1. Introduction

Forecasting the movement of exchange rates has long been a hot topic in various application fields, attracting the interest of academics, financial traders, and monetary authorities alike. For foreign exchange traders and stock market investors, the ability to accurately forecast exchange rates is helpful in reducing risk and maximizing returns from transactions [

1,

2]. From the point of view of monetary authorities, reliable exchange rate forecasting also contributes to the management of exchange rates and conduction of monetary policies. Under a managed exchange rate regime, exchange rates are allowed to fluctuate within an undisclosed band, and the authorities may intervene in this regime depending on their future expectations of the exchange rates [

3]. Moreover, when a government uses monetary policies such as cutting interest rates to stimulate the economy, this will increase the income and demand for the imported goods of a country, appreciating the currency, which will ultimately negatively affect the competitiveness of exported goods. Hence, an accurate forecast of exchange rates can help a government to determine the sufficient level of interest rate cuts, which is related to evaluating the performance of monetary policies [

4,

5]. To accurately forecast exchange rates, academic researchers begin to study the behavior of exchange rates from a theoretical point of view. Many studies have been devoted to developing a variety of exchange rate determination models that link exchange rate levels to macro-economic variables [

6,

7]. The international debt theory, purchasing power parity, interest rate parity, and the asset market theory are well-known approaches that provide theoretical explanations for the relationship between exchange rates and economic fundamentals, such as a country’s balance of payments, price levels, real income levels, money supply, and interest rates, and other economic factors [

8,

9].

To understand whether these theories can provide a good approximation to the behavior of exchange rates, Meese and Rogoff investigated these and found that many economic forecasting models perform worse in terms of the out-of-sample forecasting of exchange rates than a simple driftless random walk (RW) model that only presumes that exchange rate forecasts are at the same level as the previous level of exchange rates [

10]. The subsequent literature further indicated that during the floating exchange rate period, the relationship between the nominal exchange rate and fundamentals such as money supplies, outputs, and interest rates is clearly weak; this is referred to as the “exchange rate disconnect puzzle” [

11]. Forecasting exchange rates, therefore, seems to be a difficult task.

Recent years have seen major progress in the development of sophisticated exchange rate forecasts. Ince, for example, used a specially constructed quarterly real-time dataset to evaluate the out-of-sample forecasting performance of linear models using purchasing power parity and Taylor rule fundamentals, with the former to work better at the 16-quarter and the latter at the one-quarter horizon [

12]. Cavusoglu and Neveu examined the role of consensus forecast dispersion in forecasting exchange rates; they found that consensus forecasts largely appear to be unbiased predictors of exchange rates in the long run, but most do not hold in the short run [

13]. Pierdzioch and Rülke examined whether the exchange rate forecasts made by experts reliably predict the future behavior of exchange rates in emerging markets; however, they obtained different results for different currencies. Their overall conclusion was that forecasts are often informative with respect to directional changes of exchange rates [

14]. Dick et al. used survey data concerning forecasts collected by individual professionals and showed that good performance in forecasting short-term exchange rates is correlated with good performance in forecasting fundamentals, especially interest rates [

15]. Ahmed et al. applied linear factor models that utilize the unconditional and conditional expectations of three currency-based risk factors to examining the predictability of exchange rates. They found that all the models had worse performance than a random walk with drift in out-of-sample forecasting of monthly exchange rate returns, and that the information embedded in currency-based risk factors does not produce systematic economic value for investors [

16].

Recent studies suggested that the relationship between exchange rates and fundamentals may be difficult to detect using the Meese and Rogoff approach. Amat et al. discarded conventional rolling or recursive regressions to obtain exchange rate forecasts and adopted a no-estimation approach from machine leaning to show that fundamentals can provide useful information to improve forecasts at a 1-month horizon, providing an improvement in the RW model [

17]. Cheung et al. comprehensively examined exchange rate forecasts from a large set of models and made a comparison of forecast performance against the RW model at various horizons by using different metrics and found that model/specification/currency combinations that could perform well in one period and one performance metric do not necessarily perform well in another period and/or performance metric [

18].

Given the shortcomings of the above models, this paper adopts another approach by using machine learning (ML) to forecast changes in exchange rates. ML has received attention from academia and industry. In particular, artificial neural networks (ANNs) and statistical learning methods frequently appear in the recent exchange rate prediction literature. Several complex artificial intelligence (AI) techniques are capable of handling nonlinear and nonstationary data across various areas. Specifically, they can be used in the management of medical insurance costs [

19], the refinement of multivariate regression methods [

20], the management of missing IoT data [

21], and the analysis of data on cancer mortality and survival [

22,

23].

Nosratabadi et al. conducted a comprehensive review of state-of-the-art ML and advanced deep learning (DL) methods in emerging economic and financial applications [

24]. Recent novel ML methods include the following: Lin et al. exerted feature selection and ensemble learning to improve the accuracy for bankruptcy prediction. Chen et al. proposed a bagged-pSVM and boosted-pSVM for bankruptcy prediction [

25]. Lee et al. used a support vector regression for the safety monitoring of commercial aircraft [

26]. Husejinovic applied naïve Bayesian and c4.5 decision tree classifiers to investigate credit card fraud detection [

27]. Benlahbib and Nfaoui proposed a hybrid approach based on opinion fusion and sentiment analysis to investigate reputation generation mechanisms [

28]. Zhang proposed an improved backpropagation neural network to analyze and forecast the aquatic product export [

29]. Sundar and Satyanarayana performed stock price prediction using multi-layer feed-forward neural networks [

30]. Hew et al. applied an artificial neural network (ANN) to investigate the resistances driving mobile social commerce. Lahmiri et al. utilized ensemble learning in financial data classification [

31]. Sermpinis et al. introduced a hybrid neural network structure based on particle swarm optimization and adaptive radial basis functions (ARBF-PSO), and a neural network fitness function for financial forecasting. This was achieved by benchmarking the ARBF-PSO results with those of three different neural network architectures (nearest neighbor algorithm (k-NN), autoregressive moving average model (ARMA), moving average convergence/divergence model (MACD), and naïve strategy) [

32].

Recent notable hybrid DL methods include the following: Lei et al. presented a time-driven feature-aware joint deep reinforcement learning (DRL) for financial signal representation and algorithmic trading [

33]. Vo et al. applied a long short-term memory (LSM) recurrent neural network to optimize socially responsible investment and portfolio decision making [

34]. Moews et al. proposed a DL method based on lagged correlation to forecast the directional trend changes in financial time series [

35]. Fang et al. provided a hybrid method that combined LSTM and support vector regression (SVR) on quantitative investment strategies [

36]. Long et al. presented a hybrid DL scheme based on a convolutional neural network (CNN) and recurrent neural network (RNN) for stock price movement prediction [

37]. Shamshoddin et al. suggested a DL-based collaborative filtering technique to predict consumer preferences in the electronic market [

38]. Altan et al. promoted a DL method based on LSTM and wavelet transform (EWT) for digital currency forecasting [

39]. Wang et al. proposed a hybrid method consisting of a long short-term memory network and a mean-variance model to optimize the formation of investment portfolios combined with asset pre-selection, thereby capturing the long-term dependence of financial time series data. The experiment used a lot of sample data from the British Stock Exchange 100 Index between March 1994 and March 2019. The study found that long short-term memory networks are suitable for financial time series forecasting, defeating other benchmark models by a clear advantage [

40].

Recent notable ML methods in exchange rate forecasting include the following: Amat exploited ML on the fundamentals of simple exchange rate models (purchasing power parity or uncovered interest parity) or Taylor’s rule-based models to improve exchange rate forecasts. The study concluded that fundamentals contain useful information and that exchange rates are predictable even at shorter horizons [

17]. Yaohao and Albuquerque’s work is based on a basic model consisting of 13 explanatory variables and analyzes spot exchange rate forecasts for ten currency pairs using support vector regression (SVR). Different nonlinear dependence structures introduced by the other nine kernel functions were tested, and the estimates were compared with a random walk benchmark. They tested the SVR model’s explanatory power gain over random walk by applying White’s Reality Check Test. Their results show that most SVR models achieve better out-of-sample performance than random walk, but they fail to achieve a statistically significant predictive advantage [

41]. Zhang and Hamoir adopted random forest, support vector machine, and neural network models in four fundamental models (uncovered interest rate parity, purchasing power parity, monetary model, and Taylor’s rule model). They used six different maturities of government bonds and four price indices to perform an integrated robustness test. Their findings show that the basic model incorporating modern ML has superior performance in predicting future exchange rates compared to the effects of random walks [

42]. Galeshchuk’s work discovered artificial neural networks’ economic purpose via describing and empirically testing foreign exchange market data. Panel data on exchange rates (USD/EUR, JPY/USD, USD/GBP) were examined and optimized for time series forecasting with neural networks. The best neural network with the best predictive power was found based on specific performance metrics [

43]. For DL methods, the deep belief network (DBN) model based on DL is a new forecasting method of exchange rate data. Its structure design and parameter learning rules are essential parts of the DBN model. Shen proposed an improved DBN for exchange rate forecasting. The DBN was constructed using a continuous restricted Boltzmann machine (CRBM), and the conjugate gradient method was used to accelerate learning. Weekly GBP/USD, BRL/USD exchange rates, and INR/USD exchange rate return values were predicted by the improved DBN [

44]. Zheng et al. conducted research, analyzed the results of training analysis, set up the nodes, adjusted the number of hidden nodes, input nodes, and hidden layers, and used multivariate analysis of variance to determine the sensitive range of the nodes. Finally, experiments on Indian Rupee/US dollar and RMB/US dollar exchange rates show that the improved DBN model can better predict the exchange rate than the feed-forward neural network model [

45]. Go and Hong employed DL to forecast stock value streams while analyzing patterns in stock prices. In the study, a deep neural network DL algorithm was designed to find patterns using time series techniques, which achieved high accuracy. The results were assessed by the percentage of the test set of 20 firms. An accuracy value of 86% was obtained for the DNN [

46].

Deep reinforcement learning (DRL) features scalability and has the potential to be applied to high-dimensional problems by combining noisy and nonlinear patterns of economic data. According to Mosavi et al.’s comprehensive review paper, the use of deep reinforcement learning in economics is proliferating [

47]. DRL opens vast opportunities for addressing complex dynamic economic systems through a wide range of capabilities from reinforcement learning (RL) to DL. A comprehensive survey revealed that DRL could offer better performance and higher efficiency than conventional algorithms while facing real economic problems in the face of increasing risk parameters and uncertainty [

47]. Recently emerging studies related to the use of DRL in economics include the following works. Zhang et al. used a DRL algorithm to design a trading strategy for continuous futures contracts. They compared their algorithm with a classical time series momentum strategy and showed that the study’s approach outperforms the baseline model and can lead to positive profits, but with the limitation of high transaction costs [

48]. The applications of deep deterministic policy gradient (DDPG) and deep Q-network (DQN) have received much attention in recent years. Xiong et al. introduced a DDPG-based DRL approach for stock trading [

49]. Li et al. proposed an adaptive DRL method based on DDPG for stock portfolio allocation [

50]. Liang used DDPG-based DRL in portfolio management [

51]. Li et al. presented a DQN-based DRL method to conduct an empirical study on efficient market strategy [

52]. Azhikodan introduced a stock trading bot based on a recurrent convolutional neural network (RCNN) and DRL [

53]. The applications of DRL in portfolio management also include advanced strategy in portfolio trading [

54] and dynamic portfolio optimization [

55]. Furthermore, online services’ application involves recommendation architecture [

56] and pricing algorithms for the online market [

57].

The literature review indicates that ML and DL have been widely used in economics research in stock markets, cryptocurrencies, marketing, corporate insolvency, and e-commerce. It reflects that ML and DL methods have received attention from economics in recent years, and the trends reveal that hybrid models outperform other single learning algorithms. A future trend will be the development of complex hybrid DL models [

24].

Although the predictive performance of these nonlinear AI methods is reported to surpass that of econometric models, issues such as hyperparameter optimization and overfitting may pose difficulties [

58]. For statistical learning methods, Vapnik developed a support vector machine (SVM) and successfully applied this to classification and regression problems in a variety of research fields such as tourism management, marketing, and bioinformatics [

59,

60,

61,

62,

63]. SVM is one of the most established methods in statistical learning. In particular, SVM based on the radial basis function (RBF) kernel has been widely utilized to deal with nonlinear problems. Support vector regression (SVR) is a closely related statistical learning approach and can be considered the application of SVM to regression. It is based on the theory of structural risk minimization (SRM) and minimizes errors on the basis of generalized errors. Therefore, SVR can theoretically guarantee that the optima it finds are global ones; neural network models, by contrast, easily fall into local optima. However, SVR needs appropriate model parameters to work effectively [

64,

65].

Recently, hybrid SVR models using evolutionary algorithms have also attracted much attention because of their promising predictive performance [

64,

66,

67]. Nevertheless, a hybrid SVR with hyperparameter optimization may not be able to meet robustness criteria. Moreover, several studies have shown that ML methods such as SVR and ANN are less accurate than conventional time series models for the problem of univariate time series with one-step prediction [

68,

69]. Clearly, there is still room for improvement in the accuracy of exchange rate forecasting. Feature selection is also a topic currently of great interest in machine learning. The feature selection method based on ensemble learning has received particular attention. This method, in which many different classifiers are generated as feature selectors and total results are then aggregated, is superior to the conventional single-feature selection method in several respects, most outstandingly in its ability to deal with robustness issues that often thwart existing single-feature selection methods [

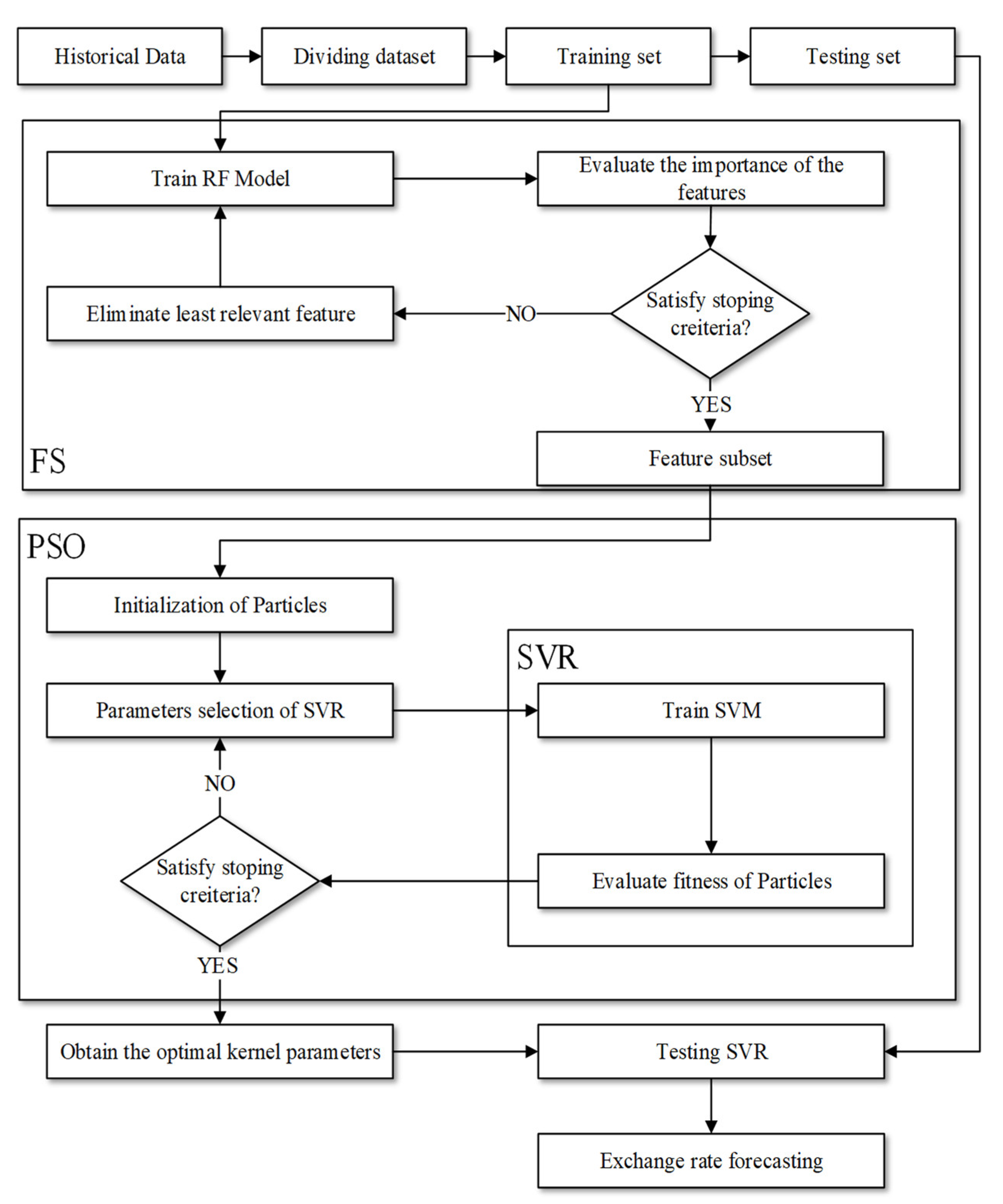

70]. Hence, this study develops a new SVR-based forecasting approach named FSPSOSVR, in order to accurately predict exchange rates. It is known that the benefits of artificial intelligence approaches depend on the use of appropriate parameter settings. Although different methods have been proposed to determine a suitable set of parameter values, there is still a lack of comprehensive guidelines for empirical researchers wishing to obtain robust results [

71]. To alleviate the negative effect of parameter settings on our empirical results, we combine particle swarm optimization (PSO), ensemble feature selection, and SVR to forecast the exchange rates. FSPSOSVR uses an ensemble feature selection mechanism. Compared to conventional single-feature selection techniques, ensemble feature selection has the advantage of robustness and shows great promise for use with high-dimensional samples of small size [

72]. More specifically, we used the random forest method, an ensemble approach based on a bagged strategy that samples a subset from the entire dataset to train the classifier. Several studies have shown that the random forest algorithm is robust to noise data [

73,

74]. As the monthly exchange rate is a dataset with a high dimension and small sample size, we expect FSPSOSVR to excel in robustness and predictive power.

Our analysis was conducted using the monthly data of exchange rates from January 1971 to December 2017 for seven countries. The out-of-sample forecast performance of the FSPSOSVR is compared with six competing forecasting models through the use of mean absolute percentage error (MAPE) and root mean square error (RMSE), including RW, exponential smoothing (ETS) [

75], autoregressive integrated moving average (ARIMA) [

76], seasonal ARIMA (SARIMA), SVR [

77], and PSOSVR. The contribution of this paper is in synthesizing the SVR model with an evolutionary mechanism, the PSO algorithm, which adjusts the SVR hyperparameters, and also in integrating it with a feature selection mechanism based on ensemble learning. Our algorithm was able to discover the exchange rates and achieve accurate and stable performance despite the nonlinearity of the problem. The robustness of the proposed algorithm was demonstrated by comparison with empirical results. To conclude, this approach incorporates foreign exchange carry trades to demonstrate the empirical relevance of exchange rate forecasts and specifically demonstrates the practicality of this approach for exchange carry trades. This work’s findings can contribute to the sustainability of business operations and the effective implementation of the central bank’s monetary policy to maintain a sustainable economic performance. For business sustainability, the findings can be applied to exchange rate risk management, enhancing foreign exchange risk visibility to reduce operational risk. The accurate currency forecasts can improve the profitability of carrying trade and achieve sustainable return performance. In terms of the sustainability of economies, the findings can design monetary policies to curb inflation, stabilize the consumer price index (CPI), achieve full employment and gross domestic product (GDP) growth, stabilize national economies, and promote stable economic growth.

4. Conclusions

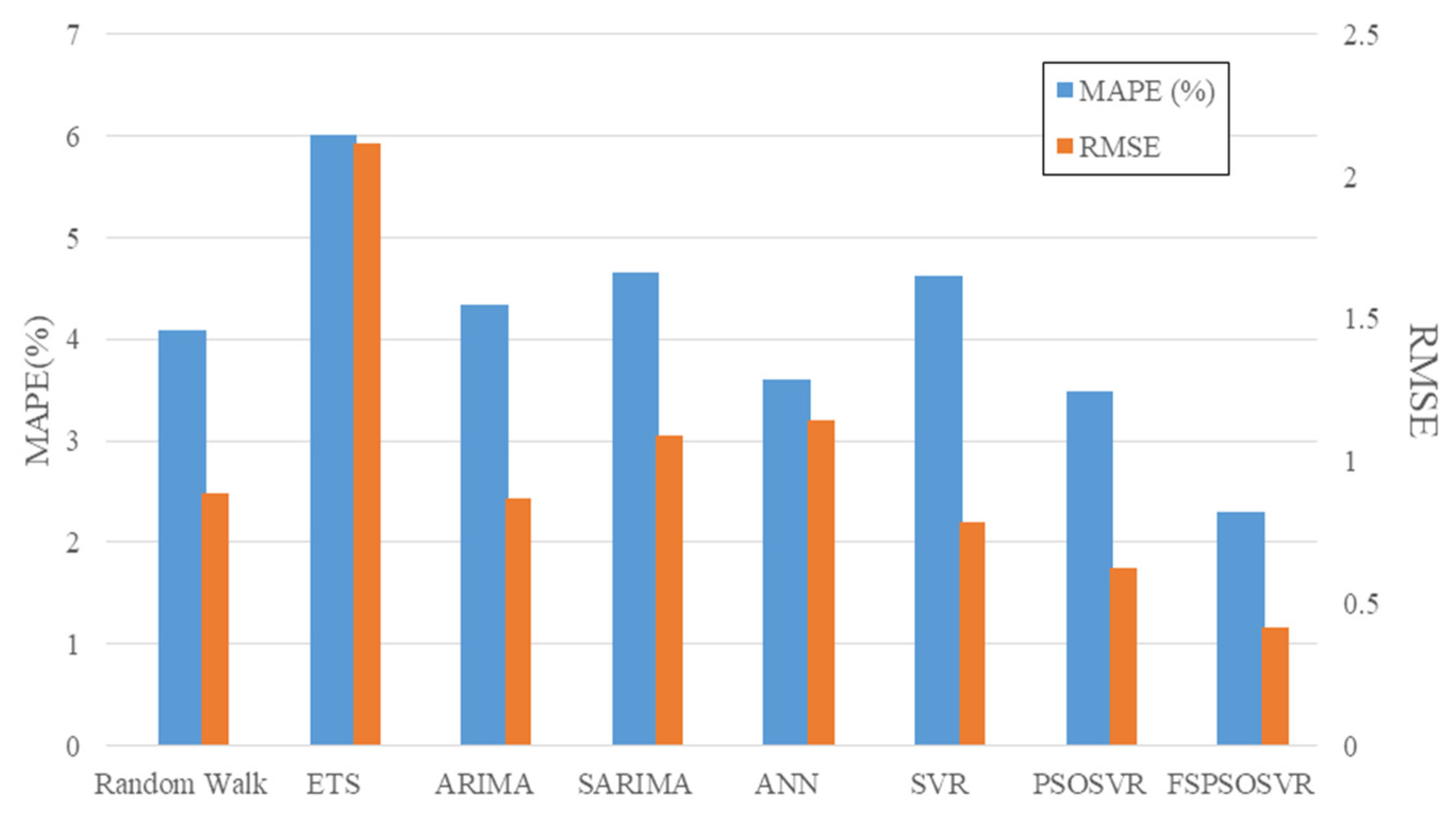

The cash flows of all international transactions are affected by expected changes in exchange rates. In this study, we developed an FSPSOSVR algorithm to forecast the exchange rates of seven countries, including the three worldwide major currencies including the euro, the Japanese yen, and the Chinese renminbi. Representative datasets were used in this study; they could validate the generality and robustness for each method. The original SVR method has the lack of an efficient and effective mechanism to discover the parameters and feature sets of data. In the FSPSOSVR algorithm, FS is able to select the important features, and PSO could optimize SVR parameters and hence improve the exchange rate forecasting accuracy. The predictive power of FSPSOSVR was compared with six predictive models, including those employing random walk, ETS, ARIMA, SARIMA, SVR, and PSOSVR. The results obtained using FSPSOSVR are more accurate than the results of SVR, indicating that the FSPSOSVR algorithm can optimize SVR parameters more effectively than SVR. Specifically, under the FSPSOSVR scheme, the MAPE was 2.296%, outperforming the 3.477%, 4.628%, 3.603%, 4.657%, 4.333%, 6.018%, and 4.089% of PSOSVR, SVR, ANN, SARIMA, ARIMA, EST, and RW, respectively. Due to limitations in the amount of data available, we only provided one-step forecasts. Future research can be directed toward the development of hybrid methods of combinations of long-term, high-frequency exchange rate data and fundamentals to provide multistep forecasts.

This paper contributes to the existing literature in the following aspects. (1) Econometric models are usually used to obtain exchange rate forecasts in the currency carry trade literature (cf. e.g., Jordà and Taylor [

1]; Lan, et al. [

109]). To the best of our knowledge, the present study is the first to apply the FSPSOSVR approach to carry trades and deliver excellent trading performance. The present findings suggest that ML methods can be used in actual financial transactions. (2) Most of the studies that have applied ML to exchange rate forecasting have typically used MAPE or MSE to measure forecasting performance. Financial trading is usually not considered under such approaches [

116,

117]. The demonstration of carry trading in the present article expands the possibility of applying machine learning-based forecasting to financial trading. (3) The O(

n3) time complexity in an SVR algorithm means that the performance of the SVR-based method may be reduced in big data applications [

118]. Nevertheless, the FSPSOSVR model outperformed all the other models in monthly rate forecasting. Therefore, applying it for analyzing small high-dimensional datasets may be feasible. Finally, we demonstrate the empirical relevance of exchange rate forecasts provided by our proposed FSPSOSVR model using carry trades; we observe that the carry trade performs well, yielding positive excess returns of more than 3% per annum for most currencies except for AUD and NTD.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}