The Effects of the RCS’s Application in the Value Added Tax Collecting Process on the Perception of SME Taxpayer in Korea’s Trade Activity: Transparency and Fairness in Trade

Abstract

:1. Introduction

2. Theoretical Background of Reverse Charge System (RCS) of VAT and Hypothesis Development

2.1. Literature Review

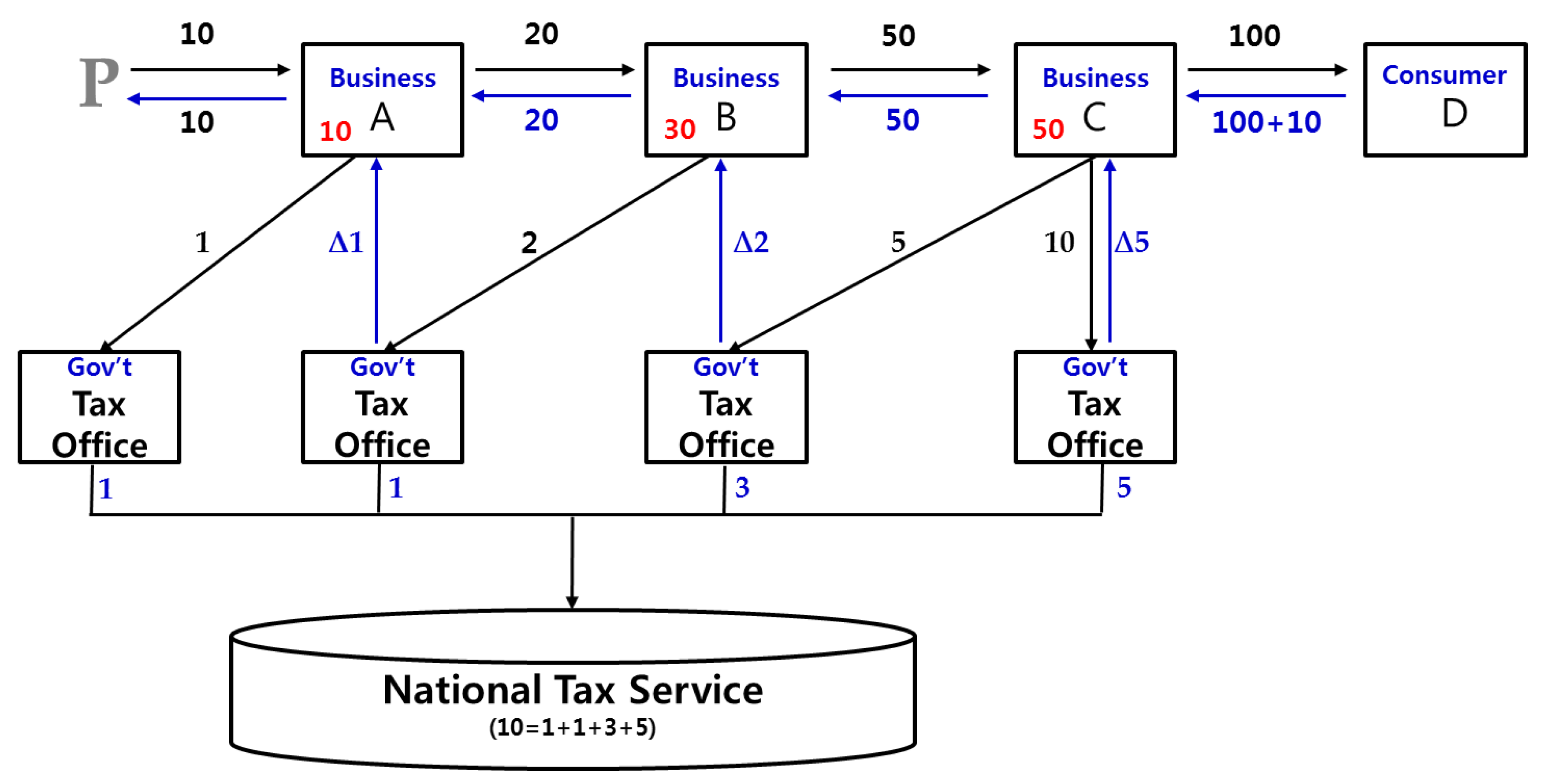

2.2. RCS of VAT

2.3. Hypothesis Development

3. Methodology and Data

3.1. Methodology

3.2. Data

4. Results of Empirical Analysis

4.1. Descriptive Statistics and Correlations of Major Variables

4.2. Results of Probit Regression Analysis

5. Conclusions

Funding

Conflicts of Interest

References

- Chung, J.S.; Yoon, S.M. The Determinants of Taxpayer’s Satisfaction of Reverse Charge System and Bank Service: Case of Korean Value-Added Tax. Int. J. Appl. Eng. Res. 2015, 10, 31649–31662. [Google Scholar]

- Ki, E.S.; Koo, J.E.; Park, M.H. A Study on Reform of VAT Reverse Charge Mechanism. Korean J. Tax. Res. 2015, 32, 139–165. (In Korean) [Google Scholar]

- Lee, H.W. Reconsidering the Concept of Transparency in Policy. J. Inst. Soc. Sci. 2016, 27, 117–142. (In Korean) [Google Scholar] [CrossRef]

- HRMS. VAT Notice 735: VAT Domestic Reverse Charge on Specified Goods and Services. UK, 2015. Available online: https://www.gov.uk/guidance/the-vat-domestic-reverse-charge-procedure-notice-735#para9 (accessed on 13 March 2018).

- Iyer, P.; Davari, A.; Paswan, A. Perceived price fairness and price decay in the DVD market. Green products: Altruism, economics, price fairness and purchase intention. Soc. Bus. 2016, 6, 39–64. [Google Scholar] [CrossRef]

- Lúðvík, L. VAT Frauds in the European Union: The Reverse Charge Mechanism, Joint and Several Liability and the “Knowledge Test”. Master’s Thesis, Lund University, Longde, Sweden, 2012. [Google Scholar]

- Kim, K.S.; Jeon, B.W. The Evasions of Gold Bullion Trades and Its Improvements. Korean Res. Tax. Law 2007, 12, 340–374. (In Korean) [Google Scholar]

- Kim, J.J.; Hong, S.Y.; Lee, H.M. Review of Problem and Effect of RCS Adoption in Steel Scrap. Korean Res. Tax. Law 2015, 15, 2–75. (In Korean) [Google Scholar]

- Milošković, A.; Dojčinović, B.; Kovačević, S.; Radojković, N.; Radenković, M.; Milošević, D.; Simić, V. Spatial monitoring of heavy metals in the inland waters of Serbia: A multi-species approach based on commercial fish. Environ. Sci. Pollut. Res. 2016, 23, 9918–9933. [Google Scholar] [CrossRef] [PubMed]

- Ainsworth, R.T. The Morphing of MTIC Fraud: VAT Fraud Infects Tradable CO2 Permits. Boston University School of Law. 2009. Available online: https://ssrn.com/abstract=14432792 (accessed on 22 February 2018).

- Zee, H.H. A New Approach to Taxing Financial Intermediation Services Under a Value-Added Tax. 2005. Available online: https://www.jstor.org/stable/41790176 (accessed on 13 March 2018).

- Ainsworth, R.T.; Musaad, A. GCC VAT: The Intra-Gulf Trade Problem. 2016. Available online: https://ssrn.com/abstract=2916252 (accessed on 20 August 2016).

- Poniatowski, G.; Bonch-Osmolovskiy, M.; Misha, B. Study and Reports on the VAT Gap in the EU-28 Member States: 2016 Final Report. 2016. Available online: https://ssrn.com/abstract=2847658 (accessed on 4 April 2018).[Green Version]

- Lamensch, M. Are ‘reverse charging’ and the ‘one-stop-scheme’ efficient ways to collect VAT on digital supplies? World J. VAT/GST Law 2012, 1, 1–12. [Google Scholar] [CrossRef]

- Hrdinková, M. Reverse Charge Method in the Environment of Harmonized VAT. Ministry of Finance of the Czech Republic Report (Closing VAT GAP through Reverse Charge Mechanism). 2015. Available online: https://www.mfcr.cz/en/news/news/2016/collection-of-the-tax-conference-23757 (accessed on 28 October 2018).

- Chung, J.S.; Yoon, S.M. A Study on Applying VAT Charge System Using Credit Card Companies. Korean Tax Account. J. 2016, 17, 163–192. (In Korean) [Google Scholar]

- OECD Consumption. Consumption Tax Trends 2010 VAT/GST and Excise Rates, Trends and Administration Issues; OECD Publishing: Paris, France, 2011. [Google Scholar]

- European Commission. Assessment of the Application and Impact of the Optional ‘Reverse Charge Mechanism’ within the EU VAT System. 2014. Available online: https://ec.europa.eu/taxation_customs/sites/taxation/files/resources/documents/common/publications/studies/kp_07_14_060_en.pdf (accessed on 17 March 2018).

- Statistics of NTS. 2010–2017. Available online: https://www.nts.go.kr/info/info_05.asp (accessed on 3 March 2018). (In Korean).

- Park, H.S.; Hyun, N. The Effects of Transparency on Citizen Satisfaction with Civil Applications Administration. Korean J. Public Admin. 2010, 12, 385–406. (In Korean) [Google Scholar]

- Jang, Y.S.; Song, E.Y. Changing Logics of Transparency in Korea, 1993~2006: A Content Analysis of Korean Newspaper Articles. Korean J. Sociol. 2008, 42, 146–177. (In Korean) [Google Scholar]

- Zimmerman, J.L. Taxes and firm size. J. Account. Econ. 1983, 5, 119–149. [Google Scholar] [CrossRef]

- Park, H.S. Improvement of Public Administration Transparency: The Case of Korea. Local Admin. Rev. 2000, 13, 39–57. (In Korean) [Google Scholar]

- Niehoff, B.P.; Moorman, R.H. Justice as a mediator of the relationship between monitoring and organizational citizenship behavior. Acad. Manag. J. 1993, 36, 527–556. [Google Scholar]

- Watts, R.; Zimmerman, J.L. Positive Accounting Theory; Edgewood Cliff: Bergen County, NJ, USA, 1986. [Google Scholar]

- Greenberg, J. The social side of fairness: Interpersonal and informational classes of organizational justice. In Series in Applied Psychology. Justice in the Workplace: Approaching Fairness in Human Resource Management; Cropanzano, R., Ed.; Lawrence Erlbaum Associates, Inc.: Hillsdale, NJ, USA, 1993; pp. 79–103. [Google Scholar]

- Lind, E.A.; Tyler, T.R. Critical issues in social justice. In The Social Psychology of Procedural Justice; Plenum Press: New York, NY, USA, 1988. [Google Scholar]

- Rifaat, S.M.; Chin, H.C. Accident Severity Analysis Using Ordered Probit Model. J. Adv. Transp. 2007, 41, 91–114. [Google Scholar] [CrossRef]

- O’Donnel, C.J.; Connor, D.H. Predicting the Severity of Motor Vehicle Accident Injuries Using Models of Ordered Multiple Choice. Accid. Anal. Prev. 1996, 28, 739–753. [Google Scholar] [CrossRef]

- Renski, H.; Khattak, A.J.; Council, F.M. Impact of Speed Limit Increases on Crash Severity: Analysis of Single-Vehicle Crashes on North Carolina Interstate Highways. Transp. Res. Rec. 1999, 1665, 100–108. [Google Scholar] [CrossRef]

- Kim, K.S.; Yoon, S.M. Taxpayer’s Perception to Tax Payment in Kind System in Support of SMEs’ Sustainability: Case of the South Korean Government’s Valuation of Unlisted Stocks. Sustainability 2017, 9, 1523. [Google Scholar] [CrossRef]

- Li, Z.; Liu, P.; Wang, W.; Xu, C. Using support vector machine models for crash injury severity analysis. Accid. Anal. Prev. 2012, 45, 478–486. [Google Scholar] [CrossRef] [PubMed]

- Anarkooli, A.J.; Hosseinpour, M.; Kardar, A. Investigation of factors affecting the injury severity of single-vehicle rollover crashes: A random-effects generalized ordered probit model. Accid. Anal. Prev. 2017, 106, 399–410. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

| Period | VAT | Corporate Tax | Individual Income Tax |

|---|---|---|---|

| FY2006-08(a) | 13.10% | 3.60% | 9.30% |

| FY2009-11(b) | 11.30% | 3.40% | 10.30% |

| FY2012-15(c) | 10.30% | 2.90% | 8.40% |

| Changes (c − a)/a | −21.37% point | −19.44% point | −9.68% point |

| Variables | Characteristics | Frequency | Ratio |

|---|---|---|---|

| Business Type of VAT | Corporate Taxpayer | 912 | 53.87% |

| Proprietorship Taxpayer | 721 | 42.59% | |

| Small Proprietorship Taxpayer | 19 | 1.12% | |

| Enterprise Owned by Government | 9 | 0.53% | |

| No Responses | 32 | 1.89% | |

| Total | 1693 | 100% | |

| Industry | Construction | 86 | 5.08% |

| Building Dismantling Construction | 29 | 1.71% | |

| Retail Store Services of Used Goods | 34 | 2.01% | |

| Collection and Sale of Materials for Recycling | 522 | 30.83% | |

| Metal Manufacturing | 364 | 21.50% | |

| Wholesale Services of Metal | 91 | 5.38% | |

| Automobile Manufacturing | 125 | 7.38% | |

| Electronics Related Manufacturing | 148 | 8.74% | |

| Others | 222 | 13.11% | |

| No Responses | 72 | 4.25% | |

| Total | 1693 | 100% |

| Variables | Mean | STD | Min | Q1 | Med | Q3 | Max |

|---|---|---|---|---|---|---|---|

| Trade_Transparency1 | 3.627 | 1.103 | 1 | 3 | 4 | 4 | 5 |

| Trade_Transparency2 | 3.506 | 1.078 | 1 | 3 | 4 | 4 | 5 |

| Trade_Fairness1 | 3.760 | 1.200 | 1 | 3 | 4 | 5 | 5 |

| Trade_Fairness2 | 4.402 | 0.979 | 1 | 4 | 5 | 5 | 5 |

| SME_Taxpayer | 2.964 | 2.386 | 1 | 1 | 2 | 4 | 9 |

| Purchase_Activity | 0.353 | 0.487 | 0 | 0 | 0 | 1 | 1 |

| Compliance_Cost | 2.582 | 1.240 | 1 | 1 | 3 | 3 | 5 |

| Expert_Advice | 0.211 | 0.408 | 0 | 0 | 0 | 0 | 1 |

| Variables | Trade_Transparency1 | Trade_Transparency2 | Trade_Fairness1 | Trade_Fairness2 | SME_Taxpayer | Purchase_Activity | Compliance_Costs |

|---|---|---|---|---|---|---|---|

| Trade_Transparency2 | 0.681 *** (0.000) | 1 | |||||

| Trade_Fairness1 | 0.220 *** (0.000) | 0.236 *** (0.000) | 1 | ||||

| Trade_Fairness2 | 0.153 *** (0.000) | 0.156 *** (0.000) | 0.414 *** (0.000) | 1 | |||

| SME_Taxpayer | 0.128 *** (0.000) | 0.123 *** (0.000) | 0.175 *** (0.000) | 0.142 *** (0.000) | 1 | ||

| Purchase_Activity | 0.047 * (0.054) | −0.013 (0.597) | 0.073 *** (0.003) | −0.046 * (0.056) | 0.037 (0.143) | 1 | |

| Compliance_Cost | −0.143 *** (0.000) | −0.171 *** (0.000) | −0.215 *** (0.000) | −0.114 *** (0.000) | −0.045 * (0.080) | 0.031 (0.212) | 1 |

| Expert_Advice | −0.002 (0.926) | −0.029 (0.230) | 0.026 (0.281) | −0.017 (0.489) | −0.083 *** (0.001) | 0.028 (0.256) | 0.041 * (0.096) |

| Variables | Trade_Transparency1 | Trade_Transparency2 | ||||

|---|---|---|---|---|---|---|

| Coefficient | Wald X2 | p-Value | Coefficient | Wald X2 | p-Value | |

| Intercept 1 | −1.881 *** | 43.32 | 0.000 | −2.057 *** | 51.83 | 0.000 |

| Intercept 2 | 0.428 *** | 112.28 | 0.000 | 0.468 *** | 128.07 | 0.000 |

| Intercept 3 | 1.403 *** | 675.41 | 0.000 | 1.525 *** | 776.80 | 0.000 |

| Intercept 4 | 2.402 *** | 1545.25 | 0.000 | 2.612 *** | 1708.53 | 0.000 |

| SME_Taxpayer | 0.039 *** | 10.30 | 0.000 | 0.032 *** | 6.79 | 0.009 |

| Purchase_Activity | 0.068 | 1.18 | 0.476 | 0.053 | 0.70 | 0.401 |

| Compliance_Cost | −0.101 *** | 18.58 | 0.000 | −0.117 *** | 25.28 | 0.000 |

| Expert_Advice | 0.057 | 0.01 | 0.548 | 0.057 | 0.68 | 0.410 |

| ∑Location | Included | Included | ||||

| ∑IND | Included | Included | ||||

| Log Likelihood Ratio | −2062.94 | −2044.39 | ||||

| Observation | 1693 | 1693 | ||||

| Variables | Trade Fairness1 | Trade Fairness2 | ||||

|---|---|---|---|---|---|---|

| Coefficient | Wald X2 | p-Value | Coefficient | Wald X2 | p-Value | |

| Intercept 1 | −1.016 *** | 11.29 | 0.000 | 0.203 | 0.32 | 0.574 |

| Intercept 2 | 0.880 *** | 616.56 | 0.000 | 0.705 *** | 374.66 | 0.000 |

| Intercept 3 | 1.552 *** | 1099.95 | 0.000 | 1.171 *** | 529.92 | 0.000 |

| Intercept 4 | 2.248 *** | 1210.77 | 0.000 | 1.886 *** | 469.98 | 0.000 |

| SME_Taxpayer | 0.047 *** | 14.32 | 0.000 | 0.052 *** | 12.33 | 0.000 |

| Purchase_Activity | −0.019 | 0.090 | 0.765 | −0.030 | 0.17 | 0.677 |

| Compliance_Cost | −0.153 *** | 41.71 | 0.000 | −0.055 ** | 4.14 | 0.042 |

| Expert_Advice | 0.059 | 0.70 | 0.102 | 0.048 | 0.37 | 0.543 |

| ∑Location | Included | Included | ||||

| ∑IND | Included | Included | ||||

| Log Likelihood Ratio | −2037.57 | −1482.32 | ||||

| Observation | 1693 | 1693 | ||||

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yoon, S.M. The Effects of the RCS’s Application in the Value Added Tax Collecting Process on the Perception of SME Taxpayer in Korea’s Trade Activity: Transparency and Fairness in Trade. Sustainability 2018, 10, 4132. https://doi.org/10.3390/su10114132

Yoon SM. The Effects of the RCS’s Application in the Value Added Tax Collecting Process on the Perception of SME Taxpayer in Korea’s Trade Activity: Transparency and Fairness in Trade. Sustainability. 2018; 10(11):4132. https://doi.org/10.3390/su10114132

Chicago/Turabian StyleYoon, Sung Man. 2018. "The Effects of the RCS’s Application in the Value Added Tax Collecting Process on the Perception of SME Taxpayer in Korea’s Trade Activity: Transparency and Fairness in Trade" Sustainability 10, no. 11: 4132. https://doi.org/10.3390/su10114132

APA StyleYoon, S. M. (2018). The Effects of the RCS’s Application in the Value Added Tax Collecting Process on the Perception of SME Taxpayer in Korea’s Trade Activity: Transparency and Fairness in Trade. Sustainability, 10(11), 4132. https://doi.org/10.3390/su10114132