Process Innovation as a Moderator Linking Sustainable Supply Chain Management with Sustainable Performance in the Manufacturing Sector of Pakistan

Abstract

:1. Introduction

2. Literature Review

SSCM Practices

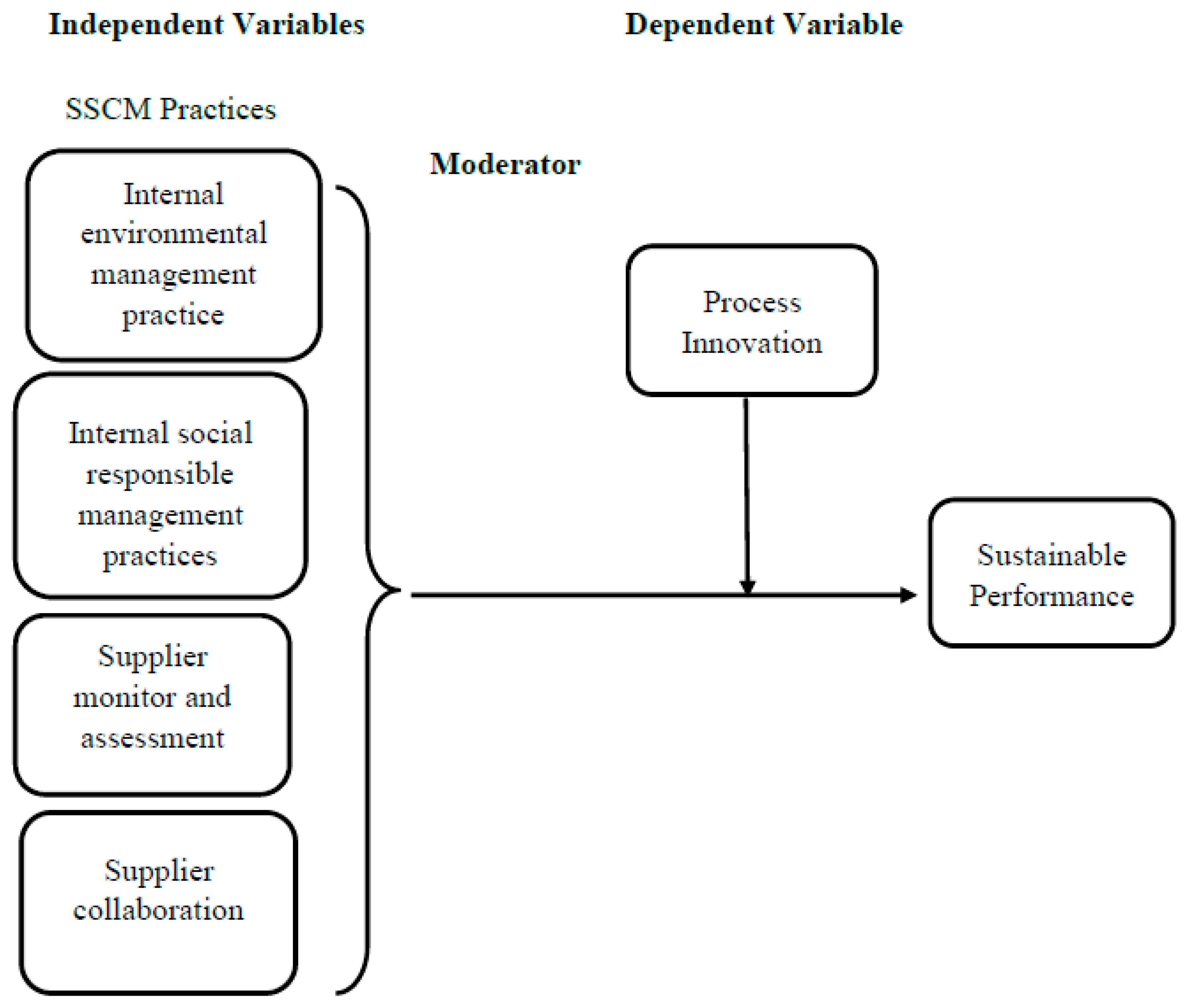

3. Research Framework and Hypotheses

3.1. Internal Environmental Management Practices and a Firm’s Sustainable Performance

3.2. Internal Social Responsible Management and Firm Sustainable Performance

External Supplier Management and Firm Sustainable Performance

3.3. Supplier Monitor and Assessment and a Firm’s Sustainable Performance

3.4. Supplier Collaboration and a Firm’s Sustainable Performance

3.5. Technological Innovation as a Moderator Between SSCM Practices and a Firm’s Sustainable Performance

4. Methodology

5. Data Analysis and Discussion

5.1. Measurement Model

Establishment of the Higher-Order Constructs

5.2. Moderation Test

Interaction Plot

5.3. Assessment of the Variance Explained in the Endogenous Latent Variables

5.4. Assessment of Effect Size (f²)

6. Conclusions and Managerial Implications

Research Limitations and Future Research

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Nieuwenhuis, P.; Touboulic, A.; Matthews, L. Is Sustainable Supply Chain Management Sustainable? In Sustainable Development Goals and Sustainable Supply Chains in the Post-Global Economy; Springer: Berlin/Heidelberg, Germany, 2019; pp. 13–30. [Google Scholar]

- Seuring, S.; Müller, M. From a literature review to a conceptual framework for sustainable supply chain management. J. Clean. Prod. 2008, 16, 1699–1710. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- Kiron, D.; Kruschwitz, N.; Haanaes, K.; von Streng Velken, I. Sustainability nears a tipping point. Mit Sloan Manag. Rev. 2012, 53, 69–74. [Google Scholar] [CrossRef]

- Eklington, J. Cannibals with Forks: The Triple Bottom Line of the 21st Century; New Society Publishers: Stoney Creek, CT, USA, 1998. [Google Scholar]

- Elkington, J. Enter the triple bottom line. In The Triple Bottom Line: Does It All Add Up? Henriques, A., Richardson, J., Eds.; Earth Scan: London, UK, 2004. [Google Scholar]

- Fera, M.; Fruggiero, F.; Lambiase, A.; Macchiaroli, R.; Miranda, S. The role of uncertainty in supply chains under dynamic modeling. Int. J. Ind. Eng. Comput. 2017, 8, 119–140. [Google Scholar] [CrossRef]

- Nagel, M.H. Environmental supply-chain management versus green procurement in the scope of a business and leadership perspective. In Proceedings of the IEEE International Symposium on Electronics and the Environment, San Francisco, CA, USA, 10 May 2000; pp. 219–224. [Google Scholar]

- Khan, S.Z.; Yang, Q.; Waheed, A. Investment in intangible resources and capabilities spurs sustainable competitive advantage and firm performance. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 285–295. [Google Scholar] [CrossRef]

- Almeida, M.F.L.d.; Melo, M.A.C.d. Sociotechnical regimes, technological innovation and corporate sustainability: From principles to action. Technol. Anal. Strateg. Manag. 2017, 29, 395–413. [Google Scholar] [CrossRef]

- Grewatsch, S.; Kleindienst, I. When does it pay to be good? Moderators and mediators in the corporate sustainability–corporate financial performance relationship: A critical review. J. Bus. Ethics 2017, 145, 383–416. [Google Scholar] [CrossRef]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The impact of corporate sustainability on organizational processes and performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef] [Green Version]

- Tipu, S.A.A.; Fantazy, K. Exploring the relationships of strategic entrepreneurship and social capital to sustainable supply chain management and organizational performance. Int. J. Product. Perform. Manag. 2018, 67, 2046–2070. [Google Scholar] [CrossRef]

- Rathore, P.; Kota, S.; Chakrabarti, A. Sustainability through remanufacturing in India: A case study on mobile handsets. J. Clean. Prod. 2011, 19, 1709–1722. [Google Scholar] [CrossRef]

- Zahidi, F. Solid Waste Management in Pakistan; ALJAZEERA News: Qatar, Doha, 2016. [Google Scholar]

- Puertas, R.; Martí, L.; García, L. Logistics performance and export competitiveness: European experience. Empirica 2014, 41, 467–480. [Google Scholar] [CrossRef]

- Arkader, R.; Ferreira, C.F. Category management initiatives from the retailer perspective: A study in the Brazilian grocery retail industry. J. Purch. Supply Manag. 2004, 10, 41–51. [Google Scholar] [CrossRef]

- Ehsan, S.; Nazir, M.; Nurunnabi, M.; Raza Khan, Q.; Tahir, S.; Ahmed, I. A Multimethod Approach to Assess and Measure Corporate Social Responsibility Disclosure and Practices in a Developing Economy. Sustainability 2018, 10, 2955. [Google Scholar] [CrossRef] [Green Version]

- Javeed, S.; Lefen, L. An Analysis of Corporate Social Responsibility and Firm Performance with Moderating Effects of CEO Power and Ownership Structure: A Case Study of the Manufacturing Sector of Pakistan. Sustainability 2019, 11, 248. [Google Scholar] [CrossRef] [Green Version]

- Buckley, P.J.; Doh, J.P.; Benischke, M.H. Towards a renaissance in international business research? Big questions, grand challenges, and the future of IB scholarship. J. Int. Bus. Stud. 2017, 48, 1045–1064. [Google Scholar]

- Visser, W. Corporate social responsibility in developing countries. In The Oxford Handbook of Corporate Social Responsibility; Oxford University Press: Oxford, UK, 2008. [Google Scholar]

- Waqas, M.; Dong, Q.-l.; Ahmad, N.; Zhu, Y.; Nadeem, M. Critical Barriers to Implementation of Reverse Logistics in the Manufacturing Industry: A Case Study of a Developing Country. Sustainability 2018, 10, 4202. [Google Scholar] [CrossRef] [Green Version]

- Carter, C.R.; Jennings, M.M. Logistics social responsibility: An integrative framework. J. Bus. Logist. 2002, 23, 145–180. [Google Scholar] [CrossRef]

- Sila, I.; Ebrahimpour, M.; Birkholz, C. Quality in supply chains: An empirical analysis. Supply Chain Manag. Int. J. 2006, 11, 491–502. [Google Scholar] [CrossRef]

- Elcio, M.T.; Yew Wong, C. Towards a theory of multi-tier sustainable supply chains: A systematic literature review. Supply Chain Manag. Int. J. 2014, 19, 643–663. [Google Scholar]

- Croom, S.; Vidal, N.; Spetic, W.; Marshall, D.; McCarthy, L. Impact of social sustainability orientation and supply chain practices on operational performance. Int. J. Oper. Prod. Manag. 2018, 38, 2344–2366. [Google Scholar] [CrossRef] [Green Version]

- Feng, M.; Yu, W.; Wang, X.; Wong, C.Y.; Xu, M.; Xiao, Z. Green supply chain management and financial performance: The mediating roles of operational and environmental performance. Bus. Strategy Environ. 2018, 27, 811–824. [Google Scholar] [CrossRef] [Green Version]

- Hong, J.; Zhang, Y.; Ding, M. Sustainable supply chain management practices, supply chain dynamic capabilities, and enterprise performance. J. Clean. Prod. 2018, 172, 3508–3519. [Google Scholar] [CrossRef]

- Wang, J.; Dai, J. Sustainable supply chain management practices and performance. Ind. Manag. Data Syst. 2018, 118, 2–21. [Google Scholar] [CrossRef]

- Khan, S.A.R.; Qianli, D. Impact of green supply chain management practices on firms′ performance: An empirical study from the perspective of Pakistan. Environ. Sci. Pollut. Res. 2017, 24, 16829–16844. [Google Scholar] [CrossRef] [PubMed]

- Calantone, R.J.; Cavusgil, S.T.; Zhao, Y. Learning orientation, firm innovation capability, and firm performance. Ind. Mark. Manag. 2002, 31, 515–524. [Google Scholar] [CrossRef]

- Tsai, K.-H. The impact of technological capability on firm performance in Taiwan′s electronics industry. J. High Technol. Manag. Res. 2004, 15, 183–195. [Google Scholar] [CrossRef]

- Foo, P.-Y.; Lee, V.-H.; Tan, G.W.-H.; Ooi, K.-B. A gateway to realising sustainability performance via green supply chain management practices: A PLS–ANN approach. Expert Syst. Appl. 2018, 107, 1–14. [Google Scholar] [CrossRef]

- Sajjad, A.; Eweje, G. Corporate social responsibility in Pakistan: Current trends and future directions. In Corporate Social Responsibility and Sustainability: Emerging Trends in Developing Economies; Emerald Group Publishing Limited: Bingley, UK, 2014; pp. 163–187. [Google Scholar]

- Wittstruck, D.; Teuteberg, F. Understanding the success factors of sustainable supply chain management: Empirical evidence from the electrics and electronics industry. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 141–158. [Google Scholar] [CrossRef]

- Hsu, C.-C.; Tan, K.-C.; Mohamad Zailani, S.H. Strategic orientations, sustainable supply chain initiatives, and reverse logistics: Empirical evidence from an emerging market. Int. J. Oper. Prod. Manag. 2016, 36, 86–110. [Google Scholar] [CrossRef]

- Seth, D.; Shrivastava, R.; Shrivastava, S. An empirical investigation of critical success factors and performance measures for green manufacturing in cement industry. J. Manuf. Technol. Manag. 2016, 27, 1076–1101. [Google Scholar] [CrossRef]

- Kaynak, H.; Hartley, J.L. A replication and extension of quality management into the supply chain. J. Oper. Manag. 2008, 26, 468–489. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J.; Lai, K.-H. Institutional-based antecedents and performance outcomes of internal and external green supply chain management practices. J. Purch. Supply Manag. 2013, 19, 106–117. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J.; Lai, K.-H. Confirmation of a measurement model for green supply chain management practices implementation. Int. J. Prod. Econ. 2008, 111, 261–273. [Google Scholar] [CrossRef]

- Zailani, S.; Jeyaraman, K.; Vengadasan, G.; Premkumar, R. Sustainable supply chain management (SSCM) in Malaysia: A survey. Int. J. Prod. Econ. 2012, 140, 330–340. [Google Scholar] [CrossRef]

- Green, K.W., Jr.; Zelbst, P.J.; Meacham, J.; Bhadauria, V.S. Green supply chain management practices: Impact on performance. Supply Chain Manag. Int. J. 2012, 17, 290–305. [Google Scholar] [CrossRef]

- Zsidisin, G.A.; Siferd, S.P. Environmental purchasing: A framework for theory development. Eur. J. Purch. Supply Manag. 2001, 7, 61–73. [Google Scholar] [CrossRef]

- Eriksson, D.; Svensson, G. Elements affecting social responsibility in supply chains. Supply Chain Manag. Int. J. 2015, 20, 561–566. [Google Scholar] [CrossRef]

- Busse, C.; Schleper, M.C.; Niu, M.; Wagner, S.M. Supplier development for sustainability: Contextual barriers in global supply chains. Int. J. Phys. Distrib. Logist. Manag. 2016, 46, 442–468. [Google Scholar] [CrossRef]

- Kytle, B.; Ruggie, J.G. Corporate Social Responsibility as Risk Management; Working Paper No. 10; Harvard University Press: Cambridge, MA, USA, 2005. [Google Scholar]

- Damanpour, F.; Evan, W.M. Organizational innovation and performance: The problem of “organizational lag”. Adm. Sci. Q. 1984, 392–409. [Google Scholar] [CrossRef]

- Singh, R.; Mathiassen, L.; Mishra, A. Organizational Path Constitution in Technological Innovation: Evidence from Rural. Telehealth MIS Q. 2015, 39, 643–665. [Google Scholar] [CrossRef]

- Coccia, M. Sources of technological innovation: Radical and incremental innovation problem-driven to support competitive advantage of firms. Technol. Anal. Strateg. Manag. 2017, 29, 1048–1061. [Google Scholar] [CrossRef]

- Anwar, M. Business model innovation and SMEs performance—Does competitive advantage mediate? Int. J. Innov. Manag. 2018, 22, 1850057. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Camisón, C.; Villar-López, A. Organizational innovation as an enabler of technological innovation capabilities and firm performance. J. Bus. Res. 2014, 67, 2891–2902. [Google Scholar] [CrossRef]

- Li, Y.; Zhao, Y.; Liu, Y. The relationship between HRM, technology innovation and performance in China. Int. J. Manpow. 2006, 27, 679–697. [Google Scholar] [CrossRef] [Green Version]

- Ordanini, A.; Rubera, G. How does the application of an IT service innovation affect firm performance? A theoretical framework and empirical analysis on e-commerce. Inf. Manag. 2010, 47, 60–67. [Google Scholar] [CrossRef]

- Miller, D.J.; Fern, M.J.; Cardinal, L.B. The use of knowledge for technological innovation within diversified firms. Acad. Manag. J. 2007, 50, 307–325. [Google Scholar] [CrossRef] [Green Version]

- Sirilli, G.; Evangelista, R. Technological innovation in services and manufacturing: Results from Italian surveys. Res. Policy 1998, 27, 881–899. [Google Scholar] [CrossRef]

- Ryu, H. The relationship between non-technological innovation and technological innovation on firm performance. Adv. Sci. Technol. Lett. 2016, 135, 27–32. [Google Scholar]

- Peteraf, M.A. The cornerstones of competitive advantage: A resource-based view. Strateg. Manag. J. 1993, 14, 179–191. [Google Scholar] [CrossRef]

- Wernerfelt, B. A resource-based view of the firm. Strateg. Manag. J. 1984, 5, 171–180. [Google Scholar] [CrossRef]

- Alvarez, S.A.; Barney, J.B. Resource-based theory and the entrepreneurial firm. Strateg. Entrep. Creat. 2017, 87–105. [Google Scholar] [CrossRef]

- Barney, J.B.; Arikan, A.M. The resource-based view: Origins and implications. Handb. Strateg. Manag. 2001, 124188. [Google Scholar] [CrossRef]

- Grant, R.M. The resource-based theory of competitive advantage: Implications for strategy formulation. Calif. Manag. Rev. 1991, 33, 114–135. [Google Scholar] [CrossRef] [Green Version]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar]

- Hussain, S.T.; Khan, U.; Malik, K.Z.; Faheem, A. Constraints Faced by Industry in Punjab, Pakistan. Lahore J. Econ. 2012, 17, 135–189. [Google Scholar] [CrossRef]

- Krause, D.R.; Handfield, R.B.; Tyler, B.B. The relationships between supplier development, commitment, social capital accumulation and performance improvement. J. Oper. Manag. 2007, 25, 528–545. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J. Relationships between operational practices and performance among early adopters of green supply chain management practices in Chinese manufacturing enterprises. J. Oper. Manag. 2004, 22, 265–289. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J.; Geng, Y. Green supply chain management in China: Pressures, practices and performance. Int. J. Oper. Prod. Manag. 2005, 25, 449–468. [Google Scholar] [CrossRef]

- Beske, P.; Seuring, S. Putting sustainability into supply chain management. Supply Chain Manag. Int. J. 2014, 19, 322–331. [Google Scholar] [CrossRef]

- Rao, P.; Holt, D. Do green supply chains lead to competitiveness and economic performance? Int. J. Oper. Prod. Manag. 2005, 25, 898–916. [Google Scholar] [CrossRef]

- Florida, R. Lean and green: The move to environmentally conscious manufacturing. Calif. Manag. Rev. 1996, 39, 80–105. [Google Scholar] [CrossRef]

- Kolk, A. The social responsibility of international business: From ethics and the environment to CSR and sustainable development. J. World Bus. 2016, 51, 23–34. [Google Scholar] [CrossRef]

- Marshall, R.S.; Cordano, M.; Silverman, M. Exploring individual and institutional drivers of proactive environmentalism in the US wine industry. Bus. Strategy Environ. 2005, 14, 92–109. [Google Scholar] [CrossRef]

- Walker, H.; Jones, N. Sustainable supply chain management across the UK private sector. Supply Chain Manag. Int. J. 2012, 17, 15–28. [Google Scholar] [CrossRef]

- Bowen, F.E.; Cousins, P.D.; Lamming, R.C.; Farukt, A.C. The role of supply management capabilities in green supply. Prod. Oper. Manag. 2001, 10, 174–189. [Google Scholar] [CrossRef]

- Gimenez, C.; Sierra, V. Sustainable supply chains: Governance mechanisms to greening suppliers. J. Bus. Ethics 2013, 116, 189–203. [Google Scholar] [CrossRef]

- Lamming, R.; Hampson, J. The environment as a supply chain management issue. Br. J. Manag. 1996, 7, S45–S62. [Google Scholar] [CrossRef]

- Vachon, S.; Klassen, R.D. Extending green practices across the supply chain: The impact of upstream and downstream integration. Int. J. Oper. Prod. Manag. 2006, 26, 795–821. [Google Scholar] [CrossRef]

- Pagell, M.; Gobeli, D. How plant managers′ experiences and attitudes toward sustainability relate to operational performance. Prod. Oper. Manag. 2009, 18, 278–299. [Google Scholar] [CrossRef]

- Baird, P.L.; Geylani, P.C.; Roberts, J.A. Corporate social and financial performance re-examined: Industry effects in a linear mixed model analysis. J. Bus. Ethics 2012, 109, 367–388. [Google Scholar] [CrossRef]

- Alexander, G.J.; Buchholz, R.A. Corporate social responsibility and stock market performance. Acad. Manag. J. 1978, 21, 479–486. [Google Scholar] [CrossRef]

- Turban, D.B.; Greening, D.W. Corporate social performance and organizational attractiveness to prospective employees. Acad. Manag. J. 1997, 40, 658–672. [Google Scholar]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Li, F.; Li, T.; Minor, D. CEO power, corporate social responsibility, and firm value: A test of agency theory. Int. J. Manag. Financ. 2016, 12, 611–628. [Google Scholar] [CrossRef]

- Wang, J.; Zhang, Y.; Goh, M. Moderating the role of firm size in sustainable performance improvement through sustainable supply chain management. Sustainability 2018, 10, 1654. [Google Scholar] [CrossRef] [Green Version]

- Damanpour, F.; Walker, R.M.; Avellaneda, C.N. Combinative effects of innovation types and organizational performance: A longitudinal study of service organizations. J. Manag. Stud. 2009, 46, 650–675. [Google Scholar] [CrossRef]

- Galende, J.; de la Fuente, J.M. Internal factors determining a firm′s innovative behaviour. Res. Policy 2003, 32, 715–736. [Google Scholar] [CrossRef]

- Mol, M.J.; Birkinshaw, J. The sources of management innovation: When firms introduce new management practices. J. Bus. Res. 2009, 62, 1269–1280. [Google Scholar] [CrossRef] [Green Version]

- Yang, C.-C.; Marlow, P.B.; Lu, C.-S. Assessing resources, logistics service capabilities, innovation capabilities and the performance of container shipping services in Taiwan. Int. J. Prod. Econ. 2009, 122, 4–20. [Google Scholar] [CrossRef]

- Coombs, J.E.; Bierly, P.E. Looking through the kalidescope: Measuring technological capability and performance. Acad. Manag. 2017, B1–B6. [Google Scholar] [CrossRef]

- Coombs, J.E.; Bierly, P.E. Measuring technological capability and performance. Res. Dev. Manag. 2006, 36, 421–438. [Google Scholar] [CrossRef]

- Nuria, G.-A.; Mariano, N.-A. Protection and internal transfer of technological competencies: The role of causal ambiguity. Ind. Manag. Data Syst. 2005, 105, 841–856. [Google Scholar]

- Teece, D.J.; Pisano, G.; Shuen, A. Dynamic capabilities and strategic management. Strateg. Manag. J. 1997, 18, 509–533. [Google Scholar] [CrossRef]

- Ortega, M.J.R. Competitive strategies and firm performance: Technological capabilities′ moderating roles. J. Bus. Res. 2010, 63, 1273–1281. [Google Scholar] [CrossRef]

- Damanpour, F. An integration of research findings of effects of firm size and market competition on product and process innovations. Br. J. Manag. 2010, 21, 996–1010. [Google Scholar] [CrossRef]

- Bessant, J.; Lamming, R.; Noke, H.; Phillips, W. Managing innovation beyond the steady state. Technovation 2005, 25, 1366–1376. [Google Scholar] [CrossRef]

- Martinez-Ros, E. Explaining the decisions to carry out product and process innovations: The Spanish case. J. High Technol. Manag. Res. 1999, 10, 223–242. [Google Scholar] [CrossRef] [Green Version]

- Porter, M.E. Competitive Advantage: Creating and Sustaining Superior Performance; Free Press: New York, NY, USA, 1985. [Google Scholar]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill Building Approach; John Wiley & Sons: Hoboken, NJ, USA, 2016. [Google Scholar]

- Carter, C.R.; Kale, R.; Grimm, C.M. Environmental purchasing and firm performance: An empirical investigation. Transp. Res. Part E Logist. Transp. Rev. 2000, 36, 219–228. [Google Scholar] [CrossRef]

- Yu, W.; Chavez, R.; Feng, M.; Wiengarten, F. Integrated green supply chain management and operational performance. Supply Chain Manag. Int. J. 2014, 19, 683–696. [Google Scholar] [CrossRef]

- Dang, S.; Chu, L. Evaluation framework and verification for sustainable container management as reusable packaging. J. Bus. Res. 2016, 69, 1949–1955. [Google Scholar] [CrossRef]

- Zsidisin, G.A.; Hendrick, T.E. Purchasing′s involvement in environmental issues: A multi-country perspective. Ind. Manag. Data Syst. 1998, 98, 313–320. [Google Scholar] [CrossRef]

- Emmelhainz, M.A.; Adams, R.J. The apparel industry response to “sweatshop” concerns: A review and analysis of codes of conduct. J. Supply Chain Manag. 1999, 35, 51–57. [Google Scholar] [CrossRef]

- Krause, D.R.; Scannell, T.V.; Calantone, R.J. A structural analysis of the effectiveness of buying firms′ strategies to improve supplier performance. Decis. Sci. 2000, 31, 33–55. [Google Scholar] [CrossRef]

- Claudia, N.; Rainer, L.; Florian, K. Integrating sustainability into strategic supplier portfolio selection. Manag. Decis. 2016, 54, 194–221. [Google Scholar]

- Tuominen, M.; Hyvönen, S. Organizational innovation capability: A driver for competitive superiority in marketing channels. Int. Rev. Retail Distrib. Consum. Res. 2004, 14, 277–293. [Google Scholar] [CrossRef]

- Camisón, C.; Villar López, A. An examination of the relationship between manufacturing flexibility and firm performance: The mediating role of innovation. Int. J. Oper. Prod. Manag. 2010, 30, 853–878. [Google Scholar] [CrossRef]

- Daily, B.F.; Bishop, J.W.; Steiner, R. The mediating role of EMS teamwork as it pertains to HR factors and perceived environmental performance. J. Appl. Bus. Res. JABR 2007, 23, 95–109. [Google Scholar] [CrossRef] [Green Version]

- Kassinis, G.I.; Soteriou, A.C. Greening the service profit chain: The impact of environmental management practices. Prod. Oper. Manag. 2003, 12, 386–403. [Google Scholar] [CrossRef] [Green Version]

- Gimenez, C.; Sierra, V.; Rodon, J. Sustainable operations: Their impact on the triple bottom line. Int. J. Prod. Econ. 2012, 140, 149–159. [Google Scholar] [CrossRef]

- Peng, D.X.; Lai, F. Using partial least squares in operations management research: A practical guideline and summary of past research. J. Oper. Manag. 2012, 30, 467–480. [Google Scholar] [CrossRef]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. Partial least squares structural equation modeling: Rigorous applications, better results and higher acceptance. Long Range Plan. 2013, 46, 1–12. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage Publications: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Hair, J.F., Jr.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V.G. Partial least squares structural equation modeling (PLS-SEM). Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis: A Global Perspective, 7th ed.; Prentice-Hall: Upper Saddle River, NJ, USA, 2010. [Google Scholar]

- Henseler, J.; Ringle, C.M.; Sinkovics, R.R. The use of partial least squares path modeling in international marketing. In New Challenges to International Marketing; Emerald Group Publishing Limited: Bingley, UK, 2009. [Google Scholar]

- Hair, J.F.; Sarstedt, M.; Ringle, C.M.; Mena, J.A. An assessment of the use of partial least squares structural equation modeling in marketing research. J. Acad. Mark. Sci. 2012, 40, 414–433. [Google Scholar] [CrossRef]

- Duarte, P.A.O.; Raposo, M.L.B. A PLS model to study brand preference: An application to the mobile phone market. In Handbook of Partial Least Squares; Springer: Berlin/Heidelberg, Germany, 2010; pp. 449–485. [Google Scholar]

- Hulland, J. Use of partial least squares (PLS) in strategic management research: A review of four recent studies. Strateg. Manag. J. 1999, 20, 195–204. [Google Scholar] [CrossRef]

- Bijttebier, P.; Delva, D.; Vanoost, S.; Bobbaers, H.; Lauwers, P.; Vertommen, H. Reliability and validity of the Critical Care Family Needs Inventory in a Dutch-speaking Belgian sample. Heart Lung 2000, 29, 278–286. [Google Scholar] [CrossRef] [Green Version]

- Sun, W.; Chou, C.-P.; Stacy, A.W.; Ma, H.; Unger, J.; Gallaher, P. SAS and SPSS macros to calculate standardized Cronbach′s alpha using the upper bound of the phi coefficient for dichotomous items. Behav. Res. Methods 2007, 39, 71–81. [Google Scholar] [CrossRef] [Green Version]

- Bacon, D.R.; Sauer, P.L.; Young, M. Composite reliability in structural equations modeling. Educ. Psychol. Meas. 1995, 55, 394–406. [Google Scholar] [CrossRef]

- Bagozzi, R.P.; Yi, Y. On the evaluation of structural equation models. J. Acad. Mark. Sci. 1988, 16, 74–94. [Google Scholar] [CrossRef]

- Chin, W.W. The partial least squares approach to structural equation modeling. Mod. Methods Bus. Res. 1998, 295, 295–336. [Google Scholar]

- Henseler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar] [CrossRef] [Green Version]

- Henseler, J.; Fassott, G. Testing moderating effects in PLS path models: An illustration of available procedures. In Handbook of Partial Least Squares; Vinzi, V.E., Chin, W.W., Henseler, H., Wang, J., Eds.; Springer: London, UK, 2010; pp. 713–735. [Google Scholar]

- Hayes, A.F. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach, 1st ed.; Guilford Press: New York, NY, USA, 2013. [Google Scholar]

- Dawson, J.F. Moderation in management research: What, why, when, and how. J. Bus. Psychol. 2014, 29, 1–19. [Google Scholar] [CrossRef]

- Falk, R.F.; Miller, N.B. A Primer for Soft Modeling; University of Akron Press: Akron, OH, USA, 1992. [Google Scholar]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences; Lawrence Erlbaum Associates: Hillsdale, NJ, USA, 1988. [Google Scholar]

- Callaghan, W.; Wilson, B.; Ringle, C.M.; Henseler, J. Exploring causal path directionality for a marketing model using Cohen′s path method. In Proceedings of the PLS′07 International Symposium on PLS and Related Methods Causalities Explored by Indirect Observation, Ås, Norway, 5–7 September 2007. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Construct | Items | Loadings | CR | AVE | VIF | |

|---|---|---|---|---|---|---|

| Internal Environment Management | ||||||

| Product Echo-Design | PED_1 PED_2 PED_3 PED_4 PED_5 PED_6 PED_7 | 0.780 0.743 0.776 0.774 0.709 0.782 0.840 | 0.912 | 0.597 | 1.955 1.799 1.917 2.012 1.546 2.077 2.281 | |

| Sustainable Packaging Product | SPP_1 SPP_2 SPP_3 SPP_4 SPP_5 SPP_6 | 0.758 0.797 0.763 0.643 0.752 0.758 | 0.883 | 0.558 | 1.735 1.966 1.796 1.454 1.826 1.812 | |

| Environmental Protect Management | EPM_1 EPM_2 EPM_3 EPM_4 EPM_5 EPM_6 EPM_7 EPM_8 | 0.731 0.750 0.738 0.777 0.667 0.802 0.723 0.785 | 0.910 | 0.559 | 1.735 1.824 1.742 1.896 1.520 2.167 1.713 2.051 | |

| Socially Responsible Management | ||||||

| Human Rights | HR_1 HR_2 HR_3 HR_4 HR_5 | 0.782 0.737 0.801 0.726 0.778 | 0.876 | 0.586 | 1.704 1.554 1.745 1.492 1.737 | |

| Philanthropy | PT_1 PT_2 PT_3 PT_4 | 0.882 0.814 0.858 0.850 | 0.913 | 0.725 | 2.466 1.834 2.372 2.130 | |

| Safety | Saf_1 Saf_2 Saf_3 | 0.859 0.888 0.907 | 0.915 | 0.783 | 1.974 2.284 2.459 | |

| External Management | ||||||

| Supplier Monitor and Assessment | SMA_1 SMA_2 SMA_3 SMA_4 SMA_5 SMA_6 SMA_8 | 0.660 0.683 0.739 0.666 0.672 0.834 0.766 | 0.882 | 0.518 | 1.463 1.550 1.633 1.468 1.417 2.209 1.787 | |

| Supplier Collaboration | SC_1 SC_3 SC_4 SC_5 SC_6 SC_7 SC_8 | 0.748 0.725 0.729 0.746 0.709 0.662 0.747 | 0.885 | 0.525 | 1.641 1.598 1.612 1.686 1.587 1.436 1.674 | |

| Technological Innovation | ||||||

| Process Innovation Capabilities | TI_2 TI_5 TI_6 TI_7 TI_8 TI_9 TI_11 | 0.732 0.722 0.783 0.799 0.628 0.763 0.640 | 0.886 | 0.528 | 1.555 1.886 2.032 1.400 1.757 1.396 1.609 | |

| Sustainable Performance | ||||||

| Economic Performance | EcP_1 EcP_3 EcP_4 EcP_5 EcP_6 | 0.753 0.713 0.717 0.701 0.740 | 0.847 | 0.526 | 1.472 1.476 1.507 1.609 1.707 | |

| Environmental Performance | EnP_1 EnP_2 EnP_3 EnP_4 EnP_5 EnP_6 EnP_7 | 0.708 0.695 0.751 0.735 0.684 0.604 0.798 | 0.878 | 0.508 | 1.501 1.490 1.848 1.639 1.572 1.337 2.029 | |

| Social Performance | SP_1 SP_2 SP_3 SP_4 SP_5 SP_6 | 0.739 0.630 0.751 0.735 0.764 0.683 | 0.864 | 0.516 | 1.542 1.346 1.622 1.664 1.779 1.470 |

| EcP | EnP | EPM | HR | PIC | Phil | PED | Safety | SP | SMA | SC | SP | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EcP | ||||||||||||

| EnP | 0.836 | |||||||||||

| EPM | 0.612 | 0.562 | ||||||||||

| HR | 0.553 | 0.536 | 0.489 | |||||||||

| TI | 0.753 | 0.705 | 0.553 | 0.484 | ||||||||

| Phil | 0.520 | 0.467 | 0.470 | 0.375 | 0.424 | |||||||

| PED | 0.461 | 0.490 | 0.458 | 0.494 | 0.393 | 0.363 | ||||||

| Safety | 0.429 | 0.474 | 0.432 | 0.416 | 0.413 | 0.344 | 0.390 | |||||

| SP | 0.786 | 0.834 | 0.567 | 0.497 | 0.692 | 0.453 | 0.507 | 0.481 | ||||

| SMA | 0.606 | 0.621 | 0.489 | 0.457 | 0.553 | 0.462 | 0.407 | 0.389 | 0.620 | |||

| SC | 0.617 | 0.652 | 0.466 | 0.455 | 0.584 | 0.298 | 0.435 | 0.298 | 0.622 | 0.479 | ||

| SP | 0.595 | 0.580 | 0.553 | 0.502 | 0.502 | 0.473 | 0.555 | 0.390 | 0.595 | 0.464 | 0.431 | |

| Items | Convergent Validity | Weights | VIF | t-Values | p-Values | |

|---|---|---|---|---|---|---|

| Internal Environment Management | PED SPP EPM | 0.717 | 0.289 0.440 0.512 | 1.380 1.491 2.356 | 3.510 5.691 6.578 | 0.000 0.000 0.000 |

| Socially Responsible Management | HR Phil Safety | 0.790 | 0.500 0.459 0.385 | 1.215 1.167 1.193 | 5.672 5.768 4.709 | 0.000 0.000 0.000 |

| Sustainable Performance | EcP EnP SP | 0.799 | 0.398 0.382 0.355 | 2.006 2.356 2.124 | 6.884 5.323 5.472 | 0.000 0.000 0.000 |

| H | Direct Paths Relationship | Path Coefficient (β) | Standard Error | T Statistics | Decision/Hypothesis |

|---|---|---|---|---|---|

| H1 | Internal Environment Management -> Sustainable Performance | 0.217 | 0.074 | 2.953 | Supported |

| H2 | Socially Responsible Management -> Sustainable Performance | 0.154 | 0.057 | 2.687 | Supported |

| H3 | Supplier Monitor and Assessment -> Sustainable Performance | 0.143 | 0.052 | 2.722 | Supported |

| H4 | Supplier collaboration -> Sustainable Performance | 0.157 | 0.051 | 3.108 | Supported |

| H | Paths Relationship with Moderation | Path Coefficient (β) | Standard Error | T Statistics | Decision/Hypothesis |

|---|---|---|---|---|---|

| H5a | IEM*PI -> Sustainable Performance | 0.126 | 0.071 | 1.785 | Supported |

| H5b | SRM*PI -> Sustainable Performance | −0.036 | 0.067 | 0.530 | Not Supported |

| H5c | SMA*PI -> Sustainable Performance | 0.129 | 0.062 | 2.100 | Supported |

| H5d | SC*PI -> Sustainable Performance | −0.073 | 0.049 | 1.494 | Not Supported |

| Latent Constructs | Variance Explained (R2) |

|---|---|

| Sustainable Performance | 67.3% |

| Latent Constructs | Effect Sizes (f2) | Degree of Effect |

|---|---|---|

| In case of Sustainable Performance: | ||

| Internal environment management | 0.074 | Small |

| Socially responsible management | 0.042 | Small |

| Supplier monitor and assessment | 0.057 | Small |

| Supplier collaboration | 0.088 | Small |

| Technological innovation | 0.154 | Medium |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shahid, H.M.; Waseem, R.; Khan, H.; Waseem, F.; Hasheem, M.J.; Shi, Y. Process Innovation as a Moderator Linking Sustainable Supply Chain Management with Sustainable Performance in the Manufacturing Sector of Pakistan. Sustainability 2020, 12, 2303. https://doi.org/10.3390/su12062303

Shahid HM, Waseem R, Khan H, Waseem F, Hasheem MJ, Shi Y. Process Innovation as a Moderator Linking Sustainable Supply Chain Management with Sustainable Performance in the Manufacturing Sector of Pakistan. Sustainability. 2020; 12(6):2303. https://doi.org/10.3390/su12062303

Chicago/Turabian StyleShahid, Hafiz Muhammad, Rafay Waseem, Humayoon Khan, Faria Waseem, Muhammad Junaid Hasheem, and Yangyan Shi. 2020. "Process Innovation as a Moderator Linking Sustainable Supply Chain Management with Sustainable Performance in the Manufacturing Sector of Pakistan" Sustainability 12, no. 6: 2303. https://doi.org/10.3390/su12062303

APA StyleShahid, H. M., Waseem, R., Khan, H., Waseem, F., Hasheem, M. J., & Shi, Y. (2020). Process Innovation as a Moderator Linking Sustainable Supply Chain Management with Sustainable Performance in the Manufacturing Sector of Pakistan. Sustainability, 12(6), 2303. https://doi.org/10.3390/su12062303