Abstract

Consumer Perceived Corporate Social Responsibility Authenticity (CPCSRA) belongs to the field of micro Corporate Social Responsibility (CSR) research. In general, understanding the formation mechanism of CPCSRA could make it better able to play its role in several ways. Firstly, most previous studies do not empirically consider a key factor, i.e., the consumer perceived senior managers’ involvement. We add this key factor into the independent variables of our formation mechanism. Secondly, most previous empirical research studies the relevant factors of consumer perceived CSR commitment as a whole. We study these relevant factors separately instead. Thirdly, we simultaneously choose the consumer perceived strategy-driven motive and consumer perceived value-driven motive as the mediating variables of our formation mechanism. Based on the above innovations, we comprehensively and systematically study the formation mechanism of CPCSRA. We use structural equation modeling to study the formation mechanism. For the convenience of data collection, our data are all from Chinese consumers. The study results show that three independent variables can directly affect CPCSRA. The three independent variables are consumer perceived level of invested resources, consumer perceived CSR efforts matching company and consumer perceived senior managers’ involvement. Consumer perceived senior managers’ involvement has the greatest effect. The two variables consumer perceived strategy-driven motive and consumer perceived value-driven motive play partial mediating effects on the relationship between independent variables and CPCSRA. Based on our empirical research, we put forward some feasible suggestions for company managers to increase company sustainability in market competition by promoting the formation of CPCSRA.

1. Introduction

In recent years, with the continuous development of the world economy and society, Corporate Social Responsibility (CSR) has attracted greater attention from consumers, researchers and companies [1,2,3,4]. Based on previous definitions of CSR [1,2], we define CSR as the actions that appear to further some social benefits, beyond the immediate economic interests and responsibility stipulated by law for companies. CSR efforts not only respond to social demands for companies to undertake acts in the public interest, but also serve as a way for companies to gain competitive advantages. A large number of studies show that consumers are very likely to reward companies for participating in CSR efforts by increasing their recognition in ways such as increasing their trust and loyalty towards that company [5,6,7]. Since the support of consumers is one of the most important determinants of company sustainability, CSR undoubtedly is an important issue in the process of sustainable development [8,9,10].

A company may attempt to practice social responsibility through environmental protection, educational support, helping the underprivileged, etc. [11,12]. However, only when consumers perceive a company’s social responsibility as authentic can they reward the company through greater purchases of the company’s goods, greater trust in the company, greater loyalty to the company, etc. [13,14]. The key to companies’ success in competition and sustainable development lies partly in consumer perceived CSR authenticity [10,15]. Thus, Consumer Perceived Corporate Social Responsibility Authenticity (CPCSRA) is an important research topic [16,17].

There is much research on CSR [17,18,19]. Most of this research are objective studies at the macro-level and meso-level [1,20,21]. Therefore, this kind of research tends to neglect specific and detailed factors of CSR research [10,22]. The research on perceived CSR authenticity [23,24,25,26] belongs to the research on individual subjective feelings at the micro-level. Some research on perceived CSR authenticity is qualitative [27,28]. Other perceived CSR authenticity research focuses on the perspective of employees [24,26]. Generally, employees are important stakeholders in companies, but consumers are the most fundamental source of company interests [29,30]. Most of this kind of research neglects empirical research on perceived CSR authenticity from the perspective of consumers [8,31]. There are also still some deficiencies in the existing research on CPCSRA [10,32,33]. For example, the independent variables do not take an important factor into account.They also study the relevant factors of consumer perceived CSR commitment as a whole. The valence of the mediation variable in their research is ambiguous. They also focus on the outcome variables. To sum up, existing research has not carried out a comprehensive and systematic study on the formation mechanism of CPCSRA.

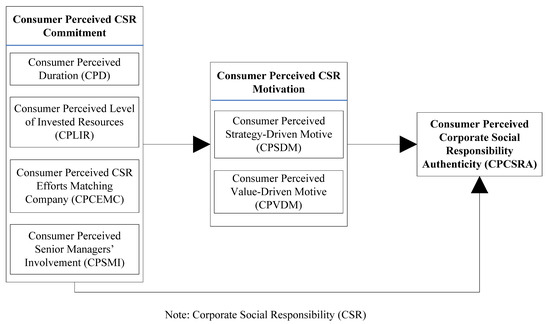

To remedy the above deficiencies, we focus on the antecedent variables. Our formation mechanism of CPCSRA has four independent variables and two mediating variables. The four independent variables are Consumer Perceived Duration (CPD), Consumer Perceived Level of Invested Resources (CPLIR), Consumer Perceived CSR Efforts Matching Company (CPCEMC) and Consumer Perceived Senior Managers’ Involvement (CPSMI). The two mediating variables are Consumer Perceived Strategy-Driven Motive (CPSDM) and Consumer Perceived Value-Driven Motive (CPVDM). CPCSRA is our dependent variable.

For the convenience of data collection, our data are all from Chinese consumers. Our survey data are based on received questionnaires via Questionnaire Star [34] and social media. We mainly use eastern China and central China as our survey scope. The use of social media means our respondents are not only from central and eastern China; a relatively small number of respondents are from other regions of China.

Our contributions are illustrated as follows:

- (1)

- Consumer perceived senior managers’ involvement is an important independent variable. Previous research neglects its effect. We add it to our formation mechanism. The result shows that this factor has the greatest effect on CPCSRA.

- (2)

- Most previous empirical research studies the relevant factors of consumer perceived CSR commitment as a whole. However, we study the relevant factors separately. In other words, we want to know how each factor affects CPCSRA. The result shows that three of the four factors have direct effects on CPCSRA.

- (3)

- We innovatively choose consumer perceived srategy-driven motive and consumer perceived value-driven motive as our mediating variables. The results show that they play partial mediating effects on the relationship between independent variables and CPCSRA.

- (4)

- For the first time, we conduct a comprehensive, systematic and empirical study on the formation mechanism of CPCSRA at the micro-level from the perspective of consumers.

2. Literature Review

2.1. CSR

Carroll proposes a most classic study in the CSR literature [35]. He studies CSR from the perspective of stakeholders for the first time. He defines stakeholders as those individuals or groups who interact with a company and have interests or rights in the company [36]. Hill et al. believe that stakeholders include shareholders, managers, employees, customers, suppliers, creditors, communities and the public [37].

Carroll believes that CSR includes four aspects: economic, legal, ethical and discretionary responsibility. Social issues involve consumerism, environment, discrimination, product safety, occupational safety and shareholders. Although this combination of CSR and stakeholders provides a comprehensive understanding of CSR, the connotation of responsibility is all-encompassing. The CSR needs of different stakeholders conflict with each other, which makes the definition of CSR vague. This is not conducive to the formulation and promotion of CSR related policies [2,27].

Jones et al. [1] and McWilliams et al. [2] propose CSR as an act that transcends immediate economic interests and responsibilities stipulated by law for companies. CSR can promote the behavior of social public interest. They point out that the ethical and discretionary responsibilities in Carroll’s model [35] should be focused. In view of the research of Yates [22], the economic behavior and legal behavior of business organizations are given behaviors. When employees evaluate CSR, ethics and philanthropic CSR efforts are the first behaviors to be considered by them. This also applies to consumers’ evaluations of CSR [22]. Driver [38] discusses CSR in a post-egoic framework. Seeking long-term economic benefits is a post-egoic characteristic. However, pursuing immediate and short-term economic benefits is the main characteristic of egoic CSR.

This paper refers to the existing definitions of CSR and puts forward the definition of CPCSRA in Section 4.3.

2.2. Perceived CSR Authenticity

In reality, companies often encounter a dilemma in the process of implementing CSR efforts. Objectively, a company may be trying to practice CSR. Subjectively, the company is not necessarily considered to have any social responsibility [13,14]. Therefore, some scholars propose to discuss CSR at the micro-level. We need to understand how micro individuals respond to CSR efforts from a psychological perspective [28,29]. In psychology, authenticity is tested from a constructivist perspective. That is, more attention is paid to experience and interpretation than to objective reality [39,40,41].

Beckman et al. [23] examine how and why CSR occurs in the underdeveloped country Chile through in-depth interviews. They find that the key to a successful implementation of CSR is that the authenticity of CSR is perceived by stakeholders. McShane et al. [24] use depth interviews to understand how employees judge the authenticity and inauthenticity of CSR efforts, and how these judgments affect employees’ perceptions of CSR. In addition, Yates [22] empirically analyzes the influence of perceived CSR authenticity on perceived organizational support, organizational trust, affective commitment and organization citizenship behavior from the perspective of employees. Ji et al. [26] empirically analyze the impact of perceived CSR authenticity on employees’ surface acting and deep acting from the perspective of employees.

Reviewing the previous literature, it is found that qualitative research and employee research account for most of the perceived CSR authenticity research. Generally, employees are the important stakeholders of companies, but consumers are the most fundamental source of company interests. Thus, the study of perceived CSR authenticity from the perspective of consumers in this paper has stronger practical significance.

2.3. Consumer Perceived Corporate Social Responsibility Authenticity (CPCSRA)

Some researchers believe that customers are pivotal stakeholders [10,33,42]. Alhouti et al. [10] conduct an empirical study on CPCSRA for the first time. They believe that CPCSRA means that consumers perceived CSR effort is the true and sincere expression of companies’ social beliefs. As our CSR is different from Alhouti et al.’s CSR, our CPCSRA is also different from Alhouti et al.’s CPCSRA. Our CPCSRA is defined in Section 4.3, which refers to Alhouti et al.’s definition. In a small number of previous studies, researchers agree that CSR authenticity can affect consumers’ trust, purchase intention and brand attitude [10,33,42]. However, current studies lack a comprehensive and systematic observation of how CSR authenticity is formed [15].

According to previous studies, there are two kinds of most critical factors for consumers to judge the authenticity of CSR: consumer perceived CSR commitment and consumer perceived CSR motivation [10,33]. Alhouti et al. [10] combine time and money commitments to form an impact variable for the consumer perceived CSR commitment. Yoh [43] refers to the study of Dwyer et al. [44]. Then Yoh takes time, finance and fit as three factors of consumer perceived CSR commitment. Some researchers remind that the participation of senior managers is also an important criterion for judging the sincerity of CSR efforts [45,46]. However, they lack empirical analysis to verify it. Ellen et al. [32] take the strategic motive, values driven motive, stakeholder driven motive and egoistic motive as four factors of consumer perceived CSR motivation. Among them, the strategic motive and values driven motive are positive forms of valence motivation, which can positively influence consumer responses. The stakeholder driven motive and egoistic motive are negative forms of valence motivation. However, the valence judgment of strategic motive and stakeholder driven motive in the studies of Alhouti et al. [10] and Jeon et al. [33] differ from Ellen et al. [32]. Meanwhile, their conclusions on the relationship between consumer perceived CSR motivation and consumer perceived CSR authenticity are also contradictory.

In addition, although previous studies explain the influence of two types of antecedents on perceived CSR authenticity, the relationship between these two types of variables was not taken into account in the explanation process. Thus, there are still some deficiencies in the existing research on CPCSRA. It is urgent for us to conduct a comprehensive, systematic and empirical study on the formation mechanism of CPCSRA.

3. Hypotheses

3.1. Consumer Perceived CSR Commitment and CPCSRA

In the eyes of consumers, a company’s commitment to CSR is an important reference factor for them to judge whether the company’s CSR effort is sincere [11,16,44,47]. Alhouti et al. [10] show that 60% of respondents admit that perceived factors related to CSR commitment are an important reference for them to judge the CSR authenticity. Based on previous studies [43,44,48], we propose that consumer perceived CSR commitment is the consumer perceptions willingness of a company’s interest in maintaining a positive relationship with the public through its CSR efforts.

Dwyer et al. [44] point out that commitment includes three factors: the durability of an association, the input and the consistency of that input. Yoh [43] consider time, finance and company-cause fit as three factors underpinning consumer perceptions of a company’s commitment towards cause-related marketing. Cause-related marketing is a form of CSR. Some researchers remind us that the participation of senior managers is also an important criterion for judging the sincerity of CSR efforts [45,46]. Van den Brink et al. [49] add management involvement to the above three factors as an important basis for considering the sincerity of CSR efforts. CSR policies and plans are carried out in the name of the company on the surface, but they are formulated, complied with and participated in by individuals [50,51]. This once again proves that it is very important and practical to observe CSR from the individual micro-level.

Senior managers are the representatives of a company’s image and the transmitter of company values. So we argue that consumers may judge CSR input and intention while referring to the attitude of senior managers. Therefore, our consumer perceived CSR commitment includes four factors: Consumer Perceived Duration (CPD), Consumer Perceived Level of Invested Resources (CPLIR), Consumer Perceived CSR Efforts Matching Company (CPCEMC) and Consumer Perceived Senior Managers’ Involvement (CPSMI).

Most previous empirical research studies the relevant factors of consumer perceived CSR commitment as a whole [10,32,43]. However, we study the relevant factors separately. In other words, we want to know how each factor affects the consumer’s judgment on CSR sincerity. Thus, we use the four factors mentioned previously as the four independent variables of CPCSRA.

According to the persuasion knowledge theory [52], we believe that consumers may judge whether a company makes practical and meaningful contributions to CSR by evaluating the company’s CSR information. The information of the four factors discussed above is perceived by consumers to affect consumers’ judgment of CSR authenticity. Specifically, CPD may directly affect CPCSRA by indicating the length and status of a company’s participation in CSR efforts. CPLIR may directly affect CPCSRA through the level of the amount and type of resources that a company invests in CSR efforts. CPCEMC may directly affect CPCSRA through the degree of the matching relationship between CSR efforts and the company’s product line, brand image, market positioning, target market, etc. CPSMI may directly affect CPCSRA through the degree of senior managers’ involvement in CSR efforts.

Based on the above analysis, the information of the above four factors related to consumer perceived CSR commitment is an important reference for consumer perceptions of the sincerity of CSR efforts carried out by companies. Therefore, hypotheses are proposed as follows:

Hypothesis H1a.

Consumer Perceived Duration positively affects CPCSRA.

Hypothesis H1b.

Consumer Perceived Level of Invested Resources positively affects CPCSRA.

Hypothesis H1c.

Consumer Perceived CSR Efforts Matching Company positively affects CPCSRA.

Hypothesis H1d.

Consumer Perceived Senior Managers’ Involvement positively affects CPCSRA.

3.2. Mediating Effect of Consumer Perceived CSR Motivation

Consumer perceived CSR motivation is consumers’ cognition of the purpose of companies performing CSR efforts [32]. Previous research finds that consumers may experience some interventions when evaluating CSR efforts [11,53,54,55,56]. Ellen et al. [32] believe that consumer attributions are affected by these interventions. Alouti et al. [10] find that factors related to CSR commitment (such as long-time impact, input resource level, etc.) are persuasive information. Persuasive information is interfered by attribution. Therefore, consumer perceived CSR motivation plays a mediating role between consumer perceived CSR commitment and CPCSRA.

Ellen et al. [32] take strategic motive and values driven motive as positive forms of valence motivation and take stakeholder driven motive and egoistic motive as negative forms of valence motivation. Researchers find that consumer perceived CSR motivation can affect CPCSRA [10,32,33]. However, the valence judgments of strategic motive and stakeholder driven motive in the studies of Alhouti et al. [10] and Jeon et al. [33] differ from those in the studies of Ellen et al. [32]. For example, Alhouti et al. [10] and Jeon et al. [33] regard strategic motive as a negative valence motivation which negatively affects consumer perceived CSR authenticity. Jeon et al. [33] regard stakeholder driven motive as a positive valence motivation, which positively affects consumer perceived CSR authenticity.

Before we put forward the hypotheses of mediating effects of consumer perceived CSR motivation, we want to answer the two questions as follows:

Question 1. How does strategic motive and stakeholder driven motive affect CPCSRA?

Question 2. In the research on CSR, there is always a binary opposition between economic and ethical. Do the four consumer perceived CSR motivations proposed by Ellen et al. [32] also have such a binary opposition?

The answer to Question 1: Firstly, Alhouti et al. [10] and Jeon et al. [33] find the economic purpose of strategic motive and think that it negatively affects consumer response. However, they ignore the intention of Ellen et al. [32] to compare the difference between a strategic motive and egoistic motive. The strategic motive emphasizes the long-term strategic orientation of companies. The company gains economic benefits through reciprocity with society. The egoistic motive emphasizes companies’ use of CSR to get immediate benefits. Therefore, they both have economic purposes, but the nature of the two motives is different. Secondly, Ellen et al. [32] use a neutral description of the stakeholder driven motive. For example, companies feel that consumers and employees expect them to implement CSR efforts. Thus, Ellen et al. think that companies are forced to implement CSR under the pressure of stakeholders. However, Jeon et al. [33] believe that CSR efforts are an initiative proactively undertaken by companies to meet the CSR demands of stakeholders.

The answer to Question 2: We think the four motives defined by Ellen et al. [32] are on a spectrum from self-interest to altruism: egoistic motive → stakeholder driven motive → strategic motive → values driven motive. While Driver [38] describes the differences between egoic and post-egoic actions, there is no clear boundary between self-interest and altruism. This transition is fuzzy.

According to the study developed by Drumwright [57] in 1996, while company managers have been emphasizing the mixed economic and social purposes of company CSR, they are also concerned that consumers may simply judge company CSR efforts as being purely for economic or purely social purposes. Later, other researchers [6,56,58] raised the same concerns. But some researchers have argued that when companies have enough communication with consumers, consumers may get enough persuasive information on a company’s motives [59]. Then consumers can analyze and accept some obvious contradictions of this information, rather than simply forming extreme judgments [60]. Therefore, in the long run, strategic motive (gain customers, increase market competitiveness, achieve sustainable development, etc.) is a basic requirement for a company to have a social role. Consumers can accept the business activities related to the strategic motive.

To sum up, the strategic motive and values driven motive both positively affect consumer perceptions of CSR authenticity. The egoistic motive and stakeholder driven motive both negatively affect consumer perceptions of CSR authenticity. Since previous researchers have tried to resolve the binary opposition between economic and ethical in CSR efforts, we focus on the discussion of the strategic motive and values driven motive. To describe our idea more clearly, the strategic motive is represented by consumer perceived strategy-driven motive in our formation mechanism of CPCSRA. The values driven motive is represented by consumer perceived value-driven motive. As such hypotheses about mediating effects are proposed as follows:

Hypothesis H2a.

Consumer Perceived Srategy-Driven Motive plays a mediating effect on the relationship between CPD and CPCSRA.

Hypothesis H2b.

Consumer Perceived Srategy-Driven Motive plays a mediating effect on the relationship between CPLIR and CPCSRA.

Hypothesis H2c.

Consumer Perceived Srategy-Driven Motive plays a mediating effect on the relationship between CPCEMC and CPCSRA.

Hypothesis H2d.

Consumer Perceived Srategy-Driven Motive plays a mediating effect on the relationship between CPSMI and CPCSRA.

Hypothesis H2e.

Consumer Perceived Value-Driven Motive plays a mediating effect on the relationship between CPD and CPCSRA.

Hypothesis H2f.

Consumer Perceived Value-Driven Motive plays a mediating effect on the relationship between CPLIR and CPCSRA.

Hypothesis H2g.

Consumer Perceived Value-Driven Motive plays a mediating effect on the relationship between CPCEMC and CPCSRA.

Hypothesis H2h.

Consumer Perceived Value-Driven Motive plays a mediating effect on the relationship between CPSMI and CPCSRA.

4. Study Design and Methods

4.1. Theoretical Model

Our purpose is to study the formation mechanism of CPCSRA. Thus, we take four related factors of consumer perceived CSR commitment as the independent variables and two related factors of consumer perceived CSR motivation as the mediating variables. The four independent variables are Consumer Perceived Duration, Consumer Perceived Level of Invested Resources, Consumer Perceived CSR Efforts Matching Company and Consumer Perceived Senior Managers’ Involvement. The two mediating variables are Consumer Perceived Srategy-Driven Motive and Consumer Perceived Value-Driven Motive. CPCSRA is our dependent variable. Figure 1 shows the theoretical model of our study.

Figure 1.

Theoretical model.

4.2. Analysis Method and Sample Characteristics

To ensure the reliability of the study results, we firstly tested the reliability and validity of all variables. Secondly, we used correlation analysis to verify the correlation between variables. Finally, we carried out our hypotheses testing.

SPSS 23.0 and AMOS 22.0 (New York, USA) were used in the analysis. For the convenience of data collection, we conducted a survey on only Chinese consumers by giving out questionnaires through Questionnaire Star [34] and social media (such as Wechat group, QQ group, etc.). Our questionnaire belongs to the text questionnaire, which is all edited using Chinese characters. It does not involve voice or other languages.

The consumer’s CSR awareness may be affected by the environment in which he/she is located. In regions where the economy and culture are more developed, consumers may have stronger CSR awareness. In China, the better economic development areas are eastern China and central China. Eastern China includes the Beijing-Tianjin-Hebei city cluster, Yangtze river delta city clusters and Pearl river delta city clusters. Central China includes Shanxi, Henan, Anhui, Hubei, Jiangxi and Hunan provinces. We mainly took eastern China and central China as our survey scope. We sent the questionnaire to a consumer alone or asked the consumer to send the questionnaire to his/her WeChat group, QQ group or circle of friends. As such, our data collection used the snowballing method. The nature of social media meant that our respondents were not only from central and eastern China but also from other regions of China. The number of respondents from other regions was relatively small.

All questionnaires were finally completed on the answer page of Questionnaire Star [34]. The questionnaire survey was conducted in the form of voluntary participation. The respondents answered the questionnaire based on the information related to the CSR efforts of the company they are interested in. Therefore, there were many companies involved in our research, such as Alibaba, Baidu, Midea, etc. After completing the questionnaire, each respondent received a red envelope. There were 4 kinds of red envelopes. The first one was Wechat cash which randomly provided 1 to 10 RMB. The second one was a telephone charge voucher. The third one was a product coupon. The last one was an online learning trial course.

The survey began on 20 October 2019, and ended on 20 November 2019. We sent out 600 questionnaires and got 496 completed questionnaires. The recovery rate was 82.6%. In the completed questionnaires, we eliminated two kinds of invalid questionnaires. One kind was taking very little time to complete the questionnaire. The other appeard to be significant inconsistencies in the questionnaire. The remaining 390 questionnaires were valid. Thus, the effective rate was 78.6%. By analyzing the samples, we obtained a statistical distribution table of demographic characteristics. Table 1 shows the sample characteristics of this study.

Table 1.

Characteristics of the Sample.

4.3. Operational Definition and Measurement of Variables

In this study, we adapted selected maturity scales according to our purpose. Scales were all from English literature, but respondents were Chinese consumers. Thus, scale items involved translation work. To ensure the accuracy of the semantic meaning of each item, the translation of scales was completed through translation and reverse translation with the help of relevant scholars. Before the formal release of the questionnaire, we conducted a small prior test to ensure that each item could be accurately understood by respondents. After that, the questionnaire was adjusted again according to the feedback of respondents in the prior test. For example, there were several ambiguities in and doubts towards the item expression. After finally confirming that all items have no questions of understanding, our formal questionnaire was formed. Our questionnaire used a 7-level Likert scale. We give 1–7 scores to items from “disagree completely” to “agree completely”. The operational definition and measurement scales of variables involved in this paper are illustrated as follows.

According to previous studies [43,44,48], we proposed that consumer perceived CSR commitment was the consumer perceived willingness degree of a company maintaining a positive relationship with the public through its CSR efforts. Our consumer perceived CSR commitment has four related factors: CPD, CPLIR, CPCEMC and CPSMI, which are shown in Figure 1. Based on previous studies [44,45,47,49,59,60,61], we defined the four related factors (i.e., independent variables) as follows.

Consumer Perceived Duration (CPD): Consumers perceive the length and status of the a company’s participation in CSR efforts. The scale adopted in this paper was adapted from the study of Van den Brink et al. [49]. The scale contains three items shown in Table 2.

Table 2.

Items of Initial Scales.

Consumer Perceived Level of Invested Resources (CPLIR): Consumers perceive the level of the amount and type of resources that a company invests in CSR efforts. The scale adopted in this paper was adapted from the studies of Van den Brink et al. [49] and Biswas et al. [62]. The scale contains four items shown in Table 2.

Consumer Perceived CSR Efforts Matching Company (CPCEMC): Consumers perceive the degree of the matching relationship between CSR efforts and the company’s product line, brand image, market positioning, target market, etc. The scale adopted in this paper was adapted from the studies of Becker-Olsen et al. [63] and Keller et al. [64]. The scale contains three items shown in Table 2.

Consumer Perceived Senior Managers’ Involvement (CPSMI): Consumers perceive the degree of senior managers’ involvement in CSR efforts. The scale adopted in this paper was adapted from the studies of De Wulf et al. [65]. The scale contains three items shown in Table 2.

Consumer perceived CSR motivation is consumers’ cognition of the purpose for companies performing CSR efforts [32]. Our consumer perceived CSR motivation has two related factors: CPSDM and CPVDM, which are shown in Figure 1. Based on previous studies [30,64,65], we defined the two related factors (i.e., mediating variables) as follows.

Consumer Perceived Strategy-Driven Motive (CPSDM): Companies implement CSR efforts because they want to achieve a long-term sustainable development strategy and gain economic benefits in the long run [32,66]. This is an important means for companies to play a good role in society. The scale adopted in this paper was adapted from the study of Ellen et al. [32]. The scale contains three items shown in Table 2.

Consumer Perceived Value-Driven Motive (CPVDM): Companies implement CSR efforts because they think it is “worth doing” the “right thing” [32,67]. The motive is therefore underpinned by the company’s perceived responsibility towards society [68]. The scale adopted in this paper was adapted from the study of Ellen et al. [32]. The scale contains three items shown in Table 2.

Consumer Perceived Corporate Social Responsibility Authenticity (CPCSRA). CPCSRA is consumers’ perception of companies’ CSR efforts, which are the sincere and true expression of companies’ belief in society [10]. In other words, this measures how much consumers think that companies’ CSR efforts are authentic. The scale adopted in this paper was adapted from the study of Alhouti et al. [10]. The scale contains seven items shown in Table 2.

4.4. Reliability and Validity Test

Before the correlation analysis and hypotheses testing, we needed to test the reliability and validity of the measurement scales. To do this, we completed the test in two steps as follows.

- (1)

- Initial scales: This step tested the initial scales and removes several invalid items. We used SPSS 23.0 for reliability tests and exploratory factor analysis. Firstly, according to the reliability tests, all variables’ Cronbach’s alpha values were greater than 0.8. This indicates that our scales have good reliability. Secondly, for each item, we got a Cronbach’s alpha without this item. Compared with the initial Cronbach’s alpha and all Cronbach’s alpha without a certain item, we found that no item needs to be deleted. Thirdly, according to exploratory factor analysis, the KMO (Kaiser-Meyer-Olkin) value was 0.946. The cumulative percentage of variance was 77.88%. These indicate our scales were suitable for factor analysis. In addition, we rotated out 7 factors. Fourthly, we used AMOS 22.0 for confirmatory factor analysis. Based on the indication of the modification indices, we deleted all items that cause the modification indices to be well above 10. Finally, Item 3 of CPLIR was deleted. Meanwhile, Items 2, 5 and 7 of CPCSRA were deleted too.

- (2)

- Final scales: This step was to conduct reliability tests and exploratory factor analysis again on the final scales after deleting invalid items. In addition, this step had two new tests. Firstly, we calculated the AVE (Average Variance Extracted) and CR (Construct Reliability) values to test the convergent validity of the variables. Afterwards, we tested the reliability and validity of the final scales’ variables. The results are shown in Table 3, where all abbreviations of variables are defined in Section 4.3 and shown in Figure 1.

Table 3. Reliability and Validity Test results.

In Table 3, Cronbach’s alpha of each variable ranges from 0.857 to 0.916, all of which are bigger than 0.7. This indicates that our scales have good reliability [69]. The AVE value of each variable ranges from 0.648 to 0.793, all of which are bigger than 0.5. The CR value of each variable ranges from 0.860 to 0.920, all of which are bigger than 0.7. The Factor loading of each variable ranges from 0.626 to 0.829, all of which are bigger than 0.5. These indicate that our scales have good convergent validity [70,71].

Second, we used the model fit of confirmatory factor analysis to test the discriminant validity and convergent validity of the variables. As for model fit, CMIN/DF (/df, Chi-square/degree of freedom), RMR (Root Mean-square Residual), RMSEA (Root Mean Squared Error of Approximation), GFI (Goodness-of-Fit Index), AGFI (Adjusted Goodness-of-Fit Index), NFI (Normed Fit Index), IFI (Incremental Fit Index) and CFI (Comparative Fit Index) were generally used as the evaluation criteria [72,73,74]. The variables’ model fit values of confirmatory factor analysis were shown in Table 4. The values shown in Table 4 illustrate that our scales have good discriminant validity and convergent validity [72,73,74].

Table 4.

Model Fit of Confirmatory Factor Analysis results.

4.5. Correlation Analysis

Before we test the hypotheses, we should also analyze the correlation. In general, if the absolute value of the correlation coefficient between two variables ranges from 0.2 to 0.4, the correlation was low. If the correlation coefficient ranges from 0.4 to 0.6, then the correlation between the two variables was medium. If the correlation coefficient was above 0.6, the correlation was high. If the correlation coefficient was above 0.8, then there may be a collinearity phenomenon. Our correlation coefficients between our variables are shown in Table 5, where all abbreviations of variables are defined in Section 4.3 and shown in Figure 1. The maximum correlation coefficient was 0.758. Therefore, there was no collinearity problem among the variables in this study.

Table 5.

The Correlation Analysis.

In addition, the square root of the AVE value of each variable is on the diagonal of Table 5. All the square roots are in parentheses. For each variable, the square root of the variable’s AVE value was bigger than the correlation coefficient between the variable and other variables. This further verifies that our study has good discriminant validity between the variables.

4.6. Hypotheses Testing

4.6.1. Structural Equation Model Analysis for Hypotheses Testing

We used AMOS 22.0 for structural equation model analysis. To test the hypotheses, we first needed to test the model fit of the structural equation. The values shown in Table 6 illustrate that our structural equation model fits well with the questionnaire data.

Table 6.

Model Fit of Structural Equation (N = 390).

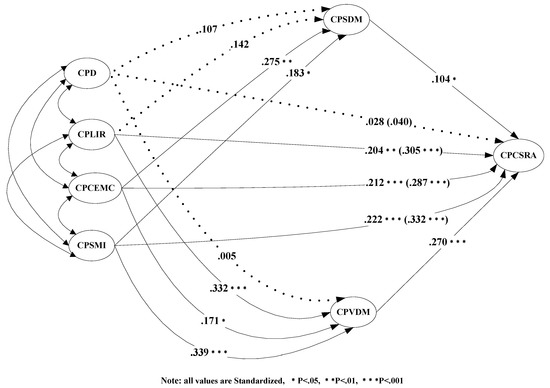

Figure 2 shows the results of our structural equation model analysis. The value on the line represents the standardized path coefficient. The value in parentheses represents the total effect and the total effect’s significance generated by all paths from the independent variable to the dependent variable, including the direct path and all indirect paths. The dotted line between A and B indicates that the relationship between A and B is not valid. The solid line between A and B indicates that the relationship between A and B is valid.

Figure 2.

Results of the structural equation model.

Then, based on the results of the structural equation model analysis shown in Figure 2, we tested the hypotheses as follows:

- (1)

- Hypotheses testing of causality between independent and dependent variables (i.e., H1a–H1d): The total effect of CPD→CPCSRA was 0.040, which was insignificant. The total effect of CPLIR→CPCSRA was 0.305, which was significant at the level of P = 0.001. The total effect of CPCEMC→CPCSRA was 0.287, which was significant at the level of P = 0.001. The total effect of CPSMI→CPCSRA was 0.332, which was significant at the level of P = 0.001. Therefore, Hypotheses H1b, H1c, and H1d were all supported, while H1a was not. This shows that CPD plays a very limited role in consumers’ judgment of CSR authenticity. Consumers pay more attention to CPLIR, CPCEMC and CPSMI. In addition, CPSMI has the greatest effect.

- (2)

- Hypotheses testing of mediating effects (i.e., H2a–H2h): The path coefficients between the mediating variables and the dependent variable were both significant. Thus, we only needed to focus on the path coefficients between independent variables and mediating variables. There were 8 path coefficients between the four independent variables and the two mediating variables. There were three cases as follows:

- (1)

- The path coefficients of CPD→CPSDM and CPD→CPVDM were both insignificant. This indicates that the relationship between CPD and CPSDM and CPVDM is insignificant, which is consistent with previous studies [32].

- (2)

- The path coefficient of CPLIR→CPSDM was insignificant, while the path coefficient of CPLIR→CPVDM was significant. This may be because the resources a company puts into CSR efforts are a good persuasive message. The higher the level of resources a company puts into CSR efforts, the more it strengthens consumer perceptions of value-driven motivation and weakens consumer perceptions of strategic-driven motivation.

- (3)

- The path coefficients between an independent variable and the two mediating variables were both significant. This indicates that there were two important inducing factors of consumer perceptions of value-driven motivation and strategic-driven motivation. One was the degree of the matching relationship between CSR efforts and the company’s product line, brand image, market positioning, target market, etc. The other was the degree of senior managers’ involvement in CSR efforts.

Based on the above three cases, the mediating effects of the two mediating variables are summarized below.

- (1)

- CPSDM: CPSDM has no mediating effect between CPD and CPCSRA. Therefore, Hypothesis H2a was not supported. CPSDM has no mediating effect between CPLIR and CPCSRA. Thus, Hypothesis H2b was not supported. CPSDM has a mediating effect between CPCEMC and CPCSRA. Thus, Hypothesis H2c was supported. CPSDM has a mediating effect between CPSMI and CPCSRA. Thus, Hypothesis H2d was supported.

- (2)

- CPVDM: CPVDM has no mediating effect between CPD and CPCSRA. Therefore, Hypothesis H2e was not supported. CPVDM has a mediating effect between CPLIR and CPCSRA. Thus, Hypothesis H2f was supported. CPVDM has a mediating effect between CPCEMC and CPCSRA. Thus, Hypothesis H2g was supported. CPVDM has a mediating effect between CPSMI and CPCSRA. Thus, Hypothesis H2h was supported.

After determining which hypotheses were supported, we also needed to know whether the mediating variables have a full or partial effect. Since the direct effects between CPLIR, CPCEMC, CPSMI and CPCSRA were significant, the mediating variables play a partial mediating effect between independent variables and the dependent variable.

4.6.2. Bootstrap Method for Hypotheses Testing

In the above section, we used the Causal Steps approach to test the mediating effects. This approach is the most widely used method to test the mediating effect. It was popularized by Baron and Kenny [75,76]. Later, the Soble test was often used as its complement to test the mediating effect [76,77].

However, the Soble test has a flaw. It requires the sampling distribution of indirect effects to have a normal distribution. The sampling distribution of indirect effects tends to be asymmetrical. The skewness and kurtosis were not zero [78,79]. Therefore, some researchers propose using the Bootstrap method and the empirical M-test to supplementarily test the mediating effect better than the Soble test. The two methods do not need to assume that the sampling distribution of indirect effects has a normal distribution [76,80].

Compared with the Bootstrap method, empirical M-test has two disadvantages: (1) It was difficult to perform this test without the help of tables. (2) Additional assumptions need to be added to this test [76]. The Bootstrap method does not need to add additional assumptions. Meanwhile, the Bootstrap method has been used in some structural equation software (such as Mplus, Amos, EQS, etc.) [76,81]. Therefore, the Bootstrap method in Amos 22.0 was used in this paper to supplementarily test the mediating effect in this study.

In this study, there were two mediating variables on the relationship between each independent variable and the dependent variable. Thus, the indirect effect between the independent variable and the dependent variable was the sum of the two mediating effects. For example, the indirect effect of CPCEMC→CPCSRA was the sum of the mediating effects of CPCEMC→CPSDM→CPCSRA and CPCEMC→CPVDM→CPCSRA. In other words, each indirect effect was the sum of two mediating effects of the two mediating paths. There were 8 mediating paths in Figure 2.

In line with Hayes’s study [76], we set the sample size of the Bootstrap method to 5000. Then Amos provided the effect for each mediating path and direct path. Meanwhile, Amos also provided the Standard Error (S.E) and the 95% Confidence Interval (CI). If the bootstrap confidence interval did not contain 0, then the corresponding indirect and direct effect exist [76]. The results are shown in Table 7.

Table 7.

The Mediating Effect Test (N = 390, Bootstrap = 5000).

Table 7 shows that the 95%CIs of the 5 mediating paths (CPCEMC→CPSDM→CPCSRA, CPSMI→CPSDM→CPCSRA, CPLIR→CPVDM→CPCSRA, CPCEMC→CPVDM→CPCSRA, CPSMI→CPVDM→CPCSRA) do not contain 0. This indicates that the mediating effects of these 5 paths exist. In other words, Hypotheses H2c, H2d, H2f, H2g and H2h were supported again.

In Table 7, the 95%CI of CPD→CPCSRA contains 0. Meanwhile, the 95%CIs of CPD→CPSDM→CPCSRA and CPD→CPVDM→CPCSRA both contain 0 too. This indicates that there was no direct or indirect effect between CPD and CPCSRA. The 95%CI of the other three direct paths do not contain 0. This indicates that the two mediating variables both play a partial mediating effect between independent variables and the dependent variable through the 5 mediating paths. Specifically, CPSDM plays a partial mediating effect between CPCEMC and CPCSRA. CPSDM plays a partial mediating effect between CPSMI and CPCSRA. CPVDM plays a partial mediating effect between CPLIR and CPCSRA. CPVDM plays a partial mediating effect between CPCEMC and CPCSRA. CPVDM plays a partial mediating effect between CPSMI and CPCSRA.

5. Conclusions

5.1. Study Conclusion and Implications

5.1.1. Study Conclusion

Based on previous CSR studies, this paper proposed a definition for CPCSRA. Then we constructed consumer perceived CSR commitment and consumer perceived CSR motivation. On these bases, we studied the formation mechanism of CPCSRA. The formation mechanism took the four related factors of consumer perceived CSR commitment as the independent variables. These four related factors are Consumer Perceived Duration, Consumer Perceived Level of Invested Resources, Consumer Perceived CSR Efforts Matching Company and Consumer Perceived Senior Managers’ Involvement. Meanwhile, the formation mechanism takes the 2 related factors of consumer perceived CSR motivation as the mediating variables. The 2 related factors are the Consumer Perceived Strategy-Driven Motive and Consumer Perceived Value-Driven Motive. CPCSRA is our dependent variable.

Our research conclusions are illustrated as follows:

- (1)

- CPLIR, CPCEMC and CPSMI are significantly positively correlated with CPCSRA. In addition, CPSMI has the greatest effect on CPCSRA.

- (2)

- CPSDM has a partial mediating effect between CPCEMC and CPCSRA. CPSDM has a partial mediating effect between CPSMI and CPCSRA. CPVDM has a partial mediating effect between CPLIR and CPCSRA. CPVDM has a partial mediating effect between CPCEMC and CPCSRA. CPVDM has a partial mediating effect between CPSMI and CPCSRA.

Combined with the above research conclusions, this paper not only enriches the theoretical research on CSR but also provides valuable references for company managers.

5.1.2. Implications for Theoretical Research

This study has several implications for further theoretical research. Firstly, in the Carroll model [35], there are six stakeholders and four responsibilities. However, we only focused on one stakeholder (i.e., consumer) and two responsibilities (i.e., ethical and discretionary). This makes it easier for us to study CSR in a more detailed way. This is also in line with the general consumers’ understanding of CSR.

Secondly, our research on CPCSRA is different from previous research at the macro or meso-level [1,20,21]. They emphasize the relationship between CSR related indicators and a company’s financial performance. However, we studied consumers’ perceptions of the authenticity behind CSR efforts from a micro psychological perspective. When using the lens of authenticity to study CSR, CSR is no longer a question about how companies benefit themselves, but a question about how companies themselves are defined and described.

Thirdly, using empirical methods, this study advances the research on the formation mechanism of consumer perceived CSR authenticity. Consumer perceived senior managers’ involvement is an important factor. However, most previous studies do not empirically consider it [10,32,43,44,45,46]. We added it to our formation mechanism. The result shows that this factor has the greatest effect on CPCSRA.

Fourthly, most previous empirical research studies the relevant factors of consumer perceived CSR commitment as a whole [10,32,43]. However, we studied the relevant factors separately. In other words, we wanted to know how each factor affects CPCSRA. The result shows that three of the four factors have direct effects on CPCSRA.

Finally, we focused on two motives for this paper: the consumer perceived strategy-driven motive and the consumer perceived value-driven motive. Most previous research studies the direct relationship between the two motives and CPCSRA [10,33]. We firstly and simultaneously choose the two motives as our mediating variables to study how they play roles in the formation mechanism of CPCSRA. The result shows that they play partial mediating effects on the relationship between independent variables and CPCSRA.

In summary, we not only explore the relationship between antecedents and CPCSRA, but also consider the relationship between antecedents. Consequently, we conduct a comprehensive and systematic formation mechanism of CPCSRA at the micro-level from the perspective of consumers for the first time.

5.1.3. Implications for Company Manager

- (1)

- The empirical results of this study prove that consumer perceived duration has no significant effect on CPCSRA. CPLIR, CPCEMC and CPSMI all have significant effects on CPCSRA. In addition, CPSMI has the greatest impact on CPCSRA. Therefore, when delivering CSR information to consumers, managers should highlight the level of invested resources in CSR efforts and their consistency with company profit-making activities through company information, while including the senior managers’ involvement in this information. Only in this way can consumers more effectively feel the sincerity and authenticity of these CSR efforts.

- (2)

- The empirical results of this study prove that CPCEMC and CPSMI can indirectly affect CPCSRA through CPSDM. CPLIR, CPCEMC and CPSMI can indirectly affect CPCSRA through CPVDM. This shows that consumers perceive both CSR strategy-driven motive and value-driven motive at the same time. Consumers may not make an extreme judgment on CSR motivations. Instead, they may rationally reconcile the contradiction between economic purpose and ethical purpose in CSR motivation. CPSDM and CPVDM play a mediating effect together to positively affect consumer perceptions of CSR authenticity. Therefore, in the process of CSR implementation, company managers can admit to CSR being part of the strategic purpose of the company, rather than deliberately hiding the strategic purpose of CSR efforts.

5.2. Limitations and Future Research

We tried our best to ensure the scientific and rigorous nature of this study. Meanwhile, we tried to make some contributions to theoretical research and company management. However, there are still several shortcomings that need to be further studied in the future.

5.2.1. Model Extension

This study only discusses the six factors (i.e., four of CSR commitment and two of CSR motivation) related to CPCSRA. In addition, community links and transparency [14] can also be discussed in the follow-up studies as antecedent variables.

There are four motives underpinning CSR: the strategic motive, values driven motive, stakeholder driven motive and egoistic motive [32]. This paper focuses on two positive valence motivations. Subsequent studies can focus on the negative valence motivations.

Some researchers suggest the existance of CSR hypocrisy, which is the opposite concept of perceived CSR authenticity [82]. They point out that inconsistent CSR information and CSR communication strategies can underpin CSR hypocrisy. Therefore, subsequent studies can also try to add the characteristics of CSR information and CSR communication into the research framework of CPCSRA.

5.2.2. Data Extension

This study adopted a questionnaire survey method which only used Chinese consumers as respondents. Therefore, the results were limited by geography and culture. There may be potential differences between Chinese consumers and other countries that are either developed or developing. As we are not sure if our findings are different in different cultural environments, follow-up studies could collect data in a cross-cultural environment and discuss the data further. In addition, follow-up research can classify the samples according to the consumers of different types of companies or different sizes of companies. We can conduct a comparative analysis based on the classification. Due to the limitation of research funding, it was difficult for us to expand our sample size and sample range. We hope follow-up research can improve on this.

Our questionnaire data were collected by a professional questionnaire collection company and social media. The data collection involved snowballing. This inevitably leads to the problem that respondents are limited to a group of people with similar ideas and attributes. This may result in underrepresentation. Thus, future research could expand the scope of questionnaire collection or use other sampling methods to collect data. Finally, the conclusion of this study is bound to be limited by the cross-sectional design. Future studies can combine time series analysis to form panel data to enhance the persuasiveness of theoretical reasoning.

Author Contributions

Conceiving Research and Designing Research Framework, J.Y. and S.N.; Collecting and Analyzing Data, J.Y., C.J. and X.Z.; Writing the paper, J.Y. and Z.C. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by National Natural Science Foundation of China, grant number 61762055; Jiangxi Provincial Natural Science Foundation of China, grant number 20181BAB202014; and Jiangxi Provincial Education Department of China, grant number GJJ190899.

Acknowledgments

This paper was supported by Wonkwang University in 2020.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Jones, D.A.; Willness, C.R.; Glavas, A. When corporate social responsibility (CSR) meets organizational psychology: New frontiers in micro-CSR research, and fulfilling a quid pro quo through multilevel insights. Front. Psychol. 2017, 8, 520. [Google Scholar] [CrossRef] [PubMed]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Vilanova, M.; Lozano, J.M.; Arenas, D. Exploring the nature of the relationship between CSR and competitiveness. J. Bus. Ethics 2009, 87, 57–69. [Google Scholar] [CrossRef]

- Bernal-Conesa, J.A.; de Nieves Nieto, C.; Briones-Peñalver, A.J. CSR strategy in technology companies: Its influence on performance, competitiveness and sustainability. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 96–107. [Google Scholar] [CrossRef]

- Bhattacharya, C.B.; Sen, S. Doing better at doing good: When, why, and how consumers respond to corporate social initiatives. Calif. Manag. Rev. 2004, 47, 9–24. [Google Scholar] [CrossRef]

- Lichtenstein, D.R.; Drumwright, M.E.; Braig, B.M. The effect of corporate social responsibility on customer donations to corporate-supported nonprofits. J. Mark. 2004, 68, 16–32. [Google Scholar] [CrossRef]

- Madrigal, R.; Boush, D.M. Social responsibility as a unique dimension of brand personality and consumers’ willingness to reward. Psychol. Mark. 2008, 25, 538–564. [Google Scholar] [CrossRef]

- Greenley, G.E.; Foxall, G.R. Consumer and nonconsumer stakeholder orientation in UK companies. J. Bus. Res. 1996, 35, 105–116. [Google Scholar] [CrossRef]

- Yoo, D.; Lee, J. The effects of corporate social responsibility (CSR) fit and CSR consistency on company evaluation: The role of CSR support. Sustainability 2018, 10, 2956. [Google Scholar] [CrossRef]

- Alhouti, S.; Johnson, C.M.; Holloway, B.B. Corporate social responsibility authenticity: Investigating its antecedents and outcomes. J. Bus. Res. 2016, 69, 1242–1249. [Google Scholar] [CrossRef]

- Cheng, W.; Appolloni, A.; D’Amatoc, A.; Zhu, Q. Green Public Procurement, Missing Concepts and Future Trends – A Critical Review. J. Clean. Prod. 2018, 176, 770–784. [Google Scholar] [CrossRef]

- Kingsley Nduneseokwu, C.; Qu, Y.; Appolloni, A. Factors Influencing Consumers’ Intentions to Participate in a Formal E-Waste Collection System: A Case Study of Onitsha, Nigeria. Sustainability 2017, 9, 881. [Google Scholar] [CrossRef]

- Webb, D.J.; Mohr, L.A. A typology of consumer responses to cause-related marketing: From skeptics to socially concerned. J. Public Policy Mark. 1998, 17, 226–238. [Google Scholar] [CrossRef]

- Mohr, L.A.; Webb, D.J.; Harris, K.E. Do consumers expect companies to be socially responsible? The impact of corporate social responsibility on buying behavior. J. Consum. Aff. 2001, 35, 45–72. [Google Scholar] [CrossRef]

- Joo, S.; Miller, E.G.; Fink, J.S. Consumer evaluations of CSR authenticity: Development and validation of a multidimensional CSR authenticity scale. J. Bus. Res. 2019, 98, 236–249. [Google Scholar] [CrossRef]

- Kim, Y.J.; Lee, W.-N. Overcoming consumer skepticism in cause-related marketing: The effects of corporate social responsibility and donation size claim objectivity. J. Promot. Manag. 2009, 15, 465–483. [Google Scholar] [CrossRef]

- Skarmeas, D.; Leonidou, C.N. When consumers doubt, watch out! The role of CSR skepticism. J. Bus. Res. 2013, 66, 1831–1838. [Google Scholar] [CrossRef]

- Beverland, M. The real thing: Branding authenticity in the luxury wine trade. J. Bus. Res. 2006, 59, 251–258. [Google Scholar] [CrossRef]

- Schaefer, A.D.; Pettijohn, C.E. The relevance of authenticity in personal selling: Is genuineness an asset or liability? J. Mark. Theory Pract. 2006, 14, 25–35. [Google Scholar] [CrossRef]

- Aupperle, K.E.; Carroll, A.B.; Hatfield, J.D. An empirical examination of the relationship between corporate social responsibility and profitability. Acad. Manag. J. 1985, 28, 446–463. [Google Scholar]

- Ruf, B.M.; Muralidhar, K.; Paul, K. The development of a systematic, aggregate measure of corporate social performance. J. Manag. 1998, 24, 119–133. [Google Scholar] [CrossRef]

- Yates, M. Dynamics and Effects of Corporate Social Responsibility Authenticity. Ph.D. Thesis, University of Cincinnati, Cincinnati, OH, USA, 2018. [Google Scholar]

- Beckman, T.; Colwell, A.; Cunningham, P.H. The emergence of corporate social responsibility in Chile: The importance of authenticity and social networks. J. Bus. Ethics 2009, 86, 191. [Google Scholar] [CrossRef]

- McShane, L.; Cunningham, P. To thine own self be true? Employees’ judgments of the authenticity of their organization’s corporate social responsibility program. J. Bus. Ethics 2012, 108, 81–100. [Google Scholar] [CrossRef]

- Lee, S.; Yoon, J. Does the authenticity of corporate social responsibility affect employee commitment? Soc. Behav. Personal. Int. J. 2018, 46, 617–632. [Google Scholar] [CrossRef]

- Ji, S.; Jan, I.U. The Impact of Perceived Corporate Social Responsibility on Frontline Employee’s Emotional Labor Strategies. Sustainability 2019, 11, 1780. [Google Scholar] [CrossRef]

- Wang, H.; Gibson, C.; Zander, U. Editors’ Comments: Is Research on Corporate Social Responsibility Undertheorized; Academy of Management Briarcliff Manor: New York, NY, USA, 2020. [Google Scholar]

- Pan, X.; Chen, X.; Ning, L. The roles of macro and micro institutions in corporate social responsibility (CSR). Manag. Decis. 2018. [Google Scholar] [CrossRef]

- Rupp, D.E.; Mallory, D.B. Corporate social responsibility: Psychological, person-centric, and progressing. Annu. Rev. Organ. Psychol. Organ. Behav. 2015, 2, 211–236. [Google Scholar] [CrossRef]

- Jo, H.; Na, H. Does CSR reduce firm risk? Evidence from controversial industry sectors. J. Bus. Ethics 2012, 110, 441–456. [Google Scholar] [CrossRef]

- Bhattacharya, C.B.; Sen, S. Consumer–company identification: A framework for understanding consumers’ relationships with companies. J. Mark. 2003, 67, 76–88. [Google Scholar] [CrossRef]

- Ellen, P.S.; Webb, D.J.; Mohr, L.A. Building corporate associations: Consumer attributions for corporate socially responsible programs. J. Acad. Mark. Sci. 2006, 34, 147–157. [Google Scholar] [CrossRef]

- Jeon, M.A.; An, D. A study on the relationship between perceived CSR motives, authenticity and company attitudes: A comparative analysis of cause promotion and cause-related marketing. Asian J. Sustain. Soc. Responsib. 2019, 4, 7. [Google Scholar] [CrossRef]

- Questionnaire Star. Available online: https://www.wjx.cn/ (accessed on 20 October 2019).

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Carroll, A.B.; Buchholtz, A.K. Ethics and Stakeholder Management; South-Western: Cincinnati, OH, USA, 1996. [Google Scholar]

- Hill, C.W.; Jones, T.M. Stakeholder-agency theory. J. Manag. Stud. 1992, 29, 131–154. [Google Scholar] [CrossRef]

- Driver, M. Beyond the stalemate of economics versus ethics: Corporate social responsibility and the discourse of the organizational self. J. Bus. Ethics 2006, 66, 337–356. [Google Scholar] [CrossRef]

- Anton, C. Selfhood and Authenticity; Suny Press: Albany, NY, USA, 2001. [Google Scholar]

- Liedtka, J. Strategy making and the search for authenticity. J. Bus. Ethics 2008, 80, 237–248. [Google Scholar] [CrossRef]

- Mazutis, D.D.; Slawinski, N. Reconnecting business and society: Perceptions of authenticity in corporate social responsibility. J. Bus. Ethics 2015, 131, 137–150. [Google Scholar] [CrossRef]

- Kim, S.; Lee, H. The Effect of CSR Fit and CSR Authenticity on the Brand Attitude. Sustainability 2020, 12, 275. [Google Scholar] [CrossRef]

- Yoh, T. The Effects of Cause-Related Marketing for Corporate Transgressions on Consumer Responses; Department of Marketing in the Graduate School, Southern Illinois University Carbondale: Caldburn, IL, USA, 2018. [Google Scholar]

- Dwyer, F.R.; Schurr, P.H.; Oh, S. Developing buyer-seller relationships. J. Mark. 1987, 51, 11–27. [Google Scholar] [CrossRef]

- Macleod, S. Why worry about CSR? Strateg. Commun. Manag. 2001, 5, 8–9. [Google Scholar]

- Miller, B.A. Social initiatives can boost loyalty. Mark. News 2002, 36, 14–15. [Google Scholar]

- Varadarajan, P.R.; Menon, A. Cause-related marketing: A coalignment of marketing strategy and corporate philanthropy. J. Mark. 1988, 52, 58–74. [Google Scholar] [CrossRef]

- MacMillan, K.; Money, K.; Money, A.; Downing, S. Relationship marketing in the not-for-profit sector: An extension and application of the commitment–trust theory. J. Bus. Res. 2005, 58, 806–818. [Google Scholar] [CrossRef]

- Van den Brink, D.; Odekerken-Schröder, G.; Pauwels, P. The effect of strategic and tactical cause-related marketing on consumers’ brand loyalty. J. Consum. Mark. 2006. [Google Scholar] [CrossRef]

- Crilly, D.; Schneider, S.C.; Zollo, M. Psychological antecedents to socially responsible behavior. Eur. Manag. Rev. 2008, 5, 175–190. [Google Scholar] [CrossRef]

- Ones, D.S.; Dilchert, S. Environmental sustainability at work: A call to action. Ind. Organ. Psychol. 2012, 5, 444–466. [Google Scholar] [CrossRef]

- Friestad, M.; Wright, P. The persuasion knowledge model: How people cope with persuasion attempts. J. Consum. Res. 1994, 21, 1–31. [Google Scholar] [CrossRef]

- Osterhus, T.L. Pro-social consumer influence strategies: When and how do they work? J. Mark. 1997, 61, 16–29. [Google Scholar] [CrossRef]

- Handelman, J.M.; Arnold, S.J. The role of marketing actions with a social dimension: Appeals to the institutional environment. J. Mark. 1999, 63, 33–48. [Google Scholar] [CrossRef]

- Lafferty, B.A.; Goldsmith, R.E. Corporate credibility’s role in consumers’ attitudes and purchase intentions when a high versus a low credibility endorser is used in the ad. J. Bus. Res. 1999, 44, 109–116. [Google Scholar] [CrossRef]

- Foreh, M.R.; Grier, S. When is honesty the best policy? The effect of stated company intent on consumer skepticism. J. Consum. Psychol. 2003, 13, 349–356. [Google Scholar] [CrossRef]

- Drumwright, M.E. Company advertising with a social dimension: The role of noneconomic criteria. J. Mark. 1996, 60, 71–87. [Google Scholar] [CrossRef]

- Barone, M.J.; Miyazaki, A.D.; Taylor, K.A. The influence of cause-related marketing on consumer choice: Does one good turn deserve another? J. Acad. Mark. Sci. 2000, 28, 248–262. [Google Scholar] [CrossRef]

- Williams, P.; Aaker, J.L. Can mixed emotions peacefully coexist? J. Consum. Res. 2002, 28, 636–649. [Google Scholar] [CrossRef]

- Whetten, D.A.; Mackey, A. A social actor conception of organizational identity and its implications for the study of organizational reputation. Bus. Soc. 2002, 41, 393–414. [Google Scholar] [CrossRef]

- Till, B.D.; Nowak, L.I. Toward effective use of cause-related marketing alliances. J. Prod. Brand Manag. 2000. [Google Scholar] [CrossRef]

- Biswas, A.; Burton, S. Consumer perceptions of tensile price claims in advertisements: An assessment of claim types across different discount levels. J. Acad. Mark. Sci. 1993, 21, 217–229. [Google Scholar] [CrossRef]

- Becker-Olsen, K.L.; Cudmore, B.A.; Hill, R.P. The impact of perceived corporate social responsibility on consumer behavior. J. Bus. Res. 2006, 59, 46–53. [Google Scholar] [CrossRef]

- Keller, K.L.; Aaker, D.A. The effects of sequential introduction of brand extensions. J. Mark. Res. 1992, 29, 35–50. [Google Scholar] [CrossRef]

- De Wulf, K.; Odekerken-Schröder, G.; Iacobucci, D. Investments in consumer relationships: A cross-country and cross-industry exploration. J. Mark. 2001, 65, 33–50. [Google Scholar] [CrossRef]

- Vlachos, P.A.; Theotokis, A.; Panagopoulos, N.G. Sales force reactions to corporate social responsibility: Attributions, outcomes, and the mediating role of organizational trust. Ind. Mark. Manag. 2010, 39, 1207–1218. [Google Scholar] [CrossRef]

- Groza, M.D.; Pronschinske, M.R.; Walker, M. Perceived organizational motives and consumer responses to proactive and reactive CSR. J. Bus. Ethics 2011, 102, 639–652. [Google Scholar] [CrossRef]

- Du, S.; Bhattacharya, C.B.; Sen, S. Reaping relational rewards from corporate social responsibility: The role of competitive positioning. Int. J. Res. Mark. 2007, 24, 224–241. [Google Scholar] [CrossRef]

- Tavakol, M.; Dennick, R. Making sense of Cronbach’s alpha. Int. J. Med. Educ. 2011, 2, 53. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Tang, X.; Gu, Y. Forced smiles or true feelings: Impact of organizational identification and organization-based self-esteem on service employees’ emotional labor. Tour. Trib. 2016, 31, 68–80. [Google Scholar]

- Byrne, B.M. Structural equation modeling with AMOS: Basic concepts, applications and programming. In Applications, and Programming; Erlbaum: Mahwah, NJ, USA, 2001. [Google Scholar]

- Kristal, M.M.; Huang, X.; Roth, A.V. The effect of an ambidextrous supply chain strategy on combinative competitive capabilities and business performance. J. Oper. Manag. 2010, 28, 415–429. [Google Scholar] [CrossRef]

- Shen, X.-L.; Cheung, C.M.; Lee, M.K. Perceived critical mass and collective intention in social media-supported small group communication. Int. J. Inf. Manag. 2013, 33, 707–715. [Google Scholar] [CrossRef]

- MacKinnon, D.P.; Lockwood, C.M.; Hoffman, J.M.; West, S.G.; Sheet, V. A comparison of methods to test mediation and other intervening variable effects. Psychol. Methods 2002, 7, 83. [Google Scholar] [CrossRef]

- Hayes, A.F. Beyond Baron and Kenny: Statistical mediation analysis in the new millennium. Commun. Monogr. 2009, 76, 408–420. [Google Scholar] [CrossRef]

- Sobel, M.E. Asymptotic confidence intervals for indirect effects in structural equation models. Sociol. Methodol. 1982, 13, 290–312. [Google Scholar] [CrossRef]

- Bollen, K.A.; Stine, R. Direct and indirect effects: Classical and bootstrap estimates of variability. Sociol. Methodol. 1990, 115–140. [Google Scholar] [CrossRef]

- Stone, C.A.; Sobel, M.E. The robustness of estimates of total indirect effects in covariance structure models estimated by maximum. Psychometrika 1990, 55, 337–352. [Google Scholar] [CrossRef]

- Holbert, R.L.; Stephenson, M.T. The importance of indirect effects in media effects research: Testing for mediation in structural equation modeling. J. Broadcasting Electron. Media 2003, 47, 556–572. [Google Scholar] [CrossRef]

- MacKinnon, D. Introduction to Statistical Mediation Analysis; Routledge: Abingdon upon Thames, UK, 2012. [Google Scholar]

- Wagner, T.; Lutz, R.J.; Weitz, B.A. Corporate hypocrisy: Overcoming the threat of inconsistent corporate social responsibility perceptions. J. Mark. 2009, 73, 77–91. [Google Scholar] [CrossRef]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).