Analyzing the Coopetition between Tourism and Leisure Suppliers—A Case Study of the Leisure Card Tirol

Abstract

:1. Introduction

- (1)

- What are the motives of suppliers for joining an alliance such as the LCT, and how is the concept of coopetition applied?

- (2)

- What are the effects of participating in a coopetition such as the LCT alliance—for the suppliers as well as for the community?

- (3)

- How satisfied are the suppliers acting in an alliance such as the LCT, and what can others learn from this experience?

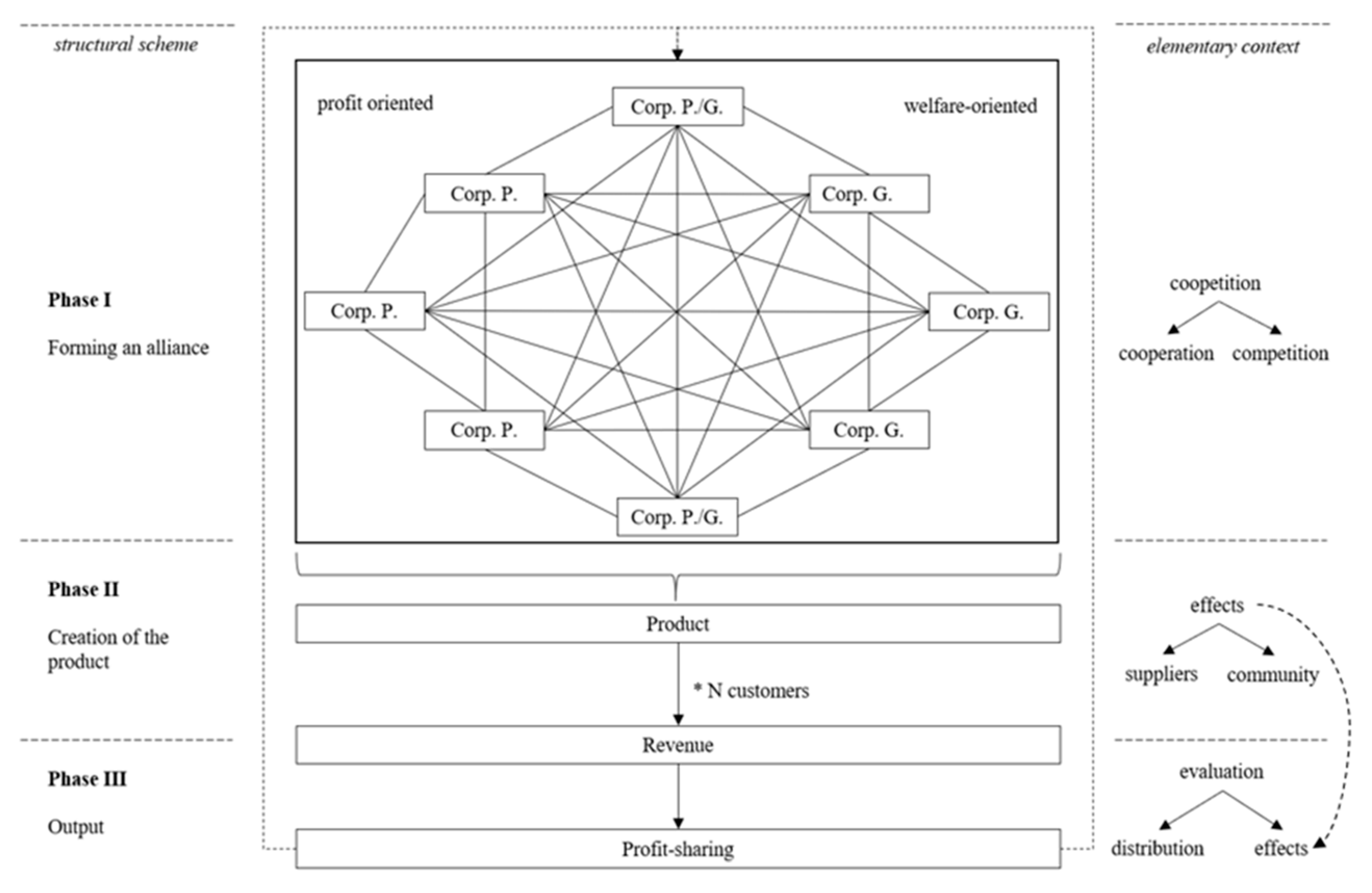

1.1. Literature Review and Analytical Framework

1.1.1. Coopetition and Motives for Coopetition

1.1.2. Effects of the Coopetition and Evaluation

1.1.3. Evaluation of the Coopetition

2. Materials and Methods

3. Results

3.1. Coopetition and Motives for Coopetition

- -

- We have heard very positive references about the LCT. There are several people who work in the museum field and already participate in the project. Furthermore, I also know swimming pool owners who warmly recommend the ticket. In my opinion, it helps in attracting new customers. This is actually the main reason. (MU1)

- -

- Getting additional customers and increasing first-time visits, extending the offer for Tiroleans. (MR3)

- -

- The Elfer is a very small skiing area. Therefore, participating in the LCT project is very inviting and interesting for us. People who would normally visit bigger skiing areas visit the Elfer because they have already purchased the ticket and think “today I will go there”. (MR1)

- -

- We wanted to increase the number of visitors and visits. I also want to mention that residents seldom appreciate the surroundings and the attractions that their area has to offer. Even the Tiroleans, who are well known for being tourism champions, spend their holidays far away and visit museums abroad, but seldom at home. Let us consider the Eiffel tower as an example: most tourists go to Paris to see and visit it, but just a few Parisians have already done that. It happens everywhere in the world. (MU2)

- -

- The number of visitors to our bathing area had dropped dramatically since the introduction of the leisure ticket, because people who purchased the leisure ticket visited businesses that were partners already. This had made a noticeable difference in what concerns the number of visitors. This is why we have joined the LCT network. (SP5)

- -

- Our skiing area has a transport capacity of 4300 people per hour, and our hotels have 5000 beds available. This means that we have an overcapacity and thus a lot of space for day guests. Day visitors need a motivating factor to drive to Gurgl, which can be achieved only by establishing discounted tariffs or creating a combined ticket like the LCT. (MR19)

- -

- Actually, we did not think about it in depth. We act as partners of the LCT because of political will. (MR15)

- -

- The main consideration is a political one. The city of Innsbruck wanted to give families and children a chance to visit the public swimming pools at a reasonable price. (SP2)

- -

- As a municipality, we are primarily responsible for our citizens, and we want to create good offers for them. Our main goal is that sport and leisure activities, especially those for children and teenagers, remain affordable and as multifaceted as possible. It is very important to us that many people do sports. This improves their health and enhances their sense of togetherness. Therefore, these offers, which represent a good supplement, are very important to us. (SP7, ISR2)

- -

- The citizens of Wattenberg wanted to become part of the leisure ticket because it enables them to use other mountain railways as well as our ski lift. (MR23)

3.2. Effects

- -

- Definitely. We also want to focus on families with promotions in magazines or reading circles. The grandstand for families and the LCT grandstand are in the same place. This is much more attractive for families with children. (BP5)

- -

- Yes, of course. They [LCT management] are very present and have clear logo guidelines. We have the logo on our website, too. (MR13)

- -

- For a small business like ours the LCT is a great opportunity, because we only have a very limited budget for marketing at our disposal. Being a part of it is definitely positive. (MR12)

- -

- We obviously did not profit from it [in terms of marketing]. (SP1)

- -

- We have noticed many immediate effects such as increased visitor numbers and new guests. We are not talking about regular visitors here: the number of new guests is increasing, and they are simply looking for places where they can go for free. Whether they return depends on us, and actually, they visit us over and over again. (SP6)

- -

- There are no disadvantages. If an LCT holder comes to us, we can be pretty sure that he would not visit the museum without it. (MU4)

- -

- Yes, it [number of visits] has definitely increased. (MR12)

- -

- The number of visitors has changed positively. Thanks to the LCT, the customer visits the ski area for a shorter time, especially in winter. The customer often comes spontaneously for two hours only, even if the weather or the slopes are not so good. This would not happen without the LCT, and due to this fact, the number of entries have developed positively. (MR9)

- -

- The number of visitors has not changed much. Visitors who used to have our own season pass opted for the LCT, though. (MR7)

- -

- We always get the same amount, it does not make a difference whether we have one or 10,000 visitors. This has had a negative economic impact on us. We get a lump sum, but people do not buy day tickets anymore, because they all prefer to purchase the LCT. (MR12)

- -

- The customer frequency has positively increased, but there is almost no connection with the overall business success. (MU5)

- -

- As I said before, the profits earned with our own season passes have decreased. When we have a great season and nice weather, the LCT has a clearly negative impact, because we could have sold more tickets. Three years ago, the season was terribly rainy: in that case, we were glad that we could count on this income and on the lump sum. To sum up: we have the same number of visitors, but we lose more money due to the noticeably decreasing number of regular tickets we sell. (SP1)

- -

- Yes, the LCT enhances our business success. (MR6)

3.3. Evaluation

- -

- It could always be more. When I have a look at my list: 30 per cent of the entries, but only 12 per cent of the sales. Our wish is to get more money. (SP8)

- -

- We are a very small skiing area with no access system, and for this reason we get paid with a lump sum. This is a bad deal for us, because we had more entries and get a relatively small compensation; the lump sum we get is too low. It was higher in the beginning and we could not report many entries during the first two years. The lump sum was reduced then and now it is not worth the effort. (MR13)

- -

- Yes, we [the LCT] are clearly too cheap, especially compared to other combined passes! Why? Because the performance of the LCT is enormous, compared to its price. (MR2)

- -

- We do not have any objections. (MR7)

- -

- We wanted to make the locals happy and we were able to do it. It did not pay off from a commercial point of view, but our citizens are satisfied. (MR23)

- -

- Yes, we simply expected a good customer stream and it is definitely here—we have it—it has come. (BP3)

- -

- Our expectations were fully fulfilled. (MR4)

- -

- No [answering the question of whether they are satisfied with the coopetition’s effects]. (BP7)

4. Discussion

4.1. Coopetition and Motives of Coopetition

4.2. Effects

4.3. Evaluation

5. Conclusions

5.1. Research Contribution

5.2. Implications

5.3. Limitations and Future Research Directions

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Steinbach, J. Tourismus: Einführung in das Räumlich-Zeitliche System; Oldenbourg: München, Germany, 2003. [Google Scholar]

- Borchert, R. Destination Cards—Eine ordnungspolitische Betrachtung eines Angebots von Destinationen. In Incomingtourismus, 1st ed.; Bochert, R., Ed.; DUV Deutscher Universitäts-Verlag: Wiesbaden, Germany, 2006; pp. 76–96. [Google Scholar]

- Collins, M.F. Leisure Cards in England: An Unusual Combination of Commercial and Social Marketing? Soc. Mark. Q. 2011, 17, 20–47. [Google Scholar] [CrossRef]

- Zoltan, J.; Masiero, L. The relation between push motivation and activity consumption at the destination within the framework of a destination card. J. Destin. Mark. Manag. 2012, 1, 84–93. [Google Scholar] [CrossRef]

- Angeloni, S. A tourist kit ‘made in Italy’: An ‘intelligent’ system for implementing new generation destination cards. Tour. Manag. 2016, 52, 187–209. [Google Scholar] [CrossRef]

- Zoltan, J.; McKercher, B. Analysing intra-destination movements and activity participation of tourists through destination card consumption. Tour. Geogr. 2015, 17, 19–35. [Google Scholar] [CrossRef]

- Pechlaner, H.; Zehrer, A. (Eds.) Destination-Card-Systeme: Entwicklung, Management, Kundenbindung; Linde: Wien, Austria, 2005. [Google Scholar]

- D’Angella, F.; Go, F.M. Tale of two cities’ collaborative tourism marketing: Towards a theory of destination stakeholder assessment. Tour. Manag. 2009, 30, 429–440. [Google Scholar] [CrossRef]

- Guiver, J.; Stanford, D. Why destination visitor travel planning falls between the cracks. J. Destin. Mark. Manag. 2014, 3, 140–151. [Google Scholar] [CrossRef]

- Figini, P.; Vici, L. Off-season tourists and the cultural offer of a mass-tourism destination: The case of Rimini. Tour. Manag. 2012, 33, 825–839. [Google Scholar] [CrossRef]

- Dorn, S.; Schweiger, B.; Albers, S. Levels, phases and themes of coopetition: A systematic literature review and research agenda. Eur. Manag. J. 2016, 34, 484–500. [Google Scholar] [CrossRef]

- Zeng, M. Managing the cooperative dilemma of joint ventures: The role of structural factors. J. Int. Manag. 2003, 9, 95–113. [Google Scholar] [CrossRef]

- Turner, N.; Swart, J.; Maylor, H. Mechanisms for Managing Ambidexterity: A Review and Research Agenda. Int. J. Manag. Rev. 2013, 15, 317–332. [Google Scholar] [CrossRef]

- Bengtsson, M.; Kock, S. Cooperation and competition in relationships between competitors in business networks. J. Bus. Ind. Mark. 1999, 14, 178–194. [Google Scholar] [CrossRef]

- Brandenburger, A.; Nalebuff, B.J. Co-Opetition; Currency Doubleday: New York, NY, USA, 1996. [Google Scholar]

- Lamoreaux, N.R. The Great Merger Movement in American Business, 1895–1904; Cambridge University Press: Cambridge, MA, USA, 1985. [Google Scholar]

- Pate, J.L. Joint venture activity, 1960–1968. Econ. Rev. 1969, 54, 16–23. [Google Scholar]

- Gnyawali, D.R.; He, J.; Madhavan, R. Coopetition. Promises and challenges. In 21st Century Management: A Reference Handbook; Wankel, C., Ed.; Sage Publ.: Los Angeles, CA, USA, 2008; pp. 386–398. [Google Scholar]

- Jorde, T.M.; Teece, D.J. Innovation and cooperation: Implications for competition and antitrust. J. Econ. Perspect. 1990, 4, 75–96. [Google Scholar] [CrossRef]

- Park, S.H.; Russo, M.V. When Competition Eclipses Cooperation: An Event History Analysis of Joint Venture Failure. Manag. Sci. 1996, 42, 875–890. [Google Scholar] [CrossRef]

- Luo, X.; Rindfleisch, A.; Tse, D.K. Working with Rivals: The Impact of Competitor Alliances on Financial Performance. J. Mark. Res. 2007, 44, 73–83. [Google Scholar] [CrossRef]

- Hamel, G. Competition for competence and interpartner learning within international strategic alliances. Strateg. Manag. J. 1991, 12, 83–103. [Google Scholar] [CrossRef]

- Kim, J.; Parkhe, A. Competing and Cooperating Similarity in Global Strategic Alliances: An Exploratory Examination. Br. J. Manag. 2009, 20, 363–376. [Google Scholar] [CrossRef]

- Ritala, P. Coopetition Strategy—When is It Successful? Empirical Evidence on Innovation and Market Performance. Br. J. Manag. 2012, 23, 307–324. [Google Scholar] [CrossRef]

- Dittrich, K.; Duysters, G. Networking as a Means to Strategy Change: The Case of Open Innovation in Mobile Telephony. J. Prod. Innov. Manag. 2007, 24, 510–521. [Google Scholar] [CrossRef]

- Peng, T.-J.A.; Bourne, M. The Coexistence of Competition and Cooperation between Networks: Implications from Two Taiwanese Healthcare Networks. Br. J. Manag. 2009, 20, 377–400. [Google Scholar] [CrossRef]

- Kotzab, H.; Teller, C. Value-adding partnerships and co-opetition models in the grocery industry. Int. J. Phys. Distrib. Logist. Manag. 2003, 33, 268–281. [Google Scholar] [CrossRef] [Green Version]

- Bouncken, R.B.; Gast, J.; Kraus, S.; Bogers, M. Coopetition: A systematic review, synthesis, and future research directions. Rev. Manag. Sci. 2015, 9, 577–601. [Google Scholar] [CrossRef]

- Fong, V.H.I.; Wong, I.A.; Hong, J.F.L. Developing institutional logics in the tourism industry through coopetition. Tour. Manag. 2018, 66, 244–262. [Google Scholar] [CrossRef]

- Weidenfeld, A.; Butler, R.; Williams, A.M. Competition in the Visitor Attraction Sector; Routledge: Abingdon, UK, 2016. [Google Scholar]

- Della Corte, V.; Aria, M. Coopetition and sustainable competitive advantage. The case of tourist destinations. Tour. Manag. 2016, 54, 524–540. [Google Scholar] [CrossRef]

- Kylänen, M.; Mariani, M.M. Unpacking the temporal dimension of coopetition in tourism destinations: Evidence from Finnish and Italian theme parks. Anatolia 2012, 23, 61–74. [Google Scholar] [CrossRef]

- Chim-Miki, A.F.; Batista-Canino, R.M. The coopetition perspective applied to tourism destinations: A literature review. Anatolia 2017, 28, 381–393. [Google Scholar] [CrossRef]

- Išoraitė, M. Importance of Strategic Alliances in Company’s Activity. Intellect. Econ. 2009, 1, 39–46. [Google Scholar]

- Mione, A. When entrepreneurship requires coopetition: The need for standards in the creation of a market. Int. J. Entrep. Small Bus. 2009, 8, 92–109. [Google Scholar] [CrossRef]

- Ritala, P.; Hurmelinna-Laukkanen, P. What’s in it for me? Creating and appropriating value in innovation-related coopetition. Technovation 2009, 29, 819–828. [Google Scholar] [CrossRef]

- Cairo, R. Co-Opetition and Strategic Business Alliances in Telecommunications: The Cases of BT, Deutsche Telekom and Telefonica de Espana. Ph.D. Thesis, London School of Economics and Political Science, London, UK, 2006. [Google Scholar]

- Clarke-Hill, C.; Li, H.; Davies, B. The paradox of co-operation and competition in strategic alliances: Towards a multi-paradigm approach. Manag. Res. News 2003, 26, 1–20. [Google Scholar] [CrossRef]

- Mention, A.-L. Co-operation and co-opetition as open innovation practices in the service sector: Which influence on innovation novelty? Technovation 2011, 31, 44–53. [Google Scholar] [CrossRef]

- Ritala, P.; Sainio, L.-M. Coopetition for radical innovation: Technology, market and business-model perspectives. Technol. Anal. Strateg. Manag. 2014, 26, 155–169. [Google Scholar] [CrossRef]

- Emden, Z.; Calantone, R.J.; Droge, C. Collaborating for New Product Development: Selecting the Partner with Maximum Potential to Create Value. J. Prod. Innov. Manag. 2006, 23, 330–341. [Google Scholar] [CrossRef]

- Lado, A.A.; Boyd, N.G.; Hanlon, S.C. Competition, Cooperation, and the Search for Economic Rents: A Syncretic Model. Acad. Manag. Rev. 1997, 22, 110. [Google Scholar] [CrossRef]

- Quintana-García, C.; Benavides-Velasco, C. Cooperation, competition, and innovative capability: A panel data of European dedicated biotechnology firms. Technovation 2004, 24, 927–938. [Google Scholar] [CrossRef]

- Powell, W.W.; Koput, K.W.; Smith-Doerr, L. Interorganizational Collaboration and the Locus of Innovation: Networks of Learning in Biotechnology. Adm. Sci. Q. 1996, 41, 116. [Google Scholar] [CrossRef]

- M’Chirgui, Z. The economics of the smart card industry: Towards coopetitive strategies. Econ. Innov. New Technol. 2005, 14, 455–477. [Google Scholar] [CrossRef]

- Dagnino, G.B.; Rocco, E. (Eds.) Coopetition Strategy: Theory, Experiments and Cases; Routledge: London, UK; New York, NY, USA, 2009. [Google Scholar]

- Bengtsson, M.; Kock, S. “Coopetition” in Business Networks—To Cooperate and Compete Simultaneously. Ind. Mark. Manag. 2000, 29, 411–426. [Google Scholar] [CrossRef]

- Belderbos, R.; Carre, M.; Lokshin, B. Cooperative R&D and firm performance. Res. Policy 2004, 33, 1477–1492. [Google Scholar] [CrossRef]

- Tether, B.S. Who co-operates for innovation, and why: An empirical analysis. Res. Policy 2002, 31, 947–967. [Google Scholar] [CrossRef]

- Fjeldstad, Ø.D.; Becerra, M.; Narayanan, S. Strategic action in network industries: An empirical analysis of the European mobile phone industry. Scand. J. Manag. 2004, 20, 173–196. [Google Scholar] [CrossRef]

- Spiegel, M. Coopetition in the Telecommunications Industry. In Obtaining the Best from Regulation and Competition; Crew, M.A., Spiegel, M., Eds.; Kluwer: New York, NY, USA, 2005; Volume 47, pp. 93–108. [Google Scholar]

- Garrette, B.; Dussauge, P.; Mitchell, W. Learning from Competing Partners: Outcomes and Durations of Scale and Link Alliances in Europe, North America and Asia. Strateg. Manag. J. 2000, 21, 99–126. [Google Scholar]

- Gomes-Casseres, B. Group versus group: How alliance networks compete. Harv. Bus. Rev. 1994, 72, 62–66. [Google Scholar]

- Möller, K.; Rajala, A. Rise of strategic nets—New modes of value creation. Ind. Mark. Manag. 2007, 36, 895–908. [Google Scholar] [CrossRef]

- Ritala, P. Is coopetition different from cooperation? The impact of market rivalry on value creation in alliances. IJIPM 2009, 3, 39. [Google Scholar] [CrossRef]

- Knudsen, M.P. The Relative Importance of Interfirm Relationships and Knowledge Transfer for New Product Development Success. J. Prod. Innov. Manag. 2007, 24, 117–138. [Google Scholar] [CrossRef]

- Robert, F.; Marques, P.; Le Roy, F. Coopetition between SMEs: An empirical study of French professional football. Int. J. Entrep. Small Bus. 2009, 8, 23–43. [Google Scholar] [CrossRef]

- Morris, M.H.; Kocak, A.; Ozer, A. Coopetition as a Small Business Strategy: Implications for Performance. J. Small Bus. Strategy 2007, 18, 35–56. [Google Scholar]

- Neyens, I.; Faems, D.; Sels, L. The impact of continuous and discontinuous alliance strategies on startup innovation performance. IJTM 2010, 52, 392. [Google Scholar] [CrossRef]

- Peng, T.-J.A.; Pike, S.; Yang, J.C.-H.; Roos, G. Is Cooperation with Competitors a Good Idea? An Example in Practice. Br. J. Manag. 2012, 23, 532–560. [Google Scholar] [CrossRef]

- Le Roy, F.; Sanou, F.H. Does Coopetition Strategy Improve Market Performance? An Empirical Study in Mobile Phone Industry. J. Econ. Manag. 2014, 17, 63–94. [Google Scholar]

- Lorgnier, N.; CheJen, S. Considering coopetition strategies in sport tourism networks: A look at the nonprofit nautical sports clubs on the northern coast of France. Eur. Sport Manag. Q. 2014, 14, 87–109. [Google Scholar] [CrossRef]

- Simmonds, B. Trends in public/private sector partnerships. J. Retail Leis. Prop. 2000, 1, 66–74. [Google Scholar] [CrossRef]

- Shaw, S.; Allen, J.B. “It basically is a fairly loose arrangement … and that works out fine, really”. Analysing the Dynamics of an Interorganisational Partnership. Sport Manag. Rev. 2006, 9, 203–228. [Google Scholar] [CrossRef]

- Levy, M.; Loebbecke, C.; Powell, P. SMEs, co-opetition and knowledge sharing: The role of information systems. Eur. J. Inf. Syst. 2003, 12, 3–17. [Google Scholar] [CrossRef]

- Thomason, S.J.; Simendinger, E.; Kiernan, D. Several determinants of successful coopetition in small business. J. Small Bus. Entrep. 2013, 26, 15–28. [Google Scholar] [CrossRef]

- Babiak, K. Determinants of Interorganizational Relationships: The Case of a Canadian Nonprofit Sport Organization. J. Sport Manag. 2007, 21, 338–376. [Google Scholar] [CrossRef]

- Ritala, P.; Laukkanen, P.H.; Blomqvist, K. Tug of war in innovation—Coopetitive service development. IJSTM 2009, 12, 255. [Google Scholar] [CrossRef]

- Kylänen, M.; Rusko, R. Unintentional coopetition in the service industries: The case of Pyhä-Luosto tourism destination in the Finnish Lapland. Eur. Manag. J. 2011, 29, 193–205. [Google Scholar] [CrossRef]

- Gomes-Casseres, B. Alliance Strategies of Small Firms. Small Bus. Econ. 1997, 9, 33–44. [Google Scholar] [CrossRef]

- Ring, P.S.; Van de Ven, A.H. Structuring cooperative relationships between organizations. Strateg. Manag. J. 1992, 13, 483–498. [Google Scholar] [CrossRef]

- Fenzl, T.; Mayring, P. Qualitative Inhaltsanalyse. In Handbuch Methoden der Empirischen Sozialforschung; Baur, N., Blasius, J., Eds.; Springer: Wiesbaden, Germany, 2014; pp. 543–556. [Google Scholar]

- Dagnino, G.B.; Padula, G. Coopetition strategic: Towards a new kind of interfirm dynamics. Proceeding of the 2th Annual Conference of the European Academy of Management, EURAM 2002, Stockholm, Sweden, 9–11 May 2002; pp. 1–32. [Google Scholar]

- Luo, Y. A coopetition perspective of MNC–host government relations. J. Int. Manag. 2004, 10, 431–451. [Google Scholar] [CrossRef]

- MacLean, J.; Cousens, L.; Barnes, M. Look Who’s Linked with Whom: A Case Study of One Community Basketball Network. J. Sport Manag. 2011, 25, 562–575. [Google Scholar] [CrossRef]

- Webster, C.M.; Morrison, P.D. Network Analysis in Marketing. Australas. Mark. J. AMJ 2004, 12, 8–18. [Google Scholar] [CrossRef]

- Bonel, E.; Rocco, E. Coopeting to Survive; Surviving Coopetition. Int. Stud. Manag. Organ. 2007, 37, 70–96. [Google Scholar] [CrossRef]

- Prévot, F. Coopétition et management des compétences: Coopetition and competence management. Rev. Fr. Gest. 2007, 176, 183–202. [Google Scholar] [CrossRef]

- Stockdale, S.; Williams, S. Leading a small business? No, it’s a rugby club! Ind. Commer. Train. 2007, 39, 339–342. [Google Scholar] [CrossRef]

- Bengtsson, M.; Johansson, M.; Näsholm, M.; Raza-Ullah, T. A systematic review of coopetition: Levels and effects on different levels. In Proceedings of the 13th Annual Conference of the European Academy of Management, EURAM 2013, Istanbul, Turkey, 26–29 June 2013. [Google Scholar]

- Arkes, H.R.; Blumer, C. The psychology of sunk cost. Organ. Behav. Hum. Decis. Process. 1985, 35, 124–140. [Google Scholar] [CrossRef]

- Czakon, W.; Mucha-Kuś, K.; Sołtysik, M. Coopetition Strategy—What is in It for All? Int. Stud. Manag. Organ. 2016, 46, 80–93. [Google Scholar] [CrossRef]

- Oum, T.H.; Park, J.-H.; Kim, K.; Yu, C. The effect of horizontal alliances on firm productivity and profitability: Evidence from the global airline industry. J. Bus. Res. 2004, 57, 844–853. [Google Scholar] [CrossRef]

- Hsieh, Y.-H.; Lin, Y.-T.; Yuan, S.-T. Expectation-based coopetition approach to service experience design. Simul. Model. Pract. Theory 2013, 34, 64–85. [Google Scholar] [CrossRef]

- Dowling, M.J.; Roering, W.D.; Carlin, B.A.; Wisnieski, J. Multifaceted Relationships under Coopetition. J. Manag. Inq. 1996, 5, 155–167. [Google Scholar] [CrossRef]

- Gnyawali, D.R.; Park, B.J.R. Co-opetition between giants: Collaboration with competitors for technological innovation. Res. Policy 2011, 40, 650–663. [Google Scholar] [CrossRef]

- Horch, H.-D. Does Government Financing have a Detrimental Effect on the Autonomy of Voluntary Associations? Evidence from German Sports Clubs. Int. Rev. Sociol. Sport 1994, 29, 269–285. [Google Scholar] [CrossRef]

- Pellegrin-Boucher, E.; Le Roy, F.; Gurău, C. Coopetitive strategies in the ICT sector: Typology and stability. Technol. Anal. Strateg. Manag. 2013, 25, 71–89. [Google Scholar] [CrossRef]

- Walley, K. Coopetition: An introduction to the subject and an agenda for research. Int. Stud. Manag. Organ. 2007, 37, 11–31. [Google Scholar] [CrossRef]

- Mariani, M.M. Coopetition as an Emergent Strategy: Empirical Evidence from an Italian Consortium of Opera Houses. Int. Stud. Manag. Organ. 2007, 37, 97–126. [Google Scholar] [CrossRef]

- Rusko, R. Exploring the concept of coopetition: A typology for the strategic moves of the Finnish forest industry. Ind. Mark. Manag. 2011, 40, 311–320. [Google Scholar] [CrossRef]

- Bouncken, R.B.; Fredrich, V. Coopetition: Performance Implications and Management Antecedents. Int. J. Innov. Manag. 2012, 16, 1250028. [Google Scholar] [CrossRef]

- Eisenhardt, K.M. Building Theories from Case Study Research. Acad. Manag. Rev. 1989, 14, 532. [Google Scholar] [CrossRef]

{kind=link}

| Mountain Railways (N = 23) | Interview Length (min) | Shareholder(s) | Season | Acronym |

| 11er-Lifte Stubai | 28 | Mixed | All | MR1 |

| Axamer Lizum | 35 | Mixed | All | MR2 |

| Bergbahnen Kappl | 20 | Government | All | MR3 |

| Bergbahnen Rosshütte | 75 | Government | All | MR4 |

| Bergbahn Silvretta Galtür | 25 | Mixed | All | MR5 |

| Innsbrucker Nordkettenbahnen | 25 | Mixed | All | MR6 |

| Kellerjoch | 20 | Private | All | MR7 |

| Kühtai | 15 | Mixed | All | MR8 |

| Muttereralm-Bergbahnen | 20 | Government | All | MR9 |

| Patscherkofelbahnen Igls | 30 | Government | All | MR10 |

| Rangger Köpfl | 10 | Government | Winter | MR11 |

| Skilift Kinderland Rinn | 50 | Government | Winter | MR12 |

| Schwannerlift | 21 | Private | Winter | MR13 |

| Serlesbahn Mieders | 10 | Government | All | MR14 |

| Silvrettaseilbahn AG Ischgl | 10 | Private | All | MR15 |

| Ski - & Freizeitarena Bergeralm | 15 | Private | All | MR16 |

| Ski Arlberg | 15 | Private | All | MR17 |

| Skilift Trins | 20 | Government | Winter | MR18 |

| Skiregion Obergurgl-Hochgurgl | 45 | Private | All | MR19 |

| Sonnenberglift Gries | 20 | Private | Winter | MR20 |

| Stubaier Gletscher | 15 | Private | All | MR21 |

| Unterberghornbahn | 20 | Private | All | MR22 |

| Wildstättlift Wattenberg | 25 | Government | Winter | MR23 |

| Swimming Pools (N = 12) | Interview Length (min) | Shareholder(s) | Season | Acronym |

| Hall AG | 35 | Government | Sommer | SP1 |

| Innsbrucker Kommunalbetriebe | 30 | Government | All | SP2 |

| Freizeitzentrum Neustift | 20 | Government | All | SP3 |

| Freizeitzentrum Axams | 25 | Government | All | SP4 |

| Ferienparadies Natterersee | 26 | Private | Summer | SP5 |

| Strandperle Seefeld | 20 | Private | Summer | SP6 |

| Erlebnisbad Schwaz | 15 | Government | Summer | SP7 |

| Schwimmbad Inzing | 20 | Government | Summer | SP8 |

| Schwimmbad Mieders | 15 | Government | Summer | SP9 |

| Familienbad Mutters | 15 | Government | Summer | SP10 |

| Freibad Wattens | 20 | Government | Summer | SP11 |

| Badeanlage Zirl | 12 | Government | Summer | SP12 |

| Ice Skating Rinks (N = 6) | Interview Length (min) | Shareholder(s) | Season | Acronym |

| Eislaufplatz Götzens | 10 | Government | Winter | ISR1 |

| Eislaufplatz Schwaz | 15 | Government | Winter | ISR2 |

| Eislaufplatz Zirl | 12 | Government | Winter | ISR3 |

| Eislaufplat Baggersee, Hötting-West, Sparkassenplatz | 15 | Government | All | ISR4 |

| Wasserkraftarena Innsbruck | 20 | Government | Winter | ISR5 |

| Eislaufplatz Wattens | 10 | Government | Winter | ISR6 |

| Bonus Partners (N = 13) | ||||

| Air 4 You Tandemflüge | 25 | Private | All | BP1 |

| Appelt Juwelen | 15 | Private | All | BP2 |

| Blue Tomato Shop Innsbruck | 10 | Private | All | BP3 |

| Body & Soul | 30 | Private | All | BP4 |

| FC Wacker Innsbruck | 25 | Mixed | All | BP5 |

| Ferdinand Purner Lichtspiele | 10 | Private | All | BP6 |

| Golfacademy Seefeld Reith | 10 | Private | Summer | BP7 |

| Intersport KHT | 25 | Private | All | BP8 |

| Intersport Pittl | 15 | Private | All | BP9 |

| Mountain Soaring | 25 | Private | All | BP10 |

| Oakley Store Innsbruck | 30 | Private | All | BP11 |

| OutdoorCircuit Innsbruck | 15 | Private | All | BP12 |

| Tobias Alexander Meier | 25 | Private | All | BP13 |

| Museums (N = 6) | ||||

| Audioversum Innsbruck | 25 | Private | All | MU1 |

| Glockengießerei Grassmayr | 20 | Private | All | MU2 |

| Museum der Völker | 20 | NPO | All | MU3 |

| Stadtmuseum Innsbruck Museum Goldenes Dachl | 30 | Government | All | MU4 |

| Swarovski Kristallwelten | 25 | Private | All | MU5 |

| Tiroler Landesmuseen | 25 | Government | All | MU6 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Schnitzer, M.; Seidl, M.; Schlemmer, P.; Peters, M. Analyzing the Coopetition between Tourism and Leisure Suppliers—A Case Study of the Leisure Card Tirol. Sustainability 2018, 10, 1447. https://doi.org/10.3390/su10051447

Schnitzer M, Seidl M, Schlemmer P, Peters M. Analyzing the Coopetition between Tourism and Leisure Suppliers—A Case Study of the Leisure Card Tirol. Sustainability. 2018; 10(5):1447. https://doi.org/10.3390/su10051447

Chicago/Turabian StyleSchnitzer, Martin, Maximilian Seidl, Philipp Schlemmer, and Mike Peters. 2018. "Analyzing the Coopetition between Tourism and Leisure Suppliers—A Case Study of the Leisure Card Tirol" Sustainability 10, no. 5: 1447. https://doi.org/10.3390/su10051447