The Impact of Airport Managerial Type and Airline Market Share on Airport Efficiency

Abstract

1. Introduction

2. Theory and Hypothesis

2.1. Integrated Management of Multiple Airports and Knowledge Transfer

2.2. Centralized Management of Multiple Airports and Scale and Scope Economies

2.3. Bargaining Power of Multiple Airports

2.4. Market Share of Dominant Carrier and Airport Efficiency

3. Methodology

3.1. Data

3.2. Model

3.2.1. Data Envelopment Analysis (DEA)

3.2.2. Coarsened Exact Matching (CEM)

3.3. Variable

3.3.1. Dependent Variables

3.3.2. Independent Variables

3.3.3. Control Variables

4. Results

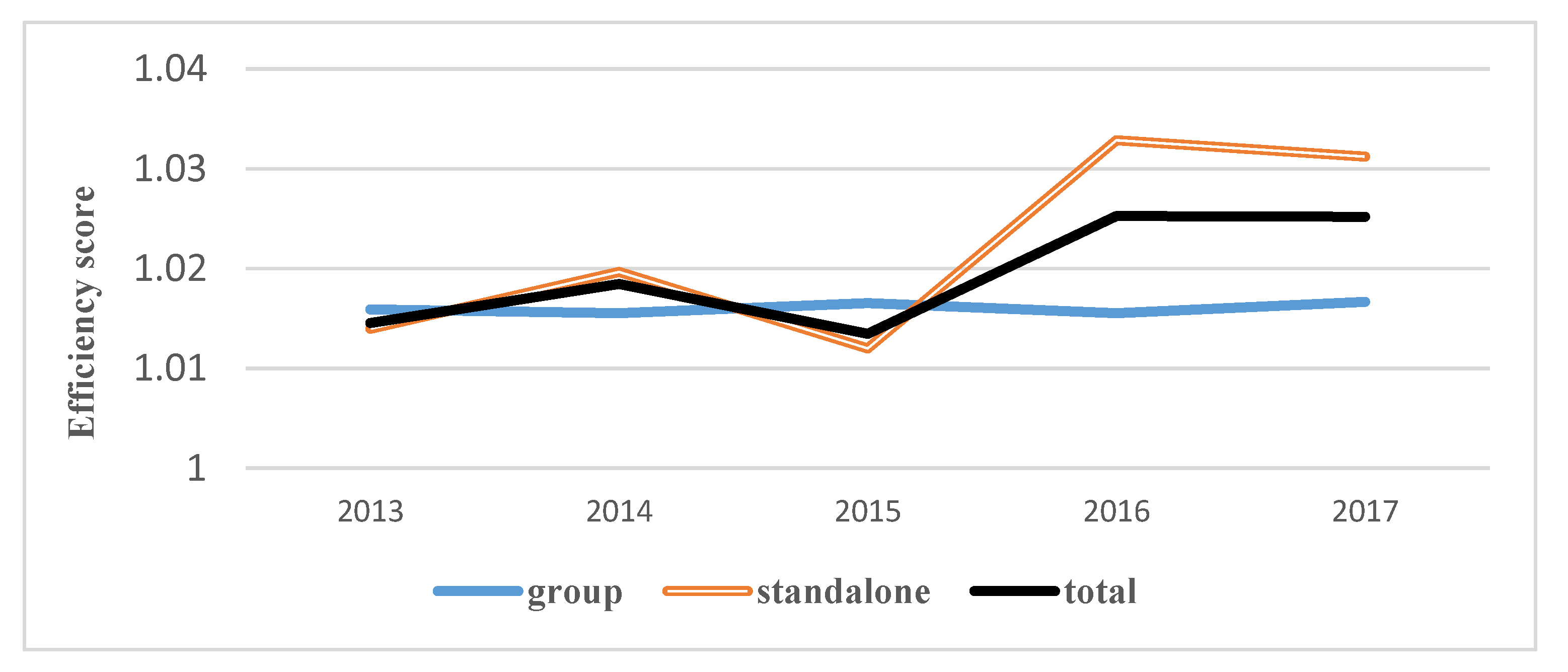

4.1. Efficiency of Group Airports and Standalone Analysis

4.2. Airline Dominance and Airport Efficiency

5. Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Assaf, A.G.; Gillen, D.; Tsionas, E.G. Understanding relative efficiency among airports: A general dynamic model for distinguishing technical and allocative efficiency. Transp. Res. Part B Methodol. 2014, 70, 18–34. [Google Scholar] [CrossRef]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Fragoudaki, A.; Giokas, D.; Glyptou, K. Efficiency and productivity changes in Greek airports during the crisis years 2010–2014. J. Air Transp. Manag. 2016, 57, 306–315. [Google Scholar] [CrossRef]

- Lai, P.; Potter, A.T.; Beynon, M.J.; Beresford, A.K.C. Evaluating the efficiency performance of airports using an integrated AHP/DEA-AR technique. Transp. Policy 2015, 42, 75–85. [Google Scholar] [CrossRef]

- Gillen, D.; Lall, A. Developing measures of airport productivity and performance: An application of data envelopment analysis. Transp. Res. Part E: Logist. Transp. Rev. 1997, 33, 261–273. [Google Scholar] [CrossRef]

- Adler, N.; Ülkü, T.; Yazhemsky, E. Small regional airport sustainability: Lessons from benchmarking. J. Air Transp. Manag. 2013, 33, 22–31. [Google Scholar] [CrossRef]

- Ferreira, D.C.; Marques, R.C.; Pedro, M.I. Comparing efficiency of holding business model and individual management model of airports. J. Air Transp. Manag. 2016, 57, 168–183. [Google Scholar] [CrossRef]

- Yoo, S.-C.; Meng, J.; Lim, S. An analysis of the performance of global major airports using two-stage network DEA model. J. Korean Soc. Qual. Manag. 2017, 45, 65–92. [Google Scholar] [CrossRef]

- Oum, T.H.; Fu, X. Impacts of airports on airline competition: Focus on airport performance and airport-airline vertical relations. Int. Transp. Forum 2008, 13, 123–137. [Google Scholar]

- Chang, Y.-C.; Yu, M.-M.; Chen, P.-C. Evaluating the performance of Chinese airports. J. Air Transp. Manag. 2013, 31, 19–21. [Google Scholar] [CrossRef]

- Ha, H.-K.; Wan, Y.; Yoshida, Y.; Zhang, A. Airline market structure and airport efficiency: Evidence from major Northeast Asian airports. J. Air Transp. Manag. 2013, 33, 32–42. [Google Scholar] [CrossRef]

- Pasaribu, B.I.; Afrianti, A.; Gumilar, G.; Rizanti, H.; Rohajawati, S. Knowledge Transfer: A Conceptual Model and Facilitating Feature in Start-up Business. Procedia Comput. Sci. 2017, 116, 259–266. [Google Scholar] [CrossRef]

- Lahti, R.K.; Beyerlein, M.M. Knowledge transfer and management consulting: A look at “the firm”. Vez. Manag. Bus. J. 2000, 31, 91–99. [Google Scholar] [CrossRef]

- Argote, L.; Ingram, P. Knowledge Transfer: A Basis for Competitive Advantage in Firms. Organ. Behav. Hum. Decis. Process. 2000, 82, 150–169. [Google Scholar] [CrossRef]

- Kogut, B.; Zander, U. Knowledge of the Firm and the Evolutionary Theory of the Multinational Corporation. J. Int. Bus. Stud. 1993, 24, 625–645. [Google Scholar] [CrossRef]

- Darr, E.D.; Argote, L.; Epple, D. The Acquisition, Transfer, and Depreciation of Knowledge in Service Organizations: Productivity in Franchises. Manag. Sci. 1995, 41, 1750–1762. [Google Scholar] [CrossRef]

- Fageda, X.; Voltes-Dorta, A. Efficiency and Profitability of Spanish Airports: A Composite Nonstandard Profit Function Approach; Universitat de Barcelona: Barcelona, Spain, 2012. [Google Scholar]

- Francis, G.; Humphreys, I.; Fry, J. The benchmarking of airport performance. J. Air Transp. Manag. 2002, 8, 239–247. [Google Scholar] [CrossRef]

- Müller, J.; Niemeier, H.M.; Adler, N. Comparative Study (Benchmarking) on the Efficiency of Avinors Airport Operations; Norwegian Ministry of Transport and Communication: Berlin, Germay, 2012. [Google Scholar]

- Von Hippel, E. “Sticky Information” and the Locus of Problem Solving: Implications for Innovation. Manag. Sci. 1994, 40, 429–439. [Google Scholar] [CrossRef]

- Bitzan, J.D.; James, H.P. The Economics of Airport Operations (Advances in Airline Economics); Emerald Publishing Limited: Bingley, UK, 2017; Volume 6, pp. 1–14. [Google Scholar]

- Doganis, R. Airport Business; Routledge: London, UK; New York, NY, USA, 1992. [Google Scholar]

- ITF. Competitive Interaction between Airports, Airlines and High-Speed Rail. In Proceedings of the ITF Round Tables, Paris, France, 2–3 October 2008. [Google Scholar]

- Červinka, M. Small regional airport performance and Low cost carrier operations. Transp. Res. Procedia 2017, 28, 51–58. [Google Scholar] [CrossRef]

- Bölke, S. Strategic Marketing Approaches within Airline Management: How the Passenger Market Causes the Business Concepts of Full Service Network Carriers, Low Cost Carriers, Regional Carriers and Leisure Carriers to Overlap; Anchor Academic Publishing: Hamburg, Germany, 2015. [Google Scholar]

- Borenstein, S. Hubs and High Fares: Dominance and Market Power in the U.S. Airline Industry. RAND J. Econ. 1989, 20, 344. [Google Scholar] [CrossRef]

- Fu, X.; Zhang, A. Effects of Airport Concession Revenue Sharing on Airline Competition and Social Welfare. J. Transp. Econ. Policy 2010, 44, 119–138. [Google Scholar]

- Forsyth, P.; Niemeier, H.-M.; Wolf, H. Airport alliances and mergers—Structural change in the airport industry? J. Air Transp. Manag. 2011, 17, 49–56. [Google Scholar] [CrossRef]

- Albers, S.; Koch, B.; Ruff, C. Strategic alliances between airlines and airports—theoretical assessment and practical evidence. J. Air Transp. Manag. 2005, 11, 49–58. [Google Scholar] [CrossRef]

- Banker, R.D.; Cooper, W.W.; Seiford, L.M.; Thrall, R.M.; Zhu, J. Returns to scale in different DEA models. Eur. J. Oper. Res. 2004, 154, 345–362. [Google Scholar] [CrossRef]

- Ülkü, T. A comparative efficiency analysis of Spanish and Turkish airports. J. Air Transp. Manag. 2015, 46, 56–68. [Google Scholar] [CrossRef]

- Örkcü, H.H.; Balıkçı, C.; Dogan, M.I.; Genç, A. An evaluation of the operational efficiency of turkish airports using data envelopment analysis and the Malmquist productivity index: 2009–2014 case. Transp. Policy 2016, 48, 92–104. [Google Scholar] [CrossRef]

- Oum, T.H.; Adler, N.; Yu, C. Privatization, corporatization, ownership forms and their effects on the performance of the world’s major airports. J. Air Transp. Manag. 2006, 12, 109–121. [Google Scholar] [CrossRef]

- Iacus, S.M.; King, G.; Porro, G. CEM: Software for Coarsened Exact Matching. J. Stat. Softw. 2009, 30, 1–27. [Google Scholar] [CrossRef]

- Heckman, J.J.; Vytlacil, E.J. Chapter 70 Econometric Evaluation of Social Programs, Part I: Causal Models, Structural Models and Econometric Policy Evaluation. Handb. Econom. 2007, 6, 4779–4874. [Google Scholar] [CrossRef]

- Kim, S. Understanding and Using the CEM Method; Focusing on the Effect of Public R&D Subsidies. Korean J. Econ. Stud. 2016, 64, 125–151. [Google Scholar]

- Qin, S. Comparing the Matching Properties of Coarsened Exact Matching, Propensity Score Matching, and Genetic Matching in a Nationwide Data and a Simulation Experiment; University of Georgia: Athens, GA, USA, 2011. [Google Scholar]

- Ho, D.E.; Imai, K.; King, G.; Stuart, E.A. Matching as Nonparametric Preprocessing for Reducing Model Dependence in Parametric Causal Inference. Political Anal. 2007, 15, 199–236. [Google Scholar] [CrossRef]

- Craig, S.; Airola, J.; Tipu, M. The Effect of Institutional form on Airport Governance Efficiency; Unpublished Manuscript; Department of Economics, University of Houston: Houston, TX, USA, 2005. [Google Scholar]

- Wanke, P.F. Efficiency of Brazil’s airports: Evidences from bootstrapped DEA and FDH estimates. J. Air Transp. Manag. 2012, 23, 47–53. [Google Scholar] [CrossRef]

{kind=link}

| Management Model | Region | Number of Airports |

|---|---|---|

| Group | Asia/pacific | 19 |

| Europe | 26 | |

| Subtotal | 45 | |

| Standalone | Asia/pacific | 34 |

| Europe | 45 | |

| Subtotal | 79 | |

| Total | 124 | |

| Author | Sample Airports | Input Variables | Output Variables |

|---|---|---|---|

| [11] | 11 Northeast Asian airports | runway length terminal size number of employees | tonnage of the combined passengers and cargo |

| [31] | 41 Spanish airports 32 Turkish airports | staff costs operating costs total runway area | number of passengers air traffic movements tons of cargo commercial revenues |

| [7] | Total 145 airports: 51 in Europe 26 in Asia/Pacific 68 North America. | boarding gates (no.) employees (no.) total length of runways (m) other operational costs (V) | flight numbers passenger numbers |

| [39] | 52 US airports | governmental structure | number of flights number of passengers tonnage of cargo and mail |

| [3] | 39 Greek airports | runway length apron size passenger terminal size | aircraft movements passenger numbers tons of cargo |

| [40] | 65 Brazilian airports | number of landings and takeoffs | Passengers cargo and of mail. |

| [32] | 21 Turkish airports | number of runways, dimension of runway units (m), passenger terminal areas | number of flights passenger throughputs cargo throughputs |

| Variable | Measure | Definition | |

|---|---|---|---|

| Input | Number of employees | In persons | Total number of employees of airport operator |

| Terminal size | Total area of passenger and cargo terminal | ||

| Number of gates | unit | Total number of gates for enplanement and deplanement | |

| Variable cost | USD | Variable cost per passenger | |

| Output | Passenger throughput | In persons | Number of annual passengers handled at airport |

| Cargo throughput | Ton | Tons of annual cargos handled at airport | |

| Net profit | Millions USD | Net profit/Total revenue | |

| Operating margin | Operating profit/Total revenue |

| Variable | Obs | Mean | Std. Dev. | Min | Max | |

|---|---|---|---|---|---|---|

| Input | Employees | 103 | 1547.592 | 2360.143 | 19 | 18,120 |

| Terminal size | 113 | 284,417.2 | 372,679.2 | 7257 | 2,122,474 | |

| Gates | 123 | 58.03252 | 47.14486 | 5 | 228 | |

| Variable costs | 97 | 11 | 7.026735 | 2 | 39 | |

| Output | Passengers | 123 | 24,849.06 | 22,237.48 | 973 | 95,786 |

| Cargo | 114 | 468,095.6 | 824,184.6 | 430 | 4,600,000 | |

| Net operating profit (millions) | 94 | 283.2185 | 390.405 | −27 | 2358 | |

| Operating income | 91 | 47.45055 | 17.02148 | 13 | 80.8 |

| Variable | Definition | |

|---|---|---|

| Independent Variables | ||

| Managerial type | Group vs. standalone | If an airport is a group airport or standalone airport |

| Market power | Market share of dominant carrier | Passenger share of dominant carrier at an airport |

| Control Variables | ||

| Governance | State share | State share of an airport |

| Competition | Competition | If there exist other airports competing with the airport in question |

| Traffic share | International traffic share | International traffic share |

| Mean | S.D. | (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|---|---|

| (1) Airport efficiency | 1.037 | 0.044 | 1 | |||||

| (2) Ownership transfer | 0.496 | 0.5 | 0.052 | 1 | ||||

| (3) Intl pax share | 63.449 | 32.07 | 0.166 * | 0.024 | 1 | |||

| (4) Airport competition | 0.374 | 0.484 | −0.079 | 0.006 | 0.078 | 1 | ||

| (5) Group/Standalone | 0.363 | 0.481 | 0.090 | 0.023 | −0.135 * | 0.250 * | 1 | |

| (6) Dominant carriers | 40.194 | 17.07 | −0.021 | −0.015 | 0.047 | 0.080 | −0.008 | 1 |

| Number of units | Treated | Untreated |

|---|---|---|

| Total units | 208 | 116 |

| Matched | 60 | 46 |

| Unmatched | 148 | 70 |

| Total strata | 109 | |

| Matched strata | 20 | |

| Variables | L1 |

|---|---|

| Multivariate | 0.26293996 |

| Ownership transfer | 2.8 × 10−17 |

| International passenger share | 0.04348 |

| Airport competition | 1.4 × 10−17 |

| Dominant carrier | 0.08489 |

| VARIABLES | Before CEM | After CEM |

|---|---|---|

| Treated (0:standalone) 11:group | −0.00192 | −0.0189 *** |

| (0.00360) | (0.00667) | |

| Market share of dominant carrier | −0.00017 | −0.000978 *** |

| carriers | (0.00011) | (0.00026) |

| Intl pax share | 0.00016 *** | 0.00042 *** |

| (5.42 × 10−5) | (0.000101) | |

| Airport competition | −0.0119 *** | −0.0177 ** |

| (0.00360) | (0.00821) | |

| Ownership transfer | 0.0006 | −0.00299 |

| (0.0033) | (0.00724) | |

| Constant | 1.021 *** | 1.047 *** |

| (0.00586) | (0.0121) | |

| Observations | 324 | 106 |

| R-squared | 0.069 | 0.237 |

| Variables | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| Airline dominance | −0.000423 *** | −0.000162 | |

| (0.000118) | (0.000158) | ||

| Ownership transfer | 0.000763 | −0.00103 | 3.34 × 10−5 |

| (0.00334) | (0.00393) | (0.00458) | |

| International pax share | 0.000148 *** | 0.000314 *** | 0.000131 * |

| (5.38 × 10−5) | (6.73 × 10−5) | (7.35 × 10−5) | |

| Airport competition | −0.0126 *** | 0.00865 ** | −0.0247 *** |

| (0.00347) | (0.00386) | (0.00524) | |

| Constant | 1.014 *** | 1.009 *** | 1.026 *** |

| (0.00438) | (0.00603) | (0.00848) | |

| Observations | 324 | 116 | 208 |

| R-squared | 0.060 | 0.212 | 0.106 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Park, J.H.; Kim, J.H. The Impact of Airport Managerial Type and Airline Market Share on Airport Efficiency. Sustainability 2021, 13, 981. https://doi.org/10.3390/su13020981

Park JH, Kim JH. The Impact of Airport Managerial Type and Airline Market Share on Airport Efficiency. Sustainability. 2021; 13(2):981. https://doi.org/10.3390/su13020981

Chicago/Turabian StylePark, Jae Hee, and Ji Hee Kim. 2021. "The Impact of Airport Managerial Type and Airline Market Share on Airport Efficiency" Sustainability 13, no. 2: 981. https://doi.org/10.3390/su13020981

APA StylePark, J. H., & Kim, J. H. (2021). The Impact of Airport Managerial Type and Airline Market Share on Airport Efficiency. Sustainability, 13(2), 981. https://doi.org/10.3390/su13020981