1. Introduction

The manufacturing industry plays an important role in promoting the world economy [

1]. With the rapid development of information technology, the Internet is promoting the transformation of industrial structures, and modern manufacturing enterprises are undergoing a critical period of transformation, upgrading and leapfrogging development [

2]. In recent years, great changes have taken place in the social environment faced by the manufacturing industry, such as increasingly fierce global market competition and diversified customer demands [

3]. Due to the transformation of the economic situation in China, the gradual rise of labor costs, the weakening of the demographic dividend advantage, and the tightening of environmental and resource constraints, manufacturing enterprises that want to develop better face enormous challenges [

4,

5]. As a major component of the manufacturing industry, small and medium-sized manufacturing enterprises are also playing an increasingly important role in promoting national economic growth, increasing employment opportunities, promoting technological innovation, and maintaining social stability. However, the management and operation of enterprises have become more and more complex, which reduces the adaptability of organizational capability and technology research and development capability [

6]. In the process of production and operation, small and medium-sized manufacturing enterprises often encounter some tough problems, such as a lack of funds, incomplete production facilities, and immature production technology [

7]. These issues have limited the sustainable development of small and medium-sized manufacturing enterprises, which has been severely squeezed in the increasingly fierce market competition. What small and medium-sized manufacturing enterprises should focus on is how to manage and improve existing key factors and achieve sustainable growth, and these key factors include productivity, quality, and flexibility [

8].

The sharing economy, which is also known as “collaborative consumption” or the “collaborative economy”, was first proposed by professor Marcus Felson and professor Joel Spaeth in 1978, and defined those events in which one or more persons consume economic goods or services in the process of engaging in joint activities with one or more others [

9]. Over time, the significance of the sharing economy is also changing. We agree that the operation of the sharing economy depends on the Internet platform, on which people can allocate underutilized resources and get compensation, or get resources and pay corresponding fees [

10,

11]. In recent years, due to the rapid development of mobile Internet and information technology, the sharing economy, a new business model, has attracted much attention and achieved success on a global scale [

12]. The sharing platform, an important component of the sharing economy business model rather than the traditional business model, relies on the Internet to act as an intermediary between suppliers and demanders [

13]. Contrary to the traditional business model based on ownership, the sharing economy is established on the use and sharing of products and services, which emphasizes the right to use resources rather than the transfer of ownership [

14,

15]. The sharing economy is different from the traditional business model and even surpasses it, which disaggregates resources and services in time and space; thereby, it has become a competitive business model [

16]. This economic model can not only meet the needs of demanders, but also reduce the waste of resources, alleviate the pressure of the ecological environment, and further cater to the concept of sustainable development by making rational and effective use of offline idle materials or labor services. For both suppliers and demanders, the business model of the sharing economy can also effectively reduce transaction costs and maximize the profits of both parties [

17]. Firstly, the Internet optimally matches demanders and suppliers, reducing the cost of information acquisition and time cost. Secondly, the shift of demand from buying to renting greatly reduces the direct cost of resource acquisition, while the rational and effective allocation of resources by suppliers can reduce the idle cost of resources and obtain additional benefits. Nowadays, due to its efficiency, convenience, and low cost, the sharing economy has penetrated into multiple fields in life, such as Uber in the taxi industry, Airbnb in the hospitality industry, and Lendico in the P2P lending field [

13]. The boom in the sharing economy is going on and on. Further, it is estimated that the sharing economy was worth

$15 billion in 2015 and is expected to rise to

$335 billion by 2025 [

18].

The emergence of the sharing economy undoubtedly provides a good opportunity for small and medium-sized manufacturing enterprises, which can help solve problems such as insufficient financial strength, incomplete production facilities, and immature production technology. Choi [

19] believed that the sharing economy platform was worthy of use, and may help enterprises achieve cost reduction and economies of scale. Meanwhile, Martin [

20] put forward another point of view that the sharing economy can create economic opportunities and achieve sustainable development for enterprises. Based on these studies, we have reason to believe that small and medium-sized manufacturing enterprises can establish a mutually beneficial relationship with other enterprises through engaging in the sharing economy, where they can rent the equipment, technology, and other resources needed in the production and development process at a low cost. Engaging in the sharing economy not only alleviates the financial pressure, reduces manufacturing costs, and improves the production efficiency on enterprises, it also promotes the sustainable development of the manufacturing industry. However, the research and applications of Engagement in the Sharing Economy of Manufacturing Enterprises (ESEME) are still limited, and ESEME is affected by many factors such as the macro policy, market situation, and maturity of the sharing platform, so there are certain risks in the process of ESEME. It is necessary to implement risk management in order to help small and medium-sized manufacturing enterprises accurately identify risks, reduce irreparable losses, and ensure the maximum benefits of enterprises in a more timely manner in the process of engaging in an uncertain sharing economy [

21].

At present, there are a few studies on the sharing economy, which are basically qualitative research on the impact of the sharing economy. The existing literature has studied perceived risk and online risk in the sharing economy, and rarely involves the research of risk assessment methods [

18,

22]. For example, Ert et al. [

23] considered that transaction information in the sharing economy is often asymmetrical, and both sides of the transaction are prone to a crisis of trust. Kim et al. [

24] have studied how increasing the reliability of the sharing platform can reduce the perceived risk of users. However, the risks faced by manufacturing enterprises can be subdivided by different life cycle phases, different sources, and different categories [

25]. For instance, by sources, risks stem from enterprises’ strategic actions, competitors, or environmental forces [

26]. In addition, the enterprise risk management model or risk management based on the supply chain has been extensively studied [

27,

28]. This work is one of the first studies to explore the risk of ESEME. After long-term research and practice, there have been many generic risk analysis methods. For instance, Samantra et al. [

29] proposed using the risk breakdown structure method to evaluate the risk of urban construction projects; Ruijters and Stoelinga [

30] thought that the fault tree analysis method was very suitable for analyzing risks related to safety and economically critical assets, such as power plants, airplanes, data centers, and web shops. Meanwhile, Garvey et al. [

31] utilized the Bayesian network approach to establish a supply network risk propagation model. As two large and important branches of the decision theory and operations research, methods based on multiple criteria decision analysis (MCDA) and weight of evidence (WoE) are also widely used in risk analysis. Thokala et al. [

32] adopted MCDA for health care decision making. Reichelt et al. [

33] studied the application of MCDA in risk management of civil and environmental engineering projects. Goetghebeur et al. [

34] combined MCDA with advanced pharmacoepidemiology for benefit–risk assessments of medicines. Lutter et al. [

35] used improved WoE approaches for chemical evaluations. Agerstrand and Beronius [

36] investigated the application of WoE evaluation in chemical risk assessment within different regulatory frameworks in the European Union. Li et al. [

37] introduced the WoE approach to assess the ecological risk of polymetallic sites. However, these methods still have some limitations for the risk identification of ESEME. For instance, fault tree analysis requires accurate knowledge of the relationship between events and the probability of failure, and fails to describe the severity of risks in detail [

38]. While the risk breakdown structure method can clearly list the risks and sub-risks that may occur, the only method available is qualitative analysis, most risk factors are ambiguous, and even some hidden risks cannot be identified [

39]. The MCDA method relies on the estimated values of indicators to determine the overall risk value, but does not take into account the value range of each indicator at different levels. Meanwhile, the WoE approach requires a lot of frequency data in the application process, but the risk of ESEME lacks frequency data. As for the emerging issue of ESEME, it involves risk factors from enterprises themselves, sharing platforms, service providers, and other aspects. In view of these ambiguous risk factors, the relationship between these risk factors is unclear, and the probability of each factor generating risks is not clear. In addition, enterprise decision making relies on a precise risk analysis result, while qualitative analysis often fails to meet the demand. However, these existing risk assessment methods all have some limitations on this issue.

Through reviewing the literature, it is found that the matter–element extension method is applied in many assessment projects in other fields. The matter–element extension based approach is mainly composed of matter–element theory and an extension set. Generally speaking, it is an approach to study the possibility of the extension of objects and the law of exploration and innovation with a formal approach. In the traditional Chinese story, Cao Chong weighed the elephant, Cao, according to the characteristics of the elephant’s weight, converting the measurement of the elephant’s weight to measure the weight of stones. By a similar means, research should not only focus on the direct quantitative relationship, but should also study the relationship and changes of objects, characteristics, and their values: this is the idea of the matter–element extension theory, which translates incompatibility problems into compatibility ones, thus solving the contradictions. Professor Cai Wen first proposed the matter–extension method in 1983, and believed that in an objective world, objects have a unity of quality and quantity, and the quantitative and qualitative changes of objects are closely related to each other [

40]. In conclusion, the matter–element extension method is a method that considers both quantitative changes and qualitative changes, and transforms the contradictory problems in the objective world into the contradictions between the matter elements [

41]. Compared with other risk analysis methods, the matter–element extension model can support multi-attribute risk analysis, be well integrated with the indicator system, and consider the differences and inaccuracies of indicators under various risk levels. What’s more, this approach is suitable for the assessment and analysis of complex systems, which integrates qualitative analysis and quantitative analysis [

42], and has been widely used in many fields. For instance, Deng et al. [

43] adopted the fuzzy matter–element model and the improved entropy weight method to evaluate the health of river in the Taihu Plain. Then, Shao et al. [

44] also conducted a performance evaluation to analyze the port supply chain, in which they used the fuzzy matter–element analysis method. Similarly, based on the matter–element extension method, Li et al. [

45] studied the risks of the Qinghai–Tibet power grid interconnection project under the fuzzy theory environment. However, Xu et al. [

46] proposed an improved TOPSIS (Technique for Order Preference by Similarity to an Ideal Solution) method that differed from the above studies based on matter–element extension theory, and they made a comprehensive assessment on the coordinated development for the regional power grid and renewable energy power supply by this method. Combined with the fuzzy analytic hierarchy process (FAHP) and entropy weight method, Liu et al. [

47] introduced the matter–element model to evaluate the urbanization of an economy–society–ecology system. In addition, Zhao et al. [

48] introduced extension theory and system engineering theory to assess the stability of a high rock slope. In the above research, the matter–element extension based approach has been used to assess many kinds of projects, and achieved good results.

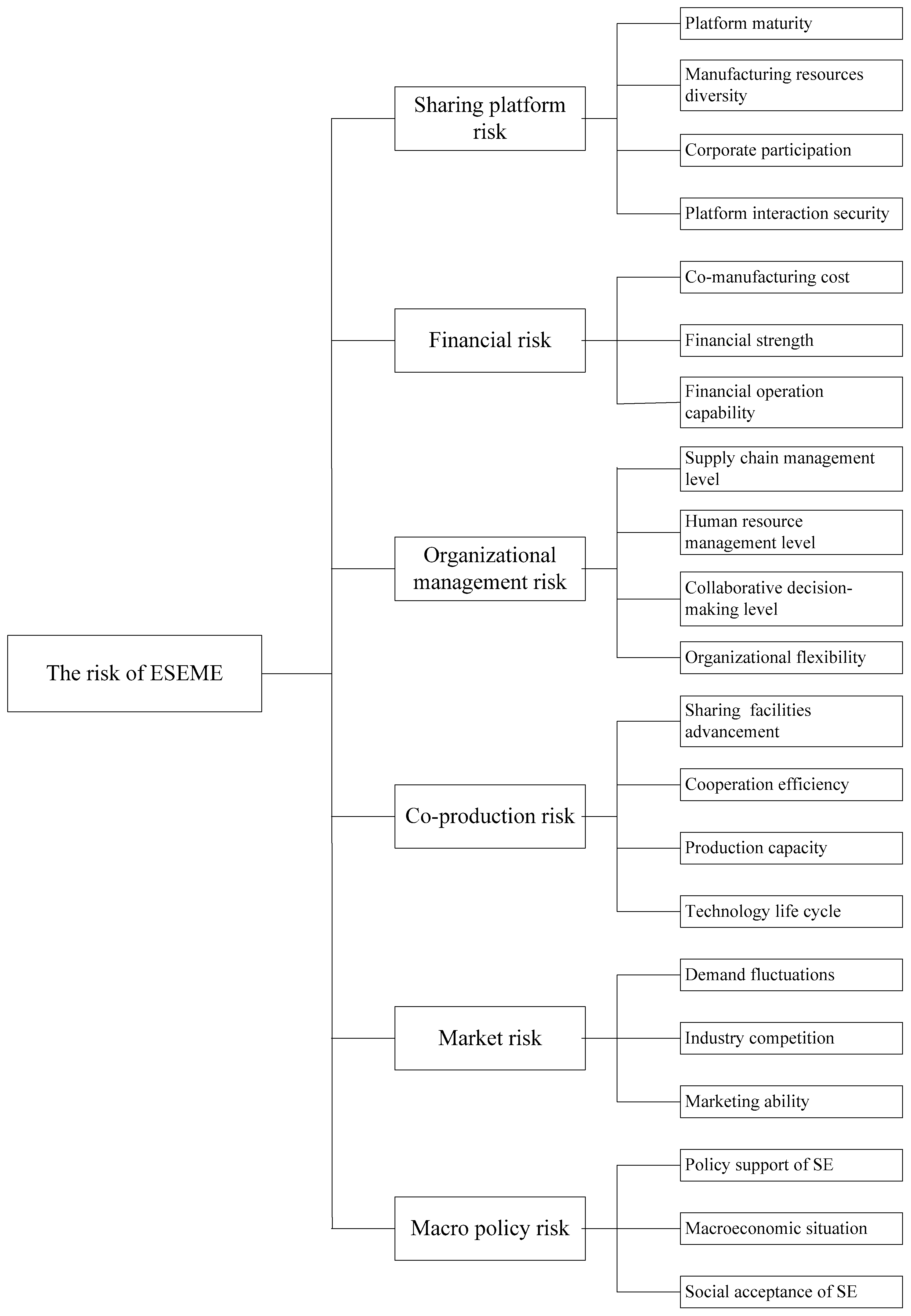

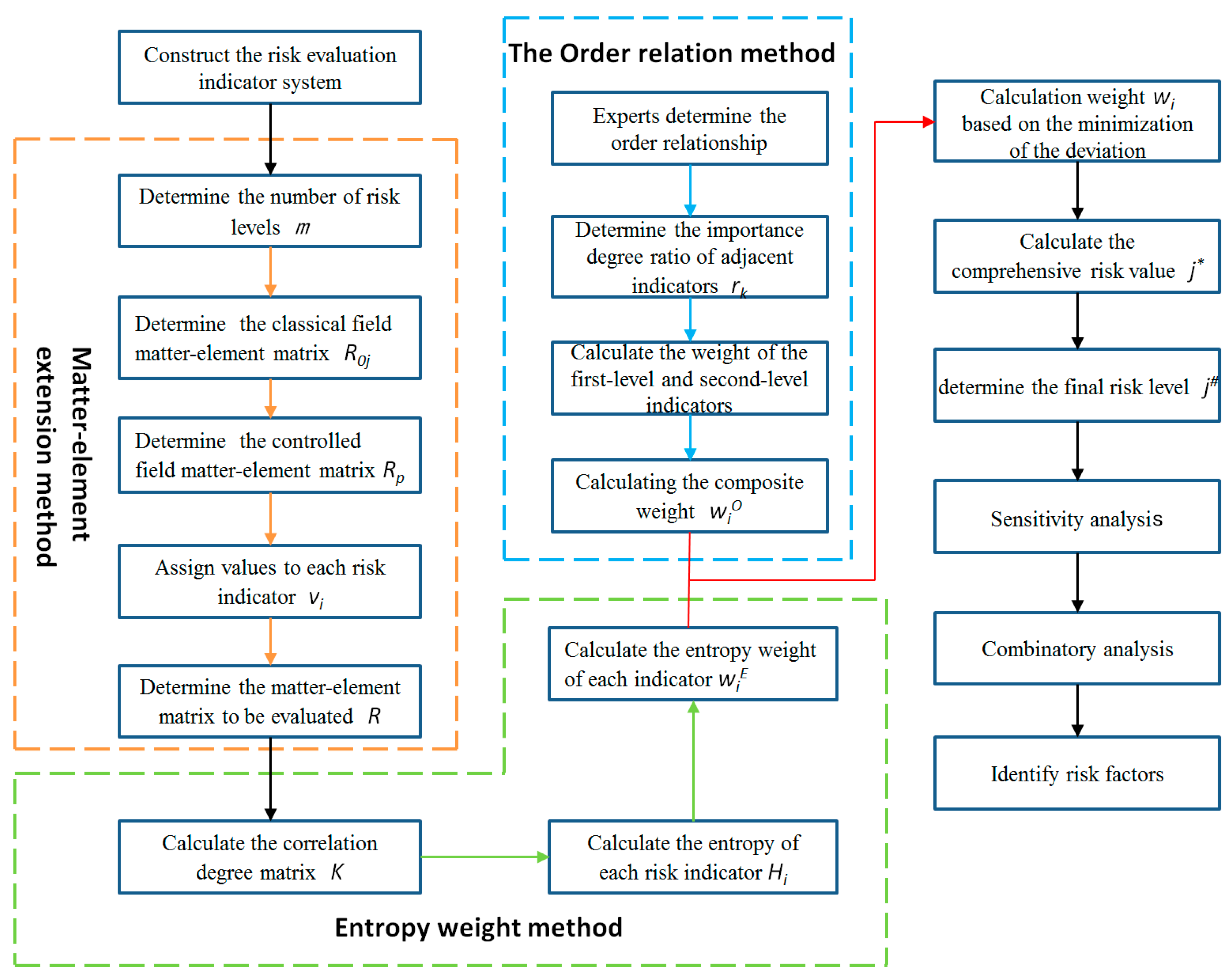

Based on the above studies, we introduce a matter–element extension based approach according to the characteristics of ESEME. The extension theory can be used to analyze and study the main risk indicators involved in the process of ESEME from the perspectives of sharing platform risk, financial risk, organizational management risk, co-production risk, market risk, and macro policy risk. Then, the matter–element extension model can be used to transform incompatible problems into compatible ones, so as to conduct risk assessment. However, different risk indicators may have different effects on the comprehensive risk value, so the weighting method of indicators is particularly important for risk assessment. The traditional matter–element model adopts a single subjective weighting method, and it has some limitations [

49]. On the basis of the literature, methods used to weight assessment indicators are often AHP (Analytic Hierarchy Process), the entropy weight method, or a combination of AHP and the entropy weight method. The order relation method is a subjective weighting method that relies on the evaluators’ subjective attention to each indicator [

50]. Compared with AHP, the order relation method is simpler and more practical, because it does not need to construct a judgment matrix and consistency test. Meanwhile, the entropy weight method is an objective weighting method, which determines indicators’ weights according to the variation degree of indicators’ values, and can effectively reflect the hidden information among indicators. Only the subjective weighting method or the objective weighting method is too one-sided in practical problems. Therefore, drawing upon the minimization of the deviation method, the comprehensive weight integrating entropy based weight and order relation based weight is obtained, and the risk level is determined. Next, by means of sensitivity analysis and combinatory analysis, sensitive risk indicators and the risk type of indicators can be identified.

The innovations of this paper are as follows:

- (1).

According to a literature review, this is one of the first studies to assess the risk of ESEME. Unlike the existing risk research of the sharing economy, the matter–element extension method is adopted to construct a risk assessment indicator system for ESEME and more systematically assess the risk of ESEME.

- (2).

On the basis of the traditional matter–element extension model, the method of indicator weighting is improved. We draw upon the minimum deviation method, which integrates the entropy weight method and the order relation method, and more reasonably reveal the importance of each risk indicator.

- (3).

This work not only conducts a sensitivity analysis on the risk indicators’ values to identify risk indicators with high sensitivity, but also performs a combinatory analysis according to the comprehensive risk value and sensitivity, and then divides the risk indicators into four categories: Safety Type, Long-Term Planning Type, Preventive Type, and Critical Concern Type.

In summary, this paper constructs an effective and practical risk assessment model for ESEME. Through the model, the comprehensive risk value of a project can be obtained, and the risk factors with high sensitivity can be identified. Further, manufacturing enterprises can more accurately locate and control risk factors, and formulate more reasonable strategic planning.

4. Example Analysis

E is a small and medium-sized manufacturing enterprise in China, which is committed to expanding its production scale and improving its sales performance. Due to insufficient internal funds and incomplete production facilities, enterprise E plans to engage in the sharing economy to solve existing issues in a low-cost way. Based on the matter–element extension method and the minimum deviation weighting method, this paper studies the risk issues of enterprise E engaging in the sharing economy. In order to assess the risks of enterprise E, an assessment group is formed, which consists of professors, associate professors, and doctoral students engaged in research related to the sharing economy and risk assessment, as well as manufacturing enterprise engineers and department managers, respectively from our university, enterprise E, and another manufacturing enterprise. Then, enterprise E provides detailed information on its business conditions, technical strengths, and progress on engagement in the sharing economy, and the assessment group evaluates indicators according to the risk indicator system in

Section 2.1. By the way, it is understandable that different experts have different opinions. On this basis, the paper implements a risk assessment of enterprise E’s engagement in the sharing economy according to the assessment process in

Section 3.6. The specific steps are as follows.

4.1. Calculation of Risk Value

4.1.1. Determination of the Matter–Element Matrices

The risk levels are divided into four categories, which are low, medium–low, medium–high, and high. According to the value range of each risk indicator in different risk levels, the classical field matter–element matrix and the controlled field matter–element matrix are determined successively.

The classical field matter–element matrix is:

The controlled field matter–element matrix is:

Since each risk indicator is a qualitative indicator, subjective valuation is required. Five experts are invited to score each risk indicator, and the score range is [0, 100]. Then, the average of the five scores is standardized (see

Appendix A). The final matter–element matrix to be evaluated is:

4.1.2. Calculation of the Correlation Degree Matrix

Calculate the correlation degree between each risk indicator and each risk level according to Formulas (5)–(7). The correlation degree matrix

is:

4.1.3. Calculation of Indicator’s Weight

First of all, for determining the weight of the first-level risk indicators based on the order relation method, five experts are invited again to rank the importance of the first-level risk indicators, and the importance degree ratio of the adjacent indicators is determined according to

Table 2. Then, the weight of each first-level risk indicator is calculated according to Formulas (11) and (12), and the average value of the weights obtained by the five experts is taken. Similarly, the weights of all the second-level indicators below each first-level indicator are calculated, respectively. The indicators’ order relationship, the importance ratio between the two adjacent indicators and indicators’ weights from the five experts are provided in

Appendix B. Then, the weight of the second-level indicator is multiplied by the weight of the first-level indicator to which it belongs, which is the combined weight of the second-level indicator based on the order relation method. Afterwards, the entropy weight is obtained according to the correlation degree matrix

and the calculation steps shown in

Section 3.2.1. Then, the minimum deviation weight is calculated through the Formulas (13) and (14), which is the comprehensive weight required in this paper. Ultimately, the indicators’ comprehensive weights are shown in

Table 3.

4.1.4. Calculation of the Comprehensive Risk Value

According to Formula (15), the correlation degree between the risk of ESEME and each risk level can be calculated, which is , and , respectively. From the above calculation results, we can know that the value of is the largest, so the risk level of ESEME is medium–low. According to Formulas (16) and (17), the final risk value of ESEME can be calculated as 2.1317.

4.2. Analysis of Calculation Results

According to the comprehensive risk value 2.1317, the overall risk of enterprise E is medium–low, indicating that enterprise E will encounter a little risk resistance in the process of engagement in the sharing economy. From the correlation degree matrix, the risk level of each second-level risk indicator can be known. Among all the 21 risk indicators, only (Policy support of SE) is at a low risk level, which means that enterprise E can get support from the government when they engage in the sharing economy, and it is conducive to its sustainable development. Fourteen indicators are at a medium–low risk level, respectively (Platform maturity), (Platform interaction security), (Co-manufacturing cost), (Financial strength), (Supply chain management level), (Human resource management level), (Collaborative decision-making level), (Sharing facilities advancement), (Production capacity), (Technology life cycle), (Demand fluctuations), (Marketing ability), (Macroeconomic situation), and (Social acceptance of SE). Although the current risks are small, these indicators remain to be seen, because they may become medium–high risk or high risk as environmental changes. Three indicators are at the medium–high risk level; these are respectively (Manufacturing resources diversity), (Financial operation capability), and (Organizational flexibility). Three indicators are also at the high level, which are (Corporate participation), (Cooperation efficiency), and (Industry competition). They require special attention, and enterprise E needs to control and prevent for different risk factors.

In addition to judging the risk level of the second-level risk indicators and calculating the comprehensive risk value, the risk level of the six first-level indicators can also be judged according to Formula (15). Since is the largest among , the sharing platform risk is at a low level; Since is the largest among , the financial risk is at a medium-high level. Since is the largest among , the organizational management risk is at a low level. Since is the largest among , the co-production risk is at a medium–low level. Since is the largest among , the market risk is at a medium–low level. Since is the largest among , the macro policy risk is at a medium–low level. Then, enterprise E could adjust the corresponding departments’ work according to the risk levels of first-level indicators.

4.3. Sensitivity Analysis

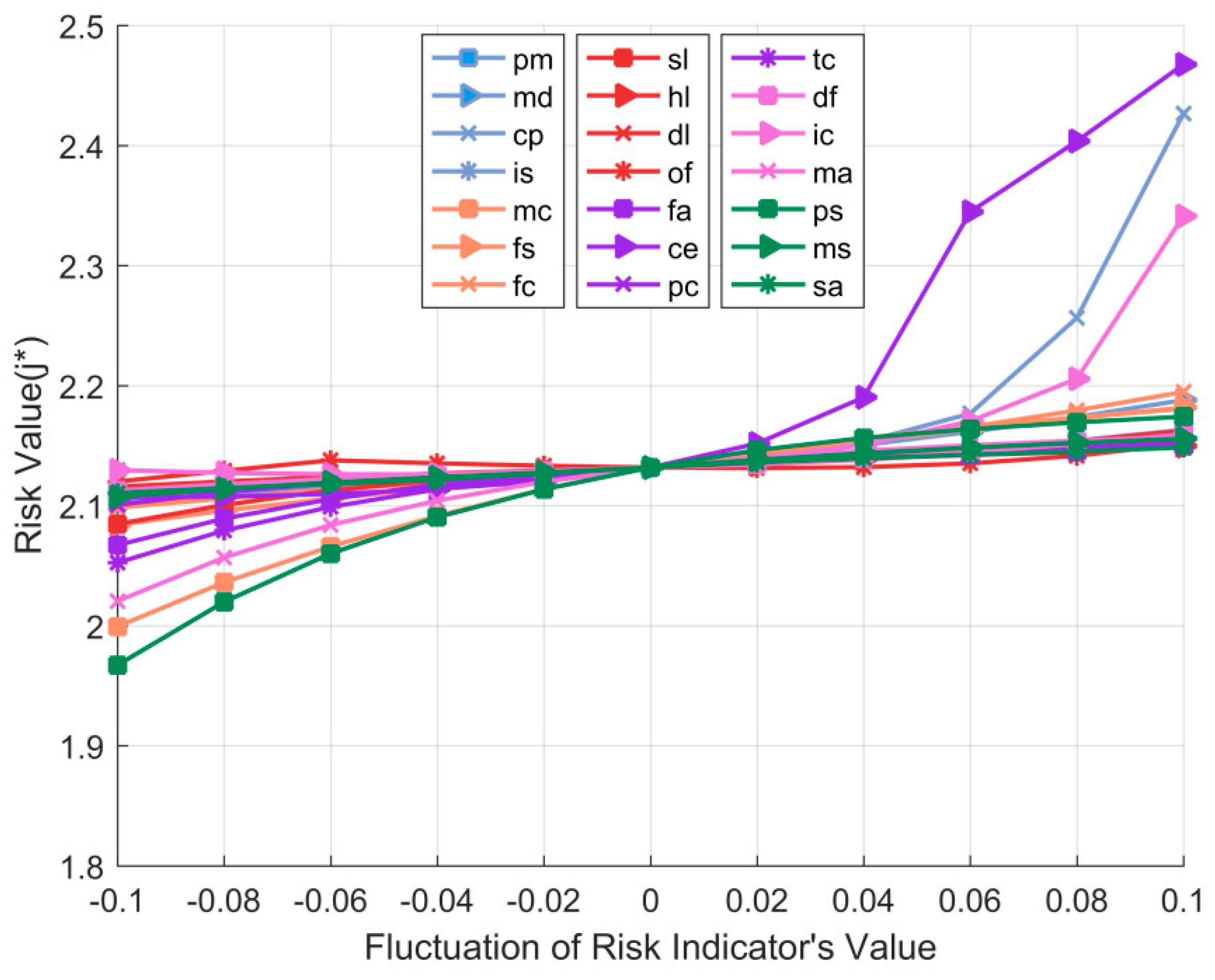

In order to observe the influence of the final risk value when the indicator’s value changes and identify the sensitive risk factors, a sensitivity analysis on the risk indicator’s value is implemented. When the value of a single indicator changes by ±0.1, the corresponding risk value changes are shown in

Figure 3.

According to the sensitivity analysis of the indicators’ values, the six most sensitive indicators are

(Cooperation efficiency),

(Corporate participation),

(Policy support of SE),

(Industry competition),

(Co-manufacturing cost), and

(Marketing ability). As can be seen from

Figure 3, when the value of

(Cooperation efficiency) increases by 0.04–0.1, the comprehensive risk value rises sharply; when the value of

(Corporate participation) or

(Industry competition) increases by 0.06–0.1, the comprehensive risk value rises significantly. What’s more, when the value of

(Co-manufacturing cost),

(Marketing ability), or

(Policy support of SE) is gradually reduced by 0.1, the comprehensive risk value slowly decreases. Therefore, in order to prevent the increase of the comprehensive risk value, it is necessary to focus on

(Cooperation efficiency),

(Corporate participation), and

(Industry competition). Assuming that the comprehensive risk value needs to be reduced, enterprise E can reduce the co-manufacturing cost, improve the marketing ability, and increase the policy support of SE.

In addition, sensitivity analyses of the comprehensive risk value based on the order relation weighting method and entropy weight method are also carried out under the same conditions. When weighting based on the order relation method, the result shows that the comprehensive risk value changes linearly with the change of a single indicator’s value. For example, with the continuous increase of

(Co-manufacturing cost), the comprehensive risk value increases linearly, while with the continuous increase of

(Corporate participation), the comprehensive risk value decreases linearly. However, this phenomenon indicates the limitation of the assessment of the matter–element extension model based on the single order relation method. While the variation trend of the comprehensive risk value based on the entropy weight method is similar to that in

Figure 3, the variation range of the comprehensive risk value is larger than that in

Figure 3, and there are differences in the details. Since the entropy weight method is an objective weighting method, which relies on objective data and in this paper depends on the correlation degree obtained by the matter–element extension model, it is unreasonable to assess the risk of enterprise E engaging in the sharing economy based on the entropy weight method alone.

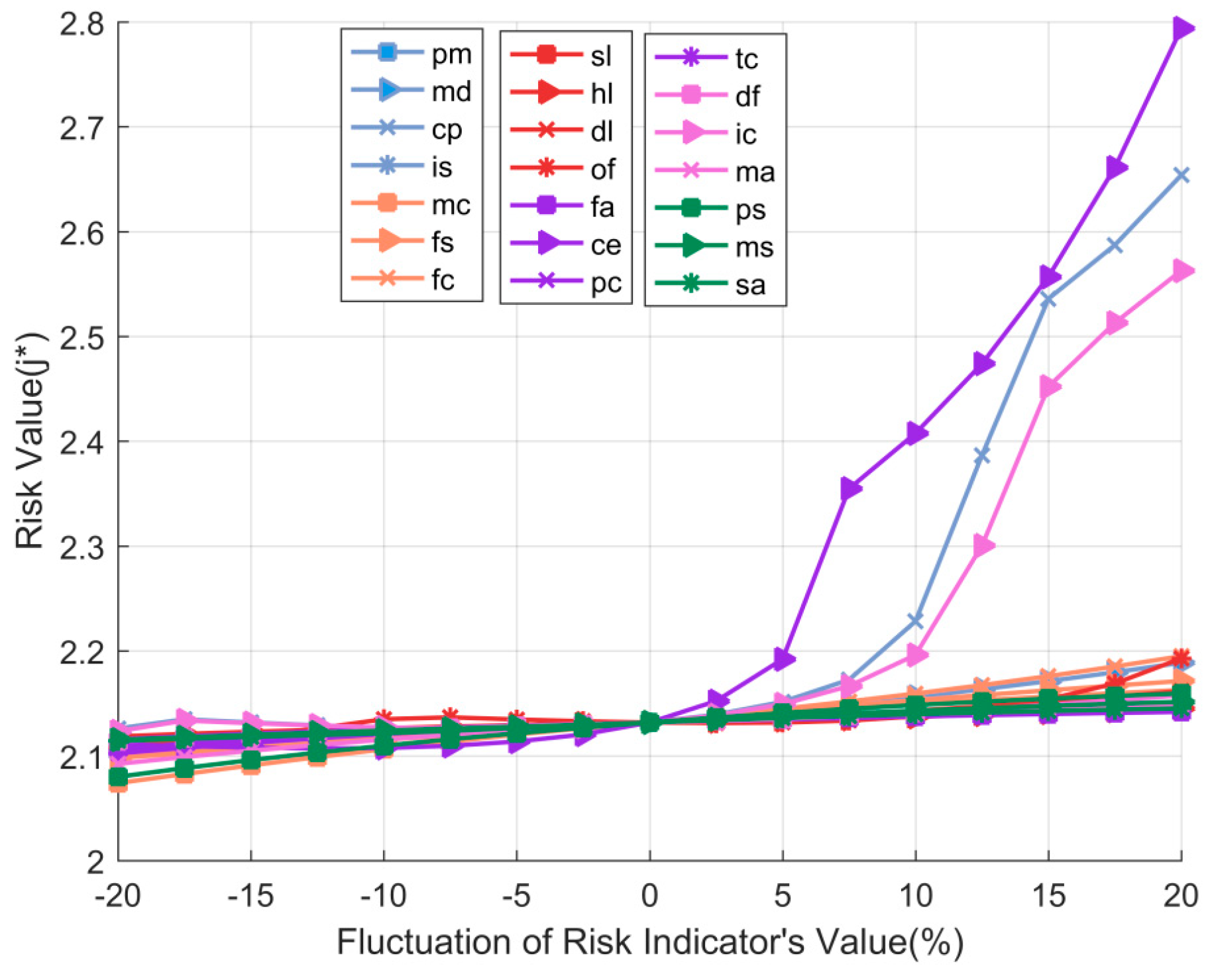

Due to there being large differences in values of these indicators, the results calculated by increasing or decreasing the fixed value will be biased. In order to eliminate this deviation, a sensitivity analysis on the comprehensive risk value when the indicator’s value changes ±20% is implemented, and the results are shown in

Figure 4. Under the same conditions, sensitivity analyses of the comprehensive risk value based on the order relation weighting method and entropy weight method are also implemented.

According to the analysis results, the six most sensitive indicators are

(Cooperation efficiency),

(Corporate participation),

(Industry competition),

(Financial operation capability),

(Co-manufacturing cost), and

(Manufacturing resources diversity). Among them, the high sensitivity of

(Corporate participation),

(Cooperation efficiency), or

(Industry competition) benefits from its high value, which requires focus. Although the value of

(Manufacturing resources diversity),

(Co-manufacturing cost), or

(Financial operation capability) is not high, they are also worthy of attention. Weighting based on the order relation method, the result shows that the comprehensive risk value decreases with the increase of some indicators’ values. Obviously, the matter–element extension model based on the order relation method alone is not reasonable. Further, the variation trend of the comprehensive risk value based on the entropy weight method is similar to that in

Figure 4, but the variation range of the comprehensive risk value is larger than that in

Figure 4, and there are subtle differences in the sensitivities of some indicators.

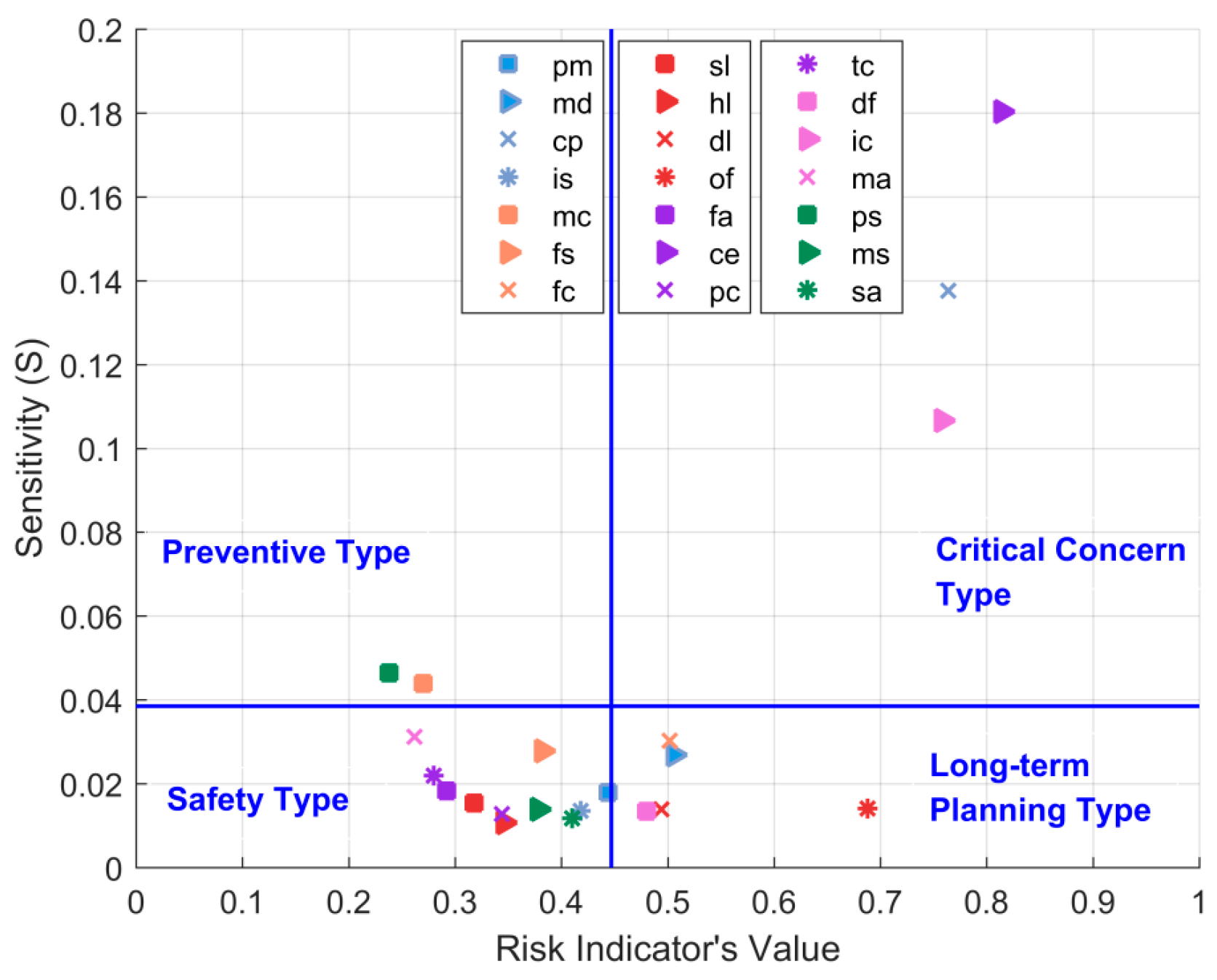

4.4. Combinatory Analysis

In order to further study the relationship between a risk indicator’s value and sensitivity, a combinatory analysis is implemented.

In

Figure 5, the horizontal axis represents the standardized indicator’s value evaluated by experts, and the vertical axis represents the average standard deviation of the risk indicator’s value changes by ±0.1 and ±20%, namely the comprehensive sensitivity of the indicator’s value. According to the distribution position of each risk indicator in the coordinate system, the types of the 21 risk indicators are determined as follows.

The “Safety Type” includes (Platform maturity), (Platform interaction security), (Financial strength), (Supply chain management level), (Human resource management level), (Sharing facilities advancement), (Production capacity), (Technology life cycle), (Marketing ability), (Macroeconomic situation), and (Social acceptance of SE); these risk indicators have little effect on the overall risk value.

The “Long-term Planning Type” includes (Demand fluctuations), (Collaborative decision-making level), (Financial operation capability), (Manufacturing resources diversity), and (Organizational flexibility). Such risk indicators have higher value, but lower sensitivity. Even if the indicator’s value changes in the short term, it will have little effect on the comprehensive risk value.

The “Preventive Type” includes (Co-manufacturing cost) and (Policy support of SE). The fluctuations of these indicators’ values may lead to large changes in the comprehensive risk value, so enterprise E needs to take measures to keep the co-manufacturing cost at a low level in advance, and strives to get the government’s support.

The “Critical Concern Type” includes (Cooperation efficiency), (Corporate participation), and (Industry competition). For such indicators, a slight change of their values may lead to a significant change in the comprehensive risk value, so enterprise E needs to pay close attention to these indicators.

5. Discussion and Implications

In order to study the risk of ESEME, this paper constructs the risk assessment indicator system of ESEME by referring to the existing literature. Then, the matter–element extension model is introduced, and the risk of enterprise E engaging in the sharing economy is assessed based on the minimum deviation weight. The assessment results include a precise risk value and the risk level, which are recognized by the experts who have previously given the risk value and weights of the indicators. In addition, highly sensitive indicators are found through sensitivity analysis, which provides a basis for small and medium-sized manufacturing enterprises to accurately identify high-risk factors. By combinatory analysis, all the risk indicators are divided into four risk types, which can help enterprises make analysis decisions more conveniently. For example, the results of the above case analysis indicate that enterprise E needs to specially focus on (Cooperation efficiency), (Corporate participation), and (Industry competition), so enterprise E should choose suppliers with high cooperation efficiency, choose a sharing platform with high participation, and strive to improve the quality of their products or services to distinguish itself from other enterprises in the industry competition. Beyond that, we believe the theoretical perspectives, assessment methodology, and results of this work will provide meaningful references for both theoretical researchers and practitioners.

5.1. Theoretical Implications

Current theoretical research on the sharing economy mainly focuses on the service industry; there are few studies on the integration of manufacturing and the sharing economy. However, through in-depth studies on the development difficulties of small and medium-sized manufacturing enterprises and the operating mechanism of the sharing economy, it is credible that the business model of the sharing economy can bring positive benefits to manufacturing enterprises facing difficulties, enterprises with idle resources, and even the whole industry. In addition to focusing on the opportunities brought by the sharing economy to manufacturing enterprises, this study pays special attention to the other side—that is, the risk of manufacturing enterprises engaging in the sharing economy. This perspective is relatively rare in previous studies. We believe that it will lay a foundation and open up new research ideas for researchers in the field of manufacturing and the sharing economy.

Specifically, this paper adopts the matter–element extension model with a minimum deviation weight to carry out a risk assessment of ESEME. Entropy weight is generally regarded as an objective weight, while the order relation weight is relatively subjective. This work integrates these two weights in the way of minimum deviation and obtains the comprehensive weight that integrates subjective and objective information, which sheds light on the multi-criteria weight integration and matter–element evaluation issues.

While traditional risk analysis methods consider that the higher the risk value of an indicator means the greater the overall risk, through the example, it is believable that the high initial risk value of an indicator does not mean an increase of the overall risk, but is related to the weight, sensitivity, and the classical field range, which exposes the non-linear nature of risk. Through the sensitivity analysis and further combinatory analysis, the proposed matter–element based method shows stronger identification and assessment capability than traditional risk analysis methods. Our results demonstrate that the combination of the evaluation value and sensitivity value of indicators as two dimensions can generate deeper knowledge of risk. The methodology of this work can be extended to other qualitative and quantitative evaluation problems combined with subjective and objective information.

5.2. Practical Implications

Our research includes practical implications for practitioners and policymakers. First, by summarizing the existing theories and applications, we construct a relatively complete risk assessment indicator system for ESEME. The indicator system includes six dimensions, namely, sharing platform risk, financial risk, organizational management risk, co-production risk, market risk, and macro policy risk. Some of these indicators are conventional indicators of risk (e.g., financial strength, human resource management level), and some are closely related to the sharing economy (e.g., platform maturity, sharing facilities advancement). Therefore, for manufacturing enterprises, on the one hand, they need to strengthen their ability to resist common risks, which is very important for any enterprise. On the other hand, they need to pay special attention to the risks related to the sharing economy, because these risk factors may not be encountered in their past business process. The indicator system we built can provide a detailed list of risks for ESEME, which is similar to a medical form tailored to manufacturing enterprises.

Secondly, this study provides an operable framework for manufacturing enterprises to assess risks when engaging in the sharing economy. At present, some manufacturing enterprises have participated in the practice of the sharing economy, but as a new business model, the sharing economy may also bring risks to manufacturing enterprises. However, to date, there are few scientific research studies that can provide practical guidance for manufacturing enterprises in this regard. We present a four-step risk assessment framework of “index system construction–matter element establishment—indicator and weight measurement–sensitivity and combinatory analysis” for manufacturing enterprises. Each step has strong operability, and the results obtained are intuitive, explanatory, and instructive. Following up on the proposed risk assessment framework, manufacturing enterprises can effectively reduce the uncertainty in the process of engaging in the sharing economy, and accurately locate, identify, and evaluate risks.

Finally, the research can provide references for the government to formulate relevant policies for ESEME. Currently, the application of the sharing economy model is expanding, but the relevant policy system is insufficient. The risks in many aspects of ESEME are inseparable from the actions of policymakers. Policymakers need to effectively control possible systemic risks while encouraging manufacturing enterprises to develop their engagement with the sharing economy. For example, policymakers can reduce platform risks by monitoring the maturity of sharing platforms and encouraging manufacturing resource providers to publish diverse resources on the platforms. Policymakers also need to have a good grasp of the overall risk situation of ESEME. For example, they can use the method of this paper to evaluate the risks of key enterprises, and through the integration of the risk of multiple enterprises, the overall assessment of the current risk can be obtained; then, the closed-loop management of risk of ESEME can be realized.

6. Conclusions

In the context of green development, the business model of the sharing economy has attracted much attention from multiple disciplines. The sharing economy can effectively solve the issues such as resource shortage and environmental degradation, and can promote the sustainable development of the manufacturing industry. Therefore, many manufacturing enterprises are considering transforming and upgrading themselves by engaging in the sharing economy. In this work, we conduct an in-depth research on the process of ESEME and mainly focus on the inevitable risk issues. In order to ensure that small and medium-sized manufacturing enterprises can identify various risk factors and subsequently avoid them in the process of engagement, an operable method for the risk assessment of ESEME is proposed.

The contribution of this work mainly lies on three aspects. Firstly, the matter–element extension method is used to assess the risk of ESEME. Most of the existing studies on sharing economy risks are qualitative analyses of the negative impact of the sharing economy on society. A cognitive framework of risk assessment is proposed in this work, which integrates objective risk information and subjective cognitive factors, and constructs a risk assessment indicator system for ESEME under the guidance of the matter–element extension based approach. Secondly, this paper draws upon the minimization of deviation method, which integrates the entropy weight method and the order relation method, and obtains a balanced comprehensive weight. The minimum deviation weighting method has many advantages, such as reducing the influence of characteristic coupling, avoiding the one-sidedness of weight, and more scientifically revealing the difference of importance among risk indicators. Finally, in order to investigate the influence of each indicator’s risk value on the comprehensive risk, sensitivity analysis and combinatory analysis are implemented, according to which, risk indicators can be identified and classified. These analyses provide practical guidance for manufacturing enterprises to locate risks more accurately and realize sustainable development.

However, there are still some limitations of this research. As some of the risk indicators come from expert ratings, this may reduce the objectivity of the results. However, since the process of risk assessment itself is a process of combining subjective and objective information, an appropriate amount of subjective indicators is also reasonable. In addition, in the model, the positive and negative types of risk indicators are mainly considered; however, the risk indicators are not actually necessarily positive or negative. They also may be moderate, so the calculating models and methods can be further improved in future works.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}