Abstract

Impact investing pursues the dual goals of creating socio-economic value for the marginalized, and ensuring net positive financial returns. Impact investing firms achieve their goals through their investments in projects and enterprises which create both social and commercial values. The primary aim of this article is to contribute to our understanding of the process of impact investing, particularly with respect to issues related to aligning impact investing and investee social enterprise goals. The research method employs case-based research methodology. The data consist of six cases of impact investing and their investee social enterprises. In addition, the data involve interviews with experts from the field of impact investing. The findings are that: (1) Social mission plays an important moderating role in the inter-organizational relationship between the impact investor and the investee social enterprise, (2) and an emphasis on due diligence, sector specialization, and communication increases the likelihood of investment while (3) social impact measurement and reporting and frequent engagement increase the likelihood of post-investment alignment. The key contribution of this article is that impact investing (unlike venture capital) is influenced by the ability of its investee to create social value, which plays an important role in the inter-organizational relationship between investor and investee. Furthermore, similar to industry specialization in the for-profit investing, social sector specialization is equally relevant for alignment and returns.

1. Introduction

Impact investing is a relatively recent term, adopted in 2007 [1], that implies the practice of investing in enterprises with the motivation of creating social and environmental value and in which the principal is repaid potentially with a return [2]. Most researchers define impact investing as an investment process for maximizing social and commercial benefits by using venture capitalist methods [3,4,5]. There has been a tremendous growth of impact investing funds, which are projected to exceed 500 billion USD by 2023 [6]. The effectiveness of an impact investing firm is primarily understood by its ability to generate social and commercial value [7,8,9]. The effectiveness of impact investing depends upon the social and financial success of its investments, which is tied to its investees [9]. During impact investing, the investee social enterprise is the major instrument through which social and financial returns are generated. The present scholarship on impact investing is nascent, focusing on the concept [10] or typologies [11]. Despite growing investments in impact investing, scholars have not explored the real operational factors and strategies within impact investing that explain the working of impact investing firms.

The relationship between the impact investor and the investee social enterprises forms the major instrument that drives the legitimacy of the impact investing field by creating social and commercial value. Therefore, it is important to understand the inter-organizational relationship between impact investing and investee social enterprise. Such a study would help in understanding the dynamics involved in impact investing at the firm (or practice level); institutional pressures it experiences and help us understand how impact investment is different from traditional commercial investments like venture capital.

Castellas, Ormiston, and Findlay [12] state that impact investing and the social entrepreneurship ecosystem are struggling to become mainstream due to the lack of standardization and replication of social impact measures. Gregory [13] cites multiple risks within the impact investing sector which would potentially reduce the financial returns. For example, a emphasis on social returns increases the risks on expected financial returns. Similarly, impact-investors’ greater communication on social returns while in practice emphasizing on financial returns increases the risks on external legitimacy. Roundy et al. [14] cite that social entrepreneurs fear the risk of mission drift when seeking funds from impact investors. Given that the field of impact investing is nascent and lacks a sufficient knowledge base, and given that impact investing draws its legitimacy from its ability to create social and financial value through its investments, it is important to understand the process of impact investing and the dynamics involved between impact investors and investee social enterprises at the inter-organizational level and how they manage their relationship.

This article further explores the factors that enable inter-organizational alignment between impact investors and investee social enterprises. One can ask what outcomes can be observed at the inter-organizational level when these goals are not aligned, in addition to how organizations can achieve long-term inter-organizational alignment. This study employs an institutional logic framework to explore and theorize the inter-organizational relationship between impact investors and investee social enterprises, and explore the strategies which can increase the effectiveness of impact investing.

2. Theoretical Framing

The institutional logics framework has been consistently used by researchers to understand hybrid organizations. To understand the impact investing process, the inter-organizational relationship between impact investors and investee social enterprises, the study employs the institutional logics framework.

2.1. Competing Logics as a Theoretical Framework for Impact Investing

Thornton, Ocasio, and Lounsbury [15] define institutional logic as “the socially constructed, historical patterns of material practices, assumptions, values, beliefs and rules, by which individuals produce and reproduce their material subsistence, organize time and space, and provide meaning to their social reality”. Logics are stratified layers of multiple institutions that nudge the decisions of individuals within organizations and impact long-term organizational strategies and identities. Each logic is associated with a unique mode of rationalization, defining the appropriate relationship between subjects, practices and objects [16]. The concept of institutional logics connects field-level values and beliefs with action at all organizational levels [17]. Studies on institutional logics have discussed the links between logics, organizational forms, organizational products and organizational practices [15].

The scholarship in impact investing demonstrates that social value generation and income generation are competing activities, in which the favoring of earnings over social value leads to mission drift, and could result in a loss of legitimacy [18,19]. The impact investment funds must manage the competing missions of social value generation as well as satisfy their financial goals [19,20]. Within literature concerning social entrepreneurship, institutional logics are an established theoretical frame for studying competing goals found within social enterprises. Many studies have examined the tensions and motivations of social mission drift between social and commercial activities via competing logics [21,22,23] among social enterprises. The two most prominent competing logics used to analyze hybrid organizations are social logic and commercial logic [21,24,25].

Charitable firms represent one extreme at the end of the investing continuum which represents the social-only motive [26,27]. The motivations of charitable firms are to maximize social value creation through funding [28]. This article defines social logic as the motivation to address the social requirements of a community (or poor, or disenfranchised, or marginalized) and possess a well-articulated social mission. Actors within charities are driven by social logic to maximize social value. Social logic is the underlying institutional structure that affords legitimacy to social enterprises and impacts investment firms (ibid.) (See Table 1).

Table 1.

Institutional logics acting on impact investing and investee social enterprise.

Venture capital represents the other end of the investing continuum, which represents the profit-only motive [26,27]. Venture capitalist firms invest in firms which have a great potential for high financial returns in the form of strong, existing possibilities (via equity sell-off) or provide IPO opportunities [29,30,31]. The performance of venture capitalist firms and their investees is purely measured based on their potential to create financial returns, and the selection process is purely driven by financial return expectations [32]. Venture capitalist organizations bring operational efficiency and provide capital through a board position, decision making and market development. Pache and Santos [21] conceptualize commercial logic as norms, practices and values with a clear goal of increasing dividends and rewarding efficiency and control (see Table 1). Purely commercial logic drives the investment decisions of venture capitalist investors.

Organizations with hybrid goals experience tensions when actors make decisions that are motivated by their commitments to specific institutional logics [15]. Such tensions ultimately influence organizational performance [15,33]. Studies on the tensions among the hybrid organisations have primarily investigated them applying the institutional logic framework at the intra-organizational level [22,23]. This study applies the institutional logic framework at the inter-organisation level exploring the tensions between the impact investor and investee social enterprise and explore the strategies which may sustain their inter-organisational collaboration.

The stabilization of intra-organizational institutional logics among social enterprises is well researched [21,22]. This article applies the competing institutional logics framework to understand how the inter-organizational relationship between impact investing firms and investee social enterprises is sustained in achieving their goals, as both the impact investing firms and investee social enterprises are exposed to strong social and commercial logics [18,21,34].

2.2. Inter-Organizational Alignment among Impact Investors

Inter-organizational alignment between two organizations is a co-operative relationship based upon the mutual interests created from the requirements of resource dependency, managing costs and reducing uncertainty [35,36]. Organizations engage in inter-organizational relationships with the motivation of creating value that far exceeds what organizations can achieve individually [37].

Huybrechts and Nicholls [36] illustrate that actors at dominant positions navigate the conversation among organizations in inter-organizational alignment. They conclude that the legitimacy and resource deficit both dominate the motivations of alignment, and those in the dominant position are more likely to steer the outcome and determine the longevity of the alignment. The literature on venture capital prominently suggests that the dominant players are the venture capitalists, as they provide capital. The impact investors seek legitimacy by creating both social and commercial value by investing in social enterprises concerning venture capitalists. This study explores how dominant characteristics influence the inter-organizational alignment.

The impact investor and its investee social enterprise share the same set of institutional logics, as both share the identical goal of creating social change via the market-inspired solution. The institutional logics influence both the organizations and their partners [38]. The sources of legitimacy for the two (invest and investee) differ; both the investor impact investing firms and investee social enterprises must pursue their respective social and commercial goals. In doing so, they are exposed to competing institutional logics, which could result in tensions [18,21,34]. Di Domenico et al. [39] suggest that factors such as ownership structure, goals, governance and accountability play important roles in sustaining the inter-organizational alignment. These factors have promise for managing post-alignment collaboration, but lack a deeper understanding of how firms with competing logics could align when any conflicts arise. In this context, this study explores the inter-organizational relationship between impact investors and investee social enterprises, the causes of misalignment and strategies for alignment at the inter-organizational level.

3. Research Method

Impact investing is an emerging research area; therefore, the case study method was favored to explore the research question and to generate theoretical propositions [40]. The article uses a comparative multiple-case-study approach, as this method closely links empirical observations with existing theories. The multiple-case-study approach helps to reveal differences and similarities among the cases, and to bring the findings into the broader picture [41,42]. This approach is useful to reduce researcher biases, and to increase the chances of building empirically valid theories [42].

3.1. Case Selection and Data Collection

To answer the research questions, this article analyzes six heterogeneous cases of impact investment firms operating within India. The cases were selected based on information-oriented sampling, as diverse cases reveal more information than do similar cases [41]. The cases were selected to increase the diversity of the data studied, while replicating selected elements (related to the social and commercial motivations of impact investors) as closely as possible [41,42].

The selected cases identified themselves as impact investing firms. The websites indicate a clear mission statement identifying as social impact first investment funds. A group of industry experts was consulted as part of the case selection, and they recognized the selected organizations as important actors in the field of impact investment in India.

All selected organizations are older than five years, and have a dedicated investment team and advisory board members. Following the Eisenhardt approach, the cases were selected based on their social and commercial goals. In addition to the selected impact investment firms, the study contacted also the investee social enterprises mentioned on the website of the impact investor. Table 2 provides the summary of the data sources.

Table 2.

Summary of the data sources used in the study.

The cases were written using both the primary and secondary data [42]. For the primary data, we conducted interviews. We triangulated and verified primary interviews using the secondary data. For the secondary data, we gathered information from the reports published on the websites of the selected cases and certain think tanks active in impact investing in India (see Table 2). The think tanks included organizations such as the German Development Bank office in India, the European Venture Philanthropy Association (EVPA), the Asian Venture Philanthropy Association (AVPA), Okapi Consulting, and the National Association of Social Entrepreneurs in India (NASE). A summary of the sources of the data collected for the construction of cases can be found in Table 2.

In addition to the data gathered from public sources, 29 interviews were conducted with company members and local cooperation partners to substantiate and complete the information regarding the research questions. The interviewee list included the fund managers who are responsible for making the investment decisions, impact reporters, CEOs of investee organizations, investors of impact investing organizations and experts in the field. The interviews occurred between February 2013 and May 2015. All interviews were conducted in English, and lasted between 20 and 70 min, with an average duration of 45 min. One working day took place prior to the interview; the interview guideline was sent to all interviewees by email. The evidence from the interview data and secondary documents helped in triangulating the data for internal validity. Table 3 represents cases of the impact investors and their investee social enterprises with varying degrees of social and commercial logics.

Table 3.

Summary of the selected case studies.

3.2. Data Analysis

This article follows the method of Gibbert et al. [41] to establish methodological rigor to ensure validity and reliability. The article employed the competing logics lens to explore the factors of the inter-organizational alignment between the two [43]. To explore the relationships between impact investors and investee social enterprises, the article conducted pattern matching in which the article compares the findings with previous research and engages in cross-case data analysis. Furthermore, to ensure construct validity, the article uses data triangulation [44,45,46] comparing the claims of the informants with a collection of archival data, publicly available reports, and Twitter data. The article uses six cases, each consisting of an investor and an investee. The external validity was addressed through multiple case selection, investee interviews and expert interviews [42]. Data collection and data analysis were conducted simultaneously. To understand the competing forces at the inter-organizational level, the article studies both successful alignments in the relationship between investor and investee, in addition to examples of tension and failure.

4. Cross-Case Analysis

In this section, the article compares the cases with one another to understand the factors which could shift the inter-organizational alignment between impact investors and investees. It explores the strategies for addressing non-alignment issues. The article refers to each case by its acronym, as introduced in Table 3.

4.1. Expectations of Social Impact Investors and Investees

4.1.1. Investor Expectations

The investee social enterprise is the only instrument through which impact investors can ensure the generation of social and commercial benefits. The ideal method for obtaining social and commercial benefits is to invest in those social enterprises which have a strong social mission and earned income activities. Impact investors select their investees with the expectation of creating social impact and earning financial benefits. Impact investor AF specifically examined investing in early-stage social ventures, which can scale and create financial value while solving complex social problems.

‘Redefining the parameters of blockbuster success—a return of 5 to 10 times on invested capital …’ while ‘Investing in enterprises that gainfully engage rural and economically weaker sections of the populations either as producers, users or owners to deliver commercial returns.’(CEO AF)

One of the primary motivations of impact investors is making investments among social enterprises that create ‘measurable, scalable’ social impact. CSF’s social mission focuses on addressing primary education in schools in India. Its investment decisions look for investee social enterprises addressing specifically the primary education sector in addition to the inefficiencies present within local public schools in India. They engage together with their investees to create solutions that can be generalized throughout India.

‘We’ve done that [seek partners who wants to create systemic (normative) change through innovation, documenting and testing] with the India school leadership institute. We’ve just recently repeated that process with another institution we started called the education alliance. This is an organization that’s focused on public/private partnerships in education.’(CSF MD)

4.1.2. Investee Expectations

Social enterprises have greater complexity due to competing goals compared with normal, for-profit models. There are insufficient examples of commercially successful social enterprises for traditional financial institutions (banks, private equity firms) to make investments in them. However, to operate and sustain, social enterprises require capital. Based on the following quotation, it appears that impact investment is potentially a viable capital for social enterprises.

‘It was just me and a piece of paper, right. There was nothing on the ground’…’I needed five million dollars to just get started in the first place’…’there were very limited options [of investment], at that time, AF, I just came across them somewhere.’(Investee AF)

In addition to capital, investee social enterprises expect their investors to acknowledge and value the social value created by their enterprise. The following quotation illustrates the importance of ‘social value creation’ and valuation during the investment process.

‘Impact investors should be putting a premium on impact, right? In terms of market valuation?’(Investee AF)

The following quotation illustrates the requirements of the investees. Investee social enterprises seek also an investment of time and knowledge from their investors. The social entrepreneurs have a proper understanding of the social sector; however, they often lack the commercial skills needed to run a venture that has an earned income social business model.

“‘We started our collaboration with a commitment that [the investors] are going to help us in providing all these [business skills], technical inputs and expertise.’(Investee USV)

Table 4 provides a summary of the relative dominance of social and commercial logics among the impact investing firms and investee social enterprises chosen for this study. It also provides their motivations which are driven by the dominant institutional logics.

Table 4.

Summary of the logics with impact investment firms and investee social enterprises.

The competing institutional logic framework assists in making sense of the impact investing strategies pursued by the impact investors, and also assists in making critical inferences.

4.2. Outcome of Non-Alignment of Investor—Investee Organizational Goals

The following section discusses the causes and effects of the non-alignment of organizational logics. All of the interviewees indicated that circumstances often exist in which social and commercial expectations between investors and investees are not aligned. It is possible that with extreme disagreements, the relationship could break down. From the data, the legal, contractual agreements used by AF and USF with their investee social enterprises are stringent on corporate governance and environment social norms. The following quotation illustrates the importance given to ESG factors by impact investors.

‘If any of the Conditions Precedent mentioned in Annexure 7 including the investor code on ESG norms is not fulfilled or satisfied by the Long Stop Date, the Investors shall have the right to terminate this Agreement.’(AF legal agreement document)

However, as illustrated in the following quotation, investees feel that the investor’s expectations regarding corporate governance are not practically implementable on the ground.

‘They said you will never pay a bribe to a government official. I was laughing about it, because you know how the business is done in India.’(Investee USF)

The following quotation further illustrates the non-alignment between investors and investees. It reveals that investor expectations were not matched by investee actions. This could potentially result in crises of the legitimacy of impact investors.

‘[The investees] were not following the minimum wages and they were not taking care of [employment] needs in terms of proper working condition as agreed upon.’(Manager AF)

While the severe variation (agreed terms and conditions) could severely damage the legitimacy of the impact investor, making investee liable for variations from the contract could potentially restrict their entrepreneurial bricolage. The following quotation illustrates how investors could nudge the investees towards commercials goals, which could potentially undermine the social value performance of the investees.

‘In the first meeting, they were asking me how will you give us an exit, I know of impact investors who also put such clauses that, in seven years or five years, you [the social entrepreneur] are forced to back the equity [return the investment] from the impact investor.’(Investee USF)

A greater emphasis on commercial goals could potentially increase tensions and misalignment. Investees are forced to dilute their focus on the social mission of their social enterprise at the cost of commercial benefits. The consequences of these differences often result in management restructuring, and in extreme cases, based on the contractual details, a change in management and of the CEO of the investee social enterprise. Increasing disagreements between investor and investee could result in investor exits or investee management change. Investor exits could lead to organizational demise.

4.3. Pre-Investment Strategies for Effective Alignment

Investees should pursue some pre-investment actions to increase the likelihood of alignment. In the following section, the article explores the pre-investment strategies to effectively align the impact investor and investee social enterprise motivations and goals.

4.3.1. Due Diligence on Organizational Missions, Goals, and Actions

Although due diligence among venture capital firms is an established process, the due diligence among impact investors is not the same as that among venture capitalists. Among venture capital firms, the due diligence process is linear, and the primary focus is on profitability, scalability, market acceptance and a profitable exit opportunity.

The following quotation illustrates that during the due diligence process, both the investor and investee reflect on each other’s social and commercial missions, goals and actions. Proper articulation of social and commercial goals, and how the investor-investee firms will organize their interaction to achieve their stated goals, is one of the most important elements in the due diligence process.

‘When an investment manager is doing the due diligence—even before the investment committee approves the investment—we go through a very detailed environment and social due diligence. We […] look at what the enterprise has done so far when it comes to environment and social impact. Going forward [we look at the] metrics that they would be measuring for us. [Only then do we] decide if we go ahead with the investment.’(Investor AF)

Respondents indicated also that to effectively manage the complexities arising after impact investment, due diligence should assess the cultural convergence of the perspective investee organizations. One of the impact investors interviewed refers to cultural convergence as the shared organizational goals (social and commercial) and characteristics.

‘There maybe trade-offs at different times, on which markets you go after, I’m sure there will there will be kinds of conflicts. But what’s important is, that you choose entrepreneurs that you believe sort of have this similar DNA to what you have. If you select well there, then you reduce amount of conflicts.’(Investor USF)

During the due diligence stage, USF and AF both strive to transparently communicate their expectations on exit opportunities and scalability with the investee social enterprises. Once social, commercial and cultural commonalities between the investor and investee have been established, the probability of post-investment non-alignment significantly decreases between the investor and the investee. Transparency in communication would reduce the risks of inter-organizational breakdown arising due to competing logics.

4.3.2. Specialization and Sector Knowledge

A unique data pattern revealed that impact investors which specialize in one particular field, such as microfinance (LC), fair wages (USF), and primary education (CSF), find it much easier to attain an alignment of organizational goals between themselves and their investee social enterprises.

For example, CSF prides themselves on being the sector expert on primary education with a social mission. Their in-depth knowledge of the sector narrows the investment funnel, focusing only on the education sector, which is fully aligned with CSF’s mission of delivering highly efficient, repeatable and measurable impact. The following quotation illustrates that specialization potentially increases the unique capabilities of the investor, and the probability of influencing policy decisions at the government level. Influencing public sector policy for the betterment of society has a disruptive social impact.

‘We work in partnership with the municipal government’s schools we take over, and put in our own staff and teachers and run the schools according to our methodology. But the idea is then to transfer these acquired leanings to the rest of the government schools. So we do research and report our hypothesis, and then through policy advocacy to see that the effective practices are being implemented by the government.’(Investee CSF)

In addition to specialization, greater sector knowledge potentially increases the financial returns on investment. For example, LC has developed expertise on microfinance in India and has executed two successful exits from its investments in the microfinance sector. The following quotation illustrates the depth of sector knowledge, execution plan, competition and the possible return of investment.

‘In microfinance actually it’s a very well documented model now, so we really can estimate all of these standard things, what should be the ideal holding period, what should be the stage at which you invest and what are the stages at which it should exit, for mainstream players.’(Investor LC)

This deep understanding of the sector level helps LC to manage reasonable financial expectations and risks. Impact investors that cover a broader portfolio of sectors tend to be less knowledgeable about the sector specificities. Based upon the above quotation, one could infer that the probability of successful alignment increases when the interacting organizations are closer to one another’s dominant sector space.

4.3.3. Communication of Scalability and Earned Income Expectations of the Investee

Social impact scalability is a major signal that social enterprises must articulate to attract investors [47,48]. Scalability potential signals a greater social value creation (ibid). However, scaling a social enterprise without revenue sources could exhaust the running capital. The following quote from LC illustrates the importance of scalability and revenues, while making investment decisions along with the social mission of the social enterprise.

‘Take, for example, RS [investee]. We invested when they had about one center and about 40 odd employees. Today they are among the largest player. So they run about 20 centers, employ 2500 employees in each of these places. On a commercial stand point, it now generates about 8 million dollars in revenues on an annual basis. Moreover, from an investment returns standpoint, I think we are close to getting an exit out of the center. We will basically be selling [to a] commercial player today and we are making a healthy return.’(Investor LC)

AF, USF, and LC predominantly focus on scalability through revenue generation in addition to the social mission when selecting early-stage investees. Impact investors with dominant financial logic have a higher expectation of scalability as it signals profitable exit.

VI and USV have a dominating social logic. They have a higher expectation from investee social enterprises for scaling the social mission and increasing the reach towards beneficiaries. The following quotation from VI illustrates the dominance of the social mission.

‘Any beneficiary should serve the low income either rural or urban [to guarantee social impact] community. Apart from these criteria we, when we do the inspection and developments, we look at financial scalability, and business scalability of fund (financial logic).’(Investor VI)

An increased focus on revenues could compromise the impact delivered to the beneficiaries, while the increased focus on beneficiaries could decrease the running capital with the investees. Therefore, it is important that the investees successfully communicate the social impact expectations, earned income expectation, and the scalability potential of impact and returns. Table 5 summarises the pre-investment alignment strategies.

Table 5.

Pre-investment alignment strateegies and post-investment alignment strategies.

4.4. Effective Alignment of Competing Goals During Inter-Organizational Collaboration (Remedial strategies)

The remedial strategies are aimed at avoiding the potential risks of misalignment during inter-organizational collaboration. The remedial measures are strategies that investors and investees should focus on to increase an alignment of goals post investment. The findings reveal several strategies that could significantly reduce the risk of misalignment after the initial investment had been made.

4.4.1. Social Impact Measures and Reporting

One USF investee mentioned ‘our interaction was never about impact, but about financial benefits’. On the other hand, one USV investor mentioned that their interaction focused too much on impact measurement and little on real business.

AF has developed their in-house impact-reporting toolbox and implemented it with their investee organizations. They have expanded into multiple domains, deploying their impact-reporting toolbox. In addition, they have succeeded in several exits. AF has a dedicated impact officer who engages in the implementation, measurement, collection and compilation of impact data. The steps taken by AF in communicating their impact are reflected in how investors and other stakeholders perceive AF.

CSF actively engages with their investees in developing social impact measures. They work together towards methodologically collecting and analyzing the data. The data analysis results are studied against the theory of change, and are documented for further implementation or publication. The social assessment reports (which are accounts of the investees) published by CSF are used by the local government to review the outcomes of local schools and their education budgeting for public primary schools. This approach helps to create trust with investees and further increase the external legitimacy of CSF as a change maker in the sector.

USV makes small investments in their investees and has a sector-specific theory of change which drives their investments. Their investees are required to properly communicate their theory of change and the impact created post investment. Investee impact reports are important factors that develop the external legitimacy of impact investors.

However, one of the LC investee social enterprises cited that the requirements of social impact assessment were only to fulfil the fiduciary duty, and in practice, they never factored into the strategic conversation between the two. LC is limited to the microfinance sector, and its investments outside the microfinance sector are not as popular as those within the microfinance sector.

Based on this analysis, we infer that even though impact measurement and reporting increase an additional bureaucratic drain on the investee, in the long run, the results are reflected in the overall social acceptance of both the impact investor and investee social enterprise.

4.4.2. Engagement and Knowledge Sharing

Active engagement and knowledge sharing are essential activities for managing competing goals. Active engagement involves not only time and control, but also sharing business knowledge and business networks that benefit the long-term strategy of investee social enterprises. Based on the quotations, one can infer that VI not only incubates and funds a social enterprise, but also frequently engages with them and helps in creating efficiency and performance for revenue generation and growth.

‘As part of the mentoring we have regular board member calls with the enterprise. […] We find one of the CXOs, CIO, COO and the CEO related to the field. Our board members are really experienced guys in different sectors. Beyond [that], if we feel that an enterprise or an entrepreneur needs support for a specific thing or in a specific sector [and] we think that we cannot provide mentorship, we also connect them to a list of [outside] mentors on our website. They run multiple enterprises in different sectors and are really experienced people.’(Investment Manager VI)

VI developed a strong mentorship program that helped their investees to grow. They attracted top CXOs as volunteers to mentor their investee social enterprises. Similarly, CSF closely engaged with their investees. According to the data, VI and CSF spent more time in mentoring their investees than did the others. The investees consequently viewed them with respect. The investor-investee relationships in these cases were better aligned and respected.

While the investors from USV and LC contributed capital and took board positions, but abstained from regular engagement (compared with VI and CSF), the relative aloofness with the investees increased the risk of tensions between the two.

As with the intra-organizational level, in which actors from different institutional logics disengage, the probability of tension increases [49]. Similarly, at the inter-organizational level, the lack of engagement accentuates the differences and increases tensions.

Frequent engagement between impact investors and investee social enterprises must be aimed at increasing both the social and commercial value creation. The greater interaction results in the alignment of goals and the creation of the sustainable inter-organizational relationship. The study concludes that to manage complexity arising due to competing goals, the firms must focus on constant engagement, sharing best business skills, business networks and firm growth, while addressing the competing goals. Table 5 summarises the post-investment alignment strategies.

5. Discussion and Theory Development

The study explores impact investing from the perspective of the investee-investor relationship, and finds that actions such as due diligence, social impact measures, sector knowledge and engagement are the essential strategies for managing the alignment of two firms at the inter-organizational level. The findings highlight the following theoretical and managerial implications.

5.1. Reasons for Alignment

The alignment between investor and investee is motivated by the expected benefits from the inter-organizational collaboration. Benefits such as liquidity for investees [39], social legitimacy for investors [36] and mutually aligned motivations for achieving common goals, are some of the pragmatic interests that outweigh competing logics during the initial stages of inter-organizational alignment, justifying [35]. The analysis of Austin [23] and Yunus, Moingeon, and Lehmann-Ortega [50] finds that inter-organizational collaboration is strengthened when firms jointly engage in value creation activities [38]. However, inter-organizational alignment is a temporal dynamic event in which tensions due to competing logics could subsequently arise [51].

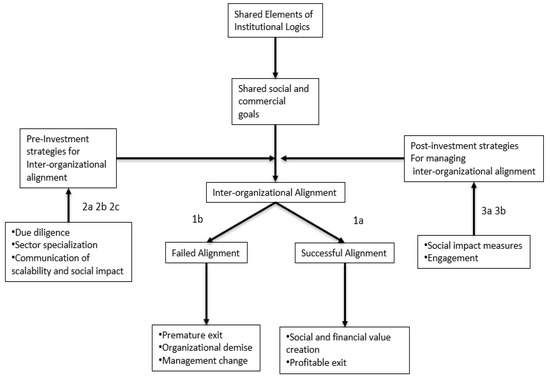

This study (see Table 4; see Figure 1) informs us that unlike for-profit enterprises (where the motive is primarily financial), the reasons for alignment among impact investing firms are driven by the consideration of commercial viability and the social value creation ability of the investees. Similar to how institutional logics nudge investees in for-profit space [38], the findings suggest that competing logics (social goals versus financial returns) are some of the predominant reasons for the alignment of impact investors and investee social enterprises. These findings extend the application of the institutional logics framework to hypothesize impact investing, in which the theory is used to study the inter-organizational alignment.

Figure 1.

Model of inter-organizational alignment of impact investor-investee social enterprise.

Huybrechts and Nicholls [36] conclude that the legitimacy gained and resource deficit dominate the collaboration, and that those in the dominant position are likelier to steer the outcome and determine the longevity of the collaboration. The findings of this study indicate that the effectiveness of impact investment is determined, not only by the dominant position held by the capital provider, but also by the social value created by the capital seeker. The dominant role of the impact investor as a capital provider is balanced by the ability of the investee social enterprise to create moral and social legitimacy, which is shared by all. The literature concerning venture capital predominantly suggests that venture capital has greater dominance in their investments [38]. The legitimacy created by social value creators (investees) and its role in the investor-investee inter-organizational relationship is unique and different from the predominantly held belief found in venture capital literature that the capital provider holds a dominant position in inter-organizational collaboration. Lawrence et al. [52] organizational collaboration results in new institutional fields. We see this subtle difference among interacting organisations (impact investor and investee social enterprise) as an institutional building practice, where a new organizational practice (impact investing) is providing a new perspective over the widely held world view.

Proposition 1a.

The alignment of social and financial goals of creating social and commercial value increases the probability of inter-organizational collaboration between impact investors and investee social enterprises.

Proposition 1b.

The non-alignment of social and financial goals between impact investors and investee social enterprises increases the likelihood of investor-investee relationship breakdown, resulting in the lack of social value creation and a likely organizational demise.

5.2. Antecedents to Effective Inter-Organizational Alignment

Most studies on due diligence were conducted by scholars studying for-profit venture capitalist strategies, which suggests that venture capitalists principally focus on maximizing economic and commercial benefits [32]. The review by Maxwell, Jeffrey, and Lévesque [32] identified the character-istics of products and services offered, characteristics and the background of the entrepreneur, team composition, market characteristics and expected return as common due diligence variables which influence the for-profit investor decision. The study by Roundy et al. [14] on the criteria of evaluation for investment used by impact investors reveals evaluation strategies used by both venture capitalists and philanthropists. The social impact is the primary criterion which involves social value creation and the social issues addressed.

Furthermore, team composition and the revenue model are other criteria which influence the decision of impact investors. This study aligns with the findings of Roundy et al. [14] on the criteria of evaluating impact investment. The findings indicate that the due diligence process for impact investors is different from those among venture capitalist firms. The findings suggest that the categorical inclusion of the social mission and valuation of the social mission in the due diligence process help to increase the alignment between impact investors and social enterprise investees. The findings suggest also that if the social mission goals of the impact investor and investee social enterprise align strongly at the due diligence stage, the probability of sustainable alignment post investment remains strong.

Proposition 2a.

A greater emphasis on their respective organizational goals during the due diligence phase results in an increased degree of alignment between the investors and the investees.

The findings of the study by Roundy et al. [14] suggest that impact investors look for specific social issues when evaluating investee social enterprises. This study considers these specific social issues as social sectors. Both private equity literature and venture capital literature attribute the performance of funds to sectors (industries). However, the comparative analysis of the performance of funds within or across a ‘social sector’ has not been explored. The findings of this article reveal that impact investors which have developed a specialization in a particular social sector demonstrate a greater alignment and success rate.

The findings suggest that impact investors would manage the tensions arising from competing logics better if they specialize in a particular sector and invest in social enterprises solving the social problems of that sector. Our findings suggest that when an impact investor has developed expertise in a particular social sector, its alignment with the investees is improved, and its performance (both social and commercial) is consequently higher. An increased focus on the social mission during the due diligence stage increases the probability of balancing competing logics at the inter-organizational level.

Proposition 2b.

Sector specialization of the impact investors increases the likelihood of inter-organizational alignment.

Effective communication is an important criterion that unites two organizations with shared interests. The dominant literature on competing institution logics states that primary actors should communicate with one another to sustain an organizational process among collaborating firms. The dominant literature on both venture capital scholarship and inter-organizational scholarship suggests that those in weaker positions must demonstrate effective communication to attract resources from dominant players [35,36,38].

In the selected cases, a few impact investors have dominating commercial logic while a few have dominating social logic. The impact investors with dominating commercial logic invest in investees which effectively communicate their commercial goals alongside their social mission with an emphasis on scalability and financial exit. On the other hand, the impact investors with dominating social logic invest in investees which effectively communicate their social goals alongside their earned income abilities with an emphasis on reach and social impact. Investees overcome the dominance of capital provider through effective communication.

Proposition 2c.

Investee social enterprises which can clearly articulate earned income expectation, social impact expectation, and scalability potential are likelier to have inter-organizational alignment.

5.3. Effective Long-Term Inter-Organizational Alignment

The activities of social enterprises result in social value creation, long-term social impact, and potentially public policy impact. To assess the social value created, the social enterprises must appropriately measure the impact of their social activities. Social impact assessment methods are not standardized, most self-reported and expensive to conduct third party social audits.

The financial auditing of firm activities is a standard process in which the metrics are strictly related to financial performance. The major risks associated with impact investing arising out of the lack of replication, established processes and the difficulty in measuring the social value created by impact investors [12,53,54].

While measuring financial value generated is a standardized coded practice, measuring social value remains under development, and is far from being unambiguously coded [10,54]. The quality of social impact created also helps to create a social reputation for both the impact investor and investee social enterprise. The social legitimacy of both depends on the veracity of the social impact created. The mutual motivation towards a greater good helps to align both the impact investor and their investee social enterprise and assists in creating a sustainable inter-organizational relationship.

Proposition 3a.

Regular social impact measurement and reporting on accepted goals increase the likelihood of successful inter-organizational alignment and inter-organizational performance over the investment period.

One postulation by Fenema and Loebbecke [37] hypothesizes that organizational structures help to manage inter-organizational tensions. The routinization of interaction and engagement by leadership further helps to manage the inter-organizational tensions. The findings of this article empirically verify the postulations theorized by Fenema and Loebbecke [37]. The engagement in the for-profit investment is linear, and focuses solely upon increasing financial performance and organizational efficiency, while encouraging organizational development. The engagement in the case of impact investing involves, not only the engagement for financial performance and organizational efficiency, but also the alignment of investee activities towards the envisioned social mission and social goals. Impact investors which side-line the social goals of the investees might send a signal that they are engaging only for financial incentives and securing their investments. Such a focus could create tensions between the two, and the larger impact of these tensions would result in a breakdown of relation or loss of social legitimacy of the impact investor. While engaging, the investor should reflect on their investment mandate, their social goals, and the goals of the investee social enterprise.

Proposition 3b.

Frequent engagement between the impact investor and investee social enterprise results in the effective alignment of organizational goals.

5.4. Inter-Organizational Alignment: An Investing Model

The model (see Figure 1) joins different scenarios at the inter-organizational level among organizations aimed at creating social and commercial value and the motivations of aligning two organizations under competing goals. The numbers in the figure illustrate the propositions developed earlier. The figure illustrates the consequences of non-alignment. Afterwards, it presents actions and strategies that organizations could consider prior to investment in addition to remedial actions and finally, post-investment strategies which broaden the present understanding of the dynamics of competing logics at the inter-organizational level.

This study provides insights into how impact investors are influenced by social and commercial institutional logics, and how these logics (associated values, beliefs and guiding principles) could affect the inter-organizational relationship and alignment post investment. Using the cases, the study also shows that dominance of one logic over other may lead to the breakdown of inter-organizational relationship between the investor and investee. The alignment of social and commercial goals (which arise from social and commercial institutional logics) is essential but not the only criterion for long term inter-organizational alignment.

6. Conclusions

Given the nascent stage of scholarship in impact investing, the growing interest of practitioners within the field, and the importance of the investee as an instrument of legitimacy for impact investing, this article explores the inter-organizational relationship between impact investors and investee social enterprises. The article explores the causes of misalignment and strategies for alignment at the inter-organizational level, and has a number of theoretical and managerial implications.

6.1. Theoretical Implications

The scholars of social entrepreneurship have predominantly used institutional logics to theorize the social entrepreneurship field and to differentiate it from commercial entrepreneurship. Until 2018, only two studies [12,53] have used institutional logics to analyze and theorize impact investing. Given that the field lacks a theoretical lens, this study contributes to both impact investing and the institutional logics literature by extending the use of institutional logics as a theoretical lens to reflect on the inter-organizational relationship between the impact investing and the investee social enterprises.

Nicholls [55] argues that the field of Impact investing lacks institutional status, because it is not fully recognized by traditional financial institutions as a reliable financial asset class, it lacks history and processes, and its performance is not fully replicable. Lawrence et al. [52] suggested the effective inter-organizational collaboration results in far-reaching effects. Among the emerging field, an effective inter-organizational collaboration involving multiple actors results in institutional creation. This study provides strategies which impact investing scholars, and which practitioners should use to reflect on and practice impact investing. The successful inter-organizational collaboration between impact investing firms and investee social enterprises would make a strong business case for impact investing, thereby strengthening the institutionalization of the field.

The findings contribute to the institutional logics literature on competing logics, particularly questions regarding how to balance competing logics at the inter-organizational level. The primary studies on competing logics have explored the intra-organizational level [15,16,19]. The firm level studies competing logics have predominantly explored the role of the founder and internal governance mechanisms in navigating the institutional complexity and managing tensions due to competing logics. Pache and Santos [19,25] discuss how social enterprises can choose their social and commercial signals to attract resources and legitimacy from multiple sources. Battilana and Dorado [22] emphasis the social motivations of the founder and human resources working within social enterprise which help in managing negative impact of competing logics.

This study suggests that the social and commercial performance of inter-organisational collaboration among impact investing organisation can be increased and risk of tensions reduced through pre-investment and post-investment strategies. The pre-investment strategies must include due-diligence, sector specialization, and communication of scalability of reach and social impact. The due-diligence would ensure the social and commercial logics of both investors and investees are aligned, while decreasing the uncertainties. The sector specialization by impact investors would help impact investors understand the risks, opportunities and social disequilibria in a specific social sector like health, education, domestic violence, gender discrimination. Therefore, the social logic of the impact investor would be dominant for a particular sector, while the commercial logic would be in a stronger position to access the risks and returns. Finally, the investees must clearly demonstrate their future goals related to scalability of the reach and social impact. Such a communication would signal usage of the investment and exist probabilities.

During the post investment period, the interacting firms must constantly engage with each other. The engagement would reduce the probability of tensions among competing logics and drift. Since, the impact investor draws its legitimacy from both social and commercial value creation, the reporting and communication of social and commercial by the investees would elongate the period of engagement. According to Tracey and Jarvis [56] the agency cost of understanding the social impact potential of social enterprises is very high, it is therefore essential that social impact created is measured and communicated frequently to ensure that the social goals are clearly articulated and the social logic maintains its legitimacy. The study suggests that the internalisation of these strategies would aid in alignment of competing logics and long-term inter-organizational collaboration.

Tilcsik [51] pointed out that organizational responses to institutional logics may change over time. The findings of this study suggest that the immediate motivations of inter-organizational alignment and those which keep the alignment secured for the long-term are slightly different. The role of founder is essential in defining the characteristics of the hybrid organization and external governance mechanism. The creation of governance principles to manage the inter-organizational relationship for better performance during the pre-investment and post-investment phase will aid in better managing the relationship.

6.2. Managerial Implications

This article studies the inter-organizational relationship between six impact investors and their investee social enterprises via the competing logics framework. The study finds that to manage effectively the non-alignment of goals at the inter-organizational level, impact investors use one of three approaches: Due diligence, specialization and engagement. Similarly, to effectively manage the non-alignment of goals at the inter-organizational level, investee social enterprises were found to engage in social impact reporting and communication of their earned income strategies. The results of this study can be generalized in other fields, such as sustainable entrepreneurship, public private partnerships, corporate social enterprises, cross-sector partnerships involving NGOs, private enterprises, government and civil society.

6.3. Limitations and Future Research Agenda

The data collected for this study was cross-sectional. A longitudinal study would reveal greater insights into decision-making complexities, and would reveal greater details on how institutional logics affect decision making. The propositions and the model developed (Figure 1) should be tested using a survey method. Future studies should be able to analyze critically the impact investing decisions and the inter-organizational relationship between impact investors and social enterprises via the institutional logics framework. The data is from India, but we present the idea that our analysis and findings are generalizable. Researchers could also use data from other countries and run cross-case analysis or test the propositions to explore inter-organizational relationship these organizations.

Author Contributions

Conceptualization, A.A.; methodology and software: A.A.; formal analysis: A.A.; investigation: A.A.; resources: A.A.; data curation, A.A.; writing—original draft preparation, A.A.; writing—review and editing: K.H.; supervision: K.H.; project administration: K.H.

Funding

This research received no external funding.

Acknowledgments

We would like to acknolwedge the support from Copenhagen Business School and valuable comments by the numerous friendly reviewers at the CBS and at the Academy of Management 2016.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Höchstädter, A.K.; Scheck, B. What’s in A Name: An Analysis of Impact Investing Understandings By Academics and Practitioners. J. Bus. Ethics 2015, 132, 449–475. [Google Scholar] [CrossRef]

- Daggers, J.; Nicholls, A. Academic Research into Social Investment and Impact Investing: The Status Quo and Future Research. In Routledge Handbook of Social and Sustainable Finance; No. 5; Routledge: Abingdon-on-Thames, UK, 2016. [Google Scholar]

- Hebb, T. Impact investing and responsible investing: what does it mean? J. Sustain. Financ. Invest. 2013, 3, 71–74. [Google Scholar] [CrossRef]

- Bugg-Levine, A.; Goldstein, J. Impact Investing: Harnessing Capital Markets To Solve Problems At Scale. Community Dev. Invest. Rev. 2009, 5, 30–41. [Google Scholar]

- Rajan, A.T.; Koserwal, P.; Keerthana, S. The Global Epicenter Of Impact Investing: An Analysis Of Social Venture Investments in India. J. Priv. Equity 2014, 17, 37–50. [Google Scholar] [CrossRef]

- Battilana, J.; Lee, M.; Walker, J.; Dorsey, C. In Search of The Hybrid Ideal. Available online: https://ssir.org/articles/entry/in_search_of_the_hybrid_ideal (accessed on 10 January 2019).

- Miller, T.L.; Wesley, C.L. Assessing Mission and Resources for Social Change: An Organizational Identity Perspective on Social Venture Capitalists’ Decision Criteria. Entrep. Theory Pract. 2010, 34, 705–733. [Google Scholar] [CrossRef]

- Scholtens, B.; Sievänen, R. Drivers of Socially Responsible Investing: A Case Study of Four Nordic Countries. J. Bus. Ethics 2013, 115, 605–616. [Google Scholar] [CrossRef]

- Weber, O. Introducing Impact Investing. In Routledge Handbook of Social and Sustainable Finance; Lehner, O.M., Ed.; Routledge, Taylor Francis Group: Oxford, UK, 2016. [Google Scholar]

- Rizzi, F.; Pellegrini, C.; Battaglia, M. The Structuring of Social Finance: Emerging Approaches for Supporting Environmentally and Socially Impactful Projects. J. Clean. Prod. 2018, 170, 805–817. [Google Scholar] [CrossRef]

- Arena, M.; Bengo, I.; Calderini, M.; Chiodo, V. Unlocking Finance for Social Tech Start-Ups: Is There A New Opportunity Space? Technol. Forecast. Soc. Chang. 2016, 127, 154–165. [Google Scholar] [CrossRef]

- Castellas, E.I.-P.; Ormiston, J.; Findlay, S. Financing social entrepreneurship. Soc. Enterp. J. 2018, 14, 130–155. [Google Scholar] [CrossRef]

- Gregory, N. De-Risking Impact Investing. World Econ. 2016, 17, 143–158. [Google Scholar]

- Roundy, P.; Holzhauer, H.; Dai, Y. Finance Or Philanthropy? Exploring The Motivations and Criteria of Impact Investors. Soc. Responsib. J. 2017, 13, 491–512. [Google Scholar] [CrossRef]

- Thornton, P.H.; Ocasio, W.; Lounsbury, M. The Institutional Logics Perspective: A New Approach to Culture, Structure and Process; Oxford University Press: Oxford, UK, 2012. [Google Scholar]

- Scott, W.R. Institutions and Organizations: Ideas, Interests, and Identities, 4th ed.; Stanford University: Stanford, CA, USA, 2014. [Google Scholar]

- Reay, T.; Hinings, C.R.R. Managing The Rivalry of Competing Institutional Logics. Organ. Stud. 2009, 30, 629–652. [Google Scholar] [CrossRef]

- Lehner, O.M.; Nicholls, A. Social Finance and Crowdfunding for Social Enterprises: A Public-Private Case Study Providing Legitimacy and Leverage. Ventur Cap. 2014, 16, 271–286. [Google Scholar] [CrossRef]

- Agrawal, A.; Hockerts, K. Impact investing: review and research agenda. J. Small Bus. Entrep. 2019. [Google Scholar] [CrossRef]

- Wood, D.; Thornley, B.; Grace, K. Institutional Impact Investing: Practice and Policy. J. Sustain. Financ. Invest. 2013, 3, 75–94. [Google Scholar] [CrossRef]

- Pache, A.C.; Santos, F. When Worlds Collide: The Internal Dynamics of Organizational Responses To Conflicting Institutional Demands. Acad. Manag. Rev. 2010, 35, 455–476. [Google Scholar]

- Battilana, J.; Dorado, S. Building Sustainable Hybrid Organizations: The Case of Commercial Microfinance Organizations. Acad. Manag. J. 2010, 53, 1419–1440. [Google Scholar] [CrossRef]

- Austin, J.; Stevenson, H.; Wei-Skillern, J. Social and Commercial Entrepreneurship: Same, Different, or Both? Entrep. Theory Pract. 2006, 30, 21–22. [Google Scholar] [CrossRef]

- Saz-Carranza, A.; Longo, F. Managing Competing Institutional Logics in Public-Private Joint Ventures. Public Manag. Rev. 2012, 14, 331–357. [Google Scholar] [CrossRef]

- Pache, A.; Santos, F. Inside The Hybrid Organization: Selective Coupling As A Response To Competing Institutional Logics. Acad. Manag. J. 2012, 56, 972–1001. [Google Scholar] [CrossRef]

- Marshall, R. Conceptualizing the International For-Profit Social Entrepreneur. J. Bus. Ethics 2011, 98, 183–198. [Google Scholar] [CrossRef]

- Bonini, S.; Emerson, J. Maximizing Blended Value—Building beyond the Blended Value Map to Sustainable Investing, Philanthropy and Organizations; BlendedValue: CO, USA, 2005; Available online: http://www.blendedvalue.org/wp-content/uploads/2004/02/pdf-max-blendedvalue.pdf (accessed on 26 July 2019).

- Porter, M.E.; Kramer, M.R. Philanthropy’s New Agenda: Creating Value. Harv. Bus. Rev. 1999, 77, 121–130. [Google Scholar]

- Davila, A.; Foster, G.; Gupta, M. Venture Capital Financing and The Growth of Startup Firms. J. Bus. Ventur. 2003, 18, 689–708. [Google Scholar] [CrossRef]

- Forlani, D.; Mullins, J.W. Perceived Risks and Choices in Entrepreneurs’ New Venture Decisions. J. Bus. Ventur. 2000, 15, 305–322. [Google Scholar] [CrossRef]

- Florin, J. Is Venture Capital Worth It? Effects on Firm Performance and Founder Returns. J. Bus. Ventur. 2005, 20, 113–135. [Google Scholar] [CrossRef]

- Maxwell, A.L.; Jeffrey, S.A.; Lévesque, M. Business Angel Early Stage Decision Making. J. Bus. Ventur. 2011, 26, 212–225. [Google Scholar] [CrossRef]

- Kent, D.; Dacin, M.T. Bankers At The Gate: Micro Fi Nance and The High Cost of Borrowed Logics. J. Bus. Ventur. 2013, 28, 759–773. [Google Scholar] [CrossRef]

- Saltuk, Y.; Bouri, A.; Leung, G. Insight into the impact investment market: An in-depth analysis of investor perspectives and over 2,200 transactions. Available online: https://thegiin.org/assets/documents/Insight%20into%20Impact%20Investment%20Market2.pdf (accessed on 11 February 2019).

- Phillips, N.; Lawrence, T.B.; Hardy, C. Inter-Organizational Collaboration and The Dynamics of Institutional Fields. J. Manag. Stud. 2000, 37, 23–43. [Google Scholar] [CrossRef]

- Huybrechts, B.; Nicholls, A. The Role of Legitimacy in Social Enterprise-Corporate Collaboration. Soc. Enterp. J. 2013, 9, 130–146. [Google Scholar] [CrossRef]

- Van Fenema, P.C.; Loebbecke, C. Sciencedirect Towards A Framework for Managing Strategic Tensions in Dyadic Interorganizational Relationships. Scand. J. Manag. 2014, 30, 516–524. [Google Scholar] [CrossRef]

- Pahnke, E.C.; Katila, R.; Eisenhardt, K.M. Who Takes You To The Dance ? How Partners Institutional Logics Influence Innovation in Young Firms. Adm. Sci. Q. 2015, 60, 596–633. [Google Scholar] [CrossRef]

- Di Domenico, M.L.; Tracey, P.; Haugh, H. The Dialectic of Social Exchange: Theorising Corporate-Social Enterprise Collaboration. Organ. Stud. 2009, 30, 887–907. [Google Scholar] [CrossRef]

- Yin, R.K. The Case Study Crisis: Some Answers. Adm. Sci. Q. 1981, 26, 8–58. [Google Scholar] [CrossRef]

- Gibbert, M.; Ruigrok, W.; Wicki, B. Research Notes and Commentaries What Passes As A Rigorous Case Study? Strateg. Manag. J. 2008, 29, 12. [Google Scholar] [CrossRef]

- Eisenhardt, K.M. Building Theories From Case Study Research. Acad. Manag. Rev. 1989, 14, 532–550. [Google Scholar] [CrossRef]

- Suddaby, R. From The Editors: What Grounded Theory Is Not. Acad. Manag. J. 2006, 49, 633–642. [Google Scholar] [CrossRef]

- Eisenhardt, M.E.G.K.M. Theory Building From Cases: Opportunities andchallenges. Acad. Manag. J. 2007, 50, 8. [Google Scholar] [CrossRef]

- Yin, R.K. Case Study Research and Applications: Design and Methods, 6th ed.; Sage publications: Thousand Oaks, CA, USA, 2018. [Google Scholar]

- Glaser, B.G.; Strauss, A.L. The Discovery of Grounded Theory: Strategies for Qualitative Research; Aldine Publishing Company: Chicago, IL, USA, 1967. [Google Scholar]

- Bloom, P.N.; Chatterji, A.K. Scaling Social Entrepreneurial Impact. Calif. Manag. Rev. 2009, 51, 114–133. [Google Scholar]

- Lyon, F.; Fernandez, H. Strategies for Scaling Up Social Enterprise: Lessons From Early Years Providers. Soc. Enterp. J. 2012, 8, 63–77. [Google Scholar] [CrossRef]

- Paul, P.; Jmatthiesen, J.J.; van de Den, A.H. A Practice Approach To Institutional Pluralism. In Institutional Work Actors and Agency in Institutional Studies of Organizations, 1st ed.; Lawrence, T.B., Suddaby, R., Leca, B., Eds.; Cambridge University Press: Cambridge, UK, 2010; pp. 284–317. [Google Scholar]

- Yunus, M.; Moingeon, B.; Lehmann-Ortega, L. Building Social Business Models: Lessons From The Grameen Experience. Long Range Plan. 2010, 43, 308–325. [Google Scholar] [CrossRef]

- Tilcsik, A. From Ritual to Reality: Demography, Ideology, and Decoupling in a Post-Communist Government Agency. Acad. Manag. J. 2010, 53, 1474–1498. [Google Scholar] [CrossRef]

- Lawrence, T.; Hardy, C.; Phillips, N. Instiutional Effects on Interorganizational Collaboration: The Emergence of Proto-Institutions. Acad. Manag. J. 2002, 45, 281–290. [Google Scholar]

- Quinn, Q.C.; Munir, K.A. Hybrid Categories As Political Devices: The Case of Impact Investing in Frontier Markets. Res. Sociol. Organ. 2017, 51, 113–150. [Google Scholar]

- Millar, R.; Hall, K. Social Return on Investment (Sroi) and Performance Measurement. Public Manag. Rev. 2013, 15, 923–941. [Google Scholar] [CrossRef]

- Nicholls, A. The Legitimacy of Social Entrepreneurship: Reflexive Isomorphism in A Pre-Paradigmatic Field. Entrep. Theory Pract. 2010, 44, 611–634. [Google Scholar] [CrossRef]

- Tracey, P.; Jarvis, O. Toward A Theory of Social Venture Franchising. Entrep. Theory Pract. 2007, 30, 667–685. [Google Scholar] [CrossRef]

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).