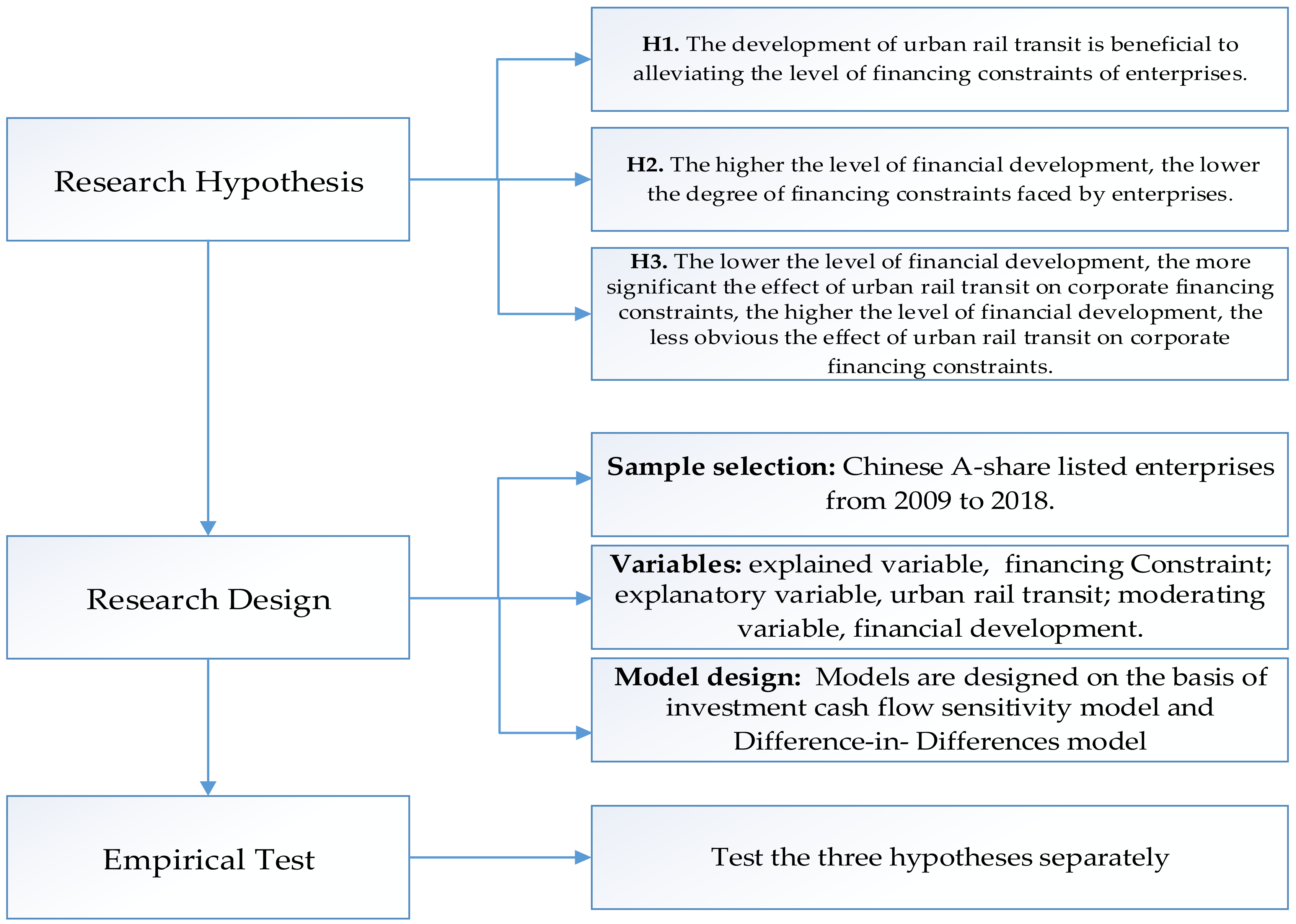

4.1. Descriptive Statistics Analysis

As showed in

Table 2, this paper described the statistical characteristics of each variable. It can be seen that the maximum value of the investment expenditure of the sample companies is 5.490, the minimum value is 0, and the mean value is 0.07, which indicates that there are certain differences in the investment expenditure of different companies, and the investment expenditure of most companies is small. The maximum value of

is 8.860, and the average value is 0.060, indicating that the cash flow of the selected sample enterprise is not particularly high. The average value of the variable

is 0.630, indicating that. as of the end of 2018, 63% of the sample companies have opened urban rail transit in their cities; “

=1” means that the sample year is after the opening year of URT system in the city where the enterprise is located, the mean value of the variable

is 0.490, means that the sample enterprises meeting the condition “

=1”account for 49% of the total sample. The maximum value of

is 2.290, and the minimum value is 0.130, indicating that the financial development level of the sample enterprises is quite different in the regions.

has a maximum value of 31.40 and a minimum value of 0.150, indicating that the investment opportunities faced by the sample companies are quite different. The maximum value of

is 27.78, the minimum value is 17.66, and the average value is 22.02, which means the size difference of the sample enterprises is relatively small. The lowest asset–liability ratio is only 1%, the average is 46%, and the highest is 98%, that is, there are large differences in the capital structure of the sample companies.

4.2. Analysis of Empirical Results

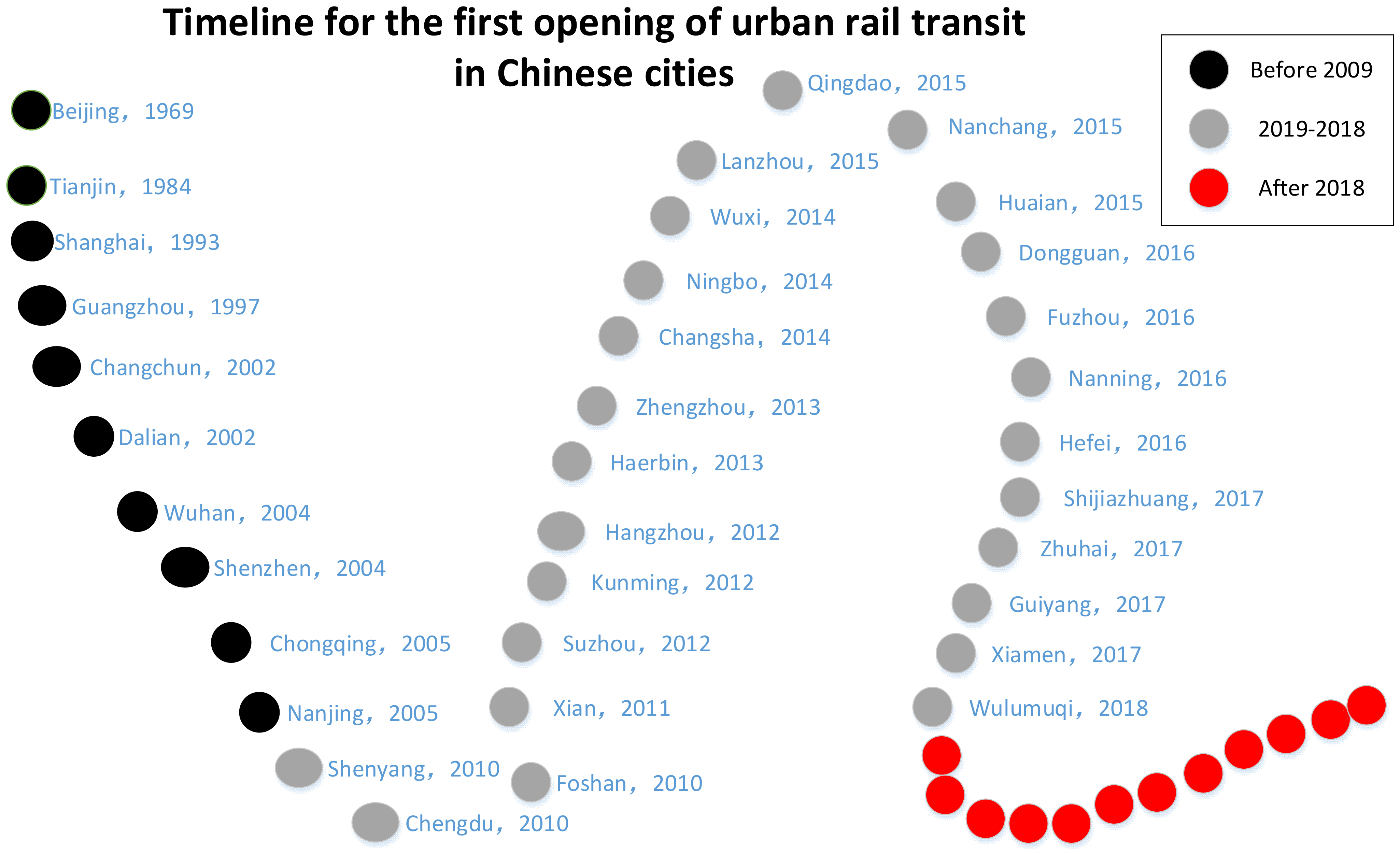

According to the statistics, there are ten cities that have operated urban rail transit before 2009; during 2009–2018, 25 cities have gradually started to operate urban rail transit, as shown in

Figure 2. We divided the sample companies into three groups according to the year in which the urban rail transit started operations: starting operations before 2009, starting operations between 2009 and 2018, and starting operations after 2018.

We perform regression analysis on Equation (2) for full sample enterprises and grouped sample enterprises respectively, shown in

Table 3. R-squared in the fourth column is the largest, indicating that the fitting effect of this group of samples is the best, that is, in the sample of urban rail transit opened after 2018, the degree of interpretation of the dependent variable by the regression equation is 68.8%. Column (1) in

Table 3 displays the regression result of the Equation (2) of the full sample of companies. The coefficient of investment-cash flow sensitivity is 0.237 and significant at the statistical level of 1%, meaning that companies have financing constraints on the whole. In the grouped sample, the coefficient

of column (2) is not significant, the coefficient

of columns (3) and (4) are both significantly positive at the 1% level, and the coefficient value of column (4) is the largest. It can be considered that among the cities where urban rail transit was opened earlier, the scale of the city is larger, the level of economic development is higher, the external economic and policy environment of the company is better, and the investment of the company is not sensitive to cash flow, that is, the financing constraints faced by the enterprise are relatively small. However, the later the year of URT system is opened, the more sensitive the company’s investment to cash flow, indicating that when the local economic development level is more backward, the degree of financing constraints faced by the company is relatively greater.

To verify the influence of the URT system on the financing constraints, first, a regression analysis of Equation (3) was performed on a full sample of enterprises, and the regression results are shown in column (1) of

Table 4. R-squared is 0.226, compared with column 1 in

Table 3, the value of R2 becomes larger, indicating that the model fits better after adding variable

. The coefficient of the variable

is significantly negative (−0.286) at the 1% level, that is, under the influence of URT system, the sensitivity of corporate investment to cash flow has weakened, indicating that the operation of URT system is beneficial to alleviate the financing constraints of enterprises, confirming Hypothesis 1.

To verify the influence of financial development level on corporate financing constraints, a regression analysis of Equation (4) was performed on a full sample of enterprises, and the regression results are shown in column (2) of

Table 4. R-squared is 0.195, compared with column 1 in

Table 3, the value of R2 becomes larger, indicating that the model fits better after adding variable

. The coefficient of the variable

is significantly negative (−0.0975) at the 1% level. That is, the sensitivity of investment cash flow of enterprises is weakened in view of the influence of financial development, indicating that the higher the level of urban financial development, the lower the degree of financing constraints of enterprises, which confirms Hypothesis 2.

To test the moderating effect of the financial development level on the relationship between urban rail transit and corporate financing constraints, a regression analysis of Equation (5) was performed on a full sample of companies. The results are shown in column (3) of

Table 4. R-squared is 0.227, compared with column 1 in

Table 3, the value of R2 becomes larger, indicating that the model fits better after adding

. The coefficient

of

is significantly positive at the level of 5% (0.0985), which indicates that under the effect of financial development level, urban rail transit does not play a role in reducing the sensitivity of enterprises to the cash flow of investment. In other words, a higher level of financial development inhibits the alleviating effect of URT system on the financing constraints of enterprises. This result proves Hypothesis 3.

Regarding Hypothesis 1, few documents directly study the relationship between URT system and financing constraints. However, studies have shown that URT will promote the occurrence of industrial agglomeration, and some scholars have proved that industrial agglomeration is beneficial to alleviating the financing difficulties. The conclusion of this article directly verifies the influence of URT on corporate financing. For Hypothesis 2, the research results of this paper are consistent with existing research conclusions, that is, the higher the level of financial development, the lower the degree of financing constraints of enterprises. Regarding Hypothesis 3, few studies have put together urban rail transit, financial development level, and corporate financing constraints for discussion. Some scholars believe that the benefits of industrial agglomeration are not monotonically increasing, but excessive agglomeration will occur. By analogy with the URT system, we conducted the test of Hypothesis 3, and the conclusion is also in line with expectations, that is, the influence of URT system on corporate financing constraints will vary depending on the level of financial development. The conclusion of this paper enriches the theoretical research of urban rail transit.

4.4. Further Test

As an economic unit, a kind of industry is not only an integral part of the national economy but also a collection of similar enterprises. Scholars often use industry association theory to study the connections between industries. Hirschman pointed out that forward correlation and backward correlation are the most basic movement mode of correlation, and the correlation in the economic development of the whole industry can be measured by the correlation degree between local industries. The operation of the URT system will promote the development of some related up and downstream industries [

16]. There will be complex and varied technical and economic connections among these related industries, and these connections will also be strong and weak due to different ways of the division of labor and cooperation. The correlation intensity between the URT system and different categories of industries is also different. On the base of industrial association theory, some scholars have calculated the correlation measure coefficient between the URT system and upstream and downstream industries by using the input-output method. The greater the value of this coefficient, the stronger the correlation between industry and urban rail transit is [

48]. For the enterprises with a strong correlation with the urban rail transit industry, the convenient conditions and positive influence created by urban rail transit should be greater, the industrial aggregation effect should be more obvious, and the alleviating effect of the URT system on the financing constraint of enterprises should be more significant.

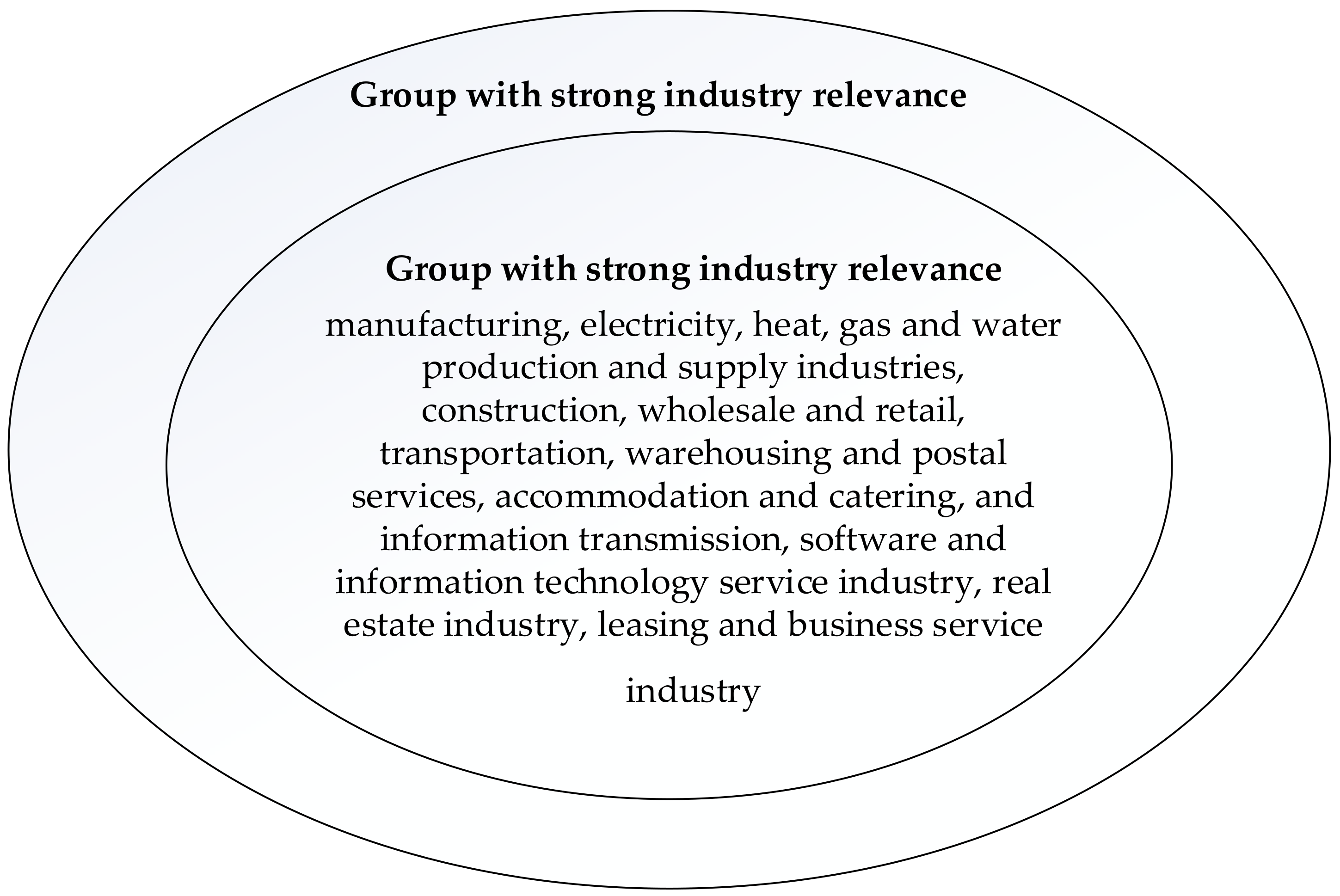

To figure out if the alleviating effect of the URT system on the financing constraint of enterprises differs among different industries, this paper, referring to existing studies, divided the entire sample of enterprises into strong industry correlation and weak industry correlation, according to the correlation between the industry types and the URT industry.

Specifically, according to the “Classification of National Economic Industries” (GB/T 4754—2017), the manufacturing, electricity, heat sectors, etc., are regarded as the groups with strong industry relevance (As shown in

Figure 3), and other industries are regarded as the groups with weaker industry relevance. After grouping, regression analysis was conducted on Equation (3) respectively, and TobinQ value and operating income growth rate were successively used to replace enterprise investment opportunities for testing. The regression results are shown in

Table 7. Compared with the strong industry correlation sample group, the value of R-squared are larger in the weak industry correlation sample group, indicating that the Weak industry correlation sample group has a better fit.

The results show that the coefficients of are significantly negative (−0.271, −0.305) at the 1% level in the samples with strong industry correlation, whether the TobinQ value or the growth rate of operating income is used to measure the investment opportunity. However, in the sample with weak industry correlation, the coefficient of the cross term is not significant. It shows that the urban rail transit has a certain alleviating effect on the financing constraint of the sample enterprises with strong industry correlation, but the influence on the sample enterprises with weak industry correlation is not obvious.

{kind=link}

{kind=link}

{kind=link}