1. Introduction

Organizational sustainability has been gaining its rightful recognition and importance as it offers competitive advantage and creates value for organizations, their stakeholders, and society [

1]. However, sustainability has not been fully integrated at the strategic and operational level [

2]. Some researchers believe that the main hurdle in operationalization of sustainability in organizations is the lack of maintainable value creation throughout the value chain, because parts of these activities are beyond the control of organizations, such as supply chain [

3]. Others argue that it is the lack of practicable frameworks and models which holds back the organizational actors from (holistically) considering sustainability in business decisions [

4]. The latter is particularly important because existing sustainability management models and frameworks are based on conceptual and theoretical designs [

4,

5]. The structure of these models lacks a fundamental practicable approach which limits their use in practice. In order to increase the potential application of existing organizational sustainability models, it is important to integrate the sustainability best-practices within the structure of these models [

4]. The reason for this is fairly simple: organizational actors generally prefer ‘practical rationale’ over ‘scholarly intellect’ [

6]. Besides applicability, the integration of theories and practices enables the model/framework developers to understand and address the practical limits of organizations in managing sustainability. Adams and Larrinaga-González [

7] argued that in order to identify how accounting and management systems may address the organizational sustainability challenges, it is imperative to learn from the practical success of sustainable organizations. The authors called for a scholarly engagement with organizations to learn from their internal processes, at the strategic and micro level.

There are only a few studies in the literature which try to capture the sustainability best-practices of organizations. These studies, however, have limited implications because of the constraints in their research scope and design. Some of the studies capture only those practices which reflect on the role of leadership in enhancing the impact of strategic initiatives [

8], whereas others try to examine the influence of sustainability practices on profitability [

9]. A few others limit the scope of research either to the strategic initiatives [

10,

11] or to the small and medium enterprises [

12]. In other instances, the selection of a sample is either restricted to a single sector [

13] or to a single country [

14,

15].

While these studies provide useful insight to organizational sustainability, the process of sample selection, extraction of sustainability practices, the top-level focus of studies, and geographical screening can be improved in order to make the results more systematic, reproduceable, and comprehensive. Therefore, the primary goal of this work is to systematically review the practical sustainability constructs based on sustainability best practices in order to develop an applied framework which can be integrated with theoretical and conceptual models. However, the scope of this study will be limited to the development of a framework; the integration of frameworks is not part of this work. Also, the scope of this review does not limit the study sample to a single sector or country, or to the strategic initiatives only; however, to ensure do-ability, a research-criteria, discussed in the Materials and Methods section, is developed and applied. The review seeks to find potential answers to the following questions: “what are the constructs of organizational sustainability management that are based on the best practices of the most sustainable firms, which can be used to develop a practical framework for organizational sustainability?”.

This article is divided into six sections. After the introduction, a brief literature review is provided in the second section. A systematic method for conducting the review is discussed in the third section. The results are offered in the fourth section. The fifth section presents a discussion around the findings, and the final section concludes the discussion and identifies opportunities for future research.

2. Literature Review

The idea of sustainable development was first coined by the Brundtland Commission, in its report—Our Common Future (1987), after which numerous multidisciplinary, multifaceted efforts have been made in order to conform with the planetary and social limits and to support a maintainable pattern of human life on earth. The range of such efforts lies in technological advancement in renewables and nanomaterials to social development through the United Nations guiding principles on business and human rights. An important, although new, member of the sustainability discipline is Sustainability Management.

Similar to the words

love,

affection, and

loyalty, sustainability management is a generally known concept, as far as conversations and discussions are concerned, but a single, widely accepted and narrow definition of any of these words is not available [

16]. United Nations Environment Programme [

17] has defined sustainability management as processes or structures that an organization uses to meet its sustainability goals and objectives while transforming inputs into a product or service. Madu and Kuei [

18] defined sustainability management through combining the definitions of ‘sustainability’ and ‘management’, i.e., enabling a condition for the continuity of economic development, environmental protection, and social equity. A more general definition of sustainability management has been offered by Starik and Kanashiro [

16]: sustainability management is the formulation, implementation, and evaluation of both environmental and socio-economic sustainability-related decisions and actions. These decisions and actions may be reflected in a range of activities on various levels; from an individual’s perspective, these may be the consumption patterns or buying habits or commuting choices, whereas, on a global level, these can be the collateral efforts made by different countries in order to contest climate change, poverty, or terrorism. Among this wide spectrum of sustainability stakeholders, a common, but crucial, role is played by the businesses, corporations, enterprises and other similar entities, which will be referred to as ‘organizations’ in the present work.

Traditionally, organizations focused on the maximization of shareholder value were considered successful. The trend has significantly changed in the last couple of decades; the organizations are expected to embed environmental and social objectives in the decision-making process in order to create value for other stakeholders, in addition to shareholders [

19]. The absolutely essential role of organizations in shifting gear from accelerated growth to maintainable development is already established in the literature and among the practitioners [

20]. In the modern world, organizations are referred to as ‘polities’ since these have a governance structure which functions in accordance with its rights and duties to address the needs of interest groups [

21]. A consensus among the researchers is yet to be established on whether the organizations opt for sustainable management practices to improve their resource efficiency and thus, increase profitability [

22], which has been extensively supported by empirical evidences [

23,

24], or if such activities are simply the result of increased social pressure from stakeholders, including governments, NGOs, employees, and others [

21]. In both cases, the role of organizations for sustainable development is inevitable.

Similar to sustainability management, a generic definition of organizational sustainability does not exist, rather various researchers took on the charge to define organizational sustainability in their own ways. Neubaum and Zahra [

25] referred to organizational sustainability as the ability of a firm to nurture and support growth over time by effectively meeting the expectations of diverse stakeholders. On a similar level, Funk [

26] noted sustainable organizations as the ones whose characteristics and activities are intended to bring a desirable future state for its stakeholders. Marshall and Brown [

27] defined sustainable organizations ideally as the ones which take a systems perspective to ensure that natural resources are not consumed faster than the rates of renewal, recycling, or regeneration of those resources. Hart and Milstein [

28] described organizational sustainability as the contribution of organizations in the process of achieving human development in an inclusive, equitable, and secure manner by delivering simultaneously economic, social, and environmental benefits.

In the past, many researchers have emphasized taking account of the organizational sustainability practices in academic research [

7,

29]. Following suit, Rondinelli [

30] analyzed the sustainability principles and practices of the 25 transnational corporations (TNCs) which shows that many TNCs are still at the elementary or engagement level, which is far from being innovative, integrative or transformative. Probably the lack of a scientific consensus with regards to the impact of organizational sustainability holds back the multinational corporations (MNCs) from practicing sustainability beyond philanthropy [

14,

31].

Eweje [

15] explored the sustainability practices of 15 large firms in New Zealand through interviews with managers. The results indicate that organizations are actively involved in introducing new sustainability initiatives to address the three facets of sustainability, namely economics, environment, and society. Some examples of these initiatives include waste management, zero carbon footprint, environmental quality, extent of the share of renewable energy, education of employees, partnership with conservative groups, and community-based fundraising. While each sustainability initiative offers benefits, the synergy between different initiatives and integration of initiatives throughout the value chain remain a challenge [

32]. Therefore, rather than applying too many tools, understanding the application of the tool to be used in the context of business and initiation of rationale programs can orchestrate sustainability in corporations.

Similar to Eweje, Williams [

11] explored the sustainability best-practices of nine billion-dollar firms, which have been referred to by the author as Green Giants. Williams [

11] identified six key factors, as shown in

Table 1, which can be directly linked with the success of Green Giants and can correlate with the financial growth of these firms. Interestingly, while the author has emphasized the importance of responsible procurement and supply chain, the importance of branding and marketing has also been stressed for organizational sustainability.

Epstein [

10] also investigated the crucial organizational sustainability benchmarks. The author identified four high-level elements which are common in the success of most sustainable organizations. These include: Leadership, Strategy, Structure, and Systems. However, as highlighted by Lozano [

32] as well, the specific programs to be rolled out largely depend on the context and impact of the firm’s activities, ranging from capital investments in new technologies or products to programs promoting ethical sourcing and diversity.

Small [

9] conducted an empirical study to explore the sustainability practices which can promote profitability in the petroleum industry. The results show that there are six areas which can be linked with the sustainability and financial performance of petroleum firms at the same time, including environment, fuels, human resources, recycling, mitigation, and water.

Batista and Francisco [

29] reviewed the sustainability best practices of the most sustainable firms in Brazil, listed in the Corporate Sustainability Index. The authors identified organizational sustainability categories and best practices in each of the three facets of sustainable development. Similarly, Kiesnere and Baumgartner [

33] conducted a survey on smaller large-sized companies in Austria to seek the best practices with regards to the organizational change for sustainability. The authors proposed a model for the communication between the change-agents which can boost the personnel and cultural attributes of the firms.

Several other studies also explore the sustainability best practices in organizations [

34,

35], but as mentioned before, the process of sample selection, extraction of sustainability practices, the top-level focus of studies, and geographical screening are the primary shortcomings in the extant literature. There is strong need for a systematic study which can offer evidence-based content to support organizational sustainability. Admittedly, the work of Batista and Francisco [

29] is closest to addressing these shortcomings, but limiting the results to a single country and dividing the sustainability practices into sustainability facets without highlighting the representative examples makes it unlikely to resolve the concerns. Furthermore, since most of the studies are restricted to the organizational sustainability at the top-level, little has been done to explore the micro-level sustainability initiatives and practices. This work aims to overcome these shortcomings by: (i) systematically selecting the sample; (ii) identifying means for the selection of the best practices; (iii) exploring the sustainability practices at the strategic and micro level; and (iv) avoiding the geographical limitations.

4. Results

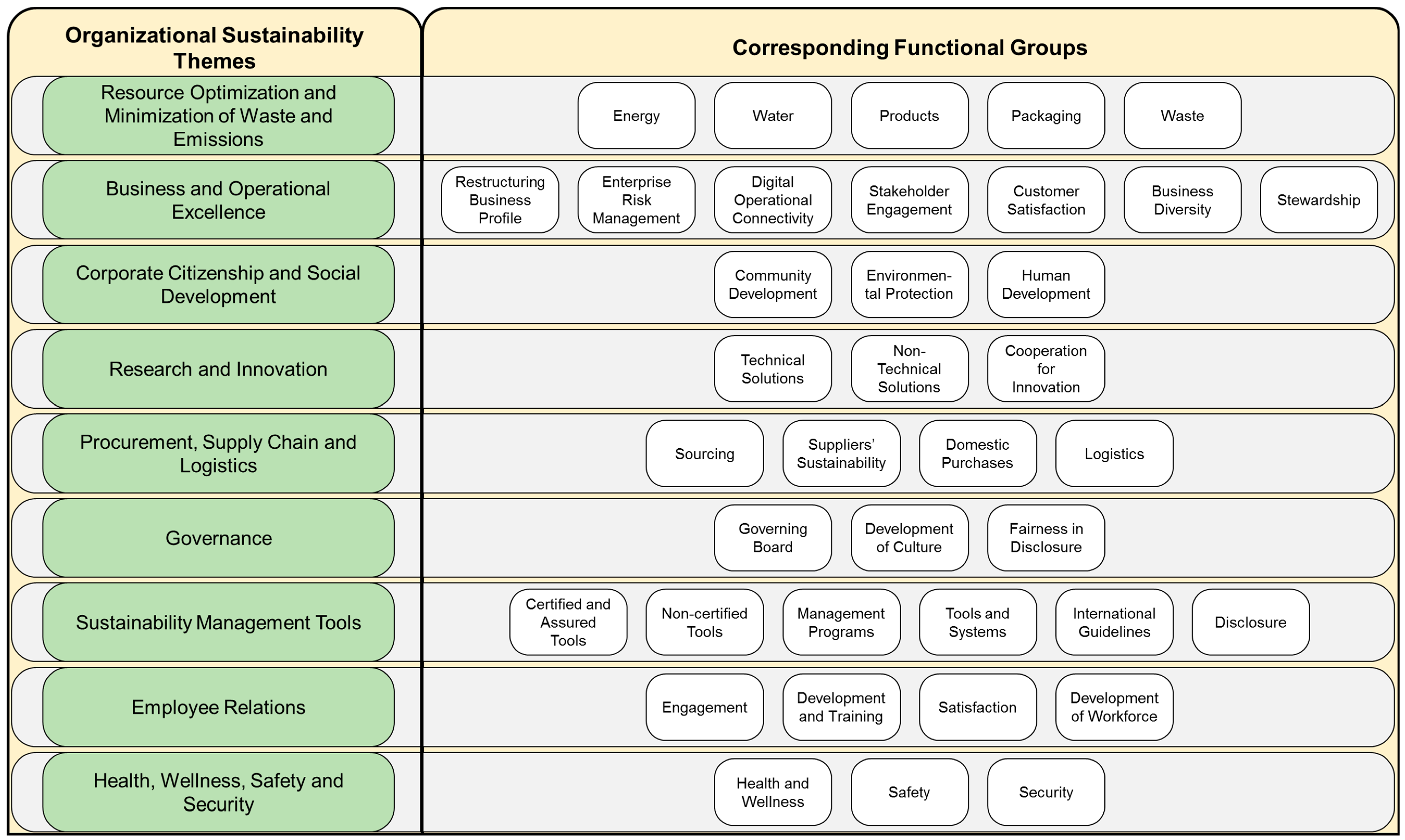

The results of the review indicate that there are nine main themes, which help the most sustainable organizations in outperforming the rest of the firms with regards to sustainability. Each theme corresponds to functional areas and best practices. The following sub-sections will discuss these sustainability themes, functional areas, and best practices in detail.

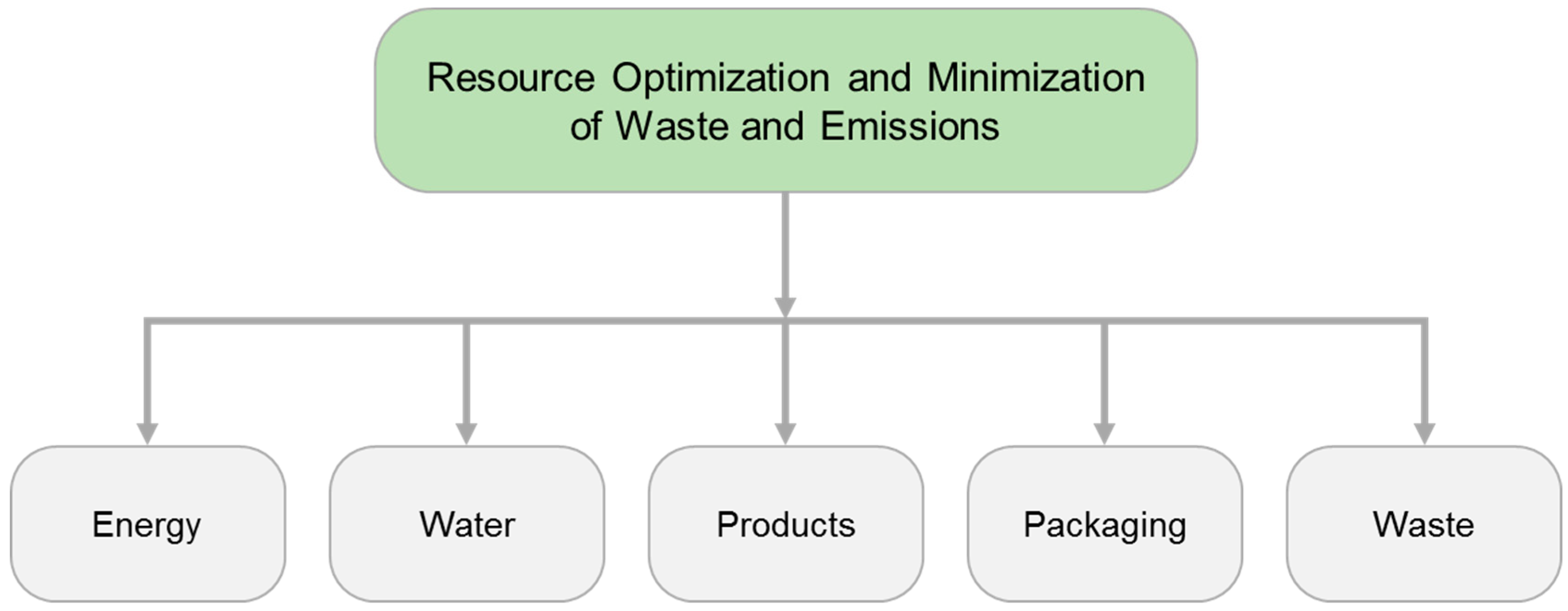

4.1. Resource Optimization and Minimization of Waste and Emissions

The functional areas of ‘resource optimization and minimization of waste and emissions’, as shown in

Figure 4, reflect on the firms’ performance in transforming the inputs to outputs by using minimum and efficient resources. This theme also signifies the importance of sustainability in the production and packaging operations, and for the end-of-life management of waste.

The best practices and the representative examples of the functional areas of ‘resource optimization and minimization of waste and emissions’ are shown in

Table 2. By performing well in these areas, the organizations, besides reducing their emissions and wastes, elevate their public image and reputation. Similarly, from the financial perspective, these activities raise the quotient of financial returns of the firms, whether it is the decrease in the fixed costs associated with energy and water, or the financial recovery from recycling and reusing activities.

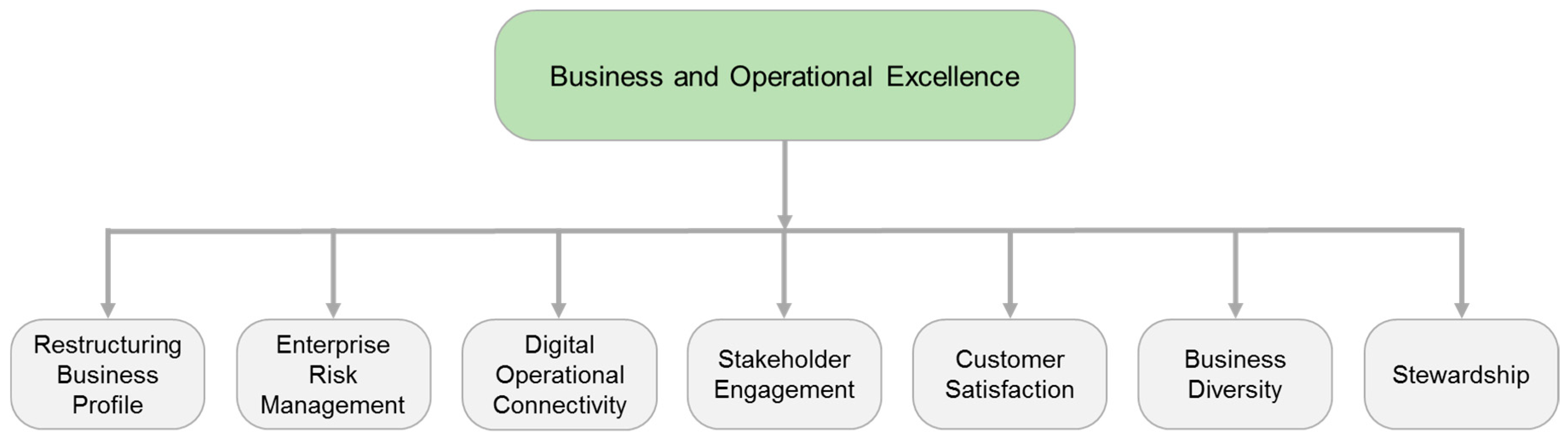

4.2. Business and Operational Excellence

The functional areas of ‘business and operational excellence’, as shown in

Figure 5, reflect on sustainability in modern business operations. While some of these functional areas are applicable to any business, regardless if it is sustainable or not, the organizational activities in these functions greatly impact the potential of economic development of the firm, which is usually neglected in the conventional sustainability management models.

By performing well in these areas, most of the organizations achieve the primary objective of their existence—to make profit. However, the way of making profit makes these organizations different from other firms—more conscious and responsible in their actions and decisions. Moreover, doing well in these functions leads the organizations to less operational errors (through better monitoring), more business opportunities (through sublime reputation), and more satisfied customers (through improved offerings). The best practices and representative examples of ‘business and operational excellence’ are tabulated in

Table 3.

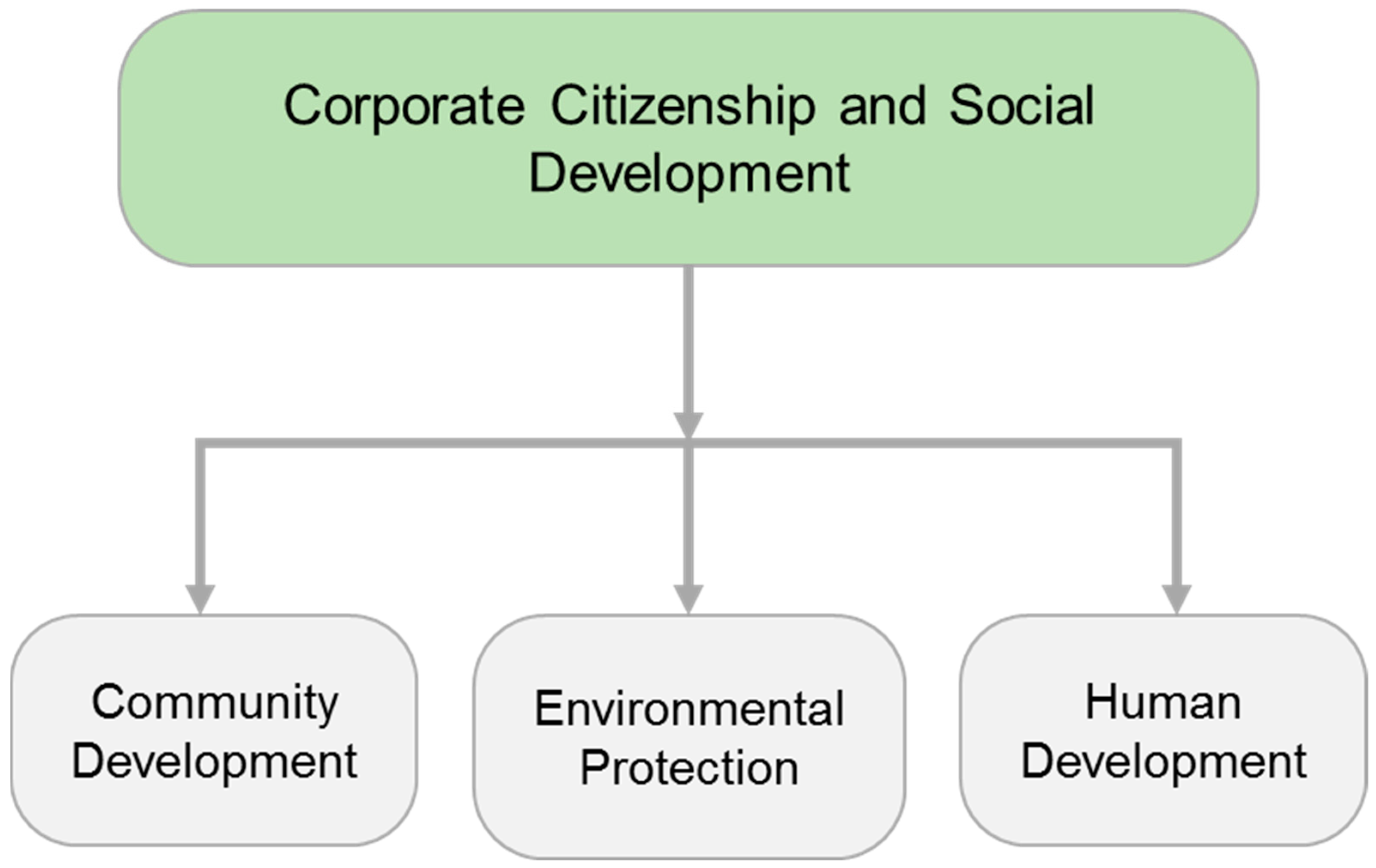

4.3. Corporate Citizenship and Social Development

Although compliance with international laws and regulations earns firms the legal license to operate, it is the quest of social license which drives these firms to think beyond organizational boundaries. Corporate citizenship refers to the responsibilities and the voluntary actions of the organizations towards betterment of societies, where these organizations generally operate. The goal of the firms as responsible corporate citizens is to boost the development activities in the communities by helping and empowering the neighboring and disadvantaged population. The functional areas of ‘corporate citizenship and social development’ are shown in

Figure 6.

Doing well as a responsible corporate citizen of the society has a number of advantages: besides the ‘feel good factor’, social activities significantly improve the marketing and public relations of organizations, along with an elevated brand image. From the receiving point of view, these activities primarily empower the people and protect the environment. At the same time, the positive image of organizations increases their chances to attract new talent, while retaining the existing staff. Concisely, these activities help the firm and the society to grow together in the globalized world. The best practices and the corresponding examples under ‘corporate citizenship and social development’ are provided in

Table 4.

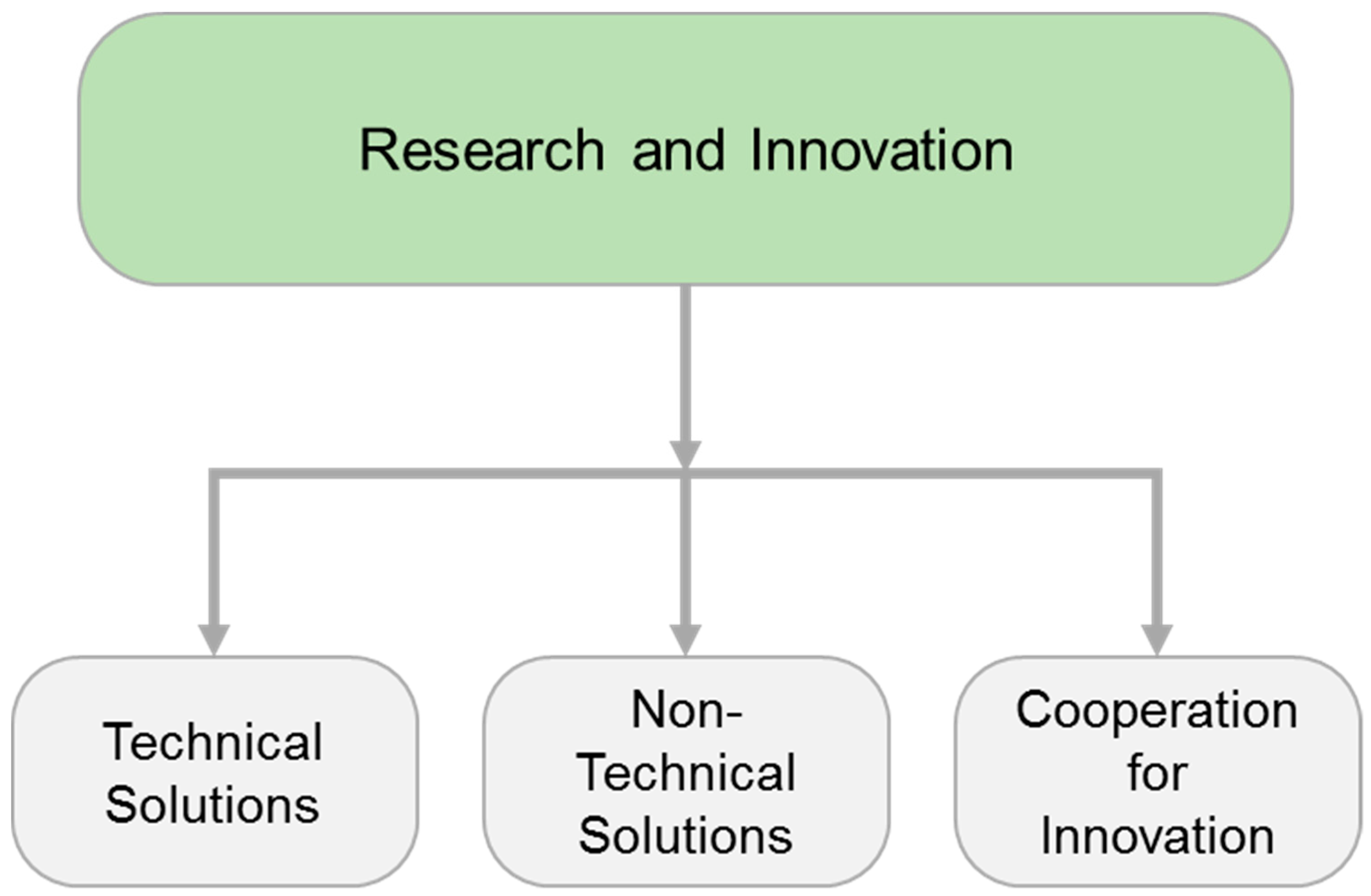

4.4. Research and Innovation

Activities related to research and innovation allow the firms to align their operations, processes, and offerings with the ever-changing needs of the modern world. In fact, the research and innovation quotient of a firm determines its potential of being a responsible manufacturer, retailer, or service provider. Naturally, the engineering organizations, or the techno-firms, such as Schneider, GE, and Siemens, have an advantage in this regard since these firms strategically rely on the development of new products and services to ensure their success in the market. Nevertheless, non-engineering firms also improve their offerings by creating innovative opportunities. The functional areas of ‘research and innovation’ are shown in

Figure 7.

Doing well in these functions helps firms in transforming from conventional business to ones where sustainability becomes the business-as-usual. It is important to note that besides collaborating with each other, these firms also pull the small business and individuals with new ideas to the main stream. This is extremely important in the modern perspective where organizations are expected to think globally but act locally. Working with small businesses enables these organizations to address the domestic challenges in the local context. The best practices and the corresponding selected examples of ‘research and innovation’ are presented in

Table 5.

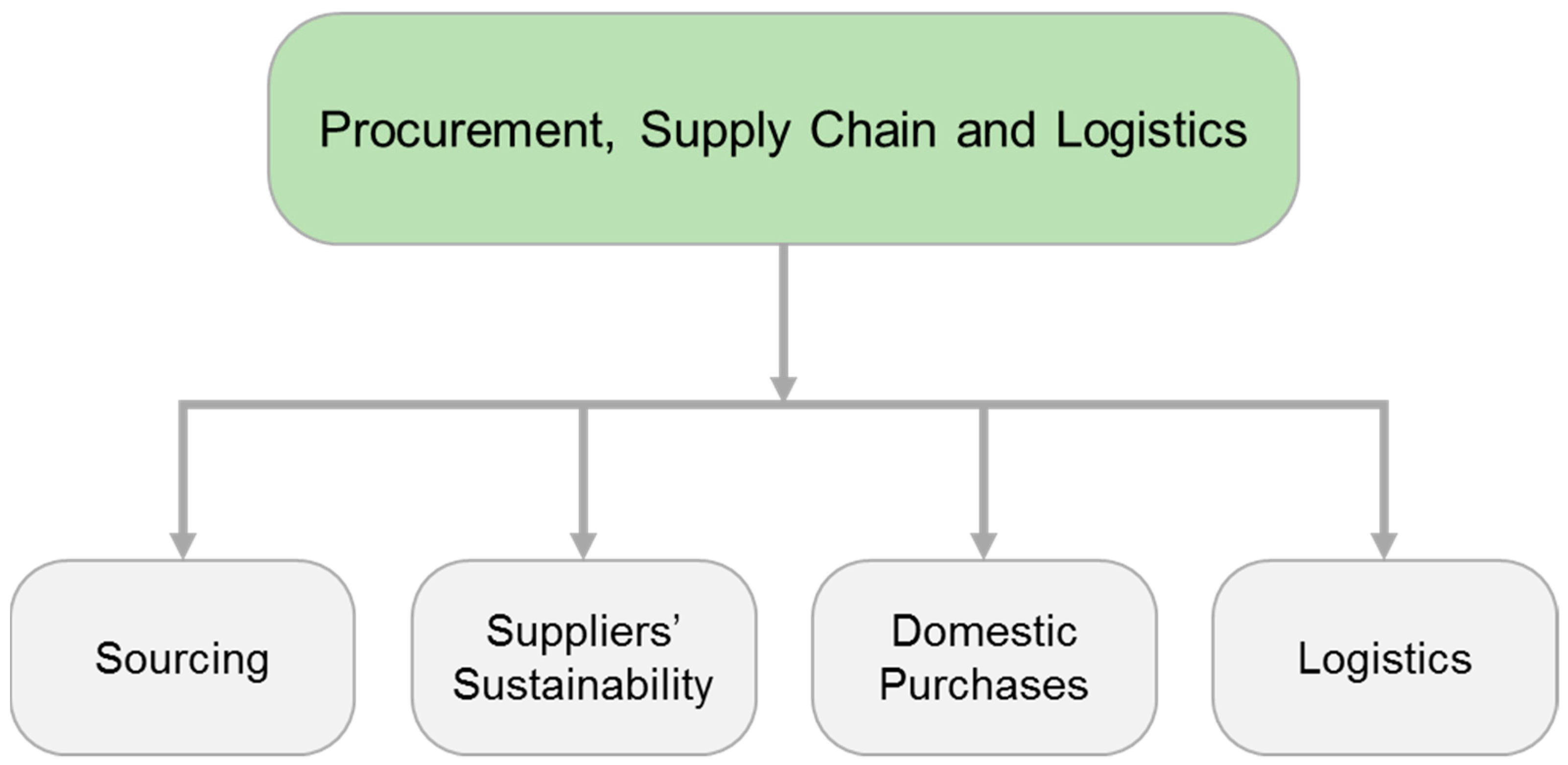

4.5. Procurement, Supply Chain and Logistics

Procurement and supply chain are considered as the weak links in organizational sustainability since the firms have limited control over suppliers’ activities. Nevertheless, the suppliers’ actions can directly affect the reputation of the firm, which is why most sustainable organizations under discussion make solid arrangements to ensure strict compliance of suppliers’ actions with the organizational vision, policies and programs. On the other hand, logistics is one segment which is in control of the organization and is, in fact, a low-hanging fruit from the sustainability perspective. The functional areas of ‘procurement, supply chain and logistics’ are shown in

Figure 8.

Initially, the organizations must pull the suppliers and contractors up in order to embark on the sustainability journey together. But after two to three cycles of monitoring and improvements, these suppliers and contractors are expected to self-develop in line with their operations and challenges. The development of suppliers eventually means a low burden (environmental and financial) on the firm’s operations and performance. Similarly, sustainability in the logistics segment means optimized channels of receiving and delivering goods and services, and more efficient ways of employees’ transportation, all of which reduces the environmental emissions on one hand and reduces the financial burden on the organization on the other. The corresponding best practices and examples of ‘procurement, supply chain and logistics’ are tabulated in

Table 6.

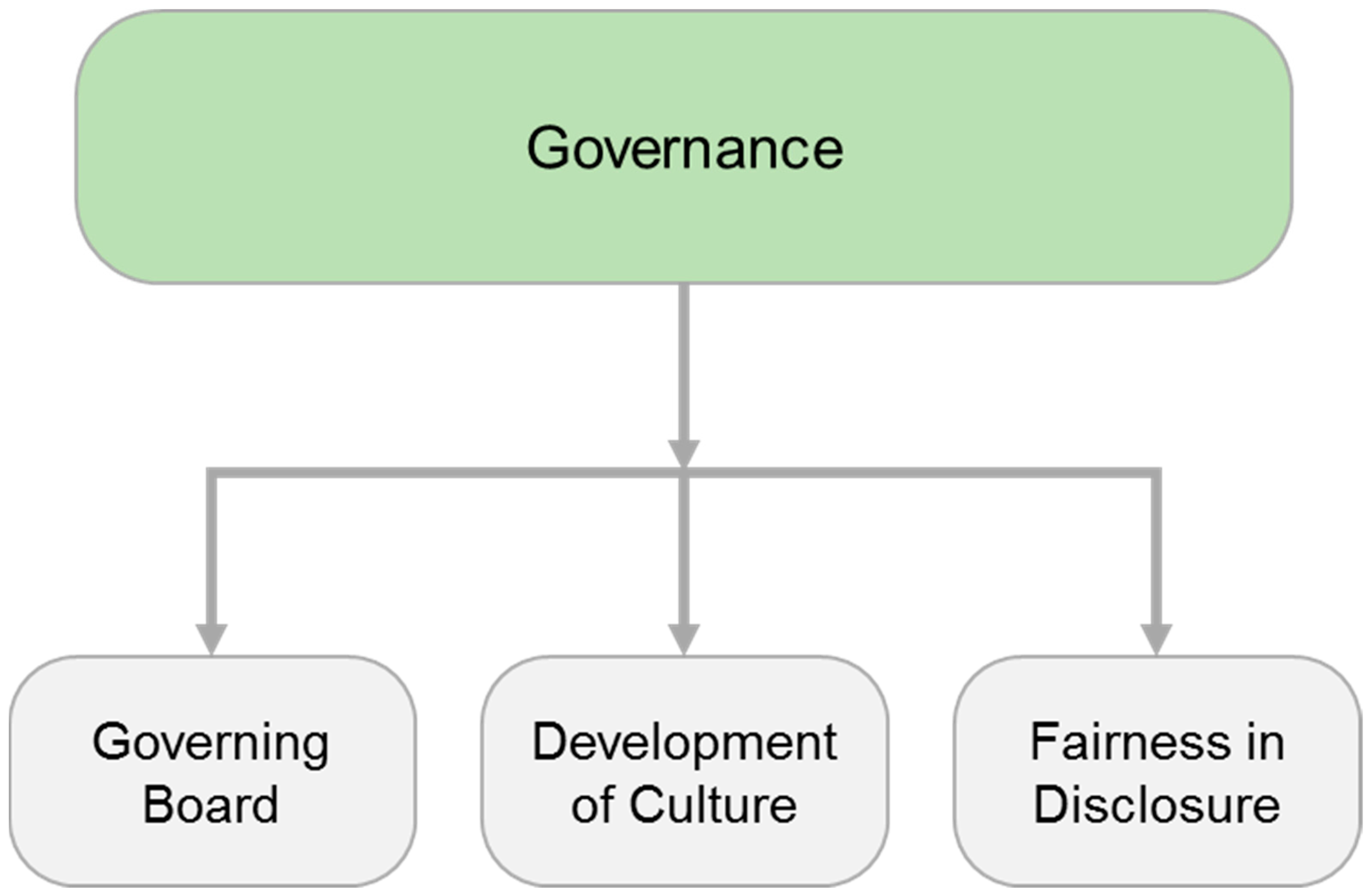

4.6. Governance

The role of governance in organizational sustainability is crucial from the perspective that the commitment of leadership, strategic alignment of company’s programs, and a clear direction for development are all linked to how well the governing bodies perform. Typically, organizations follow various guidelines to facilitate executives in governing activities, including but not limited to: OECD guidelines for multinational corporations, the universal declaration of human rights, UN declaration and guiding principles on business and human rights, ILO convention on the fundamental rights and principles at work, ICC business charter for sustainable development and principles against corruption and bribery, UN global compact initiative, and the code of conduct of the business social compliance initiative. These guidelines facilitate the firms in rolling-out initiatives and programs to deal with the governance-related sustainability issues, such as ethical misconduct, discrimination, harassment, human rights violation, corruption, fraud, bribery, embezzlement, conflict of interest, power abuse, prevention of competition, privacy breach, and whistle blowing. Providing an account on all of these will not be possible in this article. Therefore, we will discuss only some of the governing factors (

Figure 9) which are generally considered important for sustainability.

Good governance of sustainability-related issues helps the firms in creating a flourishing sustainability culture which eventually leads to a continuous evolution and development of organization—a shared trait among the most sustainable organizations. The best practices and corresponding examples of ‘governance’ are provided in

Table 7.

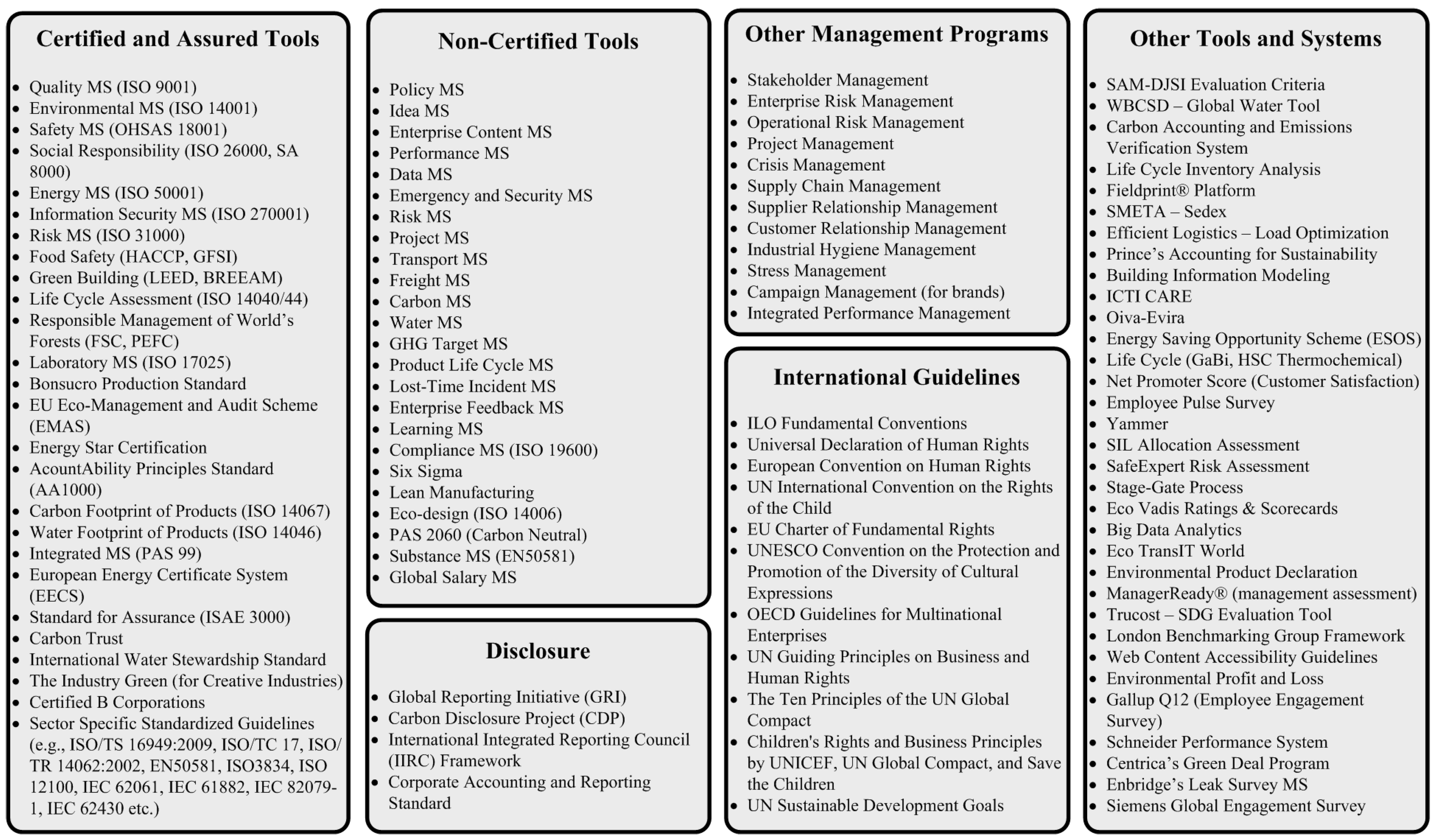

4.7. Sustainability Management Tools

While governance decisions provide broad guidelines at the strategic level, the operation managers require appropriate tools to execute the strategies and monitor and report the related activities. These tools can be the certifiable and non-certifiable systems or standards, or other systematic methods. Some of the sustainability management tools commonly used by the most sustainable firms are shown in

Figure 10.

There are also some customized tools which organizations have developed, or outsourced, to address their specific needs. For example, H&M uses an Environmental Impact Measurement tool, developed by a Spanish consultancy firm, Jeanologia, to assess the environmental impacts of its products. The products with lowest impacts are green-labelled as ‘Conscious Products’. Similarly, Schneider has developed its own tool to measure the firm’s sustainability performance, namely the Planet & Society barometer. The Planet & Society barometer allows the French firm to measure the extent of achievement of its objectives by using composite indicators. Each objective is assigned a score out of 10, based on the level of achievement. A status-review is carried out every quarter of the year to adjust the firm’s activities in order to achieve high scores for all objectives.

Henkel has also developed a systematic tool for measuring sustainability performance, namely Henkel-Sustainability#Master®. This matrix-based tool allows Henkel to align its operation in such a way that the impacts of the firm’s activities, throughout the value chain, are minimum. The tool has a ‘focus areas’ on the y-axis (performance, health and safety, social progress, materials and wastes, energy and climate, water and wastewater) and the steps in the value chain on x-axis (raw materials, production, logistics, retailing, service/use, disposal). The impact of each product is assessed on focus areas throughout the value chain. This helps the firm in identifying the hotspots and creating value. Similar to Henkel-Sustainability#Master®, RB uses its Sustainable Innovation Calculator to measure its net revenue generated from the sustainable products. The lifecycle-based tool guides the firm in the development of low-impact products.

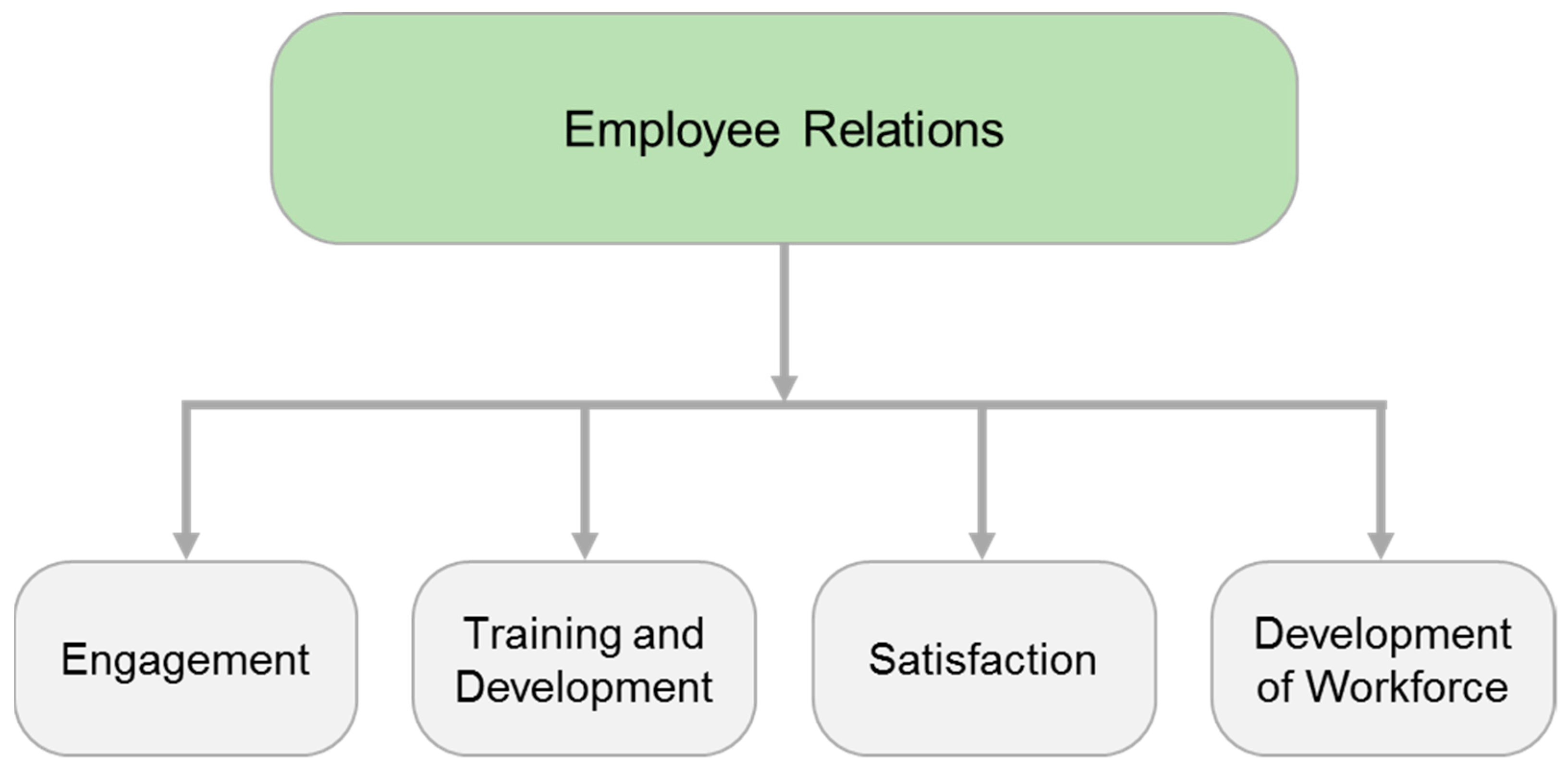

4.8. Employee Relations

Sustainability in the workforce is as important for the organizations’ sustainability as the sustainability of organizations for the world itself. Employees are at the heart of organizational operations since these are the behind-the-scene actors who run the real show. The success of other sustainability themes, such as innovation and research and customer satisfaction, is linked with the performance of employees. A good relationship between employees and the firm, and among the employees themselves, helps in developing a positive workplace culture and thus, ensures effective implementation of organizational policies and programs.

Since there are numerous employee-related initiatives which the firms roll-out, we will only discuss the important functional areas of ‘employee relations’ (

Figure 11) which are generally applicable to all organizations.

For the most sustainable organizations, the ‘development of organization’ is interchangeable with the ‘development of employees’; an organization which puts the engagement, development and satisfaction of employees ahead of other priorities ultimately performs well on all facets of sustainability, including the financial dimension. More specific best practices and corresponding examples of ‘employee relations’ are shown in

Table 8.

4.9. Health, Wellness, Safety and Security

While most organizations tend to ignore health and safety during the strategic alignment of their business activities (overly emphasizing on the environmental side), the most sustainable firms do the exact opposite; the firms under discussion make use of the health, wellness, safety, and security measures to create value for their customers, shareholders and other stakeholders. Conventionally, this theme is limited to health and safety measures taken to protect people, property and the environment. The other two segments, wellness and security, are relatively more recent and are integrated with health and safety because of the common goals and objectives of these disciplines. The functional areas of ‘health, wellness, safety and security’ are shown in

Figure 12.

The significance of this research theme for sustainability can be better explained by considering the opposite effect: how will an accident or the breach of data privacy affect the sustainability of an organization? While the breach of data privacy may result in a long legal battle leading to mammoth fines and penalties, and consequently to a poor image of the firm, hurting the customer-base, the occupational accidents may result in the loss of lives, and can cause further financial and environmental damage, through the destruction of property and equipment, in addition to the unwillingness of talented people to join the firm in the future. Consequently, the impacts of such an event may leave a permanent mark on the culture and reputation of the firm. The best practices and the corresponding examples related to ‘health, wellness, safety and security’ are provided in

Table 9.

5. Discussion

Based on the findings of the systematic review of organizational reports, as tabulated in

Table 2,

Table 3,

Table 4,

Table 5,

Table 6,

Table 7,

Table 8 and

Table 9, a content framework (CF) for organizational sustainability is proposed (

Figure 13). With nine sustainability themes and 38 corresponding functional areas, CF holistically covers the elements of organizational sustainability. Nevertheless, the sustainability themes outlined in this work must not be considered in isolation since organizational operations are usually interlinked and therefore, it is important to admit a holistic approach for using CF in practice and research.

More importantly, CF only represents the content of organizational sustainability; it cannot be operationalized without integration with a compatible structural framework. In this regard, Nawaz and Koç [

4] developed a structural framework for sustainability management based on an extensive review of sustainability management and assessment literature and the international standardized guidelines. The authors proposed a six-element cyclic framework, namely Sustainability Management Framework (SMF), which compliments CF. Hence, the integration of CF and SMF can enable the firms to manage the context-specific sustainability challenges in a holistic manner.

While the sustainability themes provide holistic coverage around the organizational operations, it is worth noting that a firm’s standing on the quantitative sustainability ranking is not necessarily linked with the firm’s performance in these themes, rather there are host of other external factors which can cause a shift in organization’s ranking. For example, we observed during the review that a warm winter may reduce the demand of clothing and utilities business (e.g., M&S and Centrica), consequently affecting the financial performance of firms in these sectors. The under-par financial performance will be subsequently reflected in low R&D investment, low or no donations for charities, low or no variable compensation for employees, and hence, a low employee satisfaction level. Since all of these measures play a crucial role in determining the sustainability ranking of organizations, it may just be the warm weather which leads to a lower sustainability ranking of an organization in a particular year.

Similarly, the indicator-based assessments may fail to evaluate the sustainability management potential of firms [

50]. It is primarily because the fluctuations in the indicators may raise or lower the position of an organization in quantitative rankings, but actual reasons behind the fluctuations remain undiscovered. For example, the total water intake and the total waste generated by Siemens in 2013 was 4% and 5% higher than the 2012 value, respectively. On a quantitative scale, such as Global 100, these two measures could have affected the ranking of Siemens, but in reality, these changes were a consequence of the acquisition of new Siemens facilities in China in the same year. Similarly, Siemens’ health care business saw a 4% decrease in the net sales value of 2013, compared to the previous year. However, this decrease was primarily due to the 5% negative currency effect. If the currency effect is normalized, Siemens’ comparable sales in 2013 would increase by 1% from that of the previous year. This is probably why many researchers advocate that the indicator-based performance assessment does not fully reflect how well a company addresses sustainability-related issues [

51,

52].

It was also observed that the shift in organizational ranking from 1 year to another may be a result of several secondary reasons: (i) the increase or decrease in the emissions due to the acquisition of new sites or closure of existing facilities, (ii) the change in the definition of quantitative measures (green products, global warming potential of refrigerants, corporate givings, age of senior employees, etc.), (iii) the one-off disposal of a large amount of waste due to its replacement with more efficient materials/methods/products, (iv) the political instability in countries where suppliers operate, (v) the change in emissions’ regulations and environmental impact factors, (vi) the implementation of cost structure programs to revise the business profile and headcounts, (vii) the negative currency effect, and (viii) increase or decrease in the sales volume. Nevertheless, it is important to note that the organizations usually address these factors in corporate and enterprise risk assessment, which is a good sign, however, it raises questions on the implementation of the risk reduction measures.

6. Conclusions

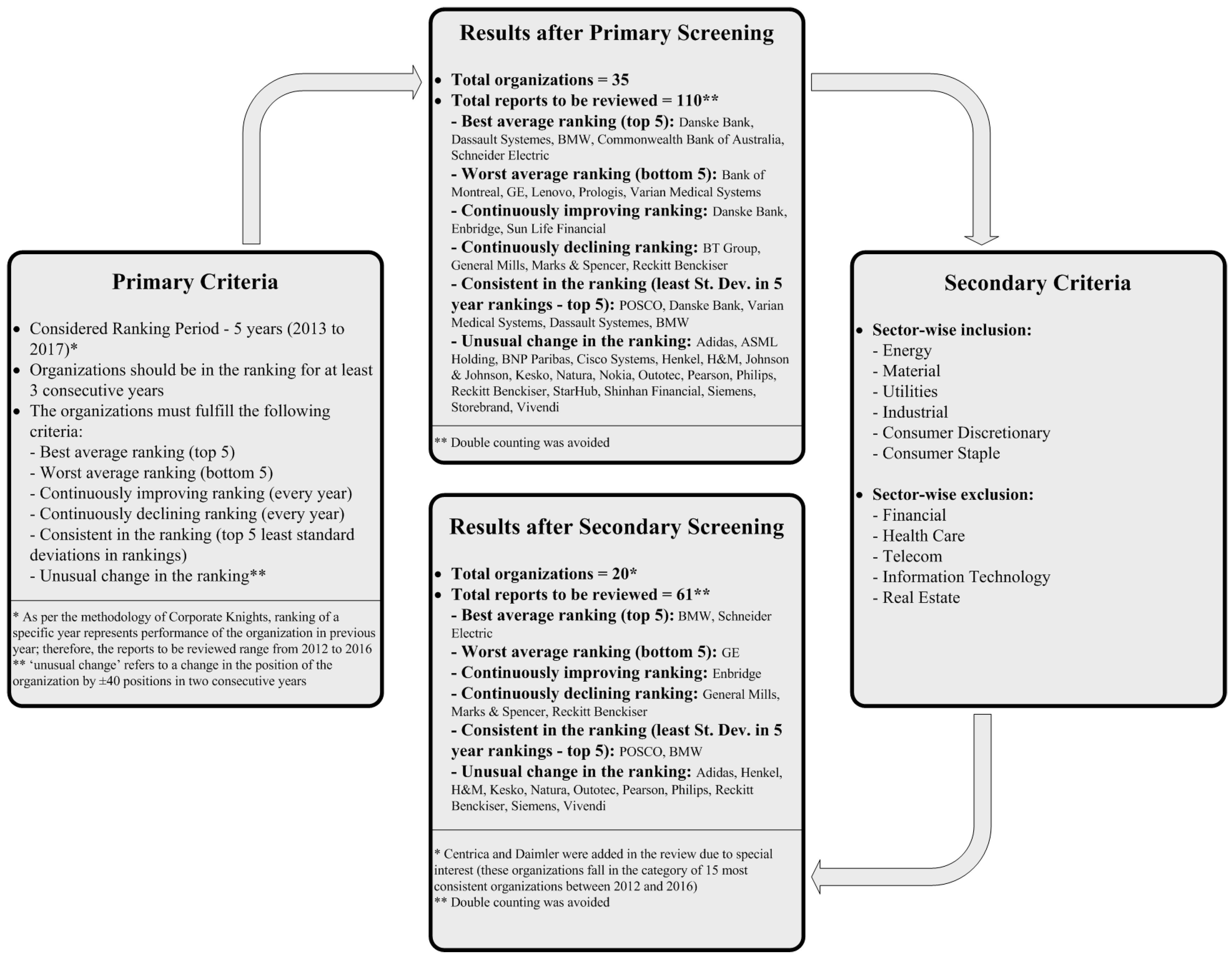

While sustainability is one of the most researched areas, the actual sustainability practices of organizations are usually overlooked in the management research. It is extremely important to bring a practical perspective to theoretical discussions in order to create a synergy between theory and practice. Such an approach will enhance the potential application of the theoretical models on one hand and will help in understanding the practical limits of the organizations on the other. The present work is an effort to systematically identify the organizational sustainability themes, functional areas, and best practices of most sustainable firms in the world.

The starting pool of 100 organizations was obtained from the 5-year rankings (2013–17) issued by Corporate Knights (Global 100). From the initial pool, we identified 20 most sustainable firms which are relevant to the context of this study and a corresponding 61 organizational reports through systematic screening. The review was carried out by using grounded mechanism. The results highlight nine main themes and 38 functional areas to maintain an exceptional sustainability performance in an organizational context (

Table 2,

Table 3,

Table 4,

Table 5,

Table 6,

Table 7,

Table 8 and

Table 9). Based on the findings, we have proposed a content framework (

Figure 13), which offers a comprehensive account on the organizational sustainability management.

The present work is unique from previous studies in four ways. First, it adopts a systematic methodology for conducting the review which offers comprehensive and reproduceable results. Second, this research accounts for the organizational sustainability practices over a period of 5 years, which was mostly limited to a single year in similar previous works. Third, this study does not limit the selection of organizations to a single geographical location. Finally, this work is not limited to the review of strategic initiatives only, rather micro-level practices are also discussed in order to contemplate the entire spectrum of organizational sustainability management.

Like any other study, this work also has some assumptions and limitations. First of all, since the initial pool of organizations was obtained from the Corporate Knights Global 100, all assumptions and limitations of Global 100 are applicable to this work. Also, the screening criteria, and especially the sector-wise exclusion, may have eliminated some organizations, and subsequently the organizational reports, which could have benefitted this study.

In future, researchers may seek empirical validation of the proposed content framework through expert survey. Moreover, it will be interesting to examine if the sustainability themes of the organizations which were not considered due to sector-wise exclusion are similar to the sustainability themes proposed in the content framework. If the two are different, there will be a need to integrate the themes in order to develop a holistic and generic tool for organizational sustainability management.

The authors would like to assert that this study does not intend to cross-compare the performance of organizations. This work only identifies the sustainability themes and practices which could potentially affect the organizational sustainability; the authors do not imply that these practices are a certain cause for the good standing of the firms, which would require a more rigorous causality analysis and hence, can be considered as a potential future opportunity. Moreover, the sustainability practices noted in this article with reference to one organization may not be limited to that organization only; other organizations may also be undertaking the same, or similar, activities but these have not been referred to due to space limitations. Furthermore, the review of sustainability practices has been limited to the organizational reports; the unreported activities are not reflected in this work. In addition, activities performed to exclusively comply with the national and international laws and regulations are mostly not included in this study. Finally, since the study encompasses a review of more than 7000 pages, the chances of human error cannot be completely overturned. However, the authors have done their best to ensure objectivity in each phase of the review (selection of organizations, identification of reports to be reviewed, and collection of sustainability practices) through systemization.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}