Determinants of the Digitalization of Accounting in an Emerging Market: The Roles of Organizational Support and Job Relevance

Abstract

:1. Introduction

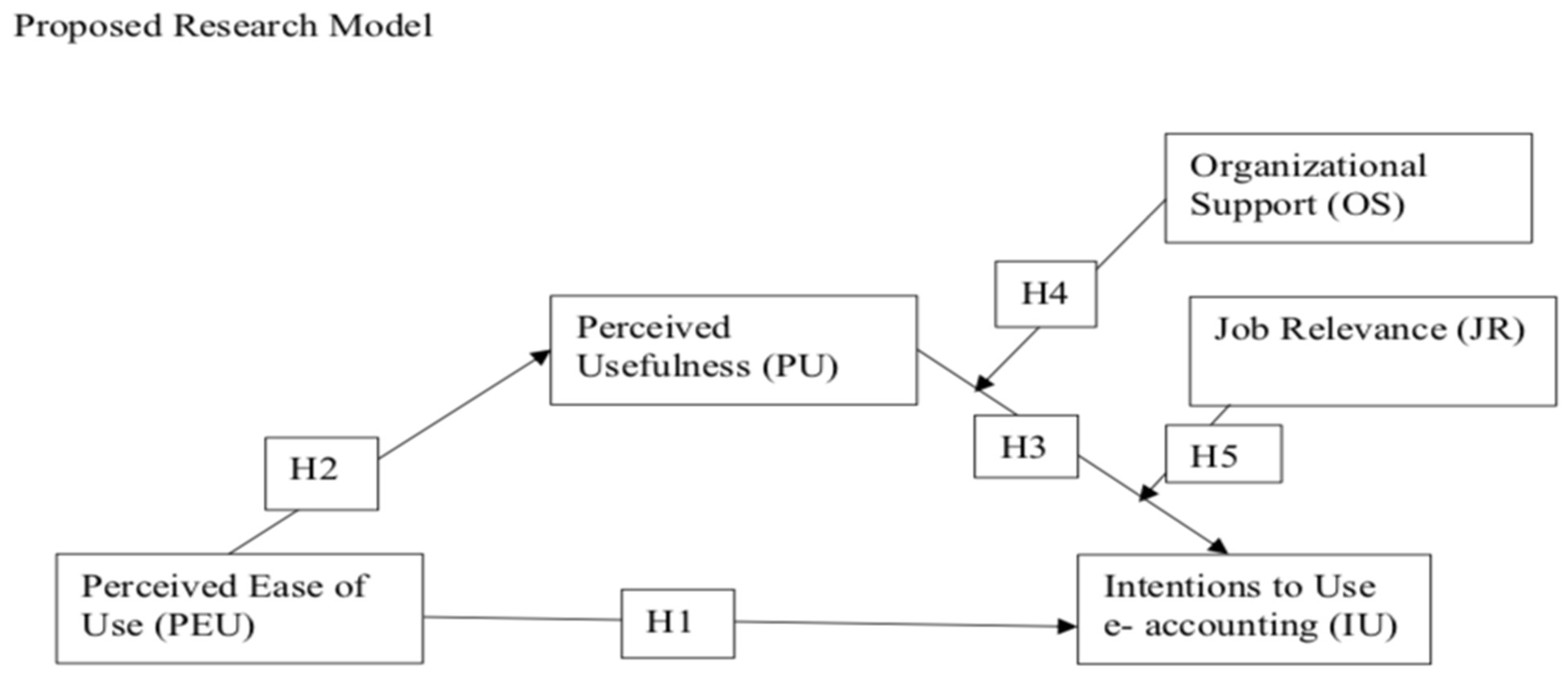

2. Research Model and Hypotheses

2.1. Technology Acceptance Model

2.2. Perceived Usefulness as Mediator

2.3. Organization Support as a Moderator

2.4. Job Relevance as a Moderator

3. Methodology

3.1. Study Context

3.2. Data Collection

3.3. Instrumentation

4. Data Analysis and Results

4.1. Scale Validation

4.2. Reliability and Validity

4.3. Hypotheses Testing

4.4. Mediation Analysis

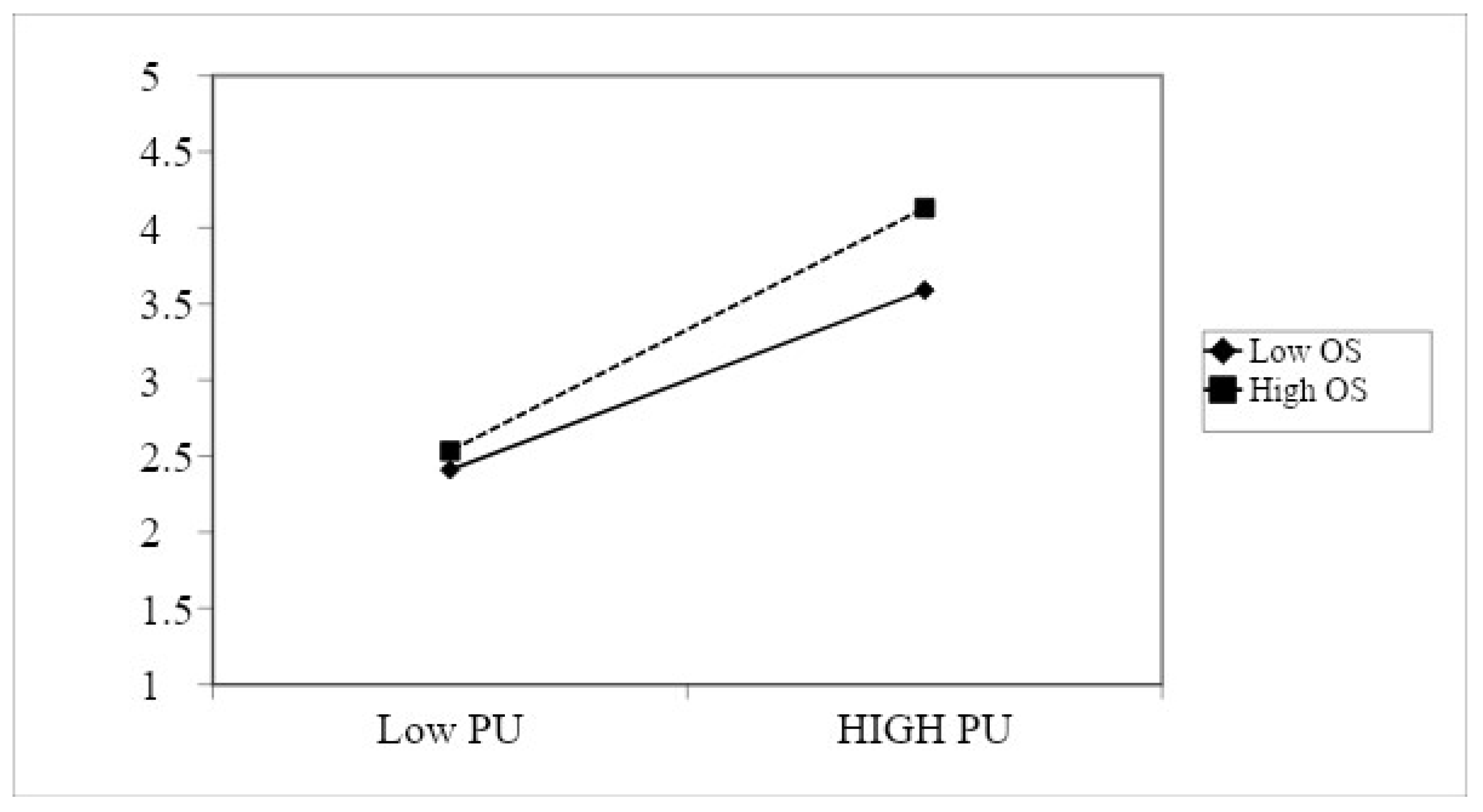

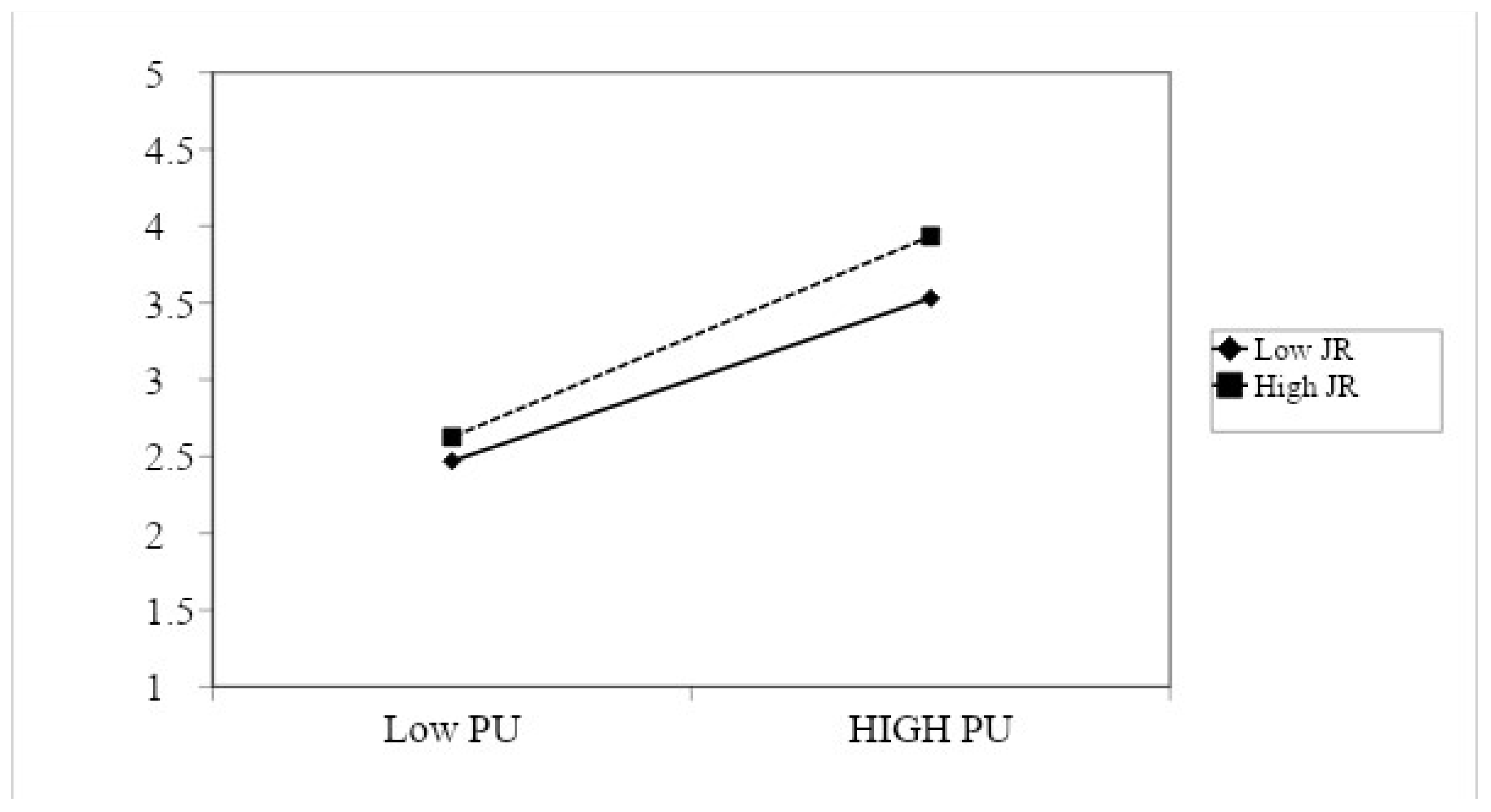

4.5. Moderation Analysis

4.6. Moderated Mediation Analysis

5. Discussion

6. Managerial and Practical Implications

7. Limitations and Future Research

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Mondejar, M.E.; Avtar, R.; Diaz, H.L.B.; Dubey, R.K.; Esteban, J.; Gómez-Morales, A.; Hallam, B.; Mbungu, N.T.; Okolo, C.C.; Prasad, K.A.; et al. Digitalization to achieve sustainable development goals: Steps towards a Smart Green Planet. Sci. Total Environ. 2021, 794, 148539. [Google Scholar] [CrossRef] [PubMed]

- Gouvea, R.; Kapelianis, D.; Kassicieh, S. Assessing the nexus of sustainability and information & communications technology. Technol. Forecast. Soc. Chang. 2018, 130, 39–44. [Google Scholar] [CrossRef] [Green Version]

- Del Río Castro, G.; Fernández, M.C.G.; Colsa, U. Unleashing the convergence amid digitalization and sustainability towards pursuing the Sustainable Development Goals (SDGs): A holistic review. J. Clean. Prod. 2021, 280, 122204. [Google Scholar] [CrossRef]

- Jovanović, M.; Dlačić, J.; Okanović, M. Digitalization and society’s sustainable development—Measures and implications. Zb. Rad. Ekon. Fak. U Rijeci Časopis Za Ekon. Teor. I Praksu 2018, 36, 905–928. [Google Scholar]

- Felsberger, A.; Qaiser, F.H.; Choudhary, A.; Reiner, G. The impact of Industry 4.0 on the reconciliation of dynamic capabil-ities: Evidence from the European manufacturing industries. Prod. Plan. Control 2020, 33, 277–300. [Google Scholar] [CrossRef]

- Miceli, A.; Hagen, B.; Riccardi, M.P.; Sotti, F.; Settembre-Blundo, D. Thriving, Not Just Surviving in Changing Times: How Sustainability, Agility and Digitalization Intertwine with Organizational Resilience. Sustainability 2021, 13, 2052. [Google Scholar] [CrossRef]

- Kamal, S. Historical evolution of management accounting. Cost Manag. 2015, 43, 12–19. [Google Scholar]

- Jasim, Y.A.; Raewf, M.B. Information Technology’s Impact on the Accounting System. Cihan Univ. -Erbil J. Humanit. Soc. Sci. 2020, 4, 50–57. [Google Scholar] [CrossRef]

- Topor, D.I.; Akram, U.; Fülop, M.T.; Căpușneanu, S.; Ionescu, C.A. E-Accounting: Future Challenges and Perspectives. In CSR and Management Accounting Challenges in a Time of Global Crises; IGI Global: Hershey, PA, USA, 2021; pp. 35–52. [Google Scholar]

- Amidu, M.; Effah, J.; Abor, J. E-accounting practices among small and medium enterprises in Ghana. J. Manag. Policy Pract. 2011, 12, 146–155. [Google Scholar]

- Esmeray, A.; Esmeray, M. Digitalization in Accounting through Changing Technology and Accounting Engineering as an Adaptation Proposal; IGI Global: Hershey, PA, USA, 2020; pp. 354–376. [Google Scholar] [CrossRef]

- Cong, Y.; Omar, A.; Sun, H.-L. Does IT Outsourcing Affect the Accuracy and Speed of Financial Disclosures? Evidence from Preparer-Side XBRL Filing Decisions. J. Inf. Syst. 2018, 33, 45–61. [Google Scholar] [CrossRef]

- Uzrail, A.H.; Bardai, B. Moderating Effect of the Adoption of Computerized Accounting Information Systems and the Perceived Effect on Financial Performance–A Study of Palestinian Companies Case. Int. J. All Res. Writ. 2019, 2, 63–74. [Google Scholar]

- Suyono, E.; Rusmana, O.; Riswan, R. The Revitalization Model Through the Implementation of Accounting Information System for Village Unit Cooperative in Banyumas Region, Indonesia. Media Ekon. Dan Manaj. 2019, 34. [Google Scholar] [CrossRef]

- Bataineh, A. The effect of using computerized accounting information systems on reducing production costs in Jordanian pharmaceutical companies. Int. J. Bus. Manag. Invent. 2018, 7, 1–10. [Google Scholar]

- Teru, S.P.; Idoko, I.F.; Bello, L. The Impact of E—Accounting in Modern Businesses. Int. J. Account. Financ. Rev. 2019, 4, 1–4. [Google Scholar] [CrossRef]

- Fiducci, T.E. Data Backup, Storage, Transfer and Retrieval System, Method and Computer Program Product. U.S. Patent 10,387,270, 19 August 2019. [Google Scholar]

- Ye, Z.; Hu, J. Internal Control of Enterprise Computer Accounting Information System in the Age of Big Data. In The International Conference on Cyber Security Intelligence and Analytics; Springer International Publishing: Cham, Switzerland, 2020; pp. 315–321. [Google Scholar] [CrossRef]

- Zhang, Y. Security Risk of Network Accounting Information System and Its Precaution. In Proceedings of the 3rd International Conference on Mechatronics Engineering and Information Technology (ICMEIT 2019), Dalian, China, 29–30 March 2019. [Google Scholar]

- Park, T.; Ellis, Y. The Effect of Randomized versus Nonrandomized Data on Accounting Students’ Academic Performance. J. Instr. Pedagog. 2020, 23, 1–11. [Google Scholar]

- Alshurafat, H.; Beattie, C.; Jones, G.; Sands, J. Forensic accounting core and interdisciplinary curricula components in Aus-tralian universities: Analysis of websites. J. Forensic Acct. Investig. Account. 2019, 11, 353–365. [Google Scholar]

- Nguyen, D.; Gopalaswamy, A.K. The interface between electronic banking and accounting modules. J. Adv. Manag. Res. 2018, 15, 241–264. [Google Scholar] [CrossRef]

- Thottoli, M.M.; Ahmed, E.R. Information technology and E-accounting: Some determinants among SMEs. J. Money Bus. 2021. [Google Scholar] [CrossRef]

- Thottoli, M.M.; Thomas, K.V.; Ahmed, E.R. Adoption of audit software by audit firms: A qualitative study. J. Inf. Comput. Sci. 2019, 9, 768–776. [Google Scholar]

- Allahyari, A.; Ramazani, M. Studying impact of organizational factors in information technology acceptance in accounting occupation by use of TAM Model (Iranian Case Study). ARPN J. Syst. Softw. 2012, 2, 12–17. [Google Scholar]

- Eltweri, A.; Cavaliere, M.L.P.L. Impact of E-Accounting Practices upon the Performance of Business. Proc. E-Book 2020, 240, 240–252. [Google Scholar]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 319–340. [Google Scholar] [CrossRef] [Green Version]

- Cropanzano, R.; Mitchell, M.S. Social exchange theory: An interdisciplinary review. J. Manag. 2005, 31, 874–900. [Google Scholar] [CrossRef] [Green Version]

- Hsiao, C.H.; Yang, C. The intellectual development of the technology acceptance model: A co-citation analysis. Int. J. Inf. Manag. 2011, 31, 128–136. [Google Scholar] [CrossRef]

- Venkatesh, V. Determinants of Perceived Ease of Use: Integrating Control, Intrinsic Motivation, and Emotion into the Technology Acceptance Model. Inf. Syst. Res. 2000, 11, 342–365. [Google Scholar] [CrossRef] [Green Version]

- Ajzen, I. The theory of planned behavior. Organ. Behav. Hum. Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Ajzen, I.; Fishbein, M. A Bayesian analysis of attribution processes. Psychol. Bull. 1975, 82, 261–277. [Google Scholar] [CrossRef]

- King, W.R.; He, J. A meta-analysis of the technology acceptance model. Inf. Manag. 2006, 43, 740–755. [Google Scholar] [CrossRef]

- Brown, S.A.; Massey, A.P.; Montoya-Weiss, M.M.; Burkman, J.R. Do I really have to? User acceptance of mandated tech-nology. Eur. J. Inf. Syst. 2002, 11, 283–295. [Google Scholar] [CrossRef]

- Huang, Y.-C.; Backman, S.J.; Backman, K.F.; Moore, D. Exploring user acceptance of 3D virtual worlds in travel and tourism marketing. Tour. Manag. 2013, 36, 490–501. [Google Scholar] [CrossRef]

- Sagnier, C.; Loup-Escande, E.; Lourdeaux, D.; Thouvenin, I.; Valléry, G. User Acceptance of Virtual Reality: An Extended Technology Acceptance Model. Int. J. Hum. -Comput. Interact. 2020, 36, 993–1007. [Google Scholar] [CrossRef]

- Elias, S.M.; Smith, W.L.; Barney, C.E. Age as a moderator of attitude towards technology in the workplace: Work motivation and overall job satisfaction. Behav. Inf. Technol. 2012, 31, 453–467. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G. Why Don’t Men Ever Stop to Ask for Directions? Gender, Social Influence, and Their Role in Technology Acceptance and Usage Behavior. MIS Q. 2000, 24, 115. [Google Scholar] [CrossRef]

- Souza, L.A.; Da Silva, M.J.P.B.M.; Ferreira, T.A.M.V. The acceptance of information technology by the accounting area. Sist. Gest. 2017, 12, 516–524. [Google Scholar]

- Abduljalil, K.M.; Zainuddin, Y. Integrating technology acceptance model and motivational model towards intention to adopt accounting information system. Int. J. Manag. Account. Econ. 2015, 2, 346–359. [Google Scholar]

- Le, O.; Cao, Q. Examining the technology acceptance model using cloud-based accounting software of Vietnamese enter-prises. Manag. Sci. Lett. 2020, 10, 2781–2788. [Google Scholar] [CrossRef]

- Grover, V. An Empirically Derived Model for the Adoption of Customer-based Interorganizational Systems. Decis. Sci. 1993, 24, 603–640. [Google Scholar] [CrossRef]

- Konradt, U.; Christophersen, T.; Schaeffer-Kuelz, U. Predicting user satisfaction, strain and system usage of employee self-services. Int. J. Hum. -Comput. Stud. 2006, 64, 1141–1153. [Google Scholar] [CrossRef]

- Sharma, R.; Yetton, P. The Contingent Effects of Management Support and Task Interdependence on Successful Information Systems Implementation. MIS Q. 2003, 27, 533. [Google Scholar] [CrossRef]

- Injai, K. The Effects of Individual, Managerial, Organisational, and Environmental Factors on the Adoption of Object Orientation in US Organisations: An Empirical Test of the Technology Acceptance Model. Ph.D. Thesis, University of Nebraska, Lincoln, NE, USA, 1996. [Google Scholar]

- Igbaria, M.; Guimaraes, T.; Davis, G.B. Testing the Determinants of Microcomputer Usage via a Structural Equation Model. J. Manag. Inf. Syst. 1995, 11, 87–114. [Google Scholar] [CrossRef]

- Emerson, R. Social Exchange Theory. Annu. Rev. Sociol. 1976, 2, 335–362. [Google Scholar] [CrossRef]

- Organ, D.W.; Lingl, A. Personality, satisfaction, and organizational citizenship behavior. J. Soc. Psychol. 1995, 135, 339–350. [Google Scholar] [CrossRef]

- Haas, D.F.; Deseran, F.A. Trust and Symbolic Exchange. Soc. Psychol. Q. 1981, 44. [Google Scholar] [CrossRef]

- Gould-Williams, J.; Davies, F. Using social exchange theory to predict the effects of HRM practice on employee outcomes: An analysis of public sector workers. Public Manag. Rev. 2005, 7, 1–24. [Google Scholar] [CrossRef]

- Kim, D.R.; Kim, B.G.; Aiken, M.W.; Park, S.C. The Influence of individual, task, organisational support, and subject norm factors on the adoption of groupware Acad. Inf. Manag. Sci. J. 2006, 9, 93–110. [Google Scholar]

- McFarland, D.J.; Hamilton, D. Adding contextual specificity to the technology acceptance model. Comput. Hum. Behav. 2006, 22, 427–447. [Google Scholar] [CrossRef]

- Lee, Y.H.; Hsieh, Y.C.; Chen, Y.H. An investigation of employees’ use of e-learning systems: Applying the technology ac-ceptance model. Behav. Inf. Technol. 2013, 32, 173–189. [Google Scholar] [CrossRef]

- Chismar, W.G.; Wiley-Patton, S. Test of the technology acceptance model for the internet in pediatrics. Proc. AMIA Symp. 2002, 155–159. Available online: https://pubmed.ncbi.nlm.nih.gov/12463806/ (accessed on 12 December 2021).

- Kim, S.; Garrison, G. Investigating mobile wireless technology adoption: An extension of the technology acceptance model. Inf. Syst. Front. 2008, 11, 323–333. [Google Scholar] [CrossRef]

- Ketikidis, P.; Dimitrovski, T.; Lazuras, L.; Bath, P.A. Acceptance of health information technology in health professionals: An application of the revised technology acceptance model. Health Inform. J. 2012, 18, 124–134. [Google Scholar] [CrossRef] [Green Version]

- Goodhue, D.L. Understanding User Evaluations of Information Systems. Manag. Sci. 1995, 41, 1827–1844. [Google Scholar] [CrossRef]

- Vessey, I. Cognitive Fit: A Theory-Based Analysis of the Graphs Versus Tables Literature. Decis. Sci. 1991, 22, 219–240. [Google Scholar] [CrossRef]

- UNDP 2020. Available online: https://hdr.undp.org/en/2020-report (accessed on 3 December 2021).

- Hayes, A.F. Model templates for PROCESS for SPSS and SAS. Available online: http://afhayes.com/public/templates.pdf (accessed on 12 December 2021).

- Rothschild, D.; Konitzer, T. Random Device Engagement and Organic Sampling [White paper]. Pollfish. Available online: https://resources.pollfish.com/market-research/random-device-engagement-and-organic-sampling/ (accessed on 3 December 2021).

- Venkatesh, V.; Davis, F.D. A Theoretical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies. Manag. Sci. 2000, 46, 186–204. [Google Scholar] [CrossRef] [Green Version]

- Kline, R.B. Principles and Practice of Structural Equation Modeling, 2nd ed.; Guilford Press: New York, NY, USA, 2005. [Google Scholar]

- McDonald, R.P.; Ho, M. Principles and Practice in Reporting Structural Equation Analyses. Psychol. Methods 2002, 7, 64–82. [Google Scholar] [CrossRef]

- Arbuckle, J.L. Amos 18 User’s Guide; Amos Development Corporation-SPSS Inc.: Chicago, IL, USA, 2009. [Google Scholar]

- Nunnally, J.C.; Bernstein, I.H. The Assessment of Reliability. Psychom. Theory 1994, 3, 248–292. [Google Scholar]

- Fornell, C.; Larker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.-Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

| Variables | Category | Frequency | Percentage |

|---|---|---|---|

| Gender | Male | ||

| Female | |||

| Age | 18–24 | 53 | 14.5 |

| 25–34 | 182 | 49.9 | |

| 35–44 | 110 | 30.1 | |

| 45–54 | 13 | 3.6 | |

| 54 and above | 7 | 1.9 | |

| Experience total | <1 | 28 | 7.7 |

| 1–3 | 76 | 20.8 | |

| 3–5 | 93 | 25.5 | |

| 5–10 | 99 | 27.1 | |

| >10 | 69 | 18.9 | |

| Experience current Org | <1 | 31 | 8.5 |

| 1–2 | 92 | 25.2 | |

| 2–5 | 139 | 38.1 | |

| >5 | 103 | 28.2 | |

| Use of e-accounting | <1 | 76 | 20.8 |

| 1–3 | 155 | 42.5 | |

| 3–5 | 66 | 18.1 | |

| >5 | 48 | 13.2 | |

| Not used | 20 | 5.5 |

| Construct/Variable | Factor Loadings | Alpha | CR | AVE |

|---|---|---|---|---|

| Perceived Ease of Use | 0.84 | 0.84 | 0.50 | |

| PEU1 | 0.711 | |||

| PEU2 | 0.669 | |||

| PEU3 | 0.614 | |||

| PEU4 | 0.693 | |||

| PEU5 | 0.699 | |||

| PEU6 | 0.684 | |||

| Perceived Usefulness | 0.86 | 0.86 | 0.50 | |

| PU1 | 0.716 | |||

| PU2 | 0.746 | |||

| PU3 | 0.669 | |||

| PU4 | 0.761 | |||

| PU5 | 0.704 | |||

| PU6 | 0.656 | |||

| Organizational Support | 0.87 | 0.83 | 0.50 | |

| OS1 | 0.696 | |||

| OS2 | 0.739 | |||

| OS3 | 0.662 | |||

| OS4 | 0.696 | |||

| OS5 | 0.713 | |||

| Job Relevance | 0.70 | 0.70 | 0.51 | |

| JR1 | 0.679 | |||

| JR2 | 0.742 | |||

| Intentions to Use E-accounting | 0.71 | 0.71 | 0.60 | |

| IU1 | 0.702 | |||

| IU2 | 0.785 | |||

| Goodness-of-Fit Indices | ||||

| χ2 = 404; d.f. = 177; χ2/d.f. = 2.28; p < 0.001; CFI = 0.96; GFI = 0.91; AGFI = 0.88; RMR = 0.02; RMSEA = 0.06. | ||||

| Variable | No. of Items | Mean | S.d. | 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|---|---|---|---|

| 1 | PEU | 6 | 1.61 | 0.49 | 0.50 | ||||

| 2 | PU | 6 | 1.63 | 0.60 | 0.69 * (0.48) | 0.50 | |||

| 3 | OS | 5 | 1.52 | 0.56 | 0.65 * (0.42) | 0.70 * (0.49) | 0.50 | ||

| 4 | JR | 2 | 1.56 | 0.66 | 0.59 * (0.35) | 0.68 * (0.46) | 0.58 * (0.34) | 0.50 | |

| 5 | IU | 2 | 1.61 | 0.66 | 0.58 * (0.34) | 0.67 * (0.45) | 0.57 * (0.32) | 0.65 * (0.42) | 0.60 |

| Path | Estimate | SE | ||

|---|---|---|---|---|

| PEU => BI (Direct Effect) | 0.313 * | 0.07 | ||

| PEU => PU | 0.842 * | 0.05 | ||

| PU => IU | 0.554 * | 0.06 | ||

| Standardized Total, Direct, and Indirect Effects using 5000 Bootstrap 95% CI | ||||

| Path | Effect | SE | LL 95% CI | UL 95% CI |

| Total Effect | 0.779 | 0.06 | 0.668 | 0.891 |

| Direct Effect | 0.235 | 0.07 | 0.174 | 0.452 |

| Indirect Effect (PEU => PU => IU) | 0.550 | 0.05 | 0.251 | 0.448 |

| DV: IU | DV: IU | |||||||

|---|---|---|---|---|---|---|---|---|

| Estimate | SE | LL 95% CI | UL 95% CI | Estimate | SE | LL 95% CI | UL 95% CI | |

| PU | 0.590 * | 0.059 | 0.474 | 0.706 | ||||

| OS | 0.332 * | 0.068 | 0.198 | 0.467 | ||||

| PU * OS | 0.208 * | 0.052 | 0.310 | 0.106 | ||||

| PU | 0.606 * | 0.053 | 0.502 | 0.710 | ||||

| JR | 0.280 * | 0.058 | 0.167 | 0.393 | ||||

| PU * JR | 0.124 ** | 0.054 | 0.231 | 0.017 | ||||

| Model Fit | ||||||||

| F-value | 114 * | 110 * | ||||||

| R2 | 0.49 | 0.48 | ||||||

| R2 Change | 0.02 * | 0.01 ** | ||||||

| DV: IU | ||||

|---|---|---|---|---|

| Estimate | SE | LL 95% CI | UL 95% CI | |

| PEU | 0.180 ** | 0.076 | 0.029 | 0.331 |

| PU | 0.426 * | 0.072 | 0.283 | 0.569 |

| OS | 0.241 * | 0.077 | 0.091 | 0.392 |

| JR | 0.158 * | 0.062 | 0.035 | 0.280 |

| PU * OS | 0.151 * | 0.060 | 0.262 | 0.041 |

| PU * JR | 0.015 | 0.057 | −0.105 | 0.134 |

| Model Fit | ||||

| F-value | 335 * | |||

| R2 | 0.48 * | |||

| R2 Change | 0.03 * | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

AlNasrallah, W.; Saleem, F. Determinants of the Digitalization of Accounting in an Emerging Market: The Roles of Organizational Support and Job Relevance. Sustainability 2022, 14, 6483. https://doi.org/10.3390/su14116483

AlNasrallah W, Saleem F. Determinants of the Digitalization of Accounting in an Emerging Market: The Roles of Organizational Support and Job Relevance. Sustainability. 2022; 14(11):6483. https://doi.org/10.3390/su14116483

Chicago/Turabian StyleAlNasrallah, Wafa, and Farida Saleem. 2022. "Determinants of the Digitalization of Accounting in an Emerging Market: The Roles of Organizational Support and Job Relevance" Sustainability 14, no. 11: 6483. https://doi.org/10.3390/su14116483

APA StyleAlNasrallah, W., & Saleem, F. (2022). Determinants of the Digitalization of Accounting in an Emerging Market: The Roles of Organizational Support and Job Relevance. Sustainability, 14(11), 6483. https://doi.org/10.3390/su14116483