1. Introduction

Broadly speaking, the concept of corporate social responsibility is deeply rooted in the idea of the long-term ‘footprint’ that an organization leaves on society, and can be seen in areas such as environmental responsibility/ sustainability [

1], employee relations [

2], and targeted marketing [

3]. Sustainability is a concept that can be interpreted in different ways, with no clear and rigorous meaning for the general public [

4]. Sustainability is often attributed as an end in itself, an ideal condition framed in absolute terms. However, sustainability is stronger than it seems, because it can be determined in different ways [

5].

Consumers value the behavior of companies for the products they buy. More and more companies are taking on their corporate social responsibilities (CSR) voluntarily, or in response to external forces [

6]. Participation in CSR is rewarded not only for the business operations, but also for loyalty [

7], identification [

8], and an increased procurement process [

9]. In recent years, consumers have become more concerned about environmental friendliness practices and the ethical standards of businesses, but interestingly, this has not significantly increased the commercial success of sustainable products [

10]. As a result, there is no balance between what consumers expect from businesses and the level at which consumers are willing to pay more, as per the wish of businesses; we refer this as a co-creation gap [

11]. The customer’s intentions and actions can be explained in many ways, one of which is the probable personal responsibility, and another is the lack of customer information. The gap between speech and action is an obstacle to sustainable development [

12]. To close this gap, a push and pull partnership is required between the consumers and the company. In other words, this gap will exist forever if the customer and the company will not collaborate with each other (co-creation) in order to produce a product that is eco-friendly and acknowledged by consumers [

13]. As a result of this collaborative approach, consumers can make more stable and realistic choices that are clearly visible and easily accessible.

Every organization wants to build a type of relationship with consumers that would encourage them to buy its products for a long period of time. Identification [

8], especially customer identification with a company via co-creation [

14], creates this type of choice, and raises issues such as strong attitude, honesty, and consistency. Co-creation creates a sense among consumers that they share the same values as those of the company. Co-creation (CC) can be regarded as an efficient, flexible and social process that aims to create relevant new products or services through communication and interaction with consumers [

15]. The perception of co-creation is that it is attractive in nature, as it can lead to many resources for the organization, including economic efficiency [

16], risk reduction [

17], relationship marketing [

18], and better understanding and competitiveness [

19]. In addition, co-creation is an inspiring experience for many consumers in different ways [

8]. First, consumers can establish warm, deep, and exclusive relationships with other members of the collaborative community. Second, when firms participate in a co-creation project, consumers always feel that they are growing as individuals, learning and being creative with the community [

20]. Most importantly, engaging in co-creation activities offers consumers opportunities for self-development, and social and hedonic [

21] resources that lead them to feel close to the brand. Remarkably, the same can be said about CSR, which seeks to ensure the value of the environment in which most participants interact.

Customers respond to CSR in different ways, and what works for one user may not work for another. Consumers also appear to be more sensitive to ‘negligent’ behavior than to ‘responsible’ company behavior [

7]. However, consumers need to have a clear understanding of the company’s efforts. They can develop (or provide an opportunity to know) a positive attitude only after learning about the company’s CSR policy [

22]. CSR creates a situation in which the consumer evaluates the company and the products, and attaches themselves to the company directly or indirectly [

23,

24]. The evaluation of the company, in turn, impacts consumer preferences. This is where social responsibility comes into play. It is clear that the relationship established between a socially responsible business and its customers ensures consistency [

25].

Green banking initiatives refer to any banking practice that creates environmental benefits [

26]. In other words, it means the promotion of environmentally friendly processes and the reduction of the carbon footprint of banking operations [

27]. The leading financial institutions of a country can improve the quality of their services and social responsibility through green initiatives and financing [

28]. Many modern banks in the world, at the local and international levels, are now making intensive and genuine effort to promote different technologies in line with green banking initiatives. Thus, green banking initiatives have become a prevalent trend in the modern banking world.

In brand policy, green positioning is achieved by combining functional characteristics and emotional resources. The same is true for the level of products as there are several product levels, in which, several groups can add values [

29]. This combination of ‘users’ and ‘non-users’ forces businesses to move from a traditional, one-sided concept of sustainability to a broad conception. This, in turn, reduces the risk to the company’s future. Due to the growing concern of environmentalism, consumers are more interested in purchasing products and services that have little impact on the environment [

11]. In addition, different studies have concluded that the environmental image of an organization can improve sales and competitiveness, while satisfying consumers [

30,

31]. Accordingly, the search for new information on various aspects of green banks has increased among consumers in the recent era, which indicates that consumers are concerned enough to monitor environmental practices of an organization [

32].

Going green has become an essential norm in the global banking industry. The idea of green banking has prompted banking institutions to introduce paperless, technology-based services, and to maintain their role as a responsible entity in sustainable development while minimizing the impact on the environment [

33]. It is important for banks to understand the need for green practices, because the main success or failure of this investment will affect the satisfaction and loyalty of their end consumers [

34]. We conceive of green consumer loyalty in line with the definition of Oliver [

35]: “the green loyalty is the preference of buyers to repurchase a product or service prompted by strong commitment of organization towards environment”.

With the growing inclination towards green banking, most researchers have studied issues in various areas, such as green banking initiatives [

33], the impact of green banks on sustainable development [

36], consumer information of green banks [

37], customer satisfaction in green banks [

38], green consumer loyalty [

33], green bank acceptance [

39], consumers’ green attitude [

40], and environment up-gradation through green banking initiatives [

41]. Accordingly, the search for new information on various aspects of green banks has increased among consumers in the recent era, which indicates that consumers are concerned with the monitoring of the environmental practices of an organization [

32]. Likewise, the transition to sustainability will change the character of banks, especially their products, services, and stakeholder relationships. Banks are one of the key players in supporting the transformation into a sustainable economy. The Goal for Sustainable Development has turned into a substantial goal for governments and businesses. This is due to a change in the understanding of the sustainable practices of organizations and the expansion of business objectives from profitability to sustainability [

42]. New economic developments are already taking place, as we have sustainable banks, environmental taxes, green investment, green purchases, industrial production, a low carbon economy, friendly-energy sources, and more. Banks are no longer impartial mediators between businesses and customers. They are seen as active participants in economic and social processes. The Responsible Banks of recent times demonstrate their social and environmental responsibility through their annual social responsibility report [

43].

The banking sector was especially chosen for the present study because of its large investment in CSR after the worldwide financial crunch in 2008, in order to restore consumer confidence and to enhance their image [

44]. Due to increased pressures from different stakeholders, including consumers, banking institutions have started to report their efforts to preserve the natural environment. In this regard, green banking initiatives can lead a bank toward consumer satisfaction, which ultimately enhances green consumer loyalty [

45,

46,

47]. Likewise, well-reputed banks in the banking industry began to engage in co-creation activities which aimed to improve the consumer experience. Consumer loyalty has a strong impact on corporate efficiency, as it is directly related to lower marketing expenses and greater revenues [

48]. Likewise, in today’s highly competitive era, organizations are trying to fight their counterparts through a variety of marketing tools, emphasizing that the inclusion of corporate social responsibility (CSR) as a core business strategy can move business forward [

49].

The homogenization of the banking segment has made it difficult for banking institutions to practice the quality of services needed in order to retain consumers. Thus, finding ways to gain the loyalty of consumers has become a challenge for the banking industry around the planet. Research has long-established that CSR is an impressive marketing approach to increase the loyalty of consumers [

8]. It has also been noted that consumers can reciprocate CSR based on their beliefs, brand identity, quality, and eventually loyalty [

50,

51]. Hence, companies involved in CSR activities can improve their institutional performance by improving consumer loyalty [

52].

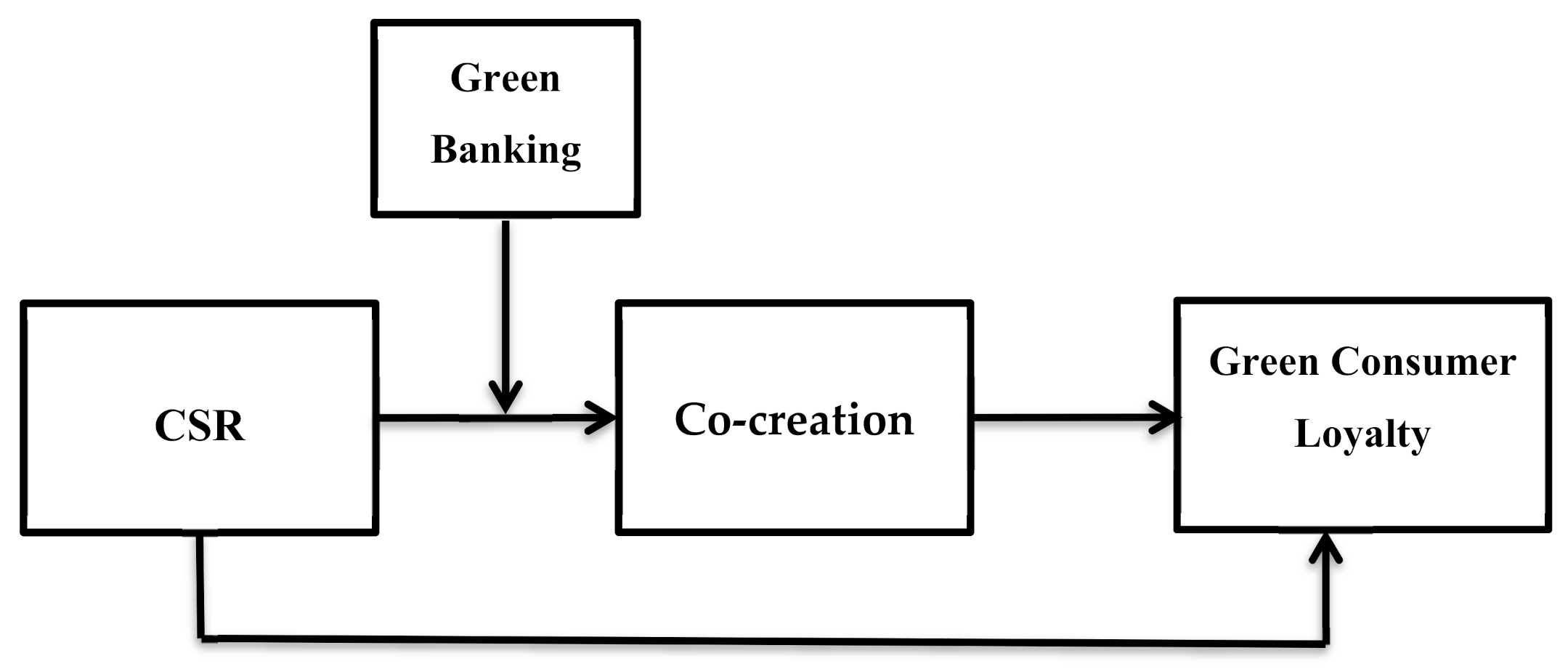

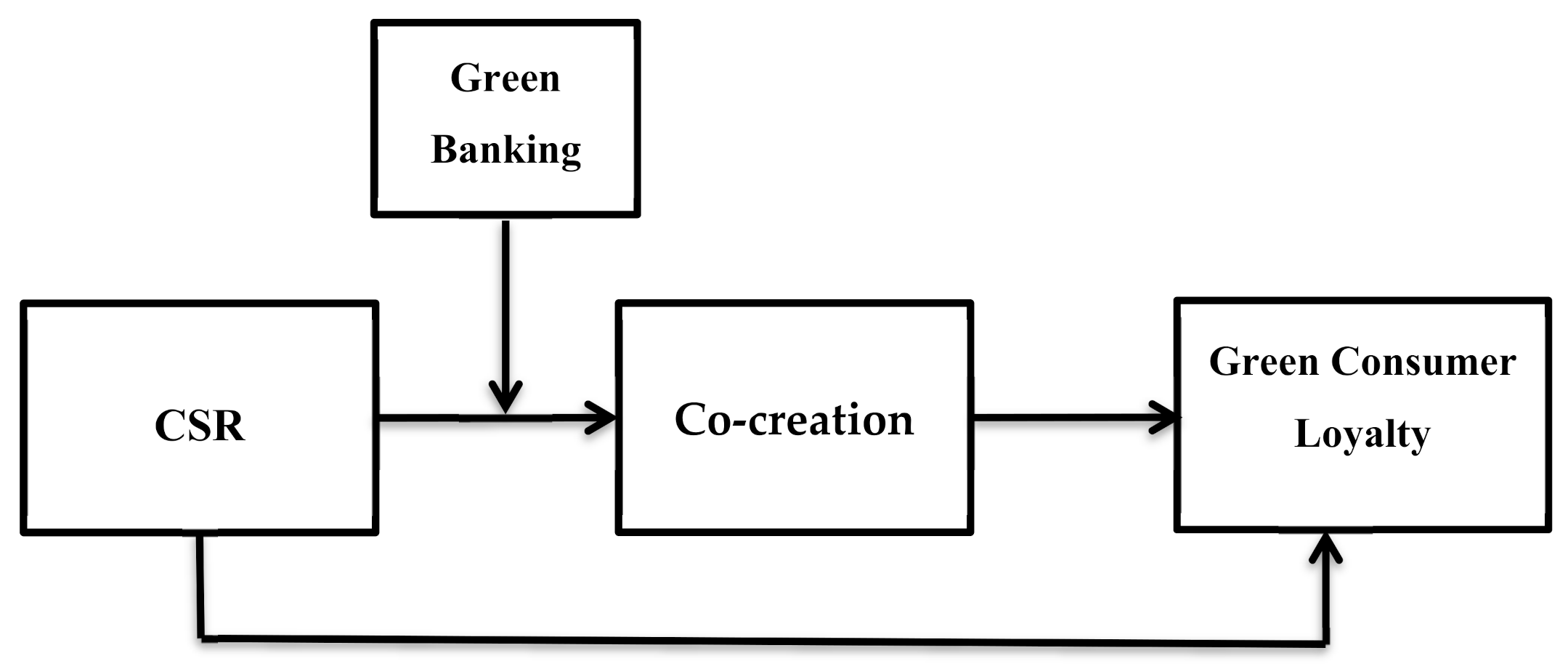

The contributions of the present study are many; first, the previous research has focused on emotional integration, such as affective engagement, with limited empirical studies of consumer behavior, particularly loyal consumer behavior [

53,

54]. Second, there are different studies confirming that consumer loyalty is a complex phenomenon, and the assumption that CSR alone will predict loyalty significantly is not wise thinking, as different studies have shown that the relationship of CSR and loyalty is made more significant by the introduction of moderators or mediators [

24,

55,

56,

57,

58]. In line with these arguments, we propose that the inclusion of co-creation variable as a mediator between CSR and consumer loyalty better explains this relationship, as supported by the extant literature [

8,

14]. Third, we argue that the green banking initiatives of a bank moderate this indirect relationship, such that green initiatives strengthen this indirect relationship and enhance green consumer loyalty. Hence, this study employs a moderated mediation approach. Fourth, there are limited evidences that CSR and co-creation can enhance the loyalty consumers in an Asian context, particularly in a developing country such as Pakistan [

8]. Fifth, much of the CSR research has been conducted on consumer behavior in advanced nations [

14,

15,

59], and the findings from such studies suggest that additional research is obligatory in the context of developing countries. The developing nations are comprised of developing economies which are expected to be more inclined to produce a social and environmental effect compared to developed nations.

The results of the current survey will help banking institutions to understand how they can develop core strategic considerations based on the integration of CSR, co-creation, and green initiatives to boost green consumer loyalty. The rest of the article is comprised of the theory building and hypothesis, research methodology, analysis of data, discussion, conclusion, and finally implications for policy makers.

5. Discussion and Conclusions

The objective of the present study was to investigate the impact of CSR activities on green consumer loyalty in the context of the banking industry of Pakistan, with the mediating effect of co-creation and the moderating effect of green banking initiatives. The results confirm that CSR activities positively predict banking consumer loyalty (beta = 0.66,

p < 0.05), which means that banks can use the CSR strategy to enhance consumer loyalty in the Pakistani banking sector. These findings are in line with previous research [

24,

52,

58,

92] studies which also support our argument that CSR can boost loyalty. Likewise, our findings also confirm that the development of co-creation is an enabler between the indirect relationship of CSR and green consumer loyalty, as co-creation partially mediates this relationship (standardized beta = 0.41 (0.142). This finding also received support from the existing literature [

8,

14]. Finally, we tested the moderation effect of green banking initiatives on the mediated relationship of CSR and consumer loyalty via co-creation. The results provide sufficient grounds to accept that green banking initiatives moderate this mediated relation. Hence, there is confirmation of the moderated mediation effect (standardized beta = 0.54 (0.144). In the coming section, we discuss and conclude our findings in detail.

The banking sector of Pakistan participates in CSR activities including charity, cause-and-effect marketing, and environmental safety. This industry is facing fierce competition, leading to an ever-increasing stiff environment. In order to increase the efficiency of their services, banks are looking for additional marketing strategies—such as CSR, green banking initiatives, and co-creation—in order to foster a favorable attitude in consumers. Technology is changing the traditional banking with a fast pace. As a result, banks pay more attention to both consumers and financial technologies in order to create products that meet the needs of consumers. Nowadays, consumers themselves are in great demand, as vanilla solutions from the banks have already been rejected by consumers. The consumers want to see the initiatives of their banking partners, especially green initiatives.

It’s not just the digital power of financial technologies that banks need to adopt in their product development programs; consumers themselves have more access to information than ever before, and this increases their ability to understand their own needs. Banks need to understand that diversified partnerships will be the standard for future of financial services. The emergence of collaborative design (co-creation) caused a paradigm transition to a typical product development model in which marketing / sales departments conduct market research and then submit it to engineers in order for them to develop a product or service. However, the danger associated with the traditional approach is that these products may not meet the needs of the market in actual terms, and hence money is wasted and time runs out, which may lead to the failure of the whole organization. The new approach (co-creation) proactively involves consumers in the product development process and receiving feedback from consumers. This iteration cycle continues several times, as organizations have to produce a product that has a much higher level of reliability than the traditional model beyond the consumer‘s perception. Alignment with this approach requires the constant participation of consumers in order to build their belief that their organization is a caring organization, on the one hand, and that it takes into account social responsibility on the other hand. The above discussion is also supported by the extant literature [

78,

107,

111,

128,

129]. Likewise, sustainability is a big trend in recent times, as eco-friendliness has become the new norm for modern consumers, who are increasingly choosing well-made ethical products and services over cheap and mass-produced ones.

Green banking initiatives are one of the most imperative aspects driving green consumer loyalty. This is because modern consumers feel a kind of stewardship regarding the environment. All of these efforts eventually contribute towards building a higher level of consumer loyalty. These findings are also in line with previous researchers [

14,

82,

110]. The importance of consumer loyalty from a green perspective is reflected in the many marketing benefits that result from increased engagement. Once a banking institution understands consumers, it is important to understand the various benefits of consumer loyalty in order to better understand how to deal with them. In today’s business, consumer trust is everything, and CSR is an important strategy for financial institutions to win the trust of consumers.

Social responsibility allows businesses to use their strengths to benefit the local community. The diffusion of CSR efforts to all stakeholders is essential, in that it allows individuals to contribute to the public account in their own way, and reduces the investment needed to benefit the organization and the community. This, in turn, has a measurable impact on all departments, as banks invest indirectly in public effort, financial literacy, diversity of access and supply, and the environment. The advantage of social responsibility beyond branding is that it establishes the perception among consumers that the brand is socially responsible and contributing to preserve nature through green initiatives. Good CSR work carefully improves the ability of individuals and consumers to engage in meaningful (co-creation) organizational approaches.

CSR is one of the ways to increase confidence through targeted, community-oriented approaches, rather than large and distant investments in resources. These results are also supported by previous research [

14,

51,

92,

108,

112]. This means offering financial literacy programs to local schools, providing access and financial assistance to older and caring adults, and offering community days for free financial counseling. It also means participation in private communities, and the allocation of CSR funds for public festivals, clean-ups, and environmental activities. This is because going local means that the efforts of a bank, that has the opportunity to do business, are visible to the public. If the bank can build trust through CSR and co-creation efforts that are not marketing-centric, but instead aimed at improving the community, then the bank has taken one of the biggest steps to protect long-term consumers and increase social benefits.

The benefits of consumer loyalty can enhance repeat business, sales opportunities, high purchase prices, and positive word of mouth. Loyal consumers continue to purchase banking services on a regular basis. As the power to build relationships with this type of consumer increases, their purchase price increases in value or volume (or, more often, in both). This is sometimes natural, but the organization may choose to implement other incentive programs in order to encourage consumer loyalty, or to increase their spending levels, which in turn increases profits. Loyal consumers not only bring in new consumers, but also come back, depending on the quality of services and their relationship with a particular bank. However, as sales grow and consumers become more diverse, there are alternatives to the creation of consumer preferences.

Co-creation is different from assembling the same; rather, the banks and their consumers work together to create good ideas, improve services, and create new products based on consumer feedback. The idea is to let participants, especially consumers, know that they are working directly and independently to improve the services of a particular bank, especially in the context of environmentalism. This not only increases their presence, but also their green loyalty, as consumers who see themselves as part of the company are determined to continue using its services. The paybacks of co-creation are many, and can affect sustainability, marketing results, and overall profitability. We conclude that the most interested consumers in the company are an unexploited tool to increase the level of success, which means that cooperation and consumer resilience will help build the brand.

5.1. Implications and Suggestions

The present study has some important implications for theory, and for people in practice. For theory, this study accentuates the role of CSR in building loyal consumers in the Pakistani banking sector. That is, while companies are committed to CSR, they do everything they can to build meaningful relationships with their consumers, employees, and the environment. Consumers support organizations with their positive attitudes. Investing in CSR ensures that banks do more humanitarian work, and the interest of all stakeholders is vital for them. Therefore, they communicate reliably with the consumer through the branding process, which ultimately leads to greater loyalty, especially green loyalty. In a similar vein, CSR strengthens co-creation activities along with the general consumer base, which motivates consumers to participate in the bank’s code of conduct in communication, and provides consumers with a lot of useful information on improving the quality of products and services. A bank’s CSR gives consumers a platform to report directly to banks, which increases their self-esteem and pushes them to cross boundaries of behavior. In addition, social identity theory reinforces the power of the ethical value-based marketing model in defining the relationship between CSR co-creation and green initiatives.

Additionally, there are some practical implications for financial policy makers in this study. If bank policy makers need to be honest with people through CSR, they need to communicate with consumers through consumer engagement activities (co-creation). Banks should encourage discussions with consumers on new products, development services, and innovations. Banks can use co-creation activities as a tool to improve consumer’s participation in the development of credit, pensions, car loans, and future investment plans. In this way, banks can easily obtain new ideas through experienced consumers. Our research also confirms that when companies understand the needs of their consumers, and involve them in the process of integration (co-creation), their loyalty increases. In addition, CSR activities not only allow consumers to identify with the organization, but to formally lead to consumer behavior. Therefore, banks need to secure this recognition through CSR-related programs, as this type of recognition is more robust than others. Banks’ CSR guidelines should translate into actions that are appropriate for different partners, such as personnel growth, consumer handling policies, ethics and regulatory policies, and working in a better environment for the community. In the end, banks should try to build a culture that accepts the experience and understanding of valued consumers. In addition, banks need to maintain close relationships with consumers based on trust and brand strength. Banks need to see them as a source of innovation. This collaborative development approach has the best potential to turn CSR models into loyal consumers.

Our research further suggests that banking institutions need to realize the importance of green initiatives from a broader perspective; rather than assuming them to be an ethical responsibility, the banks are encouraged to include green initiatives in their core business practices, as the results of present study confirm that going green induces consumer loyalty from a green perspective. Hence, the policy makers are recommended to promote green initiatives in order to reap long term benefits in the form of induced consumer loyalty. In this regard, the following suggestions may be helpful for banking institutions:

- (1)

Banks need environmental impact assessment as part of the bank’s overall consumer assessment (especially corporate consumers) before granting a loan if the consumer re-examines the environmental risk model and assesses the environmental impact of the consumer’s business.

- (2)

Green offices should be established in order to implement the green banking guidelines and to introduce environmental culture as part of the organizational culture.

- (3)

The recycling of office waste using a recycling environment should be encouraged.

- (4)

An environmental campaign needs to be launched in order to commemorate environmental days such as World Water Day, Earth Day and Environmental Day.

- (5)

Banks should choose ways to eliminate / reduce the use of paper in their day-to-day operations. These steps include a gradual transition to paperless banking.

- (6)

Banks should install solar energy systems, which will prevent the release of greenhouse gases to reduce environmental degradation.

5.2. Limitations and the Way Forward

Like any other study, this study has its limitations. First, this research was limited to the banking institutions of Pakistan, so it is logical for future researchers to conduct the same in other areas of services, such as hospitality and tourism. In addition, some researchers may also be able to take into account the manufacturing industry and compare their results with those of the service sector. Second, this study is only representative of Pakistan’s population, and its results cannot be generalized to all developing countries. In addition, since CSR activities are perceived differently by consumers in different cultures, repeating this type of research in other developing countries may generate different results. Therefore, in order to increase the integration of the research, it is recommended that researchers reproduce the present study in other developing countries.

Third, since all of the information in this study was collected through surveys, there are concerns of mono-method bias. Future research should reduce this issue by better understanding the impact of CSR on consumer loyalty, through grouping or in-depth interviews using qualitative insights. Fourth, this study only takes into account the attitudinal facet of CSR standards, co-creation, green banking, and green consumer loyalty; other studies could further strengthen our research by developing behavioral facets together with attitudinal ones. In addition to removing these limitations, there are other possibilities for future research. For example, it would be interesting to explore the ways in which employees affect the CSR opinion of consumers. This is true for service industries, as these types of services often have more communication between consumers and employees in order to build the consumer experience. Fifth, this study involves the development of co-creation with consumer loyalty; future research may involve brand-related variables, including brand equity, which is one of the most discussed variables in the world of marketing and brand management. It will be interesting to see what kind of brand equity, consumer-based brand equity, or financially-based brand equity is most affected by co-creation and green initiatives. Finally, cross-sectional data with random samples were used in this study; other studies could be performed using time series data and other sampling methods.

,

,

{kind=link}

CC

CC GCL

GCL