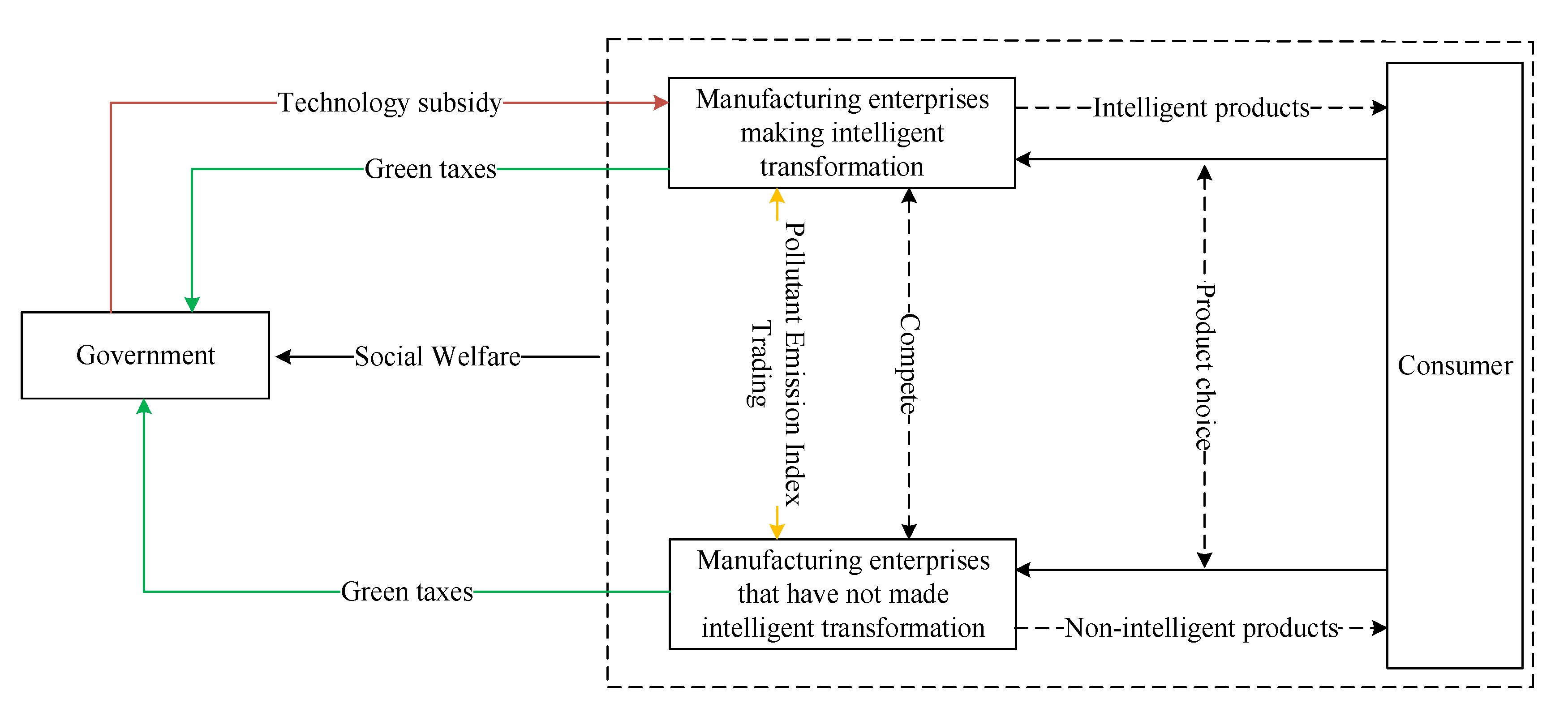

Principle of Tax Leverage: Tax leverage refers to the function of adjusting the social and economic life of the state by adjusting the tax collection relationship and the distribution of benefits among taxpayers in accordance with the tax law.

Through the design of tax rates, the state can implement incentives or restrictive measures such as tax increases, tax reductions, tax exemptions, tax rebates, and stipulated thresholds to enable taxpayers to make production-, operation-, and consumption-related decisions consistent with the national economic development plan. The use of tax leverage can compensate and correct the shortcomings of the market mechanism and give full play to the positive role of the market mechanism.

Next, according to the principle of tax leverage, this article promotes the intelligent transformation of enterprises by adjusting the green tax rate. The high tax rate reflects the government’s intention to restrict the development of non-intelligent enterprises; the low tax rate reflects the government’s intention to encourage the development of enterprises. This paper uses the excess progressive tax rate to reflect the government’s policy of encouraging high-polluting enterprises to carry out intelligent transformation.

6.1. The Green Taxes Scheme of Lightly Polluting Enterprises and Moderately Polluting Enterprises

Theorem 1. When, if,

always holds, otherwise , and the government’s optimal tax rate is .

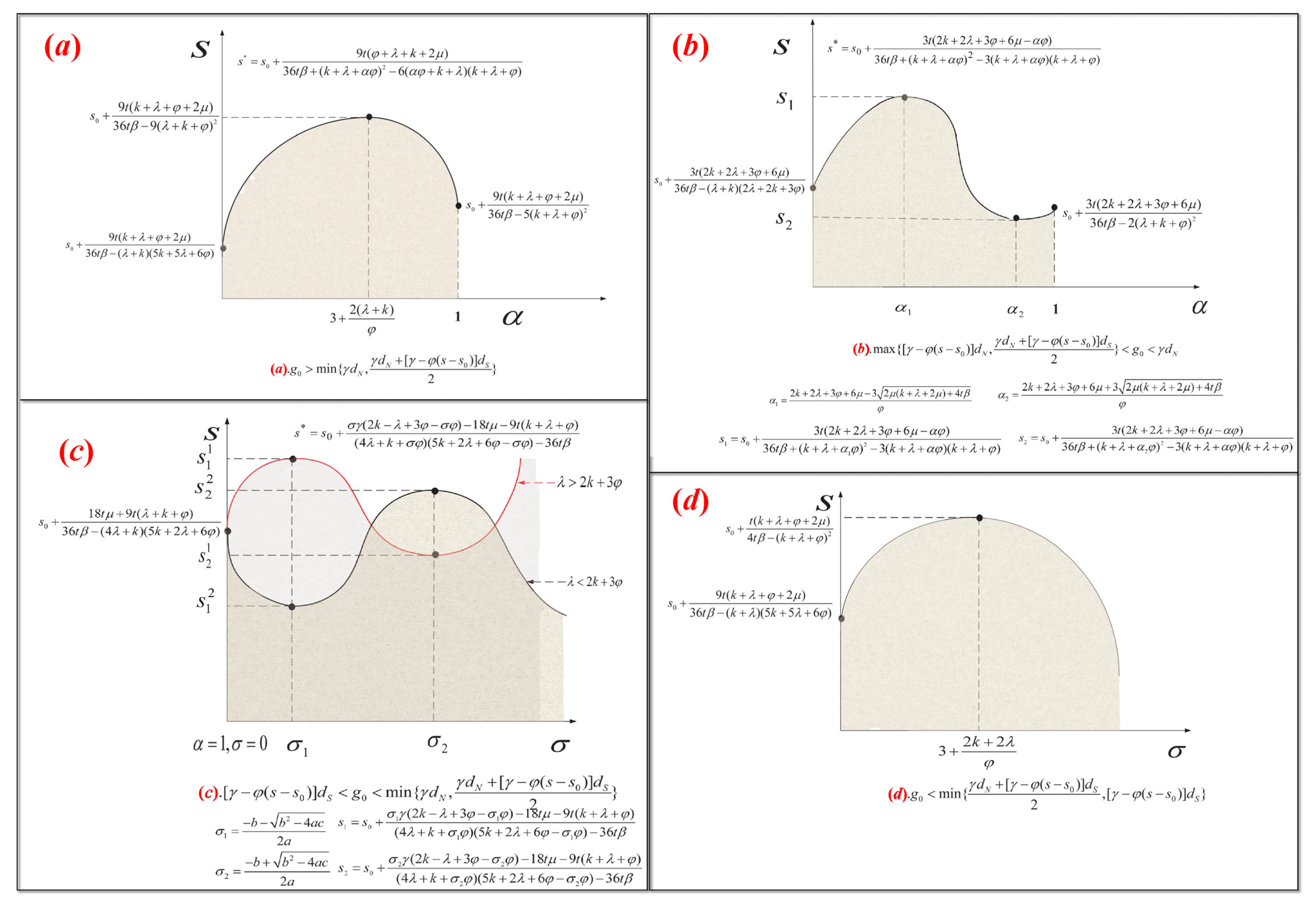

Theorem 1 and

Figure 2a indicate that when lightly polluting enterprises choose to undergo intelligent transformation, or lightly polluting enterprises do not undergo intelligent transformation but moderately polluting enterprises undergo intelligent transformation, if the government’s pollutant emissions tax rate

satisfies

, at this time, the government should appropriately lower the tax rate

to promote the degree of intelligent transformation of lightly polluting enterprises. Conversely, if the government’s pollutant emissions tax rate

satisfies

, at this time, the government should appropriately raise the tax rate

to promote the degree of intelligent transformation of lightly polluting enterprises; the government’s optimal tax rate is

.

Through Theorem 1, this paper finds that when lightly polluting enterprises choose to undergo intelligent transformation, or lightly polluting enterprises do not undergo intelligent transformation, but moderately polluting enterprises undergo intelligent transformation, the government’s careless increase in the pollution emission tax rate reduces the motivation of enterprises to intelligently transform. When the government’s decision-making objects are lightly polluting enterprises—and these enterprises all choose to carry out intelligent transformation, or there are moderately polluting enterprises among the decision-making objects but moderately polluting enterprises choose to carry out intelligent transformation—no matter how the government raises the tax rate of pollution emission, the pollution cost paid by the enterprise does not differ too much from the cost of intelligent transformation. However, the ever-increasing tax rate will result in a reduction in government technology subsidies, leading to decreased opportunities for ordinary enterprises to transform into intelligent enterprises.

Theorem 2. When , if, always holds, otherwise .

Theorem 2 and

Figure 2b indicate that when the moderately polluting enterprises do not undergo intelligent transformation and the lightly polluting enterprises do undergo intelligent transformation, if the government’s pollutant emissions tax rate

satisfies:

The government should lower the tax rate to promote the degree of intelligent transformation of lightly polluting enterprises. Conversely, if the government pollutant emissions tax rate meets or , the government should raise the tax rate to promote the degree of intelligent transformation of lightly polluting enterprises.

Through Theorem 2, this paper finds that when moderately polluting enterprises do not undergo intelligent transformation and lightly polluting enterprises do undergo intelligent transformation, the government can increase the motivation for the intelligent transformation of moderately polluting enterprises by continuously increasing the tax rate. When the government’s decision-making objects—lightly polluting enterprises—choose to undergo intelligent transformation, and moderately polluting enterprises do not undergo intelligent transformation, the government raises the tax rate of pollution emission, making the pollution tax rate higher than MAC of intelligent transformation to achieve zero pollution emissions. Therefore, moderately polluting companies will continue to improve their motivation for intelligent transformation.

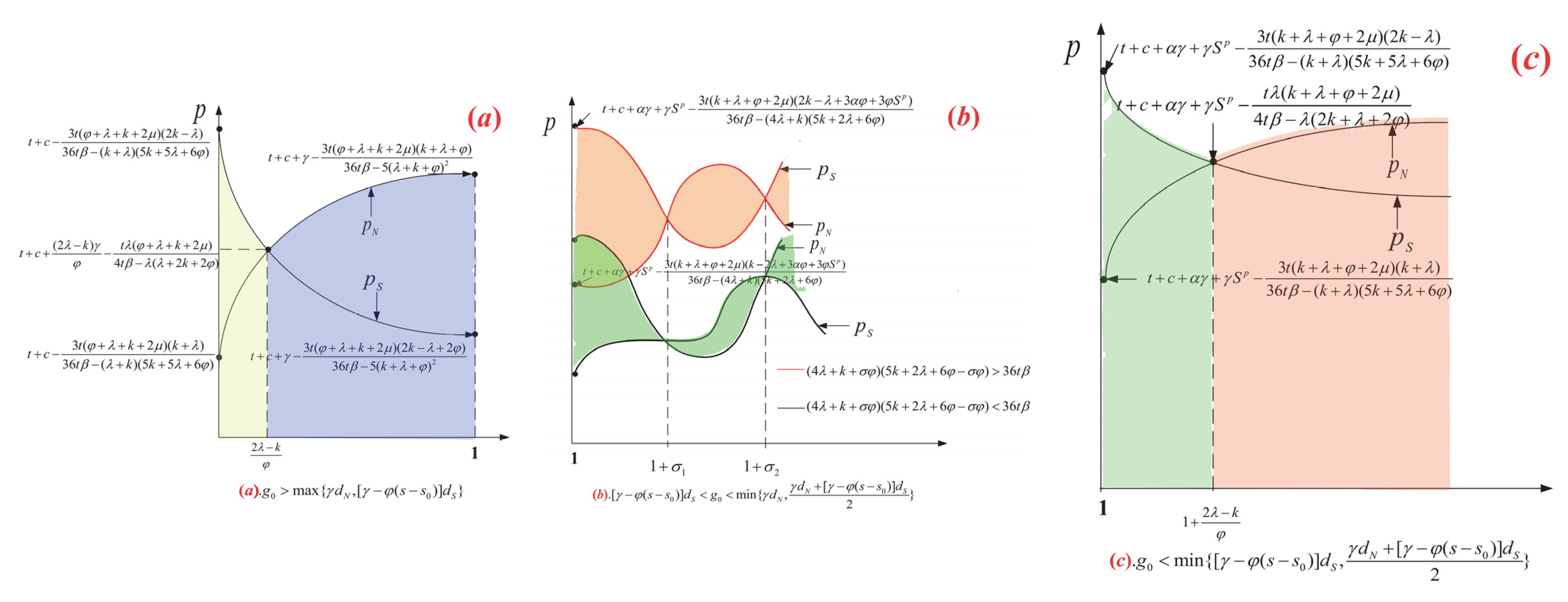

Theorem 3. When , if , always holds.

Theorem 3 and

Figure 3a indicate that to further promote the intelligent transformation of manufacturing enterprises, the government should adjust the pollutant emissions tax rate

to satisfy

. Currently, the price of intelligent products is always lower than the price of ordinary products, that is,

.

Through Theorem 3, this paper finds that when continuously increasing the tax rate of pollution emissions, non-intelligent transformation enterprises will continuously increase the price of products to compensate for the loss caused by the increase in the tax rate. When a non-intelligent transformation enterprise pays more than the transformation cost of an intelligent transformation enterprise, the price of the intelligent product will be lower than the price of the non-intelligent product. Through price competition, the intelligent transformation enterprises can occupy more market shares; thereby, the government can achieve the purpose of promoting the intelligent transformation of enterprises.

From

Figure 2, this paper finds that both the tax rate of pollution emission and the degree of intelligent transformation are non-monotonic. This non-monotonic relationship comes from the non-monotonicity between the cost advantage of intelligent transformation and the emission reduction. Once the tax rate of pollution emission is higher than the MAC for intelligent transformation to achieve zero pollution emissions, the relationship between the cost advantage and the diffusion rate and the tax rate is not significant.

6.2. The Research Object has Severely Polluting Enterprises

The price of the emission index transaction is determined by the market and is an endogenous variable. Therefore, the transaction price will be adjusted as the intelligent transformation promotes technological progress and the pollution emission volume changes. Since the emission index transaction mechanism has a small incentive effect on the intelligent transformation of enterprises, and this section involves the trading of emissions indicators, it is not discussed here.

Theorem 4. When additional utility coefficients satisfies:

- (1)

When , if , always holds, otherwise .

- (2)

When , if , always holds, otherwise.

Theorem 4 and

Figure 2c indicate that when lightly polluting enterprises are pursuing intelligent transformation, severely polluting enterprises are not pursuing intelligent transformation. (1) When the additional utility

brought by intelligent products to users is satisfied,

, and the government’s tax rate of excess pollutant emissions

satisfies

or

, the government should raise the tax rate

to promote the degree of intelligent transformation of lightly polluting enterprises. Conversely, if the government’s tax rate of excess pollutant emissions

satisfies

, the government should lower the tax rate

to promote the degree of intelligent transformation of lightly polluting enterprises. (2) When the additional utility

brought by the intelligent product to the user satisfies

, and the government sets the pollutant emissions tax rate

to satisfy

, the government should raise the tax rate

to promote the degree of intelligent transformation of lightly polluting enterprises. Conversely, if the government’s tax rate of excess pollutant emissions

satisfies

or

, the government should lower the tax rate

to promote the degree of intelligent transformation of lightly polluting enterprises.

From Theorem 4 and

Figure 2c, we find that the degree of intelligent transformation of enterprises that brings additional utility coefficients to users

affects the government’s formulation of the excess pollution emission tax. If

is large, enterprises can obtain additional benefits if they carry out intelligent transformation. Therefore, when the government increases the excess pollution emission tax rate, the enterprise will gradually increase the degree of intelligent transformation. However, if

is small, the enterprise can realize the additional benefits that the intelligent transformation cannot bring to the enterprise. Therefore, when the government continues to increase the excess pollution emission tax rate, the enterprise’s motivation for intelligent transformation will not only not increase but may even cause some enterprises to cease production. The results of the study show that there is uncertainty regarding the impact of strict taxation policies for excess pollution emission on intelligent transformation and that policies that are too strict will hinder the development of intelligent transformation. Although Theorems 2 and 4 both describe enterprises with low pollution levels to undergo intelligent transformations, enterprises with high pollution levels do not undergo intelligent transformations, and the green tax strategy taken by the government is different. The reason for this phenomenon is that the buffering effect of the PEITM and the impact of the additional utility of intelligent transformation products on consumers have led to changes in taxation strategies.

Theorem 5. When , if, always holds, otherwise, . In addition, the government’s optimal excess pollutant emissions tax rate is .

Theorem 5 and

Figure 2d indicate that when lightly polluting enterprises do not undergo intelligent transformation and severely polluting enterprises undergo intelligent transformation, or among severely polluting enterprises, when some enterprises choose to undergo intelligent transformation, if the excess pollutant emissions tax

satisfies

, the government should raise the tax rate

to promote the degree of intelligent transformation of severely polluting enterprises. Conversely, if the government’s excess pollution tax

satisfies

, the government should lower the tax rate

to promote the degree of intelligent transformation of severely polluting enterprises. In addition, the government’s optimal excess pollutant emissions tax rate is

.

From Theorem 5, this paper finds that when lightly polluting enterprises do not undergo intelligent transformation and severely polluting enterprises undergo intelligent transformation, or among severely polluting enterprises, when some enterprises choose to undergo intelligent transformation, to a certain extent, the government can effectively promote the intelligent transformation of heavily polluting enterprises by increasing the tax of excess polluting emissions. However, when the government’s tax rate of excess polluting emission is too high, due to the limited ability of the intelligent transformation to achieve emission reduction, it will cause heavily polluting enterprises to abandon transformation and stop production. Therefore, for the intelligent transformation of heavily polluting enterprises, it is necessary to set the excess pollution emission tax rate to meet , and help the government to achieve the greatest degree of promotion for the intelligent transformation of enterprises.

Theorem 6. When , we have.

When

, if , always holds.

When

, if or , always holds.

Theorem 6 and

Figure 3b indicate that when severely polluting enterprises choose not to undergo intelligent transformation and severely polluting enterprises choose to undergo intelligent transformation, to further promote the intelligent transformation of lightly polluting enterprises, if

, the government should formulate a reasonable taxation strategy for excess pollutant emissions, so that

satisfies

, the price of intelligent products is lower than the price of non-intelligent products

, and consumers tend to purchase intelligent products. Conversely, if

, the government should formulate a taxation strategy for excess pollutant emissions so that the tax rate

satisfies

or

, the price of intelligent products is lower than the price of non-intelligent products

, and consumers tend to purchase intelligent products.

From Theorem 6, this paper finds that the cost of enterprise intelligent transformation affects the formulation of government taxation policies for excess polluting emission and the price of products. When the cost of enterprise intelligent transformation is low, the government does not need to set a higher tax rate for excess polluting emissions and the price of non-intelligent transformation enterprise products can be higher than the price of intelligent transformation products. However, when the cost of the intelligent transformation of the enterprise is high, the government must continuously increase the tax rate of excess pollution emissions, so that the increased fee—of excess pollution emissions—paid by the non-intelligent transformation enterprise is greater than the transformation cost of the intelligent transformation enterprise. The price of intelligent products will be lower than that of non-intelligent products. Through price competition, intelligent transformation enterprises can occupy more market share, and then achieve the purpose of promoting the intelligent transformation of enterprises.

Theorem 7. When , if , always holds.

Theorem 7 and

Figure 3c indicate that when severely polluting enterprises choose to undergo intelligent transformation and lightly polluting enterprises choose not to undergo intelligent transformation, or in severely polluting enterprises, when some enterprises undergo intelligent transformation, to further promote the intelligent transformation of lightly polluting enterprises, the government should formulate a taxation strategy for excess pollutant emissions

to satisfy

, the price of intelligent products is lower than that of non-intelligent products

, and consumers tend to purchase intelligent products.

From Theorem 7, this paper finds that when the government continuously increases the excess pollution tax rate, non-intelligent transformation enterprises will continue to increase the price of their products to compensate for the loss caused by the increase in the excess pollution tax rate. When non-intelligent transformation enterprises’ excessive pollution discharge fee exceeds the transformation cost of the intelligent transformation enterprise, the price of intelligent products will be lower than the price of non-intelligent products. Through price competition, intelligent transformation enterprises will occupy more market shares; thereby, the government achieves the purpose of promoting the intelligent transformation of enterprises.

Conclusion 1: The impact of green taxation on the intelligent transformation of enterprises is non-monotonous, and green taxation has a threshold effect on the government’s green taxation. This also means that the government cannot blindly increase or reduce green taxes to achieve the purpose of promoting the intelligent transformation of manufacturing enterprises. Blindly raising or lowering green taxes and will not only increase the degree and willingness of intelligent transformation of manufacturing enterprises, but will also backfire, reducing the willingness and degree of manufacturing enterprises’ intelligent transformation, and this measure of manufacturing enterprises will cause the government to reduce investment in technology related to intelligent transformation, etc., creating a vicious circle. As discussed in Theorems 1, 2, 4, and 5, the government should reasonably increase or reduce the tax rate within the threshold range of taxation to promote the intelligent transformation of enterprises.

Conclusion 2: The price of intelligent products is related to the additional product experience that intelligent products bring to consumers, the cost reduction brought about by product production , and the reduction in the product production’s environmental impact . The government can change the green tax so that the price of intelligent products is always lower than the price of ordinary products. This measure will steer consumers towards purchasing smart products, subsequently allowing smart products to occupy more market share, and allowing many manufacturing companies to take the initiative to adopt smart transformation—as discussed in Theorems 3, 6, and 7.

Conclusion 3: The green tax formulated by the government will affect the government’s technical subsidies for its intelligent transformation. From

Table 1,

Table 2,

Table 3,

Table 4,

Table 5 and

Table 6, we find that the government’s optimal technology subsidy is related to the green tax rates set by the government—there is a certain relationship between them. However, due to space limitations, we do not discuss this in detail, and the relationship between them will be given in follow-up research.

Note: In this paper, and are in the same interval and satisfy . Moreover, and are in the same interval and satisfy .

{kind=link}

{kind=link}

{kind=link}