Is Innovation a Driver of Sustainability? An Analysis from a Spanish Region

Abstract

:1. Introduction

2. Theoretical Framework

2.1. Innovation as a Concept

2.2. Sustainability Concept

2.3. Measuring Sustainability

2.4. Innovation as a Driver of Sustainability

3. Objective, Materials and Methods

3.1. Objective and Hypotheses

3.2. Methodology

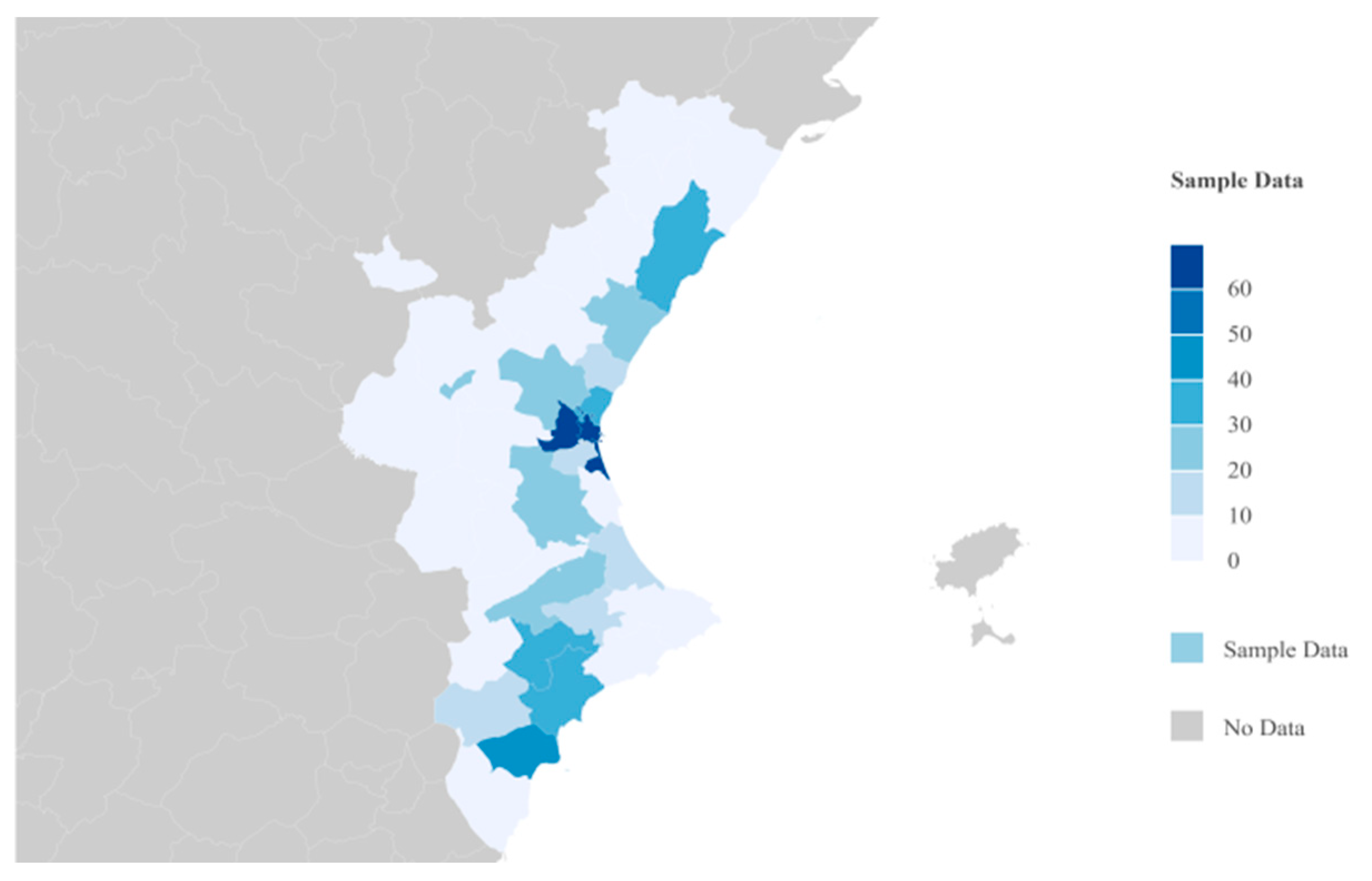

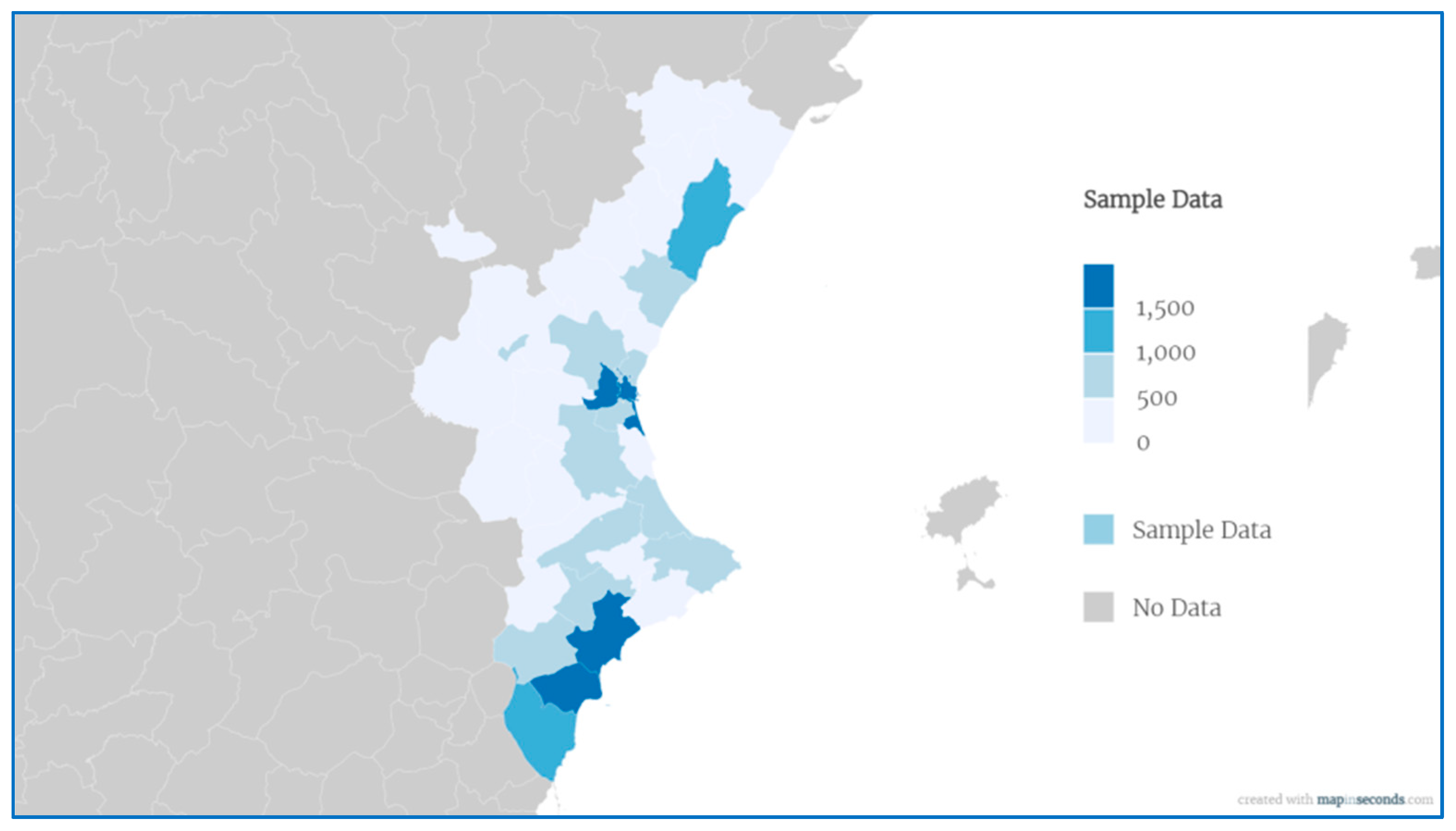

3.3. Samples and Techniques

- Display the awarded logo

- Use the logo in its commercial traffic and for advertising purposes, which is subject to fully complying with the applicable regulations, particularly as regards advertising

- Access tax benefits and rebates from Social Security contributions, as set out in Article 6 of Spanish Royal Decree 475/2014.

4. Quantitative Analysis

4.1. Statistical Analysis of the SME with the “Innovative SME” Label

4.2. Analysis of Companies with an Innovative Label and Environmental Concern

4.3. General Enterprises Analysis

4.4. Comparative Analyses and Fulfilling the Hypotheses

5. Discussion

6. Conclusions and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Schumpeter, J.A. The Theory of Economic Development; Harvard University Press: Cambridge, MA, USA, 1934; ISBN 9780674879904. [Google Scholar]

- Arjona Torres, M. Dirección Estratégica: Un Enfoque Práctico: Principios y Aplicaciones de la Gestión del Rendimiento; Díaz de Santos: Madrid, Spain, 1999; ISBN 8479783869. [Google Scholar]

- Scade, J. Responsabilidad Social y Sostenibilidad Empresarial. Available online: http//www.eoi.es/wiki (accessed on 10 April 2021).

- Srivastava, S.; Sultan, A.; Chashti, N. Influence of innovation competence on firm level competitiveness: An exploratory study. Asia Pac. J. Innov. Entrep. 2017, 11, 63–75. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 1984; ISBN 9780521151740. [Google Scholar]

- Drucker, P. The Temptation to Do Good; HarperCollins: London, UK, 1984; ISBN 9780060152536. [Google Scholar]

- European Commission SMEs and the Environment in the European Union. Available online: http://ec.europa.eu/enterprise/policies/sme/business-environment/files/main_report_en.pdf (accessed on 15 April 2021).

- Suciu (Vodă), A.-D.; Tudor, A.I.M.; Chițu, I.B.; Dovleac, L.; Brătucu, G. IoT Technologies as Instruments for SMEs’ Innovation and Sustainable Growth. Sustainability 2021, 13, 6357. [Google Scholar] [CrossRef]

- Edeigba, J.; Arasanmi, C. An empirical analysis of SMES’ triple bottom line practices. J. Account. Organ. Chang. 2021. ahead-of-print. [Google Scholar] [CrossRef]

- Klewitz, J.; Hansen, E.G. Sustainability-oriented innovation of SMEs: A systematic review. J. Clean. Prod. 2014, 65, 57–75. [Google Scholar] [CrossRef]

- Walker, B.; Redmon, J.; Sheridan, L.; Wang, C.; Goeft, U. Small and Medium Enterprises and the Environment: Barriers, Drivers, Innovation and Best Practice: A Review of the Literature; Edith Cowan University: Perth, Australia, 2008. [Google Scholar]

- European Commission Internal Market, Industry, Entrepreneurship and SMEs. Available online: https://ec.europa.eu/growth/smes/sme-definition_en (accessed on 20 March 2021).

- Obi, J.; Ibidunni, A.S.; Tolulope, A.; Olokundun, M.A.; Amaihian, A.B.; Borishade, T.T.; Fred, P. Contribution of small and medium enterprises to economic development: Evidence from a transiting economy. Data Br. 2018, 18, 835–839. [Google Scholar] [CrossRef]

- Rius-Sorolla, G.; Maheut, J.; Estelles-Miguel, S.; Garcia-Sabater, J.P. Protocol: Systematic Literature Review on coordination mechanisms for the mathematical programming models in production planning with decentralized decision making. WPOM-Working Pap. Oper. Manag. 2017, 8, 22. [Google Scholar] [CrossRef] [Green Version]

- Rosenberg, N. Inside the Black Box; Cambridge University Press: London, UK, 1983; ISBN 9780521248082. [Google Scholar]

- Nelson, R.R. Technology, Institutions, and Economic Growth; Harvard University Press: London, UK, 2006; ISBN 978-0674019164. [Google Scholar]

- Rosenberg, N. Innovation and Economic Growth. In Innovation and Growth in Tourism; OECD: Lugano, Switzerland, 2006; pp. 43–52. ISBN 9789264025028. [Google Scholar]

- Abramovitz, M. Resource and Output Trends in the United States since 1870; National Bureau of Economic Research: Cambridge, MA, USA, 1956; ISBN 0-87014-366-2. [Google Scholar]

- Eatwell, J.L.; Solow, R.M. Growth Theory: An Exposition. Econ. J. 1970, 80, 936. [Google Scholar] [CrossRef]

- Degong, M.; Ullah, F.; Khattak, M.; Anwar, M. Do International Capabilities and Resources Configure Firm’s Sustainable Competitive Performance? Research within Pakistani SMEs. Sustainability 2018, 10, 4298. [Google Scholar] [CrossRef] [Green Version]

- OECD Science and Innovation Policy Key Challenges and Opportunities Meeting of the OECD Committee for Scientific and Technological Policy at Ministerial Level. Available online: https://www.oecd.org/science/inno/23706075.pdf (accessed on 1 April 2021).

- Zerfass, A.; Huck, S. Innovation, Communication, and Leadership: New Developments in Strategic Communication. Int. J. Strateg. Commun. 2007, 1, 107–122. [Google Scholar] [CrossRef]

- Christensen, C.M. The Innovator’s Solution: Creating and Sustaining Successful Growth; Harvard Business Review Press: Boston, MA, USA, 2013; ISBN 978-1422196571. [Google Scholar]

- OECD 2010 Report on Attribution of Profits to Permanent Establishments. Available online: https://www.oecd.org/ctp/transfer-pricing/45689524.pdf (accessed on 1 April 2021).

- BCE. BCE—Informe Anual 2017. Available online: https://www.ecb.europa.eu/pub/pdf/annrep/ecb.ar2017.es.pdf (accessed on 9 April 2021).

- OECD/Eurostat. Oslo Manual 2018; The Measurement of Scientific, Technological and Innovation Activities; OECD: Paris, France, 2018; ISBN 9789264304550. [Google Scholar]

- Santandreu Mascarell, C. Propuesta de un Modelo de Gestión de Ideas Adaptado a al las Características Organizativas y de Innovación de las Empresas. El Caso de la Comarca de la Safor; Universitat Politècnica de València: Valencia, Spain, 2012. [Google Scholar]

- OECD. European Commission Manual de Oslo Guía para la recogida e interpretación de datos sobre innovación. Available online: https://www.tragsa.es/es/Lists/Publicaciones/attachments/93/ManualdeOslo.pdf (accessed on 10 April 2021).

- Corma Canós, F. Innovación, Innovadores y Empresa Innovadora; Díaz de Santos: Madrid, Spain, 2013; ISBN 9788499690070. [Google Scholar]

- Conca Flor, F.J.; Molina Manchón, H. Innovación Tecnológica y Competitividad Empresarial; Universidad de Alicante: Alicante, Spain, 2000; ISBN 978-84-7908-535-3. [Google Scholar]

- Hodges, N.J.; Link, A.N. Innovation by design. Small Bus. Econ. 2019, 52, 395–403. [Google Scholar] [CrossRef]

- Fischer, M.M. Innovation, Knowledge Creation and Systems of Innovation. In Innovation, Networks, and Knowledge Spillovers; Springer: Berlin/Heidelberg, Germany, 2006; Volume 35, pp. 169–187. ISBN 978-3-540-35981-4. [Google Scholar]

- Gurrutxaga Abad, A. Condiciones y condicionamientos de la innovación social. Arbor-Cienc. Pensam. Y Cult. 2011, 187, 1045–1064. [Google Scholar] [CrossRef] [Green Version]

- Mas, M.; Quesada, J. Las políticas de I+D+i ante la crisis. Rev. Galega Econ. 2010, 19, 1–17. [Google Scholar]

- Chen, L.; Qie, K.; Memon, H.; Yesuf, H.M. The Empirical Analysis of Green Innovation for Fashion Brands, Perceived Value and Green Purchase Intention—Mediating and Moderating Effects. Sustainability 2021, 13, 4238. [Google Scholar] [CrossRef]

- Kusi-Sarpong, S.; Gupta, H.; Sarkis, J. A supply chain sustainability innovation framework and evaluation methodology. Int. J. Prod. Res. 2019, 57, 1990–2008. [Google Scholar] [CrossRef] [Green Version]

- Silvestre, B.S.; Ţîrcă, D.M. Innovations for sustainable development: Moving toward a sustainable future. J. Clean. Prod. 2019, 208, 325–332. [Google Scholar] [CrossRef]

- Corma Cañós, F. El Canvas de la Innovación; Díaz de Santos: Madrid, Spain, 2017; ISBN 9788490520840. [Google Scholar]

- Hatch, N.W.; Mowery, D.C. Process Innovation and Learning by Doing in Semiconductor Manufacturing. Manag. Sci. 1998, 44, 1461–1477. [Google Scholar] [CrossRef]

- Reichstein, T.; Salter, A. Investigating the sources of process innovation among UK manufacturing firms. Ind. Corp. Chang. 2006, 15, 653–682. [Google Scholar] [CrossRef]

- Keupp, M.M.; Palmié, M.; Gassmann, O. The Strategic Management of Innovation: A Systematic Review and Paths for Future Research. Int. J. Manag. Rev. 2012, 14, 367–390. [Google Scholar] [CrossRef]

- Galindo Martín, M.-Á.; Ribeiro, D.; Méndez Picazo, M.T. Innovación y crecimiento económico: Factores que estimulan la innovación. Cuad. Gest. 2012, 12, 51–58. [Google Scholar] [CrossRef]

- Oecd Oslo Manual Guidalines for Collecting and Interpreting Innovation Data. Available online: https://ec.europa.eu/eurostat/documents/3859598/5889925/OSLO-EN.PDF/60a5a2f5-577a-4091-9e09-9fa9e741dcf1?version=1.0 (accessed on 10 April 2021).

- COTEC Anuario. 2019. Available online: https://content.gnoss.ws/cotec/doclinks/c3/c314/c314a4e9-e89e-4049-aa7b-3b8765a7f2af/informe-cotec-2019versionweb.pdf (accessed on 10 April 2021).

- OECD. OECD Science, Technology and Innovation Outlook 2020. Available online: https://www.oecd-ilibrary.org/science-and-technology/oslo-manual-2018_9789264304604-en (accessed on 9 April 2021).

- OECD. OECD R&D Tax Incentive Database. Available online: https://www.oecd.org/sti/B-index.pdf (accessed on 10 April 2021).

- Purvis, B.; Mao, Y.; Robinson, D. Three pillars of sustainability: In search of conceptual origins. Sustain. Sci. 2019, 14, 681–695. [Google Scholar] [CrossRef] [Green Version]

- Meadows, D.H.; Meadows, D.L.; Randers, J.; Behrens, W.W. The Limits to Growth: A Report for the Club of Rome’s Project on the Predicament of Mankind; Universe Books: New York, NY, USA, 1972; ISBN 0876631650. [Google Scholar]

- Carson, R.L. Silent Spring; Houghton Mifflin: Boston, MA, USA, 1962; ISBN 978-0618249060. [Google Scholar]

- Ehrlich, P.R. Population Control or Race to Oblivion? The Population Bomb; Ballantine Book: New York, NY, USA, 1968. [Google Scholar]

- Goldsmith, E.; Allen, R.; Allaby, M.; Davoll, J.; Lawrence, S. Blueprint for Survival; Houghton Mifflin: Boston, MA, USA, 1972; ISBN 0395140986. [Google Scholar]

- Castro, C.J. Sustainable Development. Organ. Environ. 2004, 17, 195–225. [Google Scholar] [CrossRef]

- Moldan, B.; Janoušková, S.; Hák, T. How to understand and measure environmental sustainability: Indicators and targets. Ecol. Indic. 2012, 17, 4–13. [Google Scholar] [CrossRef]

- Elkington, A.R. Cannibals with Forks: The Triple Bottom Line of 21st Century Business; Capstone Publishing Ltd.: Oxford, UK, 1997; ISBN 1-900961-27-X. [Google Scholar]

- Hansmann, R.; Mieg, H.A.; Frischknecht, P. Principal sustainability components: Empirical analysis of synergies between the three pillars of sustainability. Int. J. Sustain. Dev. World Ecol. 2012, 19, 451–459. [Google Scholar] [CrossRef]

- Hubbard, G. Measuring organizational performance: Beyond the triple bottom line. Bus. Strateg. Environ. 2009, 18, 177–191. [Google Scholar] [CrossRef]

- Fauzi, H.; Svensson, G.; Rahman, A.A. “Triple Bottom Line” as “Sustainable Corporate Performance”: A Proposition for the Future. Sustainability 2010, 2, 1345–1360. [Google Scholar] [CrossRef] [Green Version]

- Skouloudis, A.; Evangelinos, K.; Kourmousis, F. Development of an evaluation methodology for triple bottom line reports using international standards on reporting. Environ. Manag. 2009, 44, 298–311. [Google Scholar] [CrossRef]

- Rius-Sorolla, G.; Estelles-Miguel, S.; Rueda-Armengot, C. Multivariable Supplier Segmentation in Sustainable Supply Chain Management. Sustainability 2020, 12, 4556. [Google Scholar] [CrossRef]

- UN Global Compact Social Sustainability. Available online: https://unglobalcompact.org/what-is-gc/our-work/social (accessed on 29 April 2021).

- Alyson Warhust Sustainability Indicators and Sustainability Performance Management. Available online: http://pubs.iied.org/pdfs/G01026.pdf (accessed on 7 June 2021).

- Comisión Europea Comunicación de la Comisión al Parlamento Europeo, al Consejo, al Comité Económico y Social Europeo y al Comité de las Regiones. Estrategia renovada de la UE para 2011–2014 sobre la responsabilidad social de las empresas. Available online: https://eur-lex.europa.eu/legal-content/ES/TXT/PDF/?uri=CELEX:52011DC0681&from=ES (accessed on 10 April 2021).

- Testa, F.; Boiral, O.; Iraldo, F. Internalization of Environmental Practices and Institutional Complexity: Can Stakeholders Pressures Encourage Greenwashing? J. Bus. Ethics 2018, 147, 287–307. [Google Scholar] [CrossRef]

- Buhr, N.; Gray, R. Environmental Management, Measurement, and Accounting: Information for Decision and Control? Oxford University Press: Oxford, UK, 2011; ISBN 9780191735318. [Google Scholar]

- EMAS EU Eco-Management and Audit Scheme. Available online: https://ec.europa.eu/environment/emas/index_en.htm (accessed on 7 April 2021).

- SAC Higg Index. Available online: https://apparelcoalition.org/the-higg-index/ (accessed on 4 April 2021).

- Radhakrishnan, S. The Sustainable Apparel Coalition and the Higg Index. In Roadmap to Sustainable Textiles and Clothing; Springer: Singapore, 2015; pp. 23–57. [Google Scholar]

- Lab., B. El Movimiento B Corp. Available online: https://bcorporation.eu/about-b-lab/country-partner/spain (accessed on 4 April 2021).

- Shields, J.F.; Shelleman, J.M. A Method to Launch Sustainability Reporting in SMEs: The B Corp Impact Assessment Framework. J. Strateg. Innov. Sustain. 2017, 12, 10–19. [Google Scholar] [CrossRef]

- Oeko-tex OEKO-TEX. Available online: https://www.oeko-tex.com/en/ (accessed on 6 April 2021).

- ISSOP Fundación Energía e Innovación Sostenible Sin Obsolescencia Programada. Available online: https://feniss.org/ (accessed on 6 April 2021).

- Rivera, J.L.; Lallmahomed, A. Environmental implications of planned obsolescence and product lifetime: A literature review. Int. J. Sustain. Eng. 2016, 9, 119–129. [Google Scholar] [CrossRef]

- Ferro, C.; Padin, C.; Svensson, G.; Sosa Varela, J.C.; Wagner, B.; Høgevold, N.M. Validating a framework of stakeholders in connection to business sustainability efforts in supply chains. J. Bus. Ind. Mark. 2017, 32, 124–137. [Google Scholar] [CrossRef]

- Widya-Hasuti, A.; Mardani, A.; Streimikiene, D.; Sharifara, A.; Cavallaro, F. The role of process innovation between firm-specific capabilities and sustainable innovation in SMEs: Empirical evidence from Indonesia. Sustainability 2018, 10, 2244. [Google Scholar] [CrossRef] [Green Version]

- Strobel, N.; Kratzer, J. Obstacles to innovation for SMEs: Evidence from Germany. Int. J. Innov. Manag. 2017, 21, 1750030. [Google Scholar] [CrossRef]

- Rius-Sorolla, G.; Maheut, J.; Estelles-Miguel, S.; Garcia-Sabater, J.P.; Jesús Muñoz-Torres, M.; Aviles-Palacios, C. Collaborative Distributed Planning with Asymmetric Information. A Technological Driver for Sustainable Development. Sustainability 2021, 13, 6628. [Google Scholar] [CrossRef]

- Del Brío, J.Á.; Junquera, B. A review of the literature on environmental innovation management in SMEs: Implications for public policies. Technovation 2003, 23, 939–948. [Google Scholar] [CrossRef]

- Shi, H.; Peng, S.Z.; Liu, Y.; Zhong, P. Barriers to the implementation of cleaner production in Chinese SMEs: Government, industry and expert stakeholders’ perspectives. J. Clean. Prod. 2008, 16, 842–852. [Google Scholar] [CrossRef]

- Garcia, S.; Cintra, Y.; Rita de Cássia, S.R.; Lima, F.G. Corporate sustainability management: A proposed multi-criteria model to support balanced decision-making. J. Clean. Prod. 2016, 136, 181–196. [Google Scholar] [CrossRef]

- Belyaeva, Z.; Rudawska, E.D.; Lopatkova, Y. Sustainable business model in food and beverage industry—A case of Western and Central and Eastern European countries. Br. Food J. 2020, 122, 1573–1592. [Google Scholar] [CrossRef]

- Corsi, C.; Prencipe, A.; Capriotti, A. Linking organizational innovation, firm growth and firm size. Manag. Res. J. Iberoam. Acad. Manag. 2019, 17, 24–49. [Google Scholar] [CrossRef]

- Montégu, J.P.; Calvo, C.; Pertuze, J.A. Competition, R&D and innovation in Chilean firm. Manag. Res. J. Iberoam. Acad. Manag. 2019, 17, 379–403. [Google Scholar] [CrossRef]

- Del Campo, M.O.; Miguéns-Refojo, V.; Ferreiro-Seoane, F.J. Business Survival and the Influence of Innovation on Entrepreneurs in Business Incubators. Sustainability 2020, 12, 6197. [Google Scholar] [CrossRef]

- Cárdenas Gutiérrez, K.M.; Blanco López, L.Y.; Correa Barros, L.F. La Innovación y Tecnología en las Pequeñas y Medianas Empresas Agroindustriales del Departamento del Magdalena; Universidad Cooperativa de Colombia, Facultad de Ciencias Económicas, Administrativas y Contables, Administración de Empresas: Santa Marta/Medellín, Colombia, 2020. [Google Scholar]

- Fernández-Portillo, A.; Sánchez-Escobedo, M.C.; Almodóvar-González, M. Análisis del impacto de la innovación, las TIC y el clima empresarial sobre los ingresos de las PYMES. Rev. Int. Organ. 2020, 24, 183–209. [Google Scholar] [CrossRef]

- Villegas, R.M. Innovación, creatividad y desarrollo tecnológico en las PyMES de Río Gallegos, Santa Cruz. Rev. Cienc. Empres. Soc. 2021, 3, 1–14. [Google Scholar]

- Cuevas-Vargas, H.; Parga-Montoya, N.; Estrada, S. Incidencia de la innovación en marketing en el rendimiento empresarial: Una aplicación basada en modelamiento con ecuaciones estructurales. Estud. Gerenciales 2020, 36, 66–79. [Google Scholar] [CrossRef]

- Mashavira, N.; Chipunza, C.; Dzansi, D.Y. Managerial interpersonal competencies and the performance of family-and non-family-owned small and medium-sized enterprises in zimbabwe and South Africa. S. Afr. J. Child. Educ. 2019, 17, 1–15. [Google Scholar] [CrossRef]

- Martinez-Conesa, I.; Soto-Acosta, P.; Palacios-Manzano, M. Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. J. Clean. Prod. 2017, 142, 2374–2383. [Google Scholar] [CrossRef]

- Aguilar-Fernández, M.E.; Otegi-Olaso, J.R. Firm size and the business model for sustainable innovation. Sustainability 2018, 10, 785. [Google Scholar] [CrossRef] [Green Version]

- Adomako, S. Environmental collaboration, sustainable innovation, and small and medium-sized enterprise growth in sub-Saharan Africa: Evidence from Ghana. Sustain. Dev. 2020, 28, 1609–1619. [Google Scholar] [CrossRef]

- Dvouletý, O.; Blažková, I. The impact of public grants on firm-level productivity: Findings from the Czech food industry. Sustainability 2019, 11, 552. [Google Scholar] [CrossRef] [Green Version]

- Erken, H.; Donselaar, P.; Thurik, R. Total factor productivity and the role of entrepreneurship. J. Technol. Transf. 2018, 43, 1493–1521. [Google Scholar] [CrossRef] [Green Version]

- Caputo, F.; Carrubbo, L.; Sarno, D. The Influence of Cognitive Dimensions on the Consumer-SME Relationship: A Sustainability-Oriented View. Sustainability 2018, 10, 3238. [Google Scholar] [CrossRef] [Green Version]

- Jin, S.H.; Choi, S.O. The effect of innovation capability on business performance: A focus on it and business service companies. Sustainability 2019, 11, 5246. [Google Scholar] [CrossRef] [Green Version]

- Villena-Manzanares, F. El impacto del compromiso por la calidad y la cultura emprendedora sobre el comportamiento innovador de la pyme manufacturera bajo un enfoque de dirección participativa. Dir. Organ. 2016, 58, 4–15. [Google Scholar] [CrossRef]

- Uhlaner, L.M.; Berent-Braun, M.M.; Jeurissen, R.J.M.; de Wit, G. Beyond Size: Predicting Engagement in Environmental Management Practices of Dutch SMEs. J. Bus. Ethics 2012, 109, 411–429. [Google Scholar] [CrossRef]

- Yu, G.J.; Kwon, K.M.; Lee, J.; Jung, H. Exploration and exploitation as antecedents of environmental performance: The moderating effect of technological dynamism and firm size. Sustainability 2016, 8, 200. [Google Scholar] [CrossRef] [Green Version]

- Bouncken, R.B.; Fredrich, V. Business model innovation in alliances: Successful configurations. J. Bus. Res. 2016, 69, 3584–3590. [Google Scholar] [CrossRef]

- Kowalska, M. Sme managers’ perceptions of sustainable marketing mix in different socioeconomic conditions—A comparative analysis of sri lanka and poland. Sustainability 2020, 12, 659. [Google Scholar] [CrossRef]

- Kim, M.; Kim, J.; Sawng, Y.; Lim, K. Impacts of innovation type SME’s R&D capability on patent and new product development. Asia Pac. J. Innov. Entrep. 2018, 12, 45–61. [Google Scholar] [CrossRef]

- Romijn, H.; Albaladejo, M. Determinants of innovation capability in small electronics and software firms in southeast England. Res. Policy 2002, 31, 1053–1067. [Google Scholar] [CrossRef]

- Rita, D.I.G.; Ferreira, F.A.F.; Meidutė-Kavaliauskienė, I.; Govindan, K.; Ferreira, J.J.M. Proposal of a green index for small and medium-sized enterprises: A multiple criteria group decision-making approach. J. Clean. Prod. 2018, 196, 985–996. [Google Scholar] [CrossRef]

- Fadly, D. Greening industry in Vietnam: Environmental management standards and resource efficiency in SMEs. Sustainability 2020, 12, 7455. [Google Scholar] [CrossRef]

- Shahedul Quader, M.; Kamal, M.M.; Hassan, A.B.M.E. Sustainability of positive relationship between environmental performance and profitability of SMEs. J. Enterp. Communities People Places Glob. Econ. 2016, 10, 138–163. [Google Scholar] [CrossRef]

- Maas, S.; Reniers, G. Development of a CSR model for practice: Connecting five inherent areas of sustainable business. J. Clean. Prod. 2014, 64, 104–114. [Google Scholar] [CrossRef]

- Ferrón Vílchez, V. The dark side of ISO 14001: The symbolic environmental behavior. Eur. Res. Manag. Bus. Econ. 2017, 23, 33–39. [Google Scholar] [CrossRef] [Green Version]

- De Oliveira, J.A.; Oliveira, O.J.; Ometto, A.R.; Ferraudo, A.S.; Salgado, M.H. Environmental Management System ISO 14001 factors for promoting the adoption of Cleaner Production practices. J. Clean. Prod. 2016, 133, 1384–1394. [Google Scholar] [CrossRef] [Green Version]

- Graafland, J. Does Corporate Social Responsibility Put Reputation at Risk by Inviting Activist Targeting? An Empirical Test among European SMEs. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1–13. [Google Scholar] [CrossRef] [Green Version]

- Sánchez-Medina, P.S.; Corbett, J.; Toledo-López, A. Environmental innovation and sustainability in small handicraft businesses in Mexico. Sustainability 2011, 3, 984–1002. [Google Scholar] [CrossRef] [Green Version]

- Wysocki, J. Innovative Green Initiatives in the Manufacturing SME Sector in Poland. Sustainability 2021, 13, 2386. [Google Scholar] [CrossRef]

- Aguilera-Caracuel, J.; Ortiz-de-Mandojana, N. Green Innovation and Financial Performance. Organ. Environ. 2013, 26, 365–385. [Google Scholar] [CrossRef]

- De Pacheco, D.A.J.; ten Caten, C.S.; Jung, C.F.; Ribeiro, J.L.D.; Navas, H.V.G.; Cruz-Machado, V.A. Eco-innovation determinants in manufacturing SMEs: Systematic review and research directions. J. Clean. Prod. 2017, 142, 2277–2287. [Google Scholar] [CrossRef]

- Stiglitz, J.E.; Lin, J.Y.; Monga, C. Introduction: The Rejuvenation of Industrial Policy. In The Industrial Policy Revolution I; Palgrave Macmillan: London, UK, 2013; pp. 1–15. [Google Scholar] [CrossRef]

- Fagerberg, J. Mobilizing innovation for sustainability transitions: A comment on transformative innovation policy. Res. Policy 2018, 47, 1568–1576. [Google Scholar] [CrossRef]

- Lesakova, Ľ. Small and medium enterprises and eco-innovations: Empirical study of Slovak SME’s. Mark. Manag. Innov. 2019, 6718, 89–97. [Google Scholar] [CrossRef]

- Cagno, E.; Trianni, A. Exploring drivers for energy efficiency within small- and medium-sized enterprises: First evidences from Italian manufacturing enterprises. Appl. Energy 2013, 104, 276–285. [Google Scholar] [CrossRef]

- Kim, H.; Kim, E. How an open innovation strategy for commercialization affects the firm performance of Korean healthcare IT SMEs. Sustainability 2018, 10, 2476. [Google Scholar] [CrossRef] [Green Version]

- AIREF Crecimiento Interanual del PIB por CCAA: 2019 T4. Available online: https://www.airef.es/wp-content/uploads/2020/02/METCAP/2020-02-04-PIB_CCAA_2019_T4-3-de-febrero-2020.pdf (accessed on 1 April 2021).

- INE Encuesta de Población Activa EPA. Available online: https://www.ine.es/dyngs/INEbase/es/operacion.htm?c=Estadistica_C&cid=1254736176918&menu=ultiDatos&idp=1254735976595 (accessed on 1 April 2021).

- Ministerio de Ciencia e Innovación Pymes Innovadoras. Available online: https://www.ciencia.gob.es/portal/site/MICINN/menuitem.6f2062042f6a5bc43b3f6810d14041a0/?vgnextoid=45cc94d74dd4a410VgnVCM1000001d04140aRCRD (accessed on 28 December 2020).

- Gonzales-Gemio, C.; Cruz-Cázares, C.; Parmentier, M.J. Responsible Innovation in SMEs: A Systematic Literature Review for a Conceptual Model. Sustainability 2020, 12, 10232. [Google Scholar] [CrossRef]

- Staniškienė, E.; Stankevičiūtė, Ž. Social sustainability measurement framework: The case of employee perspective in a CSR-committed organisation. J. Clean. Prod. 2018, 188, 708–719. [Google Scholar] [CrossRef]

- Amrutha, V.N.; Geetha, S.N. A systematic review on green human resource management: Implications for social sustainability. J. Clean. Prod. 2020, 247, 119131. [Google Scholar] [CrossRef]

- Govindan, K.; Shaw, M.; Majumdar, A. Social sustainability tensions in multi-tier supply chain: A systematic literature review towards conceptual framework development. J. Clean. Prod. 2021, 279, 123075. [Google Scholar] [CrossRef]

- Brem, A.; Puente-Díaz, R. Creativity, Innovation, Sustainability: A Conceptual Model for Future Research Efforts. Sustainability 2020, 12, 3139. [Google Scholar] [CrossRef] [Green Version]

- Jackson, T.; Victor, P.A. Confronting inequality in the “new normal”: Hyper-capitalism, proto-socialism, and post-pandemic recovery. Sustain. Dev. 2021, 29, 504–516. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | No. | % s/Total |

|---|---|---|

| 2015 | 2 | 0.34% |

| 2016 | 3 | 0.51% |

| 2017 | 2 | 0.34% |

| 2018 | 3 | 0.51% |

| 2019 | 13 | 2.23% |

| 2020 | 16 | 2.74% |

| Totally Extinguished | 39 | 6.68% |

| No data deposited in the Mercantile register | 32 | 5.48% |

| With label and deposit accounts | 513 | 87.84% |

| Total | 584 | 100.00% |

| Expiry Year | No. | % |

|---|---|---|

| 2018 | 126 | 24.56% |

| 2019 | 16 | 3.12% |

| 2020 | 60 | 11.70% |

| 2021 | 108 | 21.05% |

| 2022 | 101 | 19.69% |

| 2023 | 95 | 18.52% |

| 2024 | 2 | 0.39% |

| 2025 | 5 | 0.97% |

| Total | 513 | 100.00% |

| SME with a valid seal | 311 | 60.62% |

| Group Code | Description | No. | % | Economical Profitability | Financial Profitability |

|---|---|---|---|---|---|

| A | Agriculture, livestock, forestry and fisheries | 3 | 0.58% | −1.48% | −6.53% |

| B | Extractive industries | 1 | 0.19% | 29.06% | 35.19% |

| C | Manufacturing industry | 255 | 49.71% | 7.08% | 13.68% |

| E | Water supply | 5 | 0.97% | 5.88% | 18.29% |

| F | Construction | 12 | 2.34% | 3.00% | 8.03% |

| G | Wholesale and retail | 60 | 11.70% | 6.21% | 13.46% |

| H | Transport & storage | 3 | 0.58% | 8.11% | 56.69% |

| J | Information and communications | 74 | 14.42% | 7.78% | 18.32% |

| K | Financial and insurance activities | 2 | 0.39% | 1.15% | 2.08% |

| L | Real-estate activities | 2 | 0.39% | 4.21% | 4.36% |

| M | Professional, scientific and technical activities | 80 | 15.59% | 26.58% | 43.22% |

| N | Administrative activities and auxiliary services | 5 | 0.97% | 12.26% | 30.59% |

| P | Education | 1 | 0.19% | 5.09% | 10.02% |

| Q | Health and social work activities | 10 | 1.95% | 16.78% | 28.97% |

| Total | 513 | 100% | 10.2% | 19.4% |

| Group Code | Description | Average Employment 2019 | Average Employment Growth 2015–2019 | Average Employment Growth % 2015–2019 |

|---|---|---|---|---|

| A | Agriculture, livestock, forestry and fisheries | 83.7 | 33.3 | 70.0% |

| B | Extractive industries | 42.0 | −4.0 | −8.7% |

| C | Manufacturing industry | 62.1 | 13.1 | 51.4% |

| E | Water supply | 95.4 | 31.0 | 211.6% |

| F | Construction | 33.3 | 7.7 | 39.6% |

| G | Wholesale and retail | 47.8 | 12.9 | 73.7% |

| H | Transport & storage | 100.7 | 12.0 | 13.4% |

| J | Information and communications | 37.2 | 15.8 | 129.0% |

| K | Financial and insurance activities | 16.0 | 10.0 | 88.9% |

| L | Real-estate activities | 4.0 | 0.0 | 42.9% |

| M | Professional, scientific and technical activities | 27.0 | 7.6 | 90.0% |

| N | Administrative activities and auxiliary services | 33.8 | 14.3 | 297.9% |

| P | Education | 103.0 | 32.0 | 45.1% |

| Q | Health and social work activities | 28.7 | 9.0 | 42.2% |

| Total | 50.1 | 12.6 | 74.8% |

| Type of Legal Form | No. | % Total | Economical Profitability | Financial Profitability | Average Employment 2019 | Average Employment Growth 2015–2019 | Average Employment Growth % 2015–2019 |

|---|---|---|---|---|---|---|---|

| Public Limited Company | 93 | 18.2% | 6.8% | 8.6% | 75.0 | 11.6 | 22.9% |

| Private Limited Companies | 420 | 81.8% | 11.0% | 21.8% | 44.5 | 12.9 | 86.6% |

| Total | 513 | 100% | 10.2% | 19.4% | 50.1 | 12.6 | 74.8% |

| Group Code | Description | No. | % | Economical Profitability | Financial Profitability |

|---|---|---|---|---|---|

| A | Agriculture, livestock, forestry and fisheries | 2 | 0.90% | 5.21% | 10.45% |

| B | Extractive industries | 1 | 0.50% | 29.06% | 35.19% |

| C | Manufacturing industry | 135 | 61.60% | 7.79% | 14.73% |

| E | Water supply | 4 | 1.80% | 5.75% | 18.87% |

| F | Construction | 6 | 2.70% | 5.92% | 11.72% |

| G | Wholesale and retail | 19 | 8.70% | 7.27% | 16.20% |

| H | Transport & storage | 3 | 1.40% | 7.78% | 36.69% |

| J | Information and communications | 14 | 6.40% | −1.40% | −0.42% |

| M | Professional, scientific and technical activities | 30 | 13.70% | −4.66% | 15.70% |

| N | Administrative activities and auxiliary services | 3 | 1.40% | 11.50% | 25.19% |

| Q | Health and social work activities | 2 | 0.90% | 35.70% | 56.97% |

| Total | 219 | 100% | 5.73% | 14.90% |

| Group Code | Description | Average Employment 2019 | Average Employment Growth 2015–2019 | Average Employment Growth % 2015–2019 |

|---|---|---|---|---|

| A | Agriculture, livestock, forestry and fisheries | 21.50 | 7.50 | 70.50% |

| B | Extractive industries | 42.00 | −4.00 | −8.70% |

| C | Manufacturing industry | 73.49 | 15.19 | 47.30% |

| E | Water supply | 106.50 | 27.25 | 34.50% |

| F | Construction | 55.00 | 11.17 | 28.80% |

| G | Wholesale and retail | 67.79 | 25.42 | 117.30% |

| H | Transport & storage | 100.67 | 12.00 | 13.40% |

| J | Information and communications | 91.00 | 40.71 | 203.00% |

| M | Professional, scientific and technical activities | 41.13 | 8.90 | 55.40% |

| N | Administrative activities and auxiliary services | 46.00 | 13.33 | 25.90% |

| Q | Health and social work activities | 73.00 | 40.00 | 113.20% |

| Total | 49.66 | 12.33 | 73.10% |

| Type | No. | % of the Total | Economical Profitability | Financial Profitability | Average Employment 2019 | Average Employment Growth 2015–2019 | Average Employment Growth % 2015–2019 |

|---|---|---|---|---|---|---|---|

| Public Limited Company | 54 | 24.66% | 4.67% | 10.48% | 79.70 | 13.04 | 23.51% |

| Private Limited Companies | 165 | 75.34% | 6.08% | 16.36% | 65.65 | 18.32 | 78.49% |

| Total | 219 | 100% | 5.7% | 14.9% | 69.13 | 17.00 | 64.37% |

| Group Code | Description | No. | % | Economical Profitability | Financial Profitability |

|---|---|---|---|---|---|

| A | Agriculture, livestock, forestry and fisheries | 113 | 0.60% | 6.82% | 18.04% |

| B | Extractive industries | 2 | 0.00% | 27.60% | 33.95% |

| C | Manufacturing industry | 5222 | 25.50% | 5.93% | 11.49% |

| E | Water supply | 112 | 0.50% | 11.21% | 23.07% |

| F | Construction | 3312 | 16.20% | 3.93% | 8.89% |

| G | Wholesale and retail | 5307 | 25.90% | 5.66% | 11.32% |

| H | Transport & storage | 1265 | 6.20% | 6.17% | 11.67% |

| J | Information and communications | 628 | 3.10% | 13.41% | 25.08% |

| K | Financial and insurance activities | 228 | 1.10% | 5.43% | 6.55% |

| L | Real-estate activities | 1559 | 7.60% | 3.43% | 4.61% |

| M | Professional, scientific and technical activities | 1634 | 8.00% | 9.82% | 15.36% |

| N | Administrative activities and auxiliary services | 502 | 2.50% | 5.04% | 7.88% |

| P | Education | 197 | 1.00% | 3.43% | 6.40% |

| Q | Health and social work activities | 408 | 2.00% | 9.13% | 12.65% |

| Total | 20,489 | 100% | 5.95% | 11.17% |

| Group Code | Description | Total Employment 2019 | Total Employment 2015 | Average Employment per Enterprise 2019 | Average Employment Growth 2015–2019 | Average Employment Growth per Enterprise 2015–2019 | Average Employment Growth % 2015–2019 |

|---|---|---|---|---|---|---|---|

| A | Agriculture, livestock, forestry and fisheries | 1563 | 1328 | 13.83 | 235 | 2.08 | 17.70% |

| B | Extractive industries | 46 | 49 | 23.00 | −3 | −1.50 | −6.12% |

| C | Manufacturing industry | 93,019 | 79,473 | 17.81 | 13,546 | 2.59 | 17.04% |

| E | Water supply | 2269 | 1890 | 20.26 | 379 | 3.38 | 20.05% |

| F | Construction | 29,117 | 21,066 | 8.79 | 8051 | 2.43 | 38.22% |

| G | Wholesale and retail | 54,382 | 46,309 | 10.25 | 8073 | 1.52 | 17.43% |

| H | Transport & storage | 18,134 | 14,042 | 14.34 | 4092 | 3.23 | 29.14% |

| J | Information and communications | 6809 | 4724 | 10.84 | 2085 | 3.32 | 44.14% |

| K | Financial and insurance activities | 1205 | 1484 | 5.29 | −279 | −1.22 | −18.80% |

| L | Real-estate activities | 3932 | 5185 | 2.52 | −1253 | −0.80 | −24.17% |

| M | Professional, scientific and technical activities | 14,062 | 11,023 | 8.61 | 3039 | 1.86 | 27.57% |

| N | Administrative activities and auxiliary services | 4904 | 3907 | 9.77 | 997 | 1.99 | 25.52% |

| P | Education | 1928 | 1854 | 9.79 | 74 | 0.38 | 3.99% |

| Q | Health and social work activities | 3492 | 3039 | 8.56 | 453 | 1.11 | 14.91% |

| Total | 234,862 | 195,373 | 11.46 | 39,489 | 1.93 | 20.21% |

| Group Code Description | Innovative Label | Total | |||||||

|---|---|---|---|---|---|---|---|---|---|

| No. | % | Economical Profitability | Financial Profitability | No. | % | Economical Profitability | Financial Profitability | ||

| C | Manufacturing industry | 255 | 49.71% | 7.08% | 13.68% | 5222 | 25.50% | 5.93% | 11.49% |

| G | Wholesale and retail | 60 | 11.70% | 6.21% | 13.46% | 5307 | 25.90% | 5.66% | 11.32% |

| J | Information and communications | 74 | 14.42% | 7.78% | 18.32% | 628 | 3.10% | 13.41% | 25.08% |

| M | Professional, scientific and technical activities | 80 | 15.59% | 26.58% | 43.22% | 1634 | 8.00% | 9.82% | 15.36% |

| Others 10 | 44 | 8.58% | 7698 | 37.60% | |||||

| Total | 513 | 100% | 10.20% | 19.40% | 20489 | 100% | 5.95% | 11.17% | |

| Variables | Innovative SME | N | Average (m€) | F | Sig. | Levene’s Test | Sig. (Bilateral) |

|---|---|---|---|---|---|---|---|

| Operations Income 2019 | Yes | 453 | 10,097.34 | 95.09 | 0.000 | No variances are assumed | 0.000 |

| No | 20,212 | 2761.45 | |||||

| Profits (EBT) 2019 | Yes | 351 | 178.43 | 505.11 | 0.000 | No variances are assumed | 0.000 |

| No | 19,510 | 53.31 | |||||

| Assets | Yes | 79 | 509.43 | 0.759 | 0.384 | Variances are assumed | 0.000 |

| No | 13,216 | 334.34 | |||||

| Equity | Yes | 132 | 411.23 | 17,100 | 0.000 | No variances are assumed | 0.000 |

| No | 15,816 | 206.07 |

| Group Code | Description | Innovative Label | Total | ||||

|---|---|---|---|---|---|---|---|

| Average employment per Enterprise 2019 | Average Employment Growth per Enterprise 2015–2019 | Average Employment Growth % 2015–2019 | Average Employment per Enterprise 2019 | Average Employment Growth per Enterprise 2015–2019 | Avergae Employment Growth % 2015–2019 | ||

| C | Manufacturing industry | 62.1 | 13.1 | 51.40% | 17.81 | 2.59 | 17.04% |

| G | Wholesale and retail | 47.8 | 12.9 | 73.70% | 10.25 | 1.52 | 17.43% |

| J | Information and communications | 37.2 | 15.8 | 129.00% | 10.84 | 3.32 | 44.14% |

| M | Professional, scientific and technical activities | 27.0 | 7.6 | 90.00% | 8.61 | 1.86 | 27.57% |

| Total | 50.1 | 12.6 | 74.80% | 11.88 | 1.93 | 20.21% | |

| Variables | Innovative Label | No. | Average | F | Sig. | Levene’s Test | Sig. (Bilateral) |

|---|---|---|---|---|---|---|---|

| Employment 2019 | Yes | 455 | 12.64 | 161.38 | 0.000 | No variances are assumed | 0.000 |

| No | 20,301 | 11.85 | |||||

| Employment growth | Yes | 444 | 12.58 | 80.29 | 0.000 | No variances are assumed | 0.000 |

| No | 20,301 | 2.56 |

| Group Code | Description | Innovative Label | Environmentally Sensitive | ||||||

|---|---|---|---|---|---|---|---|---|---|

| No. | % | Economical Profitability | Financial Profitability | No. | % | Economical Profitability | Financial Profitability | ||

| C | Manufacturing industry | 255 | 49.71% | 7.08% | 13.68% | 135 | 61.60% | 7.79% | 14.73% |

| G | Wholesale and retail | 60 | 11.70% | 6.21% | 13.46% | 19 | 8.70% | 7.27% | 16.20% |

| J | Information and communications | 74 | 14.42% | 7.78% | 18.32% | 14 | 6.40% | −1.40% | −0.42% |

| M | Professional, scientific and technical activities | 80 | 15.59% | 26.58% | 43.22% | 30 | 13.70% | −4.66% | 15.70% |

| 10 others | 44 | 8.58% | 21 | 9.60% | |||||

| Total | 513 | 100.00% | 10.20% | 19.40% | 219 | 100.00% | 5.73% | 14.90% | |

| Group Code | Description | Innovative Label | Environmentally Sensitive | ||||

|---|---|---|---|---|---|---|---|

| Average Employment per Enterprise 2019 | Average Employment Growth per Enterprise 2015–2019 | Employment Growth % 2015–2019 | Average Employment per Enterprise 2019 | Average Employment Growth per Enterprise 2015–2019 | Employment Growth % 2015–2019 | ||

| C | Manufacturing industry | 62.1 | 13.1 | 51.40% | 73.49 | 15.19 | 47.30% |

| G | Wholesale and retail | 47.8 | 12.9 | 73.70% | 67.79 | 25.42 | 117.30% |

| J | Information and communications | 37.2 | 15.8 | 129.00% | 91.00 | 40.71 | 203.00% |

| M | Professional, scientific and technical activities | 27 | 7.6 | 90.00% | 41.13 | 8.9 | 55.40% |

| Total general | 50.1 | 12.6 | 74.80% | 49.66 | 12.33 | 73.13% | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Llorca-Ponce, A.; Rius-Sorolla, G.; Ferreiro-Seoane, F.J. Is Innovation a Driver of Sustainability? An Analysis from a Spanish Region. Sustainability 2021, 13, 9286. https://doi.org/10.3390/su13169286

Llorca-Ponce A, Rius-Sorolla G, Ferreiro-Seoane FJ. Is Innovation a Driver of Sustainability? An Analysis from a Spanish Region. Sustainability. 2021; 13(16):9286. https://doi.org/10.3390/su13169286

Chicago/Turabian StyleLlorca-Ponce, Alicia, Gregorio Rius-Sorolla, and Francisco J. Ferreiro-Seoane. 2021. "Is Innovation a Driver of Sustainability? An Analysis from a Spanish Region" Sustainability 13, no. 16: 9286. https://doi.org/10.3390/su13169286