Exploring the Supply-Demand-Discrepancy of Sustainable Financial Products in Germany from a Financial Advisor’s Point of View

Abstract

1. Introduction

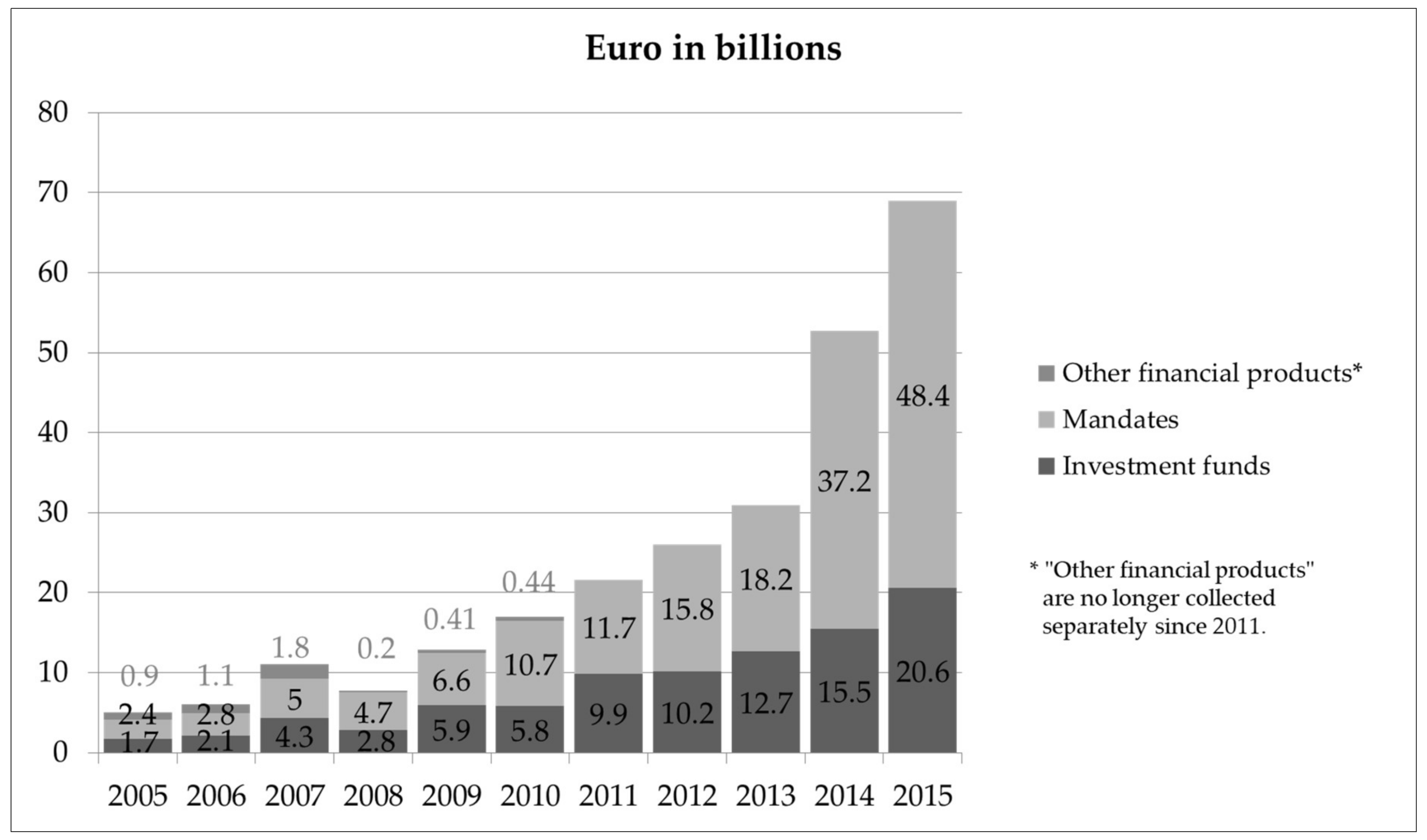

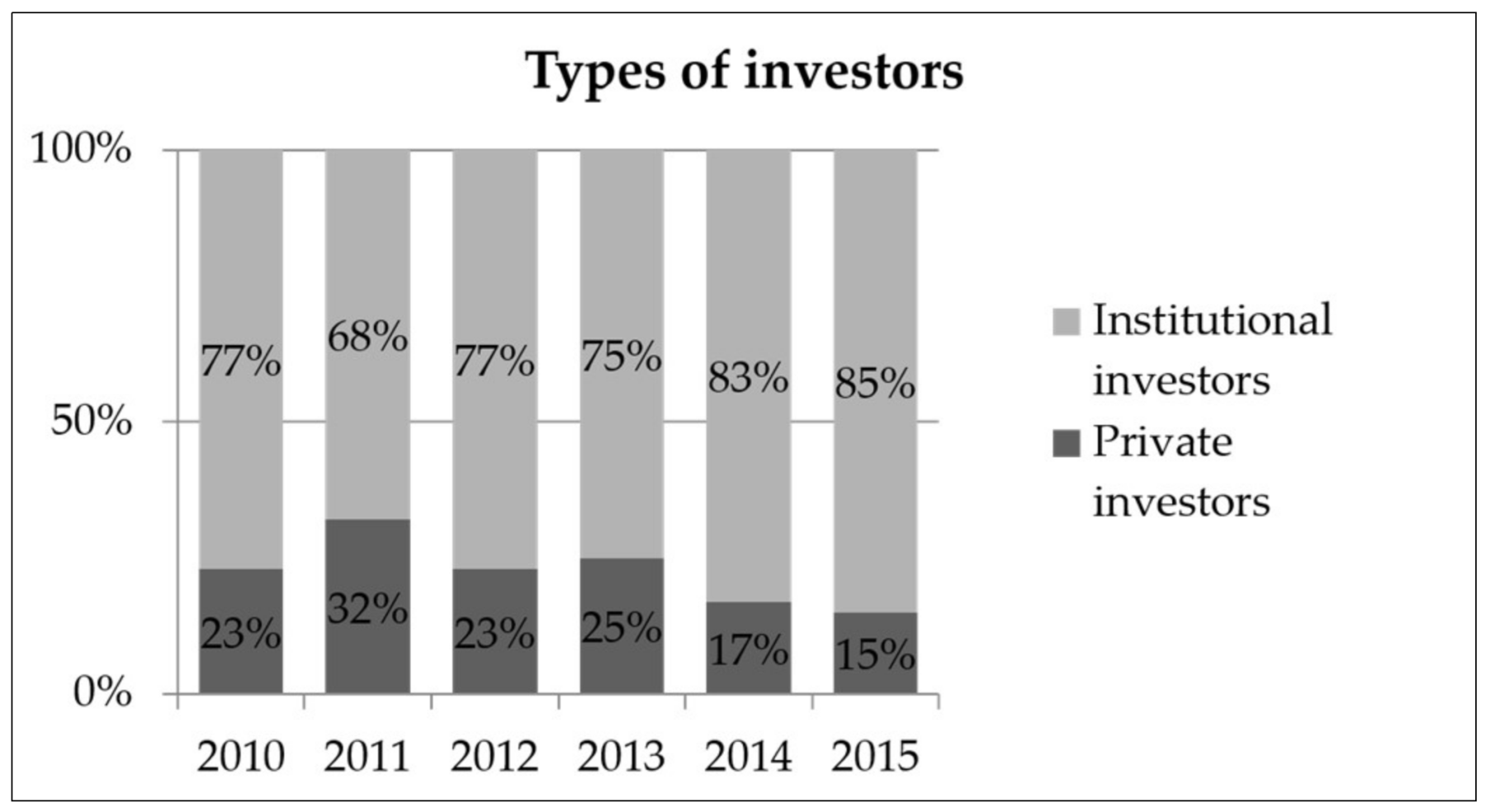

2. Basic Terminology

2.1. Sustainable Investment

2.2. The Role of the Investment Advisor

3. Data and Methodology

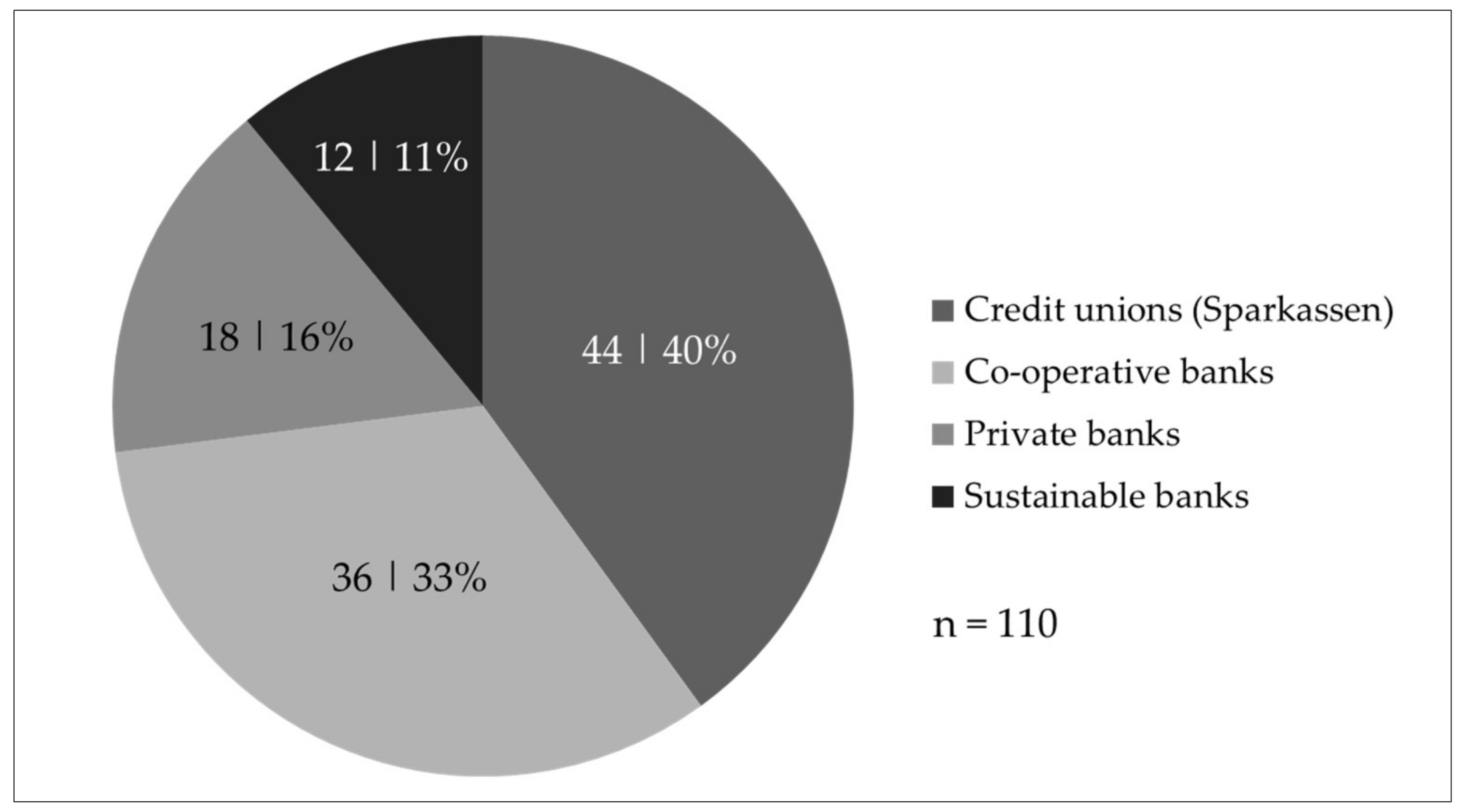

3.1. Data Collection

3.2. Data Analysis

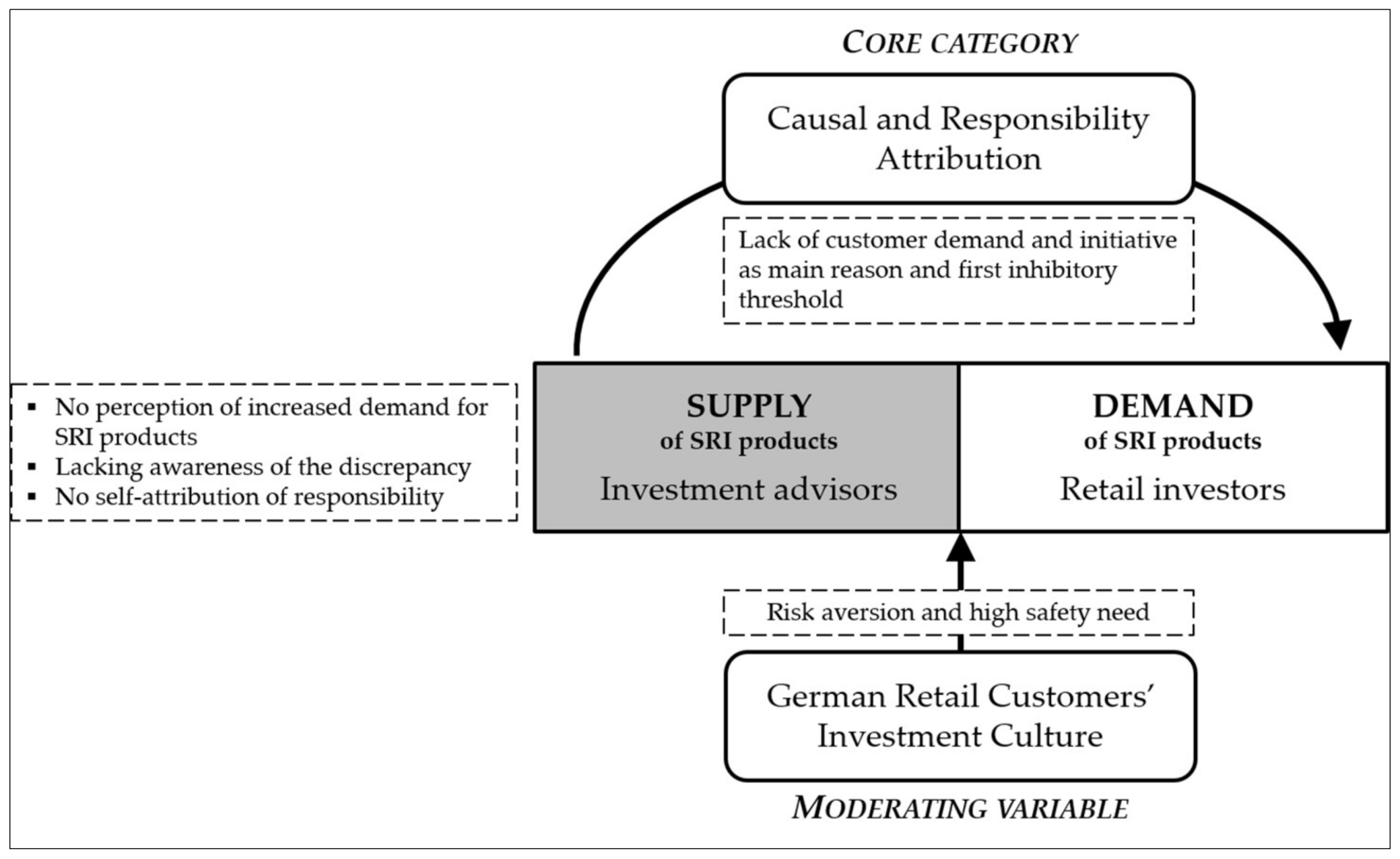

4. Findings—Developing a Theoretical Framework

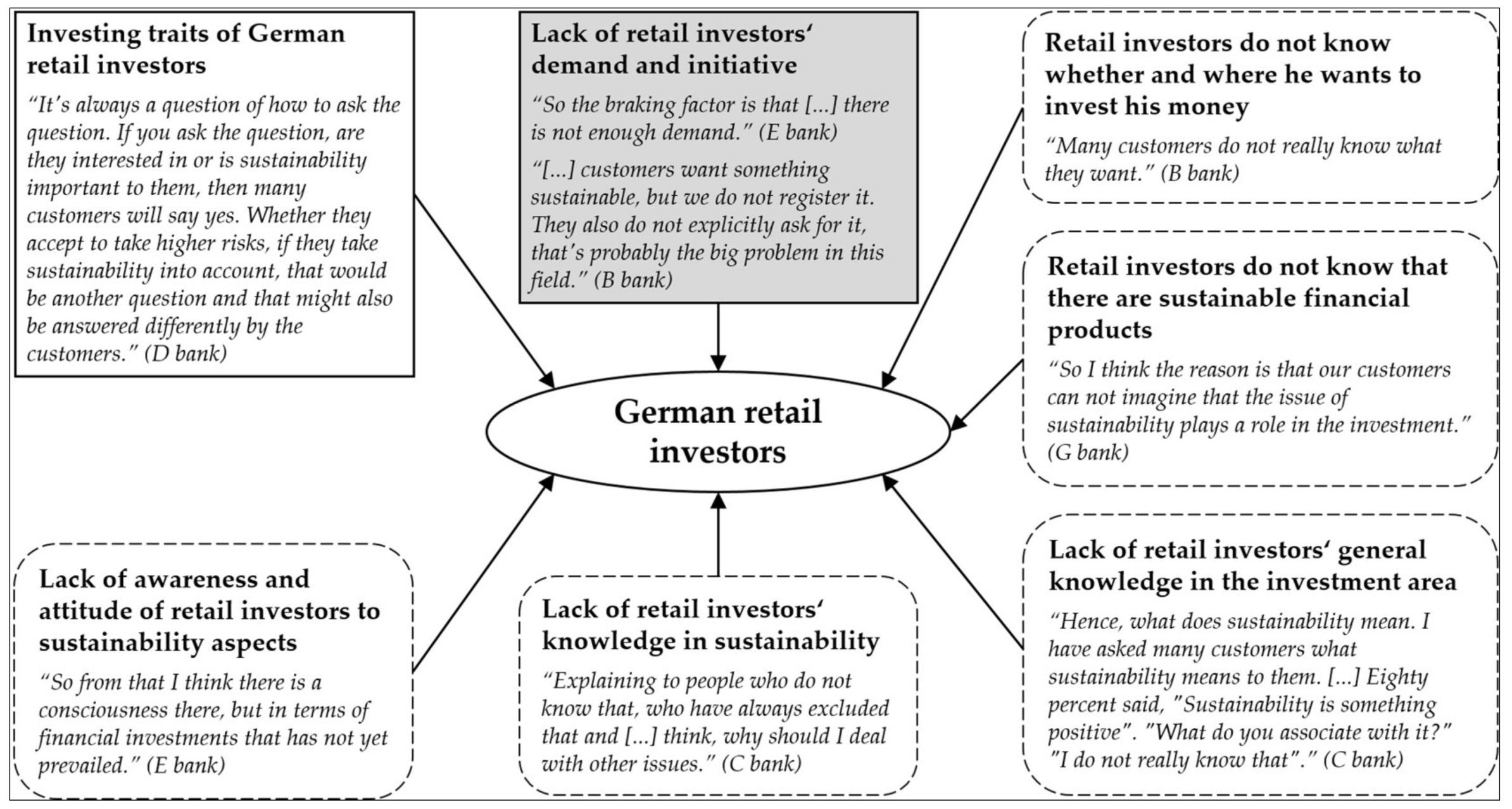

“I am a bit surprised that these surveys, which have been done on several occasions on the subject, have revealed that the customers have the need and I believe that if this need would be expressed by the customers, we financial advisors would have been much more likely to respond and created offers. […] And then I come and say, but no customer here says that he wants that. I believe that this trend is simply not being massively expressed by customers and if that does not happen, we will offer the same solutions as we have always offered. So, this rethinking will probably take a very long time for us.”(G bank)

“So, if this signal […] is sent by the investors, then the fund industry and the EZ bank [..] will adjust to it, then such products would be developed immediately which are declared as sustainable financial products.”(E bank)

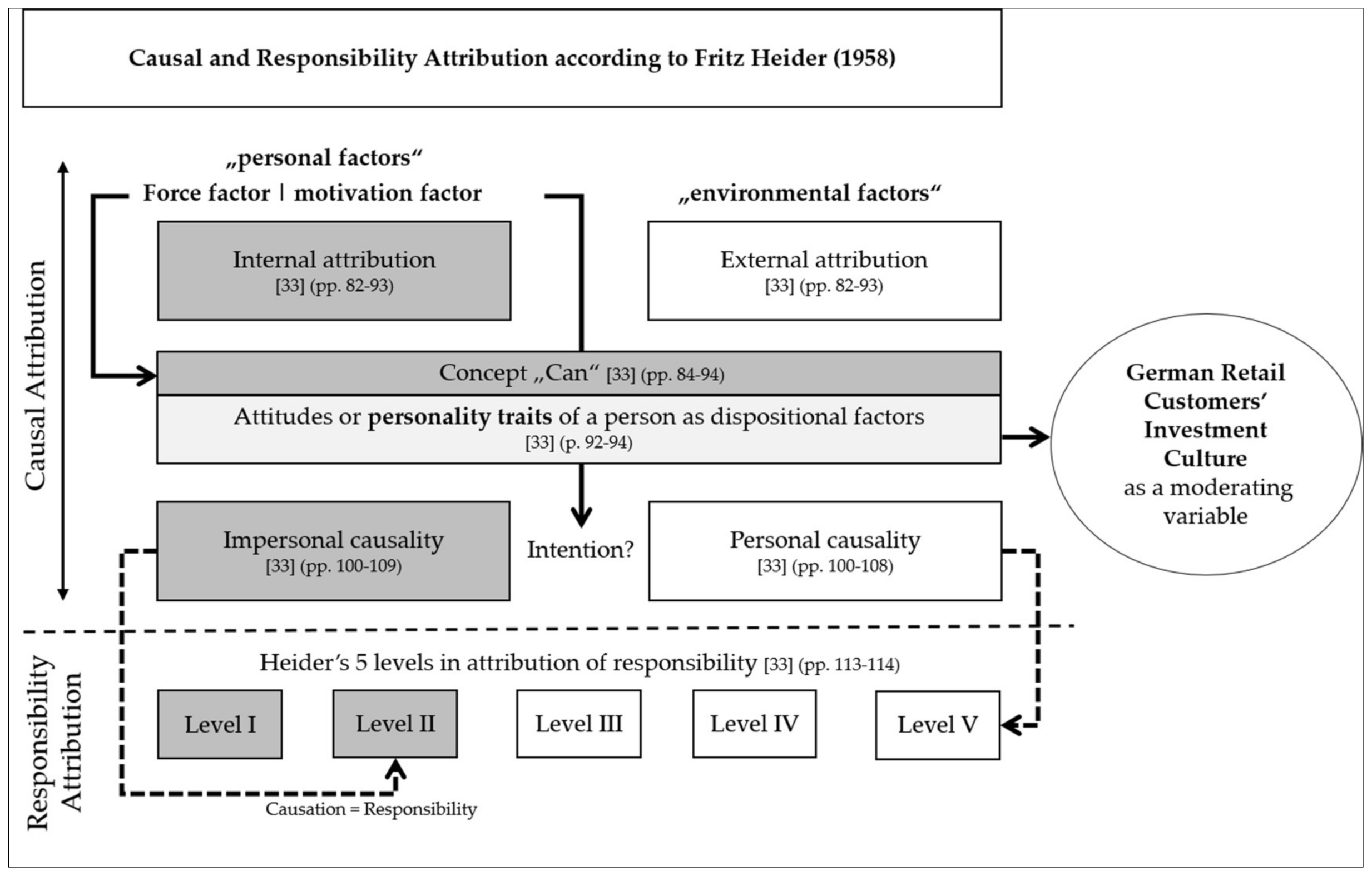

4.1. Causal and Responsibility Attribution Theory

4.2. German Retail Customers’ Investment Culture

“In fact, in our in-house opinion, we had a product on the topic of sustainability and we actively offered it. It was a mixed fund and if this mixed fund matched the client’s risk class, then we offered that fund.”(G bank)

“It’s always a question of how to ask the question. If you ask the question, are they interested in or is sustainability important to them, then many customers will say yes. Whether they accept to take higher risks, if they take sustainability into account that would be another question and that might also have been answered differently by the customers.”(D bank)

“[…] the mentality of the Germans has always been intent on security of investment. When I started here over thirty years ago, there was the savings account and […] there was—no idea—three percent interest on it. The customer had no risk of losing money. […] Nowadays, the mentality of Germans is to seek a risk-free investment. In Germany it was always like that—the largest fortune was in real estate, life insurance and economizer. There, the largest investments were always created for us Germans, completely risk-free, without fluctuations […].”(F bank)

5. Discussion

5.1. Causal and Responsibility Attribution Theory

5.2. German Retail Customers’ Investment Culture

6. Conclusions

6.1. Limitations

6.2. Practical Implications

6.3. Future Research

Acknowledgments

Author Contributions

Conflicts of Interest

Ethical Statement

References

- Renneboog, L.; Ter Horst, J.; Zhang, C. Socially responsible investments: Institutional aspects, performance, and investor behavior. J. Bank. Financ. 2008, 32, 1723–1742. [Google Scholar] [CrossRef]

- Forum Nachhaltige Geldanlagen e.V. (FNG). Marktbericht Nachhaltige Geldanlagen 2016—Deutschland, Österreich und die Schweiz. 2016. Available online: http://www.forum-ng.org/images/stories/Presse/Marktbericht_2016/FNG_Marktbericht2016_online.pdf (accessed on 27 December 2016).

- Schueth, S. Socially Responsible Investing in the United States. J. Bus. Ethics 2003, 43, 189–194. [Google Scholar] [CrossRef]

- Nilsson, J.; Nordvall, A.-C.; Isberg, S. The information search process of socially responsible investors. J. Financ. Serv. Mark. 2010, 15, 5–18. [Google Scholar] [CrossRef]

- Verbraucherzentrale Nordrhein-Westfalen & forsa. Meinungen zu nachhaltigen Geldanlagen: Ergebnisse einer repräsentativen Bevölkerungsbefragung in Nordrhein-Westfalen. 2015. Available online: http://www.verbraucherzentrale.nrw/media238700A.pdf (accessed on 2 January 2017).

- Verbraucherzentrale Nordrhein-Westfalen. Umfrage bei Banken und Sparkassen: Geldanlagen mit ethischen, sozialen und ökologischen Anlagekriterien. 2016. Available online: https://www.verbraucherzentrale.nrw/mediabig/240625A.pdf (accessed on 2 January 2017).

- Eurosif. European SRI Study 2016. 2016. Available online: http://www.eurosif.org/wp-content/uploads/2016/11/SRI-study-2016-HR.pdf (accessed on 2 January 2017).

- RaboDirect & forsa. Meinungen und Einstellung der Bundesbürger zum Thema “Sparen”. 2015. Available online: https://de.statista.com/statistik/daten/studie/163250/umfrage/meinungen-und-einstellungen-zum-thema-uebergewicht/ (accessed on 23 March 2018).

- Sandberg, J.; Juravle, C.; Hedesström, T.M.; Hamilton, I. The Heterogeneity of Socially Responsible Investment. J. Bus. Ethics 2009, 87, 519–533. [Google Scholar] [CrossRef]

- Sparkes, R.; Cowton, C.J. The Maturing of Socially Responsible Investment: A Review of the Developing Link with Corporate Social Responsibility. J. Bus. Ethics 2004, 52, 45–57. [Google Scholar] [CrossRef]

- Wins, A.; Zwergel, B. Comparing those who do, might and will not invest in sustainable funds a survey among German retail fund investor. Bus. Res. 2016, 9, 51–99. [Google Scholar] [CrossRef]

- Schrader, U. Ignorant advice—Customer advisory service for ethical investment funds. Bus. Strategy Environ. 2006, 15, 200–214. [Google Scholar] [CrossRef]

- Hafenstein, A.; Bassen, A. Influences for using sustainability information in the investment decision-making of non-professional investors. J. Sustain. Financ. Invest. 2016, 6, 186–210. [Google Scholar] [CrossRef]

- Pilaj, H. The Choice Architecture of Sustainable and Responsible Investment: Nudging Investors Toward Ethical Decision-Making. J. Bus. Ethics 2015, 81, 1–11. [Google Scholar] [CrossRef]

- Riedel, S. Zielgruppen Nachhaltiger Geldanlagen. In Nachhaltige Geldanlagen. Produkte, Strategien und Beratungskonzepte, 2nd ed.; Faust, M., Ed.; Frankfurt-School-Ver: Frankfurt, Germany, 2008; pp. 157–177. [Google Scholar]

- Zuber, M. Rendite und Qualitätswahrnehmung: Eine Experimentelle Untersuchung zur Anlageberatung. In Marketing und Neue Institutionenökonomik, 1st ed.; Deutscher Universitätsverlag: Wiesbaden, Germany, 2005. [Google Scholar]

- Von Lüde, R. Anlageverhalten auf Finanzmärkten. Wirtschaftsdienst 2013, 93, 328–336. [Google Scholar] [CrossRef][Green Version]

- Martenson, R. How financial advisors affect behavioral loyalty. Int. J. Bank Mark. 2008, 26, 119–147. [Google Scholar] [CrossRef]

- Hockerts, K.; Moir, L. Communicating Corporate Responsibility to Investors: The Changing Role of the Investor Relations Function. J. Bus. Ethics 2004, 52, 85–98. [Google Scholar] [CrossRef]

- Hummels, H.; Timmer, D. Investors in Need of Social, Ethical, and Environmental Information. J. Bus. Ethics 2004, 52, 73–84. [Google Scholar] [CrossRef]

- Keller, H. Praxishandbuch Finanzwissen: Steuern—Altersvorsorge—Rechtsfragen; Springer: Wiesbaden, Germany, 2013. [Google Scholar]

- Uffmann, K. Fehlanreize in der Anlageberatung durch interne Vertriebsvorgaben. JuristenZeitung 2015, 70, 282–292. [Google Scholar] [CrossRef]

- Reittinger, W.J.; Fabianke, D. Beratung—Der Schlüssel zum Erfolg. In Nachhaltige Geldanlagen. Produkte, Strategien und Beratungskonzepte, 2nd ed.; Faust, M., Ed.; Frankfurt-School-Verl: Frankfurt, Germany, 2008; pp. 653–680. [Google Scholar]

- Klöckner, B.W. Systemisch Verkaufen und Beraten in der Finanzbranche: Dauerhaft Erfolgreich Durch Gelingende Kundenbindung; Springer Gabler: Fachmedien/Wiesbaden, Germany, 2014. [Google Scholar]

- Wertpapierhandelsgesetz, Absatz 3, WpHG, Gesetz über den Wertpapierhandel: Abschnitt 6—Verhaltenspflichten, Organisationspflichten, Transparenzpflichten, Wertpapierhandelsgesetz. Available online: https://www.jurion.de/gesetze/wphg/31/?q=wphg&sort=1&from=1%3A140345%2C1%2C20161231 (accessed on 20 February 2017).

- BGH 06.07.1993—XI ZR 12/93 “Anlegergerechte” Beratungspflicht von Banken; Sorgfaltspflicht; “Objektgerechte” Beratung; Anlageberatungspflicht; Prüfung ausländischer Wertpapiere, Bundesgerichtshof 06.07.1993. Available online: https://www.jurion.de/urteile/bgh/1993-07-06/xi-zr-12_93/ (accessed on 12 March 2017).

- Corbin, J.M.; Strauss, A. Grounded theory research: Procedures, canons, and evaluative criteria. Qual. Sociol. 1990, 13, 3–21. [Google Scholar] [CrossRef]

- Strauss, A.L.; Corbin, J.M. Grounded Theory: Grundlagen Qualitativer Sozialforschung; Beltz, Psychologie Verlags Union: Weinheim, Germany, 1996. [Google Scholar]

- Strauss, A.L.; Corbin, J.M. Basics of Qualitative Research: Techniques and Procedures for Developing Grounded Theory, 2nd ed.; SAGE Publications: Thousand Oaks, CA, USA, 1998. [Google Scholar]

- Robrecht, L.C. Grounded Theory: Evolving Methods. Qual. Health Res. 1995, 5, 169–177. [Google Scholar] [CrossRef]

- Jeon, Y.-H. The application of grounded theory and symbolic interactionism. Scand. J. Caring Sci. 2004, 18, 249–259. [Google Scholar] [CrossRef] [PubMed]

- Deutsche Bundesbank. Anzahl der Sparkasseninstitute und Ihrer Inländischen Zweigstellen in den Jahren von 1990 bis 2016. Available online: https://de.statista.com/statistik/daten/studie/6698/umfrage/anzahl-der-sparkassen-und-inlaendischen-zweigstellen-seit-dem-jahr-1990/ (accessed on 9 March 2018).

- BVR. Anzahl der Bankstellen von Volksbanken und Raiffeisenbanken in Deutschland in den Jahren von 1970 bis 2016. Available online: https://de.statista.com/statistik/daten/studie/71934/umfrage/volksbanken-und-raiffeisenbanken---anzahl-der-bankstellen/ (accessed on 9 March 2018).

- Seuring, S.; Gold, S. Conducting content-analysis based literature reviews in supply chain management. Supply Chain Manag. Int. J. 2012, 17, 544–555. [Google Scholar] [CrossRef]

- Flick, U. An Introduction to Qualitative Research, 5th ed.; SAGE: Los Angeles, CA, USA, 2014. [Google Scholar]

- Mayring, P. Qualitative Inhaltsanalyse: Grundlagen und Techniken (12., Neuausgabe, 12., Vollständig Überarbeitete und Aktualisierte Aufl.); Bergstr: Weinheim, Germany, 2015. [Google Scholar]

- Heider, F. The Psychology of Interpersonal Relations, 1958 ed.; Martino Fine Books: Mansfield Centre, CT, USA, 2015. [Google Scholar]

- Raab, G.; Unger, A.; Unger, F. Marktpsychologie: Grundlagen und Anwendung (3., Überarbeitete Aufl.); Springer: Wiesbaden, Germany, 2010. [Google Scholar]

- Weiner, B. Attribution in Personality Psychology. In Handbook of Personality: Theory and Research; Weiner, B., Graham, S., Eds.; Guilford Press: New York, NY, USA, 1990. [Google Scholar]

- Kelley, H.H.; Michela, J.L. Attribution Theory and Research. Ann. Rev. Psychol. 1980, 31, 457–501. [Google Scholar] [CrossRef] [PubMed]

- Baron, R.M.; Kenny, D.A. The Moderator-Mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic, and Statistical Considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

- Barasinska, N.; Schäfer, D.; Stephan, A. Hohe Risikoaversion privater Haushalte bei Geldanlagen. Wochenbericht des DIW Berlin 2008, 75, 704–710. [Google Scholar]

- Popescu, A.; Rafael Smets, F. Uncertainty, Risk-taking, and the Business Cycle in Germany. CESifo Econ. Stud. 2010, 56, 596–626. [Google Scholar] [CrossRef]

- Hafenstein, A. Nachhaltigkeitsinformationen in der Anlageentscheidung: Eine Analyse der Nicht-Professionellen Anleger; Springer: Wiesbaden, Germany, 2016. [Google Scholar]

- Lusardi, A. Household Saving Behavior: The Role of Financial Literacy, Information, and Financial Education Programs. NBER Working Paper No. 13824. 2008. Available online: http://www.nber.org/papers/w13824.pdf (accessed on 9 March 2017).

- Bray, J.; Johns, N.; Kilburn, D. An Exploratory Study into the Factors Impeding Ethical Consumption. J. Bus. Ethics 2011, 98, 597–608. [Google Scholar] [CrossRef]

- Bodur, H.O.; Duval, K.M.; Grohmann, B. Will You Purchase Environmentally Friendly Products?: Using Prediction Requests to Increase Choice of Sustainable Products. J. Bus. Ethics 2015, 129, 59–75. [Google Scholar] [CrossRef]

- Diouf, D.; Hebb, T.; Touré, E.H. Exploring Factors that Influence Social Retail Investors’ Decisions: Evidence from Desjardins Fund. J. Bus. Ethics 2016, 134, 45–67. [Google Scholar] [CrossRef]

- Statman, M. Socially Responsible Investors and Their Advisors. J. Invest. Consult. 2008, 9, 15–26. [Google Scholar] [CrossRef]

- Spiegel; Manager Magazin. Wenn Sie Geldanlagen Tätigen Oder Dieses Beabsichtigen, Wie Würden Sie Sich Selbst als Anleger Beschreiben? Available online: https://de.statista.com/statistik/daten/studie/368563/umfrage/umfrage-in-deutschland-zur-selbsteinschaetzung-des-anlegertyps/ (accessed on 10 March 2018).

- Kahneman, D.; Tversky, A. Prospect Theory: An Analysis of Decision under Risk. Econometrica 1979, 47, 263–292. [Google Scholar] [CrossRef]

- US SIF. The Forum for Sustainable and Responsible Investment. Report on US Sustainable, Responsible and Impact Investing Trends 2016. 2016. Available online: http://www.ussif.org/files/SIF_Trends_16_Executive_Summary.pdf (accessed on 9 March 2017).

- Weber, E.U.; Hsee, C.K.; Sokolowska, J. What Folklore Tells Us about Risk and Risk Taking: Cross-Cultural Comparisons of American, German, and Chinese Proverbs. Organ. Behav. Hum. Decis. Process. 1998, 75, 170–186. [Google Scholar] [CrossRef] [PubMed]

- Hamilton, V.L. Who is Responsible? Toward a Social Psychology of Responsibility Attribution. Soc. Psychol. 1978, 41, 316–328. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reasons for Not Owning Sustainable Financial Products | Percentage of Respondents (Out of 409) |

|---|---|

| So far never dealt with the topic in more detail | 41% |

| So far, no recommendations from the bank or the financial advisor on sustainable financial products | 31% |

| Lack of independent information or advice (for example through consumer advice centers) | 22% |

| Lack of trusted seal of quality for the sustainability of financial products | 20% |

| Risk of sustainable investments perceived as too high | 19% |

| None of the above | 28% |

| Type of Bank | Interviewees and Their Position | Involved in the Design of the Product Range and Forming of in-House Opinion? | |

|---|---|---|---|

| A bank | Co-operative bank | Head of Private Client Advisory Services; Investment Advisor | Yes |

| B bank | Co-operative bank | Head of Retail Bank; Investment Advisor | Yes |

| C bank | Co-operative bank | Head of Department “Freelancer”; Investment Advisor | No |

| D bank | Credit union | Deputy Head of Department; Sales Support; Investment Advisor | Yes |

| E bank | Co-operative bank | Head of Market Division; Personnel Management; Investment Advisor | Yes |

| F bank | Credit union | Head of Financial Consulting; Investment Advisor | Yes |

| G bank | Co-operative bank | Head of Market Division; Personnel Management; Investment Advisor | Yes |

| Risk Classes | Corresponding Financial Products |

|---|---|

| Risk class I: Security-oriented | Savings book; Call money; Fixed deposit; Fixed-interest savings; Building society savings; German government securities; Pension funds with low risk |

| Risk class II: Conservative | Pension funds; Fixed-interest securities; Corporate bonds; Money market funds |

| Risk class III: revenue-oriented | Balanced mix of stocks and bonds and asset diversification with low and higher risk |

| Risk class IV: speculative | DAX stocks; German and international equity funds and pension funds; Certificates |

| Risk class V: very speculative | International stocks; Warrants; Futures; very speculative bonds; Certificates; strategy funds |

| Level | Definition |

|---|---|

| I. | “At the most primitive level the concept is a global one according to which the person is held responsible for each effect that is in any way connected with him or that seems in any way to belong to him.” [37] (p. 113) |

| II. | “At the next level anything that is caused by p is ascribed to him. Causation is understood in the sense that p was a necessary condition for the happening, even though he could not have foreseen the outcome however cautiously he had proceeded. Impersonal causality rather than personal causality as we have defined it, characterizes the judgement of responsibility at this level.” [37] (p. 113) |

| III. | “Then comes the stage at which p is considered responsible, directly or indirectly, for any aftereffect that he might have foreseen even thought it was not a part of his own goal and therefore still not a part of the framework of personal causality.” [37] (p. 113) |

| IV. | “Next, only what p intended is perceived as having its source in him.” [37] (p. 113) |

| V. | “Finally there is the stage at which even p’s own motives are not entirely ascribed to him but are seen as having their source in the environment. […] The causal lines leading to the final outcome are still guided by p, and therefore the act fits into the structure of personal causality, but since the source of the motive is felt to be the coercion of the environment and not p himself, responsibility for the act is at least shared by the environment.” [37] (p. 114) |

| Risk-Taking Propensity of Sustainable Financial Products | Total in Percent (Base: 752 Respondents) | ||

|---|---|---|---|

| No risk | 34% |  | 76% |

| Low risk | 42% | ||

| Medium risk | 21% |  | 24% |

| High risk | 3% | ||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Heinemann, K.; Zwergel, B.; Gold, S.; Seuring, S.; Klein, C. Exploring the Supply-Demand-Discrepancy of Sustainable Financial Products in Germany from a Financial Advisor’s Point of View. Sustainability 2018, 10, 944. https://doi.org/10.3390/su10040944

Heinemann K, Zwergel B, Gold S, Seuring S, Klein C. Exploring the Supply-Demand-Discrepancy of Sustainable Financial Products in Germany from a Financial Advisor’s Point of View. Sustainability. 2018; 10(4):944. https://doi.org/10.3390/su10040944

Chicago/Turabian StyleHeinemann, Kristin, Bernhard Zwergel, Stefan Gold, Stefan Seuring, and Christian Klein. 2018. "Exploring the Supply-Demand-Discrepancy of Sustainable Financial Products in Germany from a Financial Advisor’s Point of View" Sustainability 10, no. 4: 944. https://doi.org/10.3390/su10040944

APA StyleHeinemann, K., Zwergel, B., Gold, S., Seuring, S., & Klein, C. (2018). Exploring the Supply-Demand-Discrepancy of Sustainable Financial Products in Germany from a Financial Advisor’s Point of View. Sustainability, 10(4), 944. https://doi.org/10.3390/su10040944