [

10,

11]. According to statistics provided by the China Foundation Center, nearly 90% of corporate foundations’ board members come from the founder firms and 65% of them are top-level executives (CEOs, CFOs, and COOs). Consequently, the close ties between founder firms and their corporate foundations represent a major way for the firms to exploit the potential benefits of philanthropy [

12].

This study clarifies the self-serving earning objectives the firms are searching for with corporate foundations. Specifically, as the intermediate channel to transfer funds, corporate foundations offer an opportunity for their founder firms to exercise discretion to influence reported earnings. The firms first transfer funds to their corporate foundations (called “payins”) and simultaneously record donation expenditures on the income statements. Separately, corporate foundations then make grants and donations to promote public benefit undertakings (called “payouts”). The separation of pay-ins and pay-outs offers an opportunity for the firms to engage in discretionary funding choices to manipulate earnings since they can record donation expenditures on the income statements in any period they choose, which is subject to ensuring that the foundations have enough funds for charitable purposes. Firms can use their corporate foundations strategically to make income-increasing or income-decreasing foundation funding choices to achieve specific earnings targets, which is illustrated in

Figure 1.

Although corporate foundations may be a useful earnings management tool, whether firms actually use their corporate foundations to manipulate earnings is still an open question. As a specific expression of corporate philanthropy, corporate foundations embody a significant approach to philanthropic CSR. Ethical, political, and integrative theories of CSR suggest that firms must accept CSR as an ethical obligation and have an incentive to be honest, trustworthy, and ethical in their business processes [

13,

14]. However, earnings management is the exertion of intentional influence over the process of financial reporting in order to mislead some stakeholders or to influence contractual outcomes and, thus, it is unethical and irresponsible behavior [

15]. Literature that is more recent examines the relationship between CSR and earnings management and concludes two opposite views. Some studies relying on ethical, political, and integrative theories of CSR suggest that CSR firms always behave in a responsible manner to restrict earnings management practices [

16,

17,

18,

19,

20]. While some studies relying on opportunistic use of CSR suggest that CSR can be deemed as managerial perquisite and CSR firms are more likely to engage in earnings management to mislead stakeholders as to the value of the firm and financial performance [

21,

22,

23].

Given the two contrasting views from prior research with mixed implications on the true relation between CSR and earnings management, the question arises for corporate foundations: which viewpoint do they support? Using hand-collected data on Chinese corporate foundations and a sample of firms listed on the A-share market from 2010 to 2016, we first examine the effect of corporate foundations on earnings management of their founder firms. To do so, we employ the econometrics non-parametric propensity score matching method to classify the sample firms into two groups: one subgroup including firms with corporate foundations and the other subgroup including firms without corporate foundations. Then the overall earnings management differences are compared between the two subgroups. Using discretionary accruals as the proxy for overall earnings management level, we find that the discretionary accruals of firms with corporate foundations are significantly higher than for those without corporate foundations. Considering the important role of ownership property in shaping governance of Chinese listed firms, we further investigate the impact of ownership property on the effect of corporate foundations on earnings management. We find that the discretionary accruals are not significantly different within the stated-owned subgroup while they are significantly different within the privately-owned subgroup, which suggests that the difference of discretionary accruals between firms with and without corporate foundations is driven mainly by privately-owned firms.

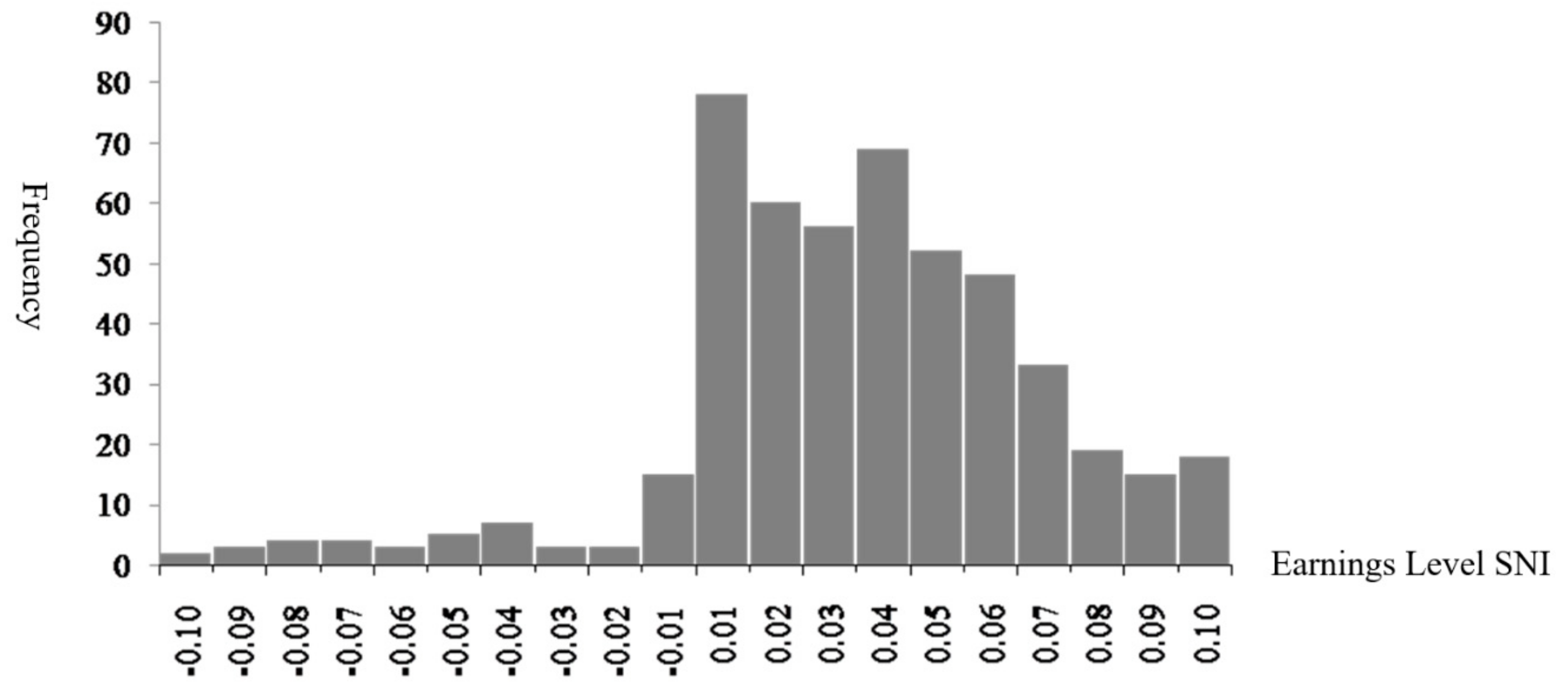

Furthermore, we explore the specific earnings targets of this type of earnings management associated with corporate foundations. To measure the magnitude of the manipulation of foundation funding choices, we develop a model of discretionary donation expenditures using a research design similar to previous single account approaches. In brief, our findings reveal the following aspects: First, we find founder firms with small profits record lower discretionary donation expenditures than those with small losses. Second, we demonstrate that founder firms with higher stock price sensitivity record lower discretionary donation expenditures than firms with lower stock price sensitivity. Third, we show that founder firms with higher income-decreasing discretionary donation expenditures are more likely to report consecutive earnings increases in subsequent periods. Taken together, the results suggest that firms strategically use their corporate foundations to manipulate earnings in order to avoid losses and decreases in earnings or to create earnings reserves for use in future periods.

This study offers several contributions to the field. First, our study highlights that for-profit firms make opportunistic use of their corporate foundations to pursue self-serving earnings objectives. This is a new and far-reaching addition to the theoretical perspectives to better understand why for-profit firms establish non-profit corporate foundations. To our knowledge and in view of the existing literature, Petrovits [

24] is one of very few researchers, if not the only one, to examine the strategic use of corporate foundations to achieve financial reporting objectives among US firms. Our study can continue to provide a healthy supplement to the literature. Unlike Petrovits [

24], our primary goal is to explore the potential role of corporate foundations in the earnings management efforts of their founder firms. To do so, we generate a novel empirical strategy that tests alternative theories of corporate foundations by comparing the overall earnings management level of firms with and without corporate foundations. More precisely, we employ the econometrics non-parametric propensity score matching method to investigate the net effect of corporate foundations on overall earnings management of their founder firms. In light of the fact that firms with corporate foundations exhibit a higher level of overall earnings management than those without corporate foundations, we interpret the findings as evidence that corporate foundations can be used as an effective earnings management tool, which is consistent with the argument that contributions transferred to corporate foundations represent an agency problem [

11,

25,

26,

27]. To a certain extent, examining the differences in earnings management between firms with and without foundations can yield insights into the nature of corporate foundations and shed light on how corporate foundations extend to earnings management behavior.

Second, our study is important because it is the first to use the context of China, which is the largest emerging market and the second largest economy, to develop an empirically instrumental analysis of corporate foundations. More importantly, there are so many differences between corporate foundations in the U.S. and China that the findings derived from the U.S. may not fit in well with China. China and the U.S. occupy two extremes in terms of the development stage and legal system of corporate foundations. More specifically, as an innovative form of social organization, corporate foundations are a novelty in China where they are almost non-existent until 2005. However, corporate foundations in the U.S. are largely thought of as a twentieth-century phenomenon [

28]. In addition, the U.S. has the most advanced governance rules for charitable foundations especially for corporate foundations. However, the fact remains that corporate foundations in China are still an overlooked non-profit organization and, thus, a favorable institutional and legal environment has not been considered to boost their expansion, which results in a specific Chinese-style philanthropy [

7]. Not surprisingly, combined with the institutional background with Chinese characteristics, we conclude different and interesting findings. Specifically, considering the impact of ownership property, we find that the manipulation of foundation funding choices is made by privately-owned firms, which is contrary to the conventional belief that state ownership is a major barrier to corporate efficiency. Based on China’s unique stock delisting system, we find that firms with small profits are more likely to engage in income-increasing foundation funding choices to avoid losses, which demonstrates an alternative goal on the opportunistic use of corporate foundations.

Third, our study offers empirical evidence relevant to the current public controversy regarding corporate hypocrisy by examining the role of corporate foundations in the earnings management practices of their founder firms. The findings in our study are consistent with agency problems of the firms in which corporate foundations offer an opportunity for managers to exercise discretion in charitable contributions to pursue self-serving earnings objectives. Thus, we regard as corporate hypocrisy any behavior that establishes corporate foundations for charitable donations but simultaneously uses them to manipulate earnings in order to achieve self-serving objectives. In China’s system of moral values, which has existed for thousands of years, good and evil are absolute opposites. A ‘charitable’ person who seeks to gain spiritual resources and moral respect but simultaneously indulges in deceit and dishonest behavior to pursue self-interest is regarded as a moral hypocrite [

29]. Ethical and integrative theories of CSR argue that there is a moral imperative for socially responsible firms to contribute to the good of society by doing what is ethically correct [

17] while the manipulation of foundation funding choices is irresponsible and unethical insofar as it conceals dishonest and immoral motivations and has negative consequences for all stakeholders. To a large extent, the opportunistic use of corporate foundations is contrary to the stated ethical standards of philanthropic CSR and, thus, can be regarded as corporate hypocrisy with self-interest embedded in benevolence.

Lastly, our evidence has important implications for policy makers and prudential regulators concerning the governance of corporate foundations and the founder firms in China. Our study summarizes that, as a kind of non-profit social organization, corporate foundations, born from for-profit firms, are a signal of agency problems and can be used as off-balance sheet fund pools to pursue self-serving earnings objectives. The findings offer evidence relevant to the current public debate on the governance of corporate philanthropy and to the regulatory question with respect to full information disclosure of the firms’ direct giving programs and their corporate foundations. On the other hand, the findings also offer evidence relevant to corporate foundations and their governance. As private-sector agents with public objectives, it is important to design a corporate foundation governance system that considers their uniqueness. In addition, evidence from this study can help stakeholders better understand firms’ financial reporting behaviors in light of corporate foundations and differentiate transparent financial information from less reliable information.

The remainder of this paper is organized as follows. In

Section 2, we introduce the institutional background, review the extant literature, and develop our research hypotheses. In

Section 3, we describe the research sample and provide variable definitions and model specifications. In

Section 4, we report the results of descriptive statistics and Pearson correlation analysis and discuss our hypotheses testing and robustness checks. Lastly, we summarize conclusions and offer a discussion of our study.

5. Conclusions and Discussion

Although some studies attempt to explore the association between CSR and earnings management, they provide two opposite views that limit our understanding of their true relationship. In this paper, we target a significant approach to philanthropic CSR that is relatively under-researched in China, which involves corporate foundations and their potential role in the earnings management efforts of their founder firms. Based on a sample of corporate foundations and firms listed on the A-share market from 2010 to 2016, we provide strong and consistent evidence consistent with the hypotheses that for-profit firms use their corporate foundations strategically as off-balance sheet fund pools to help achieve self-serving earnings objectives. Specifically, our results indicate that firms with corporate foundations behave differently from those without corporate foundations in overall discretionary accruals and, in contrast with the conventional belief that state ownership is the root of corporate inefficiency, we find that privately-owned firms are more likely to make opportunistic use of corporate foundations to manipulate earnings than comparable state-owned firms. In addition, our findings suggest that corporate foundations offer an opportunity for their founder firms to exercise substantial discretion regarding the amount of donation expenditures to increase earnings in order to avoid losses and decreases in earnings or to decrease earnings in order to create earnings reserves.

Overall, our findings demonstrate that for-profit firms strategically make income-increasing or income-decreasing foundation funding choices to pursue self-serving earnings objectives. The findings, thus, are consistent with an agency problem that the visibly ethical behavior of establishing corporate foundations does not represent the consistent embodiment of philanthropic CSR, but becomes a vehicle that enables firms to achieve self-serving earnings objectives. Since corporate foundations are burdensome to create, costly to administer, constrained by payout requirements and income taxes, and are not necessary for firms to make charitable donations, our findings also provide an enriched understanding of the motivations of profit-oriented firms for establishing non-profit corporate foundations. Moreover, documenting the opportunistic use of corporate foundations as off-balance sheet fund pools to manipulate reported earnings lends support to the argument that social responsible firms behave in an irresponsible manner to achieve self-serving earnings objectives, which contributes to drawing conclusions about the nature of the relationship between CSR and earnings management. More importantly, our findings not only have important implications for legislators and regulators concerning the governance of corporate charitable giving but also can provide new ideas for corporate foundations governance, which can guide the healthy and sustainable development of public welfare services in China.

We note that our findings should be interpreted considering several limitations. First, due to data limitations, our sample might not be so large as to represent the entire corporate foundation sector. This is especially true because corporate foundations are a novelty in China, statistics and data were rare for this new foundation sector before the China Foundation Center was launched in July 2010. In addition, our sample excludes corporate foundations that are established by unlisted firms or overseas listed firms, which occupy a large proportion of all corporate foundations. As such, our results need to be regarded as preliminary findings. Second, this study is only the first step in a broader research agenda. We view our findings as a credible demonstration that corporate foundations are a signal of agency problems in the founder firms. However, we do not further study the governance mechanisms of corporate foundations in the implementation of CSR initiatives. As boundary organizations facilitating relationships between the founder firms and public charities, corporate foundations and their governance research is increasingly the focus in the transformation process of corporate governance to social organization governance. This study provides a platform for future research among corporate foundations with a specific focus on governance.

{kind=link}

{kind=link}