Mandatory CSR Disclosure, CSR Assurance, and the Cost of Debt Capital: Evidence from Taiwan

Abstract

1. Introduction

2. Literature Review and Hypothesis Development

2.1. Background on Taiwan’s Mandatory CSR Disclosure and Assurance

2.2. Literature Review

2.2.1. CSR Disclosure and CSR Assurance

2.2.2. CSR Disclosure and the Cost of Capital

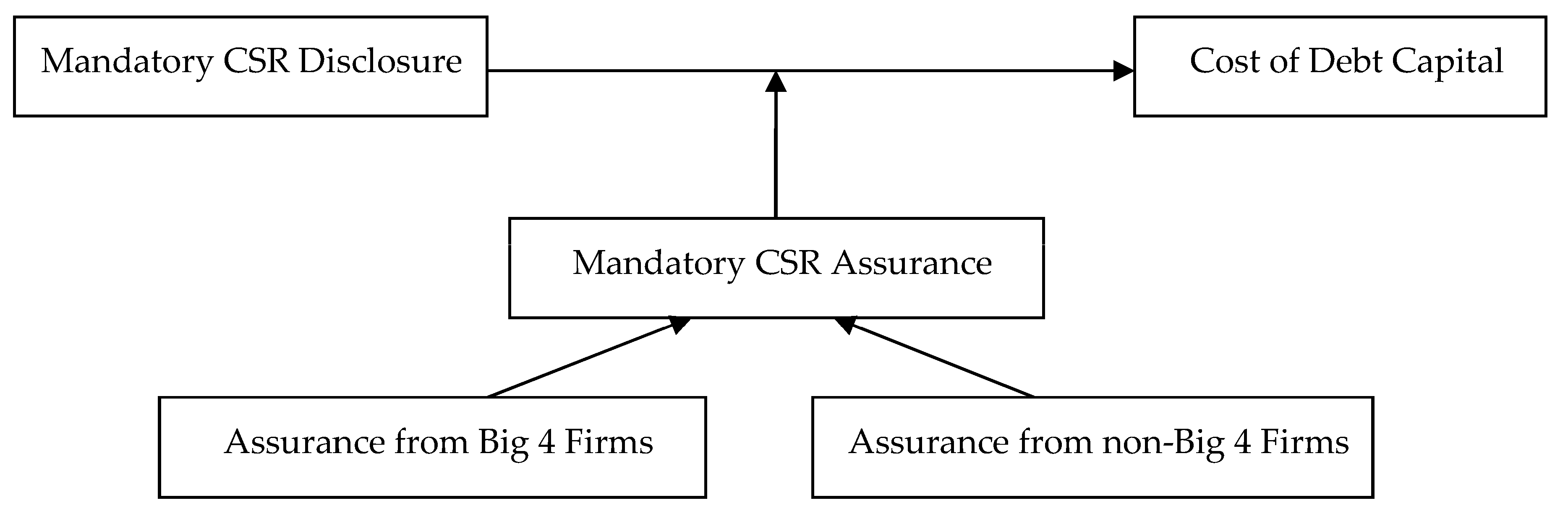

2.3. Research Hypotheses

3. Research Methods

3.1. Data Sources and Sample Selection

3.2. Variable Definitions

3.2.1. Dependent Variable: Cost of Debt Capital (COD)

3.2.2. Independent Variables

- Food-related industry (FR): For the main independent variable (FR), a value of 1 was assigned if it met the industry definition, and otherwise 0.

- Mandatory disclosure period (MDP): For mandatory disclosure period (MDP), a value of 1 was assigned if the company were subject to mandatory CSR disclosure after 2015 (the starting year of mandatory disclosure), and otherwise 0.

- Mandatory assurance (MA): For mandatory assurance (MA), a value of 1 was assigned in cases where CSR assurance was mandatory, and otherwise 0.

- Big 4 accounting firms (BIG4): For Big 4 accounting firms (BIG4), a value of 1 was assigned if CSR assurance was provided by a Big 4 accounting firm, and otherwise 0.

3.2.3. Control Variables

- Company size (SIZE): First, we consider the company size (Size). Larger companies have relatively low credit risk, such that investors are more willing to lower the required rate of returns [73].

- Market-to-book ratio (MB): We also considered the market-to-book ratio (MB). Brav et al. [74] reported that the market-to-book ratio is negatively correlated with borrowing costs, and companies with a higher market-to-book ratio face lower borrowing costs.

- Systemic risk (BETA): Another issue was systemic risk (BETA). Sharfman and Fernando [34] reported that systemic risk is significantly positively correlated with the cost of debt capital. Investors tend to increase the required rate of returns as a way to bear systemic risk.

- Debt-to-equity ratio (DE): We further examined debt-to-equity ratio (DE). Creditors view a debt-to-equity ratio as an indication of long-term solvency, wherein a higher ratio indicates higher risk and corresponding higher cost of debt capital. Sengupta [54] reported that DE is positively correlated with the cost of debt capital.

- Times-interest-earned ratio (TIE): Another important issue is the times-interest-earned ratio (TIE), which is an indicator of a company’s ability to repay interest on borrowings, wherein a higher ratio indicates better solvency. Sengupta [54] reported that a higher TIE is negatively correlated with the cost of debt capital.

- Standard deviation of stock returns (STD): Finally, we considered the standard deviation of stock returns (STD). Sengupta [54] used this metric as a proxy for market risk. In the current study, STD was based on the standard deviation of daily stock returns for a given firm.

3.3. Research Model

4. Results and Discussion

4.1. Descriptive Statistics

4.2. Empirical Model and Regression Analysis

4.3. Sensitivity Analysis: IFRS Adoption

5. Discussion

5.1. Discussion of Results

5.2. Implications for Research

5.3. Implications for Theory and Practice

5.4. Implications for National Policy

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

| Variables | Definition |

| COD | The cost of debt capital of the firm. The ratio of interest expenses for a given year divided by the average total short-term and long-term debt. |

| FR | A dummy variable equals to 1 if the firm met the industry definition (firms in the food industry and firms whose food and beverage revenue accounts for 50% or more of their total revenue), and otherwise 0. |

| MDP | A dummy variable equals to 1 if the firm were subject to mandatory CSR disclosure after 2015, and otherwise 0. |

| MA | A dummy variable equals to 1 if CSR assurance of the firm was mandatory, and otherwise 0. |

| BIG4 | A dummy variable equals to 1 if CSR assurance of the firm was provided by a Big 4 accounting firm, and otherwise 0. |

| SIZE | Firm size is measured as the natural logarithm of total assets of the firm. |

| MB | The market-to-book ratio is measured as market capitalization divided by the book value of the firm. |

| BETA | The annual systemic risk of the firm is measured as a stock’s risk reflected by measuring the fluctuation of its price changes relative to the overall market in the CAPM formula. |

| DE | The debt-to-equity ratio is measured as total debt divided by total equity of the firm. |

| TIE | The times-interest-earned ratio is measured as the sum of income before extraordinary items and interest expense divided by the interest expense of the firm. |

| STD | The standard deviation of daily stock returns of the firm. |

References

- Cohen, J.R.; Simnett, R. CSR and Assurance Services: A Research Agenda. Audit. J. Pract. Theory 2015, 34, 59–74. [Google Scholar] [CrossRef]

- Zhang, W.J.; Kuo, H.C. The relationship of corporate social responsibility reports’ reason for issuance, assurance, and assurance type to stock price reaction. J. Valuat. 2019, 13, 17–58. [Google Scholar]

- Wallace, W.A. The economic role of the audit in free and regulated markets: A look back and a look forward. Res. Account. Regul. 2010, 17, 267–298. [Google Scholar] [CrossRef]

- Chiu, A.-A.; Chen, L.-N.; Hu, J.-C. A Study of the Relationship between Corporate Social Responsibility Report and the Stock Market. Sustainability 2020, 12, 9200. [Google Scholar] [CrossRef]

- Kim, J.; Cho, K.; Park, C.K. Does CSR Assurance affect the relationship between CSR performance and fnancial performance? Sustainability 2019, 11, 5682. [Google Scholar] [CrossRef]

- Cho, S.J.; Chung, C.Y.; Young, J. Study on the Relationship between CSR and Financial Performance. Sustainability 2019, 11, 343. [Google Scholar] [CrossRef]

- Hopwood, A.G. Accounting and the environment. Account. Organ. Soc. 2009, 34, 433–439. [Google Scholar] [CrossRef]

- Gray, R. Is accounting for sustainability actually accounting for sustainability…and how would we know? An exploration of narratives of organisations and the planet. Account. Organ. Soc. 2010, 35, 47–62. [Google Scholar] [CrossRef]

- Lyon, T.P.; Maxwell, J.W. Greenwash: Corporate environmental disclosure under threat of audit. J. Econ. Manag. Strategy 2011, 20, 3–41. [Google Scholar] [CrossRef]

- Moroney, R.; Windsor, C.; Aw, Y.T. Evidence of assurance enhancing the quality of voluntary environmental disclosures: An empirical analysis. Account. Financ. 2012, 52, 903–939. [Google Scholar] [CrossRef]

- Casey, R.J.; Grenier, J.H. Understanding and contributing to the enigma of corporate social responsibility (CSR) assurance in the United States. Audit. J. Pract. Theory 2015, 34, 97–130. [Google Scholar] [CrossRef]

- Nikolaev, V.; Van Lent, L. The endogeneity bias in the relation between cost-of-debt capital and corporate disclosure policy. Eur. Account. Rev. 2005, 14, 677–724. [Google Scholar] [CrossRef]

- Jaggi, B.; Chin, C.-L.; Lin, H.-W.W.; Lee, P. Earnings forecast disclosure regulation and earnings management: Evidence from Taiwan IPO firms. Rev. Quant. Financ. Account. 2006, 26, 275–299. [Google Scholar] [CrossRef]

- Simnett, R.; Nugent, M. Developing an Assurance Standard for Carbon Emissions Disclosures. Aust. Account. Rev. 2007, 17, 37–47. [Google Scholar] [CrossRef]

- Huggins, A.; Green, W.J.; Simnett, R. The competitive market for assurance engagements on greenhouse gas statements: Is there a role for assurers from the accounting profession? Curr. Issues Audit. 2011, 5, A1–A12. [Google Scholar] [CrossRef]

- Cohen, J.; Holder-Webb, L.; Nath, L.; Wood, D. Retail Investors’ Perceptions of the Decision-Usefulness of Economic Performance, Governance, and Corporate Social Responsibility Disclosures. Behav. Res. Account. 2011, 23, 109–129. [Google Scholar] [CrossRef]

- Cohen, J.R.; Holder-Webb, L.; Zamora, V.L. Nonfinancial Information Preferences of Professional Investors. Behav. Res. Account. 2015, 27, 127–153. [Google Scholar] [CrossRef]

- Mock, T.J.; Rao, S.S.; Srivastava, R.P. The Development of Worldwide Sustainability Reporting Assurance. Aust. Account. Rev. 2013, 23, 280–294. [Google Scholar] [CrossRef]

- Park, J.; Brorson, T. Experiences of and views on third-party assurance of corporate environmental and sustainability reports. J. Clean. Prod. 2005, 13, 1095–1106. [Google Scholar] [CrossRef]

- Jones, M.J.; Solomon, J.F. Social and environmental report assurance: Some interview evidence. Account. Forum 2010, 34, 20–31. [Google Scholar] [CrossRef]

- Simnett, R.; Nugent, M.; Huggins, A.L. Developing an International Assurance Standard on Greenhouse Gas Statements. Account. Horiz. 2009, 23, 347–363. [Google Scholar] [CrossRef]

- Deegan, C.; Cooper, B.J.; Shelly, M. An investigation of TBL report assurance statements: UK and European evidence. Manag. Audit. J. 2006, 21, 329–371. [Google Scholar] [CrossRef]

- Manetti, G.; Becatti, L. Assurance Services for Sustainability Reports: Standards and Empirical Evidence. J. Bus. Ethics 2009, 87, 289–298. [Google Scholar] [CrossRef]

- O’Dwyer, B.; Owen, D.L. Assurance statement practice in environmental, social and sustainability reporting: A critical evaluation. Br. Account. Rev. 2005, 37, 205–229. [Google Scholar] [CrossRef]

- Hall, R. The strategic analysis of intangible resources. Strateg. Manag. J. 1992, 13, 135–144. [Google Scholar] [CrossRef]

- O’Dwyer, B.; Owen, D.; Unerman, J. Seeking legitimacy for new assurance forms: The case of assurance on sustainability reporting. Account. Organ. Soc. 2011, 36, 31–52. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing legitimacy: Strategic and institutional approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery Loves Companies: Rethinking Social Initiatives by Business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Radhakrishnan, S.; Tsang, A.; Yang, Y.G. Nonfinancial disclosure and analyst forecast accuracy: International evidence on corporate social responsibility disclosure. Account. Rev. 2012, 87, 723–759. [Google Scholar] [CrossRef]

- Black & Veatch. 2011 Strategic Directions Survey Results: Managing the Transition in the Electric Utility Industry. Available online: https://www.infrastructureusa.org/2011-strategic-directions-survey-results-managing-the-transition-in-the-electric-utility-industry/ (accessed on 28 November 2020).

- Core, J.E. A review of the empirical disclosure literature: Discussion. J. Account. Econ. 2001, 31, 441–456. [Google Scholar] [CrossRef]

- Healy, P.M.; Palepu, K.G. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. J. Account. Econ. 2001, 31, 405–440. [Google Scholar] [CrossRef]

- Leuz, C.; Wysocki, P.D. Economic Consequences of Financial Reporting and Disclosure Regulation: A Review and Suggestions for Future Research. SSRN 2008, 1105398. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Li, O.Z.; Tsang, A.; Yang, Y.G. Voluntary nonfinancial disclosure and the cost of equity capital: The initiation of corporate social responsibility reporting. Account. Rev. 2011, 86, 59–100. [Google Scholar] [CrossRef]

- Lackmann, J.; Ernstberger, J.; Stich, M. Market Reactions to Increased Reliability of Sustainability Information. J. Bus. Ethics 2012, 107, 111–128. [Google Scholar] [CrossRef]

- Glosten, L.R.; Milgrom, P.R. Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. J. Financ. Econ. 1985, 14, 71–100. [Google Scholar] [CrossRef]

- Merton, R.C. A simple model of capital market equilibrium with incomplete information. J. Financ. 1987, 42, 483–510. [Google Scholar] [CrossRef]

- Mazumdar, S.C.; Sengupta, P. Disclosure and the Loan Spread on Private Debt. Financ. Anal. J. 2005, 61, 83–95. [Google Scholar] [CrossRef]

- Hughes, J.S.; Liu, J.; Liu, J. Information asymmetry, diversification, and cost of capital. Account. Rev. 2007, 82, 705–729. [Google Scholar] [CrossRef]

- Lambert, R.; Leuz, C.; Verrecchia, R.E. Accounting information, disclosure, and the cost of capital. J. Account. Res. 2007, 45, 385–420. [Google Scholar] [CrossRef]

- Diamond, D.W.; Verrecchia, R.E. Disclosure, liquidity, and the cost of capital. J. Financ. 1991, 46, 1325–1359. [Google Scholar] [CrossRef]

- Botosan, C.A. Disclosure level and the cost of equity capital. Account. Rev. 1997, 323–349. [Google Scholar]

- Lombardo, D.; Pagano, M. Law and Equity Markets: A Simple Model. In Corporate Governance Regimes: Convergence and Diversity; Oxford University Press: Oxford, UK, 1999; pp. 343–362. Available online: https://ssrn.com/abstract=209312 (accessed on 28 November 2020). [CrossRef]

- Xu, H.; Xu, X.; Yu, J. The Impact of Mandatory CSR Disclosure on the Cost of Debt Financing: Evidence from China. Emerg. Mark. Financ. Trade 2019, 1–15. [Google Scholar] [CrossRef]

- Bushman, R.M.; Smith, A.J. Financial accounting information and corporate governance. J. Account. Econ. 2001, 32, 237–333. [Google Scholar] [CrossRef]

- Sloan, R.G. Financial accounting and corporate governance: A discussion. J. Account. Econ. 2001, 32, 335–347. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. People and Profits? The Search for a Link between a Company’s Social and Financial Performance; Psychology Press: East Sussex, UK, 2001. [Google Scholar]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Anderson, J.C.; Frankle, A.W. Voluntary social reporting: An iso-beta portfolio analysis. Account. Rev. 1980, 467–479. [Google Scholar]

- Richardson, A.J.; Welker, M. Social disclosure, financial disclosure and the cost of equity capital. Account. Organ. Soc. 2001, 26, 597–616. [Google Scholar] [CrossRef]

- Frankel, R.; McNichols, M.; Wilson, G.P. Discretionary disclosure and external financing. Account. Rev. 1995, 135–150. [Google Scholar]

- Healy, P.M.; Hutton, A.P.; Palepu, K.G. Stock Performance and Intermediation Changes Surrounding Sustained Increases in Disclosure. Contemp. Account. Res. 1999, 16, 485–520. [Google Scholar] [CrossRef]

- Sengupta, P. Corporate disclosure quality and the cost of debt. Account. Rev. 1998, 459–474. [Google Scholar]

- Marx, B.; van Dyk, V. Sustainability reporting and assurance: An analysis of assurance practices in South Africa. Meditari Account. Res. 2011, 19, 39–55. [Google Scholar] [CrossRef]

- Jenkins, R. Corporate Codes of Conduct: Self-Regulation in a Global Economy, Technology, Business and Society Paper no. 2; United Nations Research Institute for Social Development: Geneva, Switzerland, 2001. [Google Scholar]

- Utting, P. Beyond social auditing: Micro and macro perspectives. In Proceedings of the EU Conference on “Responsible Sources: Improving Global Supply Chains Management”, Brussels, Belgium, 18 November 2005. [Google Scholar]

- Ballou, B.; Chen, P.C.; Grenier, J.H.; Heitger, D.L. Corporate social responsibility assurance and reporting quality: Evidence from restatements. J. Account. Public Policy 2018, 37, 167–188. [Google Scholar] [CrossRef]

- Michelon, G.; Patten, D.M.; Romi, A.M. Creating legitimacy for sustainability assurance practices: Evidence from sustainability restatements. Eur. Account. Rev. 2019, 28, 395–422. [Google Scholar] [CrossRef]

- Clarkson, P.; Li, Y.; Richardson, G.; Tsang, A. Causes and consequences of voluntary assurance of CSR reports. Account. Audit. Account. J. 2019, 32, 2451–2474. [Google Scholar] [CrossRef]

- Pflugrath, G.; Roebuck, P.; Simnett, R. Impact of assurance and assurer’s professional affiliation on financial analysts’ assessment of credibility of corporate social responsibility information. Audit. J. Pract. Theory 2011, 30, 239–254. [Google Scholar] [CrossRef]

- Hodge, K.; Subramaniam, N.; Stewart, J. Assurance of sustainability reports: Impact on report users’ confidence and percep-tions of information credibility. Aust. Account. Rev. 2009, 19, 178–194. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; García-Sánchez, I.M. Sustainability assurance and cost of capital: Does assurance impact on credibility of corporate social responsibility information? Bus. Ethics Eur. Rev. 2017, 26, 223–239. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Blackwell, D.W.; Noland, T.R.; Winters, D.B. The Value of Auditor Assurance: Evidence from Loan Pricing. J. Account. Res. 1998, 36, 57–70. [Google Scholar] [CrossRef]

- Kim, J.B.; Simunic, D.A.; Stein, M.T.; Yi, C.H. Voluntary audits and the cost of debt capital for privately held firms: Korean evidence. Contemp. Account. Res. 2011, 28, 585–615. [Google Scholar] [CrossRef]

- Knechel, W.R.; Wallage, P.; Eilifsen, A.; Van Praag, B. The Demand Attributes of Assurance Services Providers and the Role of Independent Accountants. Int. J. Audit. 2006, 10, 143–162. [Google Scholar] [CrossRef]

- Wallage, P. Assurance on sustainability reporting: An auditor’s view. Audit. J. Pract. Theory 2000, 19, 53–65. [Google Scholar] [CrossRef]

- Gray, R. Current Developments and Trends in Social and Environmental Auditing, Reporting and Attestation: A Review and Comment. Int. J. Audit. 2000, 4, 247–268. [Google Scholar] [CrossRef]

- DeAngelo, L.E. Auditor size and audit quality. J. Account. Econ. 1981, 3, 183–199. [Google Scholar] [CrossRef]

- Beatty, R.P. Auditor reputation and the pricing of initial public offerings. Account. Rev. 1989, 693–709. [Google Scholar]

- Francis, J.R.; Khurana, I.K.; Pereira, R. Disclosure Incentives and Effects on Cost of Capital around the World. Account. Rev. 2005, 80, 1125–1162. [Google Scholar] [CrossRef]

- Pittman, J.A.; Fortin, S. Auditor choice and the cost of debt capital for newly public firms. J. Account. Econ. 2004, 37, 113–136. [Google Scholar] [CrossRef]

- Brav, A.; Michaely, R.; Roberts, M.; Zarutskie, R. Evidence on the trade-off between risk and return for IPO and SEO Firms. Financ. Manag. 2009, 38, 221–252. [Google Scholar] [CrossRef]

- Sharfman, M.P.; Fernando, C.S. Environmental risk management and the cost of capital. Strateg. Manag. J. 2008, 29, 569–592. [Google Scholar] [CrossRef]

- Li, S. Does mandatory adoption of International Financial Reporting Standards in the European Union reduce the cost of equity capital? Account. Rev. 2010, 85, 607–636. [Google Scholar] [CrossRef]

- Zhang, G. Private information production, public disclosure, and the cost of capital: Theory and implications. Contemp. Ac-count. Res. 2001, 18, 363–384. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and en-vironmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.Y.; Mishra, D.R. Does corporate social responsibility affect the cost of capital? J. Bank Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Kolk, A.; Perego, P. Determinants of the adoption of sustainability assurance statements: An international investigation. Bus. Strategy Environ. 2010, 19, 182–198. [Google Scholar] [CrossRef]

- Simnett, R.; Vanstraelen, A.; Chua, W.F. Assurance on Sustainability Reports: An International Comparison. Account. Rev. 2009, 84, 937–967. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic management: A stakeholder approach. Adv. Strateg. Manag. 1983, 1, 31–60. [Google Scholar]

- Ballou, B.; Heitger, D.L.; Landes, C.E. The future of corporate sustainability reporting: A rapidly growing assurance op-portunity. J. Account. 2006, 22, 5–74. [Google Scholar]

- Kolk, A.; van der Veen, M.L.; Hay, K.; Wennink, D. KPMG International Survey of Corporate Sustainability Reporting 2002; KPMG Global Sustainability Services: De Meern, The Netherlands, 2002. [Google Scholar]

- Patten, D.; Guidry, R. Market reactions to the first-time issuance of corporate sustainability reports: Evidence that quality matters. Sustain. Account. Manag. Policy J. 2010, 1, 33–50. [Google Scholar]

- Janamrung, B.; Issarawornrawanich, P. The association between corporate social responsibility index and performance of firms in industrial products and resources industries: Empirical evidence from Thailand. Soc. Responsib. J. 2015, 11, 893–903. [Google Scholar] [CrossRef]

- Farooq, M.B.; De Villiers, C. Sustainability assurance: Who are the assurance providers and what do they do? In Challenges in Managing Sustainable Business: Reporting, Taxation, Ethics and Governance; Palgrave Macmillan: Cham, Switzerland, 2019; pp. 137–154. [Google Scholar]

- Dentchev, N.A.; Van Balen, M.; Haezendonck, E. On voluntarism and the role of governments in CSR: Towards a contin-gency approach. Bus. Ethics Eur. Rev. 2015, 24, 378–397. [Google Scholar] [CrossRef]

- Gatti, L.; Seele, P.; Rademacher, L. Grey zone in—Greenwash out. A review of greenwashing research and implications for the voluntary-mandatory transition of CSR. Int. J. Corp. Soc. Responsib. 2019, 4, 1–15. [Google Scholar] [CrossRef]

- Leuz, C.; Verrecchia, R. The economic consequences of increased disclosure. J. Account. Res. 2000, 38, 91–124. [Google Scholar] [CrossRef]

{kind=link}

| Number of Observations | |||

|---|---|---|---|

| Food-Related Industries | Non-Food-Related Industries | Total | |

| Firms with CSR disclosure | 280 | 1845 | 2125 |

| Less: | |||

| Voluntary CSR disclosure and assurance | (35) | (1095) | (1130) |

| Financial institutions | - | (103) | (103) |

| Missing data | (25) | (64) | (89) |

| Final sample of this study | 220 | 583 | 803 |

| Panel A Model (1) | |||||

| Variables | Mean | SD | Min | Median | Max |

| COD (%) | 2.488 | 3.102 | 0.930 | 1.820 | 3.154 |

| FR | 0.236 | 0.468 | 0.000 | 0.000 | 1.000 |

| MDP | 0.173 | 0.335 | 0.000 | 0.000 | 1.000 |

| FR × MDP | 0.065 | 0.279 | 0.000 | 0.000 | 1.000 |

| SIZE | 15.300 | 1.423 | 10.467 | 16.240 | 19.268 |

| MB | 1.586 | 1.768 | 0.323 | 1.242 | 1.984 |

| BETA | 0.758 | 0.832 | 0.395 | 0.754 | 1.225 |

| DE | 1.437 | 7.934 | 0.016 | 0.148 | 0.502 |

| TIE | 1788.834 | 26,757.680 | −2259.74 | 15.750 | 177,197.700 |

| STD | 1.738 | 1.456 | 1.294 | 1.736 | 2.681 |

| Panel BModel (2) and Model (3) | |||||

| Variables | Mean | SD | Min | Median | Max |

| COD (%) | 2.654 | 5.153 | 0.843 | 1.975 | 3.249 |

| MA | 0.254 | 0.482 | 0.000 | 0.000 | 1.000 |

| BIG4 | 0.846 | 0.329 | 0.000 | 1.000 | 1.000 |

| MA × BIG4 | 0.247 | 0.481 | 0.000 | 0.000 | 1.000 |

| SIZE | 14.985 | 1.569 | 12.247 | 15.743 | 18.123 |

| MB | 2.345 | 2.342 | 0.869 | 1.523 | 3.256 |

| BETA | 0.584 | 0.961 | 0.186 | 0.521 | 0.852 |

| DE | 0.242 | 0.242 | 0.005 | 0.196 | 0.314 |

| TIE | 1785.834 | 11,836.750 | −13.570 | 21.295 | 44,308.090 |

| STD | 1.694 | 1.734 | 0.982 | 1.842 | 2.873 |

| FR = 0 | MDP = 0 | MDP = 1 | Diff. in Means |

| Variables | Mean | Mean | |

| COD | 2.422 | 1.891 | −0.531 * |

| SIZE | 16.678 | 15.564 | −1.114 *** |

| MB | 1.485 | 1.168 | −0.317 ** |

| BETA | 0.848 | 0.678 | −0.170 ** |

| DE | 1.956 | 0.285 | −1.671 |

| TIE | 2143.944 | 183.989 | −1959.955 |

| STD | 1.933 | 1.780 | −0.153 |

| N | 498 | 85 | 583 |

| FR = 1 | MDP = 0 | MDP = 1 | Diff. in Means |

| Variables | Mean | Mean | |

| COD | 2.723 | 1.769 | −0.954 ** |

| SIZE | 15.427 | 15.536 | 0.109 |

| MB | 1.904 | 2.203 | 0.299 |

| BETA | 0.647 | 0.448 | −0.199 *** |

| DE | 0.233 | 0.196 | −0.037 |

| TIE | 683.073 | 4423.530 | 3740.458 ** |

| STD | 1.791 | 1.454 | −0.337 *** |

| N | 145 | 75 | 220 |

| Panel A | Panel B | |||

|---|---|---|---|---|

| Dependent Variable COD | Dependent Variable COD | |||

| Variables | Model (1) | Variables | Model (2) | Model (3) |

| Constant | 1.128 | Constant | −1.682 | −2.332 |

| (0.62) | (−0.31) | (−0.41) | ||

| FR | −1.083 ** | MA | −0.884 * | 0.958 |

| (−2.12) | (−1.28) | (0.51) | ||

| MDP | −0.014 | BIG4 | - | 0.875 |

| (−0.03) | (0.78) | |||

| FR × MDP | −0.519 * | MA × BIG4 | - | −2.154 |

| (−1.46) | (−1.07) | |||

| SIZE | 0.050 | SIZE | 0.138 | 0.136 |

| (0.47) | (0.41) | (0.38) | ||

| MB | 0.215 *** | MB | 0.229 * | 0.229 * |

| (2.47) | (1.53) | (1.5) | ||

| BETA | 0.409 * | BETA | −0.386 | −0.464 |

| (1.38) | (−0.42) | (−0.54) | ||

| DE | −0.025 ** | DE | −1.545 | −1.463 |

| (−2.03) | (−0.94) | (−0.86) | ||

| TIE | −0.000 | TIE | −0.000 | −0.000 |

| (−0.76) | (−0.32) | (−0.29) | ||

| STD | 0.712 *** | STD | 1.416 *** | 1.445 *** |

| (5.06) | (2.88) | (2.96) | ||

| Industry | Yes | Industry | - | - |

| Adj. R2 | 0.178 | Adj. R2 | 0.213 | 0.229 |

| N | 803 | N | 235 | 235 |

| Panel A | Panel B | |||

|---|---|---|---|---|

| Dependent Variable COD | Dependent Variable COD | |||

| Variables | Model (1) | Variables | Model (2) | Model (3) |

| Constant | 3.245 * | Constant | 0.178 | −1.024 |

| (1.28) | (0.03) | (−0.12) | ||

| FR | −1.618 ** | MA | −1.712 ** | 0.281 |

| (−2.09) | (−2.05) | (0.11) | ||

| MDP | −0.316 | BIG4 | - | 1.223 |

| (−0.71) | (0.65) | |||

| FR × MDP | −0.945 * | MA × BIG4 | - | −2.323 |

| (−1.32) | (−0.94) | |||

| SIZE | 0.024 | SIZE | 0.033 | 0.036 |

| (0.14) | (0.06) | (0.07) | ||

| MB | 0.238 ** | MB | 0.142 | 0.154 |

| (1.78) | (0.68) | (0.71) | ||

| BETA | −0.464 | BETA | −2.478 | −2.812 |

| (−0.79) | (−1.12) | (−1.23) | ||

| DE | −0.021 | DE | −0.876 | −0.586 |

| (−0.62) | (−0.33) | (−0.22) | ||

| TIE | −0.000 | TIE | −0.000 | −0.000 |

| (−0.76) | (−0.43) | (−0.36) | ||

| STD | 0.573 *** | STD | 2.623 *** | 2.722 *** |

| (3.25) | (2.71) | (2.76) | ||

| Industry | Yes | Industry | - | - |

| Adj. R2 | 0.072 | Adj. R2 | 0.067 | 0.062 |

| N | 495 | N | 125 | 125 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kuo, L.; Kuo, P.-W.; Chen, C.-C. Mandatory CSR Disclosure, CSR Assurance, and the Cost of Debt Capital: Evidence from Taiwan. Sustainability 2021, 13, 1768. https://doi.org/10.3390/su13041768

Kuo L, Kuo P-W, Chen C-C. Mandatory CSR Disclosure, CSR Assurance, and the Cost of Debt Capital: Evidence from Taiwan. Sustainability. 2021; 13(4):1768. https://doi.org/10.3390/su13041768

Chicago/Turabian StyleKuo, Lopin, Po-Wen Kuo, and Chun-Chih Chen. 2021. "Mandatory CSR Disclosure, CSR Assurance, and the Cost of Debt Capital: Evidence from Taiwan" Sustainability 13, no. 4: 1768. https://doi.org/10.3390/su13041768

APA StyleKuo, L., Kuo, P.-W., & Chen, C.-C. (2021). Mandatory CSR Disclosure, CSR Assurance, and the Cost of Debt Capital: Evidence from Taiwan. Sustainability, 13(4), 1768. https://doi.org/10.3390/su13041768