The Relationship between Unbilled Accounts Receivable and Financial Performance of Construction Contractors

Abstract

:1. Introduction

2. Preliminary Study

2.1. Unbilled Accounts Receivable in Construction Contractor Accounting

2.1.1. Payment Method in Construction Projects

2.1.2. Percentage-of-Completion

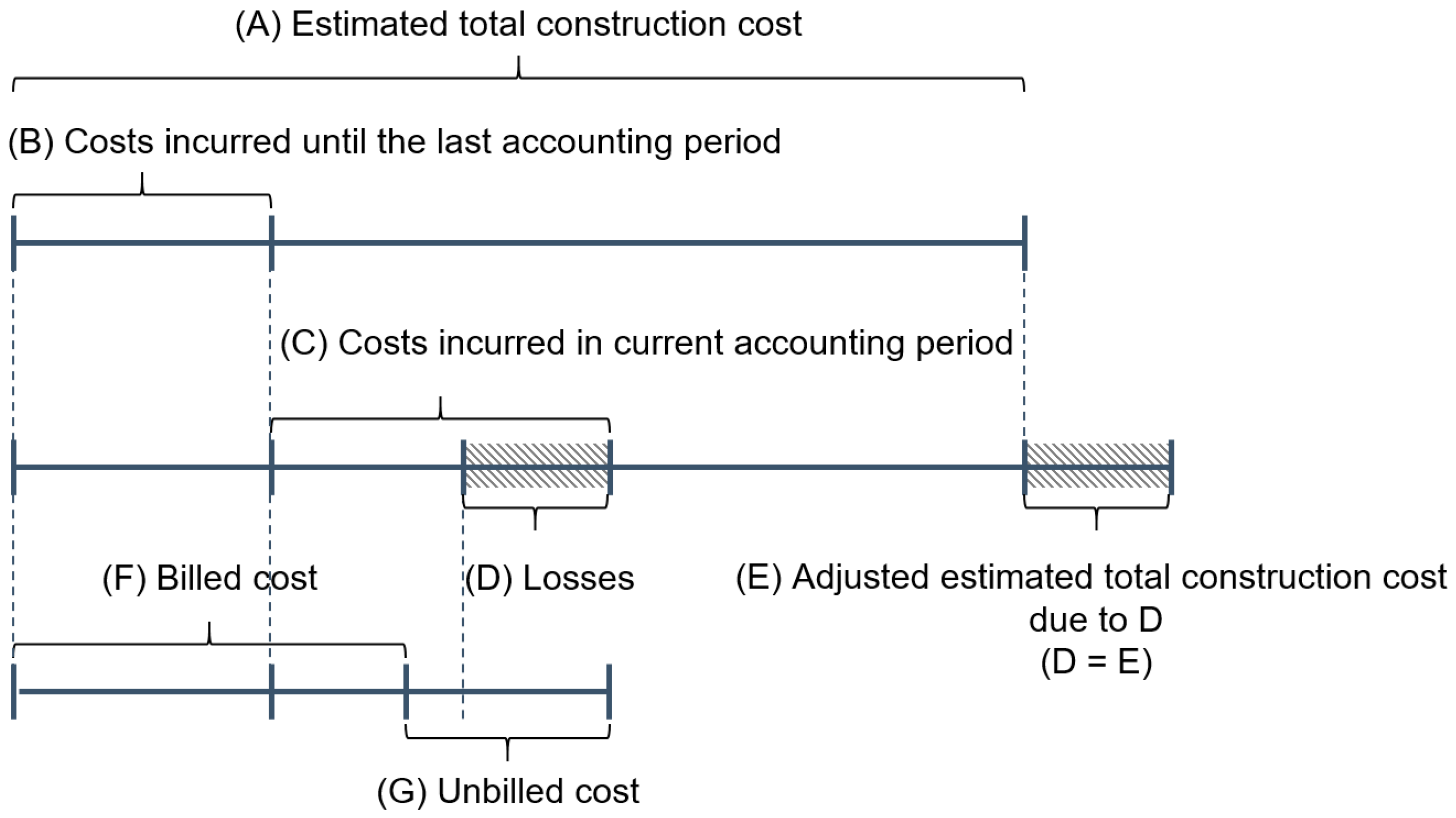

2.2. Causes of Abnormal Profit Recognition

3. Research Hypotheses

4. Research Methods and Data Collection

Analysis Design and Methodology

5. Research Variables

5.1. Average Unbilled Accounts Receivable (AUAR)

5.2. Average Financial Performance

5.3. The Volatility of a Contractor’s Financial Performance

5.4. Contractors’ Market Strategies

6. Data Collection

7. Results and Discussions

7.1. Analysis 1: Relationship between Unbilled Accounts Receivable and Financial Performance Measures

7.2. Analysis 2: Relationship between Unbilled Accounts Receivable and Market Strategy Measures

8. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Bergeron, H.E. Primer for financial management of small consulting firms. J. Manag. Eng. 1994, 10, 28–34. [Google Scholar] [CrossRef]

- Magee, G.L. Financial management primer for new project managers. J. Manag. Eng. 1996, 12, 62–67. [Google Scholar] [CrossRef]

- Dechow, P.M. Accounting earnings and cash flows as measures of firm performance: The role of accounting accruals. J. Account. Econ. 1994, 18, 3–42. [Google Scholar] [CrossRef]

- Robinson, T.R.; Henry, E.; Pirie, W.L.; Broihahn, M.A. International Financial Statement Analysis; John Wiley & Sons: Hoboken, NJ, USA, 2015. [Google Scholar]

- Birnberg, H.G. Communicating the Company’s Operating Performance Data. J. Manag. Eng. 1985, 1, 12–19. [Google Scholar] [CrossRef]

- Jensen, D.A.; Craig, J.W. The impact of TAMRA’88 on US construction accounting practices. Constr. Manag. Econ. 1998, 16, 303–313. [Google Scholar] [CrossRef]

- Halpin, D.W.; Senior, B.A. Financial Management and Accounting Fundamentals for Construction; John Wiley & Sons: Hoboken, NJ, USA, 2009. [Google Scholar]

- Comiskey, E.E.; Mulford, C.W. Contract Reporting and Analysis: Some Guidance for Lenders. Commer. Lend. Rev. 1998, 14, 30–47. [Google Scholar]

- Eldin, N.N. Measurement of work progress: Quantitative technique. J. Constr. Eng. Manag. 1989, 115, 462–474. [Google Scholar] [CrossRef]

- Jung, M.; Ko, S.; Chi, S. A progress measurement framework for large-scale urban construction projects. KSCE J. Civ. Eng. 2018, 22, 2188–2194. [Google Scholar] [CrossRef]

- Acebes, F.; Pajares, J.; Galán, J.M.; López-Paredes, A. A new approach for project control under uncertainty. Going back to the basics. Int. J. Proj. Manag. 2014, 32, 423–434. [Google Scholar] [CrossRef]

- Odeck, J. Cost overruns in road construction—What are their sizes and determinants? Transp. Policy 2004, 11, 43–53. [Google Scholar] [CrossRef]

- Loughmiller, J.; Klintworth, G. Building a business. Nat. Biotechnol. 2011, 29, 307. [Google Scholar]

- Taylor, D.H.; Hensey, M. Financial issues in engineering management: Interview. J. Manag. Eng. 1990, 6, 157–161. [Google Scholar] [CrossRef]

- Calegari, M.J. The effect of tax accounting rules on capital structure and discretionary accruals. J. Account. Econ. 2000, 30, 1–31. [Google Scholar] [CrossRef]

- Russell, J.S. Underwriting process for construction contract bonds. J. Manag. Eng. 1992, 8, 63–80. [Google Scholar] [CrossRef]

- Peterson, S.J. Construction Accounting and Financial Management; Pearson Education: Upper Saddle River, NJ, USA, 2005. [Google Scholar]

- Clough, R.H.; Sears, G.A.; Sears, S.K.; Segner, R.O.; Rounds, J.L. Construction Contracting: A Practical Guide to Company Management; John Wiley & Sons: Hoboken, NJ, USA, 2015. [Google Scholar]

- Dayanand, N.; Padman, R. Project contracts and payment schedules: The client’s problem. Manag. Sci. 2001, 47, 1654–1667. [Google Scholar] [CrossRef]

- International Accounting Standards Board (IASB). IAS 11 Construction Contracts. 2009. Available online: http://www.ifrs.org/issued-standards/list-of-standards/ias-11-construction-contracts/#about (accessed on 10 June 2018).

- Pettigrew, R. Payment under Construction Contracts Legislation; Thomas Telford Ltd.: London, UK, 2005. [Google Scholar]

- Kelly, E.S.; Haskins, S.; Reiter, P.D. Implementing a DBO project. J. Am. Water Works Assoc. 1998, 90, 34–46. [Google Scholar] [CrossRef]

- Sherif, E.; Kaka, A. Factors influencing the selection of payment systems in construction projects. In Proceedings of the 19th Annual Association of Researchers in Construction Management (ARCOM) Conference, Putney, VT, USA, 3–5 September 2003; Volume 1, pp. 63–70. [Google Scholar]

- Trotman, K.T.; Zimmer, I.R. Revenue recognition in the construction industry: An experimental study. Abacus 1986, 22, 136–147. [Google Scholar] [CrossRef]

- Forbes, L.H.; Ahmed, S.M. Modern Construction: Lean Project Delivery and Integrated Practices; CRC Press: Boca Raton, FL, USA, 2010. [Google Scholar]

- Bohusova, H.; Nerudova, D. US GAAP and IFRS convergence in the area of revenue recognition. Econ. Manag. 2009, 14, 12–19. [Google Scholar]

- Herwitz, D.R. Accounting for long-term construction contracts: A lawyer’s approach. Harv. Law Rev. 1957, 70, 449–478. [Google Scholar] [CrossRef]

- Jung, M.; Park, M.; Lee, H.; Kim, H. Weather-Delay Simulation Model Based on Vertical Weather Profile for High-Rise Building Construction. J. Constr. Eng. Manag. 2016, 142, 04016007. [Google Scholar] [CrossRef]

- Chan, S.L.; Park, M. Project cost estimation using principal component regression. Constr. Manag. Econ. 2005, 23, 295–304. [Google Scholar] [CrossRef]

- Carr, R.I. Cost-estimating principles. J. Constr. Eng. Manag. 1989, 115, 545–551. [Google Scholar] [CrossRef]

- Almarri, K.; Blackwell, P. Improving risk sharing and investment appraisal for PPP procurement success in large green projects. Procedia Soc. Behav. Sci. 2004, 119, 847–856. [Google Scholar] [CrossRef]

- Doloi, H.K. Understanding stakeholders’ perspective of cost estimation in project management. Int. J. Proj. Manag. 2011, 29, 622–636. [Google Scholar] [CrossRef]

- Ahuja, V.; Thiruvengadam, V. Project scheduling and monitoring: Current research status. Constr. Innov. 2004, 4, 19–31. [Google Scholar] [CrossRef]

- Irfan, M.; Khurshid, M.B.; Anastasopoulos, P.; Labi, S.; Moavenzadeh, F. Planning-stage estimation of highway project duration on the basis of anticipated project cost, project type, and contract type. Int. J. Proj. Manag. 2011, 29, 78–92. [Google Scholar] [CrossRef]

- Blanc-Brude, F.; Makovsek, D. Construction Risk in Infrastructure Project Finance; EDHEC Risk Institute: Singapore, 2013. [Google Scholar]

- Gunduz, M.; Önder, O. Corruption and internal fraud in the Turkish construction industry. Sci. Eng. Ethics 2013, 19, 505–528. [Google Scholar] [CrossRef] [PubMed]

- Ahiaga-Dagbui, D.D.; Smith, S.D. Rethinking construction cost overruns: Cognition, learning and estimation. J. Financ. Manag. Prop. Constr. 2014, 19, 38–54. [Google Scholar] [CrossRef]

- Lara, J.M.G.; Osma, B.G.; Penalva, F. Accounting conservatism and firm investment efficiency. J. Account. Econ. 2016, 61, 221–238. [Google Scholar] [CrossRef] [Green Version]

- Beach, R.; Webster, M.; Campbell, K.M. An evaluation of partnership development in the construction industry. Int. J. Proj. Manag. 2005, 23, 611–621. [Google Scholar] [CrossRef] [Green Version]

- Van Leeuwen, J.P.; Fridqvist, S. An information model for collaboration in the construction Industry. Comput. Ind. 2006, 57, 809–816. [Google Scholar] [CrossRef]

- Arthur, N.; Chuang, G.C. IAS 7 Alternative Methods of Disclosing Cash Flow from Operations: Evidence on the Usefulness of Direct Method Cash Flow Disclosures; The University of Sydney: Sydney, Australia, 2006. [Google Scholar]

- Lang, M.; Raedy, J.S.; Yetman, M.H. How representative are firms that are cross-listed in the United States? An analysis of accounting quality. J. Account. Res. 2003, 41, 363–386. [Google Scholar] [CrossRef]

- Givoly, D.; Hayn, C.K.; Katz, S.P. Does public ownership of equity improve earnings quality? Account. Rev. 2010, 85, 195–225. [Google Scholar] [CrossRef]

- Drew, D.; Skitmore, M.; Lo, H.P. The effect of client and type and size of construction work on a contractor’s bidding strategy. Build. Environ. 2001, 36, 393–406. [Google Scholar] [CrossRef] [Green Version]

- Ofori, G. Frameworks for analysing international construction. Constr. Manag. Econ. 2003, 21, 379–391. [Google Scholar] [CrossRef]

- Montgomery, D.C.; Peck, E.A.; Vining, G.G. Introduction to Linear Regression Analysis; John Wiley & Sons: Hoboken, NJ, USA, 2012. [Google Scholar]

- Ministry of Land, Transport and Maritime Affairs (MLTMA). Framework Act on the Construction Industry, Ministry of Government Legislation of Korea. 2010. Available online: http://www.moleg.go.kr/english/korLawEng;jsessionid=Q9j5zCeft3Yrl5nW1NGHS81eBin1bQ2DRYqsjspNfiW8HLIlZa6QYh13Z4spPH8b?pstSeq=52559&pageIndex=6y (accessed on 10 June 2018).

{kind=link}

{kind=link}

| Research Variables | Min | Mean | Max |

|---|---|---|---|

| Revenue (AMSs) | |||

| by Region | |||

| 1. Domestic Market | 25.8% | 82.6% | 100.0% |

| by Project Type | 25.8% | 82.6% | 100.0% |

| 2. Infrastructure | 0.0% | 26.2% | 63.8% |

| 3. Building and Residence | 0.0% | 53.1% | 100.0% |

| 4. Plant and Industrial Facility | 0.0% | 20.7% | 100.0% |

| Operating Profit | |||

| 5. Average (AOP) | −19.8% | −0.4% | 12.1% |

| 6. Standard Deviation (SDOP) | 0.4% | 7.7% | 25.3% |

| 7. Maximum Change (MCOP) | 0.0% | 7.7% | 32.1% |

| Cash Flow from Operating Activities | |||

| 8. Average (ACF) | −13.4% | 2.7% | 45.3% |

| 9. Standard Deviation (SDCF) | 0.9% | 14.4% | 86.4% |

| 10. Maximum Change (MCCF) | 0.0% | 13.0% | 48.2% |

| Unbilled Account Receivable | |||

| 11. Average (AUAR) | 0.4% | 15.1% | 36.0% |

| Variables | Statistics | |

|---|---|---|

| Pearson’s R | p-Value | |

| Operating Profit | ||

| 1. Average (AOP) | −0.443 | 0.001 |

| 2. Standard Deviation (SDOP) | 0.359 | 0.008 |

| 3. Maximum Change (MCOP) | 0.280 | 0.034 |

| Cash Flow from Operating Activities | ||

| 4. Average (ACF) | −0.357 | 0.008 |

| 5. Standard Deviation (SDCF) | 0.191 | 0.115 |

| 6. Maximum Change (MCCF) | 0.212 | 0.095 |

| Variables | Statistics | |

|---|---|---|

| Pearson’s R | p-Value | |

| by region | ||

| 1. Domestic | −0.507 | 0.001 |

| by construction type | ||

| 2. Infrastructure | −0.476 | 0.001 |

| 3. Building and residence | −0.312 | 0.037 |

| 4. Plant and industrial facility | 0.219 | 0.101 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jung, M.; You, S.; Chi, S.; Yu, I.; Hwang, B.-G. The Relationship between Unbilled Accounts Receivable and Financial Performance of Construction Contractors. Sustainability 2018, 10, 2679. https://doi.org/10.3390/su10082679

Jung M, You S, Chi S, Yu I, Hwang B-G. The Relationship between Unbilled Accounts Receivable and Financial Performance of Construction Contractors. Sustainability. 2018; 10(8):2679. https://doi.org/10.3390/su10082679

Chicago/Turabian StyleJung, Minhyuk, Shira You, Seokho Chi, Ilhan Yu, and Bon-Gang Hwang. 2018. "The Relationship between Unbilled Accounts Receivable and Financial Performance of Construction Contractors" Sustainability 10, no. 8: 2679. https://doi.org/10.3390/su10082679

APA StyleJung, M., You, S., Chi, S., Yu, I., & Hwang, B.-G. (2018). The Relationship between Unbilled Accounts Receivable and Financial Performance of Construction Contractors. Sustainability, 10(8), 2679. https://doi.org/10.3390/su10082679