1. Introduction

Sustainability reporting is now one of the most relevant topics both for managers and researchers. With the aim of contributing to a better understanding about how companies deal with sustainability, we considered three perspectives. First, we examined the luxury sector by focusing on the top 100 ‘Global Powers of Luxury Goods 2019’ as listed by Deloitte [

1]. Secondly, we looked at the sustainability initiatives of these companies with a focus on China. Finally, we addressed the issue of sustainability from the reporting point of view. We aimed to provide both a picture of the overall approach to sustainability adopted in China by large luxury companies and a better understanding of the reasons pushing these companies to report their China-specific sustainability initiatives.

According to Deloitte, despite the recent slowdown in economic growth in major markets including China, the Eurozone, and the U.S., the luxury goods market looks positive and the world’s top 100 luxury companies generated revenues of USD

$247 billion in FY2017, registering an annual growth of 10.8%. The financial dimension matters, but other reasons support the importance of focusing on the luxury sector. Luxury is experiencing a social, generational, behavioral, and habits revolution. Companies are facing new consumer awareness, the redefinition of reference values, and the opportunities offered by social media and new technologies. Changes in the sector are on the agenda and sustainability is increasingly considered as part of the luxury essence [

2,

3].

The debate about this issue is thoroughly developed in the literature and several contributions reflect the apparent paradox or contradiction between the two concepts of sustainability and luxury [

4,

5]. For some authors, the match depends on how consumers, or at least some categories of consumers, define luxury [

5,

6,

7]. For others, the essence of luxury brands, which is traditionally based on high quality, superior durability, and deeper value, is a perfect basis for the design and marketing of products that preserve fundamental environmental and social values [

8]. Finally, other authors focused on the process of incorporating the theme of sustainability into the strategies of these companies, identifying some best reference practices [

9,

10].

The observation of the relationship between sustainability and luxury from the Chinese geographical perspective adds further elements of interest. China represents an ideal counterpoint between luxury and sustainability not only because the Chinese government has prioritized sustainable development [

11], but also because the number of Chinese high-earners-not-rich-yet (HENRY) consumers of luxury goods is growing exponentially. The HENRY consumers are the cohort of middle-class millennials and younger that is emerging within the luxury sector [

1]. A growing number of contributions focus on the topic of sustainability in the Chinese market [

12,

13,

14] and reporting practices by Chinese companies [

15,

16]. In the Chinese luxury market, many contributions investigated consumers’ perceptions and the importance for companies to develop country-specific strategies [

17,

18,

19].

The remainder of this paper is organized as follows:

Section 2 outlines a literature review on sustainability reporting that provides the basis for the formulation of the hypotheses.

Section 3 describes the research methods, and the operationalization of the factors that affect the adoption of a sustainability report, and the reporting of China-specific initiatives by the Global Powers of Luxury Goods.

Section 4 presents both qualitative and quantitative results. In the final section, findings are discussed, and conclusions are drawn.

2. Sustainability Reporting

Sustainability reporting is today a common practice through which companies tell their stakeholders and, more generally, the public about how they intend to contribute to the satisfaction of general interests, such as environmental protection and society prosperity. When a company selects some content for its sustainability report, the rationale is to provide evidence about how certain topics or geographical areas are considered in the management of the business. Through analysis of the report’s content, it is possible to understand the company’s approach to sustainability. If the analysis focuses on country-specific initiatives, evidence may be provided about how a company conceives the relationship between its business and sustainability in that specific geographical context.

2.1. Historical and Theoretical Background

Companies started to report their non-financial performance in the 1970s [

20]. A first material issue, reported by some companies, was employee welfare. Later, product quality and social engagement began to be relevant. Environmental catastrophes in the 1980s raised awareness about the impact of business on the environment and some companies started to report their engagement in those issues [

21]. In the late 1990s, the focus shifted from a topic-related to a more comprehensive approach with the first instances of integrating reporting [

22]. Since the new century, sustainability reports have been seen as strategic instruments developed to engage stakeholders and measure results by considering the so-called triple bottom line [

23]. The number of companies that report on their sustainability has rapidly increased; today, sustainability reports are a common practice at least, but not exclusively, for big companies all over the world, including China [

15]. One of the most common standards in sustainability reporting is represented by the global reporting initiative (GRI), which is often used to increase credibility. The heterogeneity is still high, and a common methodology seems far from being adopted [

24]. The number of companies that publish sustainability reports varies from sector to sector. Until the 1990s, the most frequent and sophisticated experiences were in chemicals, oil and gas, automotive, utilities, electronics, and food and beverages. Then, sustainability reporting practice spread rapidly to other sectors like financial, trade and retail, services, communications, media, and luxury. Sustainability reporting by the Global Powers of Luxury Goods is still far from being a common practice, but some elements of uniformity are starting to be evident.

For sustainability, each company adopts a different strategy; this heterogeneity is obviously reflected in the reporting contents. However, other factors are important for understanding different approaches [

25]. Some authors considered the factors that can influence the document’s adoption, others focused on the extent, and others on the quality of reporting [

26,

27,

28]. Even if research on sustainability reporting is characterized by a lack of a comprehensive theoretical reference point, most contributions mainly refer to two theoretical frameworks: Stakeholder and institutional theory.

According to stakeholder theory, the company’s strategy is developed considering the subjects that are considered main stakeholders [

29]. The literature identifies many factors that contribute to identifying which stakeholders may be relevant: The company’s dimension, the nationality, the business sector, the composition of the governing bodies, the structure of the supply chain, and the presence in some markets. A different mix of relevant stakeholders may result in a different reporting approach, since companies choose to report their results to provide positive feedback to those actors who have certain expectations [

30,

31]. This theoretical framework can thus be applied to the analysis of sustainability reporting practices to better explain different approaches.

According to institutional theory, companies that share some institutional references, like legislation, managerial culture, and competitive scenario, tend to adopt similar decision-making processes [

32]. Since these references tend to be more uniform if we consider companies of the same nationality belonging to the same sector, these companies tend to adopt more similar structures, strategies, and processes [

33,

34]. This similarity is often defined as isomorphism, which can help better understand the adoption of common sustainability reporting practices.

2.2. The Adoption of The Sustainability Report

A first line of investigation involved analyzing whether the variability of the aforementioned factors among the Global Powers of Luxury Goods led to different choices in terms of sustainability reporting, that is, whether it is possible to trace the adoption of the sustainability report to some factors that express the relevance of some stakeholders and the influence of common institutional references. In the following, each factor is briefly discussed, and research hypotheses are introduced.

A company’s dimension in terms of revenue is one of the most relevant factors considered when analyzing determinants of sustainability reporting adoption. Some studies reported a positive correlation among revenue and presence of sustainability reports, in particular due to the higher paid dividend and share price [

35]. Others suggested that larger firms are more likely to meet stakeholders’ expectations by reporting about their sustainability [

36,

37]. Similarly, the size of the firm and its visibility, taken independently, both influence the company’s decision to disclose non-financial information through sustainability reports [

38]. Although other contributions seem to weaken the strength of the relationship between the size of revenue and the adoption of sustainability reports [

39,

40], in general, a certain agreement exists that large companies, such as the Global Power of Luxury Goods, are inclined to report their sustainability initiatives.

Hypothesis 1. The bigger the company in terms of revenue, the more likely a sustainability report is adopted.

A second relevant factor is the company’s nationality. According to Wanderley et al. [

41], the country of origin together with the industry sector strongly influence whether companies disclose sustainability information on their website. Another study revealed that the strong correlation between sustainability and the national context is related to the importance of a country’s development of such institutional capacity to promote and support sustainability practices [

42]. Evidence also supports differences in the content of sustainability disclosure depending on the corporate’s nationality. In accordance with another comparative study, for example, German companies are more committed to environmental reporting, whereas U.S. corporations tend to disclose more about social issues [

43]. Differences may be due to institutional arrangements [

44] or to different business systems intuitively varying among countries [

45].

Hypothesis 2. The company’s nationality affects the adoption of sustainability reports.

The business sector represents a third relevant factor in the analysis of sustainability reporting practices [

41]. According to Gamerschlag et al. [

46], the company’s size and industry membership influence the amount of sustainability disclosure. The GRI itself, despite being an institutionalized set of standards, provides sector-specific guidelines to be addressed to different corporate sustainability priorities [

47]. Differences exist not only in terms of sustainability reporting attitude, but also in the content of non-financial information disclosed and the selection of indicators [

48]. Similar findings were also reported by Adnan et al. [

49]: Different stakeholders expectations coincide with different reported sustainability information.

Hypothesis 3. The company’s sector affects sustainability report adoption.

Shifting the analysis to the corporate governance dimension, a fourth relevant factor in sustainability reporting is the presence of a sustainability committee or a working group on the board that focuses on the impacts of the company’s policies on social, environmental, and other matters of significance on the firm’s reputation. The literature states that the quality of sustainability disclosure increases when a sustainability committee exists [

50], which may be due to reporting seemingly representing the main task of the sustainability committee, which, instead of focusing on sustainability performance, stops to consider whether an issue is well reported, or even if it should be reported [

51,

52].

Hypothesis 4. The presence of a sustainability committee positively affects the adoption of a sustainability report.

2.3. The Reporting of China-Specific Sustainability Initiatives

A second line of investigation was aimed to understand if the presence of some factors affects the selection of sustainability reports’ contents with specific attention to China-specific sustainability initiatives. Taking stakeholder theory as a reference, we assumed that when the Chinese market is a priority for a luxury company, the relevance of this market and its stakeholders will push to develop and report more China-specific sustainability initiatives. From an institutional theory perspective, companies that share similar institutional references are likely to develop similar sustainability strategies. Therefore, a certain level of uniformity in the reporting approaches of the China-specific sustainability initiatives was expected from the companies that have the same nationality and conduct business in the same sector.

The set of hypotheses introduced in the previous subsection can therefore be reformulated by focusing on how Global Powers of Luxury Goods report their China-specific sustainability initiatives:

Hypothesis 1A. The bigger the company in terms of revenue, the more likely the company is to report about China-specific sustainability initiatives.

Hypothesis 2A. Convergence in the reporting of China-specific sustainability initiatives is expected depending on a company’s nationality.

Hypothesis 3A. Convergence in the reporting of China-specific sustainability initiatives depends on a company’s sector.

Hypothesis 4A. The presence of a sustainability committee positively affects the reporting of China-specific sustainability initiatives.

The reference literature offers some evidence about further factors that may influence sustainability strategies and the development of country-specific initiatives. Thus, in this analysis of the Global Powers of Luxury Goods sustainability reports, the following were considered: The presence of a director from East Asia on the company board, the management of the supply chain and/or operation in China, and reference to China as a key market in terms of revenue.

With regards to the board composition, the literature supports the hypothesis of a greater sustainability commitment when the board of directors embodies some key characteristics such as diversity or inclusivity, i.e., whenever the board is in balance in terms of gender or when people from different nationalities are directors in a multinational company’s board [

53,

54,

55]. No evidence from the literature was found regarding the influence and type of influence of foreign national directorship in a multi-national company’s board on sustainability disclosure toward its own country of origin when that country is a key market for the company, either in terms of supply or demand. Regardless, we assumed that directors’ nationality represents a fifth relevant factor affecting sustainability reporting contents.

Hypothesis 5. The presence of directors from East Asia on the board positively affects the reporting of China-specific sustainability initiatives.

A sixth relevant factor is the management of the supply chain and operations in a specific country. In this particular context, a localized approach is stressed in opposition to the global integration of sustainability reporting disclosure. According to Reimann et al. [

56], although global sustainability can offer advantages of coherence and responsiveness to global stakeholders, it risks being resentfully perceived as culturally absolutist or ethically imperialistic at the local level. The company commitment on a specific country or the exposure to countries where more stringent sustainability models and policies are applied is affected by factors that place pressure on sustainability reporting and engagement with regards to that specific location [

57,

58]. The selection of sustainability report contents may vary depending either on institutional arrangements or business systems that not only pertain to the country of incorporation, but also tend to embody those of the country where the corporate’s operations are predominantly conducted [

44,

45].

Hypothesis 6. The supply chain and operations management in China by a company positively affects the reporting of China-specific sustainability initiatives.

The last factor considered was the reference to China as a key market in terms of revenues. By stressing that information in its sustainability report, a company provides evidence to stakeholders about the importance of Chinese consumers. As a result, the company can be expected to prioritize these consumers and report as much information as possible about its China-specific sustainability initiatives. The literature confirms that consumers are among the salient stakeholders to whom non-financial information is reported, whereas industry associations, communities, and employees have a lesser impact [

59]. According to Park and Ghauri [

60], among all the stakeholders, consumers appear to be particularly influential as they either tend to switch brands, influenced by the sustainability commitment, keeping constant the other variables such as price and quality, or they interfere positively when the company is proactive in corporate citizenship or negatively when it is not. According to Crilly et al. [

61], the liability of foreignness perceived by local stakeholders such as customers can be minimized by reporting about do-good sustainability (creating positive externalities), more than just reporting about do-no-harm sustainability (attenuating negative externalities).

Hypothesis 7. If a company reports about China as a key market in terms of revenue, the reporting of China-specific sustainability initiatives is positively affected.

3. Research Methods and Data Collection

This section describes the sample of companies considered and how the variables were operationalized. The research was conducted on the top 100 luxury companies listed in terms of revenues by Deloitte’s report on Global Powers of Luxury Goods 2019 [

1]. In that report, luxury goods refer to luxury for personal use created for and purchased by the ultimate consumer and sold under a well-known luxury brand. As product categories, the ranking considers designer clothing and footwear (ready-to-wear), luxury bags and accessories (including eyewear), luxury jewelry and watches, and prestige cosmetics and fragrances, but it does not include automobiles, travel, and leisure services, boating and yachts, fine art and collectibles, and fine wines and spirits. Retailers of other companies’ luxury brands are also excluded.

Each assessed company reported consolidated luxury goods sales (at a 50% hurdle) in the fiscal year 2017, which is defined as the 12 months of the financial year ending 30 June 2018. Net sales were all converted to USD; consequently, exchange rate may have been discriminant. No geographical limitation was considered. Although the list of the top 100 luxury companies released by Deloitte in 2019 represents a panel of companies that, if taken together, are arguably a plausible reflection of a substantial share of the market, the list is neither all-inclusive nor exhaustive.

3.1. Dependent Variables

In the methodological approach, we considered two dependent variables: The presence of a sustainability report (‘report’) and the extent to which luxury companies report about China-specific sustainability initiatives (‘China info’).

The ‘report’ variable was measured using a binary solution: 1 when there is a kind of report and 0 otherwise. We focused on the sustainability reports referring to the two-year period 2017–2018, in line with the time horizon adopted by Deloitte in its report. All kind of reports were considered, assuming that a company can voluntary disclose its sustainability strategy either in a separate report or through an integrated financial report. As a result, 45 sustainability standalone or integrated reports were found.

The China-specific initiative variable (‘China info’) was assessed through a content analysis. A search by keywords was applied to each report using keywords ‘China’ and ‘Chinese’. The analysis was conducted by seeking information contained in the 2018 companies’ sustainability report when available and in the 2017 report for the two companies for which the 2018 report was not available on the corporate websites. Whenever the words were found in the publications, we personally evaluated the significance of the information disclosed, focusing on the identification of specific initiatives linked to China. To classify every initiative under a common framework, the GRI standard framework was applied. The 136 identified initiatives were classified into one of the three impact categories (economic, environmental, or social) then into one of the topic-specific standard categories. In some cases, content referring to a specific initiative was classified in more than one topic-specific standard category. As a further step, the initiatives’ analysis under each impact category was converted into a 3-point scale index on the basis of the amount of initiatives reported by the company: ‘1’ if one sustainability initiative was reported as actuated in China; ‘2’ if two sustainability initiatives were reported as actuated in China; and ‘3’ if three or more sustainability initiatives were reported as actuated in China. Through this methodology, the values of three additional variables (economic, environmental, and social), referring to China-specific initiatives in the three GRI areas of impact, were measured for each report. Finally, a synthetic additive index that provides an ultimate assessment of the company’s linkage with the Chinese market in terms of sustainability initiatives reporting extent was created. The additive index ‘China info’ was evaluated on a 9-point scale.

3.2. Factors Affecting Sustainability Reporting

The two dependent variables were then correlated to a selection of factors that, according to the literature review and the previous discussion, play a relevant role in influencing sustainability reporting: Company dimension (‘REV’); company’s nationality (‘GEO’); company specialization in fashion, beauty, or jewelry sub-sectors (‘SEC’); the presence of a sustainability committee (‘COM’), the presence of directors from East Asia on the board (‘BRD’); the management of the supply chain and operations in China (‘SCO’); and direct reference to China as a key market in terms of revenue in the company’s financial or non-financial reports (‘MKT’).

Information about companies’ dimensions in terms of revenues (REV) and nationality (GEO) were collected from the Global Powers of Luxury Goods 2019 Deloitte report.

Companies’ nationalities were geographically clustered with the following rationales: Italy, almost one-fourth of the companies listed are headquartered in Italy; U.S., the second largest group of companies on the list are from the United States; France, the best-performing country in terms of composite sales growth and contributes the largest share to the total sales of the companies ranked; GCH, which stands for Greater China and includes Mainland China and Hong Kong SAR (Special Administrative Region) based companies; and ROW, the rest of the world companies on the list.

For differentiation of companies within the luxury sector, three business industries were considered (SEC): ‘Fashion’ includes designer clothing, footwear, luxury bags, and accessories including eyewear; ‘Beauty’ includes prestige cosmetics and fragrances; and ‘Jewelry’ includes fine jewelry and watches. Business industry was attributed based on what the company specified in its reports and the analysis of the contents of the reports.

The presence of a sustainability committee (COM) was derived from the company’s website, usually under the heading ‘Corporate Governance’ and ‘Committees’ and was measured in a binary system: ‘0’ if the sustainability committee was neither present nor mentioned; ‘1’ if a sustainability committee was included in the boards’ committees.

The presence of East Asia in the board of directors (BRD) was assessed by checking companies’ websites under the heading ‘Corporate Governance’ and scrolling through the names, personal details, and pictures of the board members and looking them up on the Internet when in doubt with regard to their origins (Mainland China, Hong Kong, Macau, Taiwan, Mongolia, North Korea, South Korea, Japan): ‘0’ was assigned if there were no East Asian members on the board of directors; ‘1’ was assigned if at least one East Asian as a member of the board or, when if the company was East Asian.

For the supply chain management and operation in China (SCO), a keywords search was conducted for the words ‘China’, ‘Chinese’ and the correspondence with the words ‘supply’, ‘supplier’, ‘operation’, ‘manufacturing’, ‘manufactured’, ‘plant’, ‘facility’, ‘facilities’, ‘factory’, ‘factories’, ‘sourcing’, and ‘assembly’ in the available reports, either disclosing financial or non-financial information: ‘0’ was assigned when there was no findings; ‘1’ was assigned when the company disclosed that either it has Chinese suppliers or it carries out its operations, at least partly, in China.

To define whether a company discloses its market presence in China in terms of revenue (MKT), another keywords search was conducted, looking for ‘China’ and ‘Chinese’ in relation to ‘revenue’, ‘sales’, and ‘market share’ in all the available reports, either disclosing 2018 financial or non-financial information: ‘0’ was assigned if the company never mentioned the one and the other together; or ‘1’ if they did.

4. Results

The analysis of sustainability reports of the Global Powers of Luxury Goods 2019 resulted in evidence of the relevance of this practice and the importance of China-specific initiatives. Of the 100 Global Powers of Luxury Goods, only 45 released a sustainability report or a similar document in the 2017–2018 period, meaning that this practice is far from involving the majority of players in the luxury sector. Before delving into the causes of this result, a short overview of the reported China-specific initiatives reported is presented.

4.1. The Mix of Contents in Sustainability Reports

Of the 45 companies that published a sustainability report, 9 did not report any content about China. Of the remaining 36 reports, 24, 23, and 27 reported in the areas of economic, environmental, and social impacts, respectively. Considering each of the variables individually, in the cases where the company reported one or more initiatives related to China, the average value of the economic variable was 1.30 out of 3, the average value of the environmental variable was 1.32 out of 3, and the average value of the social variable was 1.78 out of 3. Both results confirmed that for companies in the luxury sector that invest in sustainability, the development of social initiatives in China is clearly a priority. On average, the value of the variable ‘China info’ between the 36 companies that reported China-specific initiative was 3.92 out of 9.

Figure 1,

Figure 2 and

Figure 3 show the number of initiatives reported for each one of the GRI topic-specific standard categories belonging to the three impact categories (economic, environmental, and social).

With regards to the economic standards (

Figure 1), the commitment of luxury companies to the Chinese context is specific and demonstrates a strong integration into this peculiar economic context in some cases. The relevant issues include the protection of intellectual property; the monitoring of counterfeiting in factories; the prevention of corruption, actuated as personnel coaching, with handbooks for gift giving/receiving, a specific issue concerning China, very guanxi-related (关系); and through rule-of-thumb assessments for sourced goods.

With reference to environmental initiatives, a substantial convergence of the strategies implemented by companies was observed (

Figure 2). Coherent with the Chinese government agenda that includes green development within the broad concept of national growth [

62], luxury companies reported their strong commitment to environmental initiatives like the implementation of energy, water, and waste efficiency standards and certification and the adoption of ethical practices of key materials sourcing such as cashmere, gold, or silk.

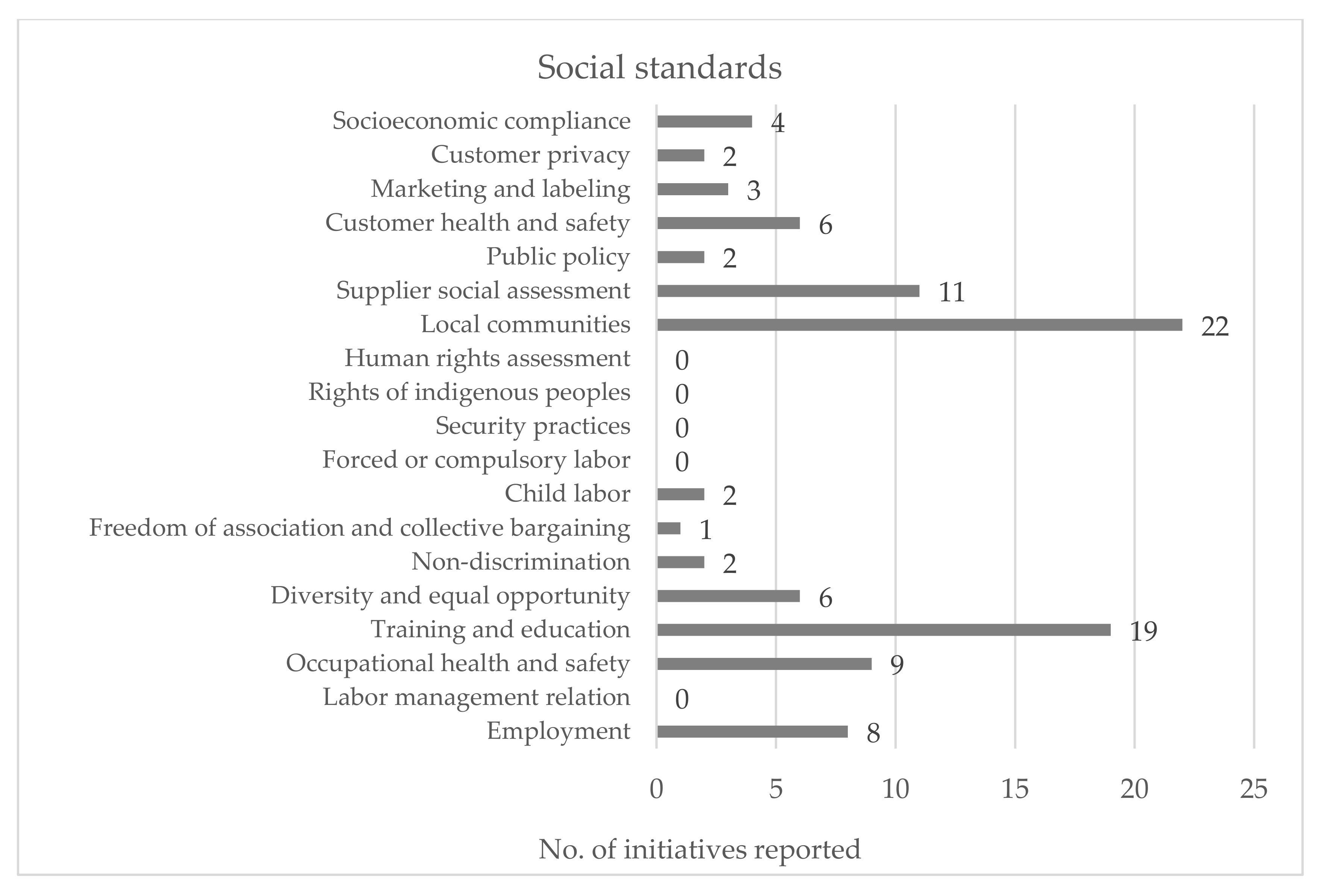

The most part of the social initiatives refers to the two standard categories of training and education and local communities (

Figure 3). This result can be explained by assuming that luxury companies in China try to operate in alignment with the Chinese government development strategy objective of nurturing talent and with the philanthropic dimension sought by Chinese luxury customers. These customers are often wary of the luxury–sustainability combination, preferring that this relationship be associated with terms such as charity and donation, rather than with product attributes or characteristics [

63]. Thus, significant initiatives were reported, such as charity programs for village schools in rural areas, contributions to the fight against cancer, or dedicated to entrepreneurship and innovation.

4.2. Explaining the Adoption of Sustainability Reports

The analysis of the correlation between the adoption of sustainability reports by luxury companies and the four factors considered confirmed some of the related hypotheses (

Table 1).

Luxury firms that released a report showed a tendency to be bigger in terms of revenue. The correlation test between the variables ‘report’ and ‘REV’ confirmed the validity of hypothesis 1 (the bigger the company in terms of revenue, the more it is likely to adopt a sustainability report).

A first aspect to consider in the analysis of the relationship between the presence of a sustainability report and the company’s nationality is the overall distribution of companies among the five clusters: 24 of the 100 companies were headquartered in Italy, 14 in the United States, 7 in France, 9 in Great China, and 21 in the rest of the world. No correlation was observed among the considered variables and therefore hypothesis 2 (company’s nationality affects sustainability report’s adoption) was rejected. Despite this result, the difference in the percentage of companies that published a sustainability report in the five geographic areas considered showed that only 33% (8 out of 24) of Italian companies developed this tool, 50% (7 out of 14) for U.S. companies, 57% (4 out of 7) for French companies, and 55% (5 out of 9) of GCH companies. The percentage for companies in the rest of the world (ROW) was 45% (21 out of 46).

For the sector, the three industries considered, i.e., fashion, jewelry, and beauty, included 57, 32, and 11 companies, respectively. Of the companies that operated in the fashion industry, 45.6% (26 out of 57) released documents about non-financial disclosure. Comparatively, this percentage is relatively an average, as companies in the jewelry industry registered a lower ratio of 37.5% (12 out of 32) and beauty companies registered a higher ratio of 63.6% (7 out of 11). The correlation between ‘report’ and ‘SEC’ was not significant; therefore, hypothesis 3 (company’s sector affects sustainability report’s adoption) was rejected.

Finally, only 28.8% (13 out of the 45) of companies that released a sustainability report actually present a dedicated committee. Only two companies of the 100 had a sustainability committee in their organization but did not publish a sustainability report. So, even though the number of firms within the list that have a committee was limited, almost all released a sustainability report (86.7%). The presence of positive relationship among the variables ‘report’ and ‘COM’ was confirmed by the correlation test, so hypothesis 4 (the presence of a sustainability committee positively affects the adoption of a sustainability report) was supported.

4.3. Explaining the Reporting of China-Specific Sustainability Initiatives

Table 2 presents correlation between the four variables measuring China-specific sustainability initiatives and the factors considered in the first four hypotheses.

According to the correlation test between company’s dimension in terms of revenues (REV) and the set of China-specific variables, larger companies paid more attention to China in their sustainability strategies. This applied in particular to environmental and social initiatives, so hypothesis 1A (the bigger the company in terms of revenue, the more likely it is to report about China-specific sustainability initiatives) was supported.

For the company’s nationality variable (GEO), hypothesis 2A (convergence in the reporting of China-specific sustainability initiatives is expected depending on a company’s nationality) was accepted only for companies based in France, Greater China, and the rest of the world, but not for Italian- and U.S.-based companies. We did not further explore why some countries may demonstrate a significant relationship with country-specific sustainability disclosure. However, it is intuitive that Chinese national luxury companies that release a non-financial report will generally refer to their home country with respect to sustainability reporting. Conversely, the French case is less self-explanatory. We did not speculate on the topic, but Sino–French interstate relations may have an impact on the matter. The analysis of the three standard categories of China-related sustainability reporting confirmed the results.

In the previous step, hypothesis 3, about the relationship between the publishing of a sustainability report and its interdependence on the business industry, was rejected. Similarly, the correlation between ‘China info’ and each of the three industries considered in the results was significant. Only the beauty industry seems to have a significant and negative correlation with the social standards category. This result is counterintuitive, as the beauty sector is presumably the most linked with some social aspects such as consumer health and safety. Therefore, hypothesis 3A (convergence in the reporting of China-specific sustainability initiatives is expected depending on a company’s sector) is accepted only for the beauty industry.

By accepting hypothesis 4, we confirmed that the presence of the sustainability committee positively influences sustainability reporting. However, correlation analysis showed that the presence of a sustainability committee is neither related to the overall ‘China info’ rating nor to any of the sub-dimensions of how a company may want to disclose information about China. So, hypothesis 4A (the presence of the sustainability committee positively affects the reporting of China-specific sustainability initiatives) was rejected.

Table 3 presents the correlation between the four variables measuring China-specific sustainability initiatives and the three additional factors that were considered in hypotheses 5, 6, and 7.

Luxury companies that report about sustainability and also have at least one East Asian on the board of directors accounted for 42% (19 out of 45) of the sample. According to the correlation analysis, the presence of East Asian directorship was significantly correlated only to the economic standard category. Thus, hypothesis 5, the presence of directors from East Asia on the board positively affects the reporting of China-specific sustainability initiatives, was only partially accepted.

Evidence from the dataset demonstrated that among the 45 luxury firms that published a sustainability report, 62.2% (28 out of 45) declared that supply chain and operations are managed in China (SCO). Correlation analysis showed that these companies invest more in China-specific sustainability initiatives, especially with regards to the environmental and social standards categories. Thereby, hypothesis 6, supply chain and operations management in China by a company positively affects the reporting of China-specific sustainability initiatives, was accepted. The results are logical because if the company is receptive to a market that is calling for sustainability, as is the case for China, and if the company further desires a tangible connection to the country, the company will have to build relationships with local actors such as suppliers, employees, or similar, rather than just with customers.

A total of 51.1% (23 out of 45) of luxury companies that reported their sustainability provided evidence of a tight relation with the Chinese market in terms of the business dimension (MKT). The correlation analysis supported hypothesis 7, if a company reports about China as a key market in terms of revenue, the reporting of China-specific sustainability initiatives is positively affected. If luxury companies declare to be present in the Chinese market, they are more likely to report about the economic dimension of sustainability with respect to China, which may include economic performance and procurement, anti-corruption, or anti-competition practices more than market presence. The results seem to be consistent with market presence being included within the GRI economic standards. For this reason, most of the companies that claim to have a significant presence in the market in China include this information in their own sustainability report.

4.4. National Approaches and Isomorphism

To summarize the results of the analysis, a two-step clustering analysis was conducted considering the ‘China info’ variable and the factors that were found to be strongly correlated with the reporting of China-specific sustainability initiatives (REV, GEO, SCO, and MKT). The model, with nine input variables, resulted in five clusters with a 0.6 (good) silhouette measure of cohesion and separation.

The cluster analysis returned a framework of five isomorphic approaches to the practice of reporting sustainability initiatives in China, which helps to understand how the Global Powers of Luxury Goods approach this theme in one of the most important markets:

Cluster 1: Rest of the world companies, with an average annual revenue of about USD $3 billion, that scored poorly in the ‘China info’ variable (between 0 and 3) and have little connection to the Chinese market;

Cluster 2: U.S. companies, with an average of USD $5.4 billion revenue, that under-perform or perform modestly in the ‘China info’ variable (from 0 to 4) and are mostly present in the Chinese market in terms of supply chain and operations;

Cluster 3: French companies, with the highest average revenue of around USD $14 billion, that modestly or highly perform in disclosing sustainability terms in China (from 4 to 7) and that are present in the Chinese market with their supply chains and operations;

Cluster 4: Italian companies, with an average revenue of about USD $2.4 billion, that have a low to modest propensity to disclose China-related sustainability initiatives (from 0 to 6) and mostly rely on the Chinese market for sourcing or operations;

Cluster 5: Chinese companies, specifically from Hong Kong SAR, as none of the four mainland China-based companies publish a sustainability report, with a revenue of about USD $2.3 billion on average, and register the highest ‘China info’ score among the whole sample (from 5 to 9) and are intuitively present in the local market both with respect to supply and demand.

The cluster composition helped us to find a nexus among the rationale behind the clustering and the relative variables. The analysis first confirmed how nationality is associated with a uniformity of approaches. What distinguished between an extremely high rating an extremely low rating was a positive (or negative) connection with the SCO and MKT variables, for which the cluster that included Chinese companies ranked high, whereas the cluster that included the rest of the world’s companies was ranked low. Finally, medium/high and medium/low ratings were distinguished by the variable REV. Medium/high scores were scored by French companies, which had the largest revenue, whereas Italian and U.S. companies scored medium/low, which had much lower revenue compared to French companies.

5. Discussion and Conclusions

In this study, we explored the sustainability reporting behaviors of the Global Powers of Luxury Goods, with a geographical focus on China. This is an interesting topic due to the importance of the Chinese market for luxury companies and the strengthening link between luxury business management and sustainability issues. We developed a theoretical framework to explain the adoption of common reporting by considering how some institutional factors act on sustainability report adoption and on the reporting of China-specific sustainability initiatives.

In terms of the content of sustainability initiatives, we revealed a general convergence between luxury companies’ China-specific sustainability disclosures and China’s performance in the areas of environmental and social sustainability. For managerial implications, we suggest that interested companies should commit to sustainability by monitoring the national playing field with the two-fold purpose of contributing to local sustainable development while generating value for the company.

Together with descriptive results, the empirical survey provides additional insights and support for the propositions developed. Current literature about the adoption of sustainability reporting practices by luxury companies is further validated. In line with the expectations developed under the stakeholder theory framework, we found that some factors, like company dimensions in term of revenue and the presence of a sustainability committee, are likely to be important determinants of sustainability reporting adoption. Other factors, like the company’s nationality and the sector of activity, seem to be irrelevant in this regard, leading to the conclusion that any homogeneous institutional pressures within specific countries or sectors are not sufficient to push luxury firms to adopt homogeneous behavior with respect to sustainability reporting.

Secondly, we found that even if the number of luxury companies producing sustainability reports is still low, the attitude toward reporting China-specific contents is positive (36 of 45 cases). The relevance of the different dimensions of sustainability (economic, environmental, and social) seems to respond to a logic of isomorphism, in particular between companies belonging to the same nation. This result is coherent with institutional theory by assuming that companies that belong to the same country share a common set of cultural pressures and values, thereby developing similar sustainability reporting practices. This result is particularly evident in the case of French and Chinese companies that belonged to national contexts characterized by a specific managerial culture [

64,

65] and by different and specific national and international (in this case bilateral) dealings. French companies are listed among the global powers of luxury goods as the biggest in terms of revenue, contributing evidence to the literature of a correlation between company revenue and country-specific sustainability initiatives.

Thirdly, the findings show that other factors help to explain the development of China-specific sustainability initiatives, like supply chain and operations management in China and the direct reference to China as a key market in terms of revenue. The relevance of both variables can be interpreted through stakeholder theory since the theory describes a scenario in which some categories of stakeholders, such as employees, suppliers, and business customers, are strongly characterized from the point of view of nationality [

65]. The Chinese market is identified by the company as one relevant stakeholder. These conditions lead the company to devote particular attention to China both in developing country-specific sustainability strategies and in reporting.

The results presented contribute to the discussion on the relationship between sustainability and the luxury sector. In this regard, the French powers of luxury goods already interpret sustainability as a competitive factor, particularly in the Chinese market. Some research showed that luxury consumption has been moving east for a long time [

66] and Chinese luxury goods buyers are more likely to be consumers who have a higher family income, have a higher education level, and live in more advanced and developed cities [

67]. In the future, a certain sensitivity toward sustainability issues will likely be included among the characteristics of the consumer of luxury goods, especially in a context like China, which is strongly investing in this direction.

A further aspect that emerged was the relevance that China assumes in the supply chain of the Global Power of Luxury Goods that are investing in sustainability. This is a bond that will likely translate into a competitive success factor since, in luxury, criticisms tend to refer to hidden parts of the supply chain, such as raw material sourcing, animal treatment, human work conditions, manufacturing methods polluting the local environment, or destruction of the environment [

7]. We identified how some large luxury firms already seem to be trying to respond univocally to the three-fold challenge of an integrated and sustainable global supply chain by implementing China-specific initiatives.

Although these findings provide an initial empirical investigation into sustainability reporting in the luxury sector, further exploration is needed. One of the limitations of the case study presented is the focus on 2018 sustainability reports. More longitudinal observation and analysis of China-specific sustainability initiatives reporting practices may be conducted in the future to confirm and further investigate the results that emerged from this analysis. Further qualitative research may also provide insights into why the number of the top 100 luxury companies that still do not report their sustainability was so high.

{kind=link}

{kind=link}

{kind=link}