Accountability through Sustainability Data Governance: Reconfiguring Reporting to Better Account for the Digital Acceleration

Abstract

:1. Introduction

- On a macro-strategic level: how can data governance, a digitalization construct built on the accountability approach, be combined with the sustainability assessment process to further improve the accountability of a business?

- On a micro-operational level: how do companies communicate their digitalization efforts to strengthen sustainability reporting, the ultimate outcome of the sustainability assessment process, ultimately increasing their accountability to stakeholders?

2. Theoretical Foundation

2.1. Digital Transformation and Business Strategy

2.2. Digital Transformation and Data Governance

2.3. Sustainability Data, Reporting, and Digital Tools

3. Methods and Data

4. Discussion of Results

4.1. Theoretical Framework for Sustainability Data Governance

4.2. Reporting Behaviors of Reporting Companies

- At the very basic level, firms tend to simply include a few relevant keywords on “data”, “privacy”, and “security”, scattered throughout the text of the document (key-wording).

- The second group of companies would figuratively ‘checkmark’ that they have done the minimum that was required of them, according to frameworks like the GRI, etc. They may, hence, dedicate a one-statement paragraph at most, to a specific data privacy and security paragraph, including only a statement on data collection, confidentiality, and protection, or a one-page paragraph with the general internal data policy on data privacy. This category represents the majority of businesses in the sample.

- On a step higher are those businesses that have already planned a (two-page) roadmap for the implementation of new digitalization projects for the following year, despite not having deployed any concrete actions to that point (road-mapping).Quadrants II and III represent slightly more advanced strategies:

- Firms in the second quadrant understand the importance of listing a variety of specific and more significant digital activities that are carried out by a dedicated cybersecurity team (e.g., developing a threat intelligence center; managing cybersecurity risks through a new framework; third party audits; special training for employees, consumers, and vendors). They can do so within one page. They usually add a new paragraph in addition to the pre-defined reporting scheme, however, they do so all in one page (listing).

- Other firms, in the third quadrant, highly rely on the popular ‘projects’ section of the report for social-environmental impact, but only to support the disclosure and measurement of sustainability initiatives by describing the value of more complex initiatives that have been developed for the company’s specific purposes, such as new digital services and tools (supporting). This represents the second most popular type of behavior in the sample.

- Some of them provide an archetype of digital expertise that other players in the industry can adopt as a best practice for framework development: they normally include a dedicated chapter detailing their digital transformation journey, ethos, and expertise (frameworking).

- Then, other businesses produce a unified annual document, or feature a dedicated page on their website, where their digital and sustainability strategies are completely intertwined (e.g., data governance for sustainability data), with digital ambitions serving as leverage to contribute to specific Sustainability Development Goals (SDGs), for promoting societal and environmental change at every step of the way (e.g, better digital lives for families, digital skills mentorship for jobseekers, SMEs support in the digital economy, advocating for green recovery through campaigns, and platforms) (integrating).

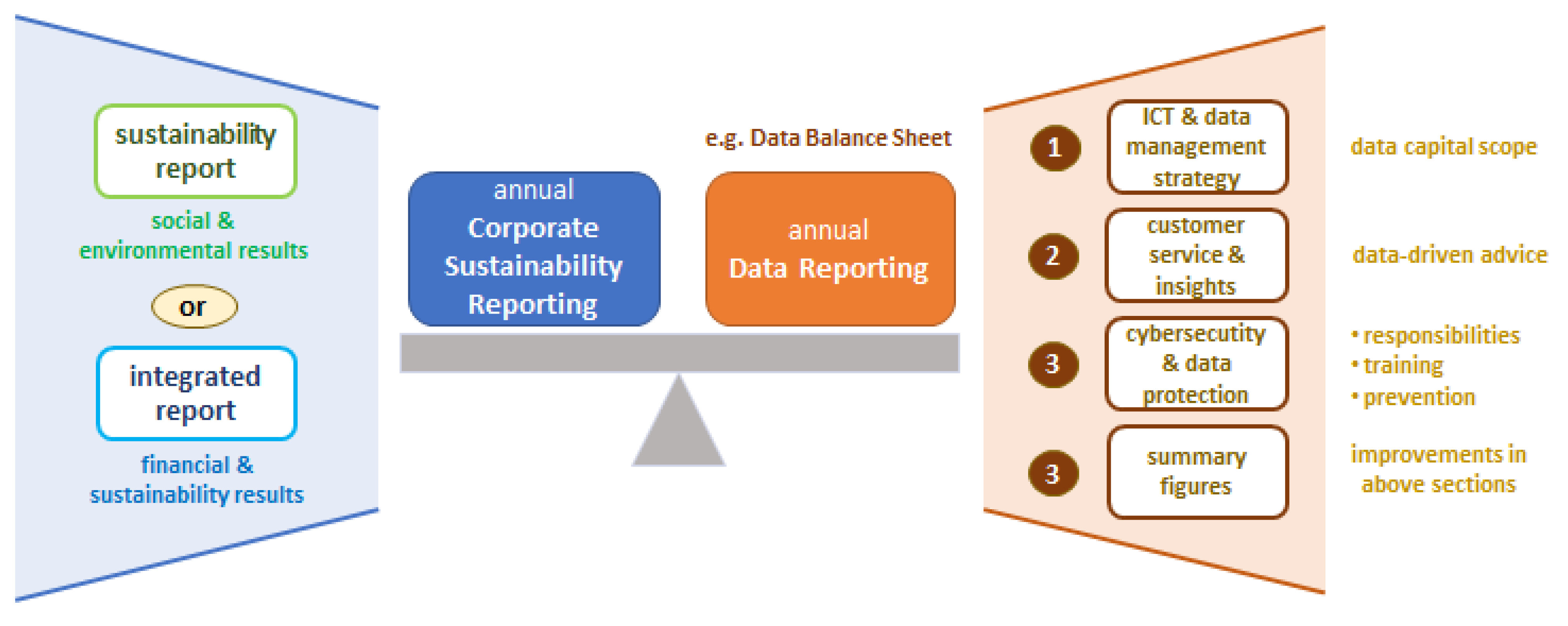

- Finally, at the very extreme of the reporting efforts, we find those of the role assigned to one specific company, OP Financial Group (OPFG), the largest Finnish provider of financial services (leading).

- (1).

- A breakdown of the general ICT strategy (e.g., mobile, Application Programming interfaces-API, cloud, technology competencies, agile working, cost management) and data management strategy, defining the scope of the company’s data capital (distinction between internal and external data available—e.g., databases, e-documents) and data assets (processes and services/products that use data capital for the benefit of sustainable value and the business/customer/operating environment).

- (2).

- A focus on how the defined data capital can be used to better serve customers, create benefits for them, and gain customer insights.

- Which service channels have been digitized and how services have been automized (digital services performance and technologies adopted—e.g., API, mobile, chatbots, cash flows management through a corporate hub).

- Use of the obtained customer insights for providing fact-based support, data-driven recommendations and marketing communications on services/products of interest, as well as for guiding company operations (e.g., real-time services that can be connected directly to the firm’s systems, such as automated payments).

- How the company’s data capital can support and simplify responsible investment.

- (3).

- Illustration of the data governance framework of reference (as a strategic component), along with all the elements taken into consideration (e.g., data capital life cycle/availability, quality/reliability, security and risk management, architecture and models, databases, documents and content, data warehousing—if decentralization or centralization of data on the cloud or in data centers).

- (4).

- Focus on data protection and security.

- Cybersecurity operating model (e.g., integrated for self-managed and agile working, boosting app development).

- Control (corporate bodies responsible for coordinating data protection activities, third-party auditing, use of external white hat hackers for testing system vulnerabilities).

- How the organization intends to increase the data protection competence internally (internal roles, personnel digital training, regular internal cyber security drills to simulate and prevent cyber-attacks).

- Mechanisms in place to protect rights of data and timely respond to the data security breaches detected (e.g., central processing, reporting to authorities and data subjects, monitoring, cookie consent, responding to customer complaints and requests to access personal data).

- (5).

- Some summary key figures, showing improvements in each of the above areas [93].

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Kostić, Z. Innovations and Digital Transformation as a Competition Catalyst. Ekonomika 2018, 64, 13–23. [Google Scholar] [CrossRef] [Green Version]

- Agostino, D.; Arnaboldi, M.; Lema, M.D. New Development: COVID-19 as an Accelerator of Digital Transformation in Public Service Delivery. Public Money Manag. 2021, 41, 69–72. [Google Scholar] [CrossRef]

- OECD. The Role of Online Platforms in Weathering the COVID-19 Shock; OECD: Paris, France, 2021. [Google Scholar]

- UNIDO COVID-19. Implications & Responses. In Digital Transformation & Industrial Recovery; UNIDO: Vienna, Austria, 2020. [Google Scholar]

- Vodafone Group. Context Consulting SME Digitalisation—Charting a Course towards Resilience and Recovery; Vodafone: Newbury, UK, 2020. [Google Scholar]

- Guo, H.; Yang, Z.; Huang, R.; Guo, A. The Digitalization and Public Crisis Responses of Small and Medium Enterprises: Implications from a COVID-19 Survey. Front. Bus. Res. China 2020, 14, 19. [Google Scholar] [CrossRef]

- Lim, D.S.; Morse, E.A.; Yu, N. The Impact of the Global Crisis on the Growth of SMEs: A Resource System Perspective. Int. Small Bus. J. 2020, 38, 492–503. [Google Scholar] [CrossRef]

- OECD. Coronavirus (COVID-19): SME Policy Responses; OECD: Paris, France, 2020. [Google Scholar]

- Priyono, A.; Moin, A.; Putri, V.N.A.O. Identifying Digital Transformation Paths in the Business Model of SMEs during the COVID-19 Pandemic. JOItmC 2020, 6, 104. [Google Scholar] [CrossRef]

- Caldwell, J.H.; Krishna, D. The Acceleration of Digitization as a Result of COVID-19; Deloitte: London, UK, 2020. [Google Scholar]

- McKinsey. How COVID-19 Has Pushed Companies over the Technology Tipping Point—And Transformed Business Forever; McKinsey & Company: New York, NY, USA, 2020. [Google Scholar]

- OECD. Digital Transformation in the Age of COVID-19: Building Resilience and Bridging Divides, Digital Economy Outlook 2020 Supplement; OECD: Paris, France, 2020. [Google Scholar]

- UNCTAD. How COVID-19 Triggered the Digital and e-Commerce Turning Point; UNCTAD: Geneva, Switzerland, 2021. [Google Scholar]

- Collibra. What Is Adaptive Data Governance? Collibra 2021. Available online: https://www.collibra.com/us/en/blog/what-is-adaptive-data-governance (accessed on 7 November 2021).

- Döhring, B.; Hristov, A.; Maier, C.; Roeger, W.; Thum-Thysen, A. COVID-19 Acceleration in Digitalisation, Aggregate Productivity Growth and the Functional Income Distribution. Int. Econ. Econ. Policy 2021, 18, 571–604. [Google Scholar] [CrossRef]

- Gartner. Top Priorities for IT: Leadership Vision for 2021. In Data and Analytics; Gartner: Stamford, CT, USA, 2020. [Google Scholar]

- Rascão, J. Data Governance in the Digital Age. In Digital Transformation and Challenges to Data Security and Privacy; Anunciação, P.F., Pessoa, C.R.M., Jamil, G.L., Eds.; Advances in Information Security, Privacy, and Ethics; IGI Global: Hershey, PA, USA, 2021; ISBN 978-1-79984-201-9. [Google Scholar]

- Jones, K.R.; Mucha, L. Sustainability Assessment and Reporting for Nonprofit Organizations: Accountability “for the Public Good”. Voluntas 2014, 25, 1465–1482. [Google Scholar] [CrossRef]

- Schmitz, A. Chapter 4: Accountability for Sustainability. In The Sustainable Business Case Book; Saylor Academy: Washington, DC, USA, 2012. [Google Scholar]

- Zimek, M.; Baumgartner, R.J. Sustainability Assessment and Reporting of Companies. In Good Health and Well-Being; Leal Filho, W., Wall, T., Azeiteiro, U., Azul, A.M., Brandli, L., Özuyar, P.G., Eds.; Encyclopedia of the UN Sustainable Development Goals; Springer International Publishing: Cham, Switzerland, 2019; pp. 1–13. ISBN 978-3-319-69627-0. [Google Scholar]

- Zattoni, A.; Pugliese, A. Corporate Governance Research in the Wake of a Systemic Crisis: Lessons and Opportunities from the COVID-19 Pandemic. J. Manag. Stud. 2021, 58, 1405–1410. [Google Scholar] [CrossRef]

- Bose, S.; Shams, S.; Ali, M.J.; Mihret, D. COVID-19 Impact, Sustainability Performance and Firm Value: International Evidence. Account. Financ. 2021, 1–47. [Google Scholar] [CrossRef]

- Gregurec, I.; Tomičić Furjan, M.; Tomičić-Pupek, K. The Impact of COVID-19 on Sustainable Business Models in SMEs. Sustainability 2021, 13, 1098. [Google Scholar] [CrossRef]

- Townsend, J.H.; Coroama, V.C. Digital Acceleration of Sustainability Transition: The Paradox of Push Impacts. Sustainability 2018, 10, 2816. [Google Scholar] [CrossRef] [Green Version]

- EC. The European Green Deal. Communication from the Commission; European Commission: Brussels, Belgium, 2019. [Google Scholar]

- EC. A New Industrial Strategy for Europe; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- EC. A New Circular Economy Action Plan; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- Horwood, R. Data Management Is the Key to Effective Sustainability Reporting. Aust. J. Multi-Discip. Eng. 2003, 1, 51–56. [Google Scholar] [CrossRef]

- GRI. ERM Corporate Leadership Group on Digital Reporting: Insights on Using Digital Tools for Sustainability Reporting Processes; ERM Group: London, UK, 2020. [Google Scholar]

- Kotsantonis, S.; Serafeim, G. Four Things No One Will Tell You About ESG Data. J. Appl. Corp. Financ. 2019, 31, 50–58. [Google Scholar] [CrossRef]

- CIPL. Accountability: Data Governance for the Evolving Digital Marketplace; CIPL: Washington, DC, USA, 2011. [Google Scholar]

- Felici, M.; Koulouris, T.; Pearson, S. Accountability for Data Governance in Cloud Ecosystems. In Proceedings of the 2013 IEEE 5th International Conference on Cloud Computing Technology and Science, Bristol, UK, 2–5 December 2013; IEEE: Bristol, UK, 2013; pp. 327–332. [Google Scholar]

- Weber, K. Data Governance—Defining Accountabilities for Data Quality Management; Luiss University Press: St. Gallen, Switzerland, 2007. [Google Scholar]

- EC. Europe’s Moment: Repair and Prepare for the Next Generation; EUR-Lex: Brussels, Belgium, 2020. [Google Scholar]

- Chen, Y.; Biswas, M.I. Turning Crisis into Opportunities: How a Firm Can Enrich Its Business Operations Using Artificial Intelligence and Big Data during COVID-19. Sustainability 2021, 13, 12656. [Google Scholar] [CrossRef]

- Deliu, D. The Intertwining between Corporate Governance and Knowledge Management in the Time of COVID-19—A Framework. J. Emerg. Trends Mark. Manag. 2020, 1, 93–110. [Google Scholar]

- Satalkina, L.; Steiner, G. Digital Entrepreneurship and Its Role in Innovation Systems: A Systematic Literature Review as a Basis for Future Research Avenues for Sustainable Transitions. Sustainability 2020, 12, 2764. [Google Scholar] [CrossRef] [Green Version]

- Elia, G.; Margherita, A.; Ciavolino, E.; Moustaghfir, K. Digital Society Incubator: Combining Exponential Technology and Human Potential to Build Resilient Entrepreneurial Ecosystems. Admin. Sci. 2021, 11, 96. [Google Scholar] [CrossRef]

- Tiron-Tudor, A.; Deliu, D. Reflections on the Human-Algorithm Complex Duality Perspectives in the Auditing Process. Qual. Res. Account. Manag. 2021. [Google Scholar] [CrossRef]

- Tiron-Tudor, A.; Deliu, D.; Farcane, N.; Dontu, A. Managing Change with and through Blockchain in Accountancy Organizations: A Systematic Literature Review. J. Organ. Chang. Manag. 2021, 34, 477–506. [Google Scholar] [CrossRef]

- Stitzlein, C.; Fielke, S.; Waldner, F.; Sanderson, T. Reputational Risk Associated with Big Data Research and Development: An Interdisciplinary Perspective. Sustainability 2021, 13, 9280. [Google Scholar] [CrossRef]

- Ismail, M.H.; Khater, M.; Zaki, M. Digital Business Transformation and Strategy: What Do We Know So Far? Camb. Serv. Alliance (Univ. Camb.) 2017, 10, 1–35. [Google Scholar] [CrossRef]

- Tratkowska, K. Digital Transformation: Theoretical Backgrounds of Digital Change. Manag. Sci. 2020, 24, 32–37. [Google Scholar] [CrossRef]

- Romero, D.; Flores, M.; Herrera, M.; Resendez, H. Five Management Pillars for Digital Transformation Integrating the Lean Thinking Philosophy. In Proceedings of the 2019 IEEE International Conference on Engineering, Technology and Innovation (ICE/ITMC), Valbonne Sophia Antipolis, France, 17–19 June 2019; IEEE: Valbonne Sophia Antipolis, France, 2019; pp. 1–8. [Google Scholar]

- McSweeney, A. Digital Transformation and Enterprise Architecture. 2019. Available online: https://doi.org/10.13140/RG.2.2.17647.07842 (accessed on 7 November 2021).

- Dunnett, M. Real Digital Transformation Starts with Data Governance. 2020. Available online: ITProPortal.com (accessed on 6 May 2021).

- HBR. A Blueprint for Data Governance in the Age of Business Transformation; Harvard Business Review Analytics Services: Boston, MA, USA, 2020. [Google Scholar]

- Informatica. Intelligent Data Management for Data-Driven Digital Transformation; Informatica: Redwood City, CA, USA, 2018. [Google Scholar]

- Sharma, S. Data Is Essential to Digital Transformation; Forbes: Jersey City, NJ, USA, 2020. [Google Scholar]

- Bärenfänger, R.; Otto, B.; Gizanis, D. Business and Data Management Capabilities for the Digital Economy. Corp. Data Qual. 2015, 10, 1–43. [Google Scholar] [CrossRef]

- Dey, S. Defining a Data Strategy: An Essential Component of Your Transformation Journey. DXC Technol. 2021. Available online: https://www.dxc.technology/analytics/insights/143882-defining_a_data_strategy_an_essential_component_of_your_digital_transformation_journey (accessed on 7 November 2021).

- Otto, B. Data Governance. Bus. Inf. Syst. Eng. 2011, 3, 241–244. [Google Scholar] [CrossRef]

- Fothergill, B.T.; Knight, W.; Stahl, B.C.; Ulnicane, I. Responsible Data Governance of Neuroscience Big Data. Front. Neuroinform. 2019, 13, 28. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Al-Ruithe, M.; Benkhelifa, E.; Hameed, K. Data Governance Taxonomy: Cloud versus Non-Cloud. Sustainability 2018, 10, 95. [Google Scholar] [CrossRef] [Green Version]

- Brous, P.; Janssen, M.; Krans, R. Data Governance as Success Factor for Data Science. In Responsible Design, Implementation and Use of Information and Communication Technology; Hattingh, M., Matthee, M., Smuts, H., Pappas, I., Dwivedi, Y.K., Mäntymäki, M., Eds.; Lecture Notes in Computer Science; Springer International Publishing: Cham, Switzerland, 2020; Volume 12066, pp. 431–442. ISBN 978-3-030-44998-8. [Google Scholar]

- Gupta, U.G.; Cannon, S. A Review of Data Governance Definitions and Emerging Perspectives. Int. J. Data Anal. 2020, 1, 30–47. [Google Scholar] [CrossRef]

- Koltay, T. Data Governance, Data Literacy and the Management of Data Quality. IFLA J. 2016, 42, 303–312. [Google Scholar] [CrossRef]

- Brous, P.; Janssen, M.; Vilminko-Heikkinen, R. Coordinating Decision-Making in Data Management Activities: A Systematic Review of Data Governance Principles. In Electronic Government; Scholl, H.J., Glassey, O., Janssen, M., Klievink, B., Lindgren, I., Parycek, P., Tambouris, E., Wimmer, M.A., Janowski, T., Sá Soares, D., Eds.; Lecture Notes in Computer Science; Springer International Publishing: Cham, Switzerland, 2016; Volume 9820, pp. 115–125. ISBN 978-3-319-44420-8. [Google Scholar]

- Otto, B. Quality and Value of the Data Resource in Large Enterprises. Inf. Syst. Manag. 2015, 32, 234–251. [Google Scholar] [CrossRef]

- Lis, D.; Otto, B. Data Governance in Data Ecosystems—Insights from Organizations. In Proceedings of the AMCIS 2020 Proceedings, Salt Lake City, UT, USA, 10–14 August 2020; Volume 12. [Google Scholar]

- Yebenes, J.; Zorrilla, M. Towards a Data Governance Framework for Third Generation Platforms. Procedia Comput. Sci. 2019, 151, 614–621. [Google Scholar] [CrossRef]

- Thomas, G. The DGI Data Governance Framework; The Data Governance Institute: Washington, DC, USA, 2020; pp. 1–20. [Google Scholar]

- Dontha, R. Data Quality—Simple 6 Step Process; Digital Transformation Pro: Folsom, CA, USA, 2018. [Google Scholar]

- PWC. Global and Industry Frameworks for Data Governance; PWC: New Delhi, India, 2019. [Google Scholar]

- Tjahjadi, B.; Soewarno, N.; Mustikaningtiyas, F. Good Corporate Governance and Corporate Sustainability Performance in Indonesia: A Triple Bottom Line Approach. Heliyon 2021, 7, e06453. [Google Scholar] [CrossRef]

- Vrolijk, H.; Poppe, K. Cost of Extending the Farm Accountancy Data Network to the Farm Sustainability Data Network: Empirical Evidence. Sustainability 2021, 13, 8181. [Google Scholar] [CrossRef]

- Nicolăescu, E.; Alpopi, C.; Zaharia, C. Measuring Corporate Sustainability Performance. Sustainability 2015, 7, 851–865. [Google Scholar] [CrossRef] [Green Version]

- Zyznarska-Dworczak, B. Sustainability Accounting—Cognitive and Conceptual Approach. Sustainability 2020, 12, 9936. [Google Scholar] [CrossRef]

- EFRAG. EFRAG & GRI Landmark Statement of Cooperation; EFRAG: Brussels, Belgium, 2021. [Google Scholar]

- Hussain, N.; Rigoni, U.; Orij, R.P. Corporate Governance and Sustainability Performance: Analysis of Triple Bottom Line Performance. J. Bus. Ethics 2018, 149, 411–432. [Google Scholar] [CrossRef]

- Bond, A.J.; Morrison-Saunders, A. Re-Evaluating Sustainability Assessment: Aligning the Vision and the Practice. Environ. Impact Assess. Rev. 2011, 31, 1–7. [Google Scholar] [CrossRef] [Green Version]

- Hacking, T.; Guthrie, P. A Framework for Clarifying the Meaning of Triple Bottom-Line, Integrated, and Sustainability Assessment. Environ. Impact Assess. Rev. 2008, 28, 73–89. [Google Scholar] [CrossRef]

- KPMG. The Time Has Come: The KPMG Survey of Sustainability Reporting 2020; KPMG: Amstelveen, The Netherlands, 2020. [Google Scholar]

- York, J.; Demberk, C.; Potter, B.; Gee, W. Sustainability Reporting to Improve Organizational Performance; Network for Business Sustainability: London, ON, Canada, 2017. [Google Scholar]

- Deloitte. Sustainability Reporting Strategy—Creating Impact through Transparency; Deloitte: London, UK, 2020. [Google Scholar]

- Barre, J. Best Practices in Sustainability Data Management—International Benchmark; ReScore Group: Rue Albert Einstein, France, 2017. [Google Scholar]

- WBCSD. Reporting Matters—Digital Deep Dive Analysis—WBCSD 2019 Addendum Report; World Business Council for Sustainable Development: Geneva, Switzerland, 2019; pp. 1–13. [Google Scholar]

- Maas, K.; Schaltegger, S.; Crutzen, N. Integrating Corporate Sustainability Assessment, Management Accounting, Control, and Reporting. J. Clean. Prod. 2016, 136, 237–248. [Google Scholar] [CrossRef]

- Mostafa, N.A.; Negm, A.M. Promoting Organizational Sustainability and Innovation: An Exploratory Case Study from the Egyptian Chemical Industry; Elsevier: Amsterdam, The Netherlands, 2017; pp. 1–8. [Google Scholar]

- Sala, S.; Ciuffo, B.; Nijkamp, P. A Systemic Framework for Sustainability Assessment. Ecol. Econ. 2015, 119, 314–325. [Google Scholar] [CrossRef]

- Jankalová, M.; Jankal, R. Sustainability Assessment According to the Selected Business Excellence Models. Sustainability 2018, 10, 3784. [Google Scholar] [CrossRef] [Green Version]

- Creswell, J.W. Qualitative Inquiry and Research Design: Choosing among Five Approaches, 3rd ed.; Sage: Thousand Oaks, CA, USA, 2013. [Google Scholar]

- Confetto, M.G.; Covucci, C. “Sustainability-Contents SEO”: A Semantic Algorithm to Improve the Quality Rating of Sustainability Web Contents. TQM J. 2021, 33, 295–317. [Google Scholar] [CrossRef]

- Sagot, S.; Ostrosi, E.; Fougères, A.-J. Improving Online Visibility and Information Sharing through the Culturalisation Process of the Product and Website; IOS Press: Modena, Italy, 2018. [Google Scholar]

- Urjanet. The Corporate Sustainability Professional’s Guide to Better Data Management; Urjanet: Atlanta, GA, USA, 2016. [Google Scholar]

- Wanner, J.; Janiesch, C. Big Data Analytics in Sustainability Reports: An Analysis Based on the Perceived Credibility of Corporate Published Information. Bus. Res. 2019, 12, 143–173. [Google Scholar] [CrossRef] [Green Version]

- Van Steenis, H. Defective Data Is a Big Problem for Sustainable Investing. 2019. Available online: FT.com (accessed on 6 May 2021).

- Cichowlas, A.; Markus, J. The Big Five Challenges in Reporting Reliable Sustainability Data; Sustainalize: Utrecht, Belgium, 2020. [Google Scholar]

- Pinchot, A.C.; Christianson, G. What Investors Actually Want from Sustainability Data. 2019. Available online: GreenBiz.com (accessed on 6 May 2021).

- Bañon Gomis, A.J.; Guillén Parra, M.; Hoffman, W.M.; Mcnulty, R.E. Rethinking the Concept of Sustainability. Bus. Soc. Rev. 2011, 116, 171–191. [Google Scholar] [CrossRef]

- Uzelac, A. How to Understand Digital Culture: Digital Culture—A Resource for a Knowledge Society? In Digital Culture: The Changing Dynamics; Uzelac, A., Cvjetičanin, B., Eds.; Culturelink: Zagreb, Croatia, 2008. [Google Scholar]

- Liakh, O.; Spigarelli, F. Managing Corporate Sustainability and Responsibility Efficiently: A Review of Existing Literature on Business Groups and Networks. Sustainability 2020, 12, 7722. [Google Scholar] [CrossRef]

- OP. Cooperative OP Financial Group’s Data Balance Sheet 2020; OP Financial Group: Helsinki, Finland, 2020. [Google Scholar]

- Hassan, A.; Elamer, A.A.; Lodh, S.; Roberts, L.; Nandy, M. The Future of Non-financial Businesses Reporting: Learning from the COVID-19 Pandemic. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 1231–1240. [Google Scholar] [CrossRef] [PubMed]

- Humphreys, K.A.; Trotman, K.T. Judgment and Decision Making Research on CSR Reporting in the COVID-19 Pandemic Environment. Account. Financ. 2021. [Google Scholar] [CrossRef]

- GRI. GRI 418: Customer Privacy 2016; GRI: Amsterdam, The Netherlands, 2018. [Google Scholar]

- ITU. Digital Trends in Europe 2021—ICT Trends and Developments in Europe 2017–2020; International Telecommunication Union: Geneva, Switzerland, 2021; pp. 1–48. [Google Scholar]

- Abueed, R.A.I.; Aga, M. Sustainable Knowledge Creation and Corporate Outcomes: Does Corporate Data Governance Matter? Sustainability 2019, 11, 5575. [Google Scholar] [CrossRef] [Green Version]

- KPMG. Sustainability Reporting during COVID-19 Pandemic; KPMG: Amstelveen, The Netherlands, 2020. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Type of Reporter | Digital Domain in Report | Scope | Content Example | Companies (Sectors) |

|---|---|---|---|---|

| 1. (5%) Keyworder | None (scattered throughout the document) | Keywords in environmental progress report | Data privacy and security |

|

| 2. (30%) Checkmarker | Privacy and data security | 1 paragraph or statement in sustainability report | Data collection, confidentiality, protection, security, or privacy |

|

| 3. (5%) Planner | Strategic and economic development | 2 pages in digital sustainability report | Digital roadmap for digital vision with partners |

|

| 4. (10%) Lister | Data privacy and cybersecurity | 1 page in ESG report | Dedicated cyber emergency response team, threat intelligence center, cybersecurity risk management framework, and training |

|

| 5. (20%) Supporter | Projects sections | Scattered throughout report sections | Core digital services, data accuracy improvement, recycling and reuse of hardware assets, employee digital “university” training platform, digitalization of communities |

|

| 6. (15%) Best practice generator | Data privacy and cybersecurity or digital transformation/ethos/inclusion chapter | 1 chapter in sustainability report | Digital principles, data protection management process, training and threat prediction, cybersecurity framework, security development life cycle process |

|

| 7. (10%) Twin integrator | None (scattered throughout the document) | Entire digital impact and sustainability report | Digital ambitions connected to SDGs for building better digitally inclusive lives, transparent description data governance/management/use |

|

| 8. (5%) Leader in responsible data governance practices | Entire report | Stand-alone data balance sheet and integrated reporting | Data management strategy, data-driven advice to customers, cybersecurity, and data protection |

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liakh, O. Accountability through Sustainability Data Governance: Reconfiguring Reporting to Better Account for the Digital Acceleration. Sustainability 2021, 13, 13814. https://doi.org/10.3390/su132413814

Liakh O. Accountability through Sustainability Data Governance: Reconfiguring Reporting to Better Account for the Digital Acceleration. Sustainability. 2021; 13(24):13814. https://doi.org/10.3390/su132413814

Chicago/Turabian StyleLiakh, Olena. 2021. "Accountability through Sustainability Data Governance: Reconfiguring Reporting to Better Account for the Digital Acceleration" Sustainability 13, no. 24: 13814. https://doi.org/10.3390/su132413814

APA StyleLiakh, O. (2021). Accountability through Sustainability Data Governance: Reconfiguring Reporting to Better Account for the Digital Acceleration. Sustainability, 13(24), 13814. https://doi.org/10.3390/su132413814