How CEO Political Connections Induce Corporate Social Irresponsibility: An Empirical Study of Tax Avoidance in South Korea

Abstract

:1. Introduction

2. Theory and Hypotheses

2.1. Corporate Social Irresponsibility and Tax Avoidance

2.2. CEO Political Connections and Tax Avoidance

2.3. The Moderating Role of CEO Tenure

3. Method

3.1. Data and Sample

3.2. Measures

3.2.1. Dependent Variable

- book-tax difference for firm i in year t; and

- total accruals for firm i in year t.

3.2.2. Independent Variable

3.2.3. Moderating Variable

3.2.4. Control Variables

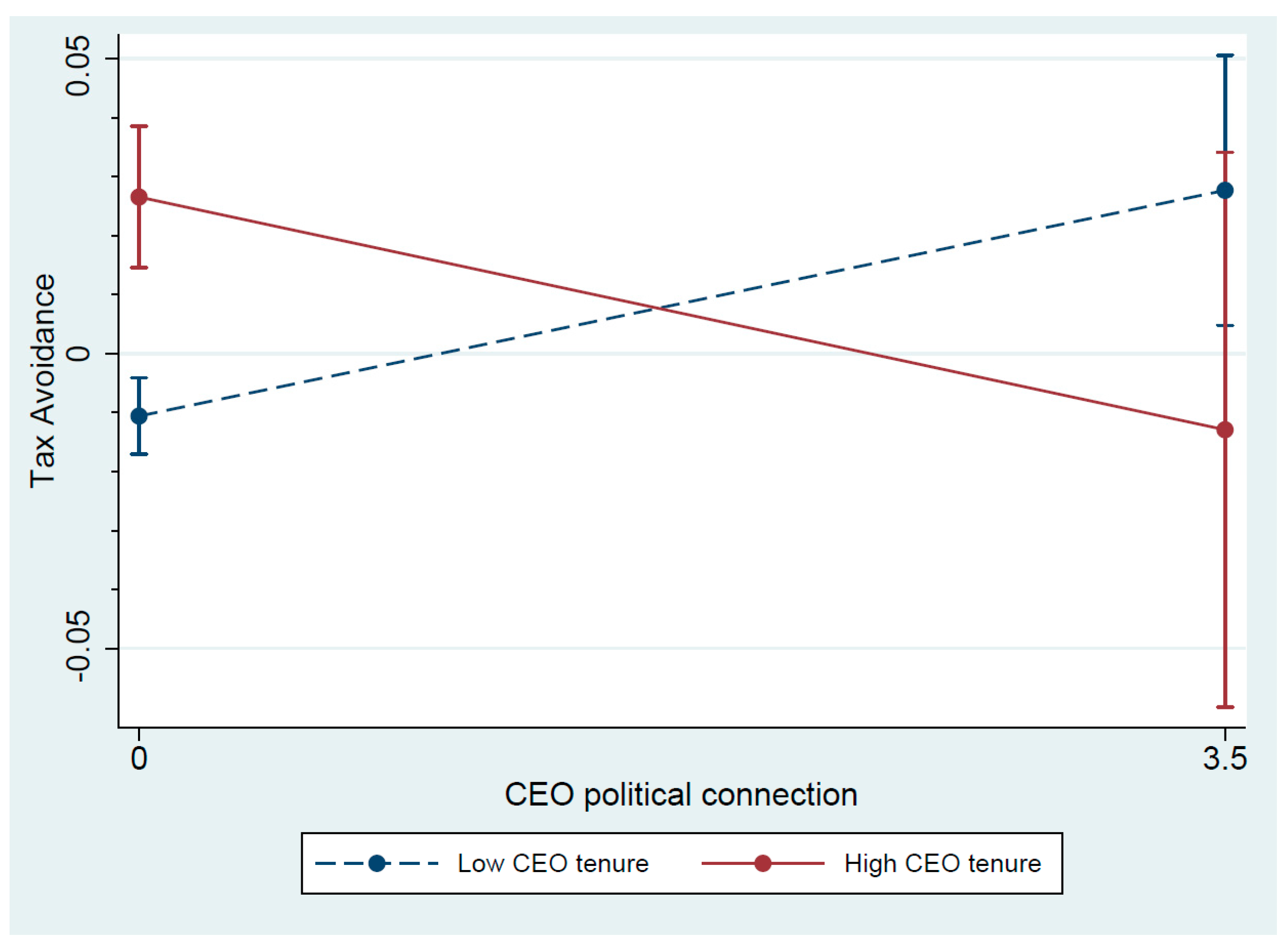

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Scholes, M.; Wolfson, M.; Erickson, M.; Maydew, E.; Shevlin, T. Taxes and Business Strategy: A Planning Approach, Pearson Prentice-Hall; Pearson Prentice-Hall: Upper Saddle River, NJ, USA, 2009. [Google Scholar]

- Mills, L.F.; Newberry, K.J. The influence of tax and nontax costs on book-tax reporting differences: Public and private firms. J. Am. Tax. Assoc. 2001, 23, 1–19. [Google Scholar] [CrossRef]

- Phillips, J.; Pincus, M.; Rego, S.O. Earnings management: New evidence based on deferred tax expense. Account. Rev. 2003, 78, 491–521. [Google Scholar] [CrossRef]

- Hanlon, M. The persistence and pricing of earnings, accruals, and cash flows when firms have large book-tax differences. Account. Rev. 2005, 80, 137–166. [Google Scholar] [CrossRef]

- Hanlon, M.; Heitzman, S. A review of tax research. J. Account. Econ. 2010, 50, 127–178. [Google Scholar] [CrossRef] [Green Version]

- Dyreng, S.D.; Lindsey, B.P. Using financial accounting data to examine the effect of foreign operations located in tax havens and other countries on US multinational firms’ tax rates. J. Account. Res. 2009, 47, 1283–1316. [Google Scholar] [CrossRef]

- Graham, J.R.; Tucker, A.L. Tax shelters and corporate debt policy. J. Financ. Econ. 2006, 81, 563–594. [Google Scholar] [CrossRef]

- Lisowsky, P. Seeking shelter: Empirically modeling tax shelters using financial statement information. Account. Rev. 2010, 85, 1693–1720. [Google Scholar] [CrossRef]

- Rego, S.O.; Wilson, R. Equity risk incentives and corporate tax aggressiveness. J. Account. Res. 2012, 50, 775–810. [Google Scholar] [CrossRef]

- Gaertner, F.B. CEO After-Tax compensation incentives and corporate tax avoidance. Contemp. Account. Res. 2014, 31, 1077–1102. [Google Scholar] [CrossRef] [Green Version]

- Armstrong, C.S.; Blouin, J.L.; Jagolinzer, A.D.; Larcker, D.F. Corporate governance, incentives, and tax avoidance. J. Account. Econ. 2015, 60, 1–17. [Google Scholar] [CrossRef] [Green Version]

- Dyreng, S.D.; Hanlon, M.; Maydew, E.L. The effects of executives on corporate tax avoidance. Account. Rev. 2010, 85, 1163–1189. [Google Scholar] [CrossRef]

- Christensen, D.M.; Dhaliwal, D.S.; Boivie, S.; Graffin, S.D. Top management conservatism and corporate risk strategies: Evidence from managers’ personal political orientation and corporate tax avoidance. Strateg. Manag. J. 2015, 36, 1918–1938. [Google Scholar] [CrossRef] [Green Version]

- Francis, B.B.; Hasan, I.; Sun, X.; Wu, Q. CEO political preference and corporate tax sheltering. J. Corp. Financ. 2016, 38, 37–53. [Google Scholar] [CrossRef] [Green Version]

- Faccio, M. Politically connected firms. Am. Econ. Rev. 2006, 96, 369–386. [Google Scholar] [CrossRef] [Green Version]

- Fisman, R. Estimating the value of political connections. Am. Econ. Rev. 2001, 91, 1095–1102. [Google Scholar] [CrossRef] [Green Version]

- Johnson, S.; Mitton, T. Cronyism and capital controls: Evidence from Malaysia. J. Financ. Econ. 2003, 67, 351–382. [Google Scholar] [CrossRef] [Green Version]

- Ma, C.; Yang, J.; Chen, L.; You, X.; Zhang, W.; Chen, Y. Entrepreneurs’ social networks and opportunity identification: Entrepreneurial passion and entrepreneurial alertness as moderators. Soc. Behav. Personal. Int. J. 2020, 48, 1–12. [Google Scholar] [CrossRef]

- Hadani, M.; Schuler, D.A. In search of El Dorado: The elusive financial returns on corporate political investments. Strateg. Manag. J. 2013, 34, 165–181. [Google Scholar] [CrossRef]

- Leuz, C.; Oberholzer-Gee, F. Political relationships, global financing, and corporate transparency: Evidence from Indonesia. J. Financ. Econ. 2006, 81, 411–439. [Google Scholar] [CrossRef]

- Chaney, P.K.; Faccio, M.; Parsley, D. The quality of accounting information in politically connected firms. J. Account. Econ. 2011, 51, 58–76. [Google Scholar] [CrossRef] [Green Version]

- Marquis, C.; Qian, C. Corporate social responsibility reporting in China: Symbol or substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef] [Green Version]

- Zhang, J.; Marquis, C.; Qiao, K. Do political connections buffer firms from or bind firms to the government? A study of corporate charitable donations of Chinese firms. Organ. Sci. 2016, 27, 1307–1324. [Google Scholar] [CrossRef]

- Kölbel, J.F.; Busch, T.; Jancso, L.M. How media coverage of corporate social irresponsibility increases financial risk. Strateg. Manag. J. 2017, 38, 2266–2284. [Google Scholar] [CrossRef]

- Brown, J.L.; Drake, K.; Wellman, L. The benefits of a relational approach to corporate political activity: Evidence from political contributions to tax policymakers. J. Am. Tax. Assoc. 2015, 37, 69–102. [Google Scholar] [CrossRef]

- Mills, L.F.; Nutter, S.E.; Schwab, C.M. The effect of political sensitivity and bargaining power on taxes: Evidence from federal contractors. Account. Rev. 2013, 88, 977–1005. [Google Scholar] [CrossRef]

- Richter, B.K.; Samphantharak, K.; Timmons, J.F. Lobbying and taxes. Am. J. Political Sci. 2009, 53, 893–909. [Google Scholar] [CrossRef]

- Vurro, C.; Dacin, M.T.; Perrini, F. Institutional antecedents of partnering for social change: How institutional logics shape cross-sector social partnerships. J. Bus. Ethics 2010, 94, 39–53. [Google Scholar] [CrossRef]

- Dharwadkar, R.; Guo, J.; Shi, L.; Yang, R. Corporate social irresponsibility and boards: The implications of legal expertise. J. Bus. Res. 2021, 125, 143–154. [Google Scholar] [CrossRef]

- Rose, J.M. Corporate directors and social responsibility: Ethics versus shareholder value. J. Bus. Ethics 2007, 73, 319–331. [Google Scholar] [CrossRef]

- Kim, C.; Zhang, L. Corporate political connections and tax aggressiveness. Contemp. Account. Res. 2016, 33, 78–114. [Google Scholar] [CrossRef]

- Yiu, D.W.; Xu, Y.; Wan, W.P. The deterrence effects of vicarious punishments on corporate financial fraud. Organ. Sci. 2014, 25, 1549–1571. [Google Scholar] [CrossRef]

- Karpoff, J.M.; Lee, D.S.; Martin, G.S. The consequences to managers for cooking the books. J. Financ. Econ. 2008, 88, 193–215. [Google Scholar] [CrossRef]

- Strachan, J.L.; Smith, D.B.; Beedles, W.L. The price reaction to (alleged) corporate crime. Financ. Rev. 1983, 18, 121–132. [Google Scholar] [CrossRef]

- Guenther, D.A.; Matsunaga, S.R.; Williams, B.M. Is tax avoidance related to firm risk? Account. Rev. 2016, 92, 115–136. [Google Scholar] [CrossRef]

- Wilson, R.J. An examination of corporate tax shelter participants. Account. Rev. 2009, 84, 969–999. [Google Scholar] [CrossRef]

- Sikka, P. Smoke and mirrors: Corporate social responsibility and tax avoidance. Account. Forum 2010, 34, 153–168. [Google Scholar] [CrossRef]

- Efendi, J.; Srivastava, A.; Swanson, E.P. Why do corporate managers misstate financial statements? The role of option compensation and other factors. J. Financ. Econ. 2007, 85, 667–708. [Google Scholar] [CrossRef]

- Firth, M.; Rui, O.M.; Wu, W. Cooking the books: Recipes and costs of falsified financial statements in China. J. Corp. Financ. 2011, 17, 371–390. [Google Scholar] [CrossRef]

- Graham, J.R.; Li, S.; Qiu, J. Corporate misreporting and bank loan contracting. J. Financ. Econ. 2008, 89, 44–61. [Google Scholar] [CrossRef] [Green Version]

- Christensen, J.; Murphy, R. The social irresponsibility of corporate tax avoidance: Taking CSR to the bottom line. Development 2004, 47, 37–44. [Google Scholar] [CrossRef]

- Hoi, C.K.; Wu, Q.; Zhang, H. Is corporate social responsibility (CSR) associated with tax avoidance? Evidence from irresponsible CSR activities. Account. Rev. 2013, 88, 2025–2059. [Google Scholar] [CrossRef]

- Lanis, R.; Richardson, G. The effect of board of director composition on corporate tax aggressiveness. J. Account. Public Policy 2011, 30, 50–70. [Google Scholar] [CrossRef]

- Fich, E.M.; Shivdasani, A. Financial fraud, director reputation, and shareholder wealth. J. Financ. Econ. 2007, 86, 306–336. [Google Scholar] [CrossRef]

- Werner, T. Gaining access by doing good: The effect of sociopolitical reputation on firm participation in public policy making. Manag. Sci. 2015, 61, 1989–2011. [Google Scholar] [CrossRef]

- Duchin, R.; Sosyura, D. The politics of government investment. J. Financ. Econ. 2012, 106, 24–48. [Google Scholar] [CrossRef]

- Wayne, L. How Delaware Thrives as a Corporate Tax Haven. New York Times, 30 June 2012. [Google Scholar]

- Adhikari, A.; Derashid, C.; Zhang, H. Public policy, political connections, and effective tax rates: Longitudinal evidence from Malaysia. J. Account. Public Policy 2006, 25, 574–595. [Google Scholar] [CrossRef]

- Wu, S.; Levitas, E.; Priem, R.L. CEO tenure and company invention under differing levels of technological dynamism. Acad. Manag. J. 2005, 48, 859–873. [Google Scholar] [CrossRef]

- Bertrand, M.; Schoar, A. Managing with style: The effect of managers on firm policies. Q. J. Econ. 2003, 118, 1169–1208. [Google Scholar] [CrossRef] [Green Version]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Castanias, R.P.; Helfat, C.E. Managerial resources and rents. J. Manag. 1991, 17, 155–171. [Google Scholar] [CrossRef]

- Penrose, E.; Penrose, E.T. The Theory of the Growth of the Firm; Oxford University Press: Oxford, UK; Blackwell: Oxford, UK, 2009. [Google Scholar]

- Bamber, L.S.; Jiang, J.; Wang, I.Y. What’s my style? The influence of top managers on voluntary corporate financial disclosure. Account. Rev. 2010, 85, 1131–1162. [Google Scholar] [CrossRef]

- Dejong, D.; Ling, Z. Managers: Their effects on accruals and firm policies. J. Bus. Financ. Account. 2013, 40, 82–114. [Google Scholar] [CrossRef]

- Barker III, V.L.; Mueller, G.C. CEO characteristics and firm R&D spending. Manag. Sci. 2002, 48, 782–801. [Google Scholar]

- Hambrick, D.C.; Fukutomi, G.D. The seasons of a CEO’s tenure. Acad. Manag. Rev. 1991, 16, 719–742. [Google Scholar] [CrossRef]

- Simsek, Z. CEO tenure and organizational performance: An intervening model. Strateg. Manag. J. 2007, 28, 653–662. [Google Scholar] [CrossRef]

- Kim, Y.; Cannella Jr, A.A. Social capital among corporate upper echelons and its impacts on executive promotion in Korea. J. World Bus. 2008, 43, 85–96. [Google Scholar] [CrossRef]

- Yonhap News Person Information. Available online: http://sales.yonhapnews.co.kr/YNA/ContentsSales/ContentsData/YISW_PeopleHome.aspx (accessed on 12 December 2020).

- Chosun Profile. Available online: http://db.chosun.com/people (accessed on 20 December 2020).

- Joins People. Available online: http://people.joins.com (accessed on 22 December 2020).

- National Assembly. Available online: http://www.assembly.go.kr (accessed on 23 January 2021).

- Office of the President. Available online: http://www.president.go.kr (accessed on 4 January 2021).

- Naver Peope Serch. Available online: http://people.search.naver.com (accessed on 4 January 2021).

- Desai, M.A.; Dharmapala, D. Corporate tax avoidance and high-powered incentives. J. Financ. Econ. 2006, 79, 145–179. [Google Scholar] [CrossRef] [Green Version]

- Hribar, P.; Collins, D.W. Errors in estimating accruals: Implications for empirical research. J. Account. Res. 2002, 40, 105–134. [Google Scholar] [CrossRef]

- Zhu, H.; Chung, C.-N. Portfolios of political ties and business group strategy in emerging economies: Evidence from Taiwan. Adm. Sci. Q. 2014, 59, 599–638. [Google Scholar] [CrossRef]

- Siegel, J. Contingent political capital and international alliances: Evidence from South Korea. Adm. Sci. Q. 2007, 52, 621–666. [Google Scholar] [CrossRef] [Green Version]

- Wu, W.; Wu, C.; Zhou, C.; Wu, J. Political connections, tax benefits and firm performance: Evidence from China. J. Account. Public Policy 2012, 31, 277–300. [Google Scholar] [CrossRef]

- Chen, S.; Chen, X.; Cheng, Q.; Shevlin, T. Are family firms more tax aggressive than non-family firms? J. Financ. Econ. 2010, 95, 41–61. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Mean | S.D. | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Tax avoidance behavior | 0.006 | 0.061 | 1 | ||||||||

| 2 | ROA | 0.078 | 0.070 | 0.198 * | 1 | |||||||

| 3 | Firm size | 19.551 | 1.602 | 0.004 | 0.126 * | 1 | ||||||

| 4 | Advertising intensity | 0.137 | 0.163 | −0.004 | 0.156 * | 0.086 * | 1 | |||||

| 5 | PPE | 0.01 | 0.044 | −0.020 | 0.011 | 0.095 * | 0.089 * | 1 | ||||

| 6 | Leverage ratio | 0.129 | 0.114 | −0.039 * | −0.138 * | 0.317 * | −0.048 * | 0.085 * | 1 | |||

| 7 | R&D intensity | 0.006 | 0.014 | 0.014 | 0.101 * | 0.109 * | 0.168 * | −0.022 | −0.020 | 1 | ||

| 8 | Net operating loss | 0.073 | 0.261 | 0.087 * | −0.037 * | −0.016 | −0.004 | −0.017 | 0.085 * | 0.001 | 1 | |

| 9 | Net operating loss dummy | 0.021 | 0.123 | −0.016 | −0.004 | −0.015 | 0.008 | −0.010 | −0.015 | 0.018 | −0.136 * | 1 |

| 10 | Market-to-Book ratio | 1.171 | 1.265 | 0.104 * | 0.388 * | 0.226 * | 0.205 * | 0.034 * | 0.073 * | 0.163 * | 0.072 * | −0.002 |

| 11 | Intangible assets | 0.015 | 0.038 | 0.039 * | −0.017 | 0.095 * | 0.178 * | 0.049 * | 0.095 * | 0.116 * | 0.036 * | 0.017 |

| 12 | CEO’s educational background | 0.500 | 0.500 | −0.027 | −0.048 * | 0.064 * | −0.027 | 0.028 | 0.109 * | −0.094 * | 0.018 | 0.001 |

| 13 | Board size | 6.959 | 2.204 | −0.005 | 0.098 * | 0.384 * | 0.043 * | 0.039 * | 0.131 * | 0.040 * | −0.004 | −0.034 * |

| 14 | Outside director ratio | 0.312 | 0.144 | 0.004 | 0.018 | 0.535 * | 0.059 * | 0.010 | 0.223 * | 0.082 * | 0.044 * | −0.028 * |

| 15 | CEO’s politician career | 0.092 | 0.289 | 0.011 | 0.036 * | 0.072 * | 0.026 | 0.017 | 0.046 * | −0.033 * | −0.001 | −0.006 |

| 16 | Outside directors’ politician career | 0.607 | 0.488 | −0.016 | 0.052 * | 0.273 * | 0.032 * | 0.036 * | 0.123 * | 0.022 | 0.004 | −0.044 * |

| 17 | CEO political connections | 0.539 | 0.582 | 0.001 | 0.013 | 0.209 * | −0.025 | −0.026 | 0.101 * | 0.072 * | 0.001 | −0.005 |

| 18 | CEO tenure | 1.891 | 0.805 | 0.018 | −0.056 * | −0.165 * | −0.054 * | −0.037 * | −0.092 * | 0.055 * | −0.041 * | −0.011 |

| Variables | Mean | S.D. | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | |

| 10 | Market-to-Book ratio | 1.171 | 1.265 | 1 | ||||||||

| 11 | Intangible assets | 0.015 | 0.038 | 0.131 * | 1 | |||||||

| 12 | CEO’s educational background | 0.500 | 0.500 | −0.024 | −0.046 * | 1 | ||||||

| 13 | Board size | 6.959 | 2.204 | 0.140 * | 0.009 | 0.102 * | 1 | |||||

| 14 | Outside director ratio | 0.312 | 0.144 | 0.195 * | 0.105 * | 0.057 * | 0.266 * | 1 | ||||

| 15 | CEO’s politician career | 0.092 | 0.289 | 0.029 * | 0.023 | 0.071 * | 0.080 * | 0.037 * | 1 | |||

| 16 | Outside directors’ politician career | 0.607 | 0.488 | 0.110 * | 0.028 * | 0.082 * | 0.235 * | 0.360 * | 0.035 * | 1 | ||

| 17 | CEO political connections | 0.539 | 0.582 | 0.068 * | −0.020 | −0.018 | 0.174 * | 0.206 * | −0.150 * | −0.134 * | 1 | |

| 18 | CEO tenure | 1.891 | 0.805 | −0.113 * | −0.095 * | 0.067 * | −0.010 | −0.128 * | 0.093 * | −0.063 * | 0.009 | 1 |

| Variables | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| ROA | 0.296 *** | 0.295 *** | 0.296 *** |

| (0.017) | (0.017) | (0.017) | |

| Total assets | 0.002 | 0.003 * | 0.002 |

| (0.001) | (0.001) | (0.001) | |

| Advertising intensity | 0.039 *** | 0.037 ** | 0.036 ** |

| (0.015) | (0.015) | (0.015) | |

| PPE | 0.036 | 0.036 | 0.035 |

| (0.030) | (0.030) | (0.030) | |

| Leverage ratio | −0.080 *** | −0.078 *** | −0.078 *** |

| (0.011) | (0.011) | (0.011) | |

| R&D intensity | 0.0963 | 0.140 | 0.155 |

| (0.152) | (0.153) | (0.153) | |

| Change in net operating loss | 0.006 | 0.006 * | 0.006 * |

| (0.003) | (0.003) | (0.003) | |

| Net operating loss dummy | 0.011 | 0.013 | 0.013 |

| (0.009) | (0.009) | (0.009) | |

| Market-to-Book ratio | 0.001 | 0.001 | 0.001 |

| (0.001) | (0.001) | (0.001) | |

| Intangible assets | −0.031 | −0.027 | −0.027 |

| (0.042) | (0.041) | (0.041) | |

| CEO’s educational background | −0.001 | −0.001 | −0.001 |

| (0.003) | (0.003) | (0.003) | |

| Board size | 0.001 | 0.001 | 0.001 |

| (0.001) | (0.001) | (0.001) | |

| Outside director ratio | −0.001 | 0.001 | 0.001 |

| (0.012) | (0.012) | (0.012) | |

| CEO’s politician career | −0.004 | −0.008 | −0.008 |

| (0.006) | (0.006) | (0.006) | |

| Outside directors’ politician career | −0.002 | −0.002 | −0.002 |

| (0.002) | (0.002) | (0.002) | |

| CEO political connections | 0.005 ** | 0.008 *** | |

| (0.002) | (0.003) | ||

| CEO tenure | 0.001 *** | ||

| (0.001) | |||

| CPC × CEO tenure | −0.006 ** | ||

| (0.001) | |||

| Firm fixed | Yes | Yes | Yes |

| Year fixed | Yes | Yes | Yes |

| Constant | −0.298 *** | −0.301 *** | −0.296 *** |

| (0.054) | (0.054) | (0.054) | |

| Observations | 4706 | 4706 | 4706 |

| R2 | 0.252 | 0.258 | 0.266 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kim, J.-H.; Lee, J.-H. How CEO Political Connections Induce Corporate Social Irresponsibility: An Empirical Study of Tax Avoidance in South Korea. Sustainability 2021, 13, 7739. https://doi.org/10.3390/su13147739

Kim J-H, Lee J-H. How CEO Political Connections Induce Corporate Social Irresponsibility: An Empirical Study of Tax Avoidance in South Korea. Sustainability. 2021; 13(14):7739. https://doi.org/10.3390/su13147739

Chicago/Turabian StyleKim, Ji-Hee, and Ji-Hwan Lee. 2021. "How CEO Political Connections Induce Corporate Social Irresponsibility: An Empirical Study of Tax Avoidance in South Korea" Sustainability 13, no. 14: 7739. https://doi.org/10.3390/su13147739

APA StyleKim, J.-H., & Lee, J.-H. (2021). How CEO Political Connections Induce Corporate Social Irresponsibility: An Empirical Study of Tax Avoidance in South Korea. Sustainability, 13(14), 7739. https://doi.org/10.3390/su13147739