Investment Leverage for Adaptive Reuse of Cultural Heritage

Abstract

:1. Introduction

- Adaptive reuse and energy retrofit of cultural built heritage structures;

- Protection and management of natural eco-systems;

- Local community social enterprise activities.

1.1. European Investment Stimulus

“If we manage to use our ever changing and vibrant European culture and heritage as a powerful catalyst for change, and as a vital component of a new European Bauhaus, the return on investment will be substantial.”[4]

1.2. The Cultural Built Heritage Investment Enigma

2. Methodology

2.1. Research Query

Can circular financial instruments be designed and tailored to protect people and ecosystems in parallel with adaptive reuse of vulnerable cultural heritage resources?

2.2. Defining the Terms of the Enquiry

2.2.1. Cultural Heritage

2.2.2. Cultural Capital

2.2.3. Adaptive Reuse

2.2.4. Circular Economy

2.3. Toolkit Design

- (i)

- Tool Knowledge relating to the operational characteristics of different financial instruments;

- (ii)

- Design Knowledge (including blending capacity) to facilitate matching complementary instruments to the needs of target recipients in order to relieve the burden of investment funding gaps, remove investment barriers and avoid displacement;

- (iii)

- Stakeholder Knowledge including collaborative partnership motivations and capacity to engage [25].

3. The Role of Market Spheres for Investment Leverage

- Supra national entities, such as, the European Commission (EC), European Structural and Investment Fund (ESIF), European Social Fund (ESF), European Central Bank (ECB), Council of Europe Development Bank (CEB) and Climate Bank (CB);

- Public sector state authorities, state agencies and quasi agencies;

- Private sector non-profit foundations and trusts (philanthropy);

- Private sector for-profit investment, development, financial and enterprise entities, including certified B-Corporations (purpose with profit);

- Public–Private Partnership arrangements, more recently Public, Private, People Partnership arrangements, including local community initiatives.

3.1. Investment Motivations of Market Spheres

- 1st Market Sphere: Direct and indirect public action for the common good (funded by tax collection and borrowing);

- 2nd Market Sphere: Profit motivated business entities (tax liability);

- 3rd Market Sphere: Mission motivated non-profit philanthropic entities (tax exempt) such as cultural foundations and charitable trusts;

- Hybrid traditional Public–Private Partnership models, including 1st, 2nd and 3rd Spheres.

- 4th Market Sphere: Profit and intentional measured impact motivated socio-cultural and environmental entities with complex legal and tax structures due to hybrid for-profit, reduced-profit and non-profit structures.

3.2. Public–Private Partnerships Structures

4. Creating Circular Hybrid Financial Instruments for the Common Good

4.1. Financial Instruments

- Leverage capacity to attract combined public and private resources;

- Revolving capacity to generate recycled flows of money via loan repayments (debt) or the realisation of investments (equity);

- Circular revenue generation and regeneration;

- Access to private sector financial tools and expertise to support public policy goals within collaborative public–private fund structures [40].

4.2. Hybrid Financial Instruments and Tailored Financing

- Leverage: Use of development finance and philanthropic funds to attract private capital into deals;

- Impact Return: Investments that drive measured social, environmental and economic progress;

- Financial Return: Financial returns for private investors in line with market expectations, based on real and perceived risks [40].

4.3. Sustainable and Circular Financial Reporting

4.4. Circular Business Models

5. Understanding Risk-adjusted Market and Impact Return Metrics

- Risk adjusted Market Return on capital or Below Market Return of capital;

- Risk adjusted Impact Return;

5.1. Market Return Metrics

5.2. Impact Return Metrics

- Sources of capital for impact investing asset managers originated from pension funds, companies, commercial investors, financial institutions, development financial institutions, High Net Worth Individuals, (HNWIs), foundations, Fund of Funds (FoF), sovereign wealth funds, endowments and ‘faith-based’ spiritual institutions;

- Private equity focused investors are more lightly to seek risk adjusted market rate returns, while private debt focused investors are more likely to employ capital preservations investment strategies;

- Returns from private equity investments, as an asset class, are more volatile, with greater return ranges than private debt and real assets [57].

Social Enterprise Investment for Impact versus Investment with Impact

- Investors for impact (Impact 1st) prioritize the achievement of intentional longterm social impact (patient investors) with or without financial return, ranging from financial loss to capital preservation below market return.

- Investors with impact (Finance 1st) prioritize the achievement of positive financial returns, with the achievement of social impact as a secondary goal [58];

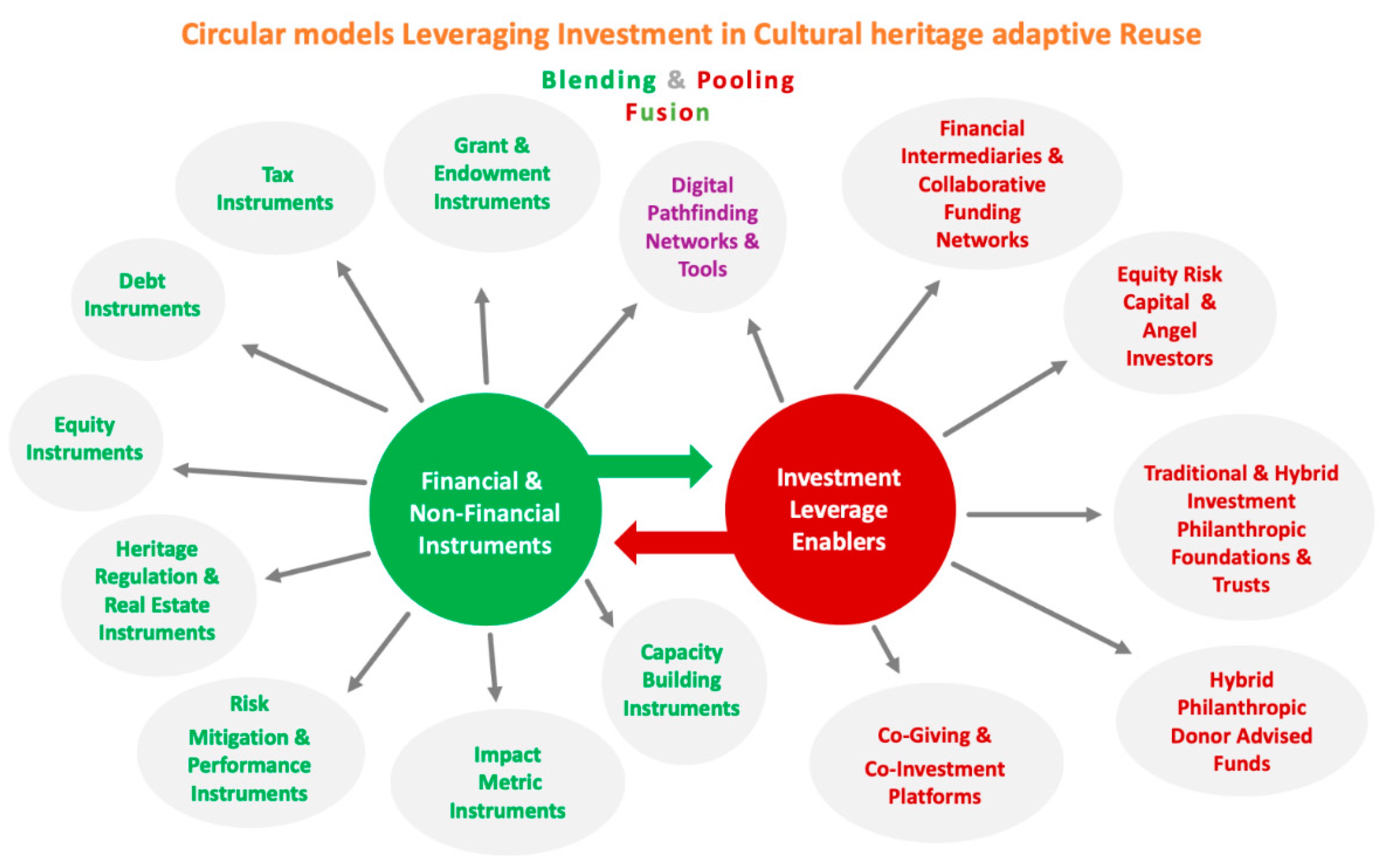

6. Arriving at an Integrated Panoptic Investment Leverage Toolkit for the Adaptive Reuse of Cultural Heritage

- (i)

- Blended with complementary instruments within tailored heritage-led, place-led or typology-led* initiatives;

- (ii)

- Pooled within collaborative hybrid fund structures.

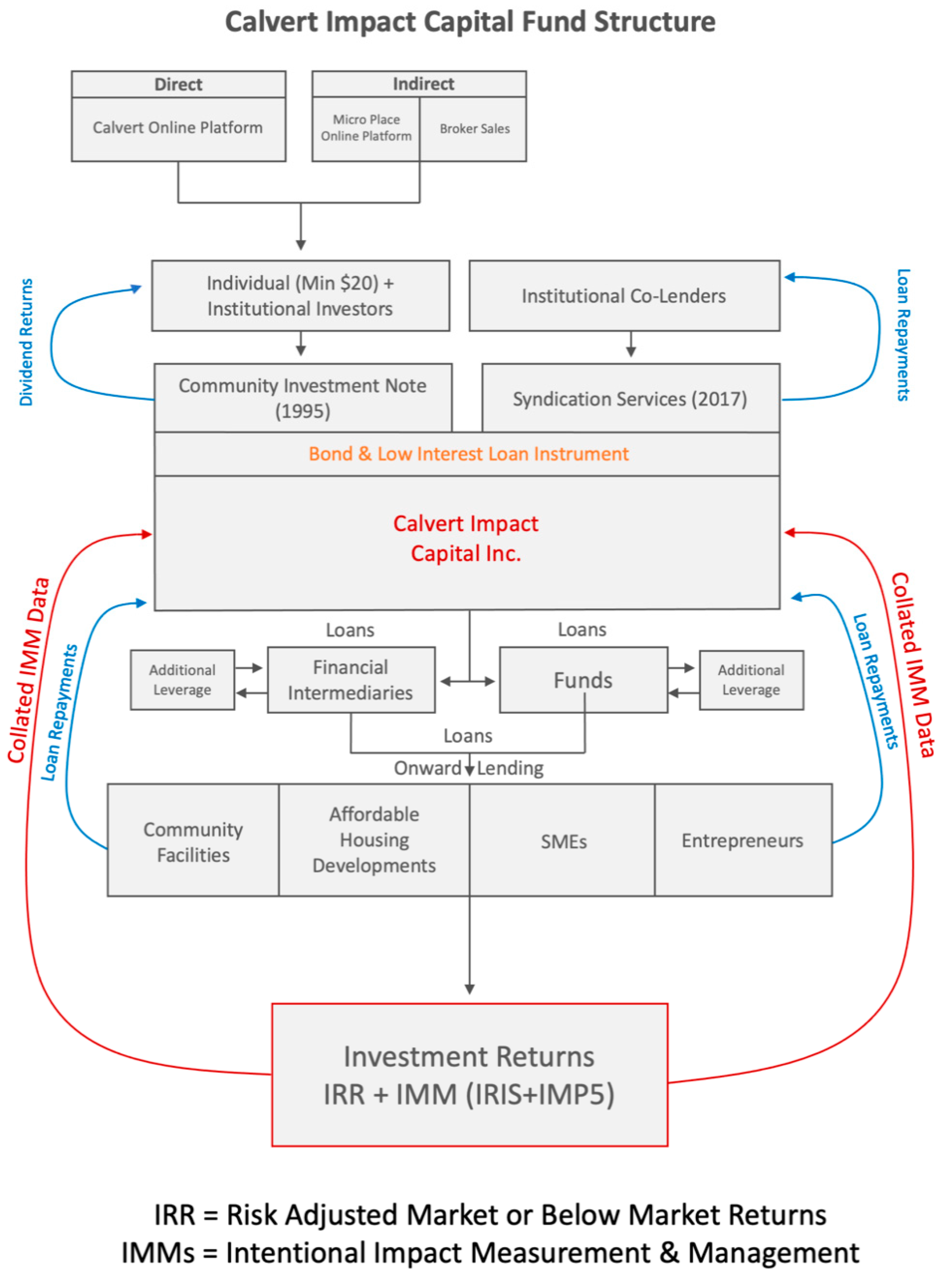

7. Case Study: Calvert Impact Fund (USA)

- Community Investment Note (short-term bond);

- Co-lending syndication service.

7.1. Calvert Community Investment Note

7.2. Calvert Co-lending Syndication Service

7.3. Catalytic and Revolving Investment Leverage and Capacity Building Support

7.4. Calvert Intentional Impact Metrics

- Investor Impact: measuring benefits for individual and institutional investors and co-lenders;

- Portfolio Impact: measuring the value and sustainable growth opportunities that leveraged capital provided to borrowers;

- Community Impact: measuring inequality and climate change solutions achieved from capital invested in global communities [59].

7.5. Viewing Calvert Hybrid Impact Fund Structure in the Context of the Panoptic CLIC Toolkit

8. Concluding Observations

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- UN Habitat. World Cities Report: The Value of Sustainable Urbanisation. 2020. Available online: https://unhabitat.org/sites/default/files/2020/11/world_cities_report_2020_abridged_version.pdf (accessed on 4 January 2021).

- ECA. European Court of Auditors, EU Investments in Cultural Sites: A Topic That Deserves More Focus and Coordination, Special Report 08/2020. 2020. Available online: https://op.europa.eu/webpub/eca/special-reports/cultural-investments-08-2020/en/ (accessed on 29 December 2020).

- EIB. Togetherness a New Heritage Deal for Europe, Written by Hermann Parzinger, 15th Essay in Big Ideas Series of European Investment Bank. 2020. Available online: https://www.eib.org/en/essays/new-heritage-deal-for-europe (accessed on 5 February 2021).

- Von der Leyen. State of the Union Address by President von der Leyen at the European Parliament Plenary, 16th September 2020, Brussels (Speech/20/1655). 2020. Available online: https://ec.europa.eu/commission/presscorner/detail/en/AC_20_1916 (accessed on 10 December 2020).

- CAE; ECF; EHA. Cultural Deal for Europe jointly Developed by Culture Action Europe (CAE), European Cultural Foundation (ECF), and Europe Nostra & European Heritage Alliance (EHA). 2020. Available online: http://cultureactioneurope.org/news/a-culture-deal-for-europe (accessed on 3 January 2021).

- EU. The Human Centred City: Recommendations for Research and Innovation Actions, Independent Expert Report. 2020. Available online: https://op.europa.eu/en/publication-detail/-/publication/5b85a079-2255-11ea-af81-01aa75ed71a1/language-en/format-PDF/source-search (accessed on 11 February 2021).

- EP. Resolution of 20 January 2021 (2019/2194(INI)) P9_TA-PROV(2021)0008, Initiated by MEP Dace Melbarde (ECR Latvia). 2021. Available online: https://www.europarl.europa.eu/doceo/document/A-9-2020-0210_EN.html (accessed on 6 February 2021).

- Quaedvlieg-Mihailovic. Speech by Sneska Quaedvlieg-Mihailovic. 2021. Available online: https://www.europanostra.org/ep-plenary-adopts-ambitious-report-on-the-legacy-of-the-european-year-of-cultural-heritage/ (accessed on 13 February 2021).

- Potts, A. European Cultural Heritage Green Paper, Europa Nostra, The Hague & Brussels. 2021. Available online: https://issuu.com/europanostra/docs/20210322-european_cultural_heritage_green_paper_fu (accessed on 5 April 2021).

- EC. A New Circular Economy Action Plan for a Cleaner and More Competitive Europe, Brussels, 11.1.2020, COM (2020) 98 final. 2020. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52020DC0098 (accessed on 10 February 2021).

- ARUP, BAM & CE100. Circular Business Models for the Built Environment, ARUP, BAM, CE100, Supported by Ellen MacArthur Foundation. 2016. Available online: https://www.ellenmacarthurfoundation.org/ce100/the-programme/enabling-collaboration (accessed on 14 September 2020).

- ARUP. The Circular Economy in the Built Environment. 2016. Available online: https://www.arup.com/perspectives/publications/research/section/circular-economy-in-the-built-environment (accessed on 14 September 2020).

- ARUP & EMF. From Principles to Practice: Realising the Value of Circular Economy in Real Estate. 2020. Available online: https://www.arup.com/perspectives/publications/research/section/realising-the-value-of-circular-economy-in-real-estate (accessed on 27 January 2021).

- EC. A Renovation Wave for Europe Greening our Buildings, Creating Jobs, Improving Lives, Building Brussels, 14.10.2020, COM(2020) 662. 2020. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52020DC0662 (accessed on 9 November 2020).

- EU. Renovation Wave: The European Green Deal. 2020. Available online: https://ec.europa.eu/commission/presscorner/detail/en/FS_20_1844 (accessed on 2 January 2021). [CrossRef]

- CLIC Project Deliverables. Available online: https://www.clicproject.eu/deliverables/ (accessed on 20 April 2021).

- Kobalt, C. Optimising the Use of Cultural Heritage. In Economic Perspectives on Cultural Heritage; Hutter, M., Rizzo, I., Eds.; MacMillan: London, UK, 1997. [Google Scholar]

- Vecco, M. A Definition of Cultural Heritage: From the Tangible to the Intangible. J. Cult. Herit. 2010, 11, 321–324. [Google Scholar] [CrossRef]

- Hutter, M.; Rizzo, I. (Eds.) Economic Perspectives on Cultural Heritage; MacMillan: London, UK, 1997. [Google Scholar]

- Throsby, D. Seven Questions in the Economics of Cultural Heritage. In Economic Perspectives on Cultural Heritage; Hutter, M., Rizzo, I., Eds.; MacMillan Press Ltd.: London, UK, 1997; pp. 13–30. [Google Scholar]

- Throsby, D. Heritage Economics: A Conceptual Framework. In The Economics of Uniqueness, Investing in Historic City Cores and Cultural Heritage Assets for Sustainable Development; Urban Development Series; Liccoardi, G., Amirtahmasebi, R., Eds.; The World Bank: Washington, DC, USA, 2012; Available online: https://openknowledge.worldbank.org/handle/10986/12286 (accessed on 2 November 2020).

- Foster, G.J. Circular Economy Strategies for Adaptive Reuse of Cultural Heritage Buildings to Reduce Environmental Impacts, Resources Conservation Recycling 152 104507, Elsevier. 2020. Available online: https://doi.org/10.1016/j.resconree.2019.104507 (accessed on 9 February 2021).

- Ellen MacArthur Foundation Definition of Circular Economy. Available online: https://www.ellenmacarthurfoundation.org/explore/the-circular-economy-in-detail (accessed on 4 February 2021).

- Girard, L.F. Implementing the circular economy: The role of cultural heritage as the entry point. Which evaluation approaches? BDC Boll. Del Cent. Calza Bini 2019, 9, 245–277. Available online: https://doi.org/10.6092/2284-4732/7269 (accessed on 10 December 2020).

- Pickerill, T.; Armitage, L. The Management of Built Heritage, A Comparative Review of Policies & Practice in Western Europe, North America & Australia, Pacific Rim Real Estate Society Conference, Sydney. 2009. Available online: https://arrow.tudublin.ie/beschreccon/36/ (accessed on 20 January 2021).

- Girard, L.F.; Gravagnuolo, A. Circular Economy and Cultural Heritage /Landscape Regeneration. Circular business, financing and governance models for a competitive Europe, Circular City and Cultural heritage Interplay. BDC Boll. Del Cent. Calza Bini 2018, 17, 35–52. Available online: https://doi.org/10.6092/2284-4732/5472 (accessed on 10 December 2020).

- EC. The Just Transition Mechanism: Making sure no one is left behind. 2020. Available online: https://ec.europa.eu/commission/presscorner/detail/en/fs_20_39 (accessed on 11 March 2021). [CrossRef]

- Gianoncelli, A.; Boiardi, P. Financing for Social Impact—The Key Role of Tailored Financing and Hybrid Finance. Available online: https://evpa.eu.com/uploads/publications/EVPA_Financing_for_Social_Impact_2017_online.pdf (accessed on 3 January 2021).

- Volkmann, C.; Tokarski, K.; Ernst, K. Financing Social Entrepreneurship in Volkmann Tokarski and Ernst. In Social Entrepreneurship and Social Business; Springer Gabler: Wiesbaden, Germany, 2012. [Google Scholar]

- Salamon, L.M. (Ed.) New Frontiers of Philanthropy; Oxford University Press: Oxford, UK, 2014; ISBN 978-0-19-935754-3. [Google Scholar]

- Leigland, J. Public Private Partnership in Developing Countries: The emerging evidenced based critique. World Bank Res. Obs. 2018, 33, 103–134. [Google Scholar] [CrossRef] [Green Version]

- O’Shea, C.; Palcic, D.; Reeves, E. Using PPP to Procure Social Infrastructure: Lessons Learned from 20 years of experience in Ireland. Public Works Manag. Policy 2020. [Google Scholar] [CrossRef]

- EPEC. Value for Money Assessment: Review of Approaches and Key Concepts, European PPP Expertise Centre with European Investment Bank. 2015. Available online: https://www.eib.org/en/publications/epec-value-for-money-assessment (accessed on 10 February 2021).

- EPEC. Hurdles to PPP Investments: A Contribution to the Third Pillar of the Investment Plan for Europe, IMF Fiscal Affairs Department, European PPP Expertise Centre with European Investment Bank. 2016. Available online: https://www.eib.org/en/publications/hurdles-to-ppp-investments (accessed on 12 February 2021).

- IMF. Public Private Partnerships, IMF Fiscal Affairs Department. 2004. Available online: https://www.imf.org/external/np/fad/2004/pifp/eng/031204.pdf (accessed on 2 February 2021).

- OECD. Public Private Partnerships: In Pursuit of Risk Sharing and Value for Money. 2008. Available online: https://www.oecd.org/gov/budgeting/public-privatepartnershipsinpursuitofrisksharingandvalueformoney.htm (accessed on 10 February 2021).

- World Bank Institute. Value for Money Analysis, Practices and Challenges, World Bank Institute (WBI). 2013. Available online: http://documents1.worldbank.org/curated/en/724231468331050325/pdf/840800WP0Box380ey0Analysis00PUBLIC0.pdf (accessed on 10 February 2021).

- O’Shea, C.; Palcic, D.; Reeves, E. Comparing PPP with traditional procurement: The case for schools procurement in Ireland. Ann. Public Coop. Econ. 2019, 90, 245–267. [Google Scholar] [CrossRef]

- OECD. Social Impact Investing—Building the Evidence Base. 2015. Available online: https://read.oecd-ilibrary.org/finance-and-investment/social-impact-investment_9789264233430-en#page1 (accessed on 2 February 2021).

- WEF/OECD. Blended Finance Vol.1 A Primer for Development Finance and Philanthropic Funders. 2015. Available online: http://www3.weforum.org/docs/WEF_Blended_Finance_A_Primer_Development_Finance_Philanthropic_Funders.pdf (accessed on 5 February 2021).

- EIB. Introducing Financial Instruments for the European Social Fund, Fi-Compass. 2016. Available online: https://www.fi-compass.eu (accessed on 14 February 2021).

- EIB. Stocktaking Study on Financial Instruments by Sector, Fi-Compass ERDF. 2020. Available online: www.fi-compass.eu (accessed on 14 February 2021).

- OECD. Blended Finance Principles for Sustainable Development. 2020. Available online: http://www.oecd.org/officialdocuments/publicdisplaydocumentpdf/?cote=DCD/DAC(2020)42/FINAL&docLanguage=En (accessed on 6 February 2021).

- ECA. European Court of Auditors, Rapid Case Review: Reporting on Sustainability: A Stocktake of EU Institutions and Agencies, June 2019. Available online: https://www.eca.europa.eu/Lists/ECADocuments/RCR_Reporting_on_sustainability/RCR_Reporting_on_sustainability_EN.pdf (accessed on 4 February 2021).

- MSCI. The MSCI Principles of Sustainable Investing, Morgan Stanley Capital International. 2019. Available online: https://www.msci.com/documents/10199/16912162/MSCI-ESG-House-View-FINAL.pdf/63bba1a1-aecf-ba80-aa49-7910748ed942 (accessed on 3 February 2021).

- Kempeneer, S.; Peeters, M.; Compernolle, T. Bringing the User Back in the Building: Analalysis of ESG in Real Estate and a Behavioral Framework to Guide Future Research. Sustainability 2021, 13, 3239. [Google Scholar] [CrossRef]

- ESMA. Letter to Commissioner in Charge of Financial Services, Financial Stability and Capital Markets Union of the European Commission, from European Securities and Markets Authority, ESMA 30-379-423 28 January 2021, Signed by Steven Maijoor. 2021. Available online: https://www.esma.europa.eu/sites/default/files/library/esma30-379-423_esma_letter_to_ec_on_esg_ratings.pdf (accessed on 10 February 2021).

- EC. Acton Plan: Financing Sustainable Growth, COM(2018) 097 Final, Brussels 8.3.2018. 2019. Available online: https://ec.europa.eu/transparency/regdoc/rep/1/2018/EN/COM-2018-97-F1-EN-MAIN-PART-1.PDF (accessed on 2 January 2021).

- EU. Regulation 2020/852 on the Establishment of a Framework to Facilitate Sustainable Investment, and Amending Regulation (EU) 2019/2008. 18 June 2020. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:32020R0852 (accessed on 14 February 2021).

- EU TEG. Taxonomy: Final Report of the Technical Expert Group on Sustainable Finance. 2020. Available online: https://knowledge4policy.ec.europa.eu/publication/sustainable-finance-teg-final-report-eu-taxonomy_en (accessed on 6 February 2021).

- EU TEG. EU Technical Expert Group on Sustainable Finance, Statement of the EU TEG on Sustainable Finance. Five High Level Princi-ples for Recovery and Resilience. 2020. Available online: https://ec.europa.eu/info/publications/sustainable-finance-technical-expert-group_en (accessed on 4 February 2021).

- EIB. A Sustainable Way of Achieving EU Economic and Social Objectives: Financial Instruments, Fi-Compass. 2015. Available online: https://www.fi-compass.eu/sites/default/files/publications/ESIF_A_sustainable_way_of_achieving_EU_economic_and_social_objectives_EN.pdf (accessed on 2 February 2021).

- Linneman, P.; Kirsch, B. Real Estate Finance & Investments Risks and Opportunities, 5th ed.; Linneman Associates: Philadelphia, PA, USA, 2020; ISBN 978-1-7923-3191-6. [Google Scholar]

- GIIN. Impact Investing Decision Making Insights on Financial Performance, Global Impact Investing Network. 2021. Available online: https://thegiin.org/research/publication/impact-investing-decision-making-insights-on-financial-performance (accessed on 17 February 2021).

- GIIN. The State of Impact Measurement and Practice, 2nd ed.; Global Impact Investing Network. 2020. Available online: https://thegiin.org/research/publication/imm-survey-second-edition (accessed on 2 February 2021).

- Gianoncelli, A.; Martínez, A.P. The Investing for Impact Toolkit; European Venture Philanthropy Association (EVPA). 2020. Available online: https://evpa.eu.com/knowledge-centre/publications/investing-for-impact-toolkit (accessed on 1 February 2021).

- GIIN. Annual Impact Survey 2020, 10th ed., Global Impact Investing Network. 2020. Available online: https://thegiin.org/research/publication/impinv-survey-2020 (accessed on 2 February 2021).

- Gianoncelli, A.; Boiardi, P. Impact Strategies—How Investors Drive Social Impact; European Venture Philanthropy Association (EVPA): Brussels, Belgium, 2018; ISBN 9789082494082. Available online: https://evpa.eu.com/uploads/publications/EVPA_Impact_Strategies_2018.pdf (accessed on 2 February 2021).

- CIC. Calvert Impact Capital Impact Report 2020: Investing for a More Equitable World, USA. 2020. Available online: https://www.calvertimpactcapital.org/impact/2020-impact-report (accessed on 11 February 2021).

- Calvert Impact Capital Portfolio Alignment with SDGs. Available online: www.calvertimpactcapital.org/portfolio/sdgs (accessed on 10 February 2021).

- Calvert Impact Capital Portfolio List. Available online: www.calvertimpactcapital.org/portfolio/list (accessed on 10 February 2021).

{kind=link}

{kind=link}

| Investment Leverage Enablers | Financial and Non-financial Instruments |

|---|---|

|

|

| Traditional Grant Instruments | Grant and Endowment Instrument Enhancements |

|---|---|

| Direct or Matching Philanthropic Grant aid including in-kind volunteer contributions Mortgage subsidy | Philanthropic Grants and Endowments combined with capacity building mentoring Grants funded by Crowd Funding Ventures Prize and Competition Grant Awards |

| Traditional Tax Instruments | Tax Instrument Enhancements |

| Tax deduction, exemption or freeze: Income/Corporation (Tax Credits) including tax-deductible sponsorship Property Tax Value Added Tax (VAT)/Sales Tax Transfer Tax (Stamp Duty) Capital Gains Tax and Inheritance Tax Land Value Capture (LVC) Instruments | Place-led, Heritage-led and Typology-led Tax Credit Initiatives Tax Increment Financing (TIF) Bond Instruments (form of Land Value Capture) Art-Bonus, Eco-Bonus, Super Bonus and Façade Bonus Tax Credits |

| Traditional Debt Instruments | Debt Instrument Enhancements |

| Loans (Debt): Commercial Bank Loans Government loan (0% or low interest) | Loans (Debt): Venture Capital Loan Quasi Equity Venture Capital Loan Micro Finance Investment Vehicles Revolving Loan Funds Green Finance Loans Energy Efficiency Mortgage Label |

| Bonds (Debt): Government Bonds | Bonds (Debt): Social Impact Government Bonds (tax exempt) Social Impact Corporate Bonds (Long term Bond/Short term Note) Tax Increment Finance (TIF) Bond Instruments (form of Land Value Capture) Human Capital Performance Bonds (Risk Performance Instrument) |

| Traditional Equity Instruments | Equity Risk Capital Instruments |

| Internal Rate of Return (IRR) Opportunity Cost of Capital (OCC) | Equity Share Instruments Quasi Debt/Equity Share Instruments ESG and Social/Environmental Impact Stock Exchange public listing Private Placement Bond Market |

| Risk Mitigation Instruments | Risk Mitigation and Performance Instruments |

| Government Loan Guarantee (on Commercial Bank Loan) | Corporate or Philanthropic Loan Guarantee Risk Performance Instruments (Human Capital Performance Bonds) Micro Insurance (low-income recipient) |

| Traditional Impact Metric Instruments | Impact Metric Instrument |

| Real Estate and Construction Market Metrics GRESB: Global Real Estate Sustainability Benchmark (ESG Integration) Wired Score Certification LEED and BREEAM Certification WELL Certification RESET Air Certification nZeb Certification (EPBD) Net Zero Carbon Standard (World Green Building Council WGBC) | Governance Metrics ESG Compliance incorporating SDGs mapping EU Taxonomy Compliance B Corporation Certification Financial Metrics Internal Rate of Return (IRR) Opportunity Cost of Capital (OCC) Intentional Impact Metrics IRIS Catalogue of Metrics IRIS+ Core Metric Sets Impact Management Projects (IMP) Financial Markets |

| Heritage Regulation and Real Estate (RE) Instruments | Heritage Regulation and Real Estate (RE) Instrument Enhancements |

| Direct and Indirect Investment Structures: Public–Private Partnership (PPP) Quasi Development Agencies Master Planning Strategic Development Zones | Direct Investment Structures: Public–Private Partnership (PPP) Public–Private People Partnerships Joint Ventures Schemes Public Asset Corporations (publicly owned and privately managed) Indirect Investment Structures: Real Estate Investment Trusts (listed or unlisted) Real Estate Investment Companies and Funds (listed or unlisted) B Corporation (public benefit for-profit) Revolving Funds |

| Real Estate Regulatory Instruments: Transfer Development Rights (TDR) Planning Bonus Easement Donations | Real Estate Regulatory Instruments: Land Value Capture (LVC) Betterment Levies and Taxes Developer Contributions Leveraging public land assets. Renovation Lease Social Value Lease Energy Efficiency Mortgage Label |

| Direct Service Provision and Advisory Instruments (Cultural Heritage) | Capacity Building Instruments (Networking, Mobilisation and Mentoring) |

| Technical or Advisory Service by Supra-national or National Government Agency | Networking and Mobilising Collaboration Technical business mentoring (Social Enterprise Angel Investors) Education and Skills Training Technical Repair and Maintenance Support |

| Digital Pathfinding Online Portals/Tools: | |

| Cultural Heritage Portals Environmental Portals Philanthropic and Social Enterprise Impact Investment Portals Stock Exchange Portals Crowd Funding Portals Lottery Funding Portals | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pickerill, T. Investment Leverage for Adaptive Reuse of Cultural Heritage. Sustainability 2021, 13, 5052. https://doi.org/10.3390/su13095052

Pickerill T. Investment Leverage for Adaptive Reuse of Cultural Heritage. Sustainability. 2021; 13(9):5052. https://doi.org/10.3390/su13095052

Chicago/Turabian StylePickerill, Tracy. 2021. "Investment Leverage for Adaptive Reuse of Cultural Heritage" Sustainability 13, no. 9: 5052. https://doi.org/10.3390/su13095052

APA StylePickerill, T. (2021). Investment Leverage for Adaptive Reuse of Cultural Heritage. Sustainability, 13(9), 5052. https://doi.org/10.3390/su13095052