Sustainable Development of a Mobile Payment Security Environment Using Fintech Solutions

Abstract

:1. Introduction

2. Literature Review

2.1. Fintech-Enabled Mobile Payment Services

2.2. Mobile Payment Service (MPS) Success Determinants

2.3. Security of Mobile Payment Services

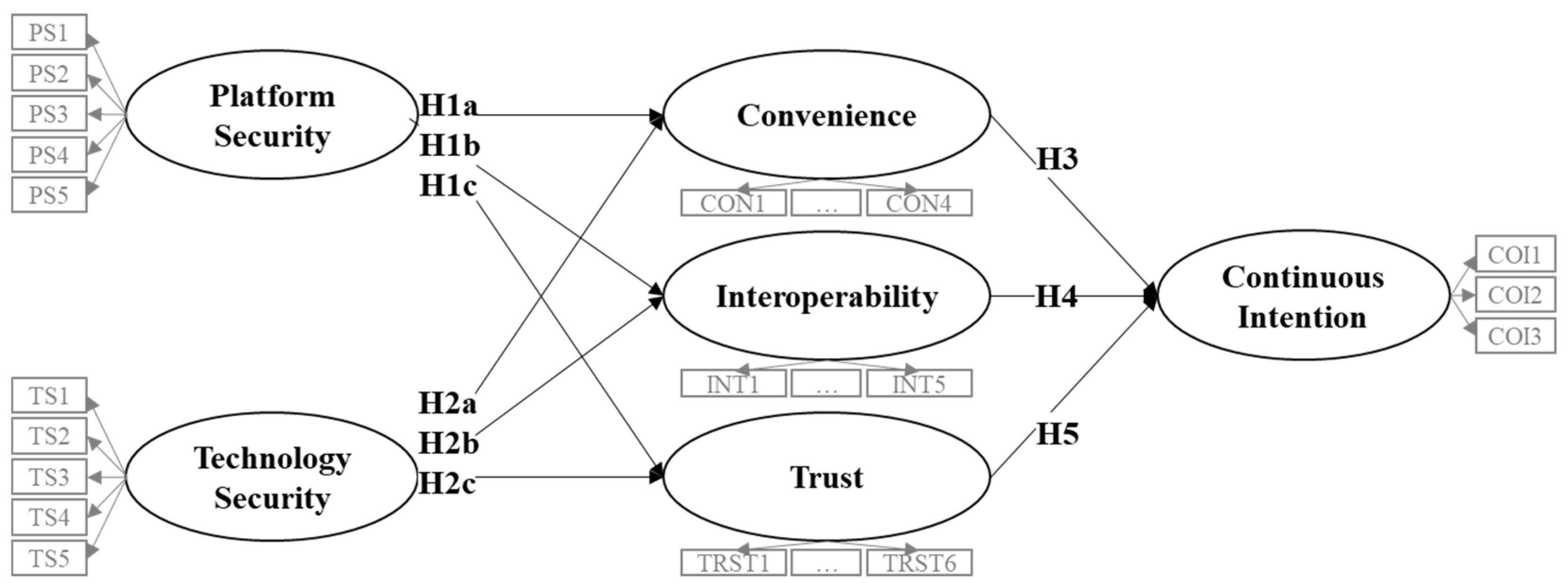

3. Hypotheses Development

3.1. Platform and Technology Securities and MPS Success Determinants

3.2. MPS Success Determinants and Continuous Usage Intention

4. Research Design and Analyses

4.1. Instrument Development

4.2. Measurement Model Analysis

4.3. Structural Equation Model Analysis

5. Conclusion and Discussions

5.1. Theoretical Insights

5.2. Managerial Insight

5.3. Sustainable Management Inspiration

5.4. Future Research Avenues

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Ghezzi, A.; Renga, F.; Balocco, R.; Pescetto, P. Mobile payment applications: Offer state of the art in the Italian market. Info 2010, 12, 3–22. [Google Scholar] [CrossRef]

- Choi, H.; Park, J.; Kim, J.; Jung, Y. Consumer preferences of attributes of mobile payment services in South Korea. Telemat. Inform. 2020, 51, 101397. [Google Scholar] [CrossRef]

- Kim, C.; Mirusmonov, M.; Lee, I. An empirical examination of factors influencing the intention to use mobile payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Intelligence, M. Mobile Payments Market-Growth, Trends, COVID-19 Impact, and Forecasts (2021–2026). Available online: https://www.mordorintelligence.com/industry-reports/mobile-payment-market (accessed on 20 May 2021).

- Lim, S.H.; Kim, D.J.; Hur, Y.; Park, K. An Empirical Study of the Impacts of Perceived Security and Knowledge on Continuous Intention to Use Mobile Fintech Payment Services. Int. J. Hum. Comput. Interact. 2019, 35, 886–898. [Google Scholar] [CrossRef]

- Tounekti, O.; Ruiz-martínez, A.; Skarmeta-gómez, A.F. Users’ evaluation of a new web browser payment interface for facilitating the use of multiple payment systems. Sustainability 2021, 13, 4711. [Google Scholar] [CrossRef]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User Acceptance of Computer Technology: A Comparison of Two Theoretical Models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Davis, F.D. Theoretical extension of the Technology Acceptance Model: Four longitudinal field studies. Manag. Sci. 2000, 46, 186–204. [Google Scholar] [CrossRef] [Green Version]

- Indiani, N.L.P.; Fahik, G.A. Conversion of online purchase intention into actual purchase: The moderating role of transaction security and convenience. Bus. Theory Pract. 2020, 21, 18–29. [Google Scholar] [CrossRef]

- Williams, M.D. Social commerce and the mobile platform: Payment and security perceptions of potential users. Comput. Hum. Behav. 2018, 1–12. [Google Scholar] [CrossRef] [Green Version]

- Wu, D.; Moody, G.D.; Zhang, J.; Lowry, P.B. Effects of the design of mobile security notifications and mobile app usability on users’ security perceptions and continued use intention. Inf. Manag. 2020, 57, 103235. [Google Scholar] [CrossRef]

- Hossain, M.A. Security perception in the adoption of mobile payment and the moderating effect of gender. PSU Res. Rev. 2019, 3, 179–190. [Google Scholar] [CrossRef] [Green Version]

- Lai, P.C. Design and Security impact on consumers’ intention to use single platform E-payment. Interdiscip. Inf. Sci. 2016, 22, 111–122. [Google Scholar] [CrossRef] [Green Version]

- Kim, B.C.; Park, Y.W. Security versus convenience? An experimental study of user misperceptions of wireless internet service quality. Decis. Support. Syst. 2012, 53, 1–11. [Google Scholar] [CrossRef]

- Mačiulienė, M.; Skaržauskienė, A. Building the capacities of civic tech communities through digital data analytics. J. Innov. Knowl. 2020, 5, 244–250. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; García-Maroto, I.; Muñoz-Leiva, F.; Ramos-de-Luna, I. Mobile payment adoption in the age of digital transformation: The case of apple pay. Sustainability 2020, 12, 5443. [Google Scholar] [CrossRef]

- Lakshmi, V.; Bahli, B. Understanding the robotization landscape transformation: A centering resonance analysis. J. Innov. Knowl. 2020, 5, 59–67. [Google Scholar] [CrossRef]

- Tiberius, V.; Schwarzer, H.; Roig-Dobón, S. Radical innovations: Between established knowledge and future research opportunities. J. Innov. Knowl. 2021, 6, 145–153. [Google Scholar] [CrossRef]

- Fosso Wamba, S.; Kala Kamdjoug, J.R.; Epie Bawack, R.; Keogh, J.G. Bitcoin, Blockchain and Fintech: A systematic review and case studies in the supply chain. Prod. Plan. Control. 2020, 31, 115–142. [Google Scholar] [CrossRef]

- Aslam, J.; Saleem, A.; Khan, N.T.; Kim, Y.B. Factors influencing blockchain adoption in supply chain management practices: A study based on the oil industry. J. Innov. Knowl. 2021, 6, 124–134. [Google Scholar] [CrossRef]

- Kang, J. Mobile payment in Fintech environment: Trends, security challenges, and services. Hum. Cent. Comput. Inf. Sci. 2018, 8. [Google Scholar] [CrossRef] [Green Version]

- Lim, S.; Hur, Y. An empirical study on the impact of the perceived securities and trust to diffusion of IoT-based smart banking services-focusing on university students. Insur. Financ. Rev. 2017, 28, 37–65. [Google Scholar]

- Nan, D.; Kim, Y.; Park, M.H.; Kim, J.H. What motivates users to keep using social mobile payments? Sustainability 2020, 12, 6878. [Google Scholar] [CrossRef]

- Choi, S. The Evolving Simple Payment Market, the Financial Industry Is Now at War with OO Pay. Available online: https://www.sktinsight.com/122067 (accessed on 24 June 2021).

- Brown, L.G. Convenience in Services Marketing Convenience: A Topic for the Convenience: A Conceptual. J. Serv. Mark. 1990, 4, 53–59. [Google Scholar] [CrossRef]

- Yoon, C.; Kim, S. Convenience and TAM in a ubiquitous computing environment: The case of wireless LAN. Electron. Commer. Res. Appl. 2007, 6, 102–112. [Google Scholar] [CrossRef]

- Chen, Y.L.; Wu, W.-N. An Exploration of the Factors Affecting User’s Satisfaction with Mobile Payments. Int. J. Comput. Sci. Inf. Technol. 2017, 9, 97–105. [Google Scholar] [CrossRef]

- Berry, L.L.; Seiders, K.; Grewal, D. Understanding service convenience. J. Mark. 2002, 66, 1–17. [Google Scholar] [CrossRef]

- Pousttchi, K. Conditions for Acceptance and Usage of Mobile Payment Procedures. In Proceedings of the 6th Annual Global Mobility Round Table, Los Angeles, CA, USA, 1 June 2007. [Google Scholar]

- Park, J.K.; Ahn, J.; Thavisay, T.; Ren, T. Examining the role of anxiety and social influence in multi-benefits of mobile payment service. J. Retail. Consum. Serv. 2019, 47, 140–149. [Google Scholar] [CrossRef]

- Jun, J.; Cho, I.; Park, H. Factors influencing continued use of mobile easy payment service: An empirical investigation. Total Qual. Manag. Bus. Excell. 2018, 29, 1043–1057. [Google Scholar] [CrossRef]

- Bonomi, F. The future mobile infrastructure: Challenges and opportunities. IEEE Wirel. Commun. 2010, 17, 4–5. [Google Scholar] [CrossRef]

- Dahlberg, T.; Mallat, N.; Ondrus, J.; Zmijewska, A. Past, present and future of mobile payments research: A literature review. Electron. Commer. Res. Appl. 2008, 7, 165–181. [Google Scholar] [CrossRef] [Green Version]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Kim, M.; Kim, S.; Kim, J. Can mobile and biometric payments replace cards in the Korean offline payments market? Consumer preference analysis for payment systems using a discrete choice model. Telemat. Inform. 2019, 38, 46–58. [Google Scholar] [CrossRef]

- Iman, N. Is mobile payment still relevant in the fintech era? Electron. Commer. Res. Appl. 2018, 30, 72–82. [Google Scholar] [CrossRef]

- Kazan, E.; Tan, C.W.; Lim, E.T.K. Towards a framework of digital platform competition: A comparative study of monopolistic & federated mobile payment platforms. J. Theor. Appl. Electron. Commer. Res. 2016, 11, 50–64. [Google Scholar] [CrossRef] [Green Version]

- Oh, J.; Kim, W. The Effects of Mobile Payment System on Consumer Attitude and Behavioral Intention. J. Internet Electron. Commer. Res. 2020, 20, 35–50. [Google Scholar] [CrossRef]

- Fan, J.; Shao, M.; Li, Y.; Huang, X. Understanding users’ attitude toward mobile payment use: A comparative study between China and The U.S. Ind. Manag. Data Syst. 2018, 118, 524–540. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; de Luna, I.R.; Montoro-Ríosa, F. Intention to use new mobile payment systems: A comparative analysis of SMS and NFC payments. Econ. Res. Istraz. 2017, 30, 892–910. [Google Scholar] [CrossRef]

- Shin, D.H. Towards an understanding of the consumer acceptance of mobile wallet. Comput. Hum. Behav. 2009, 25, 1343–1354. [Google Scholar] [CrossRef]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Commer. Res. Appl. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Bailey, A.A.; Pentina, I.; Mishra, A.S.; Ben Mimoun, M.S. Mobile payments adoption by US consumers: An extended TAM. Int. J. Retail. Distrib. Manag. 2017, 45, 626–640. [Google Scholar] [CrossRef]

- Yang, K.; Forney, J.C. The moderating role of consumer technology anxiety in mobile shopping adoption: Differential effects of facilitating conditions and social influences. J. Electron. Commer. Res. 2013, 14, 334–347. [Google Scholar]

- Sharma, S.K.; Sharma, H.; Dwivedi, Y.K. A Hybrid SEM-Neural Network Model for Predicting Determinants of Mobile Payment Services. Inf. Syst. Manag. 2019, 36, 243–261. [Google Scholar] [CrossRef]

- Lee, J. A literature review on security for internet of things in Korea based on IoT S-P-N-D-Se ecosystem model. J. Secur. Eng. 2015, 12, 397–414. [Google Scholar]

- Huang, M.; Zhao, Y.; Zhu, L. Research for e-commerce platform security framework based on SOA. In Proceedings of the 2011 4th International Conference on Biomedical Engineering and Informatics (BMEI), Shanghai, China, 15–17 October 2011. [Google Scholar] [CrossRef]

- Zhang, J.; Luximon, Y. A quantitative diary study of perceptions of security in mobile payment transactions. Behav. Inf. Technol. 2020, 1–24. [Google Scholar] [CrossRef]

- Mala Nabi, R.; Mohammed, R.A.; Mala Nabi, R. Smartphones Platform Security a Comparison Study. Int. J. 2015, 5, 4–9. [Google Scholar]

- Lee, S.H.; Huang, K.W.; Yang, C.S. TBAS: Token-based authorization service architecture in Internet of things scenarios. Int. J. Distrib. Sens. Netw. 2017, 13. [Google Scholar] [CrossRef]

- Salisbury, W.D.; Pearson, R.A.; Pearson, A.W.; Miller, D.W. Perceived security and World Wide Web purchase intention. Ind. Manag. Data Syst. 2001, 101, 165–177. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Muñoz-Leiva, F.; Sánchez-Fernández, J. A global approach to the analysis of user behavior in mobile payment systems in the new electronic environment. Serv. Bus. 2018, 12, 25–64. [Google Scholar] [CrossRef]

- Butler, S.A. Security attribute evaluation method: A cost-benefit approach. Proc. Int. Conf. Softw. Eng. 2002, 232–240. [Google Scholar] [CrossRef]

- Mu, H.-L.; Lee, Y.-C. Examining the Influencing Factors of Third-Party Mobile Payment Adoption: A Comparative Study of Alipay and WeChat Pay. J. Inf. Syst. 2017, 26, 247–284. [Google Scholar] [CrossRef]

- Arcand, M.; PromTep, S.; Brun, I.; Rajaobelina, L. Mobile banking service quality and customer relationships. Int. J. Bank Mark. 2017, 35, 1066–1087. [Google Scholar] [CrossRef]

- Yu, L.; Cao, X.; Liu, Z.; Gong, M.; Adee, L. Understanding mobile payment users’ continuance intention: A trust transfer perspective Article information: About Emerald www.emeraldinsight.com Understanding mobile payment users’ continuance intention: A trust transfer perspective. Internet Res. 2018, 28, 456–476. [Google Scholar]

- Liébana-Cabanillas, F.; Marinkovic, V.; Ramos de Luna, I.; Kalinic, Z. Predicting the determinants of mobile payment acceptance: A hybrid SEM-neural network approach. Technol. Forecast. Soc. Chang. 2018, 129, 117–130. [Google Scholar] [CrossRef]

- Kazan, E.; Damsgaard, J. Towards a market entry framework for digital payment platforms. Commun. Assoc. Inf. Syst. 2016, 38, 761–783. [Google Scholar] [CrossRef]

- De Luna, I.R.; Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technol. Forecast. Soc. Chang. 2019, 146, 931–944. [Google Scholar] [CrossRef]

- Kalinic, Z.; Marinkovic, V.; Molinillo, S.; Liébana-Cabanillas, F. A multi-analytical approach to peer-to-peer mobile payment acceptance prediction. J. Retail. Consum. Serv. 2019, 49, 143–153. [Google Scholar] [CrossRef]

- Shao, Z.; Zhang, L.; Li, X.; Guo, Y. Antecedents of trust and continuance intention in mobile payment platforms: The moderating effect of gender. Electron. Commer. Res. Appl. 2019, 33, 100823. [Google Scholar] [CrossRef]

- Chen, S.C.; Chung, K.C.; Tsai, M.Y. How to achieve sustainable development of mobile payment through customer satisfaction-The SOR model. Sustainability 2019, 11, 6314. [Google Scholar] [CrossRef] [Green Version]

- Bhattacherjee, A. Understanding Information Systems Continuance: An Expectation-Confirmation Model. Manag. Inf. Syst. 2001, 25, 351–370. [Google Scholar] [CrossRef]

- Talwar, S.; Dhir, A.; Khalil, A.; Mohan, G.; Islam, A.K.M.N. Point of adoption and beyond. Initial trust and mobile-payment continuation intention. J. Retail. Consum. Serv. 2020, 55, 102086. [Google Scholar] [CrossRef]

- Ouyang, Y.; Tang, C.; Rong, W.; Zhang, L.; Yin, C.; Xiong, Z. Task-technology Fit Aware Expectation-confirmation Model towards Understanding of MOOCs Continued Usage Intention. In Proceedings of the 50th Hawaii International Conference on System Science, Waikoloa Village, HI, USA, 4–7 January 2017; pp. 174–183. [Google Scholar] [CrossRef] [Green Version]

- Oghuma, A.P.; Libaque-Saenz, C.F.; Wong, S.F.; Chang, Y. An expectation-confirmation model of continuance intention to use mobile instant messaging. Telemat. Inform. 2016, 33, 34–47. [Google Scholar] [CrossRef]

- Susanto, A.; Chang, Y.; Ha, Y. Determinants of continuance intention to use the smartphone banking services: An extension to the expectation-confirmation model. Ind. Manag. Data Syst. 2016, 116, 508–525. [Google Scholar] [CrossRef]

- Lee, J.; Ryu, M.H.; Lee, D. A study on the reciprocal relationship between user perception and retailer perception on platform-based mobile payment service. J. Retail. Consum. Serv. 2019, 48, 7–15. [Google Scholar] [CrossRef]

- Hong Zhu, D.; Ying, L.Y.P.; Chang, L. Understanding the Intention to Continue Use of a Mobile Payment Provider: An Examination of Alipay Wallet in China. Int. J. Bus. Inf. 2017, 12, 369–390. [Google Scholar] [CrossRef]

- Zhou, T. Understanding the determinants of mobile payment continuance usage. Ind. Manag. Data Syst. 2014, 114, 936–948. [Google Scholar] [CrossRef]

- Cao, M.; Zhang, Q. Supply chain collaboration: Impact on collaborative advantage and firm performance. J. Oper. Manag. 2011, 29, 163–180. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Dehghanpouri, H.; Soltani, Z.; Rostamzadeh, R. The impact of trust, privacy and quality of service on the success of E-CRM: The mediating role of customer satisfaction. J. Bus. Ind. Mark. 2020, 11, 1831–1847. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E.; Tatham, R.L. Multivariate Data Analysis; Prentice-Hall: New Jersey, NJ, USA, 2006. [Google Scholar]

- Fan, Y.; Stevenson, M. A review of supply chain risk management: Definition, theory, and research agenda. Int. J. Phys. Distrib. Logist. Manag. 2018. [Google Scholar] [CrossRef] [Green Version]

- Milian, E.Z.; De MSpinola, M.; De Carvalho, M. Fintechs: A literature review and research agenda. Electron. Commer. Res. Appl. 2019, 34. [Google Scholar] [CrossRef]

- Thammarat, C.; Kurutach, W. A lightweight and secure NFC-base mobile payment protocol ensuring fair exchange based on a hybrid encryption algorithm with formal verification. Int. J. Commun. Syst. 2019, 32, 1–21. [Google Scholar] [CrossRef]

- Agarwal, R.; Karahanna, E. Time Flies When You’re Having Fun: Cognitive Absorption and Beliefs about Information Technology Usage. MIS Q. 2000, 24, 665. [Google Scholar] [CrossRef]

- Taherdoost, H. Understanding of e-service security dimensions and its effect on quality and intention to use. Inf. Comput. Secur. 2017, 25, 535–559. [Google Scholar] [CrossRef]

- Fan, X.; Zhao, W.; Zhang, T.; Yan, E. Mobile payment, third-party payment platform entry and information sharing in supply chains. Ann. Oper. Res. 2020. [Google Scholar] [CrossRef]

- Park, S.; Kim, Y.; Chang, H. An empirical study on security expert ecosystem in the future IoT service environment. Comput. Electr. Eng. 2016, 52, 199–207. [Google Scholar] [CrossRef]

- Ahn, K.; Cho, J.-S. Major concerns of FinTech (Financial Technology) services in the Korean market. J. Bus. Retail. Manag. Res. 2019, 14, 123–133. [Google Scholar] [CrossRef]

- Singh, N.; Sinha, N. How perceived trust mediates merchant’s intention to use a mobile wallet technology. J. Retail. Consum. Serv. 2020, 52, 101894. [Google Scholar] [CrossRef]

- Singh, N.; Srivastava, S.; Sinha, N. Consumer preference and satisfaction of M-wallets: A study on North Indian consumers. Int. J. Bank Mark. 2017, 35, 944–965. [Google Scholar] [CrossRef]

{kind=link}

| Kakao Pay | Samsung Pay | Payco | Naver Pay | |

|---|---|---|---|---|

| Launch year | September 2014 | September 2015 | August 2015 | June 2015 |

| Estimated users (RU = registered users; MAU = monthly active users) | 30 million (RU) | 20 million (RU) | 9 million (RU) | 30 million (RU) |

| 19 million (MAU) | 12 million (MAU) | 4 million (MAU) | 11 million (MAU) | |

| On/offline pay market (market share) | 9% | 37% | 10% | 44% |

| Mobile pay market (market share) | 16% | 12% | 10% | 30% |

| Key services (Top 5) | Simple payment service (QR, bar-code) Transfer service Kakao pay certification service Billing credit inquiry Certified asset management Insurance | Simple payment service (MST, NFC) Transfer service ATM deposit and withdrawal Fund transfer Transportation card function | Simple payment service (QR, bar-code, MST, NFC) Transfer service ATM deposit and withdrawal Charging point system Local tax payment | Simple payment service (QR, bar-code) Transfer service Offline store booking Small business loan Insurance |

| International transaction availability | Yes | Yes | Yes | Yes |

| International transaction (currency) coverage | Japan | International card: 24 countries across six continents Domestic card: Most of the areas where NFCs are installed (i.e., US, UK, Russia, Australia, etc.) | Japan | Japan (i.e., 1.6 million franchises through the subsidiary “LINE”) |

| Strategic positioning | Blockchain based payment service Extensive customer data | Securing franchises with low commission | User-focused service Forms partnerships with various retail stores without any bias toward any specific platform | Online and offline link services based on Naver-shopping to 0.3 million online merchants |

| Variable | Sample | Percentage |

|---|---|---|

| Sex | ||

| Male | 170 | 47.75 |

| Female | 186 | 52.25 |

| Age | ||

| Below 29 | 107 | 30.06 |

| 30–39 | 105 | 29.49 |

| 40–49 | 100 | 28.09 |

| 50 and above | 44 | 12.36 |

| Frequently used mobile payment service | ||

| Kakao Pay | 94 | 26.40 |

| Naver Pay | 148 | 41.57 |

| Samsung Pay | 73 | 20.51 |

| Other | 41 | 11.52 |

| Monthly transaction frequency | ||

| Below 5 | 88 | 24.72 |

| 5–9 | 154 | 43.26 |

| 10–19 | 65 | 18.26 |

| 20 and above | 49 | 13.76 |

| Monthly transaction amount ($1 = 1000 KRW) | ||

| Below $100 | 90 | 25.28 |

| $100–$199 | 106 | 29.78 |

| $200–$399 | 78 | 21.91 |

| $400–$599 | 47 | 13.20 |

| $600–$799 | 15 | 4.21 |

| $800–$999 | 12 | 3.37 |

| $1000 and above | 8 | 2.25 |

| Latent Constructs | Measurement Items | Loadings | |

|---|---|---|---|

| Platform Security [6,62,76] | PS 1 | I believe that important personal information and transaction records can be safely shared by using this MPS | 0.850 |

| PS 2 | This MPS provides a high level of security by operating a regular maintenance and repairing schedule | 0.874 | |

| PS 3 | This MPS safely manages personal information in real time | 0.915 | |

| PS 4 | This MPS operates and processes my transactions without problems | 0.818 | |

| PS 5 | This MPS provides a high security level of wired and wireless networks | 0.900 | |

| Technology Security [41,49,51,77] | TS 1 | I believe that this MPS has a variety of security technologies at an advanced level to protect my important personal information and transaction records | 0.920 |

| TS 2 | This MPS provides a variety of authentication methods at a high level prior to make transactions | 0.873 | |

| TS 3 | This MPS provides a high level of confidentiality, that is hidden technology, anonymous technology, and encryption and decryption are adopted to protect the security of personal information | 0.906 | |

| TS 4 | This MPS enables customization to adequately tailor security settings to improve the protection of personal information | 0.851 | |

| TS 5 | This MPS has a high level of firewall technology to prevent the intrusion of unverified systems | 0.895 | |

| Convenience [11,31,32] | CON 1 | This MPS requires minimal time and effort to use payment services | 0.934 |

| CON 2 | This MPS provides a high level of learnability in the payment procedure | 0.818 | |

| CON 3 | This MPS provides a high level of ease of use while using mobile payment services | 0.796 | |

| CON 4 | This MPS provides a high level of simplicity while conducting financial transactions | 0.839 | |

| Interoperability [22,36,38,43] | INT 1 | This MPS provides a high level of intangibility while making mobile payments without the use of actual cards | 0.785 |

| INT 2 | This MPS provides a high level of independence from financial institutions when making mobile payments | 0.829 | |

| INT 3 | This MPS provides a high level of easy payment service whenever required | 0.854 | |

| INT 4 | If I register my card information on my mobile, this MPS allows me to pay through a mobile without the use of a physical card | 0.737 | |

| INT 5 | This MPS provides a high level of interoperability, wherein mobile payments can be made through various platforms and applications | 0.778 | |

| Trust [65,78] | TRST 1 | I believe this MPS ensures that all of the involved third parties retain the entire encrypted transactional data and not use the information for their own benefit | 0.835 |

| TRST 2 | I believe this MPS has a high level of integrity, that is the service adheres to the relevant policies and provides reliable services | 0.907 | |

| TRST 3 | I believe this MPS has the skills to render excellent services | 0.807 | |

| TRST 4 | I believe this MPS will act in its users best interests | 0.713 | |

| TRST 5 | I believe that when an unauthorized transaction occurs, this MPS will solve the problem or compensate | 0.782 | |

| TRST 6 | I believe this MPS processes individual transactions accurately and in a timely manner | 0.803 | |

| Continuous Intention [79,80] | COI 1 | I plan to use MPS in the future | 0.925 |

| COI 2 | I intend to continue using MPS in the future | 0.937 | |

| COI 3 | I expect my use of MPS to continue in the future | 0.939 |

| CR | AVE | PS | TS | CON | INT | TRST | COI | |

|---|---|---|---|---|---|---|---|---|

| Platform security (PS) | 0.941 | 0.761 | 0.872 | |||||

| Technology security (TS) | 0.950 | 0.791 | 0.913 | 0.889 | ||||

| Convenience (CON) | 0.911 | 0.720 | 0.414 | 0.313 | 0.848 | |||

| Interoperability (INT) | 0.897 | 0.636 | 0.613 | 0.491 | 0.727 | 0.798 | ||

| Trust (TRST) | 0.919 | 0.656 | 0.878 | 0.893 | 0.399 | 0.575 | 0.810 | |

| Continuous intention (COI) | 0.953 | 0.872 | 0.518 | 0.483 | 0.563 | 0.651 | 0.615 | 0.934 |

| Hypothesized Relationship | Path Coefficients | p-Value | |

|---|---|---|---|

| H1a | An increased level of platform security will lead to a higher level of perceived convenience in using MPS | 1.955 | 0.001 |

| H1b | An increased level of platform security will lead to a higher level of perceived interoperability of MPS | 1.982 | 0.001 |

| H1c | An increased level of platform security will lead to a higher level of perceived trust in using MPS | 0.658 | 0.001 |

| H2a | An increased level of technology security will lead to a higher level of perceived convenience in using MPS | −1.573 | 0.001 |

| H2b | An increased level of technology security will lead to a higher level of perceived interoperability of MPS | −1.446 | 0.001 |

| H2c | An increased level of technology security will lead to a higher level of perceived trust in using MPS | 0.307 | 0.001 |

| H3 | The degree of perceived convenience positively influences users intention to continue using MPS | 0.244 | 0.001 |

| H4 | The degree of perceived interoperability positively influences user intention to continue using MPS | 0.292 | 0.001 |

| H5 | The degree of perceived trust positively influences user intention to continue using MPS | 0.308 | 0.001 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hwang, Y.; Park, S.; Shin, N. Sustainable Development of a Mobile Payment Security Environment Using Fintech Solutions. Sustainability 2021, 13, 8375. https://doi.org/10.3390/su13158375

Hwang Y, Park S, Shin N. Sustainable Development of a Mobile Payment Security Environment Using Fintech Solutions. Sustainability. 2021; 13(15):8375. https://doi.org/10.3390/su13158375

Chicago/Turabian StyleHwang, Yoonyoung, Sangwook Park, and Nina Shin. 2021. "Sustainable Development of a Mobile Payment Security Environment Using Fintech Solutions" Sustainability 13, no. 15: 8375. https://doi.org/10.3390/su13158375

APA StyleHwang, Y., Park, S., & Shin, N. (2021). Sustainable Development of a Mobile Payment Security Environment Using Fintech Solutions. Sustainability, 13(15), 8375. https://doi.org/10.3390/su13158375