1. Introduction

Since the eruption of the global economic crisis in 2008, global economic integration and the link between financial markets around the world have been reinforced. Economic policy, as a measure taken by governments to avoid economic collapse or overheated expansion, has maintained the stability of financial markets to a certain extent. However, frequent government intervention in the economy also brings about economic policy uncertainty (EPU) [

1]. The so-called EPU refers to the fact that economic entities cannot accurately predict changes in current government economic policies [

2]. Uncertainty in economic policy makes it more difficult for investors and enterprises to anticipate the future investment environment and decreases the public confidence index, leading to a negative impact on economic growth [

3]. Many studies have shown that EPU will affect the real economy, including gross domestic product (GDP), consumption, investment, and exports, as well as price variables, such as real estate price, exchange rate, and crude oil price [

4,

5,

6,

7,

8].

Crude oil, known as “industrial blood” and “black gold,” is an underlying energy product and an important industrial raw material in contemporary society [

9,

10,

11]. It plays an important role in the economic, political, and military fields, and various factors affect its prices. On a global scale, the international crude oil market benchmark price has been formed on WTI, Brent and Dubai crude oil futures markets. At the same time, the financial attributes of international crude oil assets continue to increase. The price of crude oil has become the result of a combination of supply and demand factors, macroeconomic factors, political factors, and financial factors. Especially since 2003, the crude oil price has fluctuated more frequently and violently. It had experienced sharp increases and drops before and after the 2008 financial crisis, and in 2014, it fell rapidly to the lowest price in the past decade and showed a trend of low prices [

9,

12]. Some researchers have pointed out that oil price shocks may trigger a US economic recession, and the link between oil price instabilities and macroeconomics has stimulated many studies, such as those looking at gross domestic product, inflation, and stock markets [

12,

13,

14,

15,

16,

17]. Fluctuations in oil prices could be one of the highly critical drivers of EPU and economic outcomes [

18]. Additionally, the effect of rising oil prices on a country’s macroeconomic conditions is greater than a decline. This disproportionate effect of oil prices has attracted researchers’ attention [

19,

20,

21]. Furthermore, previous studies probed the short-term and long-term irregular impacts of oil price shocks and found that only the cumulative demand effects might have a similar influence either in the short-term or long-term [

10,

20,

21]. Therefore, these studies of the asymmetric influence of crude oil price under the framework of the EPU index (see

supplementary) have also attracted our attention.

For our part, studies have not identified a volatility spillover effect on the association among EPU and prices of WTI crude oil in the context of downturns of the US economy. Therefore, our contribution is complementary to this study. A time-varying spillover effect was recorded by previous scholars between EPU and oil price downturns. For example, EPU does affect predictions in changes in oil prices [

22]. The evidence provided by Aloui et al. [

23] shows that EPU affects oil price returns in a certain period, and has a high impact on macro and micro levels. Moreover, the negative impact of EPU on oil revenues, which could be augmented by endogenous EPU responses, is also described in the literature [

24,

25]. The study by Antonakis and House [

26] investigated the association between volatility and the EPU index and noted that there is a negative association between the impact of total demand on oil prices with an American economic downturn. At the same time, the relationship between EPU and the macro-economy needs to be considered [

27]. Given the link between EPU and oil prices, the absence of measuring the volatility spillover effect will lead to endogenous issues that should be addressed in this study.

Furthermore, previous studies that mostly used “Markov switching” models and time-varying parameters VAR discovered that the uncertainty link between economic policies and oil prices is time-varying and nonlinear [

28,

29]. In addition, the study by Hailemariam et al. [

30] applied a non-parametric panel data model to investigate the influence of EPU on oil price adjustments. However, the relationship between oil prices and EPU has become complicated, and the use of the parameter VAR alone has proved insufficient to capture this unstable relationship. The multivariate “generalized autoregressive conditional heteroscedasticity” (GARCH) model can be applied to assess the volatility at distinct time scales [

31]. Therefore, this paper integrates the VAR model and the multivariate BEKK-GARCH model to depict the mean and volatility spillover effect between EPU and WTI crude oil price. After Bollerslev proposed the GARCH model in 1986 [

32], many GARCH models were derived, such as the TGARCH, EGARCH, and multivariate GARCH model.

In particular, the multivariate GARCH model was improved and expanded by many scholars based on the original model, for wide application in the research of oil price, stocks, exchange rates, etc. The multivariate GARCH model has been referred to using several different expressions across different types of studies, such as VECH-GARCH, BEKK-GARCH, CCC-GARCH, and DCC-GARCH [

33,

34].

Table 1 compares the characteristics of different GARCH models. However, compared with the others, the BEKK-GARCH model is more suitable for our research and easier to operate because it can not only guarantee that the covariance matrix is a positive definite matrix with easier estimation of the parameters, but can also measure the correlation and reflect the direction of spillover effects [

6,

35]. Therefore, we employed BEKK-GARCH, which meets the aims of this study to inspect the effect of volatility spillover between the relationship of US EPU and WTI crude oil price. This paper also analyses the Granger causality and the dynamic association between EPU and crude oil prices in order to explore the factors that affect EPU. From the correlation, we observed that the periods when the crude oil price rises and falls are also the periods when the economic policy is frequently issued. This is so that people are able to explore reference indicators and gain more effective information before the government promulgates economic policies. The public can also benefit from these resources, which allow them to have reasonable expectations. Meanwhile, the outcomes of our study can inspire investors to comprehend the effect of mean and volatility spillover between US EPU and WTI crude oil price, thereby optimizing asset allocation, and mitigating their losses. It can predict EPU for US decision-making departments based on market price trends, and then take preventive measures for economic sustainability. At the same time, the relevant departments in the US also need to adjust the energy structure to mitigate the negative effect of WTI oil price changes on.

The rest of the article is arranged as follows.

Section 2 sets out the methodology, while

Section 3 explains the empirical results and discussion. The conclusion, implications, and future research directions are provided in

Section 4.

2. Materials and Methods

It is possible to use “multi-criteria decision-making” [

43] and “time series analysis” [

23] to measure the correlations between different indicators. To identify the mean and volatility spillover effect between US EPU and the WTI crude oil price, we used the VAR-BEKK-GARCH model. The research framework is displayed in

Figure 1. First, we verified the causal relationship between EPU and the WTI oil price through the ADF stationarity test and the Granger causality test. Then, on this basis, we combined the VAR model and the BEKK-GARCH model to assess whether the transmission of information causes the price fluctuations to pass to the crude oil market when EPU fluctuates, as well as whether the shock to crude oil price will cause a fluctuation of the EPU. By integrating the results of the two models, the dynamic correlation between US EPU and the WTI oil price can be comprehensively understood, which can assist the stakeholders’ decisions in regard to risk management.

2.1. The VAR Model

In 1980, Sims introduced the VAR model to economics, which promoted the wide application of dynamic analysis of economic systems [

44]. The VAR model is often used to predict an interconnected time series and analyze the dynamic disturbance of random error terms on variables, thereby explaining the impact of various economic shocks on the economic variables. The model uses each endogenous variable as the lag value of all endogenous variables to establish functions, in order to capture the linear interdependence between multiple time series and analyze the joint changes between the internal variables.

This paper considers the two variables of the VAR model of order

p, defined as follows:

where

is a

vector of endogenous variables, Φ is the

matrix of autoregressive coefficients, C is a

intercept vector of the constant terms, and

is the

vector of uncorrelated structural disturbance.

When choosing the lag order p, a sufficiently large lag order is chosen to fully reflect the dynamic characteristics of the system. However, too large of a lag order will decrease the freedom of the model. Therefore, AIC, SC, LR, FPE and HQ criteria are normally used to determine the maximum lag order.

2.2. The BEKK-GARCH Model

The mean equation based on the VAR model is as follows:

where

denotes the change rates of Variable1 and Variable2, respectively. We assume that

satisfies the mean function, and

denotes corresponding error terms.

The variance equation satisfies the following formula:

represents the variance–covariance matrix at

t time,

C denotes the constant matrix of the upper triangle, and

A and

B denote the coefficient matrix corresponding to the ARCH and GARCH terms, respectively. Specifically, the BEKK model is described as:

The logarithmic likelihood function of the BEKK-GARCH model is:

When , the volatility of Variable2 is only affected by its own pre-volatility and residual, indicating that Variable1 has no volatility spillover effect on Variable2. When , Variable1 is only affected by its own pre-volatility and residual, and Variable2 has no volatility spillover effect on Variable1. When , there is no volatility spillover effect between Variable1 and Variable2.

4. Conclusions, Implication and Future Directions

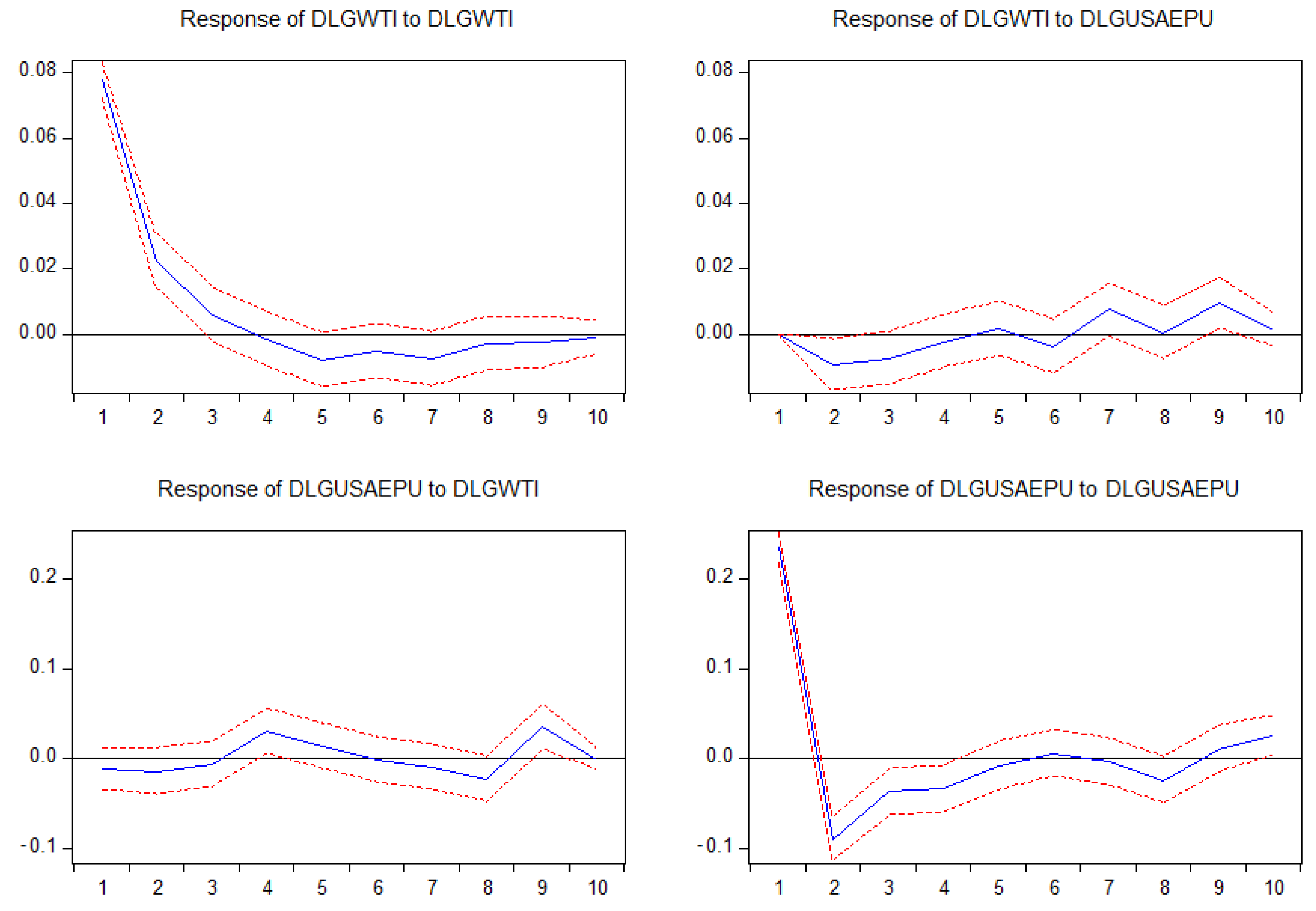

This paper extends the existing approaches in the literature by empirically examining the mean and volatility spillover effects on the association of US EPU and WTI spot crude oil price. Firstly, through the Granger causality test, the empirical outcomes showed that the change of uncertainty in economic policy in the US is the Granger cause of the WTI oil price, while the latter does not Granger cause the former. The VAR model illustrated that there is a mean spillover effect between WTI oil price and US EPU, that is, they will both be affected by past fluctuations. In addition, we found that this correlation has positive and negative directions. The BEKK-GARCH model test yielded similar conclusions to the VAR model, and strongly showed a bidirectional volatility spillover effect between the US EPU and WTI spot price.

The empirical findings revealed a significant interaction between EPU and WTI crude oil price. Investors, policymakers, and other key market participants could benefit from the results of this study, for example, by investigating the heterogeneity of spillover effects between EPU and WTI crude oil price, even in the long-term. In the process of policymaking, the government should pay more attention to policy continuity and stability, reduce the impact on crude oil prices, and reduce the impact of crude oil commodity prices on the real economy. The investors can also underline assets to minimize their losses by understanding the spillover relationship between US EPU and WTI crude oil prices. Moreover, decision-making departments in US can also restructure the energy policies for national economic sustainability. Meanwhile, in order to ensure a stable environment for domestic oil market growth, policymakers should pay attention to both the domestic oil pricing mechanism and global policies to improve their ability to respond to uncertain events.

Besides this significant contribution, the authors acknowledge some limitations. First, the sample that we used to test the proposed framework was collected only from the US. Comparative analysis of several developed countries can provide a more detailed viewpoint for other international crude oil markets. Second, because data from up to 2019 were used, we did not measure the impact of the recent COVID-19 pandemic on crude oil prices. Therefore, we recommend that the effect of the COVID-19 pandemic is integrated into the model in the future (including a ‘during’ and ‘post’ effect).

{kind=link}

{kind=link}

{kind=link}