Stakeholder groups are demanding higher CWD. Over the last decade, investors and investment institutions have shown a higher willingness to invest more in firms dedicated to water disclosure [

6,

8,

26]. This is because water disclosure has been recognized as a tool that assures that the company’s profit is not created at the expense of the environment [

27]. Besides, the Minerals Council of Australia [

20] has adopted water disclosure as a means to convey a signal of being water and environmentally friendly to stakeholders. The Coca-Cola company uses water labeling to manifest their care for water resources and the fundamental right to drinking water for all [

28]. These behaviors are associated with corporate legitimacy. If water stewardship engages stakeholder groups’ attention, firms can use water disclosure to convey to the public that they are using water resources in a reasonable manner that safeguards people’s right to water [

19]. Therefore, we believe that for analysis of drivers of CWD, legitimacy theory and stakeholder theory can offer valuable insights. In the following paragraphs, we will introduce these two theories respectively.

2.1. Legitimacy

Legitimacy is one of the most influential concepts in the research of corporate environmental reporting [

29]. For corporations, showing care for the environment is a cornerstone of legitimacy [

30,

31]. Hence, they manage to use education and data to influence social perceptions or describe their performances to shape corporate symbols and boost firm performance [

32]. In any of the above behaviors, their goal is to convey a legitimacy image through engagement in environmental protection or compliance with regulations to ultimately minimize the legitimacy gap between actual performance and social expectation of the firm [

32]. According to organization theory, legitimacy is pivotal to the long-term survival of an organization, and it is fundamentally determined by society.

Therefore, legitimacy theory suggests that organizations continually seek to ensure that they operate within the bounds and norms of their respective societies [

33]. To this end, they will endeavor to make their business activities consistent with accepted behavioral norms in larger social systems [

34]. Simply put, it is necessary for organizations to establish legitimacy within the bounds and the norms that are widely accepted in society [

32]. Recent studies [

18] have pointed out that environmental protection is an effective legitimation strategy. Corporations will use legitimacy as a signal or symbolic actions to communicate a “public image” [

34] and then align their primary goals with the image to avoid causing social or environmental problems [

35]. Environmental problems arising from climate change have posed a threat to corporate legitimacy (e.g., stakeholder groups are paying greater attention to corporate responsibility for the environment and water resources [

18], and businesses may employ legitimation strategies [

36] to achieve the primary goals, methods or outcomes of their operations). In fact, legitimacy has been recognized as a vital resource for organizations [

34]. Therefore, businesses will use environmental protection initiatives or policies to solicit social support and enhance their legitimacy [

18]. Legitimacy can also lead to a higher reputation, higher profitability, more balanced policy development, and lower risks [

37]. In a nutshell, legitimacy is an organization-society relationship that brings social support for the organization. It is also one of the incentives for businesses to disclose environmental information to stakeholders.

2.2. Stakeholder Theory

Stakeholder theory explains the relationship between stakeholders and the information they receive [

38]. When communicating water stewardship practices with stakeholders, firms’ disclosure of water-related information plays an important role. Gray et al. (1995) [

39] stated that disclosure of information to stakeholders is likely to be viewed as a kind of corporate contribution to society. Stakeholders usually use water-related information disclosed by a firm as one of the measures of a firm’s reliability and legitimacy.

Regarding corporate disclosure, two views of stakeholder theory have been developed, one is normative or ethical [

40], and the other is managerial [

41,

42]. Both views stress the importance of sufficient disclosure of internal information to stakeholders. The major difference between the two views lies in the focus of the disclosure content. The normative or ethical view suggests that equality should be considered in the disclosure of any information [

40]. The managerial view argues that stakeholders’ responsibility is to ensure that the disclosure content is relevant to decisions [

42]. To be more specific, the normative or ethical view suggests that businesses should endeavor to disclose detailed information on water stewardship to all stakeholder groups, while the managerial view suggests that disclosing water-related information that supports stakeholders’ investment decisions is well enough. There is a certain degree of difficulty for a company to provide detailed information on water stewardship [

13], and the cost-effectiveness of the disclosure should be usually considered. Firms may prefer to take the managerial view of stakeholder theory when dealing with the disclosure. Through disclosure of water stewardship information, they can communicate with stakeholders and develop a better relationship with them [

43]. Firms’ favor for the managerial view is also documented in previous research [

44,

45,

46,

47,

48].

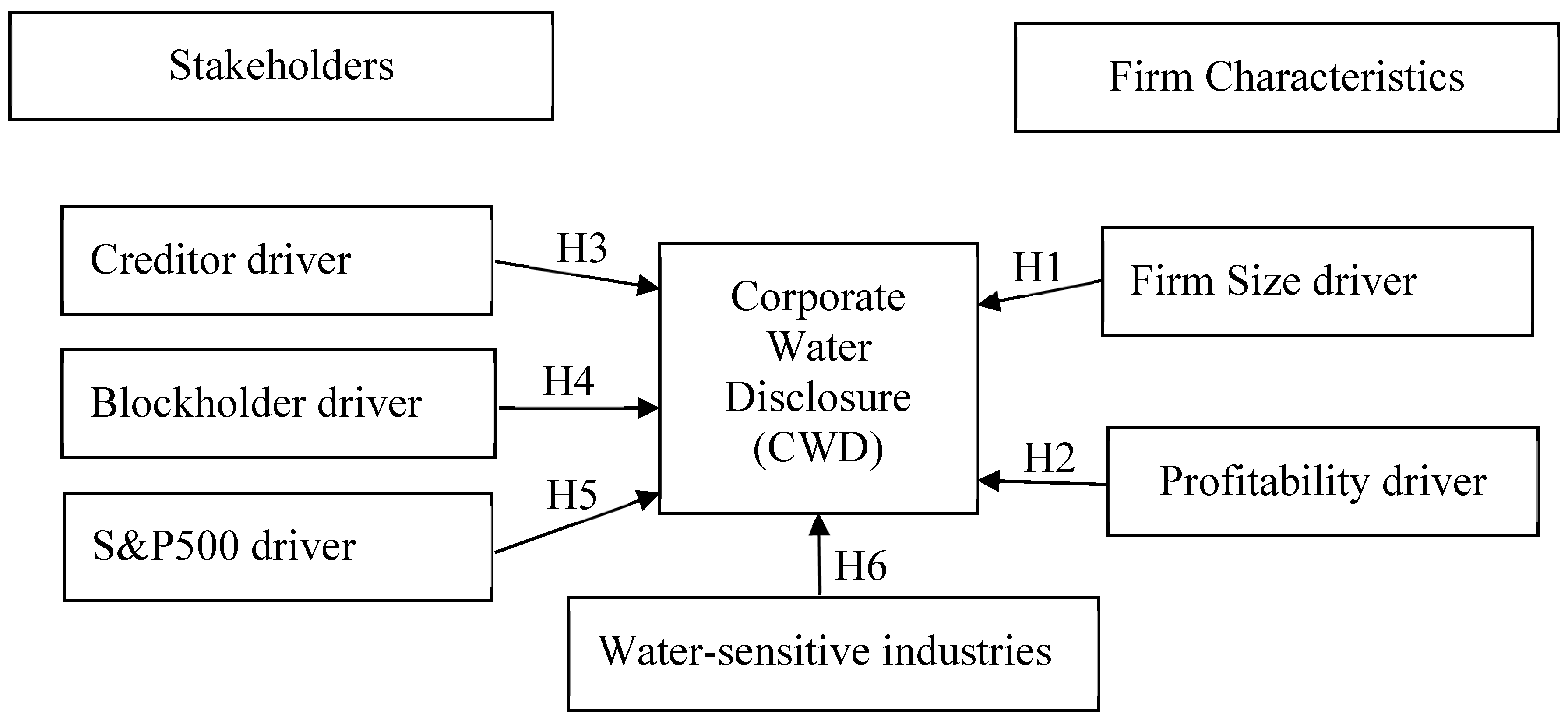

In addition, literature [

49,

50] has mentioned that pressure for water-related disclosure is related to a series of firm characteristics. In this paper, we will adopt the managerial view of stakeholder theory to discuss drivers of CWD, which include financial drivers (e.g., firm size, profitability), creditor driver (e.g., debt ratio), blockholder driver (e.g., degree of ownership concentration), market viability driver (e.g., inclusion in S&P500), and industry characteristic driver (e.g., water sensitivity). Our hypotheses will be developed based on these drivers as

Figure 1.

Financial drivers: In this paper, we evaluate only the effects of firm size, profitability, and debt ratio. Larger firms invite public attention more easily, and their operations generally involve the interests of a wider range of stakeholder groups [

51]. Larger firms are also more likely to become the subject of tight scrutiny by the government or special stakeholders (e.g., consumers with hostility or radical employees) [

27]. Therefore, larger firms are usually more willing to disclose water-related information to reduce negative attention [

22], maintain their legitimacy [

18], and also prevent consumers’ boycott of their products. This argument has been supported in many empirical studies. For instance, the empirical evidence in Huang and Kung (2010) [

52], Kuo and Yu (2017) [

53], and Marquis and Qian (2014) [

54] have confirmed that firm size is positively related to environmental reporting. Therefore, we propose the following hypothesis:

Hypothesis 1. Larger firms release more information on CWD.

Logsdon (1985) [

55] found that environmental policy is sensitive to profitability. This is because profitability provides firms with abundant resources and the agility needed for coping with stakeholder concerns [

23,

56]. Firms are also under pressure from stakeholder expectations. They need to ensure that their activities comply with social norms and regulations [

49,

57]. The correlation between profitability and environmental disclosure has been confirmed in empirical research of stakeholder theory. However, some studies [

22,

53] have offered a different insight which suggests that profitability is not related to environmental disclosure. To test whether profitability is also a driver of CWD, we propose the following hypothesis:

Hypothesis 2. Firms with a higher profitability release more information on CWD.

Creditor driver: Creditors are the provider of corporate loans. For corporations, creditors are important and powerful stakeholders, because they (creditors) are capable of influencing corporate disclosure actions [

23]. Previous research [

22] has found that when firms have a low degree of leverage, their creditor stakeholders will exert less pressure to constrain the manager’s discretion over disclosure. In other words, the disclosure level is negatively related to leverage. However, Roberts (1992) [

24] argued that when firms have a higher degree of leverage, they are expected to have more responses to issues concerned by stakeholders (e.g., environmental and social issues). A recent water stewardship report [

6] shows that water shortage will cause a tremendous loss of firms. Hence, we propose the following hypothesis:

Hypothesis 3. Firms with a higher leverage ratio release more information on CWD.

Blockholder driver: Blockholders are likely to have an impact on corporate disclosure policy. As suggested in previous research [

24,

58], both the concentration of ownership and dispersion of ownership affect corporate disclosure policy. The evidence in Reverte (2009) [

27] suggests that ownership is positively related to corporate social responsibility (CSR) disclosure score. However, there is also evidence suggesting that shareholders of firms with a more dispersed ownership structure pay more attention to environmental management and will also impose greater pressure on voluntary disclosure policies [

59], especially disclosure of environmental stewardship information [

58]. We argue that when blockholders have a higher ownership ratio, they will be more concerned about the firm’s legitimacy issues (e.g., water risks management) because these issues affect the firm’s image and reputation. Blockholders’ heightened concerns about these issues will relatively increase the pressure of water disclosure on managers. Therefore, we propose the following hypothesis to examine whether blockholders’ ownership ratio is also a driver of CWD.

Hypothesis 4. Firms with a higher blockholders’ ratio release more information on CWD.

High market visibility: Since 2009, CWD has been a concern for investment institutions [

6]. This is because the stakeholder group believes that through disclosure of water-related information, corporations also make their water risks and coping mechanisms more transparent [

60]. Besides, water disclosure assures stakeholders that the company’s profit has not been created at the expense of the environment [

27]. To be more specific, investment institutions are also changing their attitude to place a greater emphasis on sustainability [

60]. This is why more and more investment institutions consider water disclosure in the making of investment decisions [

2]. For instance, S&P500 is a market value-weighted index. Firms listed in S&P500 are relatively larger in size and playing a more important role in the stock market. The criteria for S&P500 inclusion are high. Hence, S&P500 is said to be representative of the stock market and even the US economy. Firms included in S&P500 have higher market visibility (exposure) and can more easily win the trust of market investors (institutional investors). In order to meet stakeholder expectations and legitimacy requirements, managers of these firms may volunteer to accept CDP’s evaluations in pursuit of higher environmental performances, such as water disclosure rating, which is an important reference for green investors. Therefore, we use S&P500 inclusion as a proxy variable for high market visibility. As hypothesized below, whether the inclusion in a capital market index is positively related to water disclosure is tested.

Hypothesis 5. Firms included in a famous index of capital market release more information on CWD.

Industry characteristics: Water-sensitive industries draw heightened attention from stakeholders [

57] because their operations are susceptible to close attention and scrutiny by the government, environmental groups, and the public [

18,

49]. The attention or pressure from stakeholders influences the environmental disclosure of firms in these industries. For example, Morrison et al. (2010) [

16] and Sarni (2013) [

9] pointed out that environmental disclosure is related to specific industry characteristics. Kuo and Yu (2017) [

53] found that environmentally sensitive industries are significantly associated with higher environmental disclosure levels. To be more specific, environmentally sensitive industries are expected by stakeholders to meet higher environmental disclosure and water disclosure requirements compared to non-environmentally sensitive industries [

49]. This also explains why the environmental disclosure policy of firms in environmentally sensitive industries is subject to the influences of stakeholders. To examine whether this industry characteristic is a driver of water disclosure, we propose the following hypothesis:

Hypothesis 6. Firms belonging to a water-sensitive industry release more information on CWD.

{kind=link}