Exploring the Inclusion of Sustainability into Strategy and Management Control Systems in Peruvian Manufacturing Enterprises

Abstract

:1. Introduction

2. Theoretical Development

2.1. Brief Industry Description

2.2. Literature Review

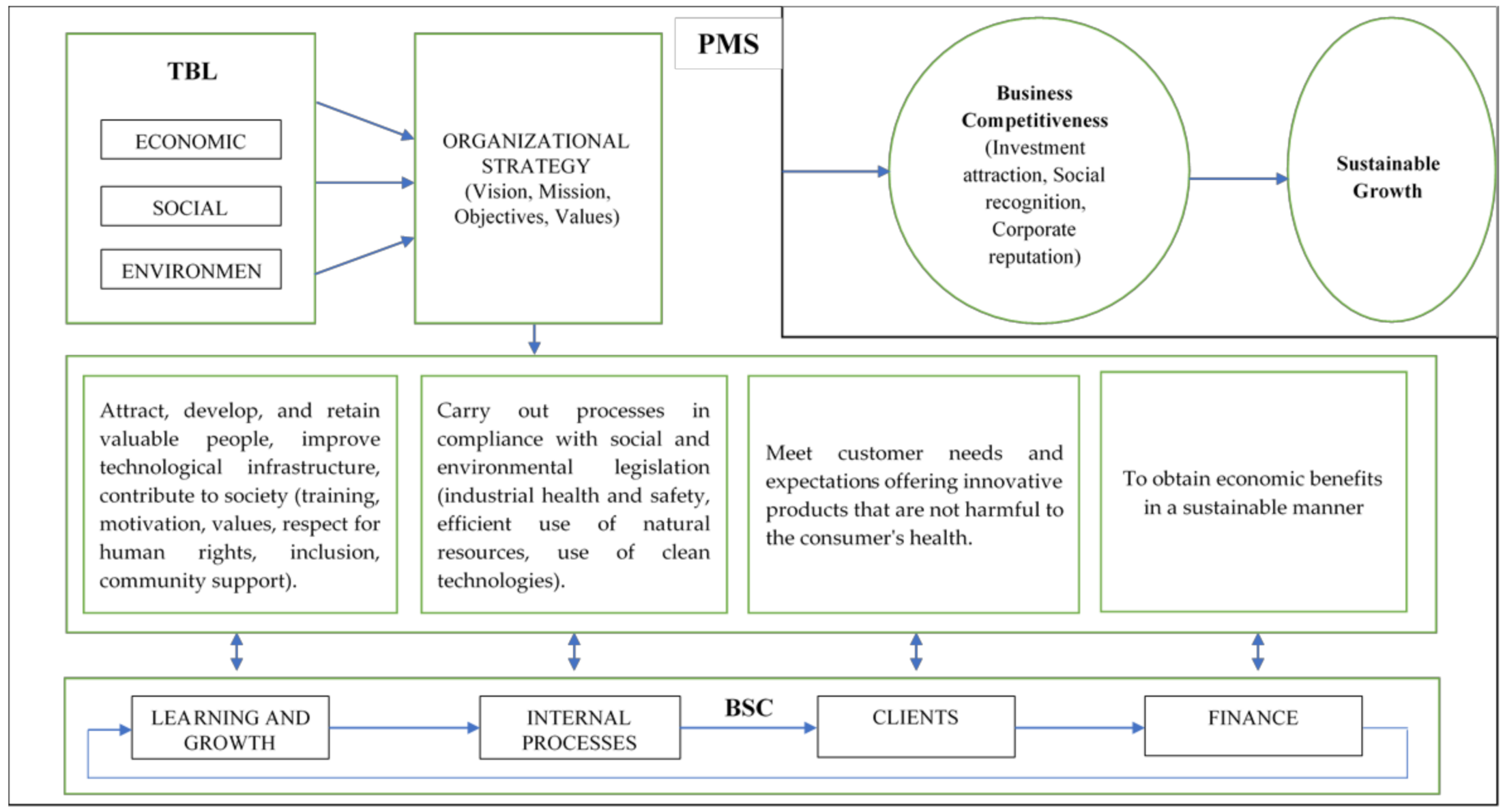

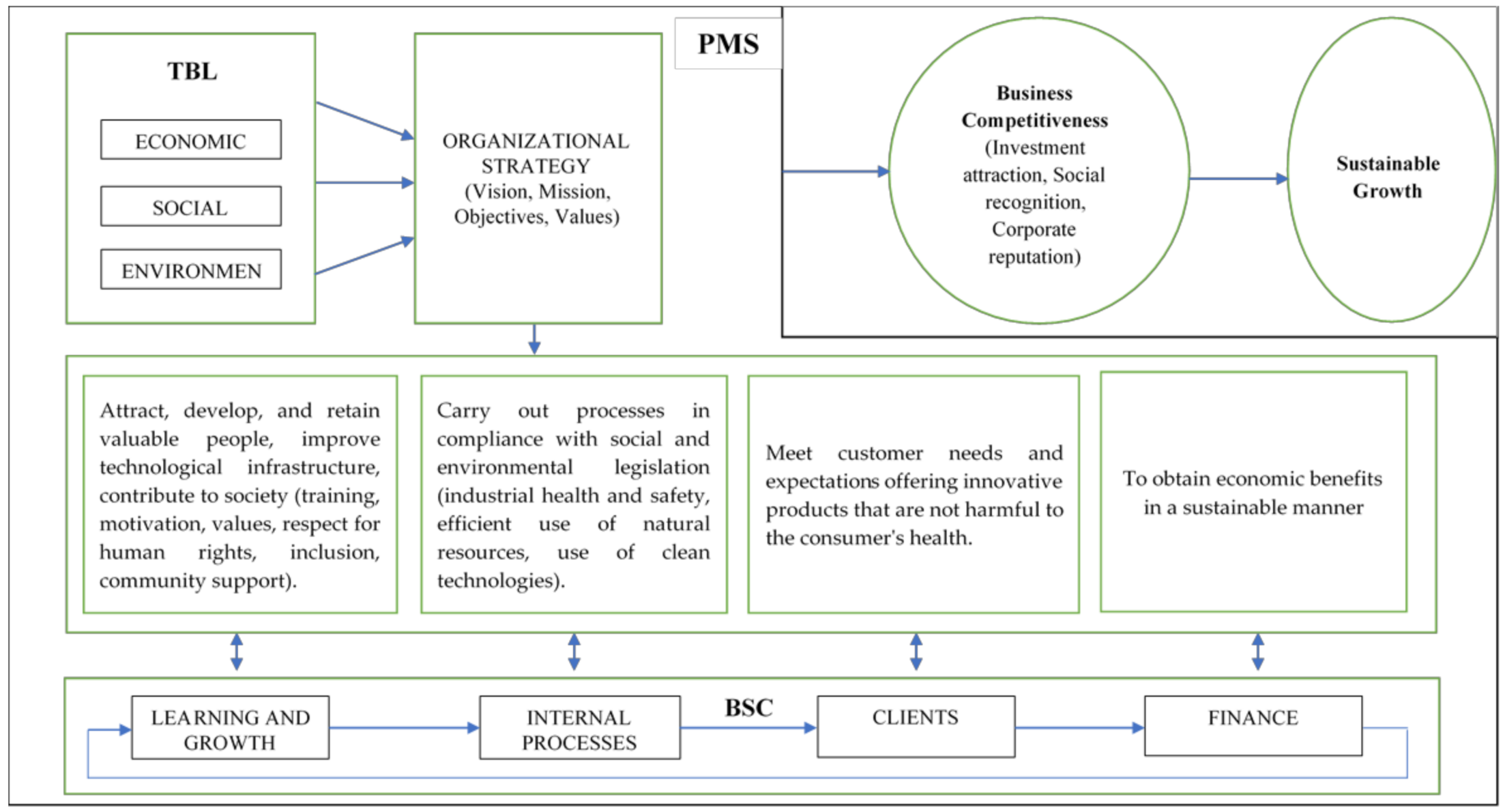

2.3. Proposed Conceptual Framework

3. Methodology

3.1. Construction and Design of the Interview Questionnaire

3.2. Data Collection

3.3. Data Analysis

4. Findings

4.1. Sustainability and Triple Bottom Line

“As a medium-sized company, it is very difficult to take this type of actions. In general, in Peru there is a lack of sincere commitment to ecology; we are not yet imbued with the meaning of TBL. It may also be that we do not know how to start. It is an issue that needs a lot of guidance from the government.”

“The economic aspect is the most important, to the extent that if we are successful in the economic results, we will have resources to carry out social and environmental actions. To be transparent, sincere and realistic in order of priority, the importance would be: first the economic factor, then the social factor and then the environmental factor.”

“It depends on the type of client. There are clients who are interested in complying with these aspects, but there are clients who are not. Complying with all aspects is aimed at formal companies of a certain size. To comply with all aspects is costly, it costs money. The vast majority of Peruvian market is guided by price and is not interested in whether or not all aspects are complied with.”

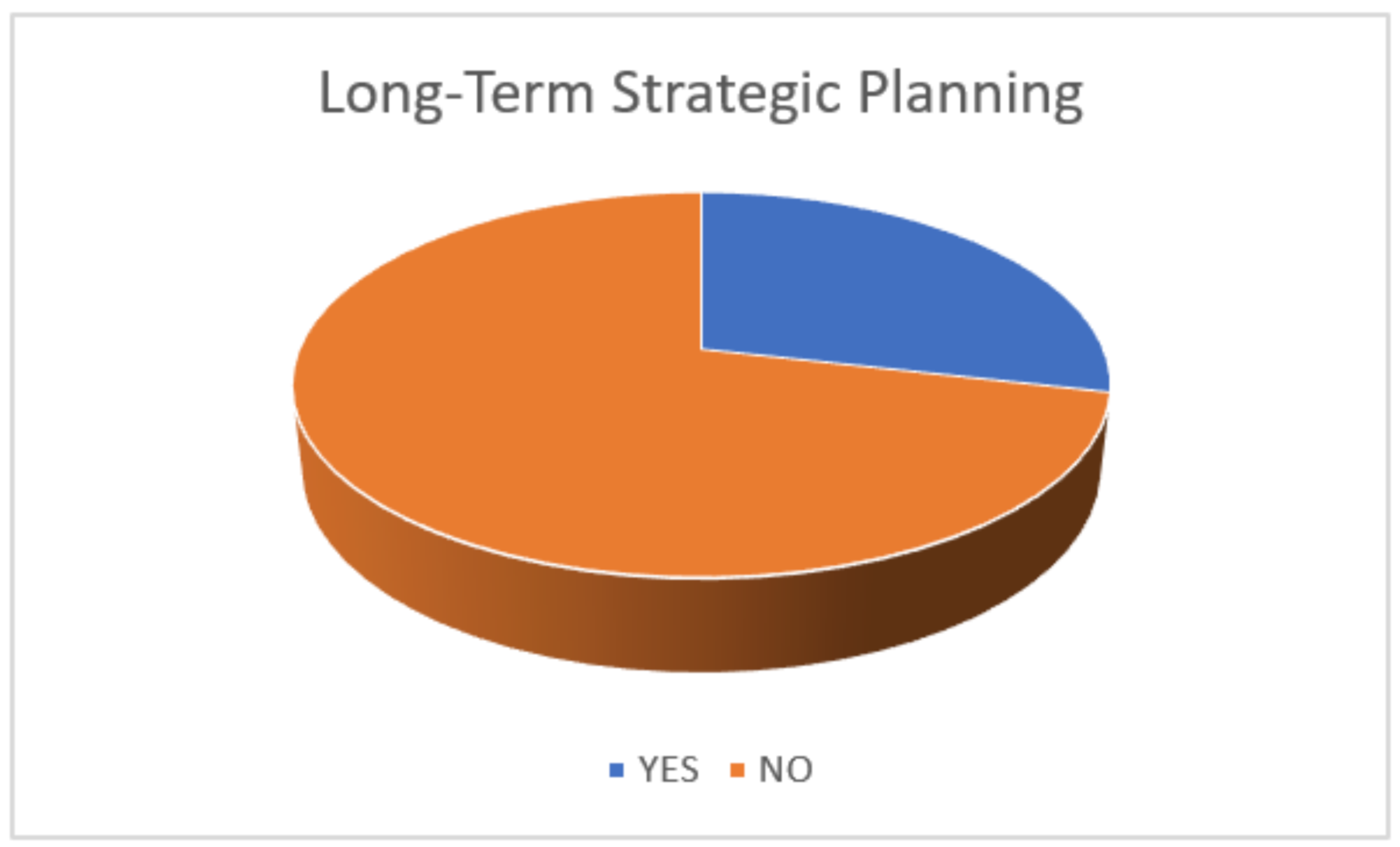

4.2. Strategy

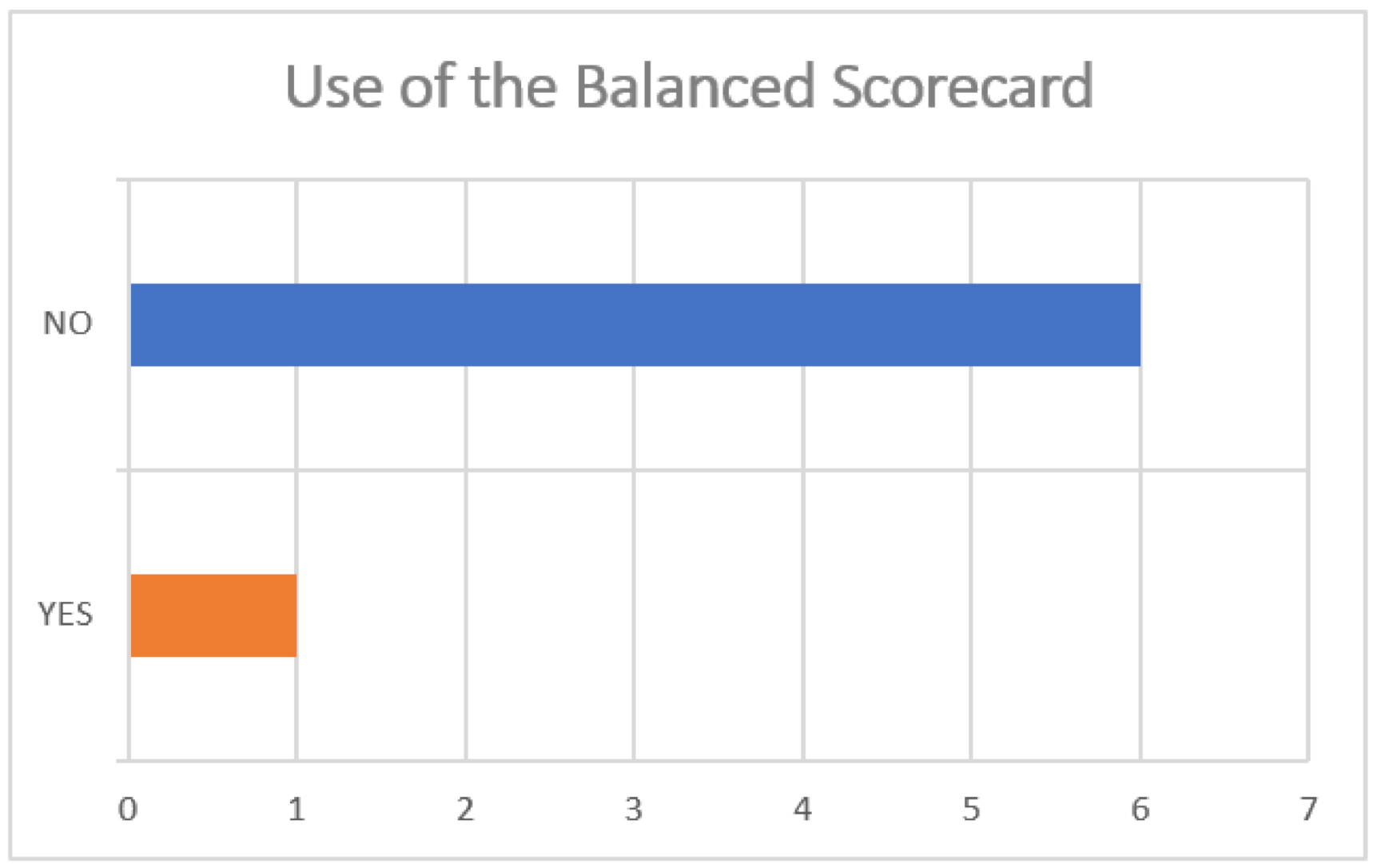

4.3. Management Control Systems

5. Discussion and Conclusions

5.1. Discussion of Findings

5.2. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

- Does sustainability mean anything to you? If so, what do you understand by sustainability? Could you comment on whether sustainability has ever been considered in your company’s activities and if it has not been taken into account, could you mention the reason?

- Does TBL mean anything to you? If so, what do you understand by TBL? What actions related to social and environmental management have been developed recently in your company?

- In the management of your company, which aspect, economic, social, or environmental, is more important to you? Why?

- If you adopt or would adopt social or environmental actions, for what reason do you or would you do so? For ethical reasons, for economic reasons, out of obligation by any regulatory body?

- Does the company periodically report the results of its social and environmental actions to any government regulatory body or other entity?

- Do you have any requirements regarding social or environmental aspects from your customers and/or suppliers (domestic or foreign)?

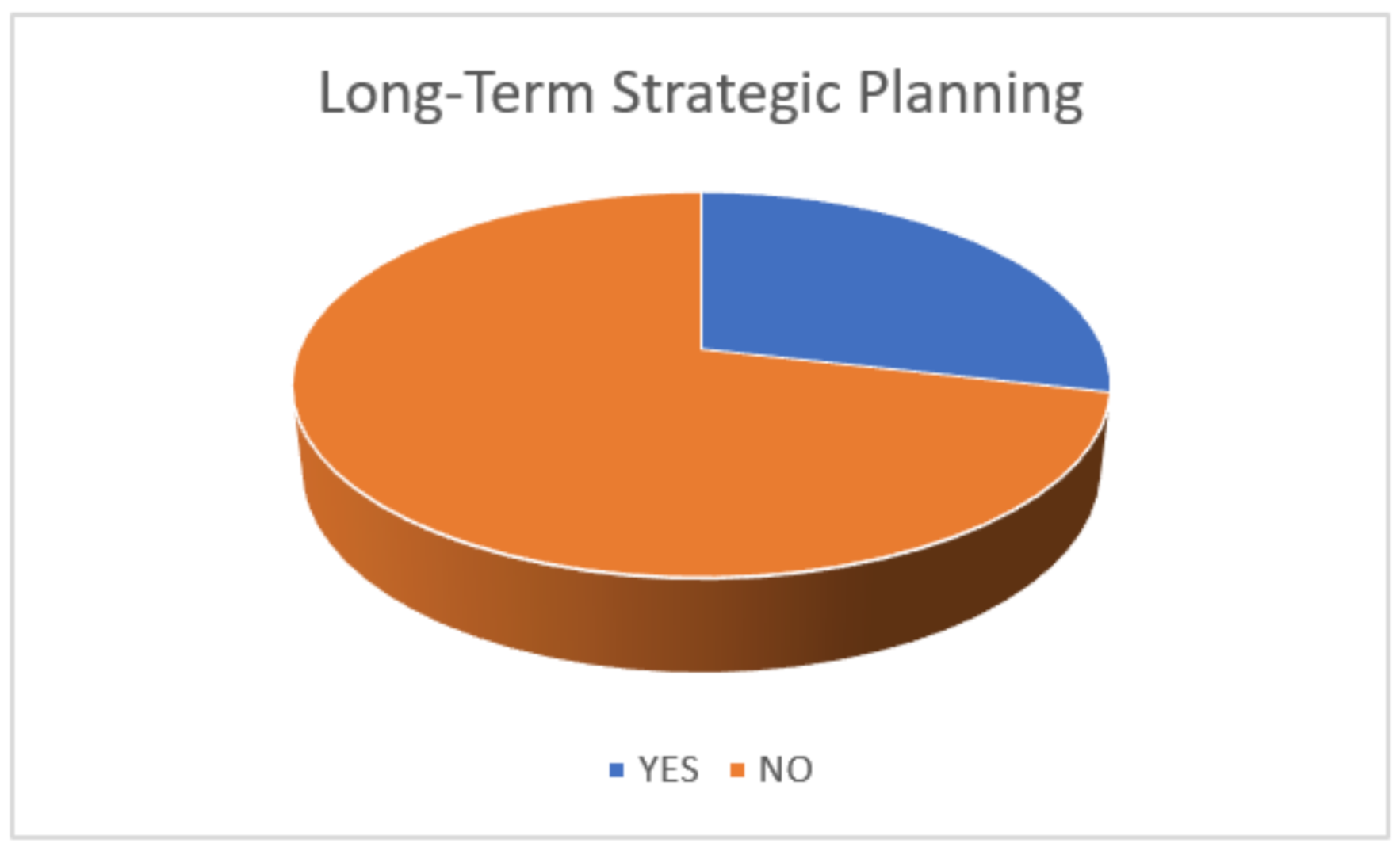

- Does the company have a strategic plan?

- Do you believe that the aspect of sustainability should be taken into account in the strategy of a manufacturing company?

- Is the sustainability aspect incorporated into your company’s strategic plan (Vision, mission, objectives, values)?

- What do you believe are the main key factors for the future success of your organization? What are the current strategic objectives of your organization?

- Do you believe that the management of social and environmental aspects influences the economic performance of a manufacturing company? Why?

- Do you think it is important to take into account TBL dimensions to achieve a competitive advantage? Why?

- How is compliance with the strategic plan measured?

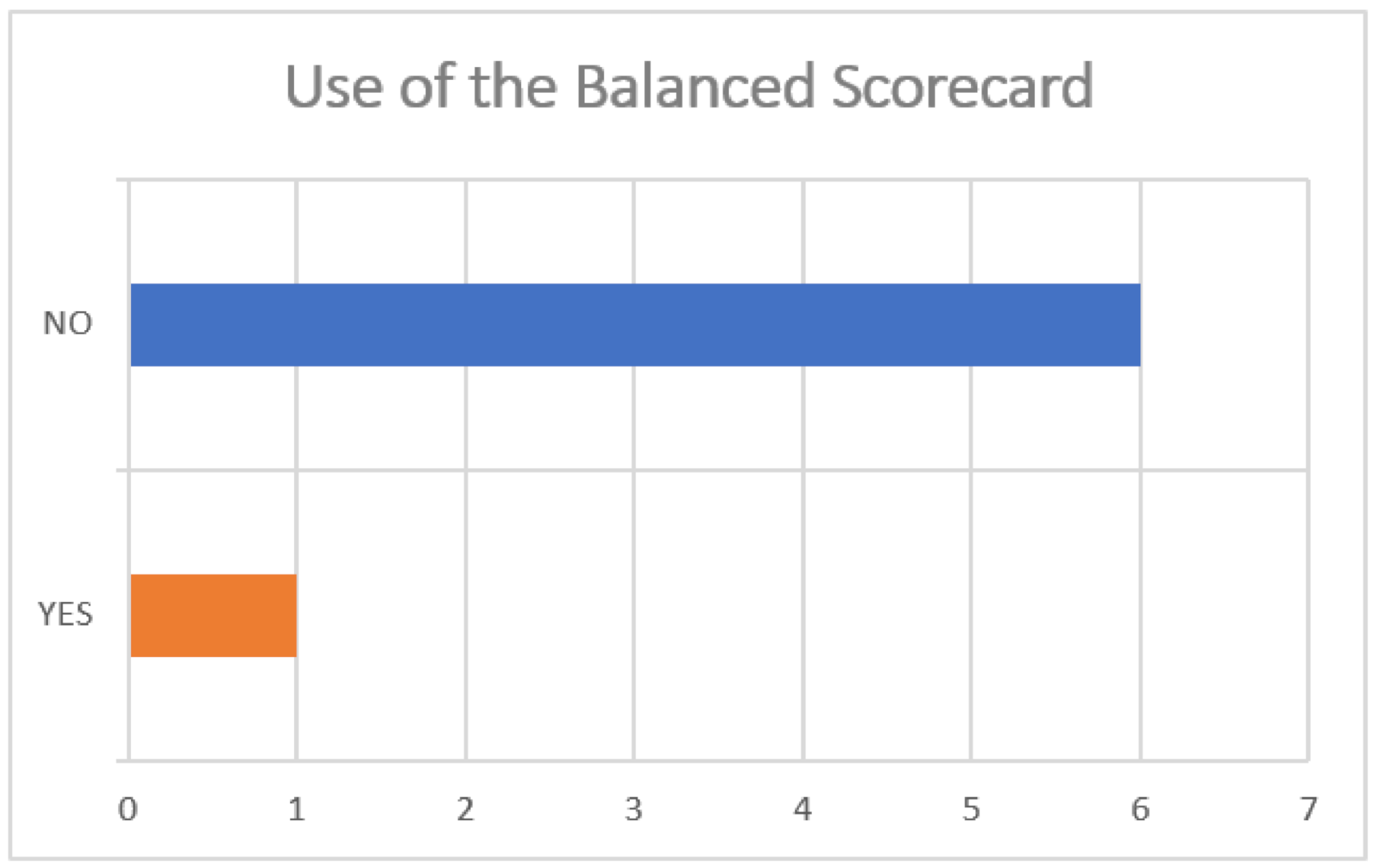

- Do you know what the balanced scorecard is and do you use it?

- If you do not use the BSC, which management control system do you use?

- Are goals established to evaluate the performance of the different areas of the company? How are these goals set (imposition, consensus, benchmarking, etc.)?

- How is employee performance evaluated, objectively/subjectively, individually/group/globally?

- What type of information technology do you use to store and process the data of the activities carried out in each of the areas of the company? How does the information flow in the company (Internet/intranet, etc.)?

- For what purposes do you use the information from the results of your control systems? Diagnostic/corrective? Interactive/proactive? Both purposes?

- Do you have any incentive system (economic and/or non-economic) to compensate the achievement of the established goals?

- Have the TBL dimensions been considered in the company’s controls? Why?

- What are the main indicators you use to measure the company’s performance?

- −

- Economic—financial:

- −

- Customers—sales:

- −

- Internal processes—production/operations:

- −

- Personnel—IT—innovation:

- What indicators would you propose to measure the social and environmental management of your company?

- −

- Social:

- −

- Environmental:

- If economic performance were shown to be positively correlated with social and environmental performance, would you incorporate environmental and social aspects into your management control and performance measurement system?

Appendix B

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Interview | Perspective | Indicator |

|---|---|---|

| 1 | Finance | |

| Clients | Sales volume, customer satisfaction | |

| Internal processes | % of shrinkage, standard times | |

| Learning and growth | ||

| 2 | Finance | |

| Clients | ||

| Internal processes | % of shrinkage, man hours, machine hours | |

| Learning and growth | ||

| 3 | Finance | Net income, acidity ratio, financial expense |

| Clients | Total sales, sales/customer, percentage change in sales by period | |

| Internal processes | Production volume, % of shrinkage, man hours, machine hours | |

| Learning and growth | Accident rate, absenteeism rate | |

| 4 | Finance | ROIC, NOPAT, EBITDA |

| Clients | Customer satisfaction, customer loyalty, product quality, positioning, brand perception | |

| Internal processes | Production volume, % of shrinkage, compliance with environmental measurements, compliance with worker health, number of hours of machine downtime, compliance with machine maintenance plan | |

| Learning and growth | Training hours, training effectiveness, organizational culture, %SAP system coverage | |

| 5 | Finance | Profitability by product, net income, cost of products |

| Clients | Market share, market penetration | |

| Internal processes | Analysis of product and raw material quality variables, % of wastage, labor productivity | |

| Learning and growth | Hours of training, % of attendance, acquisition of new technology | |

| 6 | Finance | Return on sales, liquidity, net income |

| Clients | Sales mix, customer segmentation, customer portfolio growth, sales growth, quota compliance by salesperson (by product and by value) | |

| Internal processes | % of defectives, % of waste, % of reprocesses, machine hours, man hours | |

| Learning and growth | attendance, overtime | |

| 7 | Finance | |

| Clients | ||

| Internal processes | Machine hours worked/machine hours programmed, production obtained/production standard, defective units produced/units produced | |

| Learning and growth |

Appendix C

| Interview | Perspective | Indicator |

|---|---|---|

| 1 | Social | Compliance with social regulations |

| Environmental | Compliance with environmental regulations | |

| 2 | Social | The level of well-being of personnel in the workplace |

| Environmental | ------------- | |

| 3 | Social | Personnel satisfaction |

| Environmental | ------------- | |

| 4 | Social | Externally: Satisfaction of the communities in which work has been carried out. Links with municipalities’ social assistance programs. Internally: Labor climate index. |

| Environmental | Compliance with environmental regulations. Management of material waste by the employee. | |

| 5 | Social | Labor climate |

| Environmental | ------------- | |

| 6 | Social | Compliance with regulations, organizational climate, reduction in overtime |

| Environmental | Solid waste management, reduction in electricity consumption, reduction in water consumption (although water is recycled, check for water leaks) | |

| 7 | Social | ------------- |

| Environmental | ------------- |

References

- Human Development Report. The Next Frontier. Human Development and the Anthropocene. 2020. Available online: http://hdr.undp.org (accessed on 18 January 2021).

- Batista, A.A.D.S.; De Francisco, A.C. Organizational Sustainability Practices: A Study of the Firms Listed by the Corporate Sustainability Index. Sustainability 2018, 10, 226. [Google Scholar] [CrossRef] [Green Version]

- Chung, C.-C.; Chao, L.-C.; Chen, C.-H.; Lou, S.-J. A Balanced Scorecard of Sustainable Management in the Taiwanese Bicycle Industry: Development of Performance Indicators and Importance Analysis. Sustainability 2016, 8, 518. [Google Scholar] [CrossRef] [Green Version]

- Schulz, S.A.; Flanigan, R.L. Developing competitive advantage using the triple bottom line: A conceptual framework. J. Bus. Ind. Mark. 2016, 31, 449–458. [Google Scholar] [CrossRef]

- Amui, L.B.L.; Jabbour, C.J.C.; Jabbour, A.B.L.D.S.; Kannan, D. Sustainability as a dynamic organizational capability: A systematic review and a future agenda toward a sustainable transition. J. Clean. Prod. 2017, 142, 308–322. [Google Scholar] [CrossRef]

- Bocken, N.; Short, S.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef] [Green Version]

- Pádua, S.I.D.; Jabbour, C.J.C. Promotion and evolution of sustainability performance measurement systems from a perspective of business process management. Bus. Process. Manag. J. 2015, 21, 403–418. [Google Scholar] [CrossRef]

- Venkatraman, S.; Nayak, R.R. A performance framework for corporate sustainability. Int. J. Bus. Innov. Res. 2010, 4, 475. [Google Scholar] [CrossRef]

- Kalender, Z.T.; Vayvay, Ö. The Fifth Pillar of the Balanced Scorecard: Sustainability. Proc. Soc. Behav. Sci. 2016, 235, 76–83. [Google Scholar] [CrossRef]

- Moldavska, A.; Welo, T. A Holistic approach to corporate sustainability assessment: Incorporating sustainable development goals into sustainable manufacturing performance evaluation. J. Manuf. Syst. 2019, 50, 53–68. [Google Scholar] [CrossRef]

- Guevara, D. (Diciembre del 2018) 2019 un Año de Retos Para la Industria Plástica en América Latina. Tecnología del Plástico. Available online: http://www.plastico.com/temas/2019,-un-ano-de-retos-para-la-industria-plastica-en-America-Latina+128679?pagina=3 (accessed on 4 April 2020).

- Gil, F. (11 de febrero del 2019). Sólo el 5% de las Empresas Peruanas Aplican Gestiones de Responsabilidad Social. Gestión. Available online: https://gestion.pe/economia/management-empleo/5-empresas-peruanas-aplican-gestiones-responsabilidad-social-258214-noticia/ (accessed on 24 March 2020).

- Diario Gestión. SNI: Industria Suma Seis Años Siendo la Actividad Económica que Aporta Más Impuestos. Available online: https://gestion.pe/economia/sni-industria-suma-seis-anos-siendo-actividad-economica-aporta-impuestos-nndc-256684-noticia/ (accessed on 25 February 2021).

- Informe Anual del empleo en Perú 2019. Ministerio de Trabajo y Promoción del Empleo. Available online: https://cdn.www.gob.pe/uploads/document/file/1517310/Informe%20Anual%20del%20empleo%202019.pdf (accessed on 26 February 2021).

- Revista Gan@Más.25 April 2019. SNI: Industria del Plástico Genera Alrededor de 200 mil Puestos de Trabajo. Available online: https://revistaganamas.com.pe/sni-industria-del-plastico-genera-alrededor-de-200-mil-puestos-de-trabajo/ (accessed on 25 February 2021).

- Sociedad Nacional de Industrias. Instituto de Estudios Económicos y Sociales. Reporte Sectorial de Plásticos N° 04-2019. Available online: https://www.sni.org.pe/wp-content/uploads/2019/07/Reporte-Sectorial-Plásticos_2019.pdf (accessed on 4 April 2020).

- Elkington, J. Cannibals with Forks: The Triple Bottom Line of 21st Century Business; Capstone: Oxford, UK, 1997. [Google Scholar]

- Elkington, J. Enter the triple bottom line. Triple Bottom Line Add Up 2013, 1–16. [Google Scholar] [CrossRef]

- World Commission on Environment and Development, United Nations. Our Common Future; UN Documents; United Nations: New York, NY, USA, 1987. [Google Scholar]

- Nouri, F.A.; Nikabadi, M.S.; Olfat, L. Developing the framework of sustainable service supply chain balanced scorecard (SSSC BSC). Int. J. Prod. Perform. Manag. 2019, 68, 148–170. [Google Scholar] [CrossRef]

- Bento, R.F.; Mertins, L.; White, L.F. Ideology and the Balanced Scorecard: An Empirical Exploration of the Tension Between Shareholder Value Maximization and Corporate Social Responsibility. J. Bus. Ethic 2017, 142, 769–789. [Google Scholar] [CrossRef]

- Hansen, E.G.; Schaltegger, S. Sustainability Balanced Scorecards and their Architectures: Irrelevant or Misunderstood? J. Bus. Ethic 2018, 150, 937–952. [Google Scholar] [CrossRef] [Green Version]

- Flavio, H., Jr.; Gabriel, M.L.D.S.; Gallardo-Vázquez, D.A. Triple bottom line and sustainable performance measurement in industrial companies. Rev. Gest. 2018, 25, 413–429. [Google Scholar] [CrossRef] [Green Version]

- Kerr, J.; Rouse, P.; De Villiers, C. Sustainability reporting integrated into management control systems. Pac. Account. Rev. 2015, 27, 189–207. [Google Scholar] [CrossRef]

- Junior, A.N.; De Oliveira, M.C.; Helleno, A.L. Sustainability evaluation model for manufacturing systems based on the correlation between triple bottom line dimensions and balanced scorecard perspectives. J. Clean. Prod. 2018, 190, 84–93. [Google Scholar] [CrossRef]

- Singh, S.; Olugu, E.U.; Musa, S.N.; Mahat, A.B. Fuzzy-based sustainability evaluation method for manufacturing SMEs using balanced scorecard framework. J. Intell. Manuf. 2018, 29, 1–18. [Google Scholar] [CrossRef]

- Tabatabaei, S.A.N.; Omran, E.S.; Hashemi, S.; Sedaghat, M. Presenting Sustainable HRM Model Based on Balanced Scorecard in Knowledge-based ICT Companies (The Case of Iran). Econ. Sociol. 2017, 10, 107–124. [Google Scholar] [CrossRef]

- Wang, S.H.; Chang, S.-P.; Williams, P.; Koo, B.; Qu, Y.-R. Using Balanced Scorecard for Sustainable Design-centered Manufacturing. Proc. Manuf. 2015, 1, 181–192. [Google Scholar] [CrossRef] [Green Version]

- Yadav, N.; Sagar, M. Performance measurement and management frameworks. Bus. Process. Manag. J. 2013, 19, 947–971. [Google Scholar] [CrossRef]

- Rosen, M.A.; Kishawy, H.A. Sustainable Manufacturing and Design: Concepts, Practices and Needs. Sustainability 2012, 4, 154–174. [Google Scholar] [CrossRef] [Green Version]

- Ahmad, S.; Wong, K.Y. Sustainability assessment in the manufacturing industry: A review of recent studies. Benchmark. Int. J. 2018, 25, 3162–3179. [Google Scholar] [CrossRef]

- Linke, B.S.; Corman, G.J.; Dornfeld, D.A.; Tönissen, S. Sustainability indicators for discrete manufacturing processes applied to grinding technology. J. Manuf. Syst. 2013, 32, 556–563. [Google Scholar] [CrossRef] [Green Version]

- Allen, D.; Bauer, D.; Bras, B.; Gutowski, T.; Murphy, C.; Piwonka, T.; Sheng, P.; Sutherland, J.; Thurston, D.; Wolff, E. Environmentally Benign Manufacturing: Trends in Europe, Japan, and the USA. J. Manuf. Sci. Eng. 2002, 124, 908–920. [Google Scholar] [CrossRef]

- Haapala, K.R.; Zhao, F.; Camelio, J.; Sutherland, J.W.; Skerlos, S.J.; Dornfeld, D.A.; Jawahir, I.S.; Clarens, A.F.; Rickli, J.L. A Review of Engineering Research in Sustainable Manufacturing. J. Manuf. Sci. Eng. 2013, 135. [Google Scholar] [CrossRef] [Green Version]

- Moldavska, A.; Welo, T. On the Applicability of Sustainability Assessment Tools in Manufacturing. Proc. CIRP 2015, 29, 621–626. [Google Scholar] [CrossRef]

- Corporate Sustainability Barometer 2010. Wie nachhaltig agieren Unternehmen in Deutschland? Schaltegger, S., Windolph, S.E., Harms, D., Eds.; Lüneburg/Frankfurt a.M.: Frankfurt, Germany, 2010. [Google Scholar]

- Fischer, T.M.; Huber, R.; Sawczyn, A. Nachhaltige Unternehmensführung als Herausforderung für das Controlling. Controlling 2010, 22, 222–230. [Google Scholar] [CrossRef]

- Fischer, T.M.; Sawczyn, A.; Brauch, B. 13. Nachhaltigkeit und Sustainability Accounting. In Controlling zwischen Shareholder Value und Stakeholder Value; De Gruyter: Berline, Germany, 2014; pp. 261–287. [Google Scholar]

- Habisch, A.; Jonker, J.; Wegner, M.; Schmidpeter, R. Corporate Social Responsibility Across Europe; Springer: Berlin, Germany, 2005. [Google Scholar]

- Quick, R.; Knocinski, M. Nachhaltigkeitsberichterstattung—Empirische Befunde zur Berichterstattungspraxis von HDAX-Unternehmen. J. Bus. Econ. 2006, 76, 615–650. [Google Scholar] [CrossRef]

- Preller, E. Controlling und Sustainability. Controlling 2007, 19, 51–54. [Google Scholar] [CrossRef]

- Weber, J.; Schäffer, U. Introduction to Controlling; Schäffer-Poeschel: Stuttgart, Germany, 2008. [Google Scholar]

- López, M.V.; Garcia, A.; Rodriguez, L. Sustainable Development and Corporate Performance: A Study Based on the Dow Jones Sustainability Index. J. Bus. Ethic 2007, 75, 285–300. [Google Scholar] [CrossRef]

- Rausch, A.; Osmanagić Bedenik, N.; Fafaliou, I.; Labas, D.; Porada-Rochon, M. Controlling and Sustainability: Empirical Evidence from Europe. Zagreb Int. Rev. Econ. Bus. 2013, 16, 37–63. [Google Scholar]

- Ferreira, A.; Otley, D. The design and use of performance management systems: An extended framework for analysis. Manag. Account. Res. 2009, 20, 263–282. [Google Scholar] [CrossRef]

- Bouwens, J.; Abernethy, M.A. The consequences of customization on management accounting system design. Account. Organ. Soc. 2000, 25, 221–241. [Google Scholar] [CrossRef]

- Chenhall, R. Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Account. Org. Soc. 2003, 28, 127–168. [Google Scholar] [CrossRef]

- Naranjo-Gil, D. The Role of Management Control Systems and Top Teams in Implementing Environmental Sustainability Policies. Sustainability 2016, 8, 359. [Google Scholar] [CrossRef] [Green Version]

- Kaplan, R.; Norton, D. El Cuadro de Mando Integral: The Balanced Scorecard, 2nd ed.; Gestión 2000: Barcelona, Spain, 2000. [Google Scholar]

- Simons, R. Levers of Control: How Managers Use Innovative Control Systems to Drive Strategic Renewal; Harvard Business School Press: Boston, MA, USA, 1995. [Google Scholar]

- Yin, R.K. Case Study Research and Applications: Design and Methods; Sage Publications: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Eisenhardt, K.M. Building Theories from Case Study Research. Acad. Manag. Rev. 1989, 14, 532. [Google Scholar] [CrossRef]

- Sulich, A.; Grudziński, A. The Analysis of Strategy Types of the Renewable Energy Sector. Acta Univ. Agric. Silvic. Mendel. Brun. 2019, 67, 1643–1651. [Google Scholar] [CrossRef] [Green Version]

- Rozario, S.D.; Venkatraman, S.; Chu, M.-T.; Abbas, A. Enabling Corporate Sustainability from a Talent Acquisition Perspective. J. Sustain. Res. 2020, 2. [Google Scholar] [CrossRef]

| Enterprise | Interview | Period of Time | Interviewee Charge | Interviewee’s Guild Position | Enterprise Size | Main Product Line | Main Production Proccess |

|---|---|---|---|---|---|---|---|

| A | 1 | 57′28′′ | General Manager | Vice President of the Plastics Committee of the National Society of Industries of Peru | Medium | Thermoformed pacakges | Thermoforming molding |

| 2 | 57′10′′ | Chief of Production | |||||

| 3 | 41′18′′ | Head of Administration and Finance | |||||

| B | 4 | 45′49′′ | General Manager | President of the Plastics Committee of the National Society of Industries of Peru | Large | Pipes and water tubes for water and sewage installation | Extrusion molding |

| C | 5 | 56′23′′ | General Manager | Medium | Bags and films | Extrusion and blow molding | |

| D | 6 | 1 h 01′39′′ | General Manager | Medium | Articles for cleaning | Injection molding | |

| 7 | 1 h 03′02′′ | Chief of Production |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Córdova-Aguirre, L.J.; Ramón-Jerónimo, J.M. Exploring the Inclusion of Sustainability into Strategy and Management Control Systems in Peruvian Manufacturing Enterprises. Sustainability 2021, 13, 5127. https://doi.org/10.3390/su13095127

Córdova-Aguirre LJ, Ramón-Jerónimo JM. Exploring the Inclusion of Sustainability into Strategy and Management Control Systems in Peruvian Manufacturing Enterprises. Sustainability. 2021; 13(9):5127. https://doi.org/10.3390/su13095127

Chicago/Turabian StyleCórdova-Aguirre, Luis Jesús, and Juan Manuel Ramón-Jerónimo. 2021. "Exploring the Inclusion of Sustainability into Strategy and Management Control Systems in Peruvian Manufacturing Enterprises" Sustainability 13, no. 9: 5127. https://doi.org/10.3390/su13095127

APA StyleCórdova-Aguirre, L. J., & Ramón-Jerónimo, J. M. (2021). Exploring the Inclusion of Sustainability into Strategy and Management Control Systems in Peruvian Manufacturing Enterprises. Sustainability, 13(9), 5127. https://doi.org/10.3390/su13095127