2.1. Socially Responsible Investment Theory

The socially responsible investment (SRI) theory, which is motivated by the need to invest ethically, is said to have been in practice since the ancient days of Christianity, Islam, and Judaism, respectively [

23]. As with any other complex concept, there seems to be no consensus yet regarding the definition of the SRI theory [

24]. For instance, terms such as ethical, sustainability, social, environmental, green investment, at different instances, have been inter used as a logic for SRI [

25,

26]. Moreover, community investing and impact investing are common phrases that have, on several occasions, been swapped for each other when talking about SRI theory. SRI theory centers on integrating individual value and societal wellbeing as important factors which should be considered when evaluating investment choices [

26,

27]. Similar studies viewed SRI as a social impact investment that could be in-form of direct SRI or indirect SRI, with both categories significantly enhancing the social benefits of investors and that of the community [

28,

29].

The SRI theory focuses on encouraging the use of finance in the actualizations of both financial and other life goals [

30], and socially motivated financial firms, such as the micro finance institutions, have over the years, been used for solving environmental challenges, job creation, and urban and rural development [

31]. Furthermore, the SRI theory has been empirically viewed from the social, environmental, and sustainability dimensions [

25]. The social dimension focuses on using finance to accomplish both financial and social values, beliefs, and goals simultaneously [

32,

33,

34,

35], the environmental dimension aims at exploring financial benefits by adopting environmentally concerned investments [

36,

37,

38], while the sustainability aspect focuses on the involvement in businesses with financial, social, and environmental benefits [

39,

40,

41].

The SRI theory serves as a blueprint which could be used to enhance the relationship between green banking practice and green image, bank trust, bank loyalty, and focusing on socially responsible investment as a means of improving sustainability performance has been considered to be of advantage to both policymakers and managers [

42]. For instance, one of the essential prerequisites of a green bank is to be socially responsible by considering the impact of intended or existing projects on the safety of the environment in a short and long term before approving loans [

43]. This results from the high demands from present-day stakeholders which have gone beyond factors such as return on investment and low risk [

44]. Investors now attach positive attitudes toward SRI because of its social and environmental benefits [

45]. This has also been considered as an important approach that could be used by firms in establishing a positive image, which in return could be instrumental for employee retention, and in strengthening the relationship between firms and customers and government [

46]. In addition, preference for social and environmental benefits is considered to have a significant influence on the investment decisions of stakeholders [

47], which can be supported by the willingness of stakeholders to trade off a significant portion of their financial returns from investments, for social benefits [

48]. Furthermore, Igbudu et al. proposed the SRI concept as an instrumental approach necessary for enhancing corporate image and bank loyalty through sustainable banking practices [

49].

2.2. Green Banking Effect

The economic hardship experienced as a result of the global economic meltdown during the period 2007–2008, called for the adoption of ideal measures in banking, that should be used for the common good of the society [

50,

51], and the green banking approach is one of the few concepts that has been identified to be appropriate in the delivery of banking products and services for the greater good of mankind [

52,

53]. As a means of ensuring an ideal energy development, green banking as a concept gained prominence in 2008 [

16], which has led to the establishment of green banks in various countries (such as Australia, Japan, Malaysia, United Kingdom, United States of America), aimed at developing green financing as an important measure which could facilitate the attainment of the green agenda at all levels of society [

54].

A banking system that is value-driven, and meets the desires of the customers by ensuring the safety of their deposits, investments and the environment is considered to be a green bank [

55,

56], and adopting a green banking approach is considered to be vital for risk reduction [

57]. The main focus of green banks is considered to be in the development of green technologies that are commercially feasible, with low risk, and could be used as a hub for generating benefits for investors [

58]. Therefore, contrary to the conventional banking approach, a green bank is one that adopts operational techniques that are beneficial to the environment [

53].

A public or seemingly public financial firm which adopts innovative techniques for financing and developing the market, in collaboration with the private sector, for the development of technologies that enhance clean energy, could be considered as some of the major characteristics of a green bank [

16]. Questions on the importance of renewable energy financing have been raised [

59], and improving the renewable energy market through financial development is considered an important approach for battling environmental challenges, such as climate change [

60]. The essence of green banking is to minimize the cost of energy for customers and improve investments that could be used to attain a minimal carbon economy [

61]. This could be achievable by utilizing public funds to grasp investment from the private sector in developing innovative technologies for clean energy. From a multi-dimensional perspective, green banking is centered on rapidly improving the growth of the clean energy market, ensuring cleaner and affordable energy for consumers, creating jobs, and safeguarding taxpayers’ finances [

16].

Adopting green values could be beneficial to banks and stakeholders because such an approach enhances operational efficiency, minimizes fraud and the cost of banking [

6]. In addition, green investment is considered as a vital tool for cementing long term relationship between firms and banks [

62]. Attaining the global environmental goal requires financial institutions, such as banks, to show greater commitment to green investments [

63]. However, achieving this goal is considered to have been hindered by the insufficiency of ‘green financing’ [

64,

65]. Developing and implementing policies that support green credit, and providing subsidies for the production of renewable energy could be considered as an important step banks could use to improve green financing [

65]. Furthermore, providing green credit for green projects that control environmental pollution is considered to be very significant for the development of green financing and the economy [

66].

Some factors serve as barriers for sufficient investment in green projects, such as green energy. For instance, insufficient documentation provided by companies seeking finance for clean energy projects present banks with little information to ascertain the benefits and importance of investing in such projects [

67]. This, in return, may discourage banks from investing in clean energy projects. From the consumer perspective, despite the considerable reduction in the cost of clean energy innovations, consumers still find it difficult to subscribe to clean energy innovations because of factors such as the upfront costs which are usually high [

68].

When talking about the importance and effect of green banking practice, customers now focus on banks that are more responsible and are concerned about and committed to preserving the environment [

69]. In line with this, present-day customers or investors do not only consider the safety of their deposit or investment as a reason for relying on a bank but also consider the prospect of their deposit or investment being used to improve the environmental and living standards of the society [

55]. A similar study conducted indicated a positive effect of green value on trust [

70]. Integrating environmental issues into marketing strategies is considered as leverage toward enhancing loyalty [

71]. Furthermore, adopting a green approach to banking as a way of enhancing sustainability is considered as an adequate measure for building a positive image of banks [

18].

The perception of customers about a firm’s value has a significant effect on the loyalty of such a customer to the firm [

72]. A similar study indicated that the post-purchase behavior of a customer is hugely affected by the customer perception of a firm’s value [

73]. Furthermore, Chen posited that there is a positive relationship between green value and loyalty [

70]. Based on the above assertions, we propose the following hypotheses:

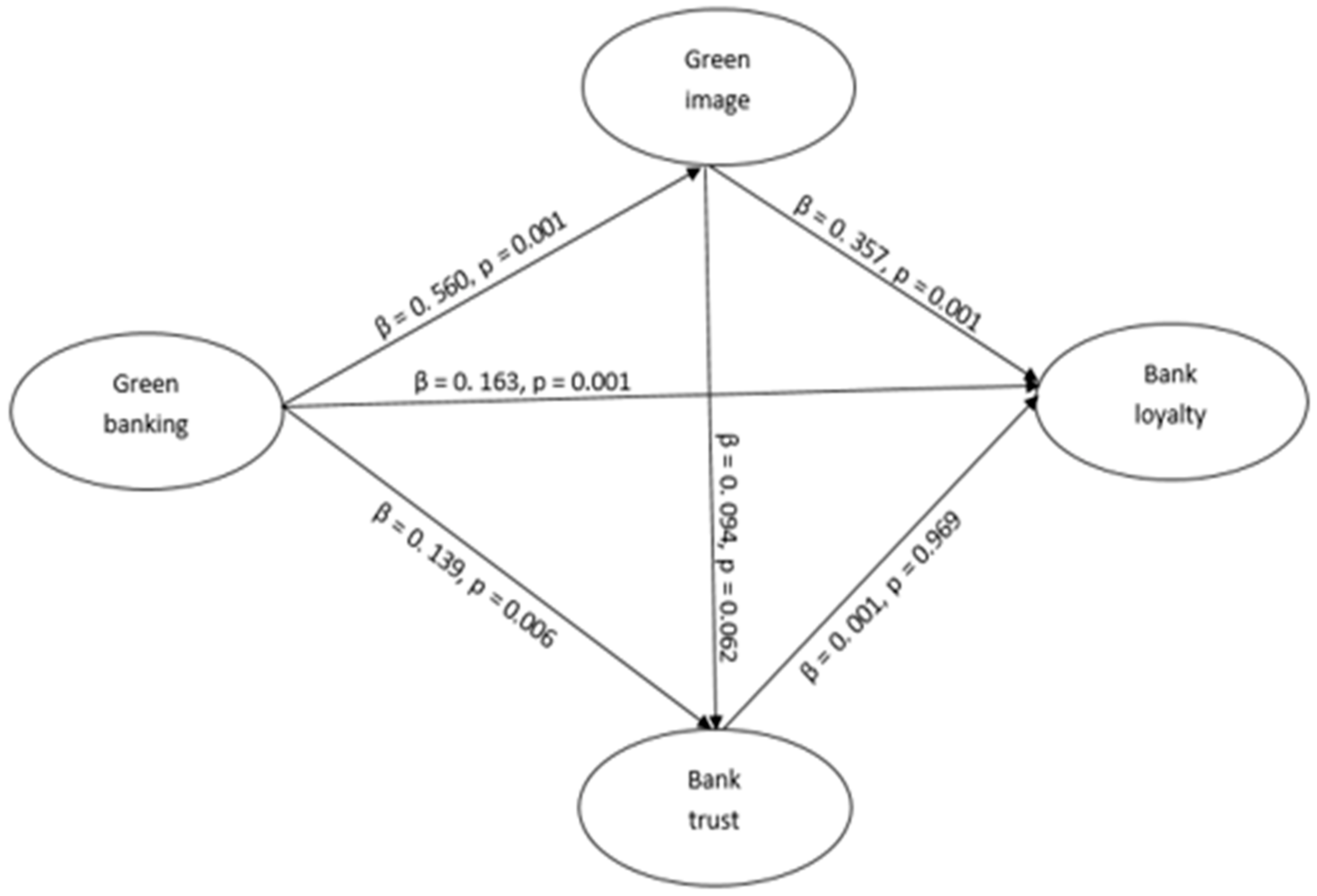

H1.The relationship between green banking practice and green image is significant.

H2.The relationship between green banking practice and bank trust is significant.

H3.The relationship between green banking practice and bank loyalty is significant.

2.3. Green Image Effect

The call for more environmental or green approaches to be integrated with other approaches for marketing goods and services has been trending over the decade [

74]. This is as a result of the willingness of individuals to spend more on green products and services [

17,

75]. Moreover, the benefit of a pro-environmental society to social wellbeing is considered to be higher in societies where individual green self-image is high [

76], and according to research, individuals with a high green self-image tend to be more satisfied with life [

76,

77].

There seems to be a relationship between the concepts of green image and corporate image. This is because the activities of firms which affect nature and the environment have become an important factor for building corporate image [

78]. Furthermore, communicating the environmental commitments, which represent the green image of any given firm, significantly enhances the overall corporate image of such a firm [

22].

Stakeholders’ perception about firms, which could be through the various signals (corporate vision, culture, company’s name, and logo) a firm present to the public, determines the image of a firm [

20]. Therefore, adopting a positive attitude toward environmental issues creates an environmentally-friendly image that could be used in building a green image [

79]. There are several benefits a firm could gain from adopting or having a green image. For instance, having a green image reduces scrutiny from the government and non-governmental organizations [

80], and consolidates firm–stakeholder relationships [

81]. This stresses the need for firms to frequently communicate their environmental commitment to the public as a way of showing concern for green issues [

82].

Managing the image of banks should be the responsibility of all involve in the operational activities of the bank [

83]. Furthermore, when corporate social responsibility is perceived by stakeholders to be ideal, which could be built by the green innovative awareness of a firm, the trustworthiness of such a firm to deliver on its promises is improved [

82]. In addition, firms that build a positive corporate image are likely to improve customers trust, and the possibility of the customer communicating positively about the firm is likely in such situations [

84]. Further research on the effect of green image on green trust indicated a positive relationship between both variables [

85].

When talking about the determinants of loyalty, patronage could be repeated on a product or service whose firm maintains a positive image [

21]. Moreover, customers maintain a loyal relationship with firms that present a good corporate image [

86]. Findings from a related study opined that the level of loyalty could be determined by the perception of customers about the corporate image of a firm [

87]. In addition, a similar study identified a significant impact from the corporate image of firms on loyalty [

88]. Therefore, it is in line with the above mentioned, we propose the following hypotheses:

H4.The relationship between green image and bank trust is significant.

H5.The relationship between green image and bank loyalty is significant.

2.4. Bank Trust

The situational nature of trust makes it difficult to conceptualize [

89]. This has attracted significant attention on trust from various disciplines and in various contexts [

90]. Trust could be defined as a conviction that an actor will act in accordance with expected behaviors [

91,

92,

93]. From the green perspective, relying on a firm based on their green commitment and performance could be considered as green trust [

94]. Trusting a financial firm could be described as an individual having confidence that their deposit or investment is safe with the financial firm [

95]. Furthermore, trust is considered as an important factor for financial system effectiveness [

96] and is also considered to be an essential factor for sustaining the relationship between banks and customers [

97].

There are several factors that have been identified as a determinant of trust. For instance, the compatibility of value which could otherwise be seen as value congruent is considered to be an important determinant of trust [

98]. In addition, factors such as competence, customer orientation, integrity, transparency, are considered as important factors that influence trust [

97]. A related study opined that security, reputation, mobility, and customization are important determinants of trust [

99]. From the banking perspective, factors such as self-reported wellbeing, financial status are considered as influential determinants of bank trust [

100]. The ability to act reliably, adhere to principles, and show commitment to the interest of the public has, in a different study, been considered as the determinants of bank trust [

101]. The geographical proximity of a financial service provider has also been seen as a determinant that builds trust [

102]. This is because an individual’s inability to reach their bank physically within a day likely diminishes the level of trust of such individual in the financial firm.

There are several studies that emphasize the importance of trust in the firm–customer relationship [

103,

104,

105,

106]. In line with this, the level of trust customers have in a company is considered to have a significant influence on the loyalty of the customer to the company [

107]. A further study conducted by van Esterik-Plasmeiber and van Raaij discovered the importance of trust on bank loyalty [

97]. From a more precise perspective, Chen indicated a positive impact of green trust on green loyalty [

70]. Based on this finding, we propose that:

H6.There is a significant relationship between bank trust and bank loyalty.

{kind=link}