Knowledge Management and Sustainable Balanced Scorecard: Practical Application to a Service SME

Abstract

:1. Introduction

- Diagnosis of the SME ecosystem: Analysis of European and national policies and guidelines; Characterization of the situation and needs of SMEs.

1.1. Socio-Political Justification of the Proposed Work

1.2. Academic Justification of the Proposed Work

1.3. Brief Description of the Company

2. Bibliography Review and Working Methodology

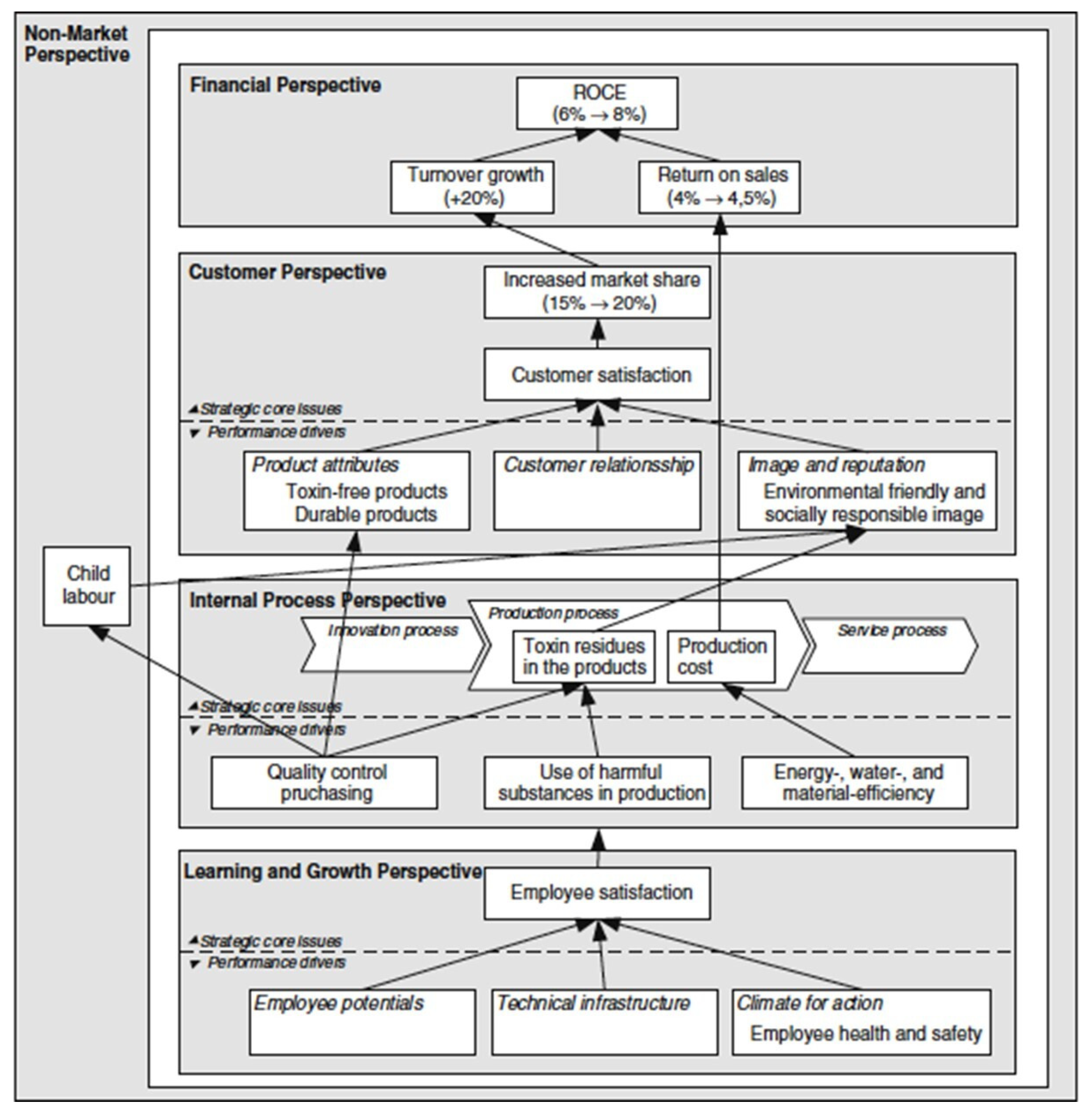

2.1. Sustainability Balanced Scorecard (SBSC): Integrating CSR in the BSC

- Its capacity to adapt, through some modifications and improvements, to different business sectors [62].

2.2. Knowledge Management (KM) and the Main Challenges of Its Management

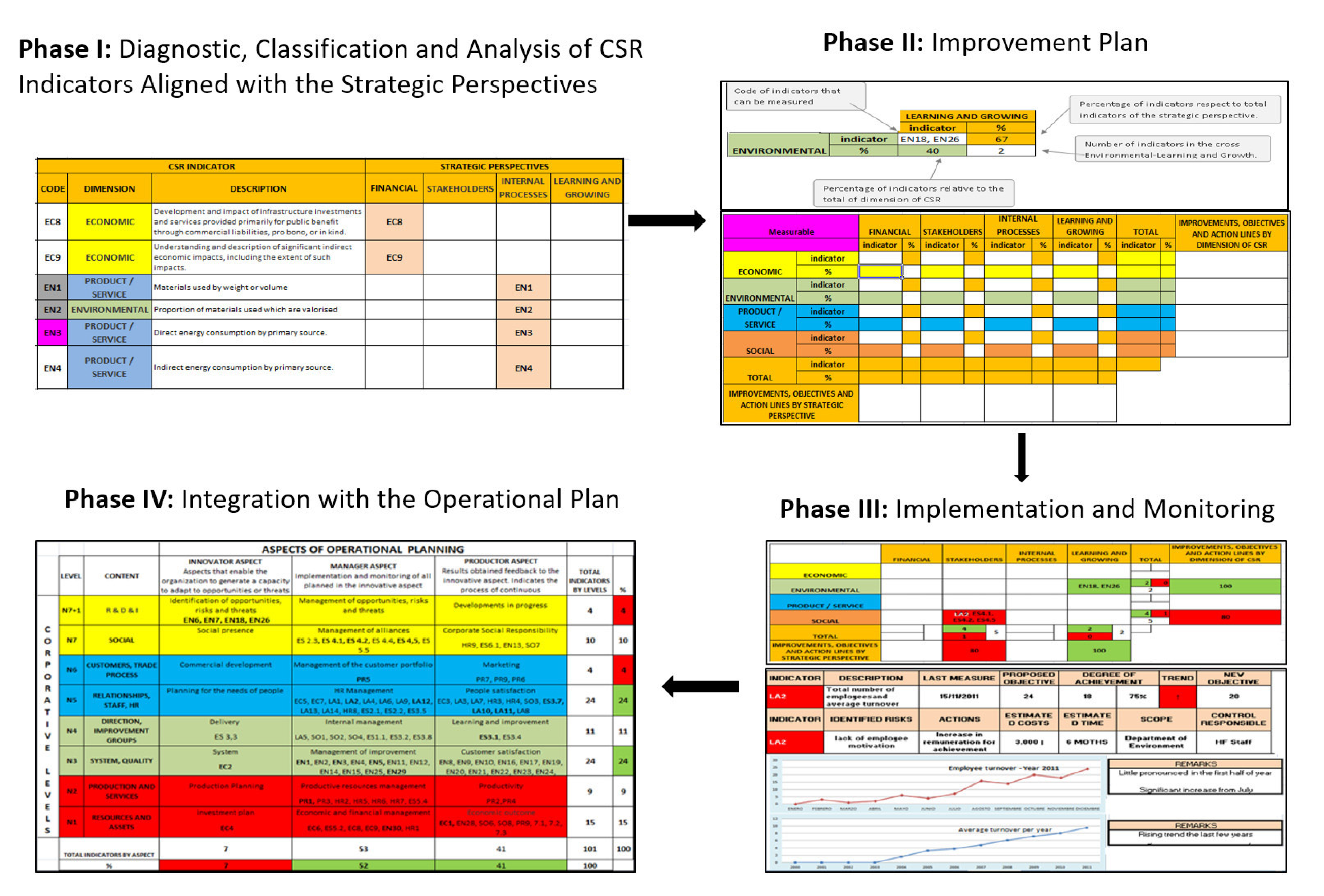

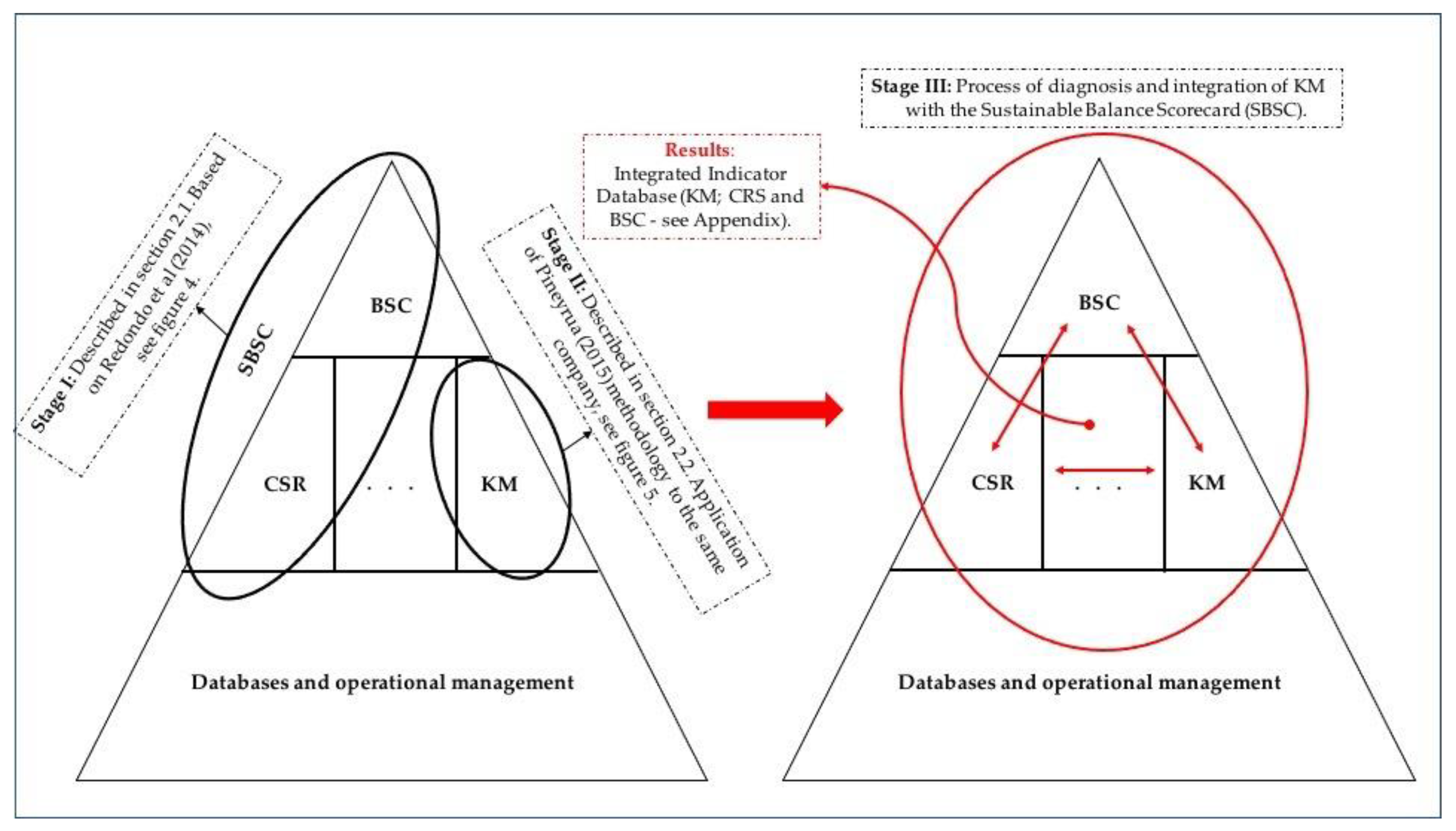

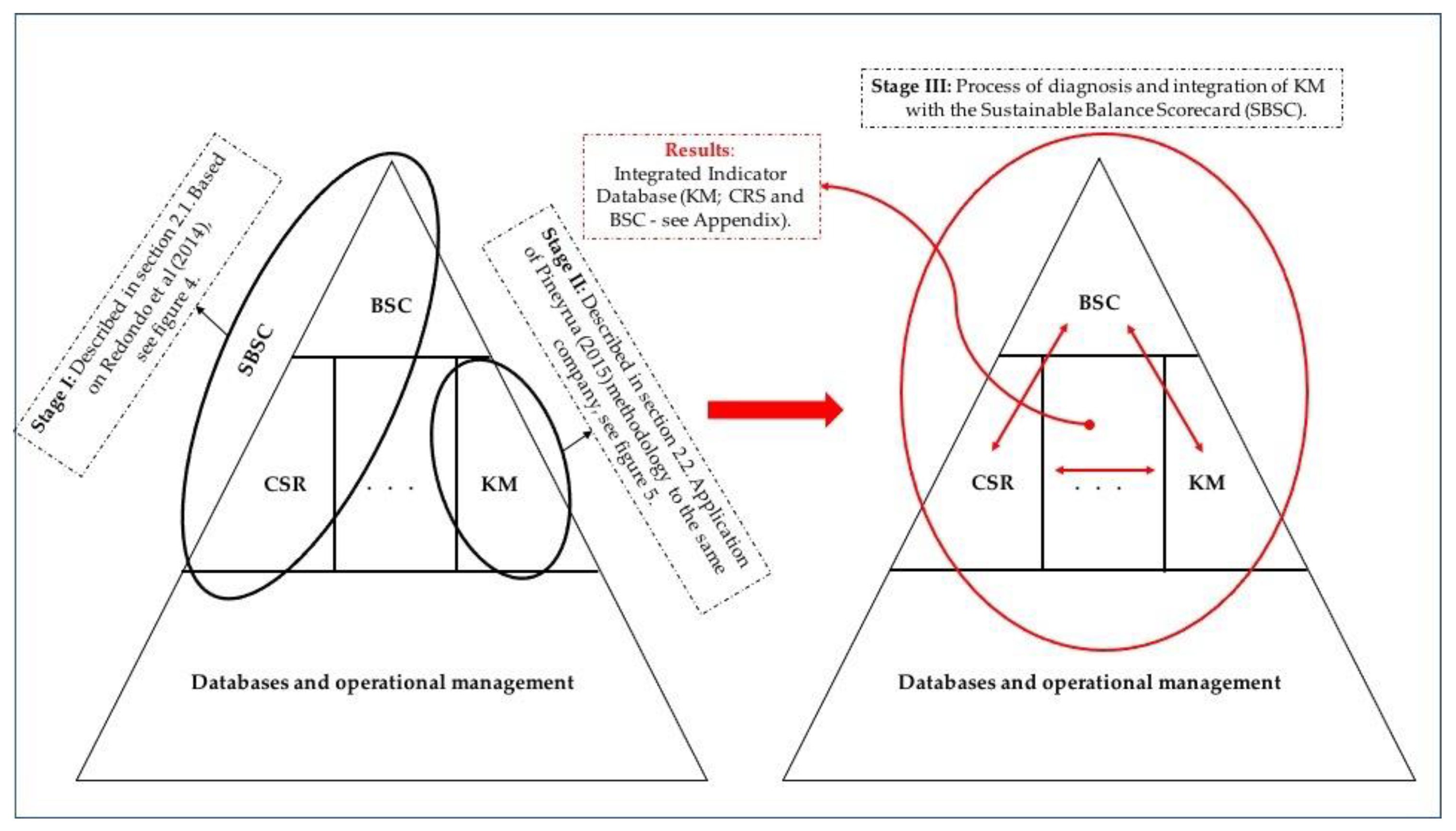

3. Process of Diagnosis and Integration of KM with the Sustainable Balance Scorecard (SBSC)—Results

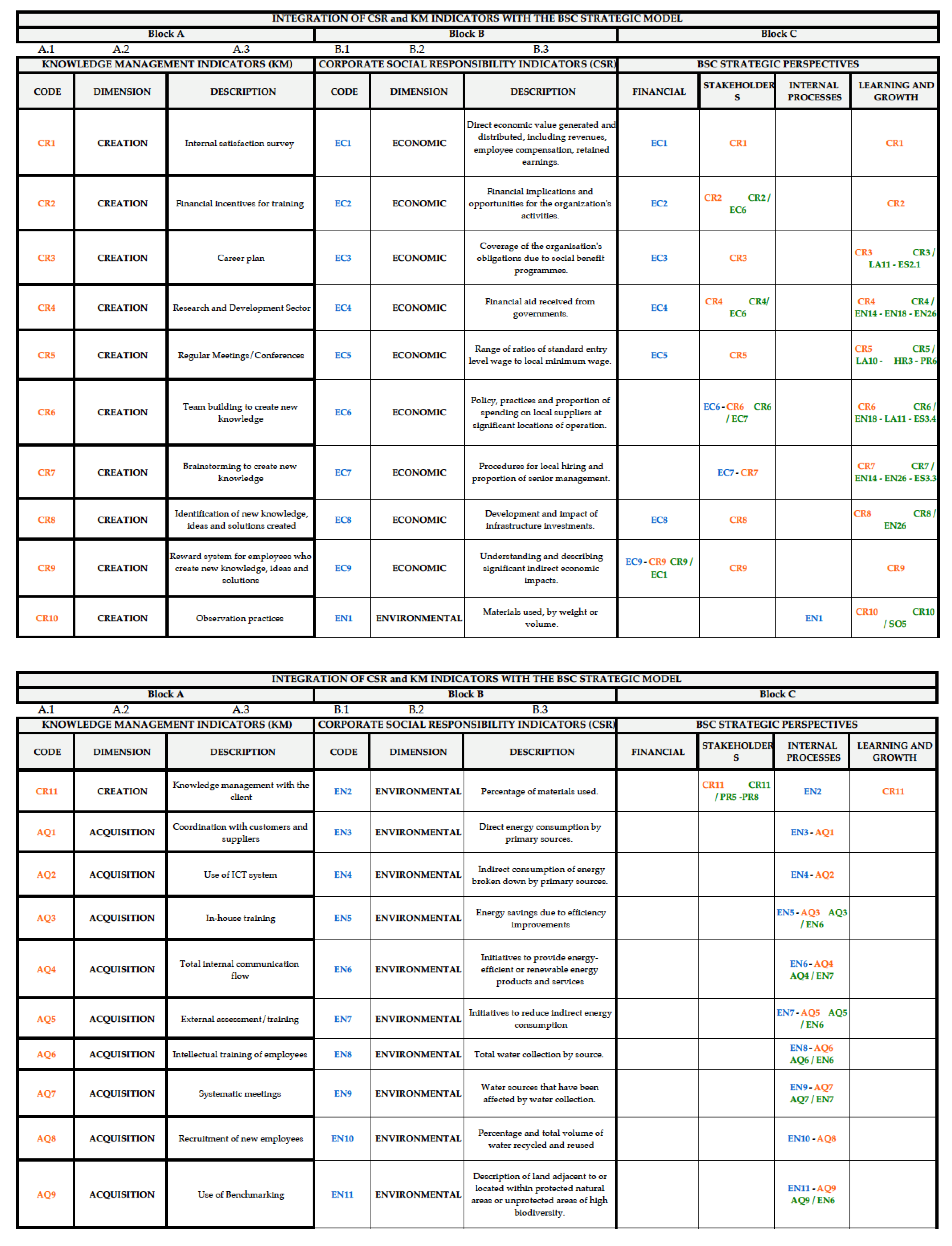

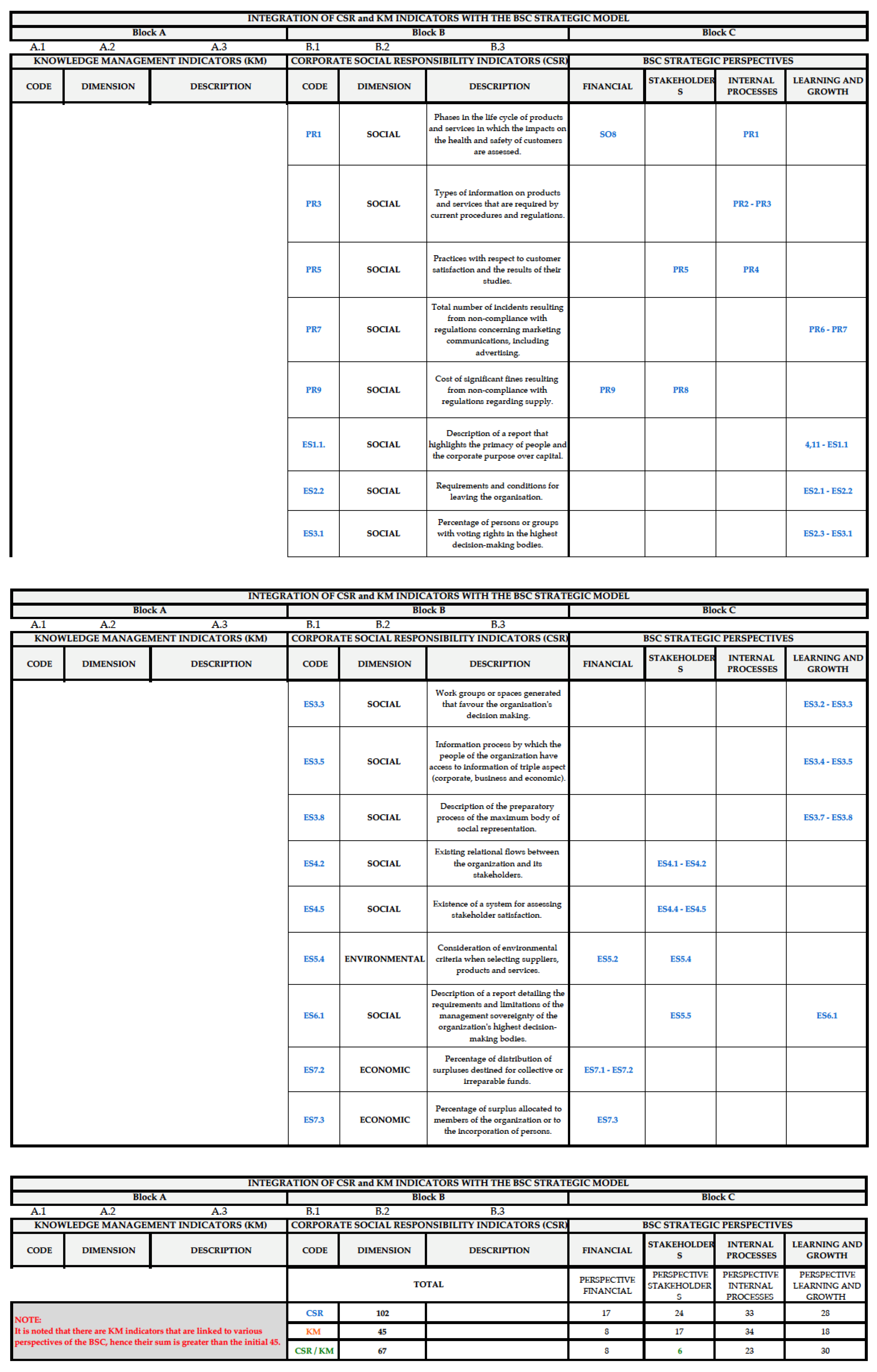

- The research of Mazorodze and Buckcley [71], Mehralian, Nazari and Ghasemzadeh [24], Gupta and Chopra [65] and Lee and Wong [25], together with the work of Pineyrua [38], allowed us to identify 45 indicators of KM in companies, compared with 13 in the original work (Column A.1 of Block A of Appendix A).

- Subsequently, based on the work of Lyu, Zhou and Zhang [75] and Kefe [79], together with Pineyrua’s [38] “knowledge creation process”, the mapping of these 45 indicators was realized with each of the perspectives of the BSC (Column A.2 of Block A of the table in Appendix A).

- In the third stage, the KM indicators were integrated with the BSC perspectives and indicators defined in Muñoz’s [39] work. The result is shown in Block C of the table in Appendix A. To achieve this result, the classification criteria shown in Table 2 have been considered.

3.1. Identification of KM and CSR Indicators in an SME

3.2. Integrated Management Model (BSC + CSR + KM) in a Consulting SME

- Level 1. Resources and Assets: These are the material and financial resources available to the organization and necessary to carry out its activity. The fundamental activities included in this level are knowledge and study of costs of each of the 7 + 1 Corporate Levels, as well as the income of the different productive units; control of margins by level; development of a budget, annual with systematic monthly monitoring; planning and control of investments; provision of the necessary financial guidelines; and management of purchases and suppliers.

- Level 2. Production and Services: Everything related to the productive activity of the company is included, with the products and services it offers. At this level, the organization’s production is planned and managed and the performance and compliance with the planning in each project is measured. The activities included in this level are definition of the organization’s service/product portfolio; production capacity and margins by product; analysis of products/services by profitability and useful life; and programming of multi-person and/or multi-task jobs and projects.

- Level 3. Quality System: Includes the management by processes of the organization and the systems implemented, whether quality, environmental management, prevention of occupational risks, energy management, etc. In addition, at this level, processes related to excellence and openness and monitoring of parts or actions aimed at continuous improvement are controlled, with all types of indicators.

- Level 4. Management—Improvement Groups: Managing the leadership of people, policies and strategy, other levels of the organization, meeting management, etc.

- Level 5. Staff: Includes management of the people who make up the organization. Personnel plans are managed for conciliation, training and the evaluation of people’s satisfaction. The activities developed are evaluation, selection, training and promotion of people (PIDE process); job maps, personnel maps; remuneration and incentive plans; and satisfaction of the people in the organization.

- Level 6. Customers—Commercial Process: Performs all activities related to customer management. It includes activities to attract new customers, information gathering to discover customers’ needs and requirements, offer processes, customer relations, customer portfolio management, satisfaction measurement, marketing, market research, etc.

- Level 7. Social: Includes everything that unites the company with society and the impact of its activity on it. It includes the legal requirements demanded by the administrations for the operation of the company, the corporate image, all the activities related to Corporate Social Responsibility, the management of external relations with public or private bodies and the management of alliances.

- Level 7 + 1. R + D + I: This level establishes one more part to be developed within each of the other seven levels, innovation, which must reach all areas of the organization. It represents excellence at all levels, and how, based on innovation and learning, the continuous improvement of the organization is sought. At this level, R&D and the design of new and innovative services are managed, as well as all the processes related to the monitoring of the environment, which allow the organization to be up to date with external innovations that can give rise to opportunities for improvement.

4. Conclusions

- From a financial perspective, the KM indicators identified (see Table 5) correspond to the “knowledge application” stage, and their objective is to improve the efficiency of the company’s management and productivity levels, taking into account the knowledge of the workers, and expressed through measurable financial indicators.

- The perspective of the stakeholders is linked to the processes of creation and application of knowledge. Through the indicators collected there, it is shown how the company responds to external changes, which is demonstrated through the quality, performance and support of the company’s products and services, in addition to developing innovation in its technologies and services.

- The work carried out corroborates the importance that KM has on the perspective of improving the company’s internal processes, as already indicated in Gupta and Chopra [64]. Just like in the mapping carried out by Lyu, Zhou and Zhang [75], for the service SME analyzed, the internal process perspective is the one that presents the highest number of KM processes. This allows us to analyze and manage the company’s capacity to acquire, transfer and apply knowledge, thus contributing to the improvement of its internal processes.

- For the company not only to maintain but also to improve its performance (growth), employees must learn, grow and innovate continuously. All these aspects are linked to the process of creation and the application of knowledge, which has a very high correlation with the learning and growth perspective of the BSC.

- SMEs are highly dependent on external knowledge from customers and suppliers, as their sources of knowledge are limited, all of which are captured in indicators AQ1, CR11 and TR12.

- Indicators are also needed to assess how employees are acquiring knowledge, and indicators AP2, AP4, CR7, AQ5, AQ11, AQ12 and TR11 are often used for this purpose.

- Knowledge sharing in an SME occurs through informal activities, such as those listed in indicators TR6 and TR9, while the use of IT in SMEs is usually assessed using indicators AQ2, AQ11 and TR1.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

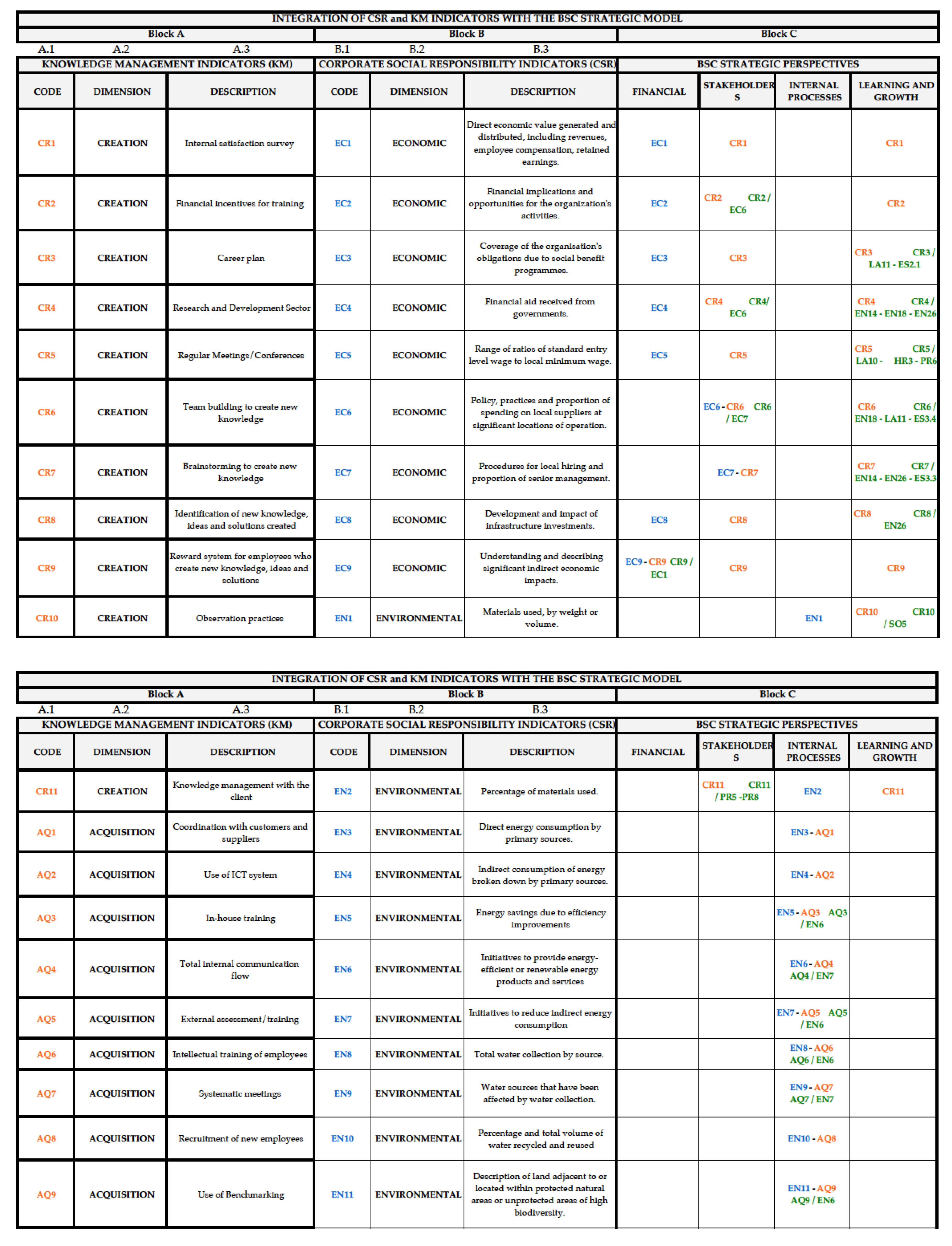

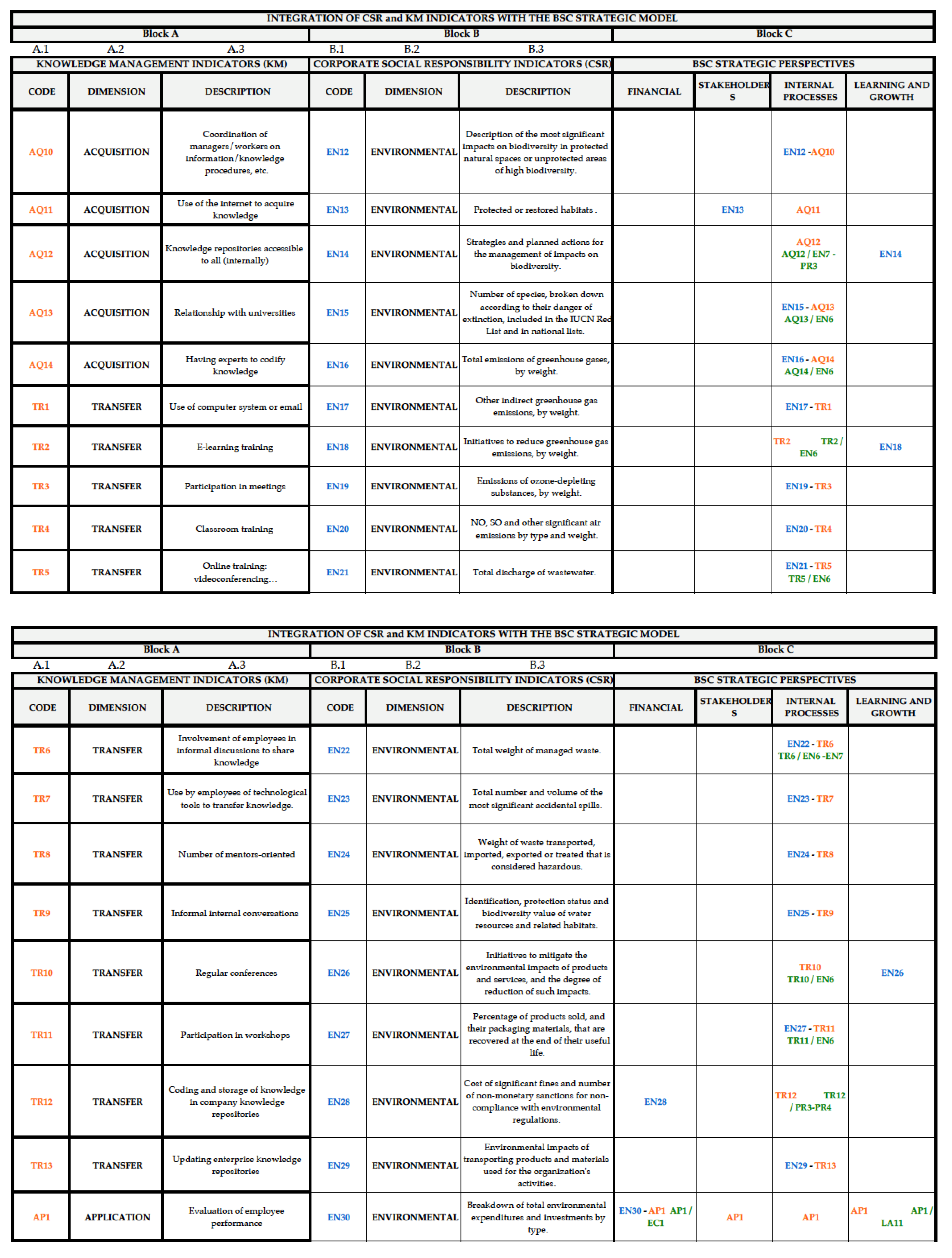

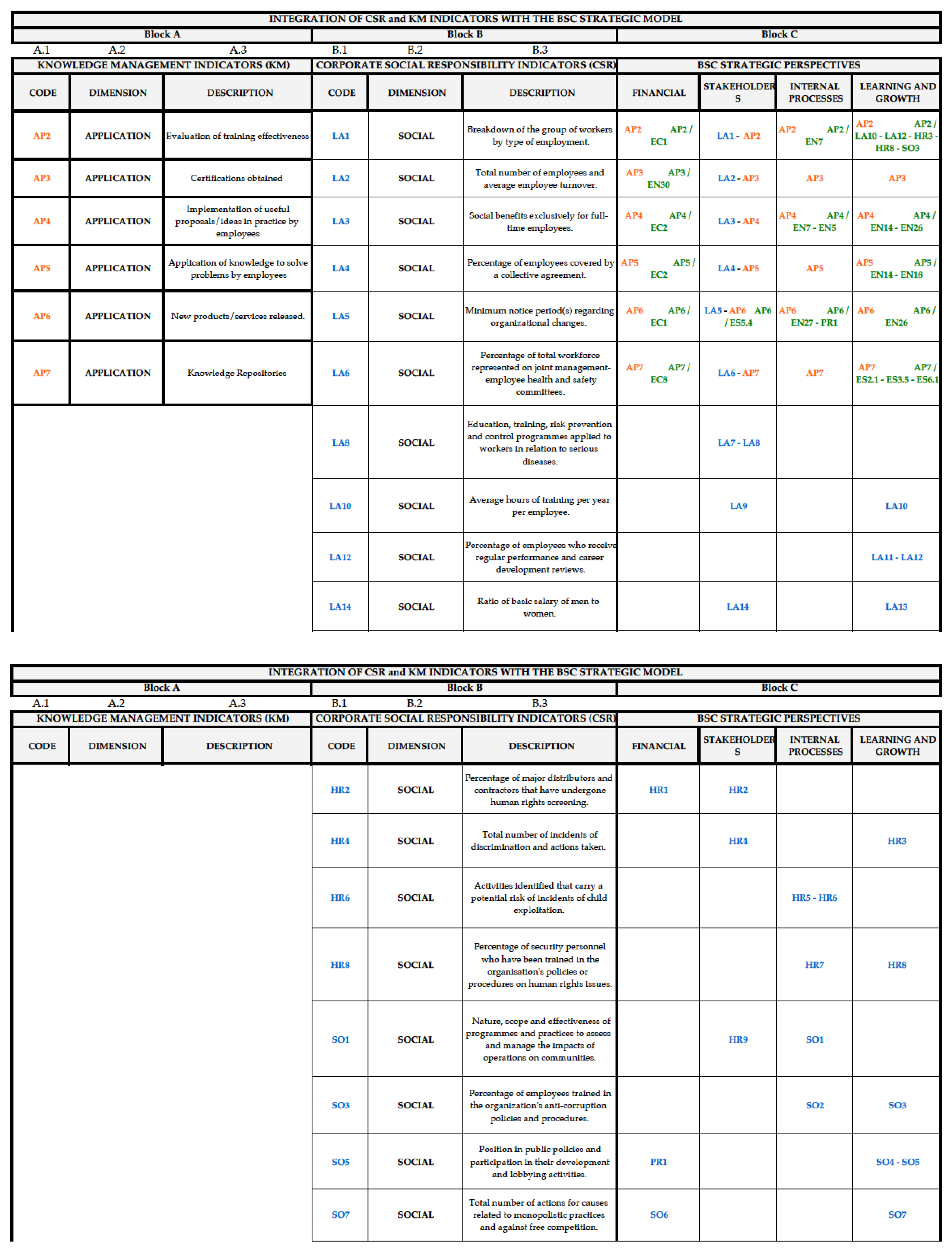

Appendix A

References

- Cardozo, E.; Velasquez de Naime, Y.; Rodríguez, C. El concepto y la clasificación de PYME en América Latina. Glob. Conf. Bus. Financ. Proc. 2012, 7, 1657–1668. [Google Scholar]

- International Finance Corporation. SME Governance Guidebook; Pennsylvania Avenue: Washington, DC, USA, 2019. [Google Scholar] [CrossRef]

- Turner, R.; Ledwith, A. Project Management in Small to Medium-Sized Enterprises: Fitting the Practices to the Needs of the Firm to Deliver Benefit. J. Small Bus. Manag. 2016, 56. [Google Scholar] [CrossRef]

- Commission Regulation (EU) No 651/2014 of 17 June 2014 declaring certain categories of aid compatible with the internal market in application of Articles 107 and 108 of the Treaty. Off. J. Eur. Union 2014, L 187, 1–78.

- International Labour Organization—ILO. Small Matters: Global Evidence on the Contribution to Employment by the Self-Employed, Micro-Enterprises and SMEs; Executive Summary; International Labour Organization: Geneva, Switzerland, 2019. [Google Scholar]

- International Labour Organization—ILO. Small Matters: Global Evidence on the Contribution to Employment by the Self-Employed, Micro-Enterprises and SMEs; Report; International Labour Organization: Geneva, Switzerland, 2019. [Google Scholar]

- U.S. Bureau of Labor Statistics. United States Small Business Profile; 2018. Available online: https://www.bls.gov/web/cewbd/table_f.txt (accessed on 5 March 2021).

- Gouardères, F. Small and Medium-Sized Enterprises. Fact Sheets on the European Union; European Parliament: Brussels, Belgium, 2021; Available online: https://www.europarl.europa.eu/factsheets/en/sheet/63/small-and-medium-sized-enterprises (accessed on 3 April 2021).

- Ministerio de Industria, Comercio y Turismo. Cifras Pyme Marzo 2021; Ministerio de Industria, Comercio y Turismo: Madrid, Spain, 2021. [Google Scholar]

- Muñoz, A.E.; Mayor, M.P. Las pyme en América Latina, Japón, la Unión Europea, Estados Unidos y los clúster en Colombia. Adm. Desarro. 2015, 45, 7–24. [Google Scholar] [CrossRef]

- Henriquez, L. Políticas para las MIPYMES Frente a la Crisis. Conclusiones de un Estudio Comparativo de América Latina y Europa; Documento de Trabajo; OIT: Geneva, Switzerland; EuropeAid: Brussels, Belgium, 2009. [Google Scholar]

- OECD. OECD SME and Entrepreneurship Outlook 2019; Publishing: Paris, France, 2019. [Google Scholar] [CrossRef]

- Moral-Benito, E. Growing by learning: Firm-level evidence on the size-productivity nexus. SERIEs 2018, 9, 65–90. [Google Scholar] [CrossRef] [Green Version]

- Cámara, L.; Lozano, J. Understanding Cloud Computing Market Dynamics in Europe; BBVA Research; Digital Economy and Digital Regulation: Madrid, Spain, 2019. [Google Scholar]

- Camison, C.; de Lucio, J. La competitividad de las PYMES españolas ante el reto de la globalización. Econ. Ind. 2010, 375, 19–40. [Google Scholar]

- Campo, S.; Jiménez, J. El capital directivo y las buenas prácticas de gestión de las PYMES españolas. Econ. Ind. 2019, 414, 93–106. [Google Scholar]

- FAEDPYME, Fundación para el Análisis Estratégico y Desarrollo de la Pyme. Análisis Estratégico para el Desarrollo de la PYME en España: Digitalización y Responsabilidad Social; FAEDPYME: Madrid, Spain, 2018; ISBN 978-84-17619-75-6. [Google Scholar]

- OECD. OECD Compendium of Productivity Indicators 2019; OECD Publishing: Paris, France, 2019. [Google Scholar] [CrossRef]

- CEPYME, Confederación Española de la Pequeña y Mediana Empresa. Guía para Pymes ante los Objetivos de Desarrollo Sostenible; Consejo General de Economistas de España, Red Española del Pacto Mundial de Naciones Unidas: Madrid, Spain, 2019; ISBN 978-84-86658-78-6. [Google Scholar]

- Communication from the Commission to the Council, the European Parliament, the European Economic and Social Committee and the Committee of the Regions—“Think Small First”—A “Small Business Act” for Europe {SEC(2008) 2101} {SEC(2008) 2102} /* COM/2008/0394 Final. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52008DC0394&from=EN (accessed on 4 March 2021).

- Federal Ministry for Economic Affairs on behalf of the SME Envoys Network. European SME-Action Programme; Federal Ministry for Economic Affairs: Madrid, Spain, 2017. [Google Scholar]

- Ministerio de Industria, Comercio y Turismo. Marco Estratégico en Política de Pyme 2030; Ministerio de Industria, Comercio y Turismo: Madrid, Spain, 2019. [Google Scholar]

- Catoiu, I.; Tudor, L.; Bisa, C. Knowledge-intensive business services and business Consulting services in Romanian changing economic environment. Amfiteatru Econ. J. 2016, 18, 40–54. Available online: http://hdl.handle.net/10419/168986 (accessed on 16 March 2021).

- Mehralian, G.; Nazari, J.A.; Ghasemzadeh, P. The effects of knowledge creation process on organizational performance using the BSC approach: The mediating role of intelectual capital. J. Knowl. Manag. 2018, 22, 802–823. [Google Scholar] [CrossRef]

- Lee, C.S.; Wong, K.Y. Development and validation of knowledge management performance measurement constructs for small and medium enterprises. J. Knowl. Manag. 2015, 4, 711–734. [Google Scholar] [CrossRef]

- Dneprovskaya, N.; Urintsov, A.; Komleva, N.; Staroverova, O. Evaluation Indicators of Knowledge Management in the State Service. In Proceedings of the 19th European Conference on Knowledge Management (ECKM 2018), Padua, Italy, 6–7 September 2018; pp. 182–189, ISBN 978-1-5108-7210-3. Available online: http://toc.proceedings.com/41358webtoc.pdf (accessed on 5 March 2021).

- Ling, Y.H. Influence of corporate social responsibility on organizational performance Knowledge management as moderator. Vine J. Inf. Knowl. Manag. Syst. 2019, 49, 327–352. [Google Scholar] [CrossRef]

- Iwamoto, H.; Suzuki, H. An empirical study on the relationship of corporate financial performance and human capital concerning corporate social responsibility: Applying SEM and Bayesian SEM. Cogent Bus. Manag. 2019, 6. [Google Scholar] [CrossRef]

- Öberseder, M.; Schlegelmilch, B.B.; Murphy, P.E.; Gruber, V. Consumers’ perceptions of corporate social responsibility: Scale development and validation. J. Bus. Ethics 2014, 124, 101–115. [Google Scholar] [CrossRef] [Green Version]

- Latif, F.; Pérez, A.; Alam, W.; Saqib, A. Development and validation of a multi-dimensional customer-based scale to measure perceptions of corporate social responsibility (CSR). Soc. Responb. J. 2019, 15, 492–512. [Google Scholar] [CrossRef] [Green Version]

- Redondo, A.C.; Pascual, J.A.R.; Gento, A.M.M.; Muñoz, J.S. Sustainable balanced scorecard: Practical application to a services company. Managing Complexity. Lect. Notes Manag. Ind. Eng. 2014, 67–75. [Google Scholar] [CrossRef]

- Lorino, P.; Tarondeau, J.C. De la stratégie aux processus stratégiques. Rev. Fr. Gestion 2015, 253, 231–250. [Google Scholar] [CrossRef]

- Kaplan, R.; Norton, D. The balanced scorecard measures that drive performance. Harv. Bus. Rev. 1992, 70, 71–79. [Google Scholar]

- Kaplan, R.; Norton, D. Using the balanced scorecard as a strategic management system. Harv. Bus. Rev. 2007, 85, 150–161. [Google Scholar]

- Karabece, K.; Gürbüz, T. An Integrated Balanced Scorecard and Fuzzy BOCR Decision Model for Performance Evaluation. Adv. Intell. Syst. Comput. 2019, 843–851. [Google Scholar] [CrossRef]

- Doorn, J.V.; Onrust, M.; Verhoef, P.C.; Bügel, M.S. The impact of corporate social responsibility on customer attitudes and retention—the moderating role of brand success indicators. Mark. Lett. 2017, 28, 607–619. [Google Scholar] [CrossRef] [Green Version]

- Gangi, F.; Mustilli, M.; Varrone, N. The impact of corporate social responsibility (CSR) knowledge on corporate financial performance: Evidence from the European banking industry. J. Knowl. Manag. 2019, 23, 110–134. [Google Scholar] [CrossRef]

- Pineyrua, D.G.F. A Criação do Conhecimento na Indústria de Celulose: Estudos de Casos Múltiplos. Ph.D. Thesis, Universidade Nove de Julho, São Paulo, Brazil, 2015. [Google Scholar]

- Muñoz, J.S. Cuadro de Mando Responsable: Aplicación Práctica en la Consultora 1A Consultores. Proyecto Fin de Carrera, Dirigido por A. Redondo Castán en la E.I. Industriales; Universidad de Valladolid: Valladolid, Spain, 2012. [Google Scholar]

- Clara, C.; de la Morena, J.; Cortés, H. Evolución y nuevas tendencias de Responsabilidad Social en las prácticas empresariales. Rev. Responsab. Soc. Empresa 2018, 29, 17–50. [Google Scholar]

- Villafán, K.B. Evolución Conceptual de La Responsabilidad Social. Rev. Fac. Contaduría Cienc. Adm. 2020, 5, 69–80. [Google Scholar]

- Latapí Agudelo, M.A.; Jóhannsdóttir, L.; Davídsdóttir, B. A literature review of the history and evolution of corporate social responsibility. Int. J. Corp. Soc. Responsib. 2019, 4. [Google Scholar] [CrossRef] [Green Version]

- Abhishek, T.; Bains, A. Evolution of Corporate Social Responsibility: A Journey from 1700 BC till 21st Century. Int. J. Adv. Res. 2013, 1, 788–796. [Google Scholar]

- Yevdokymova, M.; Zamlynskyi, V.; Minakova, S.; Biriuk, O.; Ilina, O. Evolution of corporate social responsibility applied to the concept of sustainable development. J. Secur. Sustain. Issues 2019, 8, 473–480. [Google Scholar] [CrossRef]

- Font, I.; López, M.; Pérez, S. La Responsabilidad Social Empresarial: Un Fenómeno en Evolución. In Políticas Públicas y Renovación Social en el Siglo XXI, 1st ed.; Editorial HESS, S.A.: Mexico City, Mexico, 2017; pp. 227–259. ISBN 978-987-1285-53-2. [Google Scholar]

- Lizcano-Prada, J.; Lombana, J. Responsabilidad Social Corporativa (RSC). Civ. Cienc. Soc. Hum. 2018, 18, 119–134. [Google Scholar] [CrossRef]

- Puentes, A.; Lis Gutiérrez, M. Medición de la responsabilidad social empresarial: Una revisión de la literatura (2010–2017). Rev. Suma Neg. 2018, 9, 145–152. [Google Scholar]

- Global Reporting Initiative (GRI). GRI and ISO 26000: How to Use the GRI Guidelines in Conjunction with ISO 26000; Global Reporting Initiative: Amsterdam, The Netherlands, 2011; ISBN 978-90-8866-041-2. [Google Scholar]

- Hansen, E.G.; Schaltegger, S. The Sustainability Balanced Scorecard: A Systematic Review of Architectures. J. Bus. Ethics 2016, 133, 193–221. [Google Scholar] [CrossRef]

- Epstein, M.J.; Wisner, P.S. Using a Balanced Scorecard to Implement Sustainability. Environ. Qual. Manag. 2001, 11, 1–10. [Google Scholar] [CrossRef]

- Epstein, M.J.; Wisner, P.S. Good Neighbors: Implementing Social and Environmental Strategies with the BSC. In Balanced Scorecard Report; Reprint Number B0105C; Harvard Business School: Cambridge, MA, USA, 2001. [Google Scholar]

- Rohm, H.; Montgomery, D. Link Sustainability to Corporate Strategy Using the Balanced Scorecard; The Balanced Scorecard Institute: Cary, NC, USA, 2011. [Google Scholar]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The sustainability balanced scorecard—Linking sustainability management to business strategy. Bus. Strategy Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Valmohammadi, C.; Ahmadi, M. The impact of knowledge management practices on organizational performance. A balanced scorecard approach. J. Enterp. Inform. Manag. 2015, 28, 131–159. [Google Scholar] [CrossRef]

- Nguyen, D.; Ngo, T.; Nguyen, R.; Cao, H.; Pham, H. Corporate social responsibility, balanced scorecard system and financial performance in the service sector: The case of Vietnam. Manag. Sci. Lett. 2019, 9, 2215–2228. [Google Scholar] [CrossRef]

- Shafiee, M.; Hosseinzadeh, F.L.; Saleh, H. Supply chain performance evaluation with data envelopment analysis and balanced scorecard approach. Appl. Math. Model. 2014, 38, 5092–5112. [Google Scholar] [CrossRef]

- Jones, P. Strategy Mapping for Learning Organizations: Building Agility into Your Balanced Scorecard; Rutledge: Abingdon-on-Thames, UK, 2016; ISBN 978-0-566-08811-7. [Google Scholar]

- Niven, P.R. Balanced Scorecard Evolution: A Dynamic Approach to Strategy Execution; John Wiley & Sons: Hoboken, NJ, USA, 2014; ISBN 978-1-118-72631-0. [Google Scholar]

- Smith, R.F. Business Process Management and the Balanced Scorecard: Using Processes as Strategic Drivers; John Wiley & Sons: Hoboken, NJ, USA, 2007; ISBN 978-0-470-04746-0. [Google Scholar]

- Wiraeus, D.; Creelman, J. Agile Strategy Management in the Digital Age: How Dynamic Balanced Scorecards Transform Decision Making, Speed and Effectiveness; Palgrave MacMillan: London, UK, 2019. [Google Scholar] [CrossRef]

- Bhagwat, R.; Sharma, M.K. Performance measurement of supply chain management: A balanced scorecard approach. Comput. Ind. Eng. 2007, 53, 43–62. [Google Scholar] [CrossRef]

- Pérez, C.A.; Montequín, V.R.; Fernandéz, F.O.; Balsera, J.V. Integration of Balanced Scorecard (BSC), Strategy Map, and Fuzzy Analytic Hierarchy Process (FAHP) for a Sustainability Business Framework: A Case Study of a Spanish Software Factory in the Financial Sector. Sustainability 2017, 9, 527. [Google Scholar] [CrossRef] [Green Version]

- Hristov, I.; Chirico, A.; Appolloni, A. Sustainability Value Creation, Survival, and Growth of the Company: A Critical Perspective in the Sustainability Balanced Scorecard (SBSC). Sustainability 2019, 11, 2119. [Google Scholar] [CrossRef] [Green Version]

- Nikolaou, I.E.; Tsalis, T.A. Development of a Sustainable Balanced Scorecard Framework; Ecological Indicators; Elsevier: Amsterdam, The Netherlands, 2013; Volume 34, pp. 76–86. [Google Scholar]

- Gupta, V.; Chopra, M. Gauging the impact of knowledge management practices on organizational performance—A balanced scorecard perspective. J. Inform. Knowl. Manag. Syst. 2018, 48, 21–46. [Google Scholar] [CrossRef]

- Muñumer, H. La Responsabilidad Social de la Empresa. Actualización del Sistema de Gestión Ética (SGE21:2008) e Integración de los Criterios de la Guía de Responsabilidad Social ISO26000:2010. Proyecto Fin de Carrera, dirigido por A. Redondo Castán en la E.I. Industriales; Universidad de Valladolid: Valladolid, Spain, 2011. [Google Scholar]

- Iazzolino, G.; Laise, D.; Gabriele, R. Knowledge-based strategies and sustainability: A framework and a case study application. Meas. Bus. Excel. 2017, 21, 152–174. [Google Scholar] [CrossRef]

- Nonaka, I.; Takeuchi, H. The Knowledge-Creating Company: How Japanese Companies Create the Dynamics of Innovation; Harvard Business Press: Boston, MA, USA, 1997. [Google Scholar]

- Hanif, M.I.; Malik, F.; Hamid, A.B.A. The effect of knowledge management and entrepreneurial orientation on organization performance. J. Entrep. Educ. 2018, 21, 1–13. [Google Scholar]

- Pour, M.J.; Zadeh, Z.K.; Zadeh, N.A. Designing an Integrated Methodology for Knowledge Management Strategic Planning. The roadmap toward strategic alignment. Knowl. Manag. Strateg. Plan. 2018, 48, 373–387. [Google Scholar] [CrossRef]

- Mazorodze, A.H.; Buckley, S. Knowledge management in knowledge-intensive organisations: Understanding its benefits, processes, infrastructure and barriers. S. Afr. J. Inform. Manag. 2019, 1, 1–6. [Google Scholar] [CrossRef]

- Mills, A.M.; Smith, T.A. Knowledge management and organizational performance: A decomposed view. J. Knowl. Manag. 2011, 15, 156–171. [Google Scholar] [CrossRef]

- Arora, R. Implementing KM—A balanced scorecard approach. J. Knowl. Manag. 2002, 240–249. [Google Scholar] [CrossRef]

- Wake, N.J. The use of the balanced scorecard to measure knowledge work. Intern. J. Product. Perfor. Manag. 2015, 64, 590–602. [Google Scholar] [CrossRef]

- Lyu, H.; Zhou, Z.; Zhang, Z. Measuring Knowledege Management Performance in Organizations: Na Integrative Framework of Balanced Scorecard and Fuzzy Evaluation. Information 2016, 7, 29. [Google Scholar] [CrossRef] [Green Version]

- Rajnoha, R.; Lesníková, P.; Krajcík, V. Influence of business performance measurement systems and corporate sustainability concept to overal business performance: “Save the planet and keep your performance”. Bus. Adm. Manag. 2017, 1, 111–127. [Google Scholar] [CrossRef]

- Bumberová, V.; Milichovský, F. Sustainability Development of Knowledge-Intensive Business Services: Strategic Actions and Business Performance. Sustainability 2019, 11, 5136. [Google Scholar] [CrossRef] [Green Version]

- Chen, H.; Miao, Y. Knowledge Management for SMEs Based on the Balanced Scorecard. In Proceedings of the International Conference on Management and Service Science, Wuhan, China, 24–26 August 2010. [Google Scholar] [CrossRef]

- Kefe, I. The Determination of Performance Measures by using a Balanced Scorecard Framework. Found. Manag. 2019, 11, 43–56. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Governance model: It is the cornerstone in the development of the Strategic Framework, and its main objective is to support the monitoring and subsequent achievement of the lines of action. | |

| Challenges and opportunities | Lines of action |

| Organisational structure | Its organisational and functional structure must be aligned with the strategic lines of action. |

| Monitoring model | Defining the right set of indicators, and Establish the necessary instruments to carry out a complete and comprehensive monitoring of indicators in accordance with the defined strategy. |

| Strategic lines | |

| Challenges and opportunities | Lines of action |

| Entrepreneurship | LA1. Boosting skills development and training for employment LA2. Prestigate and promote vocational training LA3. Strengthening the SME culture and fostering entrepreneurship LA4. Measures to stimulate the entrepreneurial ecosystem LA5. Continue to make progress in the simplification of setting up an SME, as well as in the improvement and development of support services. LA6. Encourage and simplify the transfer of businesses LA7. Measures to promote second chance |

| Business management and talent | LA8. Measures for attracting and retaining talent in SMEs. LA9. Improving business management training. LA10. Advancing the digital skills of employers and employees LA11. Encourage intra-entrepreneurship LA12. Promoting corporate social responsibility |

| Regulatory framework | LA13. Encourage the creation of larger companies through the merger of existing SMEs. LA14. Advise SMEs through personalised support that favours their growth. LA15. Simplify sectoral regulation LA16. Improve inter-administrative coordination in relation to SME activity. LA17. Encourage cooperation between large companies and SMEs: Encourage cooperation between large and small companies through procurement to enable the latter to improve their management and productivity. LA18. Encourage public procurement of SMEs by the Administration. |

| Funding | LA19. Promote alternatives to bank financing LA20. Expanding financial availability at different stages of the life cycle of SMEs LA21. Reorient taxation conditions to improve SME financing. LA22. Simplifying access to aid for SMEs LA23. Strengthening mechanisms to reduce late payments LA24. Development of a framework on Moveable Collateral LA25. Strengthen the Spanish guarantee system and promote its knowledge and use among SMEs. LA26. Promote information and training on public finance LA27. Promoting good governance and financial transparency of SMEs LA28. Encourage more flexible access requirements and promote the advantages of the Alternative Stock Market and the Alternative Fixed Income Market, as well as crowdfunding and crowdlending platforms. LA29. Other financing measures |

| Innovation and digitalisation | LA30. Incorporate digital tools in the relationship between SMEs and the Administration. LA31. Facilitating the digital transformation of SMEs as a key element in their life cycle. LA32. Fostering business collaboration and the development of business clusters LA33. Encourage innovation programmes among SMEs as well as the development of innovative ecosystems. LA34. One-stop shop for innovation LA35. Funding for digitisation LA36. Develop assistance programmes for SMEs in Industry 4.0. LA37. Supporting the uptake of enabling technologies—KETs LA38. Promote awareness among SMEs on how to protect their industrial property rights as well as intellectual property. LA39. Funding for innovation |

| Sustainability | LA40. Promoting environmental information, communication and dissemination LA41. Make progress in the simplification and implementation of environmental regulation. LA42. Facilitating the transformation to a circular economy LA43. Facilitating the transition to a low-carbon economy |

| Internationalization | LA44. Increase information on the resources and services available for internationalization assistance. LA45. Favour the integral accompaniment of the company in its internationalization process. LA46. Increase the base of companies that export regularly. LA47. Ensure financial support for internationalization operations. LA48. Encourage foreign investment in Spain LA49. Facilitating the digitalization of SMEs as a dynamizing element of their export activity. LA50. Expand and strengthen the presence of Economic and Commercial Offices in the external network |

| Perspective | Items Included |

|---|---|

| Financial | Economic profitability. Sales and income, expenses and costs. Sources of income: customers, products, markets. Improvement of tangible and intangible economic assets. Creation of value and turnover. Financial management and structure (including threats, opportunities and risks). Investments. Sanctions. |

| Stakeholders | Stakeholder management (shareholders, partners, staff, customers, suppliers, competition, society, public administrations, financial institutions, associations, universities, NGOs, media). Environmental management not related to the direct activity developed in the company. Information and communication systems (ICT). Commitment to the principles of social responsibility. Education, training, advice, prevention and control of occupational risks. |

| Internal Processes | Operational process management. Innovation management. Management of labor and environmental regulation processes directly related to the business activity. |

| Learning and Growth | Corporate governance and management. Training and development plans and courses. Initiatives, improvements, proposals, etc. |

| Indicators | Financial | Stakeholders | Internal Processes | Learning and Growth | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Type | No. of Indicators | % | No. of Indicators | % | No. of Indicators | % | No. of Indicators | % | No. of Indicators | % |

| Currently being measured | 27 | 60.0 | 4 | 50.0 | 9 | 52.9 | 22 | 64.7 | 9 | 50.0 |

| Susceptible to measurement | 12 | 26.7 | 3 | 37.5 | 6 | 35.3 | 8 | 23.5 | 6 | 33.3 |

| Not applicable | 6 | 13.3 | 1 | 12.5 | 2 | 11.8 | 4 | 11.8 | 3 | 16.7 |

| TOTAL | 45 | 100 | 8 | 100 | 17 | 100 | 34 | 100 | 18 | 100 |

| Indicators | Financial | Stakeholders | Internal Processes | Learning and Growth | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Type | No. of Indicators | % | No. of Indicators | % | No. of Indicators | % | No. of Indicators | % | No. of Indicators | % |

| Currently being measured | 35 | 34.3 | 11 | 64.7 | 9 | 37.5 | 3 | 9.1 | 12 | 42.9 |

| Susceptible to measurement | 32 | 31.4 | 1 | 5.9 | 7 | 29.2 | 12 | 36.4 | 12 | 42.9 |

| Not applicable | 35 | 34.3 | 5 | 29.4 | 8 | 33.3 | 18 | 54.5 | 4 | 14.3 |

| TOTAL | 102 | 100 | 17 | 100 | 24 | 100 | 33 | 100 | 28 | 100 |

| Innovative Feature | Management Aspect | Creative Aspect | |||

|---|---|---|---|---|---|

| Level | Content | Activities to Build Capacity to Adapt to Opportunities or Threats | Implementation and Planning of Innovation Activities | Results and Feedback of Innovation Actions | Total Indicators by Level |

| 7 + 1 | R + D + i | Identification of Opportunities, Risks and Threats CR4, CR6, CR7, CR8, AQ3, AQ4, AQ5, AQ6, AQ7, AQ9, AQ12, AQ13, AQ14, TR2, TR6, TR10, TR11, AP2, AP4, AP6 | Management of Opportunities, Risks and Threats | Developments in progress | KM—20 |

| 7 | Social | Social presence | Partnership Management ES2.3, ES4.1, ES4.2, ES4.4, ES4.5, ES5.5 | Corporate Social Responsibility AP7 HR9, ES5.4, ES6.1, EN13, SO7 | KM—1 CSR—11 |

| 6 | Customers | Sales Development | Customer portfolio management CR11 PR5 | Marketing CR11 PR7, PR8, PR6 | KM—2 CSR—4 |

| 5 | Staff | Planning for people’s needs | HR Management CR3, CR6, AP2, AP7 EC5, EC7, LA1, LA2, LA4, LA6, LA9, LA12, LA13, LA14, HR8, ES2,1, ES2.2, ES3.5 | People’s satisfaction CR3, CR5, AP1, AP2 EC3, LA3, LA7, HR3, HR4, SO3, ES3.7, LA10, LA11, LA8 | KM—8 CSR—24 |

| 4 | Management | Delivery CR7 ES3,3, EN18, EN26 | Internal Management LA5, SO1, SO2, SO4, SO5, 4, 11, ES1.1, ES3.2, ES3.8 | Learning and improvement CR6 ES3.1, ES3.4 | KM—2 CSR—14 |

| 3 | Quality System | System AP4, AP5 EC2, EN6, EN7 | Improvement Management CR4, CR7, AP4, AP5 EN1, EN2, EN3, EN4, EN5, EN11, EN12, EN14, EN15, EN25, EN29 | Customer Satisfaction EN8, EN9, EN10, EN16, EN17, EN19, EN20, EN21, EN22, EN23, EN24, EN27 | KM—6 CSR—26 |

| 2 | Production and Services | Production planning | Management of productive resources AQ12, TR12, AP6 EC6, PR1, PR3, HR2, HR5, HR6, HR7 | Productivity TR12 PR2, PR4 | KM—4 CSR—9 |

| 1 | Resources and Assets | Investment Plan EC4 | Economic and financial management CR2, AP7 ES 5.2, EC8, EC9, EN30, HR1 | Economic Results CR9, AP1, AP2, AP6 EC1, EN28, SO6, SO8, PR9, 7.1, 7.2, 7.3 | KM—6 CSR—14 |

| Total indicators | KM—23 CSR—7 | KM—14 CSR—53 | KM—12 CSR—42 | KM—49 CSR—102 | |

| KM Process | Indicators | BSC Perspectives |

|---|---|---|

| Application of Knowledge | AP1: Evaluation of employee performance AP2: Evaluation of the effectiveness of the training carried out AP4: Evaluation of the proposals/idea applied by the employees AP6: Number of new products/services launched | Financial Stakeholders Internal Processes Learning and Growth |

| Knowledge Creation | CR3: Career plan CR4: Research and development sector CR5: Fortnightly conferences CR7: Brainstorming sessions to create new knowledge CR11: Customer relationship management | Stakeholders Learning and Growth |

| Acquisition of Knowledge | AQ1: Consultation with customers and suppliers AQ2: Use of computer system AQ3: Internal training AQ5: Searching for external training AQ7: Fortnightly lectures AQ8: Hiring new employees AQ9: Use of benchmarking AQ11: Use of the Internet to acquire knowledge AQ12: Access by the employee to the company’s knowledge repositories to acquire knowledge | Internal Processes |

| Transfer of Knowledge | TR1: Use of computer system or e-mail TR2: E-Learning training TR3: Participation in meetings TR4: Face-to-face training TR6: Participation of employees in informal discussions to share knowledge TR9: Internal informal discussions TR11: Participation in workshops TR12: Coding and storage of knowledge in the company’s knowledge repositories TR13: Updating of company knowledge repositories | Internal Processes |

| CSR Dimensions | Indicators | BSC Perspectives |

|---|---|---|

| Economic | EC1: Direct economic value generated and distributed, including revenues, employee compensation, retained earnings. EC3: Coverage of the organization’s obligations due to social benefit programmes. EC4: Financial aid received from governments. EC5: Range of ratios of standard entry level wage to local minimum wage. EC7: Procedures for local hiring and proportion of senior management. | Financial Stakeholders |

| Environmental | EN28: Cost of significant fines and number of non-monetary sanctions for non-compliance with environmental laws and regulations. EN30: Breakdown of total environmental expenditures and investments by type. EN3: Direct energy consumption by primary source. EN7: Initiatives to reduce indirect energy consumption. EN8: Total water withdrawal by source. | Financial Internal Processes |

| Social | EN28: Cost of significant fines and number of non-monetary sanctions for non-compliance with environmental laws and regulations. EN30: Breakdown of total environmental expenditures and investments by type. PR9: Cost of significant fines for non-compliance with regulations concerning supply. ES5.2: Existence of actions linked to socially responsible investments. ES7.1: Percentage of liabilities corresponding to collective or irrevocable funds. ES7.2: Percentage distribution of surplus to collective or irrevocable funds. ES7.3: Percentage of surplus allocated to members of the organization or to the incorporation of persons. LA1: Breakdown of the collective of workers by type of employment. LA2: Total number of employees and average turnover. LA4: Percentage of employees covered by a collective bargaining agreement. LA14: Ratio of basic salary of men to women. PR5: Practices related to customer satisfaction and survey results. PR8: Total number of complaints regarding respect for privacy and leakage of customer data. ES4.1: Definition of a map of stakeholders focused on the organization. ES5.5: Number and type of cooperation activities carried out with other organizations. LA10: Average hours of training per year per employee. LA11: Programs for skills management and continuous training. LA12: Percentage of employees who receive regular performance and professional development evaluations. LA13: Composition of corporate governance bodies and diversity indicators staff. ES1.1: Description of a report that highlights the primacy of people and the corporate purpose over capital. ES2.1: Requirements for new members to join the organization ES2.2: Requirements and conditions for leaving the organization. ES2.3: Evolution of partners or members, describing the variation of registrations and cancellations. ES3.3: Working groups or spaces generated that favour the organization’s decision-making. ES3.7: Average actual participation in the highest decision-making bodies. ES3.8: Description of the preparatory process for the maximum body of social representation. ES6.1: Description of a report detailing the requirements and limitations of the management sovereignty of the organization’s maximum decision-making bodies. | Financial Stakeholders Learning and Growth |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ferber Pineyrua, D.G.; Redondo, A.; Pascual, J.A.; Gento, Á.M. Knowledge Management and Sustainable Balanced Scorecard: Practical Application to a Service SME. Sustainability 2021, 13, 7118. https://doi.org/10.3390/su13137118

Ferber Pineyrua DG, Redondo A, Pascual JA, Gento ÁM. Knowledge Management and Sustainable Balanced Scorecard: Practical Application to a Service SME. Sustainability. 2021; 13(13):7118. https://doi.org/10.3390/su13137118

Chicago/Turabian StyleFerber Pineyrua, Diego G., Alfonso Redondo, José A. Pascual, and Ángel M. Gento. 2021. "Knowledge Management and Sustainable Balanced Scorecard: Practical Application to a Service SME" Sustainability 13, no. 13: 7118. https://doi.org/10.3390/su13137118

APA StyleFerber Pineyrua, D. G., Redondo, A., Pascual, J. A., & Gento, Á. M. (2021). Knowledge Management and Sustainable Balanced Scorecard: Practical Application to a Service SME. Sustainability, 13(13), 7118. https://doi.org/10.3390/su13137118