1. Introduction

The profession of property valuer plays a key role in many areas of economic activity, influencing the financial decisions and assets of companies, institutions, public entities, and individuals. They act as experts in a market that has been traditionally considered as inefficient [

1], mainly because of the heterogeneity, indivisibility, and illiquidity of real estate, and the classic causes of market failure like information asymmetry, high information and transaction costs, and the existence of externalities and public goods [

2]. Although other studies call into question the hypothesis of the low efficiency of the real estate market (for a review of the literature, see [

3,

4]), the specific characteristics of real estate products and the real estate market can certainly not be denied. Despite the advancements in information and communication technologies [

5], information asymmetry is a failure that still affects the functioning of the real estate market [

6,

7]. The property valuer performs an important, efficiency-enhancing role [

8] by estimating the market value of a property as the most likely price to be obtained in an open market transaction [

9], thereby guiding market participants [

10]. Nevertheless, in their professional practice, property valuers also deal with the problem of market information transparency, the complexities of the valuation process, and an information-rich environment [

9].

Valuation outcomes are a function of the information gathered by the property expert and their ability to process this information [

5]; however, they always remain in greater or lesser uncertainty about the information used as input and the results achieved as an output [

11]. The problem of information limitations and uncertainty in valuation has two corollaries. One is related to the property valuer’s potential susceptibility to influence from a third party, and the other is professional experience and education. The latter promotes professionalism and independence in the valuation process, which should go hand-in-hand with accountability for their valuation advice in terms of social responsibility and a sustainable property market development [

12].

The foundations on which the profession of the appraiser is built are the relevant competencies (in some countries confirmed by certificates attesting to knowledge and experience) and principles of professional ethics, such as integrity, impartiality, objectivity, and independence from the influence of any stakeholders over the valuation process. Compliance with the standards of professional practice and legal regulations, as well as conducting professional activities within the existing institutional framework, guarantees clients the appropriate quality of services and adequacy of valuations. Moreover, in a broader context, it allows the valuer to fulfil their role as members of an institution founded on public trust, social responsibility, and professionalism [

12]. Even highly qualified experts, however, face limitations from market circumstances, like information access, dataset quality, and uncertainty about market prospects [

13,

14], or from individual decision-making, such as biases and heuristics [

15,

16,

17,

18,

19], all of which may affect the accuracy of valuations. Research also shows that ethical values, being fundamental for the profession, vary according to characteristics such as age, experience, and education [

20]. Moreover, there is also evidence that gender may diversify responses to ethical dilemmas [

21]. Thus, because of the importance of valuation accuracy for business and individual decision-making, and the evidence of relatively high variance in property valuations [

14,

22,

23,

24,

25], discussions have revolved around the factors influencing valuation outcomes.

Among an increasing number of studies emphasizing the behavioral nature of factors impacting valuation outcomes, those arising from the relationship between the valuer and their clients are the most intensively explored [

26]. Roberts and Roberts [

27] stress that the most frequent causes of variance stem from the influence of someone who has an interest in the particular property. They point at the client as a major party dictating the circumstances under which the property is valued. So far, studies verifying this belief have been conducted only in a few countries: New Zealand [

28,

29], the USA [

9,

30,

31,

32,

33,

34,

35], the UK [

5,

10,

30,

36,

37], Nigeria [

38,

39,

40], Singapore [

41,

42], Taiwan [

41,

43], and Malaysia [

44]. To the best of our knowledge, there is only one published work (see [

45]) relating to the impact of client pressure on Polish valuers; however, the survey method used to identify biased valuations seems debatable. In light of the results of a research experiment conducted by Gallimore and Wolverton [

30] on American appraisers and British valuers, which indicated the impact of cultural context on valuation outcomes, it seems justified to extend the research to other countries, taking into account their specificities. A particularly clear research gap concerns the countries of Central and Eastern Europe, where the profession of property valuer was established after 1990. Although these countries have drawn on the experience of well-established democracies, and to a greater or lesser extent the practice of valuations, the economic environment and the institutional frameworks differ. Therefore, the main objective of our research is to determine which of the factors characterizing the valuer and their professional activity may be vulnerable to pressure from the client. The implementation of the main objective will allow us to answer the following research questions:

Do the main characteristics of the valuer (age and professional experience) influence how client pressure is perceived?

Do other characteristics of the valuer, namely gender, education, and the scope of professional activity, influence the perception of pressure from the client?

Our research findings contribute to current knowledge of the influence of the client on valuation, primarily from the perspective of the property valuer. To a certain extent, we follow Kucharska-Stasiak, Źróbek, and Cellmer [

45]; however, we focus on the valuers’ perception of pressure rather than the impact of this pressure on valuation results. Such an approach allows us to obtain more reliable and realistic answers from respondents, as opposed to posing direct questions about client pressure and its impact on valuation outcomes. We expect that the perception of pressure varies, and that it results, among other things, from the characteristics of the valuer and the specific valuation circumstances. The feeling of pressure itself does not mean giving in to it; however, it can be assumed that some cases may result in valuation bias.

The analysis was based on unique data from a detailed survey conducted among practicing Polish valuers affiliated to professional associations. The research sample consisted of 278 correctly completed questionnaire forms. We used the linear probability and logit models to analyze the relationship between certain valuer and valuation features and valuer perception of client pressure. Our findings show that the perception of pressure is influenced by the following variables: gender, age, work experience, education, territorial coverage of the valuer’s business, and client type. Our research is exceptional not only because of its cultural context but also for focusing on relatively understudied valuer-related factors correlated with client pressure, and for taking into account the institutional framework of valuer activities, indicating directions for change that could contribute to more reliable and objective valuations in developing real estate markets. Over the years, Polish property valuers have faced not only economic changes, affecting the formation and development of the real estate market, but also the remodeling of the legal and institutional environment. Although the profession has undergone a number of transformations, there are still several issues worth discussing.

The paper is organized as follows.

Section 2 contains an overview of the relevant literature.

Section 3 provides an institutional background for the valuation profession in Poland.

Section 4 outlines the main weaknesses of the profession and their impact on valuer performance.

Section 5 presents an empirical strategy and the data used.

Section 6 includes model estimations and a discussion of the results. Finally,

Section 7 rounds the conclusions.

2. Previous Studies

In the literature, there are two main streams in behavioral research on property valuation. The first has its roots in more general studies on the nature of decision-making, derived from cognitive psychology [

46], and focuses on the outcome of valuation in light of the influence of bias and heuristics [

47]. The second is based on agency problems in the context of moral hazards [

48] in client–agent relationships and looks at the causes of unreliable valuation under the influence of the client. Both of these trends overlap in some areas. As Diaz [

49] states, anchoring a valuation can be both the result of the influence of heuristics in decision-making as well as the client–valuer relationship [

50].

The influence that the client tries to exert on the valuer takes various forms. In the literature, terms such as pressure and feedback are often used interchangeably. Achu [

26] noted the way in which a customer acts and whether their actions actually change the outcome of the valuation or are merely a direct or indirect attempt to exert influence. For the purposes of this research, we used the term “pressure” to denote direct client action, not necessarily resulting in real impact on the valuation outcome.

Empirical research on client pressure and its causes was initiated by Roberts and Roberts [

27], based on case studies presenting a variety of reasons for discrepancies between the value of a property and the transaction price achieved, as well as between valuations by different valuers. They suggest that client influence is one of the primary drivers behind these disparities. One of the first studies conducted in the United States by Smolen and Hambleton [

31] aimed at identifying customer pressure on valuers. The results were overwhelming. Their survey shows that almost 80% of valuers recognized the influence of clients on the estimated value. This is manifested in both client actions aimed at altering the value as well as the tendency of valuers to, alarmingly, service their clients’ demands by providing unrealistic valuations. Mortgage lenders and commercial bankers appeared to be the most likely to pressure valuers. The power of this pressure comes from the relatively high degree of substantial financial consequences for valuers and their business, who risk their removal from the accepted valuers’ list and the subsequent decrease of future instructions. Other studies confirm the widespread occurrence of customer pressure. For example, in surveys by Kinnard, Lenk, and Worzala [

32] as well as Worzala, Lenk, and Kinnard [

33] conducted on commercial and residential valuers, over 90% of respondents declared that they had experienced client pressure. The results of the above early studies consistently show that this is a problem mainly affecting commercial valuers who experience various types of pressure, including direct threats to “opinion shop” [

51] prior to handing the appraisal instruction [

32]. In a similar survey conducted in Singapore, 85% of respondents confirmed that valuers are sometimes under client pressure to change the value of the property appraised. Studies in Nigeria [

38] also supported earlier results. The vast majority of respondents (80%) indicated that clients seek to influence valuers in order to alter the outcome of the appraisal. Another survey in Taiwan [

43] showed that 89% of respondents admitted that clients would explicitly or implicitly suggest an expected value, and 56% of the valuers reported that the valuation was affected by client expectations.

The influence of customers on property valuers and appraisal results is determined by various factors. Levy and Schuck [

28,

29] identified a set of factors determining the type and magnitude of the impact of the customer, distinguishing four main categories: (1) valuer and appraisal company characteristics, (2) client characteristics, (3) appraisal characteristics, and (4) external characteristics. Their qualitative research was conducted from the perspective of both valuers and clients ordering appraisals. On the basis of a literature review, Achu [

26] rebuilt Levy and Shuck’s [

28] model of client influence. Next, Crosby, Devaney, Lizieri, and McAllister [

10] proposed a conceptual model of the determinants of client influence on appraisals. They note that the extent of customer influence is the “product of balance” of a set of external and internal factors affecting both the client and the valuer. For the client, one of the most critical drivers for exerting pressure on the valuer is the importance of the appraisal, while for the valuer the incentive to succumb to that pressure is rooted in economic dependence [

10].

The multitude of identified factors pointing at client influence and estimation bias has encouraged research in this field. So far, however, only selected factors have been empirically verified, with a number identified from respondents’ opinions but lacking solid empirical evidence.

Table 1 presents a summary of previous study results, in which a regression analysis was used to confirm the relationship between specific factors related to valuer or client characteristics, where client pressure was the dependent variable. Valuer characteristics such as age, experience, and education have been investigated in a few papers, but the results are ambiguous [

34,

43,

45]. Gender, as a differentiating factor in the exertion of client pressure or its impact on valuation results, is most often ignored. Only in [

45] was gender found to be a significant factor influencing the odds of effective client pressure. According to this research, it is slightly more frequent for males to have their valuations affected by clients. The relationship between gender and ethics or rules has attracted more interest in the field of business ethics [

21]. Although the results of such studies vary, Hoffman [

21] states that the way men and women respond to ethical dilemmas depends on the ethical issue and/or the strategic situation associated with the ethical dilemma, with women responding more ethically in some situations.

Appraisal company characteristics, like the range of services offered [

34] and the size of the company [

43], have been found to be statistically significant in regression analyses. Wolverton [

34] has interpreted the positive impact of valuer affiliation with the firm offering consulting services on coercive client pressure as the result of probable internal conflicts of interest in these kinds of firms. A partly opposite conclusion can be drawn from the studies by Chen and Yu [

41], in which the investigated valuers in Taiwan indicated that multiservice companies providing broader consultancy services are better at resisting client pressure. According to research by Liao, Chu, and Peng [

43] in Taiwan, company size in practice weakens the independence of appraisals as a consequence of the pressure under which large appraisal companies perform. The territorial range of services offered by valuers or appraisal companies have not been a subject of analytical study in client–valuer relationship research so far; however, Havard [

47] emphasizes the importance of the degree of familiarity with the location for a valuer’s use of heuristics.

The impact of client characteristics on the appraisal process and outcomes has been of greater interest than the valuer or appraisal company characteristics, although empirical evidence provided through analytical investigation is relatively weak and ambiguous. Evidence of pressure exerted by certain groups of clients arises from questionnaire research [

10,

31,

38,

42] and analytical examinations [

34]. According to the above, the types of clients who put pressure on valuers in order to influence the appraisal results include mortgage banks, loan companies, institutional investors, developers, and private individuals. Client size as a factor effectively affecting appraisal results was verified through regression analysis based on data from the case scenario questionnaire by Kinnard, Lenk, and Worzala [

32]. Conversely, similar research by Worzala, Lenk, and Kinnard [

33], Shi-Ming [

42], as well as Amidu and Aluko [

38] has found lack of significance of the client size factor. Other studies, based on the opinions of valuers from Singapore, suggest that long-term clients, clients more familiar with the firms, clients more knowledgeable about a property market, clients with more information, and clients that are investors tend to exert stronger pressure compared to others [

41].

Different approaches to define client pressure and methods of collecting and analyzing data pose limitations to the interpretation and comparison of the research findings. Mainstream research is based on quasi-experiments [

32,

33,

38,

42], interviews [

28,

29,

36], and surveys [

31,

35,

39]. It is likely, however, that in the case of sensitive ethical problems, both experimental and survey studies do not reflect reality fully. The analysis of data is also carried out in a number of ways: descriptive statistics, statistical tests, factor analysis, and econometric models (mostly the logistic regression model). Even where econometric models were used, the way of defining a dependent variable was not uniform. Moreover, empirical findings may naturally differ because of the regulatory environment, market conditions, and the overall cultural context based on the timing and locality of a particular study. The above claims have been partly supported by cross-reference studies by Gallimore and Wolverton [

30], examining in parallel American and British valuers, and by Chen and Yu [

41], investigating licensed valuers in Singapore and Taiwan. Differences in research findings were attributed to the local context. Therefore, the primary aim of the research in client–valuer relationships is not so much to find universal factors for the unethical behavior of both clients and valuers, but rather to study this phenomenon and provide empirical evidence with problem-solving solutions relevant to different institutional conditions.

3. Institutional Background

The basis for the functioning of the valuation profession in Poland, as in other post-communist countries, was laid out in 1990 with the emergence of the capitalist economy [

52,

53,

54]. The real estate market transformation process has been ongoing for almost a decade and has been carried out in distinct stages resulting in the adoption of changes in the existing legal, financial, administrative, fiscal, and social systems [

55,

56]. Processes such as property privatization, private ownership rights protection, financial liberalization, legal reforms, and infrastructure development are the driving forces behind further market development in increasing availability and attractiveness to individual and institutional investors.

The Polish market has opened up to new real estate transactions made for different purposes, both in the private and public sectors. Regardless of the ownership and functional structure of a property, all transactions were dealt with at arm’s length, which required information concerning the market value of that property. Prior to the transformation, the concept of market value did not exist in the Polish valuation nomenclature. Because of the lack of transaction data, limited legal regulations, and unformed valuation methodology, properties were only valuated through the replacement cost approach. In the new reality, this valuation concept has become ineffective in relation to market needs. It became necessary to build a comprehensive system of property valuation, adhering to institutional and legal frameworks, which led to the establishment of the profession of property valuer.

The formation process of the real estate appraisal profession lasted over seven years. It was a time of significant changes covering many areas of market functioning, including the regulation of the procedures for transforming the legal status of real estate, the setting out of the principles of recording real estate transactions and collecting market data by various institutions, and finally the methodology of property valuation. During that time, the principles of granting professional qualifications to property valuers and the requirements for the candidates were systematically specified. The idea was to create both an educational system for candidates to prepare theoretically and practically for the profession, and the requirements to verify the acquired qualifications. All this was intended to create a group of respected professionals capable of providing a wide range of valuation services.

A milestone for the profession of property valuer was the Real Estate Act—so far the most important legal regulation concerning valuers’ activity. Since then, the requirements for obtaining professional qualifications and the valuation methodology have been included in state law. According to the Act, only persons with a postgraduate degree who have completed two semesters in the field of valuation and 12 months of professional practice (with the requirement to make 15 appraisals), and who have passed written and oral state exams, could become valuers.

In addition to the requirements for candidates, the law has regulated the professional activities of existing valuers. Upon obtaining their professional qualifications, all property valuers must possess mandatory third-party liability insurance and are required to continue their education and professional development. For the first time, legislation covered the valuation methodology, officially indicating four main approaches. The Act defined certain types of real estate value and assigned approaches to them. It strongly interfered in the area of valuation for public–private settlements. It regulated the role of the valuer for public auctions, administrative fees (i.e., perpetual usufruct fees, adjacent fees), or any settlements accompanying property expropriation. In this respect, the Act and its executive regulations precisely indicate the type of estimated value and suggest an appropriate valuation methodology. The role of the valuer has become very formalized, and the methodology has been rigidly adjusted to the type of valuation.

Legal regulations are supported by professional standards. Polish professional standards are closely related to developments in the field of valuation theory and practice, and they are harmonized with European and international standards. Although constantly improved and re-evaluated, however, Polish professional standards are treated only as recommendations, which the valuer is not obliged to follow.

The second milestone in the establishment of the institutional framework for the profession was the introduction of the so-called deregulation process, conducted by the Polish government in 2014. The state’s policy was to limit interventionism in professional activities and facilitate access to the many professions previously regulated by state law. The deregulation process included property valuers.

Deregulation has indeed facilitated access to the profession of property valuation by lowering the requirements for candidates in terms of education. It became possible to obtain professional qualifications with only a bachelor’s, as opposed to a master’s degree, as previously required. The two semesters of postgraduate studies were still required, but the mandatory minimum duration of the internship was decreased from 12 to 6 months, and the number of required appraisal reports prepared by the apprentice was limited from 15 to 6. The appraisal state exam requirements were also lowered. Thus far, the exam covered 90 multiple-choice questions, one case study task, and the analysis of three appraisal reports. After the deregulation process, the case study part was omitted, and the number of analyzed reports was reduced to two.

Lowering the requirements shortened the time needed to prepare for the profession and simplified access to it, which was the main intention of the legislator, but unfortunately it contributed to a decrease in the quality of services provided by valuers [

57]. The following section presents the weaknesses of the profession that may affect the resistance of Polish property valuers to client pressure.

4. Weaknesses of the Profession and Their Impact on Valuers’ Performance

The limited transparency of the real estate market results in investment decisions made in the face of uncertainty and lack of reliable data. In such circumstances, a correctly and objectively determined value of real estate supports the decision-making process with regard to the allocation of resources in the real estate market, affecting the sustainability of market development in general [

58]. Determining the value of real estate undoubtedly requires the valuer’s independence, their objectivity, and their ability to justify the results. The problem of customer pressure on valuation results certainly exists. Regardless of the legal status of the profession, it is an undeniable fact that the valuer is a service provider that performs their activities for the benefit of clients who usually have specific expectations about the outcome of valuations. An indication of the expected value by the client is quite natural and can be considered common, resulting from the willingness to share their business expectations for the property with the person who is to appraise it. In these circumstances, the key issue is the perception of the strength of this suggestion and the valuer’s resistance to any pressure exerted. Knowing the expected value can anchor the valuer and subconsciously influence their work. It can also encourage an unethical valuer to succumb to the client’s suggestions and manipulate the valuation process.

For the purposes of this article, the authors present only the most important issues related to the profession of property valuers, which may affect their perception of pressure as exerted by clients. This is based on the arguments of Hill et al. [

12] that the allocation of responsibility for acting in the public interest rests with the individual professional and the institution and, in some cases, requires collaboration across the built environment institutions.

The following institutional weaknesses of the real estate appraisal profession in Poland do not constitute a criticism of the existing system; they only indicate potential areas that may affect the bias of valuations. The following areas were identified on the basis of the conducted research and the opinion of Polish valuation experts (see [

57,

59,

60]).

4.1. Insufficient Requirements for Candidates

First of all, as mentioned above, professional activities in the field of property valuation in Poland can only be performed by authorized experts who have complied with the statutory requirements. These are persons who have completed higher education and relevant postgraduate studies in real estate appraisal, who then underwent an appraisal apprenticeship and passed the state exam. The law allows for shortening this educational path only in justified cases. Usually, under normal circumstances, with a university degree, it is necessary to spend an additional two years preparing for property appraising. The minimum age to become a valuer is 24, if the requirements are met.

The postgraduate studies mainly include theoretical knowledge in the fields of economics, law, real estate general information, construction, spatial management, and valuation methodology. The candidates gain practical skills during the internship to prepare appraisal reports under the supervision of an experienced valuer. As a result of the deregulation of the profession, the duration of the internship and its program have been reduced. At present, six valuation projects are sufficient to complete the practical level of professional preparation. Unfortunately, the program does not reflect the types of valuations that the future valuer will have to deal with in his or her work. During both the studies and the internship, issues such as winning briefs, negotiating, questioning, or defending the valuation result among others are omitted. Young valuers experience these issues later in their work life when they start cooperating with clients and prepare their own valuations. Unfortunately, they are then no longer supported by a supervisor. Inability to cope with these problems, combined with young age and inexperience, may affect the independence of the valuer, his or her self-confidence, and, thus, his or her resistance to client influence.

4.2. Lowering the Quality of Services and Their Prices

The deregulation process has definitely facilitated access to the profession, which resulted in increasing the number of valuers who are insufficiently prepared to perform high-quality valuations. Polish valuers attract clients through price, rather than qualitative, incentives [

61]. Property valuation services in Poland on the so-called consumer market have an excessive supply of service providers, which may encourage clients to sift through the competition and find those valuers who are able to succumb to pressure and make a deceptive valuation. Such a situation may be an opportunity for dishonest and unethical valuers to obtain or retain clients expecting biased valuations.

The customer market has another consequence. Competing valuers lower the prices of their services. The willingness to receive higher remuneration can be an effective incentive to prepare an unethical valuation about a property.

4.3. Questioning the Valuation Results

Lowering the quality of valuations often causes a need to verify the correctness and usefulness of the valuation reports. Even if this procedure lowers the reputation of valuers as experts, it has become an integral part of the profession. The Real Estate Act has assigned appropriate powers to the Professional Responsibility Commission and other professional organizations to supervise the proper performance of the activities of valuers. The role of the Professional Responsibility Commission is to investigate professional liability issues, mainly in the area of compliance of professional activities with statutory requirements. Other bodies, such as local professional associations, are exclusively authorized to assess the correctness of the valuation reports.

In practice, the party unsure or dissatisfied with the result of the valuation can obtain an opinion on the correctness of the valuation report. A negative assessment of the professional association is the basis for questioning the valuation result and its subsequent correction. Another solution is to order an alternative valuation from another expert, which may also become the subject of further questioning.

The option to undermine the result of the valuation raises the need for difficult, questionable, and ambiguous valuations to be carried out by experienced valuers capable of defending their arguments. Here, the role of valuer is extended—they are not only the author of the valuation but also the advocate of their own work. Such valuations may encourage pressure to be exerted on the client–valuer cooperation.

4.4. Lack of Transparent Market Data

Unethical behavior in the area of property valuation is facilitated by lack of transparent market data, especially information concerning real estate transaction prices. These data are not publicly available, either to market participants or transaction parties. The unavailability of data results in difficulties in assessing the potential of a property and, consequently, in mismatching the level of property prices with their actual market value. Ultimately, the transaction price registers dedicated to property valuers for valuation purposes contain highly distorted data. In addition, the property descriptions in these registers are incomplete. Unfortunately, the inconsistency and diversity of market data can be a source of difficulty in delivering proper valuation results, but it may also facilitate the interpretation of the valuation outcome suggested by the client. As a consequence, it may encourage unethical valuers to manipulate valuation results.

4.5. Valuers’ Specialisation

Another issue worth highlighting in this article is the lack of valuers’ professional specialization. First of all, the educational path open to valuers and its requirements are the same for all candidates, regardless of their individual interests. Specialization is shaped informally alongside experience. As a result, the valuer becomes an expert in a chosen field only by acquiring special skills over time.

The choice of professional specialization may be related to the profile of the education obtained. According to our research, among Polish valuers the most common educational backgrounds are economic, technical, and legal [

61], which can direct expertise in specific areas such as investment property valuation, building replacement costs, or public purpose valuations. Of course, the choice of specialization may also result from the types of properties most frequently valued or the type of customers mainly served. In the context of pressure felt by valuers, gaining experience and professional specialization seems to be an important issue.

4.6. Diversity of Valuation

It should be mentioned that biased valuations might also be affected by three additional elements: the object of the valuation, the objective of the valuation, and the type of customer being served. In Poland, property valuers value all kinds of properties on behalf of private and public entities. Estimating the value of real estate serves different purposes. In some cases it is required by law, in others it depends on the will and needs of the ordering party. Property valuers provide valuation services for banks and financial institutions for the purposes of estimating the value of collateral for credit receivables, for courts in matrimonial and business cases and resolving property disputes, for public authorities selling public property, calculating local fees and estimating compensations for expropriation of property, and finally for investors and individuals in supporting market transactions, credit decisions, and investment activities. The clients’ investment or business intentions towards the property may lead to a more or less suggestive indication of the expected value.

Summarizing the above considerations, it is worth noting that the existing valuation conditions in Poland (i.e., weaker preparation of candidates for the profession, growing competition, the ease of questioning valuation results, non-transparent market data, lack of formal valuers’ specialization, and the diversity of services) may favor the subjectivity of performed valuations. Unreliable valuations contradict the idea of fair market value and the expert valuation of the property itself. The transparency and reliability of the valuation process may contribute to the increased efficiency of the real estate market and enhance its sustainable development. By providing reliable information on the value of real estate, property valuers strengthen the investment decision process not only in an economic context but also in an ethical one. This article attempts to assess the extent of valuers’ perception of customer pressure depending on selected criteria.

6. Discussion of the Results

The estimation results of the LPM and logit models are presented in

Table 4. Firstly, we started the estimation with only three variables concerning the sex, age, and work experience of a valuer. Then, we extended the basic model (LPM1 and Logit1) with sets of independent variables describing the respondents’ education, their company, as well as their profile of valuation activity (models 2 to 4). In the context of the regressors that were at the center of our attention, the age variable proved to be relevant in almost all models, while a variable explaining work experience was relevant only in models LPM4 and Logit4. In particular, estimates of LPM models indicated that each additional year of a valuer’s experience reduced the probability of pressure occurring by 0.12, 0.11, 0.10, and 0.05, depending on the specific form of the LPM model. It should be noted that the logit models gave very similar results for the age variable. In particular, the marginal effect for this variable in the Logit4 model was equal to −0.09, which means that an increase in age by one unit caused a decrease in the probability of pressure occurring by 9%. When analyzing the work experience variable, one can conclude that each additional year of performing valuations led to a decrease in the probability of pressure occurring by 0.01 both in the LPM4 and Logit4 models.

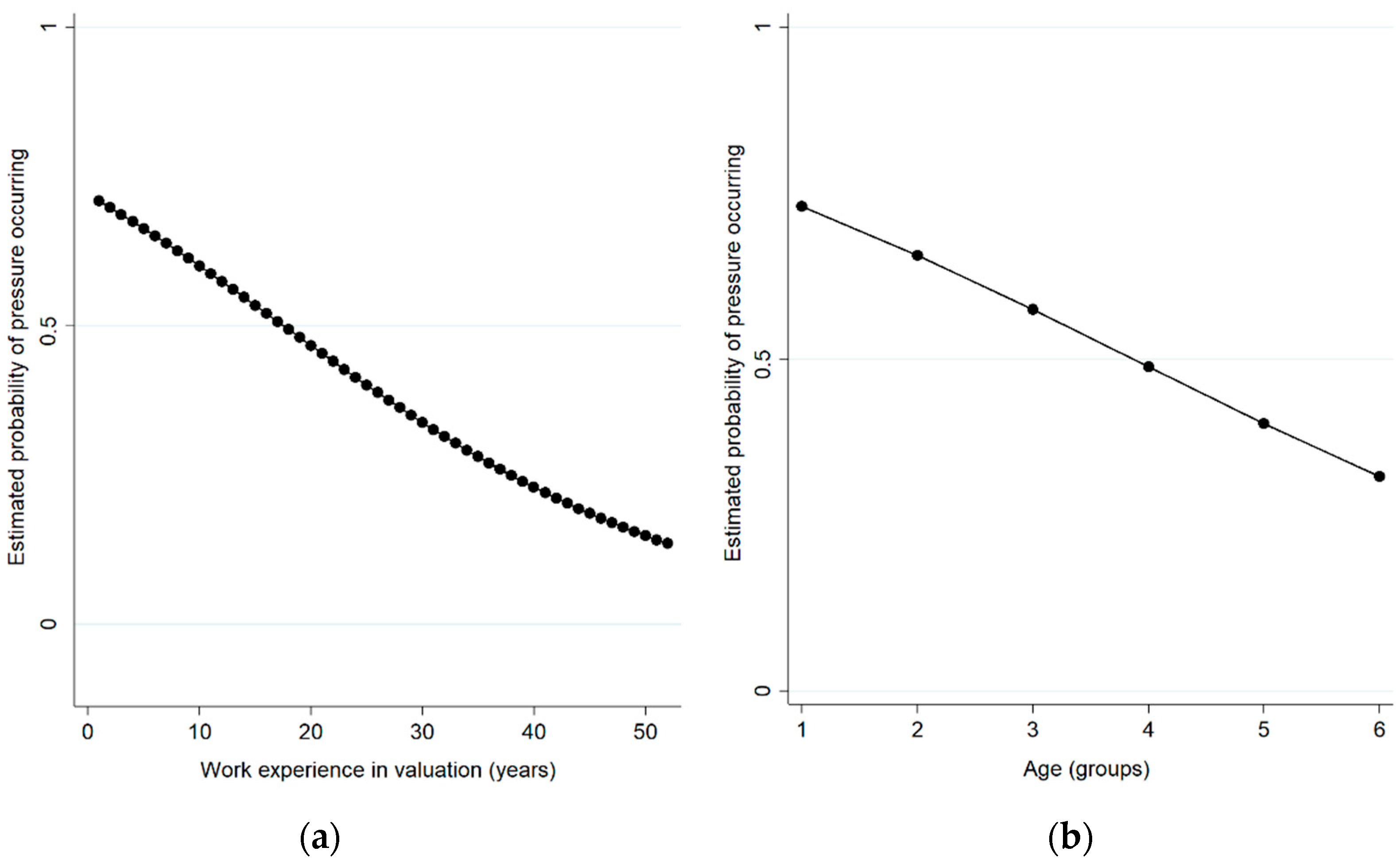

Moreover, on the basis of the Logit4 estimates, we calculated the estimated probabilities of pressure occurring for both the age and work experience variables while taking into account the means of other independent variables. The results of this analysis are presented in

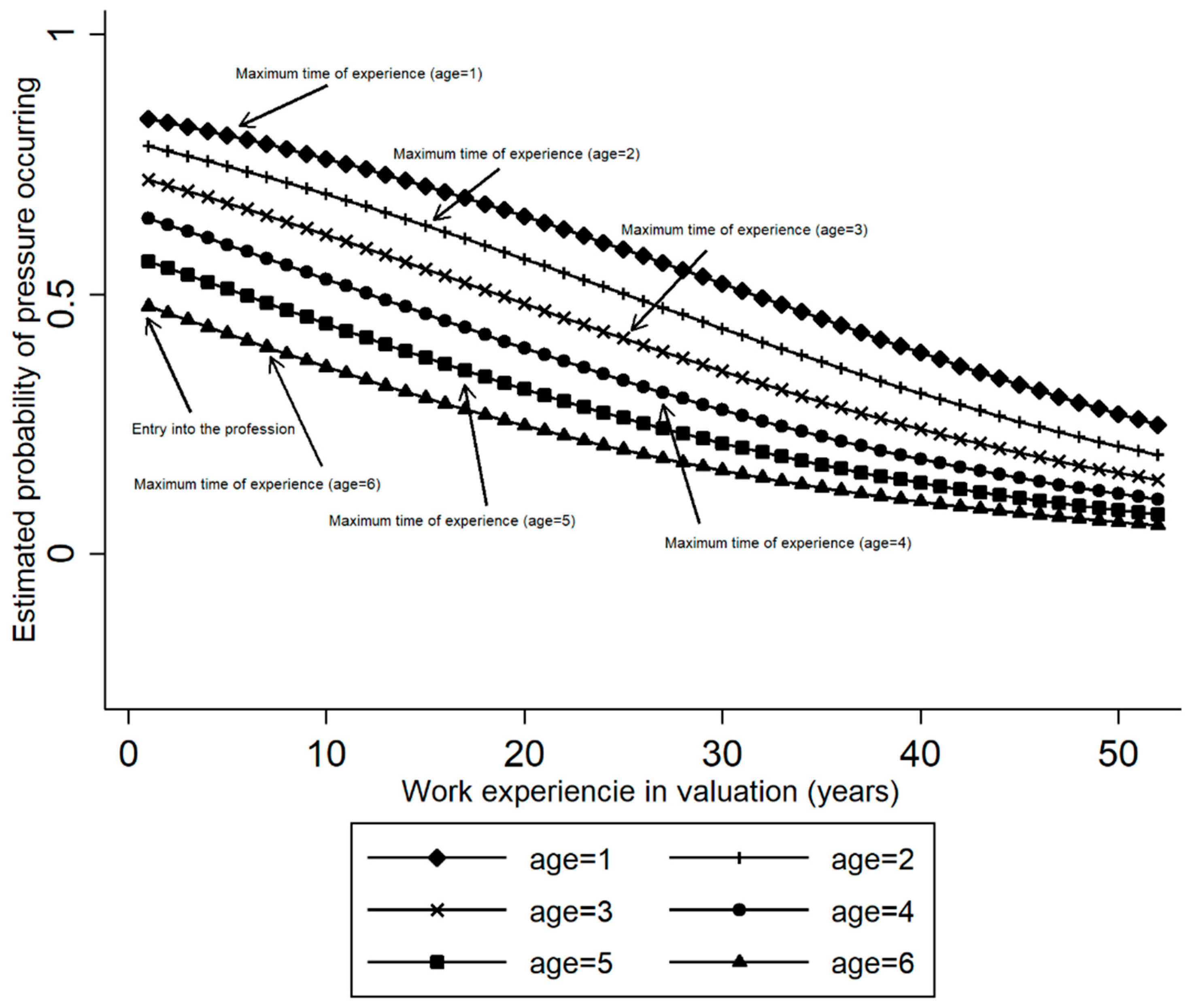

Figure 1a,b. It should be stressed that the possibility of pressure occurring for both young or inexperienced valuers was very high and equal to about 0.75. On the contrary, the same possibility for the oldest and most experienced valuers was significantly lower, well below 0.5. Furthermore, it is of interest to see how this probability changed for the work experience variable when grouped by age (see

Figure 2). Taking into consideration these two variables together, it should be noted that the probability of pressure occurring varied across age groups. People who entered into the profession at different ages had a varied tendency to feel pressure. In particular, for the youngest, the occurrence of pressure was almost certain. For the oldest, however, this was about 0.5. Nonetheless, the lines in

Figure 2 converge. In this respect, it can be said that, over time, age became less important in relation to work experience. This interpretation, however, cannot be considered certain because the maximum duration of work experience can be identified for the analyzed age groups. This mainly is due to the fact that in Poland the minimum age at which one can obtain professional qualifications for real estate valuation is 24.

It should be noted that our findings are consistent with other empirical studies [

44,

62] concerning the impact of age and experience on pressure occurring in real estate valuations. The feeling of increased pressure by young or inexperienced valuers in the process of a property’s valuation is not surprising and is due to several reasons. First of all, it should be noted that such valuers may simply be overwhelmed by clients because of their lack of experience in valuation or certain areas of it [

63]. In addition, these valuers may not have reliable data to conduct the valuation process, which is a result of their limited experience. As noted by Bellman [

11] and Achu [

63], the lack of reliable data increases the risk of client influence on the work of the valuer. This influence may include, but is not limited to, pressure from the client to estimate an indicated value and also pressure to use information provided by the client themselves. The latter is extremely important for inexperienced property valuers who may not have the practical knowledge to acquire or process the necessary information to perform a property valuation. Therefore, these valuers may be willing to accept information provided by clients. It should be noted that this information may concern both the property object and the property market [

11]. Unfortunately, such information may be uncertain, which increases the probability of errors in the valuation process.

When discussing the results of studies on the influence of age and experience on the occurrence of pressure among property valuers, we should also pay attention to another very important aspect: that increased pressure on young valuers, entering the profession at around 24 years of age, is also the result of the fact that they did not have the opportunity to work with similar clients beforehand as agents or real estate managers.

Another factor explaining the presence of strong pressure among young and inexperienced valuers is the fact that clients expect quick delivery of the ordered valuations [

64,

65]. This pressure may be compounded by the lack of knowledge of inexperienced valuers about complex valuations, where the number of parameters used in the valuation model multiplies [

66].

It should be noted that the problem of pressure in the valuation process among young valuers is extremely important and worthy of further research, as according to Murphy [

65] pressure is one of the main factors blocking the inflow of young people into the valuation profession.

In the LPM and logit models, other factors also significantly affected the dependent variable. In particular, the valuer’s type of education should be emphasized here. The model estimates indicated that valuers with a legal degree perceived much weaker pressure during the valuation process than others. In particular, a legal degree was characterized by a decrease in the possibility of pressure occurring by about 0.50. Such a result is not surprising in the context of the specificity of the profession in Poland, where property valuers are forced to prove the correctness of their arguments and often to defend their work in courts, commissions, and professional associations.

In addition, in recent years, an increasing number of valuers have chosen economics as an educational background. The explanation for the less pressure experienced among property valuers with a legal degree may also result from the fact that, in Poland, this field of study is considered to be much more prestigious than, for example, economics. Moreover, until recently, legal studies in Poland were conducted by only a few of the top universities. It seems, therefore, that a legal degree gives the valuer greater self-confidence, which increases resistance to client pressure. Similar conclusions were reached by Bellman, Lind, and Öhman [

67], who argued that valuers in Sweden who have graduated from prestigious universities have a high level of self-confidence and belief in what they are doing.

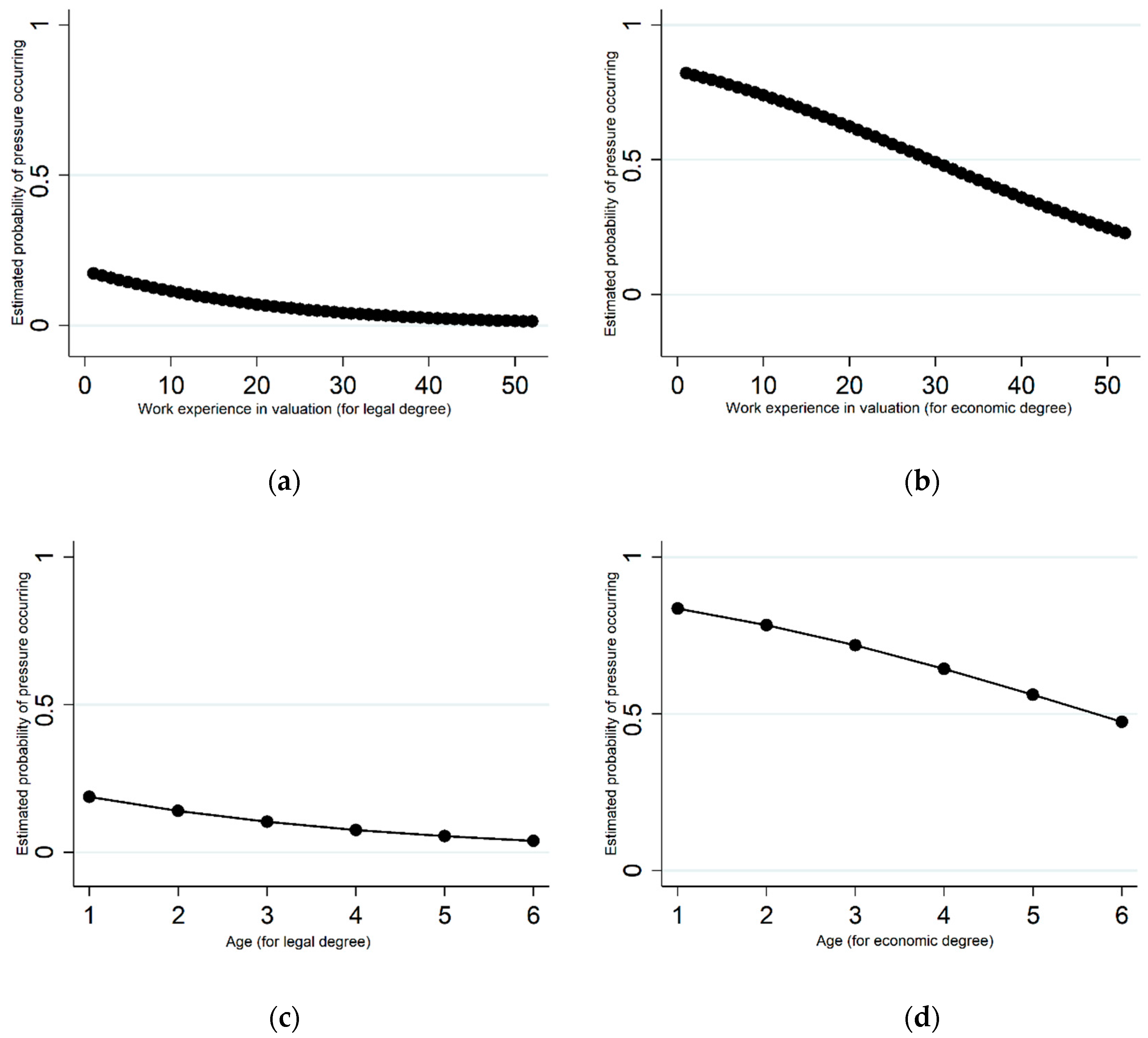

Moreover, it is very interesting to compare the probabilities of pressure occurring for the age and work experience variables, while taking into account differentiation in educational background. Based on the results presented in

Figure 3a–d, one can conclude that for property valuers with legal education, pressure was very unlikely to occur. This applied across age groups and years of work experience. On the contrary, valuers with economic degrees were very likely to experience pressure. These values decreased significantly over time, but even after 50 years of professional experience, the probability of pressure was higher when compared to property valuers entering the profession with a legal education. On this basis, we would like to stress that legal education should play a much greater role in the preparation of future valuers in Poland. Moreover, according to our knowledge, this is the first empirical study that takes into account the impact of the type of education of the valuer on the pressure experienced during the valuation process. Therefore, this topic should be subject to further research, as confirmed by Page [

68], who states that analyses on the impact of the education of property valuers on their appraisals are rare.

In our models, there are also four additional variables that had a significant impact on pressure occurring. The first is gender. In particular, the probability of pressure occurring is much higher for men. This finding is consistent with the study conducted by Kucharska-Stasiak, Źróbek, and Cellmer [

45], and it may result from the fact that women can be, as mentioned earlier, more ethical in some situations. This fact was partially confirmed by research conducted by Agboola, Ojo, and Amidu [

69] on a sample of real estate agents in Nigeria. In particular, it was found that women had a significantly lower level of fraud acceptance than men. Conversely, other empirical studies on valuers did not identify significant differences between the ethical values of women and men [

20,

70]. Therefore, further research on the ethical standards in the real estate professions should be conducted.

The next variable that affected the dependent variable is the territorial coverage of the valuers’ professional activity. Estimation results indicated that the higher the value of this variable, the higher the probability of pressure occurring. A similar interpretation has been adopted in [

47] in studying the use of heuristics by property valuers. Their research showed that knowledge of the area in which a property is located affected the outcome of adoption of an anchoring and adjustment strategy. Heurestic behavior was shown to be associated with high levels of variance, where valuers had low domain-specific knowledge [

47].

The last two relevant variables related to the specificity of the performed valuations. Especially in this context, the strongest impact came from individuals, which significantly increased the probability that valuers felt pressured. This finding is consistent with the studies conducted by Shi-Ming [

42], Amidu and Aluko [

38], as well as Źróbek, Kucharska-Stasiak, and Cellmer [

71], and it results from a couple of premises.

First of all, in Poland, valuations are very often ordered privately by individuals in lending cases. In such situations, clients have clear incentives to exert pressure on the valuer [

5] because the estimated value of the property affects, through the loan-to-value (LTV) ratio, the amount of the loan granted and its costs to the borrower. Second, high pressure on valuers from private individuals may result from valuations they order in administrative and judicial matters. In this respect, the valuation is intended to counterbalance the value of the property estimated by the authorities or courts. As a result, clients may put a lot of pressure on valuers to determine the value they want under the threat of not ordering a valuation.

7. Conclusions

The standardization of valuation services should guarantee the objectivity of the valuation process and confirm that the obtained valuation result is an undistorted image of the real estate value. The objectivity of valuation should be desirable in the process of determining real value. This could be ensured during the valuation process when the client has no expectations towards the property value and the valuer has no temptation to distort the valuation result. In business reality, such a situation practically never occurs, as the party ordering the valuation usually has clearly defined needs. The client may inform the valuer about these needs, exerting more or less noticeable pressure on them. In this situation, the key problem is to identify the main factors reducing or increasing the resistance of valuers to pressure and to consider institutional support for their independence.

The main goal of our research was to determine which of the factors characterizing the valuer and their professional activity were conducive to feeling pressured from the client.

We found that among the characteristics of a property valuer and the scope of their work, the most influential to feeling pressured were: gender, age, work experience, education, spatial area of services provided, and the type of clients served. In particular, research results showed that women were less susceptible to pressure, and the probability of feeling pressure decreased with age and length of professional life. Legal education reduced the chance of pressure being felt, while the greater the spatial range of work, the higher the risk of pressure being perceived. Working with individuals and developers also increased the possibility of experiencing pressure. Thus, the results of the research allowed us to answer all of the research questions.

Taking into account the results of our research and the existing institutional weaknesses in property valuation in Poland, we have attempted to indicate the main areas requiring special attention and further research.

Firstly, we point out that the current system of educating property valuers is not sufficient, resulting in the poor preparation of candidates. In light of the conducted research, the educational process should be enriched with legal elements, both theoretical and practical, giving experts procedural knowledge of evaluating and questioning the correctness of valuations as well as the ability to defend them. The training program should also be extended to psychological elements, which are necessary for negotiating contract terms, curbing assertive attitudes, as well as dealing with stressful situations. Knowledge in those areas could be helpful in building a responsible and independent professional attitude.

Secondly, young property valuers entering the profession are not specialized. They usually offer a wide range of valuations on a basic level. Informal specializations are acquired over time through customer service in a selected market segment. It would be worth considering the introduction of a specialization path for candidates, directing their professional career towards selected types of valuation (e.g., residential, commercial, agricultural) or valuations for specific purposes. Although such direction would narrow down the scope of performed orders, it would better prepare young experts better for and improve the quality of the services provided. An alternative solution worth considering is the possibility of obtaining formal specializations in the course of one’s professional career through a certified training system.

Finally, the valuers need the support of a professional organization providing direct legal and methodological advice. The professional chamber could also provide indirect support by supervising the cooperation of market institutions with valuers and by raising public awareness of the importance of reliable and independent valuations.

The above suggestions will not eliminate the problem of pressure or guarantee the full resistance of valuers. Ultimately, resistance to exerted pressure is a very personal matter, resulting from individual attributes, assertiveness, and the ability to cope with stressful situations among others. Regardless of substantive knowledge and institutional support, the problem of pressure is an accompanying element of the profession. It is important for market participants to be aware of the possibility of biased valuations in their business activities and for policy makers to consider these issues when penning professional regulations.

{kind=link}

{kind=link}

{kind=link}