A Tax Coming from the IPCC Carbon Prices Cannot Change Consumption: Evidence from an Experiment

Abstract

:1. Introduction

2. Background and Literature

3. Data

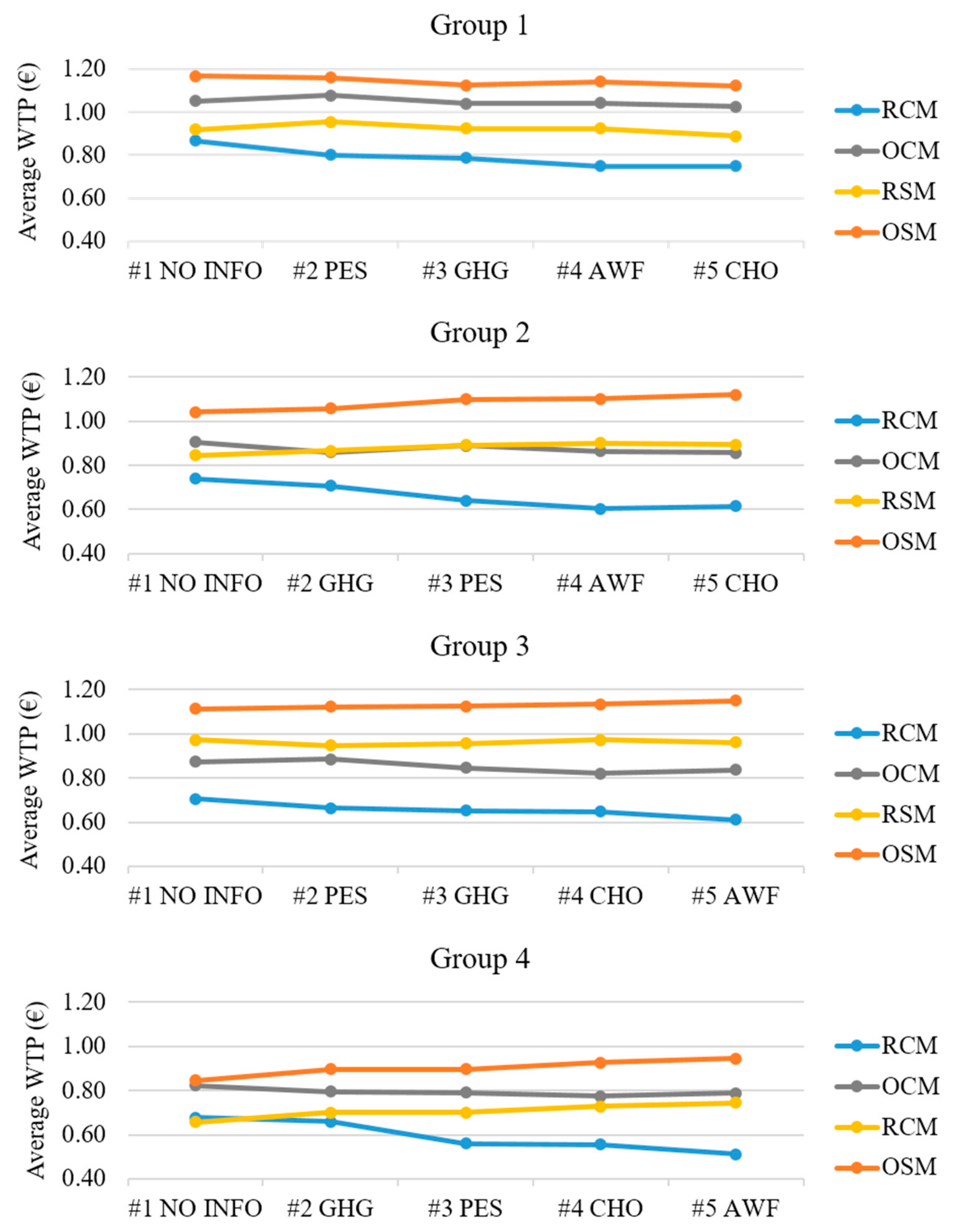

3.1. Experiment and Data Collection

3.2. Analysis of WTP

4. Methods

4.1. Explanation with a Simplified Example

4.2. Surpluses with the Four Types of Milk

4.2.1. Scenarios with an Optimal Tax and Subsidy in the Absence of Information

4.2.2. Taxes Based on the IPCC Carbon Price

5. Results

5.1. Perfect Information Scenario

5.2. Scenarios with Optimal Tax and Subsidy in the Absence of Information

5.3. Taxes Based on IPCC Carbon Prices

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Consumers’ Surpluses with Four Products

References

- IPCC Reports 2019. Available online: https://www.ipcc.ch/reports/ (accessed on 1 July 2019).

- Carbon Pricing Leadership Coalition. Report on the high-level commission on carbon prices. Available online: https://www.ipcc.ch/reports/ (accessed on 1 July 2019).

- Edenhofer, O.; Pichs-Madruga, R.; Sokona, Y.; Farahani, E.; Kadner, S.; Seybothm, K.; Adler, A.; Baum, I.; Bruner, S.; Eickmeier, P.; et al. Climate change 2014: Mitigation of Climate Change; Contribution of Working Group III to the Fifth Assessment. Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, UK, 2014. [Google Scholar]

- Eurostat, J. Agriculture—Greenhouse Gas Emission Statistics; European Commission: Luxemburg, 2015. [Google Scholar]

- Springmann, M.; Mason-D’Croz, D.; Robinson, S.; Wiebe, K.; Godfray, H.C.J.; Rayner, M.; Scarborough, P. Health-motivated taxes on red and processed meat: A modelling study on optimal tax levels and associated health impacts. PLoS ONE 2018, 13, e0204139. [Google Scholar] [CrossRef] [PubMed]

- FranceAgriMer. Données et Bilan Lait; Technical report; Etablissement National des Produits de L’agriculture et de la Mer; FranceAgriMer: Montreuil, France, 2017. [Google Scholar]

- Sunstein, C.R. Behavioural economics, consumption and environmental protection. In Handbook of Research on Sustainable Consumption; Reisch, L.A., Thøgersen, J., Eds.; Edward Elgar Publishing: Cheltenham, UK, 2015. [Google Scholar]

- Moser, A. Thinking green, buying green? Drivers of pro-environmental purchasing behavior. J. Consumer Mark. 2015, 32, 167–175. [Google Scholar] [CrossRef]

- Thøgersen, J.; Ölander, F. Spillover of environment-friendly consumer behavior. J. Environ. Psych. 2003, 23, 225–236. [Google Scholar] [CrossRef]

- Akerlof, G.A. The market for “lemons”: Quality uncertainty and the market mechanism. Quart. J. Econ. 1970, 84, 488–500. [Google Scholar] [CrossRef]

- Yokessa, M.; Marette, S. A review of eco-labels and their economic impact. Int. Rev. Environ. Resour. Econ. 2019, 13, 119–163. [Google Scholar] [CrossRef]

- Disdier, A.-C.; Marette, S. Taxes, minimum-quality standards and/or product labeling to improve environmental quality and welfare: Experiments can provide answers. J. Regul. Econ. 2012, 41, 337–357. [Google Scholar] [CrossRef]

- Cornwell, A.; Creedy, J. Environmental Taxes and Economic Welfare; Edward Elgar Publishing: Cheltenham, UK, 1997. [Google Scholar]

- Aasness, J.; Larsen, E.R. Distributional effects of environmental taxes on transportation. J. Consumer Policy 2003, 26, 279–300. [Google Scholar] [CrossRef]

- Bansal, S.; Gangopadhyay, S. Tax/subsidy policies in the presence of environmentally aware consumers. J. Environ. Econ. Manag. 2003, 45, 333–355. [Google Scholar] [CrossRef]

- Barnett, A.H. The pigouvian tax rule under monopoly. Am. Econ. Rev. 1980, 70, 1037–1041. [Google Scholar]

- Hafstead, M. Introducing the E3 carbon tax calculator: Estimating future CO2 emissions and revenues. Available online: https://www.resourcesmag.org/common-resources/introducing-the-e3-carbon-tax-calculator-estimating-future-co2-emissions-and-revenues/ (accessed on 22 August 2019).

- Heal, G.; Schlenker, W. Coase, hotelling and pigou: The incidence of a carbon tax and CO2 emissions. Nat. Bur. Econ. Res. 2019. working paper No. 26086. [Google Scholar]

- Guo, D.; He, Y.; Wu, Y.; Xu, Q. Analysis of supply chain under different subsidy policies of the government. Sustainability 2016, 8, 1290. [Google Scholar] [CrossRef]

- Lusk, J.L.; Marette, S. Welfare effects of food labels and bans with alternative willingness to pay measures. Appl. Econ. Perspect. Policy 2010, 32, 319–337. [Google Scholar] [CrossRef]

- McFadden, D.; Leonard, G. Issues in the contingent valuation of environmental goods. In Contingent Valuation: A Critical Assessment; Hausman, J., Ed.; Emerald Group Publishing Limited: Bingley, UK, 1993; Volume 220, pp. 165–215. [Google Scholar]

- Hasson, R.; Löfgren, Å.; Visser, M. Climate change in a public goods game: Investment decision in mitigation versus adaptation. Ecol. Econ. 2010, 70, 331–338. [Google Scholar] [CrossRef] [Green Version]

- Kallbekken, S.; Kroll, S.; Cherry, T.L. Do you not like Pigou, or do you not understand him? Tax aversion and revenue recycling in the lab. J. Environ. Econ. Manag. 2011, 62, 53–64. [Google Scholar] [CrossRef] [Green Version]

- Lanz, B.; Wurlod, J.-D.; Panzone, L.; Swanson, T. The behavioral effect of pigovian regulation: Evidence from a field experiment. J. Environ. Econ. Manag. 2017, 87, 190–205. [Google Scholar] [CrossRef]

- Sarr, H.; Bchir, M.A.; Cochard, F.; Rozan, A. Nonpoint Source Pollution: An Experimental Investigation of the Average Pigouvian Tax; Working Paper; Université de Franche-Comté: Besançon, France, 2016. [Google Scholar]

- Borger, B.D.; Glazer, A. Support and opposition to a pigovian tax: Road pricing with reference-dependent preferences. J. Urban Econ. 2017, 99, 31–47. [Google Scholar] [CrossRef]

- Gahvari, F. Second-best pigouvian taxation: A clarification. Environ. Resour. Econ. 2014, 59, 525–535. [Google Scholar] [CrossRef]

- MacKenzie, I.A.; Ohndorf, M. Coasean bargaining in the presence of pigouvian taxation. J. Environ. Econ. Manag. 2016, 75, 1–11. [Google Scholar] [CrossRef]

- McAusland, C.; Najjar, N. Carbon Footprint Taxes. Environ. Resour. Econ. 2015, 61, 37–70. [Google Scholar] [CrossRef]

- Akaichi, F.; Nayga, R.M., Jr.; Gil, J.M. Assessing consumers’ willingness to pay for different units of organic milk: Evidence from multiunit auctions. Can. J. Agric. Econ. 2012, 60, 469–494. [Google Scholar] [CrossRef]

- Bai, J.; Zhang, C.; Jiang, J. The role of certificate issuer on consumers’ willingness-to-pay for milk traceability in China. Agric. Econ. 2013, 44, 537–544. [Google Scholar] [CrossRef]

- Bernard, J.C.; Bernard, D.J. What is it about organic milk? An experimental analysis. Am. J. Agric. Econ. 2009, 91, 826–836. [Google Scholar] [CrossRef]

- Rousu, M.; Huffman, W.E.; Shogren, J.F.; Tegene, A. Effects and value of verifiable information in a controversial market: Evidence from lab auctions of genetically modified food. Econ. Inquiry 2007, 45, 409–432. [Google Scholar] [CrossRef]

- Rousu, M.; Lusk, J. Valuing information on GM foods in a WTA market: What information is most valuable? AgBioForum 2009, 12, 226–231. [Google Scholar]

- Rousu, M.C.; Corrigan, J.R. Estimating the welfare loss to consumers when food labels do not adequately inform: An application to fair trade certification. J. Agric. Food Ind. Org. 2008, 6, 1–26. [Google Scholar] [CrossRef]

- Becker, G.M.; Degroot, M.H.; Marschak, J. Measuring utility by a single-response sequential method. Behav. Sci. 1964, 9, 226–232. [Google Scholar] [CrossRef] [PubMed]

- Huffman, W.E.; Rousu, M.; Shogren, J.F.; Tegene, A. The effects of prior beliefs and learning on consumers’ acceptance of genetically modified foods. J. Econ. Behav. Org. 2007, 63, 193–206. [Google Scholar] [CrossRef]

- Lusk, J.L.; House, L.O.; Valli, C.; Jaeger, S.R.; Moore, M.; Morrow, B.; Traill, W.B. Consumer welfare effects of introducing and labeling genetically modified food. Econ. Lett. 2005, 88, 382–388. [Google Scholar] [CrossRef]

- Lusk, J.L.; Shogren, J.F. Experimental Auctions. Methods and Applications in Economic and Marketing Research; Cambridge University Press: Cambridge, UK, 2007. [Google Scholar]

- Foster, W.; Just, R.E. Measuring welfare effects of product contamination with consumer uncertainty. J. Environ. Econ. Manag. 1989, 17, 266–283. [Google Scholar] [CrossRef]

- González, A.D.; Frostell, B.; Carlsson-Kanyama, A. Protein efficiency per unit energy and per unit greenhouse gas emissions: Potential contribution of diet choices to climate change mitigation. Food Policy 2011, 36, 562–570. [Google Scholar] [CrossRef]

- Cederberg, C.; Stadig, M. System expansion and allocation in life cycle assessment of milk and beef production. Int. J. Life Cycle Assess. 2003, 8, 350–356. [Google Scholar] [CrossRef]

- Kahneman, D.; Knetsch, J.L. Valuing public goods: The purchase of moral satisfaction. J. Environ. Econ. Manag. 1992, 22, 57–70. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Income | |

|---|---|

| ≤€2000 | 31.7% |

| between €2000 and €4000 | 49.6% |

| between €4000 and €6000 | 13.0% |

| >€6000 | 1.6% |

| No answer | 3.3 % |

| Academic | |

| No degree | 0.8% |

| High school degree | 51.2% |

| Bachelor to master’s degree | 48.0% |

| Sex | |

| Female | 49.6% |

| Male | 50.4% |

| Do you regularly consume organic cow’s milk? * | |

| Yes | 57.7% |

| Do you regularly consume soy milk? * | |

| Yes | 17.1% |

| Picture |  |  |  |  |

|---|---|---|---|---|

| Code | RCM | OCM | RSM | OSM |

| Type | Cow’s milk | Cow’s milk | Soy milk | Soy milk |

| Characteristics | Regular | Organic | Regular | Organic |

| Market price (€) | 0.80 | 1.10 | 1.20 | 1.30 |

| Round #1 | Round #2 | Round #3 | Round #4 | Round #5 | |

|---|---|---|---|---|---|

| Group 1 31 participants | no message | PES | GHG | AWF | CHO |

| Group 2 32 participants | no message | GHG | PES | AWF | CHO |

| Group 3 28 participants | no message | PES | GHG | CHO | AWF |

| Group 4 32 participants | no message | GHG | PES | CHO | AWF |

| #1 to #3 | #3 to #5 | #1 to #5 | |

|---|---|---|---|

| RCM | 0.076 | 0.397 | 0.009 |

| OCM | 0.822 | 0.878 | 0.713 |

| RSM | 0.767 | 0.922 | 0.701 |

| OSM | 0.724 | 0.800 | 0.552 |

| ∆MSRCM | ∆MSOCM | ∆MSRSM | ∆MSOSM | ∆CS (s, t) | ∑CS (s, t) | |

|---|---|---|---|---|---|---|

| No. of Unit | No. of Unit | No. of Unit | No. of Unit | €/Unit | Million € | |

| Value | −12 (13) | 0 (3) | −1 (0) | +4 (22) | +0.0215 | +71.98 |

| Percentage | −52 | 0 | −100 | +22 | +13.2 | +13.2 |

| Scenarios | t∗ | s∗ | ∆MSRCM | ∆MSOCM | ∆MSRSM | ∆MSOSM | ∆MStot |

|---|---|---|---|---|---|---|---|

| €/Unit | €/Unit | No. of Unit | No. of Unit | No. of Unit | No. of Unit | No. of Unit | |

| S1 Value | 0.4 | 0.1 | −24 (1) | −2 (1) | +1 (2) | +11 (29) | −14 (33) |

| Percentage | −96.0 | −66.7 | +100.0 | +61.1 | −28.9 | ||

| S2 Value | 0.4 | 0.1 | −25 (0) | +12 (15) | −1 (0) | +7 (25) | −7 (40) |

| Percentage | −100.0 | +400 | −100.0 | +38.9 | −14.9 |

| Scenarios | t∗ | s∗ | ∆CS (s, t) | ∑CS (s, t) | Rtot |

|---|---|---|---|---|---|

| €/Unit | €/Unit | € | Million € | Million € | |

| S1 Value | 0.4 | 0.1 | +0.0020 | +4.49 | −154.00 |

| Percentage | +1.2 | +1.2 | |||

| S2 Value | 0.4 | 0.1 | +0.0063 | +17.0 | −234.35 |

| Percentage | +3.9 | +3.9 |

| Scenarios | t∗ | s∗ | ∆CS (s, t) | ∑CS (s, t) | Rtot |

|---|---|---|---|---|---|

| €/Unit | €/Unit | € | Million € | Million € | |

| S1 Value | 0.4 | 0.1 | +0.0137 | +30.18 | −154.00 |

| Percentage | +14 | +14 | |||

| S2 Value | 0.4 | 0.1 | +0.0314 | +84.05 | −234.35 |

| Percentage | +32.3 | +32.3 |

| Type of Milk | Emission | Tax2020 | Tax2030 | Tax2040 |

|---|---|---|---|---|

| Kgeq CO2/Unit | €/Unit | €/Unit | €/Unit | |

| Cow’s milk | 1.0 | 0.0348–0.0696 | 0.0435–0.0870 | 0.1087–0.1217 |

| Soy milk | 0.075 | 0.0026–0.0052 | 0.0033–0.0065 | 0.0082–0.0091 |

| Scenarios | PCO2 $/ton | taxcowmilk €/Unit | taxsoymilk €/Unit | ∆MSRCM Unit | ∆MSOCM Unit | ∆MSRSM Unit | ∆MSOSM Unit | ∆MStot Unit | ∆CS(s, t) €/Unit | Milion € | RTot Million € |

|---|---|---|---|---|---|---|---|---|---|---|---|

| S4: 2020 | |||||||||||

| Value Percentage | 40 | 0.0348 | 0.0026 | −1 −4.0% | 0 0.0% | 0 0.0% | +3 +16.7% | +2 +4.0% | −0.0025 −1.5% | −8.07 −1.5% | 66.74 |

| Purchase | 24 | 3 | 1 | 21 | 49 | ||||||

| S5: 2020 | |||||||||||

| Value Percentage | 80 | 0.0696 | 0.0052 | −9 −36% | 0 0% | 0 0% | −4 −22.2% | −5 −11% | −0.0041 −2.5% | 11.55 −2.5% | 96.55 |

| Purchase | 16 | 3 | 1 | 22 | 42 | ||||||

| S4: 2040 | |||||||||||

| Value Percentage | 125 | 0.1087 | 0.0033 | −17 −68% | −1 −33.3% | −1 −100% | +5 +27.8% | −13 −28.0% | −0.0066 −4.0% | −14.96 −4.0% | 85.96 |

| Purchase | 8 | 2 | 0 | 23 | 34 | ||||||

| S5: 2040 | |||||||||||

| Value Percentage | 145 | 0.1217 | 0.0082 | −17 −68.0% | −1 −33.3% | 0 0.0% | +5 +27.8% | −13 −28.0% | −0.0066 −4.0% | −14.98 −4.0% | 96.11 |

| Purchase | 8 | 2 | 1 | 23 | 34 | ||||||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yokessa, M.; Marette, S. A Tax Coming from the IPCC Carbon Prices Cannot Change Consumption: Evidence from an Experiment. Sustainability 2019, 11, 4834. https://doi.org/10.3390/su11184834

Yokessa M, Marette S. A Tax Coming from the IPCC Carbon Prices Cannot Change Consumption: Evidence from an Experiment. Sustainability. 2019; 11(18):4834. https://doi.org/10.3390/su11184834

Chicago/Turabian StyleYokessa, Maïmouna, and Stéphan Marette. 2019. "A Tax Coming from the IPCC Carbon Prices Cannot Change Consumption: Evidence from an Experiment" Sustainability 11, no. 18: 4834. https://doi.org/10.3390/su11184834

APA StyleYokessa, M., & Marette, S. (2019). A Tax Coming from the IPCC Carbon Prices Cannot Change Consumption: Evidence from an Experiment. Sustainability, 11(18), 4834. https://doi.org/10.3390/su11184834