1. Introduction

In recent years, most countries, particularly in the developing world, are focusing on economic expansion, while downplaying ecological improvement. Consequently, different environmental problems such as air pollution, climate change, land loss, biodiversity loss, deforestation, environmental damage, etc., have emerged [

1,

2]. Recently, the international agreement on environmental preservation, action against climate change awareness, and the United Nations’ advocacy for SDGs by the year 2030 [

3] have collectively heightened the interest in green finance [

4,

5]. The implementation of an effective green economy through green finance is a significant outlet for economic growth and sustainability in underdeveloped nations [

6,

7]. Therefore, to ensure sustainable and uniform development, the consciousness of environmental issues should be invoked among academics, bankers, investors, administrations, legislators, advocacy groups, corporations, and communities [

8]. Unfortunately, the extent of the success of environmental sustainability among the various stakeholders remains unclear.

Climate change and its respective environmental implications have become a major issue affecting developed and developing countries[

9]. In a developing and agro-based country such as Bangladesh, it resulted in an economic hardship owing to its high susceptibility to weather changes [

10,

11]. Consequently, several strategies, such as the prevention of environmental degradation and the implementation of sustainable development through formal and coordinated green investments as per global norms, have been enacted [

1] to mitigate the threats and environmental consequences of climate change [

12]. In this regard, banking institutions can play an important role by investing in a variety of environmentally friendly projects, such as renewable energy, clean energy, green industry development and waste management, among others [

2,

8], all of which directly contribute to the nation’s long-term economic development [

1]. Therefore, green finance can be regarded as a vital financial instrument for improving the sustainability performance of an organization and the achievement of SDGs in a country.

The financial industry of Bangladesh is not only dominated by banks [

13] but also non-bank financial institutions (NBFIs), insurance companies, microfinance institutions, and capital market intermediaries. Under the supervision of Bangladesh Bank (the country’s central bank), there are 59 scheduled banks and 5 non-scheduled banks functioning in the country. On the other hand, there are also 34 NBFIs operating businesses in Bangladesh. In comparison to industrialized countries and sophisticated markets, the banking industry meets both the country’s long- and short-term finance demands [

13,

14]. Considering the importance of commercial banks in developing the green economy of Bangladesh, it is imprudent to ignore the financial industry in the economic paradigm shifting toward the integration of environmental factors. In this regard, the banking sector in Bangladesh plays a crucial role in achieving sustainable economic development of the country through its investments in various eco-friendly projects to mitigate the adverse effects of climate change. In addition, many industrial ventures with potentially major negative social or environmental consequences, such as textiles, cement, steel, power, paper, fertilizers, chemicals, and so on rely heavily on banking institutions for funding [

13]. As funders, they have a huge impact on industrial projects, and green banking can therefore play an important role in promoting responsible behavior among businesses [

1,

13]. Green finance can be considered as a critical financial component in ensuring sustainable economic growth in any country. In terms of green financing, private commercial banks (PCBs) are the significant contributors, accounting for around 75% of total green financing in Bangladesh, followed by NBFIs (12%). Hence, it can be noted that banks and NBFIs have been playing a crucial role in the prevention of environmental deterioration as well as the attainment of SDGs in the country through green financing [

1,

12,

13]. As a result, expanding green finance is critical to achieving sustainable economic growth and ecological sustainability, as well as resolving the existing conflict between economic development and environmental conservation [

7,

15].

The concept of green finance, also known as green investments [

1], is widely employed in academia and business, and have a variety of meanings [

5]. Green finance (GF) is a developing concept [

7] that lacks a clear and universal definition [

16]. However, the goal of GF is to balance the advancement of monetary events, environmental stability, and ecological protection to accomplish long-term development [

15]. According to Wang and Zhi [

17], GF is a new monetary phenomenon that combines economic benefits with environmental conservation, and therefore represents the best option for funding environmentally friendly projects and organizations that prioritize environmental protection [

1]. It takes environmental outcomes into account in funding a project and prioritizes investment in various eco-friendly activities, such as renewable energy, waste management (solid and liquid), clean energy, climate change mitigation and adaption strategies, alternative energy, green brick manufacturing, green industry development, paper waste recycling, energy-efficient technology, biodiversity protection, and so on. Therefore, the development of GF is crucial to the banking industry as it aids in the transition to a green economy for better management of concerns, such as climate change, environmental catastrophes, and energy efficiency. The term “sustainability” can be subsequently described as the ability to preserve well-being over an extended and possibly endless length of time. This mostly addresses the environmental aspect of the three pillars of sustainability (social, economic, and environmental); however, it should be noted that the terms “environment performance” and “sustainability performance” are not synonymous [

18]. Sustainability performance refers to a firm’s performance in terms of sustainability across all areas and for all determinants of corporate sustainability [

19]. Consequently, GF has emerged as a new growth point for the promotion of green economic growth, social responsibility and environmental security [

1]. Besides, it also aids banks in improving their sustainability performance [

19]. Several nations, such as China and Bangladesh, have developed financial industry sustainability rules in addition to voluntary industry codes of conduct to address both corporate ethics and financial sector stability [

20]. For example, Bangladesh Bank established the Environmental Risk Management (ERM) policies for banks and financial institutions in 2011 in order to limit investment in various polluting sectors and enhance financing of more environmentally friendly projects. The ERM guidelines are intended to encourage banks and financial institutions to incorporate social and environmental principles into their credit risk management systems, thereby improving social and environmental standards, as well as sustainability assessment and refinancing initiatives for environmentally friendly projects in Bangladesh [

13,

20].

Numerous studies have been recently conducted in the field of GF worldwide [

1,

3,

12,

16,

21,

22,

23,

24,

25,

26,

27,

28,

29,

30,

31,

32], and these studies are mostly centered on GF for sustainable economic development [

23,

24,

25,

31,

32]; the impact of GF on Fintech [

26]; GF trends and opportunities [

3,

16,

22,

28]; the environmental effect of GF reform and innovations [

17,

29]; GF development and sustainability [

1,

27,

33,

34]; GF standards and green bonds [

21,

30]; and GF and sustainable development [

12,

35,

36,

37]. Besides this, a few studies have tried to identify the relationship between GF and the green economy [

7,

38]; GF, carbon intensity, and non-fossil energy consumption, as well as climate change mitigation in the context of N11, BRICS countries, and China [

39,

40]; and sustainability performance [

19,

41]. Although several existing studies have emphasized the practices, prospects, challenges, and sustainable reporting of green financing, bankers’ perceptions regarding the major dimensions of GF and the sources of green financing in the context of Bangladesh [

1,

2,

10,

32] and the effect of GF dimensions (social, economic, and environmental) on the sustainable performance of banks remain largely unexplored. Based on primary data, limited studies exist on PCBs in Bangladesh. On the other hand, sustainable finance has recently emerged as an appealing subject of study in the sustainability literature; nevertheless, studies in developing nations are lacking in the literature [

42]. To the author’s knowledge, no study on the factors affecting the sustainability performance of the banks has been conducted.

Therefore, this study attempts to bridge the research gap in the following ways. First, it depicts the present scenario of green financing in the banks and NBFIs in Bangladesh based on the reports of Bangladesh Bank (BB) from 2015 to 2020. Second, it investigates various aspects of GF—social, economic, and environmental—in the context of PCBs in Bangladesh based on the primary data. Third, the study analyzes the impact of the dimensions of GF on the sustainability performance of the banks. Summarily, the main purpose of the study is to measure the major dimensions of GF (social, economic, and environmental) and their effects on the sustainability performance of banks in the context of PCBs in Bangladesh. The study also highlights the state of green financing in the context of banks and NBFIs in Bangladesh from 2015 to 2020. In achieving the aforementioned goals, this study aims to answer the following two questions: (1) “what is the present state of banks and NBFIs’ green financing of eco-friendly projects in Bangladesh?” and (2) “What are the impacts of the GF dimensions (social, economic, and environmental) on the sustainability performance of banks in Bangladesh based on the knowledge of bankers?”. Furthermore, in comparison with existing works of literature, this study differs in at least three major ways. First, the study presents the current scenario of green financing by banks and NBFIs in Bangladesh based on BB’s reports from 2015 to 2020. Second, different aspects of GF, namely social, economic, and environmental, have all been examined based on the primary data. Third, this study develops a three-dimensional scale of GF to comprehensively quantify its growth and impacts on the sustainability performance of the banking sector in developing countries, such as Bangladesh.

The remainder of the paper is structured as follows:

Section 2 presents recent literature on GF, GF dimensions, and sustainability performance, followed by the hypotheses development of the study.

Section 3 advances the sampling method, data collection, study instruments, and analysis process.

Section 4 deals with the results and findings of the study.

Section 5 delineates the discussion and conclusion of the report, after which major policy consequences and limitations are discussed in

Section 6 and suggestions for future studies in

Section 7. The list of abbreviations and terminologies used in the study are presented in

Table 1.

5. Discussion and Conclusions

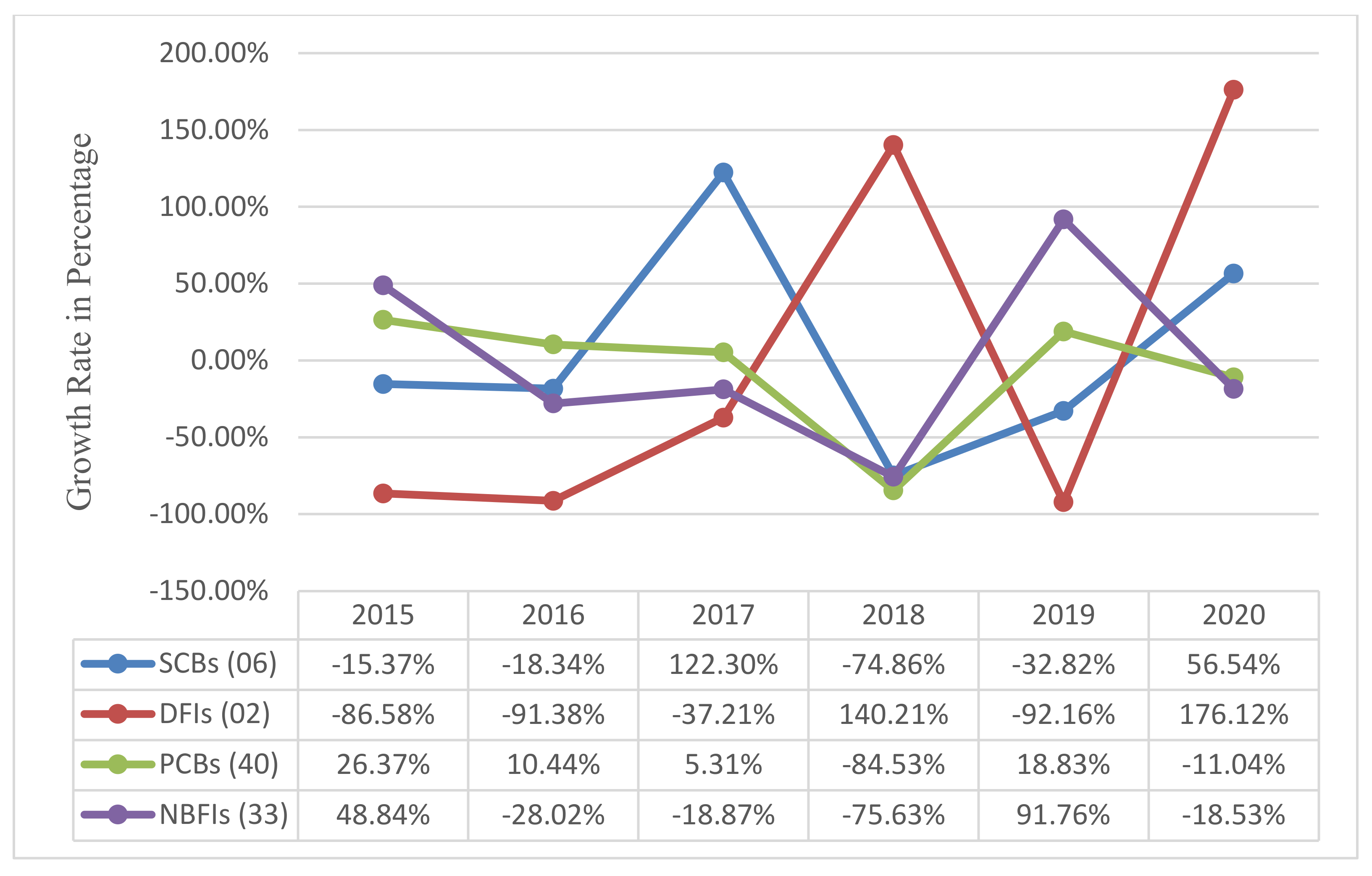

The main purpose of the study is to identify the impact of GF dimensions on banks’ sustainability performance in the context of PCBs in Bangladesh. The study further presents the state of green financing by banks and NBFIs from 2015 to 2020. To assess the effect of GF dimensions on the sustainability performance of the banks, primary data were obtained from bankers of PCBs in Bangladesh. In addition, secondary data were obtained from the published annual reports of the Bangladesh Bank and selected sample banks over the study period. To test the research hypotheses among the study variables, SEM was used. Descriptive statistics, growth rate, and various graphs were further employed to explore the present conditions of green financing by the banks and NBFIs in Bangladesh. The findings of the study indicated that the total green projects financing by the banks and NBFIs stood at BDT 1,805,541.19 million between 2015 and 2020. Amongst the banks and NBFIs, PCBs were observed to be the highest contributor to green financing, accounting for 78.12% of the total green financing in Bangladesh, succeeded by FCBs (17%), NBFIs (4%), SCBs (1.07%), and DFIs (0.03%). These findings are in agreement with past studies [

1,

2,

10,

56]. Furthermore, in comparison with other banks, a positive growth trend of green financing was observed by the PCBs during the study period, except in 2018 and 2020 during which the growth rate decreased by 84.53% and 11.04%, respectively. Additionally, the growth rate of NBFIs was observed to contract by 28.02%, 18.87%, 75.63%, and 18.53% in years 2016, 2017, 2018, and 2020, respectively. These findings are in agreement with other studies [

1,

13]. Therefore, it can be concluded that PCBs play a significant role in “greening” the economy of the country via investment in eco-friendly projects, thereby fostering the attainment of sustainable development goals (SDGs).

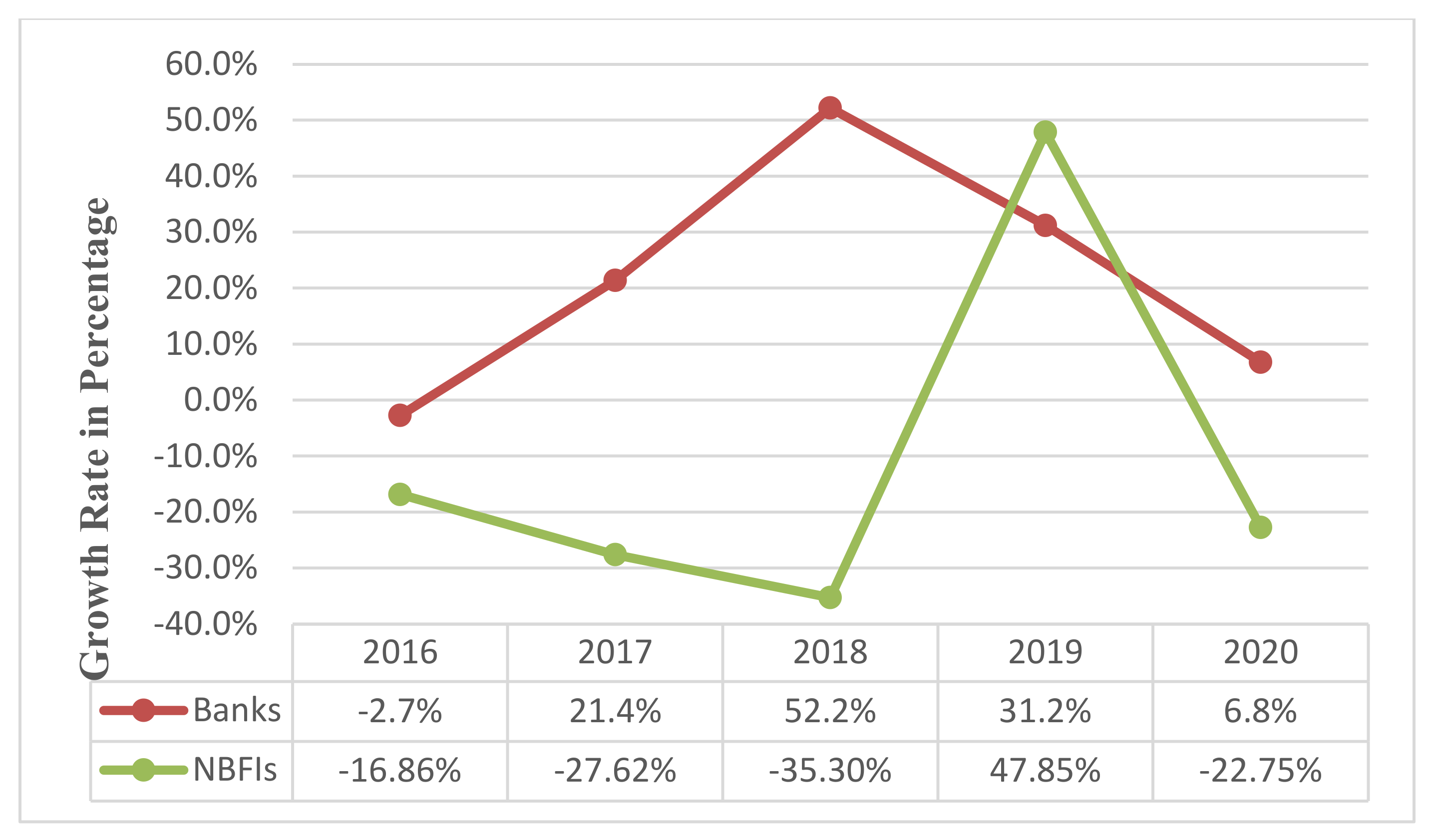

In terms of sector-wise green financing by the banks and NBFIs in Bangladesh during the study period, the findings revealed that the banks were mostly financing green establishments (34.49%), followed by solid and liquid waste management (24.64%), green brick manufacturing (15.43%), and recycling and recyclable products (10.17%). On the other hand, renewable energy, energy efficiency, alternative energy, and others were the least financed by the banks during the study period, accounting for 5.80%, 4.19%, 0.16%, and 5.12%, respectively. The NBFIs generally invested in various eco-friendly projects such as renewable energy (44.73%), green brick manufacturing (14.29%), energy efficiency (14.22%), and green establishment (12.12%). On the contrary, the NBFIs’ least financed areas were waste management (9.01%), recycling and recyclable product (4.16%), others (1.42%), and alternative energy (0.05%), respectively. The study further revealed that the banks experienced a positive growth rate via investment in eco-friendly projects in the last four years, except in 2016 during which a negative growth rate was recorded. In contrast, NBFIs observed a negative growth rate of green financing during the last five years, except in 2019 when a positive growth rate of 47.85% was recorded. These findings are supported by the recently conducted studies [

1,

10,

13]. Therefore, it can be asserted that banking institutions contribute to the sustainable development of the economy via investment in various eco-friendly projects such as green establishment, waste management, green brick manufacturing, recycling and recyclable products, energy efficiency, and the renewable energy sector. To expand the investment opportunities for environmentally friendly products, the BB formed a revolving refinance framework with a worth of BDT 2 billion in 2009 and gradually expanded it to BDT 4 billion [

13]. Currently, the cumulative amount refinanced under the scheme stands at BDT 3117.04 million. The most influencing activities under the scheme were the green industry (40.13%), effluent treatment plant (17.28%), HHK technology in brick kilns (10.90%), safe working environment (9.66%), and biogas (7.41%). On the contrary, solar assembly plant (5.27%), solar home system (4.43%), energy-efficient technology (2.24%), paper waste recycling (1.28%), solar irrigation pump (0.87%), solar mini-grid (0.32%), and vermicompost (0.19%) constituted the least financed activities between 2015 and 2020. Similar findings were also cited from previous studies [

1,

2,

10,

13,

45].

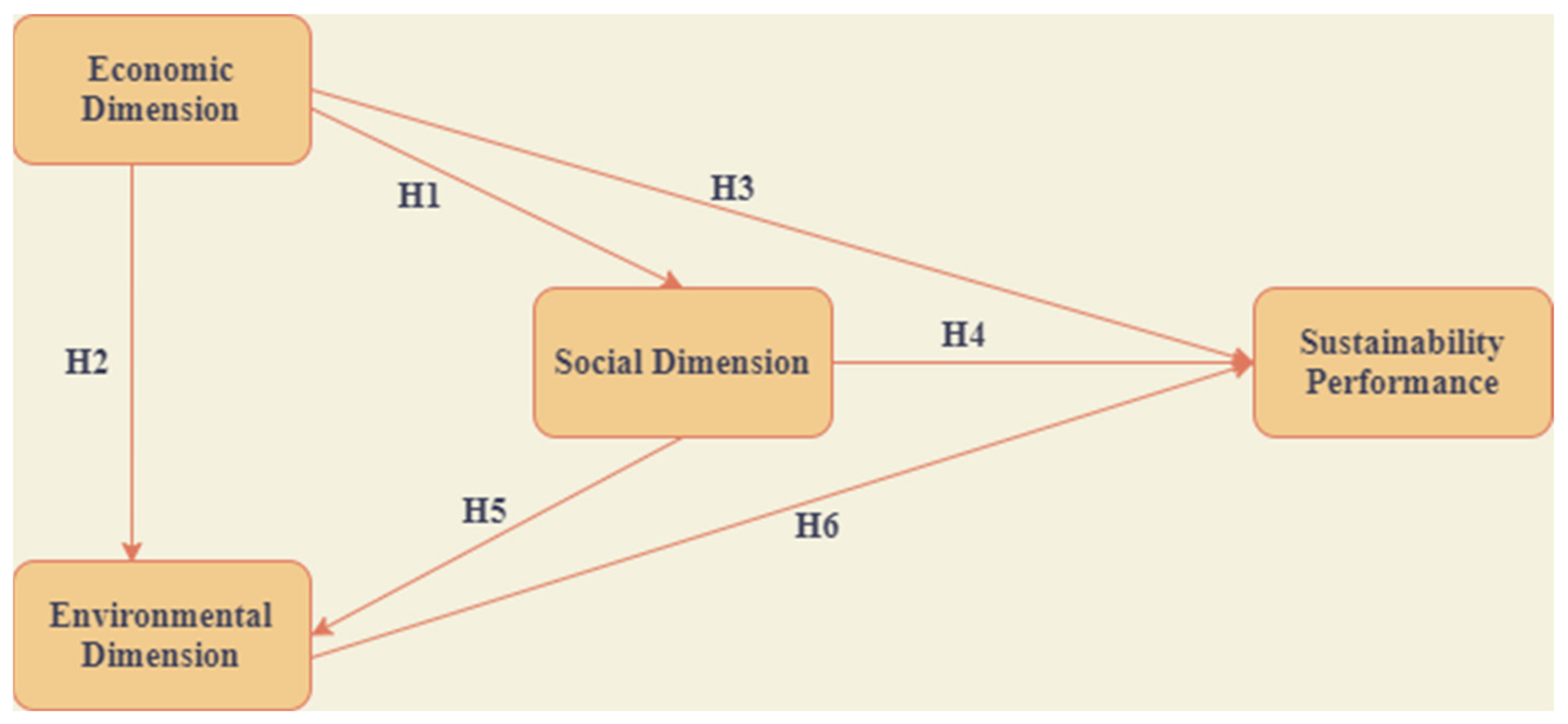

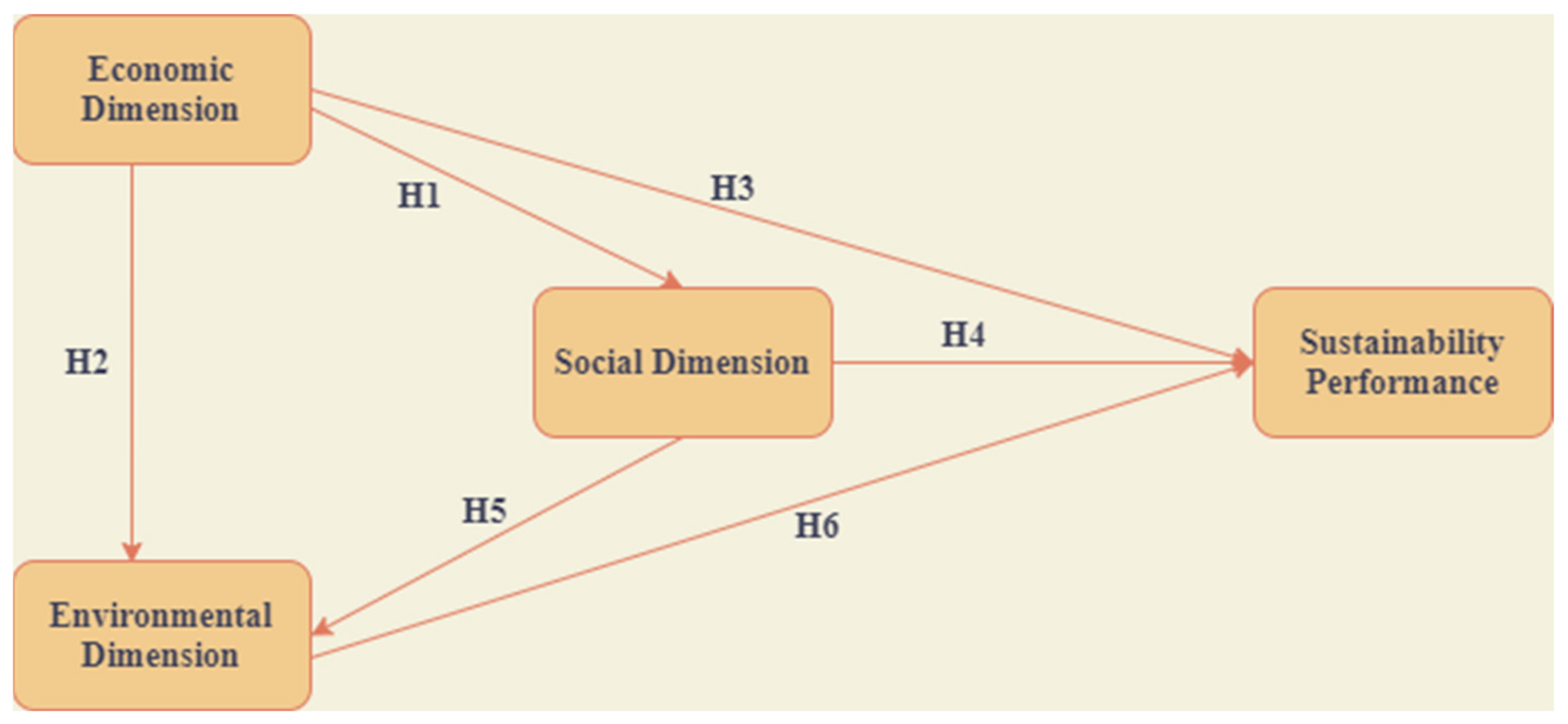

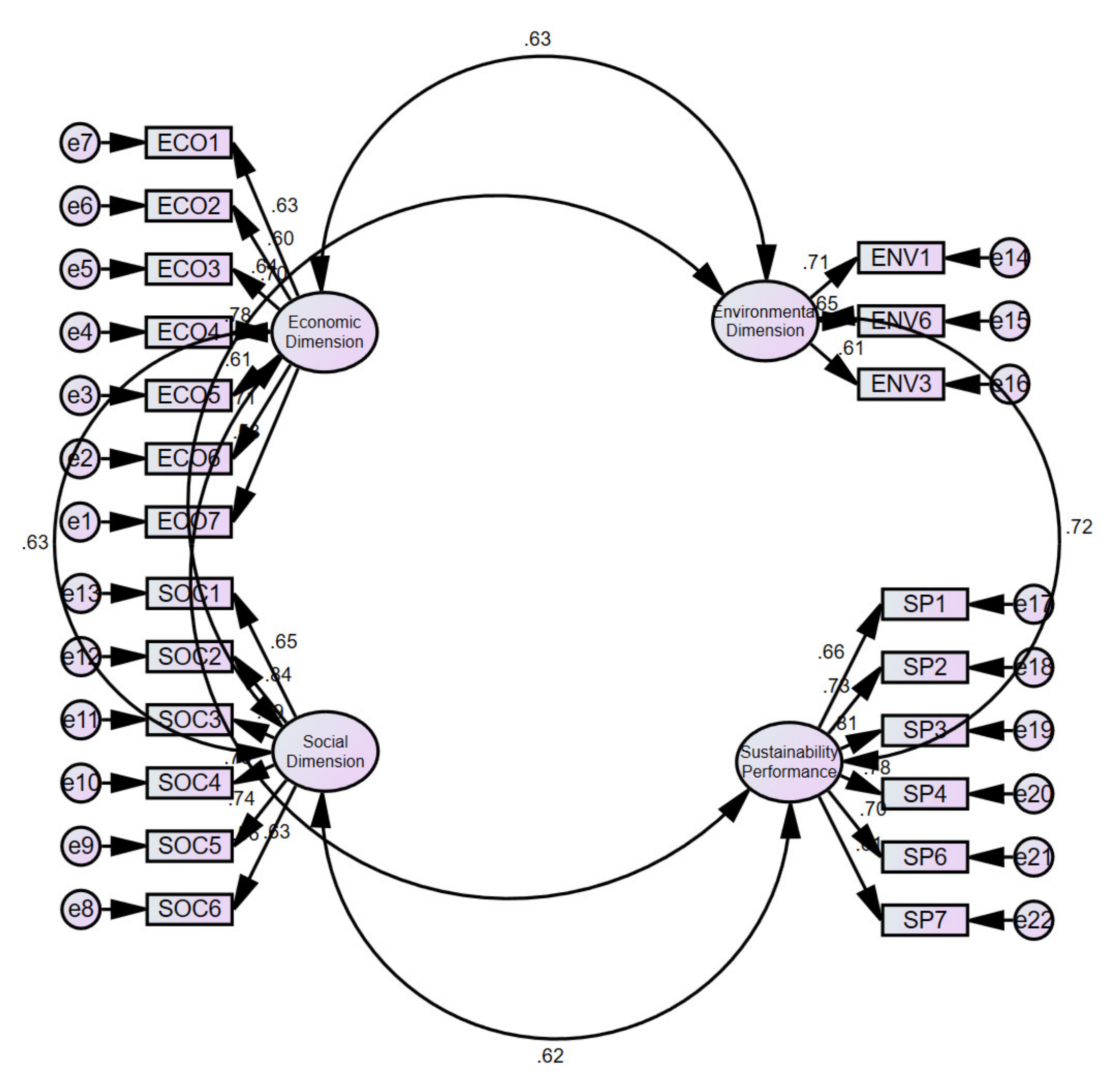

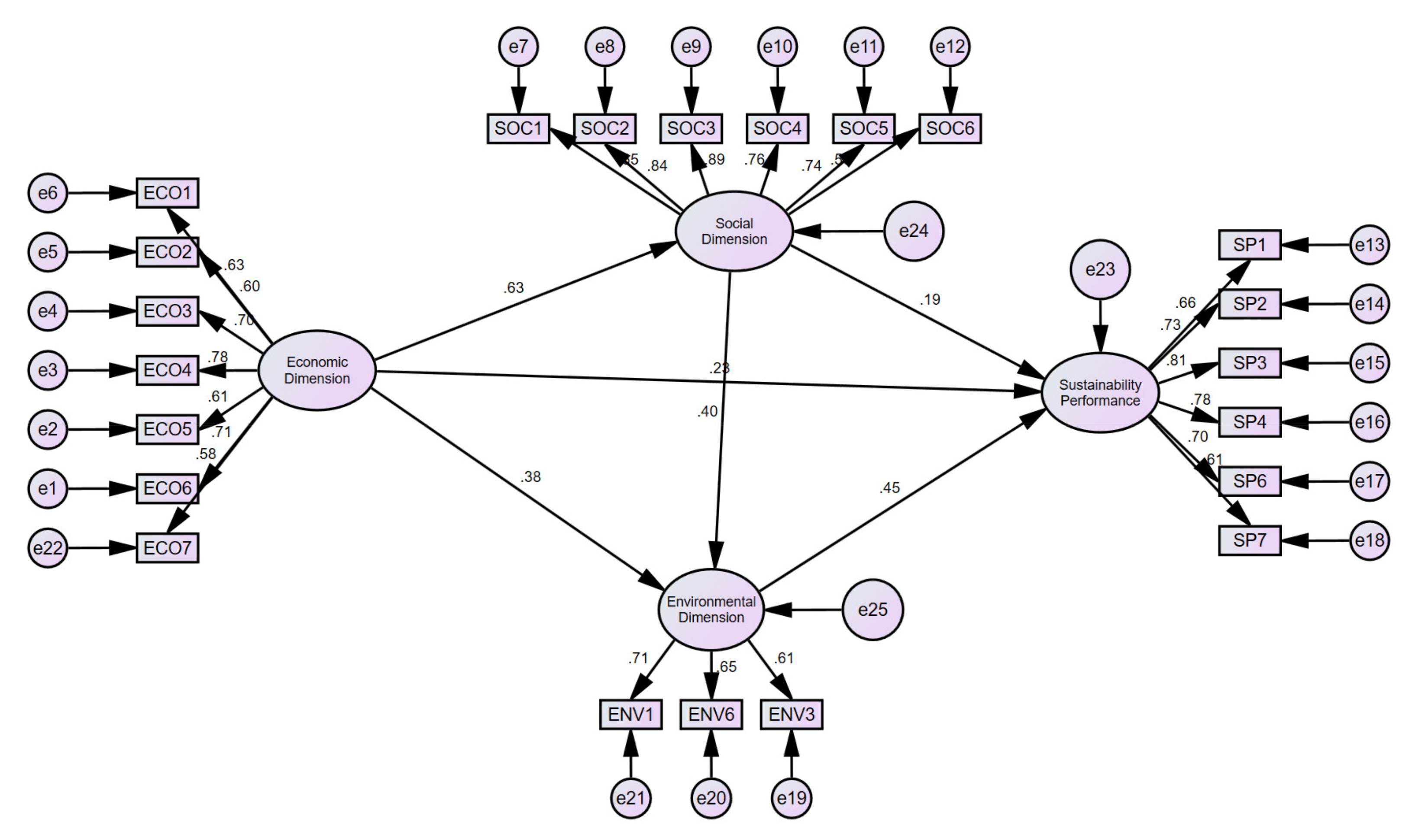

Furthermore, the empirical results indicate the validity of hypothesis 1 that the economic aspect of GF has a positive impact on the social aspect of GF dimensions of PCBs in Bangladesh. Besides, the economic aspect of GF positively influenced the environmental aspect of GF dimensions, thus corroborating hypothesis 2. According to these findings, three dimensions of GF, namely social, economic, and environmental, are linked to the ideas of ESG criteria and SDGs. These findings also imply that the three aspects of GF have significant practical implications for banks and financial institutions to improve their sustainability performance by prioritizing investment in environmentally friendly projects. These observations are consistent with the extant studies [

1,

32]. The study also discovered a strong positive relationship between the economic dimensions of GF and the sustainability performance of banks, thus validating hypothesis 3. It can be concluded that the economic dimension of GF is one of the most significant characteristics of the organization, owing to its interconnectivity with the social and environmental dimensions of GF and substantial impact on the sustainability performance of the banks. Based on our findings, hypothesis 4 is accepted, indicating that the social aspect of GF has a positive and significant impact on the sustainability performance of the banks. It can be concluded from the findings that investing in environmentally friendly projects has a variety of social benefits, such as improved the bank’s image, enhanced trust, stakeholder engagement plans, better customer’s satisfaction, more employee benefits, as well as improved organization’s sustainability performance. In addition, the findings of this study revealed a strong positive relationship between the social and environmental aspects of GF in the context of PCBs in Bangladesh, thus validating hypothesis 5. These findings are consistent with the previously conducted studies [

1,

19,

32]. Therefore, it can be stated that the social element of GF is another key factor impacting the sustainability performance of banks, as it helps to address the internal and external environmental challenges of organizations, such as carbon emissions and energy consumptions. Finally, hypothesis 6 is validated, confirmed by the statistically significant influence of environmental aspect of GF on the sustainability performance of the banks. This finding is corroborated by the study of Malsha et al. [

19], which highlighted that the environmental issues of green banking directly influenced the sustainability performance of the Sri Lankan banking sector. Therefore, it can be inferred that the environmental aspect of GF plays an important role in enhancing the sustainability performance of banks through investment in environmentally favorable projects.

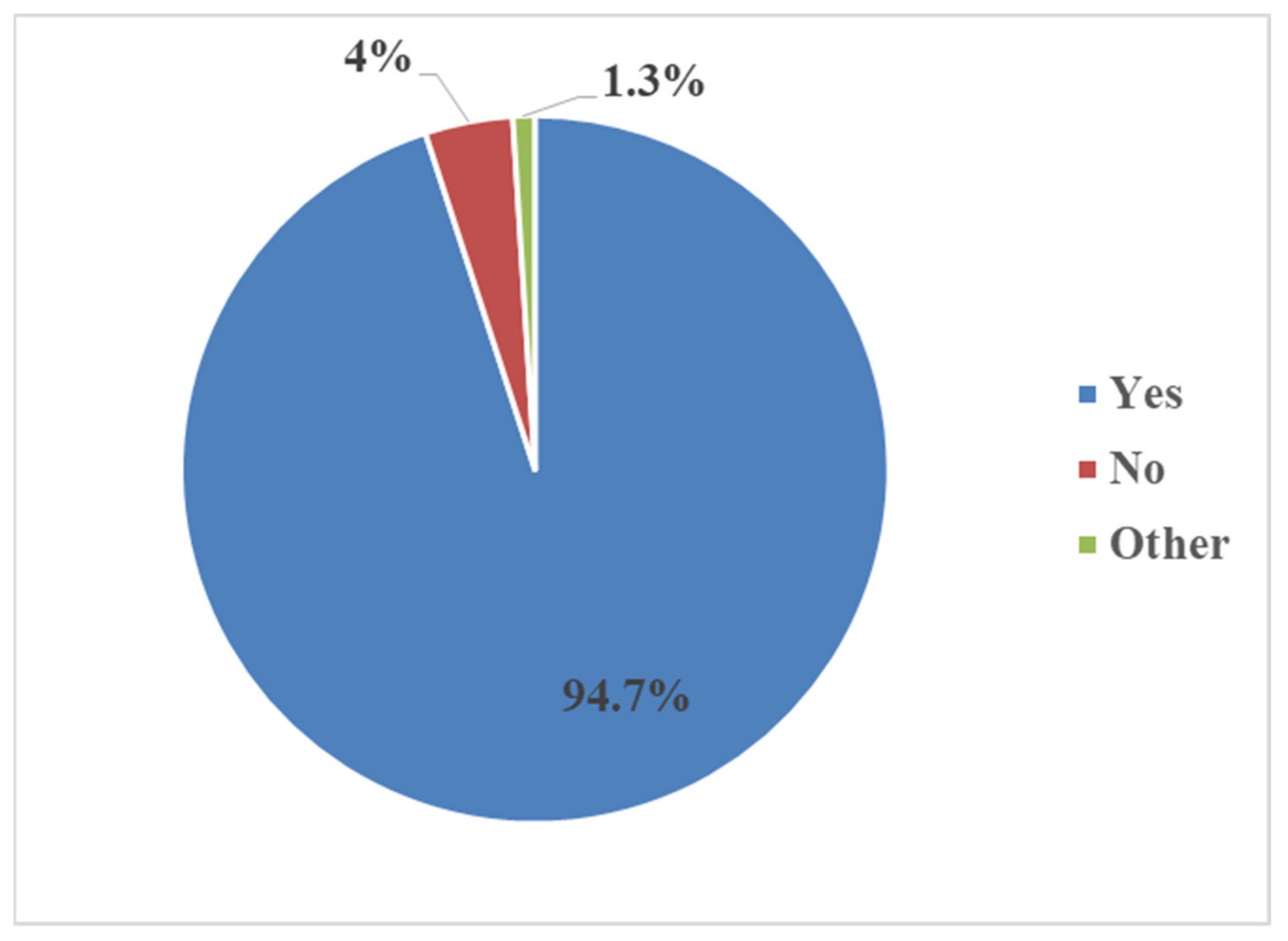

The empirical results indicated that 94.70% of bankers considered green financing to be a significant element in the transient and long-term development plan of the banking industry in Bangladesh. In contrast, only 4% of bankers believed that green financing plays no crucial role in the sustainable growth of their banks. This empirical result is also supported by several studies [

59,

74], which highlighted GF as being one of the essential points for the growth and development of banks and financial institutions. Recently, everyone is concerned with preserving a healthy environment and ensuring an ecological balance. To increase public understanding of environmental issues, the assistance of a variety of stakeholders, including the general public, the news media, environmental organizations, businesses, and the government, are required. All of these stakeholders have benefitted from a business’s sustainability efforts, which have a broader impact on society and the global environment. Banks and financial institutions play a critical role in protecting the environment by financing a variety of eco-friendly projects, such as renewable energy, green sector development, and waste management. Based on our findings, green financing benefits a variety of stakeholders, including bankers, managers, suppliers, academics, and communities, by assisting them in achieving environmental sustainability through the implementation of various strategies such as energy conservation, online banking, paperless transactions, employee engagement programs, and training and development, etc. In summary, green financing is crucial to the country’s long-term sustainable economic expansion and development of the banking sector in Bangladesh.

6. Implications of the Study

6.1. Theoretical Implications

The study’s empirical findings offer a variety of theoretical implications in light of the existing literature on green finance, green finance dimensions, and corporate sustainability performance in the context of banks and financial institutions in emerging economies. This study is regarded as one of the first studies to scientifically assess the various components of green finance (e.g., social, economic, and environmental), as well as their effects on the sustainability performance of banking institutions in Bangladesh. Furthermore, in comparison with existing works of literature, this study differs in at least three major ways. First, the study presents the scenario of green financing by banks and non-bank financial institutions in Bangladesh from 2015 to 2020. Second, different aspects of green finance, namely social, economic, and environmental, were all examined based on the primary data. Third, this study develops a three-dimensional scale of GF to comprehensively quantify its growth and impacts on the sustainability performance of the banking sector in developing countries such as Bangladesh. This could serve as a starting point for future research in the areas of green financing and sustainability performance of banks and financial institutions. Similarly, this study fills a gap in the literature on green financing and corporate sustainability from the perspective of banking sector, thus providing some insight for scholars, academics, managers, bankers, government officials, clients, and investors in developing countries, such as Bangladesh. In addition, the model developed in this study could be extended to new situations or other developing countries, such as Pakistan, India, and China, among others. Researchers can extend or duplicate this research in the future, as the measurement scales have been validated by AMOS statistical analysis, such as structural equation modeling.

6.2. Practical Implications

The empirical findings also provide some useful implications for financial institutions, managers, bankers, government authorities, clients, and investors of Bangladesh to promote green financing for the sustainable economy of the country. This study assists scholars in understanding the impact of GF components—social, economic, and environmental—on banks’ sustainability performance. The following are some of the key policy implications of the study. First, amongst banks and NBFIs in Bangladesh, the PCBs were the highest contributor to green financing, followed by the FCBs. Therefore, the managers of these sample banks should be retained, while the banks should increase their investments in environmentally friendly initiatives to boost the long-term economic prosperity of the country. Second, in terms of sector-wise financing by banks and NBFIs, the study indicated that they invest more in various eco-friendly projects, such as green establishment, waste management, green brick manufacturing, recycling and recyclable products, and energy efficiency. However, there is a need to extend their funding to various energy-related sectors, such as renewable energy, alternative energy, and energy efficiency projects, in order to support the clean energy industry. Third, the empirical data revealed that the three basic elements of GF (social, economic, and environmental) reflect distinct paradigms that are interconnected. Therefore, it is suggested that banks and NBFIs focus more on social activities (local community engagement and development programs, stakeholder engagement programs, brand awareness improvement, and provision of more employee benefits), economic aspects (increment of competitive advantage and long-term benefits, improvement in existing assets, and reduction in the overall risks and cutting down on costs), and environmental aspects (reduction in carbon emissions, energy savings within and outside the organizations, and energy requirements for products and services) to promote green financing in the Bangladeshi banking sector, towards attaining the SDGs. In this regard, the government of Bangladesh can also play a critical role in promoting the benefits of eco-friendly financing amongst the communities towards achieving the nation’s long-term economic development. Fourth, the study identified the social, economic, and environmental aspects of GF as having a positive influence on the sustainability performance of the banks. Consequently, it is proposed that banks should invest more in environmentally friendly initiatives to improve their sustainability performance, strengthen their competitive advantage, and lower their total risks. In this regard, the BB should evaluate and offer relevant instructions to sample banks to improve their sustainability performance and promote green financing as a tool for the country’s long-term economic development. Finally, the output of the study indicated that the majority of the bankers considered green financing to be a significant element in the transient and long-term development plan of the banking industry in Bangladesh. Therefore, it is suggested that the banking institutions should give more priority to green financing, as it is considered an essential point for their growth and development. Although much more is to be done to attain an adequate level of green finance in the country, the banking strategy would determine the probability of achieving green financing in the long run. Hence, the government should provide more rewards and incentives to financial institutions based on the level of their green investments to encourage green financing and, in turn, mitigate environmental deterioration.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}