Comparative Review and Analysis of Organizational (In)Efficiency Indicators in Qatar

Abstract

:1. Introduction

1.1. Background

1.2. Measuring Organization Efficiency in the Qatari Context

- Organizational strategy;

- Organizational structure;

- Buildup of management and business systems;

- Development of the corporate and employee culture;

- Employee motivation;

- Training of employees;

- Goal-setting for employees.

- Monitoring progress of operational processes: Operational processes can be tracked to measure the throughput, process cycle time to deliver the output along with the quality of the output. This measure shows the health of the process;

- Monitoring implementation of the strategy: Implementation of strategy depends on establishing clear goals, timelines, resource requirements, and responsibilities. Once KPIs are identified, tracking the implementation of the strategy becomes easy.

- Degree of productivity, profitability, and self-maintenance;

- Degree to which an organization adds value to its member and stakeholders;

- Degree to which an organization and its members are a value to the society.

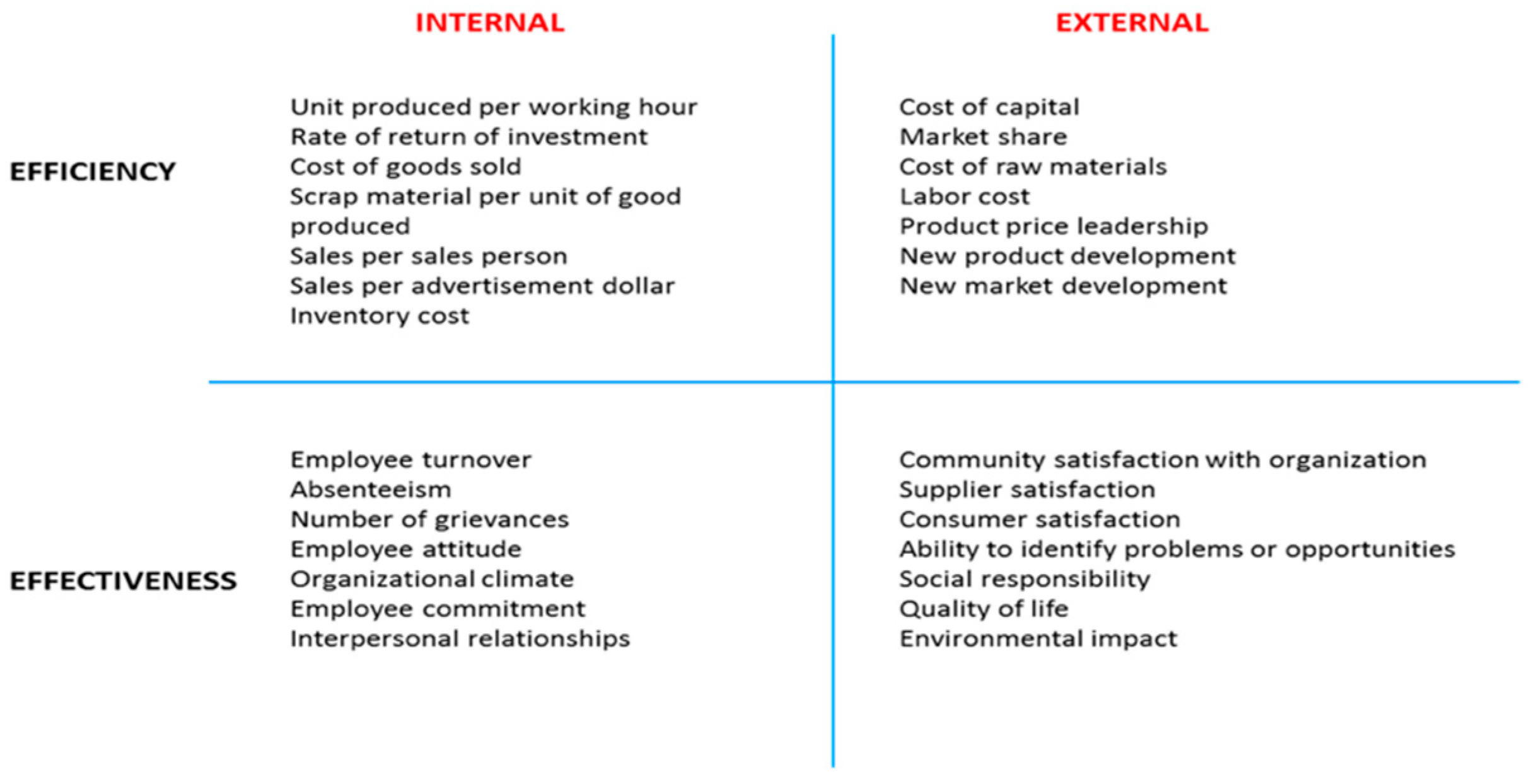

- Effectiveness: The bottom line of organizational performance and efficiency;

- Efficiency: Resource consumption versus output generation;

- Quality: Internal quality (fulfilling internal process requirements) and external quality (fulfilling customer requirements and expectations);

- Timeliness: Three key time parameters to establish organizations’ efficiency—cycle time (time to complete one iteration of an operational process), waited time (time lag experienced by the customer to receive a product or service), and completed on time (tasks completed on time considering internal or external timelines);

- Finance: Profitability and spending according to budgets are two critical criteria of organizational efficiency from finance perspective;

- Workplace environment: Physical amenities for employees and organizational culture constitute workplace environment [22].

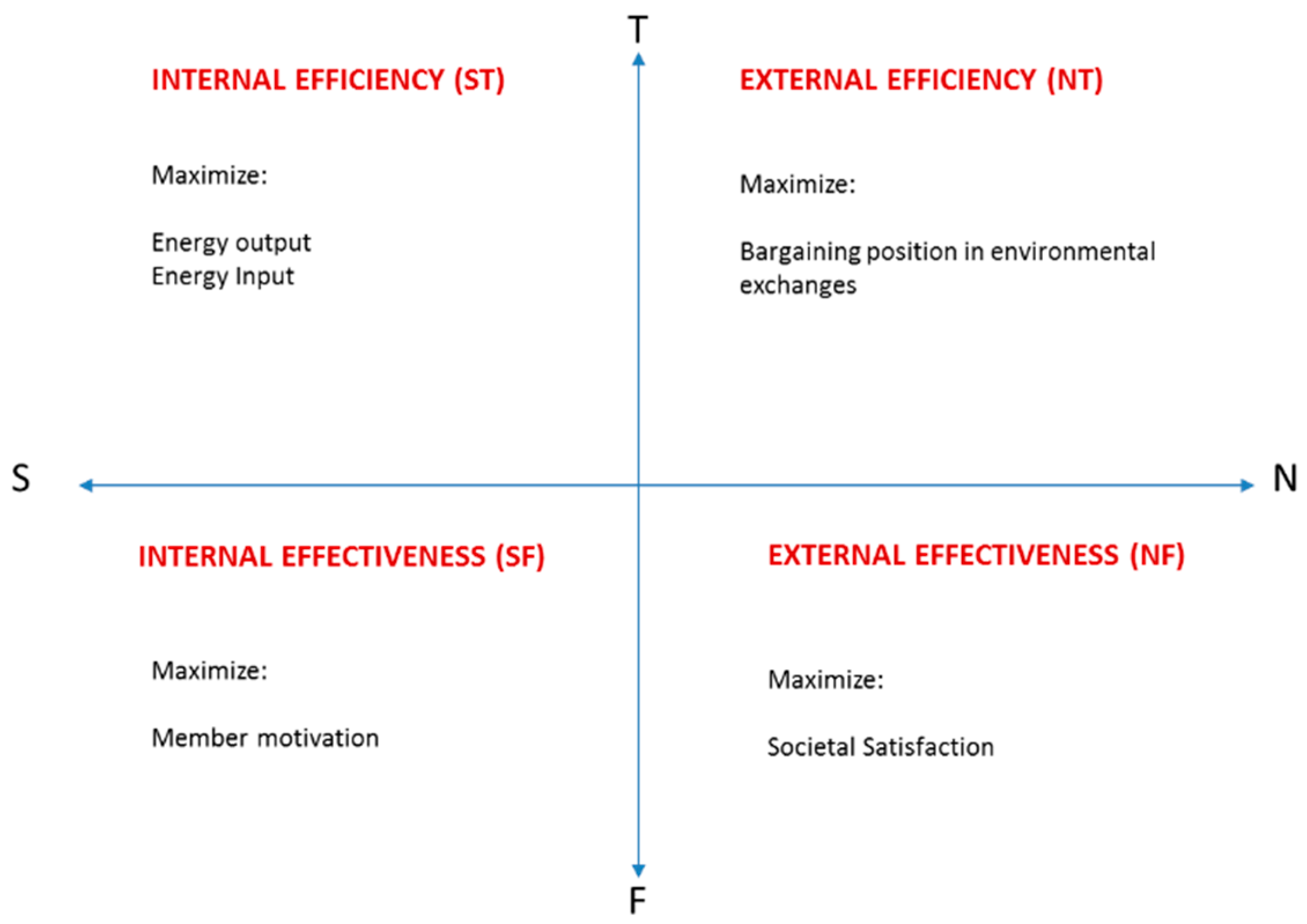

- The Bass model measures three key parameters: (a) Profitability, (b) value creation for stakeholders, and (c) value creation for society; and

- Sink and Tuttle’s model signifies the importance of measurable parameters such as timeliness, quality, efficiency and effectiveness, profitability, and employee satisfaction in establishing organization efficiency.

1.3. Factors Affecting Organization Efficiency

1.4. Limitations of Research

2. Review Methods

2.1. Measuring and Benchmarking Organizational Sustainability and Efficiency

- Identify “as is” state of organizational sustainability and efficiency in the organization;

- Identify best sustainability practices across peer organizations;

- Equip the organization with the appropriate tools and skills to implement the identified best practices to fill the efficiency gap.

- Strategic sustainability-realistic vision and goals established;

- Product and program sustainability-high-quality products, services, and programs developed;

- Personnel sustainability-personnel can effectively and reliably perform to fulfill their KPIs;

- Financial sustainability-profit generation as per agreed targets, adequate financial reserves, contingency planning, and positive cash flow to maintain sustained operation [44].

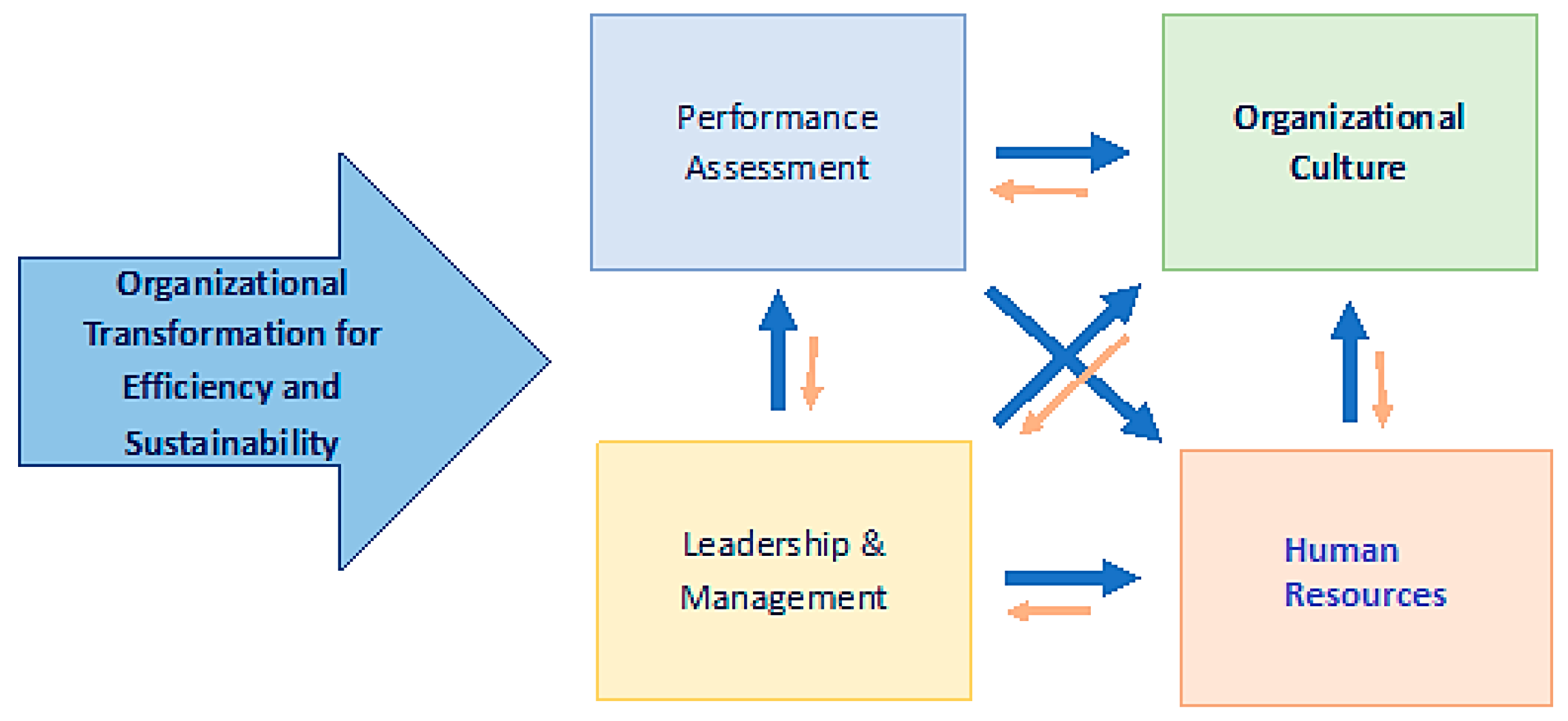

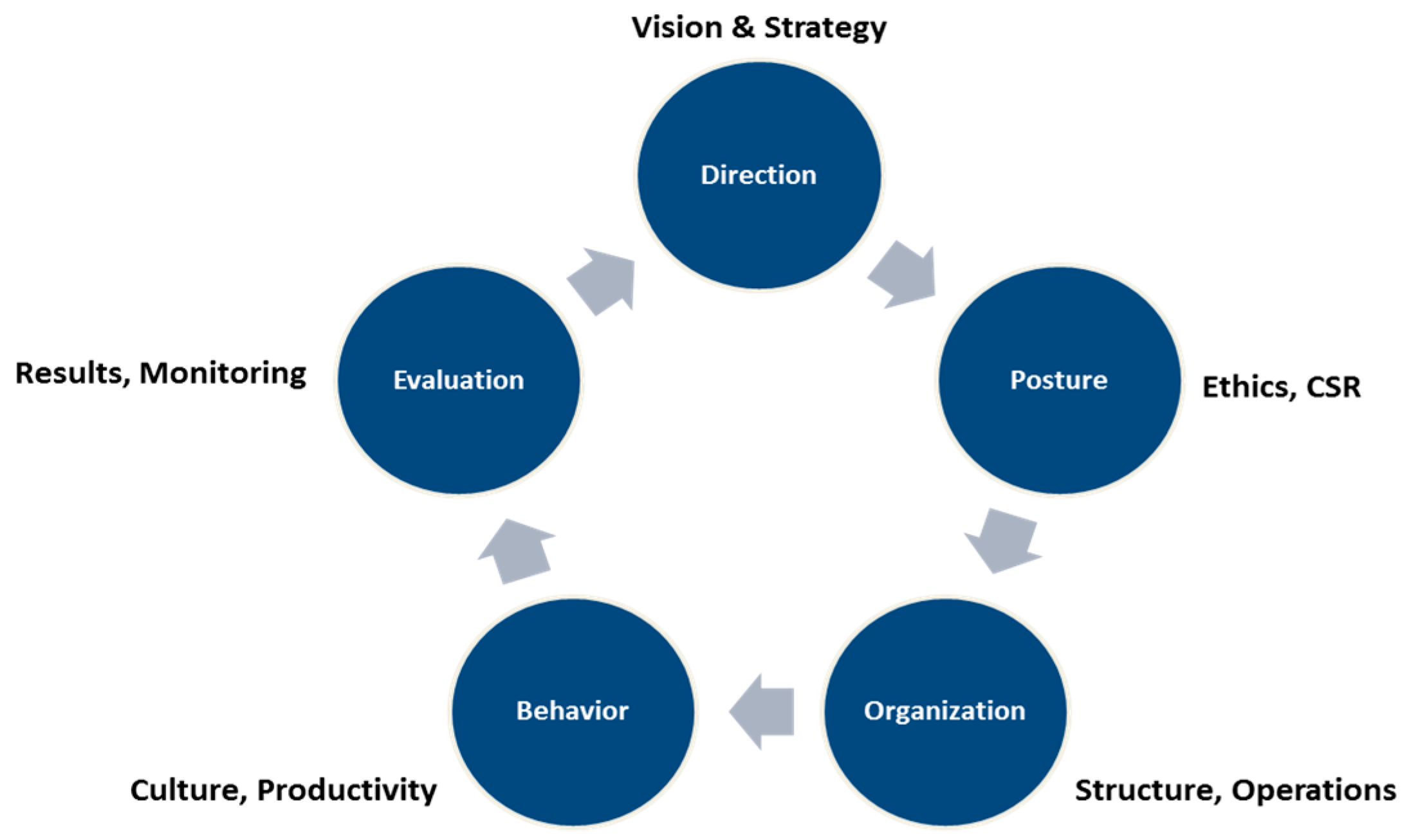

- Direction: In analyses of the economic health of the organization, the capacity to conceive and visualize strategic goals and developing plans to achieve them through encouraging innovation within the organization;

- Posture: Conduct of the management should be ethical to garner credibility and respect for the organization and to inculcate good attitudes and key behaviors that foster a performance culture and innovation to ensure the development of a balanced economy and society;

- Organization: Parameters measure the management activity of the organization in managing various process systems and technologies in the context of financial results and alignment to business strategies;

- Behavioral: Measurements of quality within the organization, and tracking compliance with standards and procedures within an organization to ensure efficiency and effectiveness in its operations;

- Evaluation: Measurements of efficiency and effectiveness of procedures and analyses organizational performance per the strategic objectives and goals of the organization.

- Direction:

- Mission, values, and corporate policies (Why?);

- Business strategy and definition of strategic objectives (How?);

- Timeframe and quantification of strategic objectives (When and what?);

- Integration of business strategy to economic group policies/strategies (How?);

- Action markets (Where?);

- Target customers (Who?);

- Products and services (What?);

- Time to market (When?);

- Products and services placement (How?).

- Posture:

- Values and corporate culture;

- Ethical principles;

- Organizational principles and code of conduct;

- Social responsibility principles and code of conduct;

- Environmental principles and code of conduct;

- Principles and codes of professional conduct;

- Principles of relationships with suppliers;

- Principles of action and participation in the community;

- Legal framework of activities.

- Organization:

- Organizational structure;

- Integration and compatibility of organizational structure in economic groups;

- Functional diagrams and operational rules;

- Organizational information systems;

- Training and information of employees, suppliers, and subcontractors;

- Planning of activities and resource allocation;

- Strategic business partnerships;

- Business units, geographic action areas, and subsidiaries/branch offices;

- Outsourcing of activities and functions.

- Behavior:

- Certifications and sub-systems of management;

- Level of effectiveness (objectives);

- Level of efficiency (resources);

- Productivity levels;

- Internal audits;

- Customers and employee’s satisfaction analyses;

- Action on internal faults and complaints;

- Continuous improvement processes;

- Conciliation between strategy and operational actions.

- Evaluation:

- Indicators and evaluation metrics;

- Evaluation of results;

- Appraisal between expected and obtained results;

- Monitoring of organizational efficiency;

- Monitoring of organizational effectiveness;

- Economic and markets analyses;

- Adjustment of actions according to results;

- Forecasting and development of future scenarios and potential markets;

- Strategic realignment procedures.

- Scores for each of the queries were analyzed based on the following scale:

- Explicitly defined, well exposed, and applied (Type 5);

- Explicitly defined but insufficiently exposed and applied (Type 4);

- Implicitly defined and collectively recognized (Type 3);

- Implicitly defined but individually recognized (Type 2);

- Undefined, not cleared, or not applied (Type 1);

- Do not know/do not answer/not applicable (Type 0);

- Type 5 denotes an organization with proper disclosure and a satisfactory evaluation from management;

- Type 4 organizations show that management is concerned and wants to improve the disclosure and knowledge effectiveness within an organization;

- Type 3 denotes the gaps in disclosure and knowledge effectiveness within an organization;

- Type 2 organizations have parameters but are susceptible to interpretation, and no general notion of parameters exists within such organizations;

- Type 1 denotes that neither parameters nor competencies are identified or tracked;

- Type 0 denotes the absence of knowledge about organizational sustainability parameters and competencies [45].

- Another model to determine the organization sustainability of corporations—this model facilitates the classification of organizations into one of the following six levels:

- Level 0: In such organizations, no steps are taken for sustainability. However, specific steps could be planned or initiated because of regulations such as government legislation on consumer protection. The organizations in this state are generally in a “pre-sustainability” state;

- Level 1: In such organizations, organization sustainability is considered a provision for societies’ welfare through actions such as CSR initiatives. Level 1 organizations are generally considered to have taken initial steps to improve organization sustainability;

- Level 2: In such organizations, organizational sustainability is considered in ethical, social, and environmental spheres because it strengthens organization market standing and brand equity, which are directly linked to the economic health of the organization. The primary motivator for Level 2 organizations are the economic benefits from the reputation of the brand;

- Level 3: In such organizations, an organization’s sustainability initiatives have matured. These organizations balance their social, economic, and environmental initiatives. Motivations for Level 3 organizations are beyond economic benefits and the well-being of society. Maximizing human potential and the well-being of the planet are critical motivators;

- Level 4: In such organizations, initiatives are implemented to create economic, social, and environmental benefits. Motivations for organizations at Level 4 are based on the knowledge that sustainability is part of the organization’s short- and long-term progress; hence, sustainability is inevitable;

- Level 5: In such organizations, sustainability is incorporated into every aspect of an organization to improve the standards of living of its employees, stakeholders, and surrounding community. The motivation occurs because individuals, the community, society, and organizations are interdependent, and a universal responsibility exists regarding sustaining the well-being of others.

2.2. Initial Review

2.3. Corporate Information on Qatari Organizations

3. Results and Discussion

3.1. Air Transport

3.2. Electric Utility

- Electricity Production/Supply

- Amount of electricity received from the power-generating units and sent to the grid for customers (gigawatt hour—GWh);

- Peak Demand—KWh (kilowatt hour);

- Average duration of power interruption per customer (Frequency/duration in minutes);

- Transmission losses (gigawatt hour—GWh).

- Water Supply Operations

- Total annual production of water—Million cubic meter MM3;

- Number of pipe bursts per 100 KM;

- Per capita water and electricity consumption (liter per head per day/watt-hour per person per month);

- Savings in potable water consumption for other uses through using treated sewage effluent (TSE).

- Human Resource Management

- Turnover rate %;

- Percentage of females employed concerning the total number of employees;

- Percentage of Qatari nationals employed concerning the total number of employees;

- Number of Qatari students sponsored for studies in local and international institutions;

- Total hours of training provided to full-time employees.

- Health Safety and Environment

- Recycled waste as a percent of total waste generated;

- CO2 emissions in tons;

- Number of fatalities per year;

- Number of reported injuries and frequency;

- Total hours lost because of injuries.

- Financial Indicators

- Total Revenue—QAR;

- Total operating cost—QAR;

- Gross/Net profit—QAR;

- Percentage of procurement spent on local suppliers;

- Total gross assets—QAR.

3.3. Oil and Gas

3.4. Retail Banking

- Customer satisfaction and data privacy;

- Regulatory compliance;

- Access to financial services;

- Responsible communication;

3.5. Steel Manufacturing

- Make steel matter–improving use of steel across various domains;

- Contribute to Qatar’s development;

- Reduce environmental impact through its operations;

- Ensure a safe and healthy work environment for its employees and contractors;

- Develop a high performing and motivated team of employees;

- Instill good governance and accountability;

- Achieve profitable growth.

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- O’Donnell, O.; Boyle, R. Understanding and Managing Organisational Culture; Institute of Public Administration: Dublin, Ireland, 2008; ISBN 978-1-904541-75-2. [Google Scholar]

- Corporate Knights. The results for the 2017 Global 100 Most Sustainable Corporations in the World index. 2015. Available online: https://www.corporateknights.com/magazines/2015-global-100-issue/2015-global-100-results-14218559/ (accessed on 29 May 2016).

- Qatargas. Forging Lasting Relationships Building on Qatargas’ reputation for safety, flexibility andreliability. Available online: https://www.qatargas.com/english/MediaCenter/The%20Pioneer/The%20Pioneer%20-%20Quarter%203,%202016.pdf (accessed on 2 August 2016).

- Posco. Integrated Report of Economic, Environmental and Social Sustainability. Posco Report 2016. Available online: http://www.posco.com/homepage/docs/eng5/dn/sustain/customer/2016_POSCO_Report_EN.pdf (accessed on 29 May 2016).

- Qatar Steel. Sustainbility Report; Qatar Steel: Mesaieed, Qatar, 2016. [Google Scholar]

- Fysikopoulos, A.; Pastras, G.; Theocharis Alexopoulos, T.; Chryssolouris, G. On a generalized approach to manufacturing energy efficiency. Int. J. Adv. Manuf. Technol. 2014, 73, 1437–1452. [Google Scholar] [CrossRef]

- Pinprayong, B.; Siengtai, S. Restructuring for organizational efficiency in the banking sector in Thailand: A case study of siam commercial bank. J. Psychol. Bus. 2012, 8, 29–42. [Google Scholar]

- Henri, J. Performance Measurment and Organizational Effectivness Bridging the Gap. Manag. Financ. 2004, 30, 93–123. [Google Scholar]

- Brovkin, V.; Sitch, S.; von Bloh, W.; Claussen, M.; Bauer, E.; Cramer, W. Role of land cover changes for atmospheric CO2 increase and climate change during the last 150 years. Glob. Chang. Biol. 2004, 10, 1253–1266. [Google Scholar] [CrossRef]

- Lewis, H.F.; Lock, K.A.; Sexton, T.R. Organizational capability, efficiency, and effectiveness in Major League Baseball: 1901–2002. Eur. J. Oper. Res. 2009, 197, 731–740. [Google Scholar] [CrossRef]

- Bartuševičienė, I.; Šakalytė, E. Organizational Assessment: Effectiveness Vs. Efficiency. Soc. Transform. Contemp. Soc. 2013, 2013, 45–53. [Google Scholar]

- Henry, E.A. Is The Influence of Organizational Culture on Organizational Effectiveness Universal? An Examination of The Relationship in The Electronic Media (Radio) Service Sector in The English Speaking Caribbean; Nova Southeastern University: Broward County, FL, USA, 2011. [Google Scholar]

- Federman, M. Essay: Towards An Effect-Ive Theory of Organizational Effectiveness. 2006. Available online: https://www.google.ch/url?sa=t&rct=j&q=&esrc=s&source=web&cd=2&cad=rja&uact=8&ved=2ahUKEwiFjuPM-aTlAhVQ3qQKHf0vDf0QFjABegQIAhAC&url=http%3A%2F%2Findividual.utoronto.ca%2Fmarkfederman%2FTowards_an_Effective_Theory_of_OE_Seminar.doc&usg=AOvVaw3yN-RXlNUuBhK1MDOIs7hd (accessed on 27 May 2016).

- Cameron, K. Measuring Organizational Effectiveness In Institutions Of Higher Education. Adm. Sci.Q. 1978, 23, 604–632. [Google Scholar] [CrossRef]

- Mccann, J. Organizational Effectiveness: Changing Concepts For Changing Environments. Hum. Resour. Plan. 2004, 27, 42. [Google Scholar]

- Balduck, A.L.; Buelens, M. A Two-Level Competing Values Approach to Measure Nonprofit Organizational Effectiveness. 2008. Available online: http://wps-feb.ugent.be/Papers/wp_08_510.pdf (accessed on 27 April 2017).

- Kilmann, R.H.; Herden, R.P. Towards Systemic Methodology For Evaluating The Impact Of Interventions On Organizational Effectiveness. Acad. Manag. Rev. 1976, 1, 87–98. [Google Scholar] [CrossRef]

- Hoy, F.; Hellriegel, D. The Kilmann and Herden Model of Organizational Effectiveness Criteria for Small Business Managers. Acad. Manag. J. 1982, 25, 308–322. [Google Scholar]

- Schermerhorn, J.A. Organizational Behavior; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2002. [Google Scholar]

- Ashraf, G.; Abd Kadir, S. bte A review on the models of organizational effectiveness: A look at Cameron’s model in higher education. Int. Educ. Stud. 2012, 5, 80–87. [Google Scholar] [CrossRef]

- Bass, B.M. From transactional to transformational leadership: Learning to share the vision. Organ. Dyn. 1990, 18, 19–31. [Google Scholar] [CrossRef]

- Tuttle, S.S. Planning and Measurement in Your Organization of the Future; Industrial Engineering and Management Press: Norcross, GA, USA, 1989. [Google Scholar]

- Higgins, R. Organizational transformation What is it, why do it, and how? 2010. Available online: https://www.opm.gov/policy-data-oversight/performance-management/reference-materials/historical/planning-and-measurement-in-your-organization-of-the-future/ (accessed on 29 August 2018).

- Yilmaz, C.; Ergun, E. Organizational culture and firm effectiveness: An examination of relative effects of culture traits and the balanced culture hypothesis in an emerging economy. J. World Bus. 2008, 43, 290–306. [Google Scholar] [CrossRef]

- Wright, P.M.; Dunford, B.B.; Snell, S.A. Human resources and the resource based view of the firm. J. Manage. 2001, 27, 701–721. [Google Scholar] [CrossRef]

- Marimuthu, A. Human Capital Development and Its Impact on Firm Performance: Evidence From Developmental Economics. J. Int. Soc. Res. 2009, 2, 265–272. [Google Scholar]

- Alnasseri, N.; Osborne, A.; Steel, G. Organizational Culture, Leadership Style and Effectiveness: A Case Study of Middle Eastern Construction Clients. In Proceedings of the 29th Annu ARCOM Conference, Reading, UK, 2–4 September 2013; pp. 393–403. [Google Scholar]

- William, B. (Ed.) Managing Transition: Making the most of Change; Da Capo Lifelong Books: Boston, MA, USA, 2010. [Google Scholar]

- Estalaki, K.G. On the impact of organizational structure on organizational efficiency in industrial units: Industrial units of Kerman and Hormozgan Provinces. 2017. Available online: https://www.researchgate.net/publication/321927740_On_the_impact_of_organizational_structure_on_organizational_efficiency_in_industrial_units_industrial_units_of_Kerman_and_Hormozgan_provinces (accessed on 11 August 2016).

- Scott, D.; Bishop, J.W.; Chen, X. an Examination of the Relationship of Employee Involvement With Job Satisfaction, Employee Cooperation, and Intention To Quit in U.S. Invested Enterprise in China. Int. J. Organ. Anal. 2003, 11, 3–19. [Google Scholar] [CrossRef]

- Greenberg, J. The intellectual adolescence of organizational justice: You’ve come a long way, maybe. Soc. Justice Res. 1993, 6, 135–148. [Google Scholar] [CrossRef]

- Choudhry, N.; Philip, P.J.; Kumar, R. Impact of Organizational Justice on Organizational Effectiveness. Ind. Eng. Lett. 2011, 1, 18–25. [Google Scholar]

- Cohen, W. Drucker on Leadership: New Lessons from the Father of Modern Management; Jossey-Bass: San Francisco, CA, USA, 2010. [Google Scholar]

- Pasmore, W.; Wiley, C.; Lacey, A.; Luff, D.; Arham, A.F.; Authors, F.; Corriere, M.A.; Rosenbloom, D.H.; Crewson, P.E.; DeBerry, S.L.; et al. The Relationship between Leadership, Effectiveness and Organizational Performance. Cent. Creat. Leadersh. 2014, 11, 1–28. [Google Scholar]

- Khan, R.A.G.; Khan, F.A.; Khan, M.A. Impact of Training and Development on Organizational Performance. Glob. J. Manag. Bus. Res. 2011, 11, 63–69. [Google Scholar]

- Schultz, T.W. Human Capital: Policy Issues and Research Opportunities. 1972. Available online: https://core.ac.uk/download/pdf/6908045.pdf. (accessed on 12 September 2017).

- Harbison, F. Educational Planning and Human Resource Development; UNESDOC: Paris, France, 1967. [Google Scholar]

- Bing, J.; Gardelliano, S. Team Building at the United Nations Industrial Development Organization; UNIDO: Vienna, Austria, 2005. [Google Scholar]

- Sharma, V.C.; Jain, T.K. Leadership Practices in India and the USA. ADR J. 2016, 3, 7–10. [Google Scholar]

- Rudnick, M.; Kouba, W. Is Transforming Employee ( Hint: It has nothing to do with search). 2006. Available online: https://robertoigarza.files.wordpress.com/2008/11/rep-how-the-google-effect-is-transforming-employee-communications-ww-2006.pdf (accessed on 12 September 2017).

- Jones, J.L.S.; Linderman, K. Process management, innovation and efficiency performance: The moderating effect of competitive intensity. Bus. Process Manag. J. 2014, 20, 335–358. [Google Scholar] [CrossRef]

- Visser, W. Corporate sustainability and the individual: A literature review. 2007. Available online: http://www.waynevisser.com/wp-content/uploads/2007/05/paper_sustainability_individual_lit_wvisser.pdf (accessed on 13 March 2017).

- Porter, M.E.; Kramer, M.R. The Big Idea: Creating Shared Value. Harv. Bus. Rev. 2011, 89, 62–77. [Google Scholar]

- Anderson, C.; Brown, C.E. The functions and dysfunctions of hierarchy. Res. Organ. Behav. 2010, 30, 55–89. [Google Scholar] [CrossRef]

- Santos, J.R.; Anunciação, P.F.; Svirina, A. A Tool To Measure Organizational Sustainability Strength. 2013. Available online: https://core.ac.uk/download/pdf/62691770.pdf (accessed on 14 February 2018).

- Cella-de-oliveira, F.A. Indicators of Organizational Sustainability: A Proposition From Organizational Competences. Int. Rev. Manag. Bus. Res. 2013, 2, 962–979. [Google Scholar]

- Tranfield, D.; Denyer, D.; Smart, P. Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Cameron, K.S.; Whetten, D.A. Organizational Effectiveness and Quality: The Second Generation. Handb. Theory Res. 1996, XI, 265–306. [Google Scholar]

- Qatar Airways. Sustainbility Report; Qatar Airways: Mesaieed, Qatar, 2017. [Google Scholar]

- Kahramaa. Sustainbility Report; Kahramaa: Doha, Qatar, 2016. [Google Scholar]

- QP Annual Review. Qatar Pet. 2016, 91, 399–404.

- Oryx GTL Limited. Committed to Excellence. 2016. Available online: http://www.oryxgtl.com.qa/sustainability-reports/Oryx_Sustainability_Report_V6.pdf (accessed on 14 February 2018).

- Qchem. Sustainbility Report; Qchem: Mesaieed, Qatar, 2016. [Google Scholar]

- Doha Bank. Sustainbility Report; Doha Bank: Doha, Qatar, 2016. [Google Scholar]

- Qatar Steel. Sustainbility Report. 2015. Available online: https://www.qatarsteel.com.qa/wp-content/uploads/2016/12/sustainability-Report-2015.pdf (accessed on 14 February 2018).

- Tretyakov, S. Business Operations between Efficiency and Effectiveness. J. Inf. Organ. Sci. 2014, 30, 251–262. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Steps Taken during the Systematic Review | Description and Results | |

|---|---|---|

| Step 1—Keywords | Organization Performance, Business Efficiency, Organization Effectiveness, and Organization Efficiency Measurement | |

| Step 2—Inclusion, Exclusion criteria | Basic Search Criteria |

|

| Initial Criteria |

| |

| Final Criteria |

| |

| Step 3—Search database | Science Direct, Springer, Wiley, Sage, Taylor and Francis, JSTOR, Emerald, and Google Scholar | |

| Step 4—Results Returned | Science Direct (^) | 5267 |

| Springer (+) | 19 | |

| Wiley (*) | 18 | |

| Sage (*) | 7 | |

| Taylor and Francis (*) | 8 | |

| JSTOR (^) | 317 | |

| Google Scholar (+) | 22 | |

| Emerald (*) | 6 | |

| Step 5—Number of articles selected after the initial screening | 66 | |

| Step 6—Number of articles selected after final screening | 40 | |

| No | Organization | Industry | Year of Publishing |

|---|---|---|---|

| 1 | Qatar Petroleum | Oil and Gas | 2016 |

| 2 | Doha Bank | Retail Banking | 2016 |

| 3 | Dolphin Energy | Oil and Gas | 2015 |

| 4 | Kahramaa | Utilities | 2016 |

| 5 | Nakilat | LNG Transportation | 2016 |

| 6 | Oryx GTL | Oil and Gas | 2015 |

| 7 | Qatar Airways | Aviation | 2016 |

| 8 | Qatar Fertilizer Company | Fertilizers | 2016 |

| 9 | Qatar Gas | Oil and Gas | 2016 |

| 10 | Qatar Steel | Steel Production | 2016 |

| 11 | Qatalum | Aluminum Production | 2016 |

| 12 | Q Chem | Industrial Chemicals | 2016 |

| 13 | Vodafone | Telecom | 2016 |

| 14 | Woqood | Fuels | 2016 |

| No | Organization | Industry | Publishing Year |

|---|---|---|---|

| 1 | Ahli Bank | Retail Banking | 2017 |

| 2 | Al Meera | Retail Stores chain | 2016 |

| 3 | Aamal Holdings | Industrial Conglomerate | 2016 |

| 4 | Mannai Corporation | Industrial Conglomerate | 2017 |

| 5 | Barwa Real estate | Real estate Management | 2017 |

| 6 | Commercial Bank | Retail Banking | 2016 |

| 7 | Ooredoo | Telecom | 2016 |

| 8 | Qapco | Petrochemicals | 2016 |

| 9 | Qatar Islamic Bank | Retail Banking | 2016 |

| 10 | Qatar Petroleum | Oil and Gas | 2016 |

| 11 | Qatar Tourism Authority | Tourism Regulator | 2016 |

| No | Organization | Industry | Year of Publishing |

|---|---|---|---|

| 1 | Ahli Bank | Retail Banking | 2017 |

| 2 | Al Meera | Retail Stores chain | 2016 |

| 3 | Aamal Holdings | Industrial Conglomerate | 2016 |

| 4 | Mannai Corporation | Industrial Conglomerate | 2017 |

| 5 | Barwa Real estate | Real estate Management | 2017 |

| 6 | Commercial Bank | Retail Banking | 2016 |

| 7 | Ooredoo | Telecom | 2016 |

| 8 | Qapco | Petrochemicals | 2016 |

| 9 | Qatar Islamic Bank | Retail Banking | 2016 |

| 10 | Qatar Petroleum | Oil and Gas | 2016 |

| 11 | Qatar Tourism Authority | Tourism Regulator | 2016 |

| Worker’s health and safety | Contribution to the national economy |

| Governance and legal compliance | Product and service quality |

| Production/Output | Human Rights |

| Process safety/emergency management | Emissions |

| Flaring (effluent gas burning process) | Effluent Management |

| Business ethics | Managing oil spills |

| Qatarization | Water Management |

| Financial growth | Energy efficiency |

| Employment creation | Welfare of the workforce and employee engagement |

| Sustain financial performance | Contractor safety |

| Employee safety | Product traceability |

| Product quality | Operational efficiency |

| Product innovation | Occupational health |

| Customer satisfaction | Qatarization |

| Emergency response preparedness | Corporate governance |

| Waste management and recycling | Water consumption |

| Energy consumption | Training and development |

| Greenhouse gases emission | Performance-based compensation and rewards |

| Risk Management | Strategic investments |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Al-Shaiba, A.S.; Al-Ghamdi, S.G.; Koc, M. Comparative Review and Analysis of Organizational (In)Efficiency Indicators in Qatar. Sustainability 2019, 11, 6566. https://doi.org/10.3390/su11236566

Al-Shaiba AS, Al-Ghamdi SG, Koc M. Comparative Review and Analysis of Organizational (In)Efficiency Indicators in Qatar. Sustainability. 2019; 11(23):6566. https://doi.org/10.3390/su11236566

Chicago/Turabian StyleAl-Shaiba, Abdulla S., Sami G. Al-Ghamdi, and Muammer Koc. 2019. "Comparative Review and Analysis of Organizational (In)Efficiency Indicators in Qatar" Sustainability 11, no. 23: 6566. https://doi.org/10.3390/su11236566

APA StyleAl-Shaiba, A. S., Al-Ghamdi, S. G., & Koc, M. (2019). Comparative Review and Analysis of Organizational (In)Efficiency Indicators in Qatar. Sustainability, 11(23), 6566. https://doi.org/10.3390/su11236566