Abstract

Research and development (R&D) investment is widely recognised as one of the crucial elements of generating the competitive advantage of contemporary companies. At the same time, it is also considered to represent one of the key determinants of overall sustainable development. Global competition, which is becoming increasingly harsh and forces companies to provide value-added products, processes and services, constitutes a reason why R&D investment is indispensable in contemporary business operations as they facilitate keeping the companies’ position in the market in terms of their competitiveness. The main aim of this paper is therefore to examine the impact of R&D expenditures on corporate performance. Using a multiple regression analysis, two different panel datasets covering Slovenian and world R&D companies are analysed. This gives a unique opportunity to obtain comprehensive and interesting findings, representing the main originality and value of the paper. The empirical results reveal that R&D expenditures are not effective in the short-term period and bring certain benefits in the long-term period. The findings of this paper provide several important theoretical and practical implications.

1. Introduction

Nowadays, research and development (R&D) investment is becoming a critical element of generating the (sustainable) competitive advantage of companies and economies, causing them to invest persistently in R&D activities [1,2,3,4,5,6,7]. This stems from the global economy shifting from an economy based on industry to one based on knowledge, which has drastically altered both the business environment and how different stakeholders function. This is seen in global competition becoming ever tougher, which is forcing companies to provide value-added products, processes and services. This is why R&D investment is indispensable in modern business operations because it helps companies retain their market position in terms of competitiveness. According to the current rising position of R&D investment, it is no surprise that R&D expenditures play a vital role in the business sector’s overall investment activity [8,9]. Moreover, they have also important implications for overall sustainability [1].

In contemporary society, sustainability is considered as an integration of environmental, social, economic and cultural perspectives, acting as mutually complementary elements [10]. However, sustainability is usually oriented towards environmental or social issues, leaving economic sustainability heavily neglected [11]. Namely, in the situation when companies are not able to achieve a desirable level of sustainability, there exists a high risk of failing in environmental and social sustainability. This suggests that the economic perspective of sustainability is a prerequisite for achieving overall sustainability. Accordingly, R&D investment represents a necessary condition for innovation, which is one of the key determinants of sustainable development in general [12]. Usually the main reason why companies invest in R&D and perform innovative activities lies in gaining competitive advantages over their competitors and achieving better performance. However, some companies may even be more inclined toward R&D investment and innovation in order to produce more sustainable production systems as a response to new environmental and social issues [13]. Nevertheless, all companies that are engaged in R&D can (purposely or not) can contribute to better overall sustainability as beneficial effects for sustainability are often considered as parallel effects of R&D and innovation [1].

Therefore, the main aim of this paper is to answer the main research question of how R&D expenditures influence operating and market corporate performance. In this context, the study seeks to empirically verify whether the conflicting results observed in the literature arise from the fact that the impact of R&D expenditures depends on: (1) different measurements of corporate performance; (2) different characteristics of companies; and (3) a different economy-specific legal framework and financial environment. For these purposes, empirical analysis is performed on a sample of predominantly small and non-listed Slovenian companies by utilising different indicators for operating performance. An additional empirical analysis is performed on a sample of world R&D companies, i.e., companies that heavily invest in R&D and operate in the European Union (EU), the United States of America (USA), China and Japan in order to further confirm the results and obtain extra insights into market performance. Moreover, the utilisation of two different datasets allows the factors associated with different characteristics of companies and economies to be isolated, which may bring important implications for corporate performance. Finally, the use of both databases gives a unique opportunity to obtain comprehensive and interesting findings. The remaining sections of this paper are structured as follows. The second section presents the theoretical considerations and literature review. The third section describes the data and the research methods. In the section four, the empirical results are presented. At the end, concluding remarks are provided.

2. Theoretical Considerations and Literature Review

According to the resource-based theory, companies possess strategic resources that give them an exceptional opportunity to develop (sustainable) competitive advantages over their competitors [14,15]. This implies that investment activity should be seen as one of the most important activities because it is central to all companies’ functioning. In this context, due to the intangible nature of R&D expenditures, they may be considered an important part of companies’ resources since they are unique and are thus able to generate a sustainable competitive advantage leading to a better overall corporate performance. The role of intangible assets is even more strongly emphasised in the knowledge-based theory, which addresses complex issues regarding intangible capital [16]. Finally, assuming perfect information in the market, the efficient market theory provides a reasonable explanation of the relationship between R&D expenditures and market performance. Namely, under the assumption of market efficiency, any kind of investment activity, including R&D expenditures, should be immediately recognised by the market and reflected in the better market performance of the company [17]. From a theoretical perspective, R&D expenditures should have important implications for corporate performance.

2.1. R&D Expenditures and Operating Performance

The impact of R&D expenditures on operating performance is widely studied. Some empirical studies establish that R&D expenditures have an immediate beneficial impact on current operating performance. This is confirmed by several empirical studies for companies operating in the USA [18,19]. Similar evidence can be found also for companies operating in the global electronics industry, the study reveals a positive relationship between R&D expenditures and gross profit, although it shows that R&D expenditures do not enhance return on equity (ROE) and return on assets (ROA) [20].

To the contrary, some empirical studies establish a positive impact of R&D expenditures only for future operating performance. The empirical evidence from Turkey shows that that R&D expenditures have a positive impact on long-term operating performance for periods longer than one year [21,22]. Similar evidence can be found for Indian listed companies [23]. Further, a study comparing China and Japan reveals the lag between R&D expenditures and profitability is about one year in Japan and two years in China [24]. Finally, the two-year lag between R&D investment and financial returns is also confirmed for a sample of Taiwanese high-tech companies [25].

The review of the literature on R&D expenditures and operating performance suggests that R&D expenditures are important for enhancing operating performance. However, the findings of different empirical studies are inconclusive. Some studies suggest there is an immediate positive impact of R&D expenditures on operating performance, while others suggest there is instead a lag effect between R&D expenditures and operating performance. Nevertheless, the dominant belief is that there should be no significant or even negative impact of R&D expenditures on current operating performance, while the impact becomes positive for the operating performance in future periods. This implies that R&D spending in the current period is effective in the long term more than in the short term [26]. Given the above discussion, the following research hypothesis is proposed:

Hypothesis 1.

R&D expenditures deteriorate current operating performance and improve future operating performance.

2.2. R&D Expenditures and Market Performance

The literature also contains some empirical studies examining the impact of R&D expenditures on market performance. The empirical evidence for a large sample of companies operating in the USA suggests a positive association between R&D expenditures and market performance. The results are similar for manufacturing and non-manufacturing companies as well as for domestic and multinational corporations [27,28,29,30]. There are also some empirical studies, which extend the investigation to other countries. Bae and Kim [31] establish a significant and positive impact of R&D investment on market value and stock return volatility in the USA, Germany and Japan. Similar results can be found also for companies operating in Taiwan [32], the EU [33] and Turkey [34].

Unlike previous empirical researchers, Cazavan-Jeny and Jeanjean [35] establish that R&D expenditures have a negative impact on market performance for a sample of French companies. As a reason for such unexpected results, they argue that legal enforcement may play a role in the relationship between R&D expenditures and market performance.

Nevertheless, Vithessonthi and Racela [36] explain why the impact of R&D expenditures on corporate performance is negative in the short run and positive in the long run through the application of net present value. Namely, R&D investment is often considered as a long-term investment in different R&D projects that are usually estimated to have a positive net present value. In the short term, the cash flows associated with R&D projects are negative and consequently harm corporate performance in profitability terms. Yet, in the long run, assuming that an R&D project’s expected net present values are positive, an R&D investment should increase the company’s market value. Competitive companies with innovative products, processes and services can also attract the attention of investors and see them increase their market share [37]. According to the above discussion, the following research hypothesis is proposed:

Hypothesis 2.

R&D expenditures improve current and future market performance.

3. Data and Research Methods

3.1. Sample Selection

A comprehensive empirical analysis is performed on two different panel datasets covering Slovenian and world R&D companies. First, the dataset for Slovenian companies is obtained from the Statistical Office of the Republic of Slovenia (SORS) [38], which also provides the data from Agency of the Republic of Slovenia for Public Legal Records and Related Services (AJPES) covering balance-sheet and income-statement data. The sample of Slovenian companies is restricted to the latest available data for the five-year period 2012–2016, covering non-financial private companies operating in either the manufacturing (NACE 10-33) or service (NACE 35-99) sectors and taking the legal organisational form of a private or public limited company. In addition, company-year observations with incomplete data or negative equity are excluded from the empirical analysis. Finally, in order to mitigate the small deflator problem, company-year observations with less than 10,000 EUR in net sales are excluded from the analysis. The final unbalanced panel dataset of Slovenian companies consists of 3,399 company-year observations. The distribution of the final sample of Slovenian companies by years is shown in Table 1.

Table 1.

Sample distribution of Slovenian companies by years (number and share of companies).

An additional empirical analysis is performed on a sample of world R&D companies in order to further confirm the results and obtain additional insights into market performance. The world R&D companies are companies operating in major world economies, that is, the EU, the USA, China and Japan and are considered as companies which invest heavily in R&D on the world level. The dataset for world R&D companies is obtained from the EU Industrial R&D Investment Scoreboard 2017 and 2018 provided by the European Commission that covers economic and financial information on the top R&D corporate investors extracted directly from companies’ annual reports for the three-year period 2015–2017 [39,40]. In order to obtain a representative sample of world R&D companies for the empirical analysis, meaning that they are continuously engaged in R&D investment, a balanced panel dataset of companies having more than 1 million EUR in net sales for the entire period 2015–2017 is created. The final sample consists of 1,700 companies for the three-year period, resulting in 5,100 company-year observations. Table 2 presents the distribution of the companies by major world economies.

Table 2.

Sample distribution of world research and development (R&D) companies by major world economies (number and share of companies).

3.2. Variables

3.2.1. Dependent Variables

Several dependent variables that try to capture corporate performance are employed in this empirical study. Corporate performance refers to operating performance in terms of profitability indicators and market performance in terms of market value indicators. Namely, the use of two different datasets allows accounting-based and market-based performance indicators to be considered for measuring corporate performance. However, profitability indicators can be applied to both Slovenian companies and world R&D companies, while market value indicators can solely be applied to world R&D companies as they are listed on the stock exchange.

The first dependent variable is operating performance, which can be measured by different accounting-based performance indicators. In the empirical literature, the most common ratios for measuring operating performance are return on assets (ROA) [41], return on equity (ROE) [42] and return on sales (ROS) [43]. In this empirical study, all three accounting-based performance indicators (ROA, ROE and ROS) are employed for a sample of Slovenian companies, while only ROS is used for the sample of world R&D companies due to data limitations. These measures for operating performance in fact indicate whether companies are effectively using their assets, equity and sales to generate profits [44,45].

The second dependent variable is market performance, which can also be measured by different market-based performance indicators. These indicators are typically used to evaluate the economic status of companies listed on the market and are important for assessing the current price of companies’ shares. Accordingly, market value indicators can give management information about investors’ perceptions regarding the company’s future prospects. There is a wide variety of market value indicators, with the most common being earnings per share (EPS), book value per share (BVPS), price-to-earnings ratio, and price-to-sales ratio (PSR) [46,47]. In this empirical study, the price-to-sales ratio (PSR) is used as a measure of market performance for the sample of world R&D companies. The price-to-sales ratio (PSR) actually measures how much investors are willing to pay for each monetary unit of sales, which means it is a very good indicator of a stock’s popularity among investors [48].

3.2.2. Independent Variable

The main independent variable is R&D intensity (RDI), which is also widely used in empirical studies [49,50]. The ratio of R&D expenditures to net sales also represents a comparable basis for companies of different sizes. R&D intensity (RDI) is identically defined for the sample of Slovenian companies as for the sample of world R&D companies. For the purposes of investigating the current and lagged impacts of R&D expenditures on operating and market performance, a current (RDIt) and lagged (RDIt−1) variable for R&D intensity is considered in the empirical analysis. A one-year lag is used since R&D expenditures are often considered to be a driver of future corporate performance. Although the effects of R&D expenditures may be reflected over a longer lag period, a one-year lag can be assumed for companies which are engaged in R&D activity in any way. These are companies which perform R&D activity as their core business, benefit from public support for R&D investment or persistently invest in R&D activity. The consideration of a one-year lag can also be justified by the short-term nature of much commercial R&D, which is often the domain of the business sector [51]. According to the proposed research hypotheses, it expected that R&D intensity (RDIt) has a negative impact on current operating performance and a positive impact on future operating performance. On the other hand, it is expected that R&D intensity (RDIt−1) positively impacts current and future market performance.

3.2.3. Control Variables

Empirical studies suggest other factors can also exert an impact on corporate performance in terms of operational and market performance. Due to the availability of different financial information for the sample of Slovenian companies and world R&D companies, various control variables are considered for each sample. In both cases, it is ensured that the control variables represent other relevant and key determinants which may affect corporate performance.

For the sample of Slovenian companies, the following control variables are considered in the empirical analysis. The first one refers to financial leverage (LEV), which is expected to negatively impact operating performance since higher debt requires more company resources in order to repay the debt, which then reduces the funds available for any investments [52,53]. The second control variable is liquidity (LIQ), which is expected to have a positive impact on operating performance, since high liquidity reduces exposure to the risk of being unable to meet financial commitments in the short term [54]. The next control variable is company net sales growth (NSG), which is expected to positively impact operating performance, mainly due to the extra income generated and increasing profitability [52,53,55,56,57]. Finally, the company size (SIZE) is another control variable, which is usually considered to have a positive impact on corporate performance, since larger companies are able to use economies of scale, have facilitated or better access to capital markets and can create barriers to newly emerging companies [53,58]. In addition, year dummy variables (YEAR) are included in the empirical analysis for the purposes of controlling for time effects.

For the sample of world R&D companies, two control variables are considered in the empirical analysis. The first control variable is capital expenditure intensity (CEI). This control variable is expected to have a negative impact on operating performance. It is established that, to invest in physical assets such as equipment, property and industrial buildings, companies usually require large amounts of funding. This may then lead to a lower operating performance [59,60,61]. On the contrary, according to Chung [62] capital expenditure intensity (CEI) is expected to positively impact market performance since the market positively values new capital expenditures. The second control variable is company size (SIZE), which is expected to have a positive impact on operating performance due to the reasons stated above concerning economies of scale, access to capital markets and barriers to newly emerging companies. Yet, company size (SIZE) is expected to have a negative impact on market performance [63]. In addition, year dummy variables (YEAR) are included in the empirical analysis for the purposes of controlling for time effects.

This empirical study includes the entire range of different variables from the two different samples of Slovenian and world R&D companies. The use of individual variables for a given sample of companies depends on data availability. Nevertheless, all variables are suitable for the empirical analysis in order to investigate the impact of R&D investment on corporate performance. A summary of all variables employed in the empirical analysis is systematically presented in Table 3.

Table 3.

Summary of variables used in the empirical analysis.

3.3. Research Methods

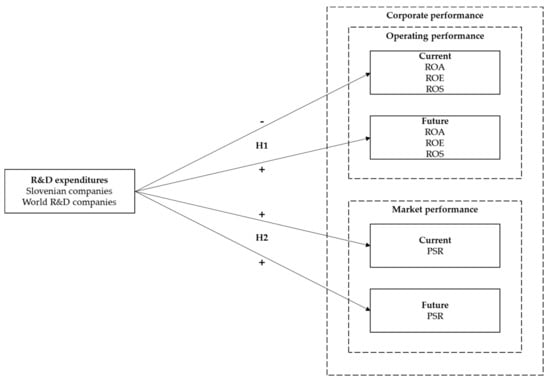

This empirical study involves a comprehensive empirical analysis of the impact of R&D expenditures on corporate performance for Slovenia and beyond. Panel data regression analysis is applied on a sample of Slovenian and world R&D companies. Since the sample of Slovenian companies consists solely of companies not listed on the stock exchange, an additional dataset of world R&D companies is utilised in order to obtain additional insights. To examine the impact of R&D expenditures on corporate performance and consequently test the proposed research hypotheses, operating and market performance indicators are regressed against the main independent variables of interest (see Figure 1).

Figure 1.

Research framework. Source: Own presentation.

For the sample of Slovenian companies, the dependent variables (ROA, ROE and ROS) are regressed against the R&D intensity (RDIt) and lagged R&D intensity (RDIt−1), which are estimated in separate models. In addition, some control variables are included in the multiple regression models, namely financial leverage (LEV), liquidity (LIQ), net sales growth (NSG) and company size (SIZE). In order to control for year effects, time dummy variables (YEAR) are also taken into consideration. The multiple regression models considering different profitability indicators (ROA, ROE and ROS) are presented in Equation (1), Equation (2) and Equation (3) respectively, where the effects of current and lagged R&D intensity (RDI) are considered in separate models.

Similarly, in order to obtain additional empirical verification, for the sample of world R&D companies the dependent variable return on sales (ROS) is regressed against R&D intensity (RDIt) and lagged R&D intensity (RDIt−1), which are estimated in separate models. Due to data limitations, fewer control variables are included in the multiple regression models: capital expenditures intensity (CEI) and company size (SIZE). In order to control for year effects, time dummy variables (YEAR) are also taken into consideration. The regression model is presented in Equation (4) where the effects of current and lagged R&D intensity (RDI) are considered in separate models.

The sample of world R&D companies also allows an examination of the impact of R&D spending on market performance. For this purpose, the dependent variable price-to-sales ratio (PSR) is regressed against the main independent variables of interest, R&D intensity (RDIt) and lagged R&D intensity (RDIt−1), which are estimated in separate models. In addition, some control variables are further included in the multiple regression models, namely capital expenditure intensity (CEI) and company size (SIZE). In order to control for year effects, time dummy variables (YEAR) are also included. The regression model is presented in Equation (5).

All of the proposed regression models can be estimated using different econometric specifications. Generally, three main different alternative econometric specifications of regression models exist for panel data: the pooled regression model, random effects model and fixed effects model. In this context, it is necessary to consider that companies differ from each other due to different market conditions. Considering the particularities of the data, fixed effects model seems to be the most suitable econometric specification as it assumes that something within the company may affect or bias the predictor or outcome variables and therefore it is necessary to control for this [64]. Nevertheless, in order to statistically determine which econometric specification is most suitable for the data used in the empirical analysis, a three-step procedure is applied. First, the LM test is used in order to decide between the random effects and pooled regression models. Second, the F test is applied to compare between the pooled regression and fixed effects models. Third, the Hausman test is conducted to choose between the random effects and fixed effects models [65].

Regression disturbances are assumed in standard panel regression models to be homoscedastic and to entail the same variance across individuals. This assumption does not fully apply to company-level panel data since companies vary greatly in size [66]. A serious consequence of heteroscedasticity is the bias of standard errors. Since standard errors are a central parameter for conducting significance tests, their bias therefore leads to inappropriate statistical inferences [67]. In order to alleviate the problem of heteroscedasticity, the heteroscedasticity-robust (White) standard errors are employed in the multiple regression models.

4. Empirical Results

4.1. Descriptive Statistics

Descriptive statistics of variables (except year effects) are presented for the sample of Slovenian companies and world R&D companies separately. Since the companies are a very heterogeneous group of units, there may be some outliers in the data. In order to eliminate the effect of possibly spurious outliers, all of the continuous variables are winsorised at the 2.5% and 97.5% levels by each year for the sample of Slovenian companies and at the 5% and 95% levels by each year for the sample of world R&D companies. Further, the Winsorisation procedure is often also considered as robust statistics [68].

Table 4 presents descriptive statistics for Slovenian companies for the period 2012–2016. It shows the mean and standard deviation values for the variables included in the empirical analysis. The mean values of return on assets (ROA), return on equity (ROE) and return on sales (ROS) indicate that on average Slovenian companies are effectively using their assets, equity and sales to generate profits. Moreover, the mean values of R&D intensity (RDI), financial leverage (LEV) and liquidity (LIQ) show they are at a relatively high level compared to the current operating performance in terms of company profitability. Finally, the descriptive statistics reveal that Slovenian companies on average grow at a rate of 10.50%.

Table 4.

Descriptive statistics of the variables for the Slovenian companies.

Similarly, Table 5 shows descriptive statistics for world R&D companies for the period 2015–2017. It presents the mean, standard deviation, minimum and maximum values for the variables included in the empirical analysis. The mean value of return on sales (ROS) indicates that, on average, world R&D companies are effectively using their sales to generate profits. Further, the mean value of the price-to-sales ratio (PSR) shows it is at a relatively high level compared to the current company profitability. The mean values for R&D intensity (RDI) and capital expenditures intensity (CEI) suggest world R&D companies devote more funds to R&D investment rather than to acquiring or upgrading their physical assets such as equipment, property and industrial buildings.

Table 5.

Descriptive statistics of the variables for the world R&D companies.

Table 6 shows Pearson’s correlation between variables (except year effects) for the sample of Slovenian companies. The simple correlation shows a strong, positive and significant correlation between the operating performance indicators (ROA, ROE and ROS), which are used as dependent variables in separate multiple regression models. The Pearson correlation matrix also reveals that R&D intensity (RDI) and financial leverage (LEV) are negatively correlated with operating performance. Liquidity (LIQ) and net sales growth (NSG) seem positively correlated with operating performance. This is in line with expectations. However, company size (SIZE) seems to be negatively correlated with operating performance, which is contrary to expectations. Nevertheless, the simple correlation between the explanatory variables does not indicate any strong linear relationship, suggesting there is no issue of multicollinearity in the data for the Slovenian companies.

Table 6.

Pearson’s correlation matrix of the variables for the Slovenian companies.

Similarly, Table 7 shows Pearson’s correlation between variables (except year effects) for the sample of world R&D companies. The Pearson correlation matrix reveals that R&D intensity (RDI) is negatively correlated with return on sales (ROS) and positively correlated with price-to-sales ratio (PSR). Capital expenditure intensity (CEI) is negatively correlated with return on sales (ROS) and positively correlated with price-to-sales ratio (PSR), while the correlation between company size (SIZE) and corporate performance indicators is invertible. This is in line with expectations. Still, the simple correlation between the explanatory variables does not indicate any strong linear relationship, suggesting there is no issue of multicollinearity in the data for the world R&D companies.

Table 7.

Pearson’s correlation matrix of the variables for the world R&D companies.

4.2. Multiple Regression Analysis

Multiple regression models may be estimated using three main different alternative econometric specifications: the pooled regression model, random effects model and fixed effects model. Based on a three-step procedure of different model specification tests (LM test, F test and Hausman test), it is statistically determined that the fixed effects model is the most preferred model for almost all of the multiple regression models (except for Model 5 (a and b) for low-tech sample of world R&D companies). This is also in line with the initial expectations when considering the particularities of the data. Moreover, the heteroscedasticity-robust (White) standard errors are employed in the multiple regression models in order to alleviate the problem of heteroscedasticity.

The empirical results for the relationship between R&D expenditures and operating performance for the total sample of Slovenian companies are presented in Table 8. According to Model 1 (a), Model 2 (a) and Model 3 (a), the regression coefficient of R&D intensity (RDIt) for operating performance indicators suggests that a 1% increase in R&D intensity (RDIt) leads to a 0.029% decrease in return on assets (ROA), a 0.056% decrease in return on equity (ROE) and a 0.030% decrease in return on sales (ROS). All of these regression coefficients are significant at the 1% level and suggest that R&D intensity (RDIt) negatively impacts current operating performance regardless of different measurements of operating performance. Moreover, the results for the control variables are in line with the initial expectations.

Table 8.

Multiple regression results for the relationship between R&D expenditure and operating performance for the Slovenian companies.

Since R&D expenditures often concern long-term performance, their impact on future operating performance is further examined in additional multiple regression models with a one-year lagged R&D intensity (RDIt−1). According to Model 1 (b), Model 2 (b) and Model 3 (b), the regression coefficient of lagged R&D intensity (RDIt−1) for the operating performance indicators suggests that a 1% increase in lagged R&D intensity (RDIt−1) leads to a 0.034% increase in return on assets (ROA), a 0.047% increase in return on equity (ROE) and a 0.033% increase in return on sales (ROS). The regression coefficients for return on assets (ROA) and return on sales (ROS) are significant at the 1% level, while the regression coefficient for return on equity (ROE) is significant at the 5% level and suggests that lagged R&D intensity (RDIt−1) positively impacts current operating performance regardless of different measurements of operating performance. Moreover, the results for the control variables are in line with the initial expectations.

Table 9 presents the empirical results for the relationship between R&D expenditures and operating performance for the Slovenian high-tech companies. The results show a significant impact of R&D expenditures on return on assets (ROA) and return on sales (ROS), while the impact on return on equity (ROE) is not significant. According to Model 1 (a), Model 2 (a) and Model 3 (a), the regression coefficient of R&D intensity (RDIt) for operating performance indicators suggests that a 1% increase of R&D intensity (RDIt) leads to a 0.024% decrease in return on assets (ROA), a 0.043% decrease in return on equity (ROE) and a 0.027% decrease in return on sales (ROS). Furthermore, according to Model 1 (b), Model 2 (b) and Model 3 (b), the regression coefficient of lagged R&D intensity (RDIt−1) for the operating performance indicators suggests that a 1% increase in lagged R&D intensity (RDIt−1) leads to a 0.031% increase in return on assets (ROA), a 0.046% increase in return on equity (ROE) and a 0.039% increase in return on sales (ROS). Moreover, the results for the control variables are in line with the initial expectations. The empirical results suggest a negative impact of R&D expenditures and a positive impact of lagged R&D expenditures on current operating performance regardless of different measurements (except for ROE, where the empirical results are not statistically significant) of operating performance.

Table 9.

Multiple regression results for the relationship between R&D expenditure and operating performance for the Slovenian high-tech companies.

Table 10 presents the empirical results for the relationship between R&D expenditures and operating performance for the Slovenian low-tech companies. The results show significant impact of R&D expenditures on return on assets (ROA) and return on equity (ROE) while the impact on return on sales (ROS) is not significant. According to Model 1 (a), Model 2 (a) and Model 3 (a), the regression coefficient of R&D intensity (RDIt) for operating performance indicators suggests that a 1% increase of R&D intensity (RDIt) leads to a 0.041% decrease in return on assets (ROA), a 0.099% decrease in return on equity (ROE) and a 0.030% decrease in return on sales (ROS). Furthermore, according to Model 1 (b), Model 2 (b) and Model 3 (b), the regression coefficient of lagged R&D intensity (RDIt−1) for the operating performance indicators suggests that a 1% increase in lagged R&D intensity (RDIt−1) leads to a 0.089% increase in return on assets (ROA), a 0.126% increase in return on equity (ROE) and a 0.040% decrease in return on sales (ROS). Moreover, the results for the control variables are in line with the initial expectations. The empirical results suggest a negative impact of R&D expenditures and a positive impact of lagged R&D expenditures on current operating performance regardless of different measurements (except for ROS, where the empirical results are not statistically significant) of operating performance.

Table 10.

Multiple regression results for the relationship between R&D expenditure and operating performance for the Slovenian low-tech companies.

Table 11 presents the empirical results for the relationship between R&D expenditures and operating performance for the world R&D companies. According to Model 4 (a), the significant regression coefficient of R&D intensity (RDIt) suggests that a 1% increase in R&D intensity (RDIt) leads to a decrease in return on sales (ROS), namely 1.162% for the total sample, 1.160% for the high-tech sample and 1.405% for the low-tech sample. Further, when examining the impact of R&D expenditures on future operating performance (Model 4 (b)), the regression coefficient of one-year lagged R&D intensity (RDIt−1) is positive and significant (except for low-tech sample). This indicates that a 1% increase in lagged R&D intensity (RDIt−1) leads to an increase in return on sales (ROS), namely 0.275% for the total sample, 0.279% for the high-tech sample and 0.210% for the low-tech sample. These results reveal that higher R&D intensity leads to a lower current operating performance and to a higher future operating performance. Moreover, the results for the control variables are in line with the initial expectations.

Table 11.

Regression results for the relationship between R&D expenditures and operating performance for the world R&D companies.

Based on the presented empirical results for the relationship between R&D expenditures and operating performance for the Slovenian and world R&D companies, the first research hypothesis (Hypothesis 1) stating that R&D expenditures deteriorate current operating performance and improve future operating performance is confirmed.

The empirical results for the relationship between R&D expenditures and market performance for the world R&D companies presented in Table 12 show the following. According to Model 5 (a), the regression coefficient for R&D intensity (RDIt) is positive and significant, thereby suggesting that a 1% increase in R&D intensity (RDIt) leads to an increase in the price-to-sales ratio (PSR), namely 3.155% for the total sample, 3.036% for the high-tech sample and 5.197% for the low-tech sample. Further, when examining the impact of R&D expenditures on market performance in the subsequent year (Model 5 (b)), the regression coefficient of one-year lagged R&D intensity (RDIt−1) suggests the following. A 1% increase in lagged R&D intensity (RDIt−1) leads to an increase in the price-to-sales ratio (PSR), namely 1.051% for the total sample, 1.115% for the high-tech sample and 4.394 for the low-tech sample. However, the regression coefficient is significant only for the low-tech sample. The results suggest that, while accounting profitability follows only one year after RDI, market returns are immediate and generally fade away after a year. Moreover, the results for the control variables are in line with the initial expectations.

Table 12.

Regression results for the relationship between R&D expenditures and market performance for the world R&D companies.

Based on the presented empirical results for the relationship between R&D expenditures and market performance for the world R&D companies, the second research hypothesis (Hypothesis 2) stating that R&D expenditures improve current and future market performance can be confirmed. However, it can be confirmed with certainty only for the relationship between R&D expenditures and current market performance, which is actually an approximation for long-term corporate performance.

5. Concluding Remarks

5.1. Discussion and Conclusion

This paper is focused on examining the impact of R&D expenditures on corporate performance. The results of the empirical study explain that R&D expenditures are an important determinant of operating and market performance. As regards operating performance, R&D expenditures have an adverse impact on current operating performance and a positive impact on future operating performance. The results are the same for the samples of Slovenian companies and world R&D companies operating in major world economies. This means that R&D expenditures hold similar implications for operating performance in those companies. Initially, the impact of R&D expenditures on operating performance is negative due to the insufficient profits that are generated, which are not high enough to exceed the R&D expenditure, and companies’ inability to provide innovation outcomes in the same year as R&D activity is performed. Later on, the impact of R&D expenditures on operating performance becomes positive, suggesting that after one year of R&D expenditures being made, companies may benefit from the scale production and marketing of their R&D outputs. Nevertheless, the comparison of the Slovenian and world R&D companies reveals that Slovenian companies have good potential to exploit R&D expenditures in terms of improving their future operating performance since they do not differ much or lag behind the world R&D companies with respect to the relationship between R&D expenditure and operating performance.

The utilisation of the dataset of world R&D companies listed on the stock exchange, allows for additional further insights into the relationship between R&D expenditures and market performance. The results show that R&D expenditures improve market performance, albeit this effect becomes non-significant for market performance in the subsequent year. This suggests that after one year, R&D expenditures become mature and do not impact market performance. Still, the results also support the idea that R&D expenditures are ineffective in the short run and bring certain benefits to companies in the long run, as suggested by market performance, which captures investors’ expectations of companies’ future earnings.

5.2. Theoretical and Practical Implications

The study results lend further empirical support to the main theoretical foundations commonly used to explain the impact of R&D expenditures on corporate performance. According to the resource-based theory, companies possess different unique resources to improve their corporate performance. Further, the knowledge-based theory highlights that R&D expenditures especially can be seen as a main driver of the generation of competitive advantage over competitors. The results suggest that higher levels of R&D intensity lead to lower levels of operating performance in the same year due to high uncertainty and risk. On the other hand, higher levels of R&D intensity lead to higher levels of operating performance in the future, which supports these two theories. This result is further supported by the positive impact of R&D expenditures on market performance as a measure of long-term corporate performance and supports the efficient market theory, which states that all kinds of investment should be immediately reflected in market performance. This implies that some time is needed to acquire the benefits of innovation outputs, indicating that R&D expenditures bring negative returns in the short term and positive returns in future periods. Thus, these findings provide new insights into the complex relationship between R&D expenditures and corporate performance and may be seen as a meaningful complement to existing empirical studies in this research area.

The findings of this study also hold several important practical implications. The overall findings suggest that a company should wait at least one year to obtain beneficial effects from an R&D investment in operating performance terms. On the other hand, market performance is enhanced in the year the R&D investment is made. These findings may be especially of use to managers, who are often inclined to pursue short-term goals and short-term corporate performance, which are not necessarily aimed at generating corporate performance in a future period. Namely, it is important that managers be aware that R&D investment does not bring an immediate positive effect on operating performance. The benefits of R&D investment on operating performance should become more evident in a future period. Therefore, focusing on short-term corporate performance should be used to justify managers not investing in R&D activities. Managers are recommended to exercise patience when investing in R&D activities since such investment is not instantly reflected in a better operating performance. At the same time, managers should be aware that R&D investment is positively valued by the market and immediately enhances market performance, which is often used to proxy for corporate performance in the long term. Briefly, in this case, managers are actually exposed to a trade-off between short- and long-term performance. This is why it is important that managers have a comprehensive picture of the effects of R&D investment on corporate performance because they can then take appropriate investment decisions on this basis. The results may also be beneficial for policymakers in order to stimulate R&D investment on the company level and to reduce the risk of such investment failing. This includes promoting R&D investment with appropriate public support mechanisms as well as establishing a stable and predictable business environment without unnecessary administrative barriers. This is crucial because R&D expenditures are expected to be a key determinant of the corporate performance of modern companies.

5.3. Limitations and Future Research

This paper offers new and interesting insights regarding the relationship between R&D spending and corporate performance. Yet, the paper also has some limitations that, while not diminishing its significance, should be seen as providing directions for future research. First, the research period for the sample of Slovenian companies is restricted to the period 2012–2016 and to 2015–2017 for the sample of world R&D companies. Therefore, one direction for future research is to extend the research period. This may provide additional empirical evidence on this research topic, especially during the recent economic crisis. The second limitation, somewhat touching on the limited research period, refers to the research methods adopted. Namely, the limited research period for Slovenian and world R&D companies makes it difficult to use sophisticated econometric approaches, as they often require a longer research period if credible empirical results are to be reached. Moreover, the use of sophisticated econometric approaches would allow the issue of endogeneity to be controlled, a possible concern while investigating the R&D spending/corporate performance relationship. Further, investigating the impact of R&D expenditures on corporate performance may engage the issue of reverse causality. This issue is partially controlled by lagging a suspected endogenous variable. Accordingly, a suggestion for further research is to use more sophisticated econometric approaches and techniques so as to reduce the bias of the empirical results. The third limitation is the lack of information on innovation, implying that the non-financial aspect of R&D expenditures is neglected in this study. Namely, the main obstacle for incorporating non-financial or qualitative research approach in the study is particularly strict financial data confidentiality for Slovenian companies, which unfortunately does not allow for identifying the companies in order to merge non-financial and financial data. Therefore, it would be very useful to conduct additional qualitative study by using surveys or interviews in order to obtain further insights beyond those obtainable only through financial data. Finally, this study does not account for different economic systems, which may hold important implications for the relationship between R&D expenditures and corporate performance. Namely, many business operations of top world R&D companies are often performed by their subsidiaries operating all over the world, which makes the identification of the appropriate institutional framework for these companies very hard. Accordingly, a direction for future research would be to consider economic characteristics in the separated study with the focus on subsidiaries.

Author Contributions

D.R. performed analysis and wrote the paper. A.A. supervised the work on the paper and revised it. All authors have read and agreed to the published version of the manuscript.

Acknowledgments

The authors acknowledge the financial support from the Slovenian Research Agency (research core funding No. P5-0093).

Conflicts of Interest

The authors declare no conflict of interest.

References

- Cadil, J.; Mirosnik, K.; Petkovova, L.; Mirvald, M. Public Support of Private R&D–Effects on Economic Sustainability. Sustainability 2018, 10, 4612. [Google Scholar] [CrossRef]

- Chang, S.C.; Chiu, S.C.; Wu, P.C. The Impact of Business Life Cycle and Performance Discrepancy on R&D Expenditures-Evidence from Taiwan. Account. Financ. Res. 2017, 6, 135–146. [Google Scholar] [CrossRef]

- Chung, H.; Eum, S.; Lee, C. Firm Growth and R&D in the Korean Pharmaceutical Industry. Sustainability 2019, 11, 2865. [Google Scholar] [CrossRef]

- Ravšelj, D.; Aristovnik, A. R&D Subsidies as Drivers of Corporate Performance in Slovenia: The Regional Perspective. Law Econ. Rev. 2017, 8, 79–95. [Google Scholar] [CrossRef]

- Ravšelj, D.; Aristovnik, A. The Impact of Private Research and Development Expenditures and Tax Incentives on Sustainable Corporate Growth in Selected OECD Countries. Sustainability 2018, 10, 2304. [Google Scholar] [CrossRef]

- Ravšelj, D.; Aristovnik, A. The Impact of Public R&D Subsidies and Tax Incentives on Business R&D Expenditures. Int. J. Econ. Bus. Adm. 2020, 8, 160–179. [Google Scholar]

- Sun, I.; Kim, S. Energy R&D towards sustainability: A panel analysis of government budget for energy R&D in OECD countries (1974–2012). Sustainability 2017, 9, 617. [Google Scholar] [CrossRef]

- Lee, N. R&D Accounting Treatment, R&D State and Tax Avoidance: With a Focus on Biotech Firms. Sustainability 2019, 11, 44. [Google Scholar] [CrossRef]

- Ravšelj, D.; Aristovnik, A. The Impact of R&D Accounting Treatment on Firm’s Market Value: Evidence from Germany. Soc. Sci. 2019, 14, 247–254. [Google Scholar] [CrossRef]

- Lang, A.; Murphy, H. Business and Sustainability: Between Government Pressure and Self-Regulation, 1st ed.; Springer: Berlin, Germany, 2014. [Google Scholar] [CrossRef]

- Doane, D.; MacGillivray, A. Economic Sustainability: The Business of Staying in Business; The SIGMA Project: Saint Louis, MO, USA, 2001. [Google Scholar]

- Hameed, T.; Von Staden, P.; Kwon, K. Sustainable Economic Growth and the Adaptability of a National System of Innovation: A Socio-Cognitive Explanation for South Korea’s Mired Technology Transfer and Commercialization Process. Sustainability 2018, 10, 1397. [Google Scholar] [CrossRef]

- Núñez-Cacho, P.; Molina-Moreno, V.; Corpas-Iglesias, F.A.; Cortés-García, F.J. Family Businesses Transitioning to a CircularEconomy Model: The Case of “Mercadona”. Sustainability 2018, 10, 538. [Google Scholar] [CrossRef]

- Barney, J.B. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Penrose, E.T. The Theory of Growth of the Firm; John Wiley: New York, NY, USA, 1959. [Google Scholar]

- Grant, R.M. Toward a knowledge-based theory of the firm. Strateg. Manag. J. 1996, 17, 109–122. [Google Scholar] [CrossRef]

- Malkiel, B.G.; Fama, E.F. Efficient capital markets: A review of theory and empirical work. J. Financ. 1970, 25, 383–417. [Google Scholar] [CrossRef]

- Apergis, N.; Sorros, J. The role of R&D expenses for profitability: Evidence from US fossil and renewable energy firms. Int. J. Econ. Financ. 2014, 6, 8–15. [Google Scholar] [CrossRef]

- Eberhart, A.C.; Maxwell, W.F.; Siddique, A.R. An examination of long-term abnormal stock returns and operating performance following R&D increases. J. Financ. 2004, 59, 623–650. [Google Scholar] [CrossRef]

- Shin, N.; Kraemer, K.L.; Dedrick, J. R&D, value chain location and firm performance in the global electronics industry. Ind. Innov. 2009, 16, 315–330. [Google Scholar] [CrossRef]

- Ayaydin, H.; Karaaslan, İ. The effect of research and development investment on firms’ financial performance: evidence from manufacturing firms in Turkey. J. Knowl. Econ. Knowl. Manag. 2014, 9, 43–59. [Google Scholar]

- Kiraci, M.; Celikay, F.; Celikay, D. The Effects of Firms’ R & D Expenditures on Profitability: An Analysis with Panel Error Correction Model for Turkey. Int. J. Bus. Soc. Sci. 2016, 7, 233–240. [Google Scholar]

- Busru, S.A.; Shanmugasundaram, G. Effects of Innovation Investment on Profitability and Moderating Role of Corporate Governance: Empirical Study of Indian Listed Firms. Indian J. Corp. Gov. 2017, 10, 97–117. [Google Scholar] [CrossRef]

- Rao, J.; Yu, Y.; Cao, Y. The effect that R&D has on company performance: Comparative analysis based on listed companies of technique intensive industry in China and Japan. Int. J. Educ. Res. 2013, 1, 1–8. [Google Scholar]

- Hsu, F.J.; Chen, M.Y.; Chen, Y.C.; Wang, W.C. An empirical study on the relationship between R&D and financial performance. J. Appl. Financ. Bank. 2013, 3, 107–119. [Google Scholar]

- Asthana, S.C.; Zhang, Y. Effect of R&D investments on persistence of abnormal earnings. Rev. Account. Financ. 2006, 5, 124–139. [Google Scholar] [CrossRef]

- Bae, S.C.; Noh, S. Multinational corporations versus domestic corporations: A comparative study of R&D investment activities. J. Multinatl. Financ. Manag. 2001, 11, 89–104. [Google Scholar] [CrossRef]

- Chan, K.; Chen, H.K.; Hong, L.H.; Wang, Y. Stock market valuation of R&D expenditures—The role of corporate governance. Pac. Basin Financ. J. 2015, 31, 78–93. [Google Scholar] [CrossRef]

- Ehie, I.C.; Olibe, K. The effect of R&D investment on firm value: An examination of US manufacturing and service industries. Int. J. Prod. Econ. 2010, 128, 127–135. [Google Scholar] [CrossRef]

- Ho, Y.K.; Keh, H.T.; Ong, J.M. The effects of R&D and advertising on firm value: An examination of manufacturing and nonmanufacturing firms. IEEE Trans. Eng. Manag. 2005, 52, 3–14. [Google Scholar] [CrossRef]

- Bae, S.C.; Kim, D. The effect of R&D investments on market value of firms: Evidence from the US, Germany, and Japan. Multinatl. Bus. Rev. 2003, 11, 51–76. [Google Scholar] [CrossRef]

- Wang, C.H. Clarifying the Effects of R&D on Performance: Evidence from the High Technology Industries. Asia Pac. Manag. Rev. 2011, 16, 51–64. [Google Scholar] [CrossRef]

- Duqi, A.; Mirti, R.; Torluccio, G. An analysis of the R&D effect on stock returns for European listed firms. Eur. J. Sci. Res. 2011, 58, 482–496. [Google Scholar]

- Başgoze, P.; Sayin, H.C. The effect of R&D expenditure (investments) on firm value: Case of Istanbul stock exchange. J. Bus. Econ. Financ. 2013, 2, 5–12. [Google Scholar]

- Cazavan-Jeny, A.; Jeanjean, T. The negative impact of R&D capitalization: A value relevance approach. Eur. Account. Rev. 2006, 15, 37–61. [Google Scholar] [CrossRef]

- Vithessonthi, C.; Racela, O.C. Short-and long-run effects of internationalization and R&D intensity on firm performance. J. Multinatl. Financ. Manag. 2016, 34, 28–45. [Google Scholar] [CrossRef]

- Usman, M.; Shaique, M.; Khan, S.; Shaikh, R.; Baig, N. Impact of R&D investment on firm performance and firm value: Evidence from developed nations (G-7). RGFC 2017, 7, 302–321. [Google Scholar] [CrossRef]

- Statistical office of the Republic of Slovenia (SORS). Microdata on R&D Activity of Slovenian Companies; SORS: Ljubljana, Slovenia, 2018. [Google Scholar]

- European Commission. The 2017 EU Industrial R&D Investment Scoreboard; European Commission: Brussels, Belgium, 2017. [Google Scholar]

- European Commission. The 2018 EU Industrial R&D Investment Scoreboard; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- Hitt, M.A.; Hoskisson, R.E.; Kim, H. International diversification: Effects on innovation and firm performance in product-diversified firms. Acad. Manag. J. 1997, 40, 767–798. [Google Scholar] [CrossRef]

- Grant, R.M. Multinationality and performance among British manufacturing companies. J. Int. Bus. Stud. 1987, 18, 79–89. [Google Scholar] [CrossRef]

- Geringer, J.M.; Tallman, S.; Olsen, D.M. Product and international diversification among Japanese multinational firms. Strateg. Manag. J. 2000, 21, 51–80. [Google Scholar] [CrossRef]

- Robins, J.; Wiersema, M.F. A resource-based approach to the multibusiness firm: Empirical analysis of portfolio interrelationships and corporate financial performance. Strateg. Manag. J. 1995, 16, 277–299. [Google Scholar] [CrossRef]

- Al-Matari, E.M.; Al-Swidi, A.K.; Fadzil, F.H. The measurements of firm performance’s dimensions. AJFA 2014, 6, 24–49. [Google Scholar] [CrossRef]

- Leibowitz, M.L. The levered P/E ratio. Financ. Anal. J. 2002, 58, 68–77. [Google Scholar] [CrossRef]

- Vruwink, D.R.; Quirin, J.J.; O’Bryan, D. A Modified Price-Sales Ratio: A Useful Tool For Investors? J. Bus. Econ. Res. 2007, 5, 31–40. [Google Scholar] [CrossRef][Green Version]

- Fisher, K.L. Super Stocks; Dow Jones-Irwin: Homewood, IL, USA, 1984. [Google Scholar]

- Czarnitzki, D.; Delanote, J. R&D policies for young SMEs: Input and output effects. Small Bus. Econ. 2015, 45, 465–485. [Google Scholar] [CrossRef]

- González, X.; Jaumandreu, J.; Pazó, C. Barriers to innovation and subsidy effectiveness. RAND J. Econ. 2005, 36, 930–950. [Google Scholar]

- Klette, T.J.; Møen, J. From Growth Theory to Technology Policy-Coordination Problems in Theory and Practice; Discussion Paper No. 219; Statistics Norway Research Department: Oslo, Norway, 1998. [Google Scholar]

- Asimakopoulos, I.; Samitas, A.; Papadogonas, T. Firm-specific and economy wide determinants of firm profitability: Greek evidence using panel data. Manag. Financ. 2009, 35, 930–939. [Google Scholar] [CrossRef]

- Nunes, P.J.; Serrasqueiro, Z.M.; Sequeira, T.N. Profitability in Portuguese service industries: A panel data approach. Serv. Ind. J. 2009, 29, 693–707. [Google Scholar] [CrossRef]

- Goddard, J.; Tavakoli, M.; Wilson, J.O. Determinants of profitability in European manufacturing and services: Evidence from a dynamic panel model. Appl. Financ. Econ. 2005, 15, 1269–1282. [Google Scholar] [CrossRef]

- Jovanovic, B. Selection and the Evolution of Industry. Econometrica 1982, 50, 649–670. [Google Scholar] [CrossRef]

- Lee, J. Does size matter in firm performance? Evidence from US public firms. Int. J. Econ. Bus. 2009, 16, 189–203. [Google Scholar] [CrossRef]

- Yazdanfar, D. Profitability determinants among micro firms: Evidence from Swedish data. Int. J. Manag. Financ. 2013, 9, 151–160. [Google Scholar] [CrossRef]

- Titman, S.; Wessels, R. The determinants of capital structure choice. J. Financ. 1988, 43, 1–19. [Google Scholar] [CrossRef]

- King, A.; Lenox, M. Exploring the locus of profitable pollution reduction. Manag. Sci. 2002, 48, 289–299. [Google Scholar] [CrossRef]

- Manrique, S.; Martí-Ballester, C.P. Analyzing the effect of corporate environmental performance on corporate financial performance in developed and developing countries. Sustainability 2017, 9, 1957. [Google Scholar] [CrossRef]

- Russo, M.V.; Fouts, P.A. A resource-based perspective on corporate environmental performance and profitability. Acad. Manag. J. 1997, 40, 534–559. [Google Scholar] [CrossRef]

- Chung, K.H.; Wright, P.; Charoenwong, C. Investment opportunities and market reaction to capital expenditure decisions. J. Bank. Financ. 1998, 22, 41–60. [Google Scholar] [CrossRef]

- Kim, W.; Park, K.; Lee, S.; Kim, H. R&D Investments and Firm Value: Evidence from China. Sustainability 2018, 10, 4133. [Google Scholar] [CrossRef]

- Torres-Reyna, O. Panel Data Analysis Fixed and Random Effects Using STATA (v. 4.2). 2007. Available online: https://www.princeton.edu/~otorres/Panel101.pdf (accessed on 25 February 2019).

- Hausman, J.A. Specification tests in econometrics. Econometrica 1978, 46, 1251–1271. [Google Scholar] [CrossRef]

- Lee, S. Growth, profits and R&D investment. Econ. Res. Ekon. Istraz. 2018, 31, 607–625. [Google Scholar] [CrossRef]

- Washington, S.P.; Karlaftis, M.G.; Mannering, F. Statistical and Econometric Methods for Transportation Data Analysis, 2nd ed.; Chapman and Hall: London, UK, 2010. [Google Scholar]

- Reifman, A.; Keyton, K. Winsorize. Encyclopedia of Research Design; Salkind, N.J., Ed.; Sage: Thousand Oaks, CA, USA, 2010; pp. 1636–1638. [Google Scholar]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).