1. Introduction

The massive and profound impact of the current pandemic has posed unique economic, social, and health challenges due to its cumulative effects in terms of propagation, global reach, and unprecedented steps taken by governments to contain its spread (shutdown of borders, travel restrictions, national lockdowns, closure of restaurants and hotels). As a result of the COVID-19 outbreak, most tourist destinations were forced to halt operations during 2020 due to lockdown measures and travel bans, canceled bookings, and local logistics. In conjunction, such evolution has placed tourism among the most severely impacted sectors in terms of revenue, jobs, and few available alternatives for maintaining operations during a lockdown. Coupling the sector’s negative multiplier effect on other supporting industries, with its economic relevance and the registered global jobs losses, requires strong support to mitigate the effects of COVID-19 in tourism-related industries and to uphold recovery [

1].

Before the pandemic, at a global level, the industry accounted for 10.6% of total employment (334 million jobs), 10.4% of global GDP (USD 9.2 trillion), and international tourist spending totaled USD 1.7 trillion (27.4% of global services exports) [

2]. The broad implementation of travel restrictions in response to the pandemic resulted in a 98% decrease in international tourist arrivals in May 2020 compared to the same month of 2019 [

3]. Domestic visitor spending fell by 45%, while international visitor spending fell by a record 69.4% [

2]. A report released by the World Travel and Tourism Council (WTTC) in collaboration with Oxford Economics estimates that in 2020, the sector lost between USD 4.5 and 4.7 trillion, its contribution to global GDP fell by 49.1% from 10.6% to 5.5%, and 62 million jobs were lost (−18.5%) [

2]. Currently, job losses continue to be a concern, as 100-120 million direct tourism jobs are at risk. In some cases, jobs are currently funded by government retention programs and may be lost if the industry does not fully recover (e.g., the European Commission provided EUR 100 billion to mitigate unemployment risks through the “Support to mitigate Unemployment Risks in an Emergency (SURE)” instrument [

4], which provides loans to the Member States aimed to support short-time work schemes).

Additionally, the UNWTO Barometer indicates a loss of 300 million visitors and USD 320 billion in foreign tourism revenues, more than three times the loss experienced during the 2009 Financial Crisis. Overall, destinations worldwide have received 1 billion fewer international arrivals in 2020 than in the previous year [

3]. For instance, as shown in

Table 1, for all G20 countries T&T % of GDP has decreased significantly, with Spain, the United Kingdom, China, Turkey, Canada, and Italy registering a decrease larger than 50% [

2]. There is a clear general shift towards domestic spending in T&T products, while the impact in terms of change in spending has been considerably lower for domestic demand.

Similarly, according to an ETC report for Q4 2020, all European destinations experienced declines in overall tourist arrivals of between 51% and 85% in 2020. A closer national level examination reveals even more dramatic figures, with Cyprus experiencing an 84% decline in tourist arrivals, Romania 83%, and Spain a loss of 77%. Nonetheless, the return to more normal patterns of international travel demand will be incremental, with 2019 levels expected to be restored by 2023 [

5].

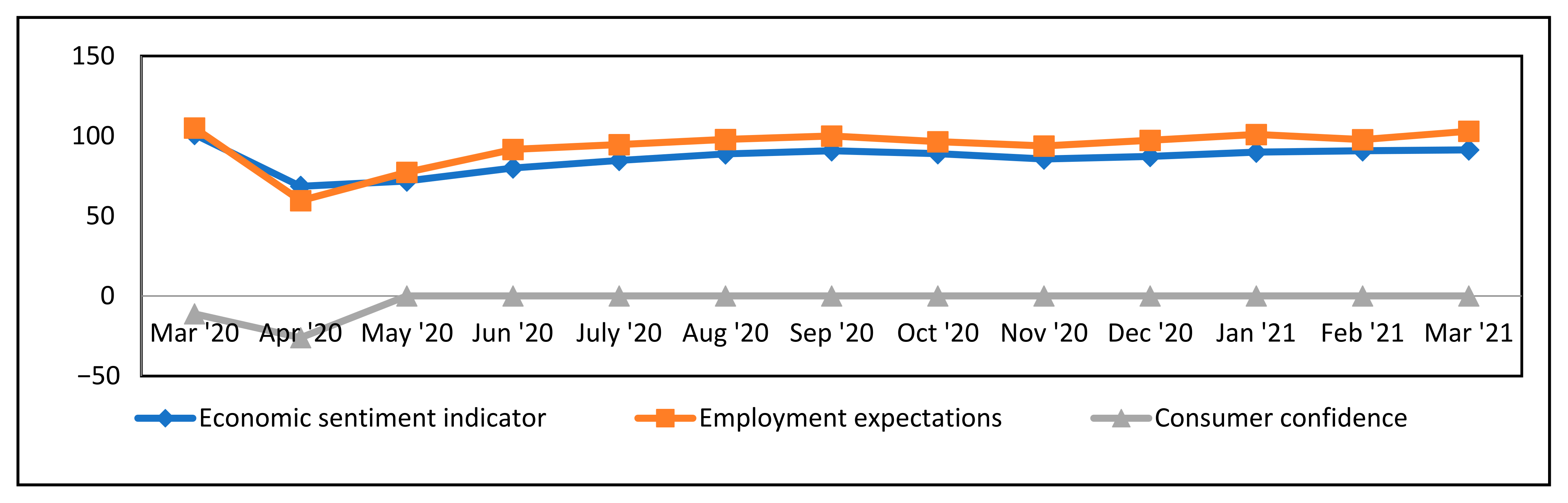

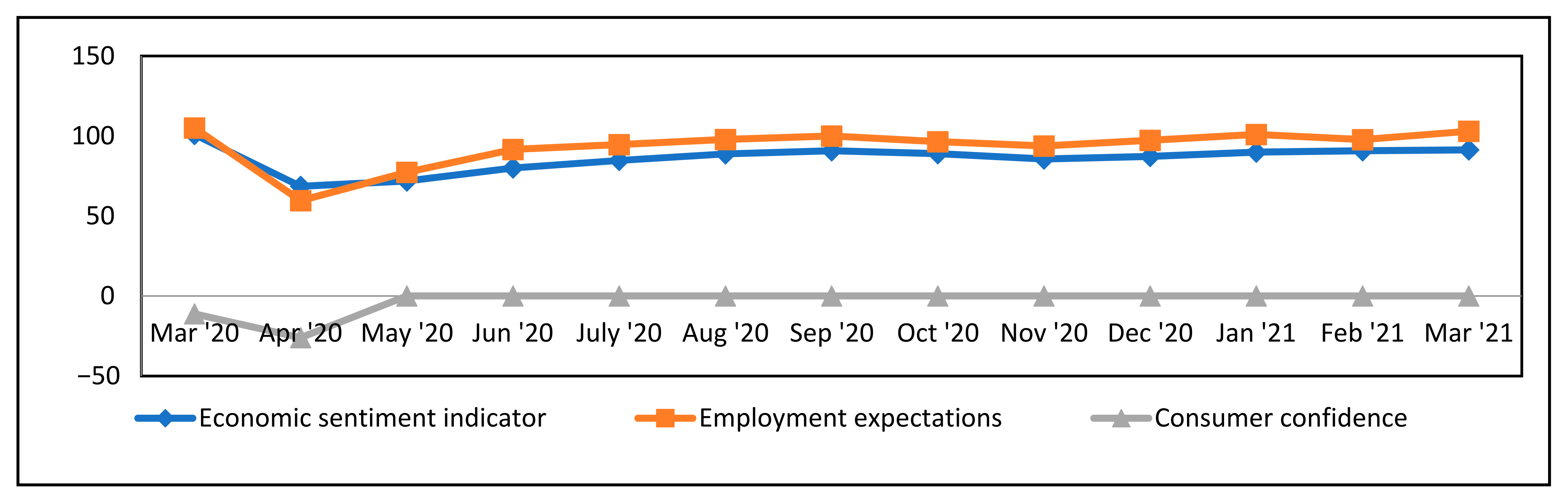

As for the specific case of Romania, as shown in

Figure 1 [

6], confidence indicators have been severely affected, with a first drop registered in March 2020 and the lowest levels for economic sentiment indicator, employment expectations, and consumer confidence recorded in April 2020. Tourism and hospitality were the most affected industries registering a negative change of 67.4% in the GDP in the second quarter of 2020 compared to the first quarter. The sector’s contribution to GDP dropped to 3.69%, compared to 5.3% in 2019 [

6].

The outlook for 2021 remains cautious, as the latest data of the World Tourism Organization (UNWTO) indicate an 87% decline in international tourist arrivals in January compared to 2020. With 32% of all global destinations fully closed to foreign tourists as of February 1, the UNWTO anticipates a tough start to global tourism in 2021 [

3]. According to current trends, the UNWTO foresees that foreign tourist arrivals will decline by approximately 85% in the first quarter of 2021 compared to the same timeframe in 2019 [

3].

Undoubtedly, the T&T industry is venturing into uncharted territory. The sector is renowned for its resilience in the face of several global crises over the years but has never faced a crisis such as this one [

2,

3,

5]. The industry has recovered rapidly from previous epidemics and downturns—Dufry (DUFN) and Amadeus (AMS) analysts indicated a recovery in six to seven months following previous disease outbreaks [

7]. However, after the dramatic evolution of the sector, one of the largest questions continues to be if and how the industry will rebound this time? Estimations about foreign tourist numbers returning to the pre-COVID-19 status indicate various scenarios varying from six months [

4] to at least two to five years [

5]. UNWTO has proposed two scenarios for 2021 and considers a potential turnaround in international travel in the second part of the year (July or September) [

3]. The United Nations Agency for tourism extended scenarios for 2021–2024 indicates a turnaround in the second half of 2021, similar to UNWTO’s forecasts of a revival in foreign tourism in the third quarter of 2021 [

3]. However, approximately 20% of UNWTO’s Panel of Experts believe the turnaround will occur only in 2022.

Along with virus contamination and low consumer trust, travel restrictions are seen as the primary impediment to international tourism recovery [

3]. Notwithstanding, there seem to be some suitable premises to consider when looking at the future. According to a BCG study in May 2020, when asked which things they miss the most during the pandemic, irrespective of nation, age groups, and income levels, consumers consistently place leisure travel first, with more than 60% agreeing that they “can’t wait to travel again” [

8].

Even though businesses display a long-term concern on preparing and adapting for the future, most companies are still currently understandably focused on staying afloat in the short term by controlling costs and, where possible, developing new, innovative ways to meet and retain customers. Recent surveys and trend analysis [

1,

8,

9,

10,

11,

12,

13] have shown that the COVID-19 health crisis affects consumer patterns. Changes are observed in the short-term, and they are expected to persist in the medium- and long-term term. Would consumers’ pre-pandemic travel patterns revert to their pre-pandemic levels, or will a new normal in consumer travel emerge? What changes can companies and marketers make to their marketing strategies in order to re-engage travelers?

The current empirical research focuses on the Romanian market and was conducted to understand customer sentiments and conditions that need to be met for purchasing T&T services and how they can be reinforced post-COVID crisis to ensure business models’ sustainability. The article’s central aim is to provide specific guidance for hospitality businesses and decisionmakers to consider the industry recovery and ensure business models’ sustainability. For this purpose, the paper addresses a threefold objective: (1) to examine how perceptions on T&T expenditure have shifted during the May-December 2020 lapse and the prospects for the upcoming months; (2) to understand consumers’ expectations when reconsidering purchasing such services and relevant criteria to move from intention into action, and (3) to measure respondents’ awareness and support of governmental help for the T&T industry.

The paper is structured as follows:

Section 1 highlights the relevance and context of the research and reviews the current state of the research field,

Section 2 covers the methodological approach and the empirical results, and

Section 3 is dedicated to discussions on translating the gathered insights into targeted business and policy support recommendations.

3. Materials and Methods

3.1. Methodology

As described in the previous section, the global COVID-19 outbreak has caused widespread concern, posed unprecedented challenges, and brought a large spectrum of effects developing at an alarming pace in all spheres of economic, social, and day-to-day activities. Although COVID-19-related uncertainty persists globally, its impact varies across countries, and both consumers’ responses to the crisis and business strategies of adapting to the new standard vary significantly. Moreover, although previous research indicates that consumers’ behavior changes significantly during periods of crisis, along with their utility trend [

48], it is quite challenging to forecast customer behavior in the T&T industry after a crisis [

49]. Consequently, understanding the path back to pre-COVID-19 levels of operation, recovery support, and decision-making entails various in-depth qualitative and quantitative metrics. Further research is particularly needed to advise industries among the most affected ones, such as T&T.

The current empirical research was conducted to address a threefold objective (focused on the Romania’s T&T case): (1) to examine how perceptions on T&T expenditure have shifted during the May–December 2020 lapse and the prospects for the upcoming months; (2) to understand consumers’ expectations when reconsidering to purchase such services and the relevant criteria to move from intention into action, and (3) to measure respondents’ awareness and support of governmental help for the T&T industry. The results of this research are the foundation on which we provide specific guidance for hospitality businesses and decisionmakers on the actions to consider towards the industry recovery while keeping an eye on the business models’ sustainability. Exploring such elements might prove essential for understanding the best strategies to recover from the significant losses the T&T industry has experienced. Understanding the underlying factors that determine consumers’ trust and willingness to purchase T&T products and services can uncover novel ways to tackle consumers’ increased feelings of uncertainty and lack of trust. In the context of this paper, “T&T products” refer to any type of travel and tourism service bought for the purpose of relaxation, be it transportation, accommodation, or more comprehensive packages (such as all-inclusive service packages).

The paper presents insights from a quantitative survey-based research on the Romania market using two consumer samples in different moments of the pandemic evolution. The first phase of data collection was undertaken during the national lockdown. Before the beginning of summer (May 2020), it was typically known as a strong season for leisure and traveling. The second period (December 2020) was characterized by strict distancing rules and restrictions and covered the time before Winter Holidays, also recognized for increased demand for both inbound and outbound travel. The May sample comprised 1015 participants, whereas the December sample included 1020 participants; in both cases, surveys were created using online panels, ensuring representativeness for the entire adult population (participants were at least 18 years old under the ESOMAR code of ethics). The two samples may or may not include the same respondents; however, they were configured using a similar approach to provide a consistent and meaningful comparison of the data. The size of both test samples guarantees a 3% margin of error and a 95% confidence level.

The employed research method was a structured questionnaire comprising questions capturing respondents’ views on future travel and spending on tourism and recreation, their expectations on reconsideration of such purchases, and their level of knowledge and support for governmental help T&T industry. The questionnaire was divided into three sections:

Section 1 aimed to identify respondents’ perception of their current financial situations and the prospect for the next three months and used a 5-point Likert rating scale where: (1) much better; (2) a little better; (3) the same; (4) a little more difficult; (5) much more difficult. Respondents were asked to rate the level of importance on the basis of their judgment, and they also had the option “I don’t know”.

Section 2 evaluated respondents’ sentiment about future travel and spending on tourism and recreation, their expectations on reconsideration of such purchases, and their level of knowledge and support for governmental help for the T&T industry.

Section 3 was dedicated to identifying the demographic variables, which made it possible to identify the socioeconomic characteristics of the studied population characteristics such as gender, income, age, education, and residence (rural or urban). Data collection was completed through online surveys. The gathered data examined how views and perceptions vary according to different contexts and personal circumstances.

The primary data collected was analyzed using IBM SPSS Statistics program (version 27) for both a univariate analysis, undertaken by performing tests on several key points (such as the intentions when it comes to T&T purchases, the intended budget for T&T in the next 6 months), and bivariate analysis to assess the influence of various elements on customer perceptions through Spearman’s correlation tests (all of the correlation coefficients reported in the analysis were relevant at the 0.01 level, two-tailed, and they were all performed on the entire research sample which included both May and December samples).

3.2. Results

The results presented in this section focus on the impact of COVID-19 on the Romanian T&T industry from the consumers’ perspective, evaluating respondents’ perceptions and intentions concerning their T&T product purchasing behavior. To begin with, we evaluated respondents’ intentions related to granting part of their budget to purchasing T&T products. As it can be seen in

Table 4, there was slight optimism in December, as opposed to May 2020, since 11.5% of the December respondents (as compared to only 8.5% of the May respondents) mentioned that they would dedicate a bigger or significantly bigger budget for T&T product purchases. This result shows that as people get more comfortable with uncertainty (therefore diminishing their level of perceived uncertainty), they are more likely to resume their previous activities, including traveling. Still, we cannot ignore that 37.1% of the May respondents and 35.3% of the December respondents declared their intention of not buying any T&T product. It might be a result that even in December 2020, we are at the beginning of the recovery stage in the T&T industry. We still have a long way to go before fully recovering our traveling appetite.

When correlating these results with some socio-demographic variables of the respondents (the overall sample), we discovered a slight indirect correlation with the respondents’ monthly income (−0.148 correlation coefficient), meaning the higher the income, the more likely they are to dedicate a bigger budget for purchasing T&T products in the next 6 months, as compared to 6 months ago. Moreover, a 0.142 correlation coefficient showed that when people are employed or have their own business, they are more likely to invest a bigger budget in buying T&T products than when they are unemployed, retired, or students. These results show an intuitive correlation that is likely to occur in regular times, not only in a time of crisis such as the COVID-19 pandemic.

Nevertheless, when referring to respondents’ behavior and estimations in times of a crisis, we discovered that a 0.211 correlation coefficient proved a direct and mild correlation between respondents’ intentions related to the T&T budget and their evaluation of their families’ financial situation now as opposed to 3 months ago (a coefficient computed for the whole respondent sample of 2035 individuals)—the better-looking the estimation of their financial situation, the more likely they are to dedicate a larger budget for T&T products. Furthermore, this goes even further: the more optimistic respondents are about their family’s financial situation in the next 3 months, the more likely they are to dedicate a bigger budget for T&T products (a 0.235 correlation coefficient demonstrated this). Moreover, when respondents estimated that they would rely solely on their incomes and their savings for surviving the next 3 months (as opposed to respondents estimating that they will need to borrow from friends or banks for managing the predicted expenditures), they were more likely to estimate that they will dedicate a bigger budget for T&T product purchases (a 0.251 correlation coefficient proved this). These results prove that financial optimism and optimistic estimation directly impact how people buy products dedicated to their relaxation needs. The investments people make in T&T products are secondary to those investments considered more critical to the consumers, thus creating the context in which people can feel secure about their financial future is essential in stimulating the T&T industry recovery.

The degree to which respondents do not feel that T&T should be considered a priority for governmental support for ensuring recovery is proof that respondents do not see tourism as essential for their wellbeing. A total of 66.2% of the May respondents believed that the hotels and restaurants industry should not be included in the list of priority industries that should receive government support to overcome the current crisis, while 56.1% of the December respondents believed the same. When seeing that agriculture and healthcare were the top two industries that respondents felt like they needed most of the governmental support for recovery, it is easy to discover respondents’ interest in basic survival needs before any other leisure-related needs.

Nonetheless, consumers are still willing to travel (even though they are a smaller proportion of the entire adult population).

Table 5 illustrates respondents’ intentions related to travelling once the restrictions are lifted. Firstly, as it can be seen in the December sample (even though the two samples’ sizes were approximately the same), we discovered roughly 200 extra respondents that were more willing to make a choice, proving their intention to travel (regardless of their choice in terms of destination).

Secondly, we see a clear preference for traveling nationally, proving how the COVID-19 crisis leads to exposing the population to national options when traveling. This strategy might have multiplied positive effects in terms of sustainability—reduced international transportation pressure and increased connection with the national heritage that can enhance people’s sense of belonging to a culture and a nation. Thirdly, we discovered a new sense of trust and openness in the choices mentioned by the December respondents—there has been a switch between the preferred means of transportation should they choose to travel internationally: respondents seemed to feel more confident in traveling by plane than by car in December, as opposed to those surveyed in May. It might prove that airline transportation is now slowly entering a recovery stage (which might take a while before reaching a complete recovered stage, but things seem to be moving towards a new type of ordinary). Moreover, this is more visible, especially in the respondents with higher incomes: a 0.140 correlation coefficient proves that the more they earn, the more likely they are to express their intent to travel internationally by plane.

Besides evaluating respondents’ intentions of traveling, it is essential to discover what elements will influence their choice when purchasing T&T products. In this sense,

Table 6 shows the criteria considered to be of great importance when purchasing travel and T&T products.

On the basis of the results in this table, we can see that even though people might be more relaxed and optimistic when it comes to traveling in December 2020 as opposed to May 2020, their concerns related to safety are still significant to them. As a result, the most important criterion when choosing a travel destination for respondents in both samples was “not being too crowded” (the mode was the most relevant statistical indicator as this variable was measured on an ordinal scale), followed closely by the “destination’s safety” in terms of sanitary policies. Moreover, taking more cautious general purchasing decisions was correlated with ranking higher “destination’s safety” among the criteria used for choosing a travel destination (a 0.147 correlation coefficient proved this). On the other hand, taking more cautious general purchasing decisions was correlated with ranking lower “the attractiveness level of the destination” among the criteria used for choosing a travel destination (a −0.136 correlation coefficient proved this). Therefore, the shape and form of the destination faded away when faced with the safety that the destination offers to the more cautious traveler.

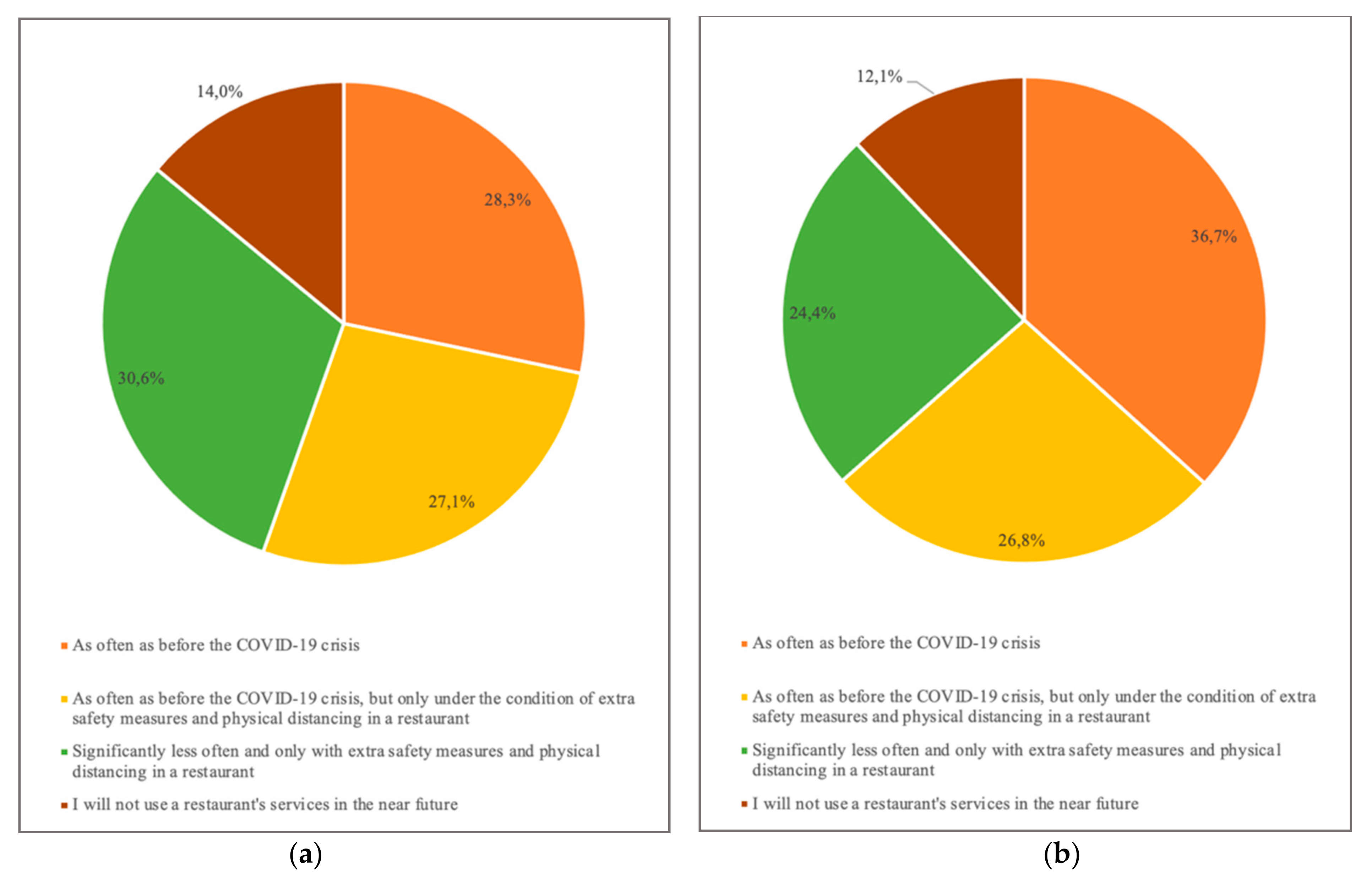

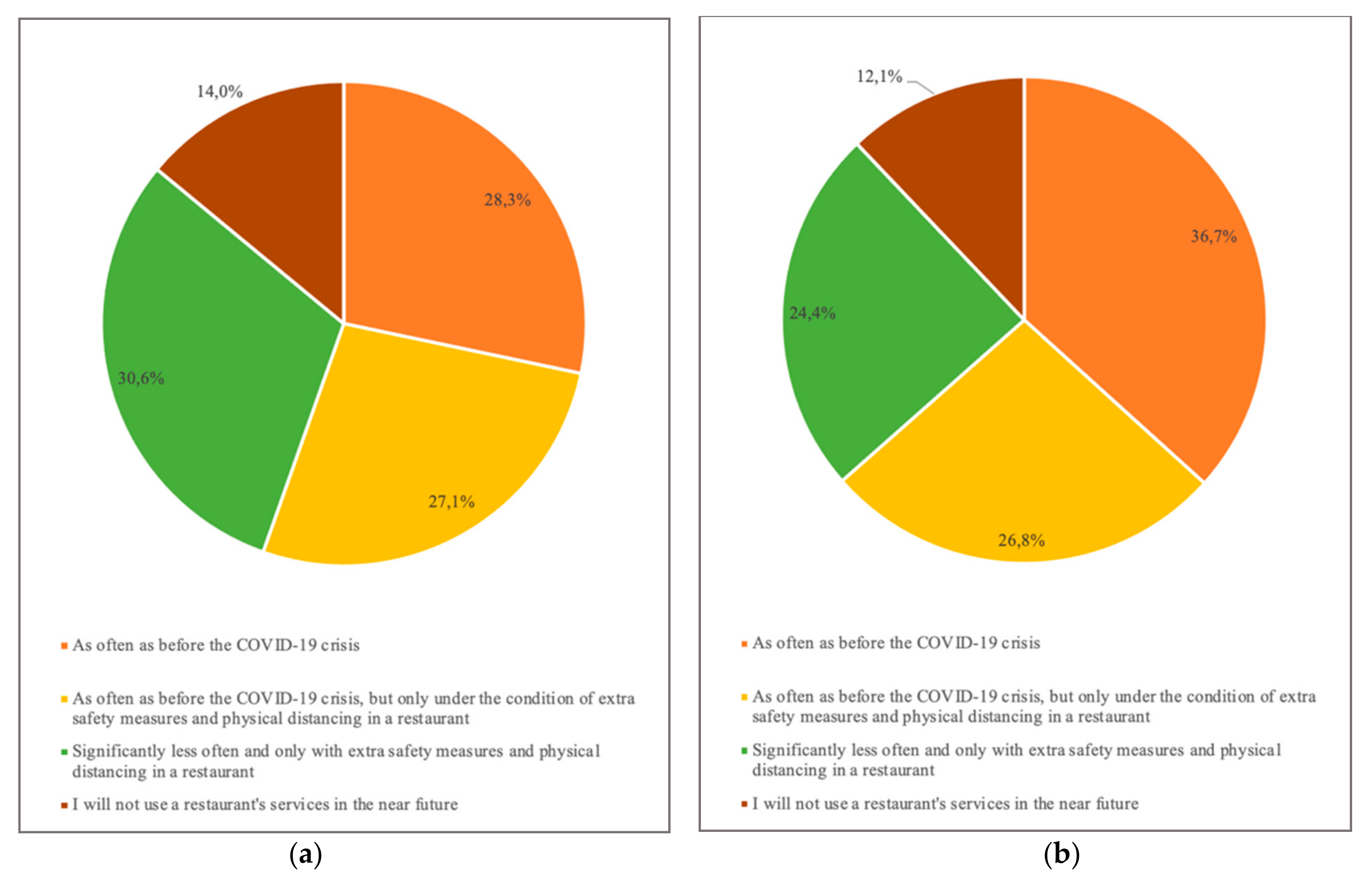

These respondents’ safety concerns were also visible when evaluating their willingness to use restaurants’ services soon. As shown in

Figure 2, 30.6% of the May respondents and 24.4% of the December respondents stated that they would use restaurants’ services significantly less and only with extra safety measures and physical distancing in the restaurant.

Moreover, there were another 14% of the May respondents and 12.1% of the December respondents that proved no intention of using a restaurant’s services soon. These results show yet another lack of interest in accessing services that are not essential for survival. Even though restaurants’ services can be used either when traveling or when searching for a socializing context, people’s concern on safety when using such services might have an influence also when deciding whether to travel or not. Therefore, when developing a recovery plan for tourism, making travelers feel safe about using a restaurant’s services is essential in comforting them and their concerns about traveling.

4. Discussion

The research results gathered and presented in the previous section are consistent with previous research projects on a similar topic. These confirmations or partial confirmations are presented in the following sub-sections.

4.1. Willingness to Travel and the Dedicated Budget

When referring to people’s willingness to travel and their intention of dedicating a more significant proportion of their budget to purchasing T&T products, our research showed a slightly more optimistic view in December 2020 as opposed to May 2020, while there were still more than a third of the respondents in both samples that had no interest in buying such products in the next 6 months. These results are similar to the global evolution over the same period: STR research conducted throughout March 2020 over a total of 917 respondents from more than 60 countries indicated that 33% of those surveyed stated that they were more likely to spend less on travel and leisure in the next 12 months. Only around 20% of consumers were still planning to travel more in the year ahead [

50].

Moreover, our results indicate that financial optimism and positive estimation have a direct impact on how people buy products related to leisure activities. The investments people make in T&T products are secondary to those investments considered more critical to the consumers, and thus creating the context in which people can feel secure about their financial future is essential in stimulating the T&T industry recovery. A similar conclusion was reached by a Roy Morgan Holiday Travel Intention report released in April 2020, which showed that “people’s intention to travel over the next 12 months is tightly linked to the confidence they are feeling in the overall economy” [

51]. Unsurprisingly, intention to travel plummeted due to the pandemic and the accompanying recession and the everyday challenges people estimate in their current and future financial situations. This outcome is also consistent with a report issued by Euromonitor stating that expenditure on hotels and catering is estimated to drop sharply in the 2019–2023 time frame instead of the 2015–2019 period of time [

52]. Furthermore, these changes in expenditure decisions apply across a wide range of industries and are not limited only to the T&T industry: between 50% and 60% of industries expect final consumer expenditures’ drop at least in the mid-term [

53].

4.2. Choosing a Destination

Current research data indicate a clear preference for traveling nationally (84.3% in May and 74.7% in December), supporting strategies focused on exposing the population to national options when traveling. Given the pandemic repercussions on purchasing power, tourists may want to reduce travel spending by re-orientating towards more affordable destinations or towards lower transportation costs (forecasts by the International Air Transport Association (IATA) estimate that ticket prices could go up by 43–54%) [

54]. This strategy might prove to have multiplied positive effects in terms of sustainability—an excellent opportunity to revitalize domestic tourism, focus on nearby tourism, reduce international transportation pressure, and increase connection with the national heritage. People turning to national T&T products (defined as any intra-country travel service purchased for relaxation), together with the psychological effect of striving to survive in uncertain times, has led to governments and destinations that “acted individually and nationalistic”, even though systems theory proves that a collective solution package is preferred for more rapid and better results [

55].

The trade recovery barometer released by WTTC (2021) indicates that in 2020 for all G20 countries (except Turkey), domestic tourism represented more than 60% in total T&T services reaching levels beyond 90% in Japan, Brazil, the USA, Argentina, and Australia. Moreover, for all G20 countries, inbound tourism has experienced significantly lower changes in demand (ranging from −63.2% to −30%) compared to outbound ones (−71.6% to −82.9%) [

2]. McKinsey also concludes that domestic tourism will reach pre-crisis levels approximately one to two years before outbound travel due to numerous factors such as fewer constraints for domestic travel, more alternatives to air travel, and a greater demand coming from business travel [

56].

At the EU level, a series of initiatives targeting incentives to boost domestic tourism have already been designed and implemented through special offers of hotel discounts to permanent residents, provision of affordable prices for tourist accommodation, and subsidizing 25% of the cost of accommodation (Cyprus); lower VAT rate (from 15% to 10%) on accommodation, culture, sport (Czech Republic); online campaigns (e.g., #CetÉtéJeVisiteLaFrance; #JeRedécouvrelaFrance in France, #DescubreLoIncreible in Spain, also in Latvia and Lithuania); corporate or business holiday travel vouchers; subsidies for citizens through the social tourism program “Tourism for All”, addressed to low-income groups (EUR 16,000 annual individual income, EUR 28,000 for family income) (Greece); Széchenyi Tourist Card—free-use loan with zero interest rates (allocated HUF 100 billion (EUR 278 million) in Hungary); system of holiday vouchers for medical people in Lithuania (EUR 200) or for families with children in Poland (EUR 111); and Tourist Pass Holiday initiative (holiday vouchers for public employees similar to the meal tickets) in Romania [

57].

Other studies on the Romanian market [

58,

59] also indicate that the pandemic will shift tourists’ preferences towards more secure or familiar destinations, most likely national destinations, and an increased appetite for individual tourism, ecotourism, or green/sustainable tourism.

4.3. Criteria to Travel

Besides simply evaluating respondents’ intentions of traveling, it is essential to discover what elements will influence their choice when purchasing T&T products, and the criteria are considered greatly important. Results indicate that even though people might be more relaxed and optimistic when traveling in December 2020, as opposed to May 2020, their concerns related to safety are still significant to them. People focus on less crowded destinations and resorts, together with the destination’s safety, while not granting too much attention to the destination’s attractiveness, thus signaling a shift towards a more sustainable consumer behavior also when it comes to T&T products purchases. On the basis of research on the Romania market, Volkmann et al. (2021) also conclude that among the primary criteria for selecting a vacation destination will be hygiene, uncrowded areas, quality, and ecotourism [

58]. The conclusion is accordant with the drivers likely to impact the recovery identified by McKinsey: the attractiveness of domestic destinations, the materiality of air transport, health and hygiene factors, business travel, and sustainability [

56]. Similarly, Sigala [

19] mentions that as opposed to the pre-COVID-19 era, these new concerns of travelers require “servicescapes to be redesigned eliminating or inhibiting sensorial elements” that used to be essential in building the entire T&T experience. This research shows the importance of the smell of cleanliness instead of fragrance, as well as there being a new benchmark for the psychological comfort related to the perceived crowdedness [

19]. Such connections between variables are explained by Kock et al. [

55], who proved in their research that people correlate COVID-19 contagion with “crowding perceptions”, “xenophobia”, and “ethnocentrism”.

The premium that the COVID-19 pandemic has put on hygiene and the quality of public healthcare is likewise reflected in respondents’ safety concerns are also visible when evaluating the intentions of their willingness to use restaurants’ services in the future: almost a third of both samples argued that they would use restaurants’ services significantly less and only with extra safety measures and physical distancing in the restaurant, while more than 1 in 10 respondents stated that they have no intention of using such services. Previous studies point out results alike when it comes to perceived risks and restaurant services [

60,

61].

According to the findings of this study, one of the main consequences of this health crisis is grooming and health awareness. It means that when planning their next vacation, travelers will prioritize the cleanliness of airports, public spaces, hotels, restaurants, tourist attractions, and everyday needs, as well as the accessibility and standard of treatment provided by the destination. Thus, quality requirements and the health system’s success in the host country become considerations in the travel decision.

Governments are already developing steps to strengthen their tourism economies in the aftermath of COVID-19 through strategies meant to help tourism’s sustainable recovery, encouraging the digital transformation and the transition to a more green tourism framework, and reimagining tourism for the future. Analyzing recovery measures adopted by European governments indicates that authorities are relatively aware of too imperative a need to strengthen tourists’ sense of security, satisfy the increased need for information, and stimulate confidence. Adopted solutions comprise new service and information concepts (Austria); guidelines for the accommodation places (Belgium, Poland); a four-tier system (green, orange, red, and gray countries) determining different risks and entry requirements (Cyprus); digital coronavirus passports (Denmark); national digital and social network campaigns (France, Ireland, Spain); interactive maps to locate all tour operators who are open and dedicated to health protocols (France); apps for smart devices supporting digital transition and providing tailor-made information and innovative services (Greece); COVID-19 helpline specifically for tourists (Malta); “Clean/Green and Safe” seal for tourist activities that comply with hygiene and cleanliness requirements for the prevention of COVID-19 (Portugal, Slovenia, Spain); travel insurance for foreign tourists (Portugal); campaigns to promote more responsible and sustainable tourism (Portugal); “Traffic light for Tourism” in Slovakia (depending on the virus’s distribution, this scheme establishes conditions for the operations of accommodations and wellness resorts, restaurants, large gatherings, and swimming pools, segmented according to tourist and employee target categories, as well as hygienic–epidemiological steps and services) [

32].

4.4. Support for Hotels and Restaurants

The data collected in the present study shows that more than half of the respondents in both samples believe that the T&T industry should not prioritize governmental support while believing that the other two industries are essential to support: agriculture and healthcare. For example, in Australia, the recovery measures mainly target broadband and healthcare improvements in rural areas, primary manufacturing and agriculture [

62].

Moreover, on the basis of the findings related to T&T Competitiveness Index (presented in

Table 2), because of its emerging-market status, Romania offers higher rates of return for T&T investors willing to cope with less favorable environments, especially as it became more internationally opened and investments in infrastructure and destination assets improved in the last years [

63]. Even though it has rich natural and cultural resources, it is held back by underdeveloped infrastructure, security concerns, or policy or structural issues; the support for hotels and restaurants is mainly subject to public involvement and not a private one.

4.5. Recommendations

A few recommendations can be drafted for both the industry representatives and the government representatives that can contribute to turbo-charging recovery in a post-COVID-19 era. Before diving into those recommendations, we argue that now more than ever the recovery of the T&T industry can happen far easier and faster when various types of forces decide to work together (businesses, governmental representatives, stakeholders). Therefore, these recommendations rely on various actors working together for the ultimate purpose of helping this industry reinvent itself so that we could all enjoy its long-term benefits on our wellbeing, human growth, cultural awareness, and feeling connected.

When it comes to the business in the T&T industries, they have the most prominent role in making recovery possible and the first steps that they need to undertake is to strive to understand the T&T customer and their concerns, as well as to become aware of their salient mission in reinventing themselves in the face of the crisis. Then, T&T companies need to build new or modified products that answer the current concerns of customers to help them move from a fearful state to a relaxed one. Achieving this is done through creativity, innovation, and a strong sense of empathy over what the customers are struggling with. When it comes to tactical measures: paying extra attention to the safety of resorts, accommodation units, or airports; leveraging people’s interest in local and national tourism; and building cheaper products for low-income or even average-income consumers are just some of the paths towards recovery. Last but not least, T&T companies need to reinvent their communication systems so that they become a source of calm and comfort for concerned customers. It can be achieved by offering a unique value proposition on the T&T market and frequent updates for loyalty members. Keeping in touch with customers or potential customers and developing long-lasting relationships with them is now more critical than ever.

The research results indicate that customer emotions are more important than ever in T&T marketing. Regardless of the outside effects, customer perceptions prove to be the most important predictor of their intentions, decisions, and actions. For example, a smaller level of perceived danger is linked to a more optimistic approach to customers’ future decisions and intentions related to traveling. On the basis of the obtained insights, travel destinations (such as cities, resorts, accommodation units) need to develop: (1) a strategy to avoid crowds; (2) a sanitary strategy that is likely to offer some sense of safety to travelers, and (3) a communication strategy that will inform consumers or potential consumers on the previous two strategies and their effectiveness in tackling with travelers’ safety concerns. Moreover, we can argue that making travelers feel safe about using a restaurant’s services might become essential in comforting them and their concerns related to traveling. Additionally, since confidence in a brand’s health and safety policies will continue to be critical in the future, stepping back in health and hygiene shall not be an option for T&T brands. On the contrary, to restore travelers’ confidence and stimulate demand, priority should be given to health and safety for guests and staff, adopting globally recognized health standards, introducing social distancing restrictions, and shifting to lower occupancy levels. All the measures shall be clearly outlined on websites and constantly disseminated through information apps for visitors.

Since it will be critical to redefine domestic leisure as a priority and ensure that local communities understand the importance of tourism and are open to contributing to the revival of the sector, T&T companies need support from the government and local authorities as regional or global regulators. In this sense, easing people’s concerns about their health and safety is the number one mission of policymakers. These policymakers have a significant role also in regulating the T&T market and the sanitary and safety rules it should comply with. When it comes to the financial support directed towards the T&T industry, it can come in at least two forms: direct financial support to T&T industries or indirect financial support through support granted to travelers to help them get a more positive perspective on their financial situation (now and in the future) as the foundation of their interest (or lack of it) in traveling. In this respect, working together, on a regional or global level, as utopian as it may seem, might lead to better results for everybody in the long run (were we to consider the system theory). It is even more critical when thinking about how future times in which perhaps restrictive measures will be more relaxed are likely to exacerbate consumers’ sense of vulnerability and drive demand for services that are “adaptive” to environmental changes. Shaping the T&T recovery means that we also have a chance to reinvent it, and, in this context, now it is time to reshape T&T as a sustainable business. Since customers saw the considerable impact that the pollution decrease had on the environment in various parts of the world [

64,

65], they are now more aware than ever about the impact of irrational transportation, waste, and carelessness in enjoying the beauties of this world.

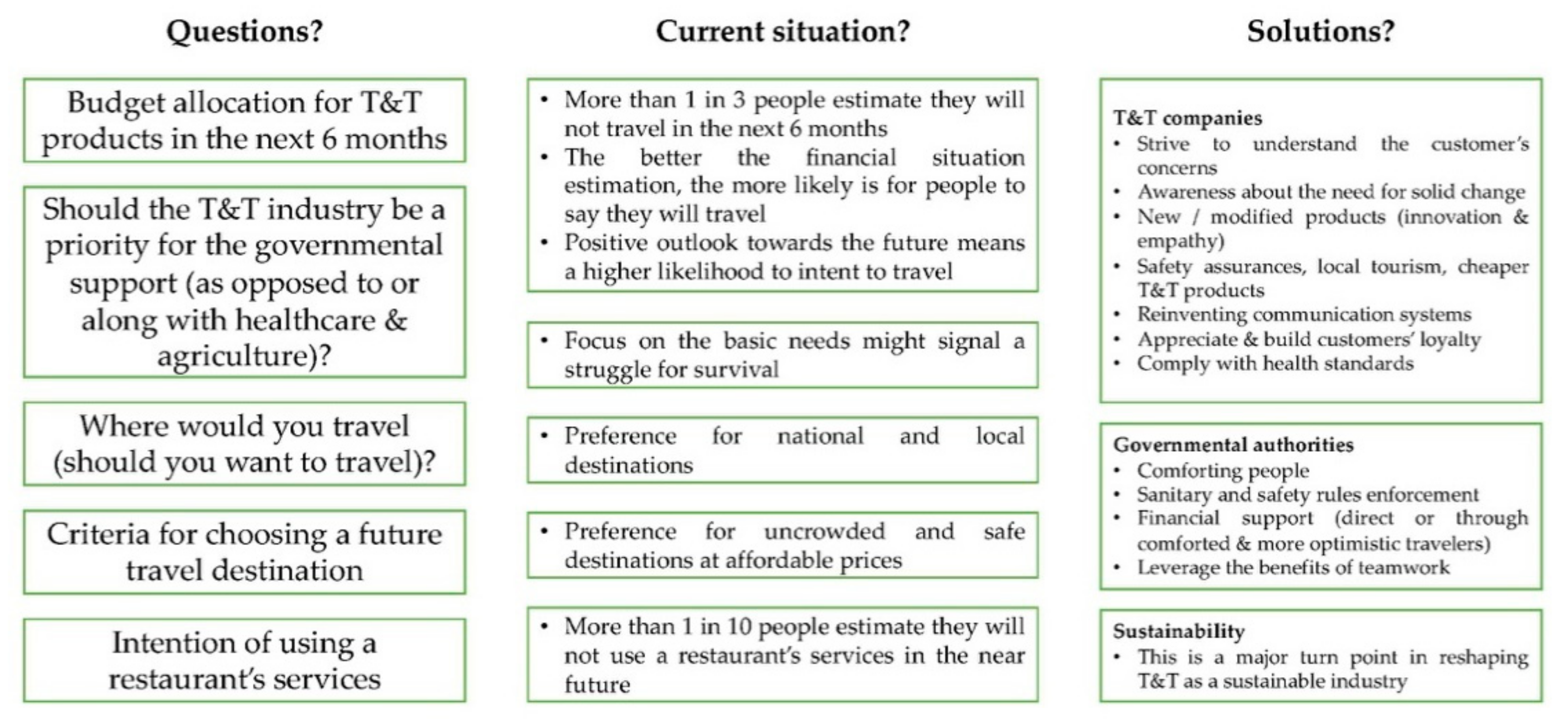

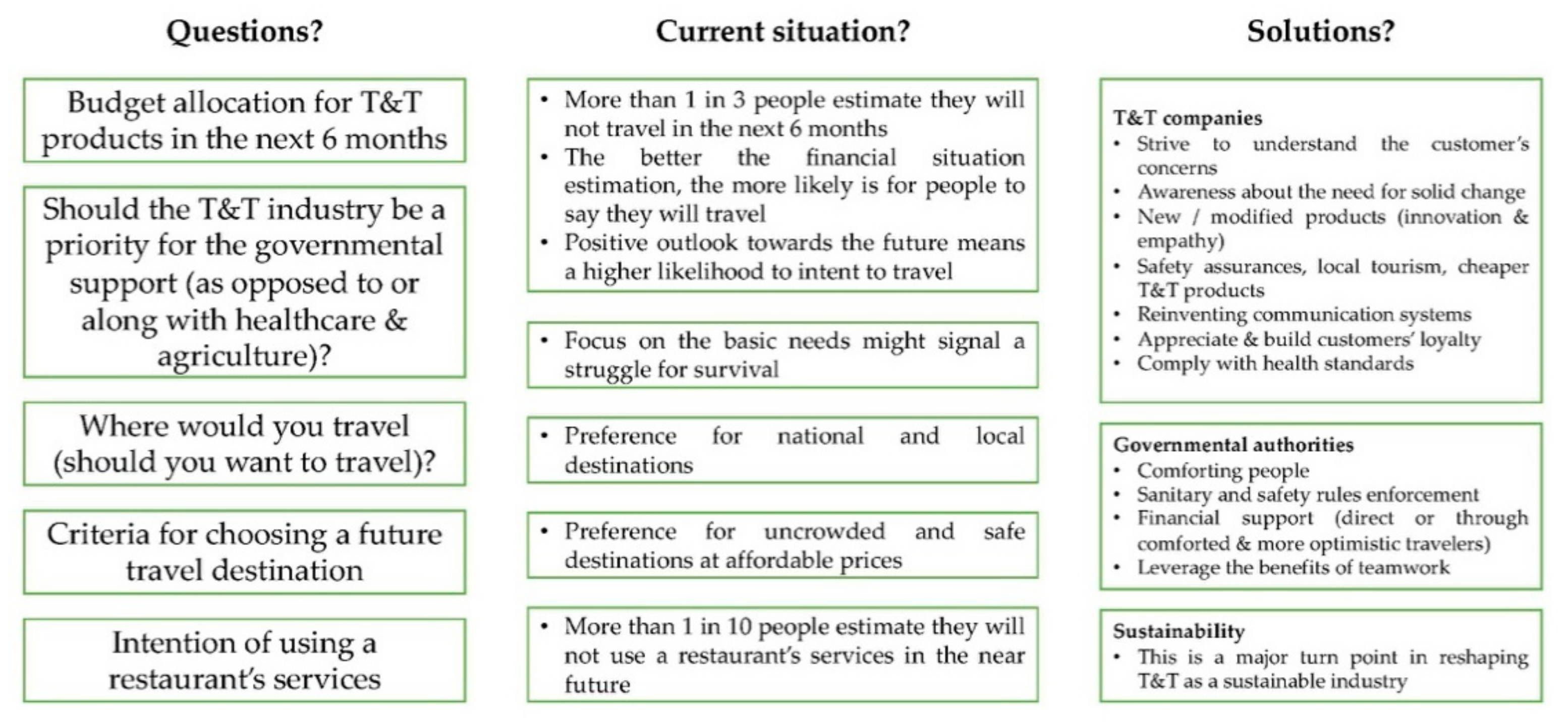

All these recommendations, together with an inventory of the major highlights of the current paper, can be found in

Figure 3. The following section will cover final remarks, conclusions, and possible directions for future research.

5. Conclusions

Due to the need to overcome the periods of lockdowns and keep the industry on a float, governmental (special layoff schemes, access to particular bank loans or subsidies, support liquidity) and business measures adopted have been primarily focused on supply-side policies. As we come closer to the recovery era, it becomes mandatory to adequately address demand-side aspects, which seem to be influenced by psychological and economic factors. Psychological factors, primarily the fear of contamination, impact travelers’ willingness to travel and their conditions and preferences for vacation destinations. It can be concluded that COVID-19 has influenced travel patterns and habits and, at least in the medium term, people will avoid traveling in large groups and being in crowded places. Hygiene and health conditions in the host destination can represent essential factors in travel decisions. Confronted with a cautious clientele, T&T businesses (such as transport, accommodation, catering) should further enhance their hygiene conditions to restore confidence. Economic factors are associated with a decline in household income, an increased propensity towards saving, or uncertain economic prospects.

The main objective of this research was to examine the fluctuating tourist perceptions on T&T expenditure and understand consumers’ expectations and criteria to reconsider purchasing such services as to provide a clear background for appropriate strategies and response measures for the T&T industry recovery. Thus, the findings of this study can serve as a point of reflection for destination marketers and crisis managers attempting to recover from this crisis. The article attempted to provide specific guidance for hospitality businesses and decisionmakers and serve as a point of reflection for destination marketers and crisis managers to consider the industry recovery, even if they come from Romania or other countries experiencing similar conditions. More specifically, the research carried out in this paper on Romania and its findings can be used as a benchmark for other market research or other countries.

The research illustrates a snapshot of a specific period during the pandemic evolution in Romania. Given that the process is a very dynamic one, a future investigation of the pandemic’s long-lasting impacts on travel behavior should be considered in a post-COVID-19 framework. Furthermore, conclusions suggest an increasing role of consumer preferences and behavioral science in sustainable tourism research.

,

,

{kind=link}

{kind=link}

{kind=link}